Deck 15: Alternative Minimum Tax

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Beulah,who is single,provides you with the following information from her financial records for 2017.Compute Beulah's AMTI.

A)$0

B)$174,050

C)$228,000

D)$232,050

E)None of the above

A)$0

B)$174,050

C)$228,000

D)$232,050

E)None of the above

Question

Ashby,who is single and age 30,provides you with the following information from his financial records for 2017.

Calculate his AMT exemption for 2017.

A)$0

B)$26,075

C)$28,225

D)$54,300

Calculate his AMT exemption for 2017.

A)$0

B)$26,075

C)$28,225

D)$54,300

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Ted,who is single,owns a personal residence in the city.He also owns a condo near the ocean.He uses the condo as a vacation home.In March 2017,he borrowed $50,000 on a home equity loan and used the proceeds to acquire a luxury automobile.During 2017,he paid the following amounts of interest.

What amount,if any,must Ted recognize as an AMT adjustment in 2017?

A)$0

B)$4,800

C)$6,200

D)$11,000

What amount,if any,must Ted recognize as an AMT adjustment in 2017?

A)$0

B)$4,800

C)$6,200

D)$11,000

Question

Question

Question

Question

Question

Question

Question

Question

Question

Prior to the effect of the tax credits,Justin's regular income tax liability is $200,000.and his tentative minimum tax is $195,000.Justin reports the following credits.

Calculate Justin's tax liability after credits.

A)$190,000

B)$194,000

C)$195,000

D)$200,000

Calculate Justin's tax liability after credits.

A)$190,000

B)$194,000

C)$195,000

D)$200,000

Question

Question

Question

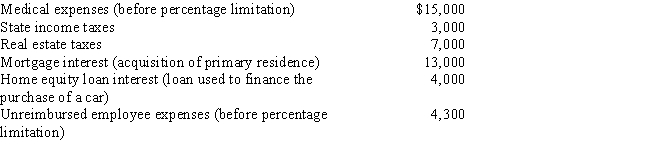

Mitch,who is single and age 46 and has no dependents,had AGI of $100,000 this year.His potential itemized deductions were as follows.

What is the amount of Mitch's AMT adjustment for itemized deductions for 2017?

A)$10,000.

B)$12,300.

C)$16,300.

D)$34,300.

What is the amount of Mitch's AMT adjustment for itemized deductions for 2017?

A)$10,000.

B)$12,300.

C)$16,300.

D)$34,300.

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/132

Play

Full screen (f)

Deck 15: Alternative Minimum Tax

1

Paul incurred circulation expenditures of $180,000 in 2017 and deducted that amount for regular income tax purposes.Paul has a $60,000 negative AMT adjustment for each of 2018,2019,and for 2020.

False

2

In deciding to enact the alternative minimum tax,Congress was concerned about the inequity that resulted when taxpayers with substantial economic incomes could avoid paying regular income tax.

True

3

Assuming no phaseout,the AMT exemption amount for a married taxpayer filing separately for 2017 is more than the AMT exemption amount for C corporations.

True

4

The net capital gain included in an individual taxpayer's AMT base is eligible for the lower tax rate on net capital gain.This favorable alternative rate applies both in calculating the regular income tax and the AMT.

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

5

Unless circulation expenditures are amortized over a three-year period for regular income tax purposes,there will be an AMT adjustment.

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

6

Business tax credits reduce the AMT and the regular income tax in the same way.

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

7

AMT adjustments can be positive or negative,whereas AMT preferences are always positive.

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

8

The phaseout of the AMT exemption amount for a taxpayer filing as a head of household both begins and ends at a higher income level than it does for a single taxpayer.

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

9

A taxpayer who expenses circulation expenditures in the year incurred for regular income tax purposes will have a positive AMT adjustment in the following year.

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

10

Keosha acquires used 10-year personal property to use in her business in 2017 and uses MACRS depreciation for regular income tax purposes.As a result,Keosha will incur a positive AMT adjustment in 2017,because AMT depreciation is slower.

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

11

If Abby's alternative minimum taxable income exceeds her regular taxable income,she will incur an alternative minimum tax.

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

12

Negative AMT adjustments for the current year caused by timing differences are offset by the positive AMT adjustments in prior tax years also caused by timing differences.

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

13

If the AMT base is greater than $187,800,the AMT rate for an individual taxpayer is the same as the AMT rate for a C corporation.

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

14

Prior to consideration of tax credits,Clarence's regular income tax liability is $200,000 and his tentative minimum tax (TMT) is $180,000.Clarence holds nonrefundable business tax credits of $35,000.His tax liability is $165,000.

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

15

Since most tax preferences are merely timing differences,they eventually will reverse and net to zero.

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

16

Madge's tentative minimum tax (TMT) is $112,000.Her regular income tax liability is $99,000.Madge's AMT is $13,000.

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

17

After personal property is fully depreciated for both regular income tax purposes and AMT purposes,the positive and negative adjustments that have been made for AMT purposes will net to zero.

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

18

Joel placed real property in service in 2017 that cost $900,000 and used MACRS depreciation for regular income tax purposes.He is required to make a positive adjustment for AMT purposes in 2017 for the excess of depreciation calculated for regular income tax purposes over the depreciation calculated for AMT purposes.

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

19

The required adjustment for AMT purposes for pollution control facilities placed in service this year is equal to the difference between the amortization deduction allowed for regular income tax purposes and the depreciation deduction computed under ADS.

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

20

The AMT calculated using the indirect method will produce a different amount than the AMT calculated using the direct method.

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

21

In the current tax year,Ben exercised an incentive stock option (ISO),acquiring stock with a fair market value of $190,000 for $170,000.As a result,his AMT basis for the stock is $170,000,his regular income tax basis for the stock is $170,000,and his AMT adjustment is $0 ($170,000 - $170,000).

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

22

The sale of business property could result in an AMT adjustment.

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

23

Income from some long-term contracts can be reported using the completed contract method for regular income tax purposes,but the percentage of completion method is required for AMT purposes for all long-term contracts.

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

24

The AMT adjustment for mining exploration and development costs can be avoided if the taxpayer elects to deduct the expenditures in the year incurred for regular income tax purposes,rather than writing off the expenditures over a 10-year period for regular income tax purposes.

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

25

Benita expensed mining exploration and development costs of $500,000 incurred in the current tax year.She will be required to make negative AMT adjustments for each of the next ten years and a positive AMT adjustment in the current tax year.

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

26

Nell records a personal casualty loss deduction of $14,500 for regular income tax purposes.The loss was computed as $26,600,but it was reduced by $100 and by $12,000 (10% × $120,000 AGI).For AMT purposes,the casualty loss deduction also is $14,500.

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

27

If a gambling loss itemized deduction is permitted for regular income tax purposes,no AMT adjustment results.

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

28

Cher sold undeveloped land that originally cost $150,000 for $225,000.There is a positive AMT adjustment of $75,000 associated with the sale of the land.

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

29

Because passive losses are not deductible in computing either taxable income or AMTI,no AMT adjustment for passive losses is required.

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

30

Kerri,who has AGI of $120,000,itemized her deductions in the current year.She incurred unreimbursed employee business expenses of $8,500.Kerri incurs a positive AMT adjustment of $2,400 in computing AMT.

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

31

If the regular income tax deduction for medical expenses is $0,under certain circumstances the AMT deduction for medical expenses can be greater than $0.

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

32

Interest on a home equity loan cannot be deducted for AMT purposes.

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

33

The AMT adjustment for research and experimental expenditures can be avoided if the taxpayer capitalizes the expenditures and amortizes them over a 10-year period for regular tax purposes.

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

34

Elmer exercises an incentive stock option (ISO) in March for $6,000 (fair market value of the stock on the exercise date is $7,600).If Elmer sells the stock in November of the same tax year for $8,000,he reports a $1,600 AMT adjustment for the year.

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

35

In 2017,the amount of the deduction for medical expenses for regular tax purposes may be different than for AMT purposes if the taxpayer is at least age 65.

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

36

Evan is a contractor who constructs both commercial and residential buildings.Even though some of the contracts could qualify for the use of the completed contract method,Evan decides to use the percentage of the completion method for all of his contracts.This increases Evan's AMT adjustment associated with long-term contracts for the current year.

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

37

The deduction for charitable contributions in calculating the regular income tax can differ from that in calculating the AMT,because the percentage limitations (20%,30%,and 50%) may be applied to a different base amount.

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

38

The deduction for personal and dependency exemptions is allowed for regular income tax purposes,but is disallowed for AMT purposes.This results in a positive AMT adjustment.

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

39

The recognized gain for regular income tax purposes and the recognized gain for AMT purposes on the sale of stock acquired with an incentive stock option (ISO) are always the same,because the adjusted basis is the same.

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

40

AGI is used as the base for application of percentage limitations (i.e.,20%,30%,50%) that apply to the charitable contribution deduction for regular income tax purposes.Modified AGI is used as the base for application of percentage limitations that apply to the charitable contribution deduction for AMT purposes.

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

41

Which of the following statements is correct?

A)If the tentative minimum tax exceeds the regular income tax liability,AMT is $0.

B)The AMT exemption amount decreases as AMTI increases.

C)The highest AMT tax rate for individuals is 26%.

D)Only a.and c.are correct.

E)a.,b.,and c.are correct.

A)If the tentative minimum tax exceeds the regular income tax liability,AMT is $0.

B)The AMT exemption amount decreases as AMTI increases.

C)The highest AMT tax rate for individuals is 26%.

D)Only a.and c.are correct.

E)a.,b.,and c.are correct.

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

42

For individual taxpayers,the AMT credit is applicable for the AMT that results from timing differences,but it is not available for the AMT that results from the adjustment for itemized deductions or exclusion preferences.

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

43

Which of the following statements is incorrect?

A)AMTI calculated under the direct and indirect methods produces the same amount.

B)AMTI calculated under the direct and the indirect methods produces different amounts.

C)The tax forms use the direct method to calculate the AMT.

D)Only b.and c.are incorrect.

E)a.,b.,and c.are incorrect.

A)AMTI calculated under the direct and indirect methods produces the same amount.

B)AMTI calculated under the direct and the indirect methods produces different amounts.

C)The tax forms use the direct method to calculate the AMT.

D)Only b.and c.are incorrect.

E)a.,b.,and c.are incorrect.

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

44

Kay claimed percentage depletion of $119,000 for the current year for regular income tax purposes.Cost depletion would have been $60,000.Her basis in the property was $90,000 at the beginning of the current year.Kay must treat the percentage depletion deducted in excess of cost depletion,or $59,000,as a preference in computing AMTI.

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

45

A,B and C are each single,report wage income of $135,000,and take the standard deduction.The following additional information is provided about each taxpayer.

A: Resides in New York.$45,000 interest income from Treasury bonds.

B: Resides in Nevada.$45,000 capital gain from the sale of stock.

C: Resides in Florida.$45,000 interest income from private-activity municipal bonds.

All else being equal and taking into consideration the principles underlying the AMT,which of these taxpayers has the highest likelihood of being subject to the AMT in the current tax year?

A)Taxpayer A.

B)Taxpayer B.

C)Taxpayer C.

D)Taxpayer D.

A: Resides in New York.$45,000 interest income from Treasury bonds.

B: Resides in Nevada.$45,000 capital gain from the sale of stock.

C: Resides in Florida.$45,000 interest income from private-activity municipal bonds.

All else being equal and taking into consideration the principles underlying the AMT,which of these taxpayers has the highest likelihood of being subject to the AMT in the current tax year?

A)Taxpayer A.

B)Taxpayer B.

C)Taxpayer C.

D)Taxpayer D.

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

46

C corporations are not required to make AMT adjustments for depreciation.

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

47

Beulah,who is single,provides you with the following information from her financial records for 2017.Compute Beulah's AMTI.

A)$0

B)$174,050

C)$228,000

D)$232,050

E)None of the above

A)$0

B)$174,050

C)$228,000

D)$232,050

E)None of the above

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

48

Ashby,who is single and age 30,provides you with the following information from his financial records for 2017.

Calculate his AMT exemption for 2017.

A)$0

B)$26,075

C)$28,225

D)$54,300

Calculate his AMT exemption for 2017.

A)$0

B)$26,075

C)$28,225

D)$54,300

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

49

All of a C corporation's AMT is available for carryover as a minimum tax credit,regardless of whether the adjustments and preferences originate from timing differences or AMT preferences.

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

50

The AMT exemption for a C corporation is $50,000,reduced by 50% of the amount by which AMTI exceeds $150,000.

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

51

Jackson sells qualifying small business stock for $125,000 (adjusted basis of $105,000) in 2017 (the stock was acquired in 2011).In calculating gross income for regular income tax purposes,he excludes all of his realized gain of $20,000.The $20,000 exclusion is a preference in calculating Jackson's AMTI.

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

52

Which of the following statements describing the alternative minimum tax (AMT) is most correct?

A)Generally,those taxpayers most concerned about being in AMT are low income taxpayers who elect the standard deduction.

B)The AMT was enacted in an attempt to limit the ability of taxpayers to engage in questionable tax planning activities.

The goal of the AMT

C)The goal of the AMT is to try and ensure that all taxpayers with economic income pay at least some income tax.

D)Exemption amounts are higher for regular tax purposes than for AMT purposes.

E)a.and d.are correct

A)Generally,those taxpayers most concerned about being in AMT are low income taxpayers who elect the standard deduction.

B)The AMT was enacted in an attempt to limit the ability of taxpayers to engage in questionable tax planning activities.

The goal of the AMT

C)The goal of the AMT is to try and ensure that all taxpayers with economic income pay at least some income tax.

D)Exemption amounts are higher for regular tax purposes than for AMT purposes.

E)a.and d.are correct

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

53

Vicki owns and operates a news agency (as a sole proprietorship).During 2017,she incurred expenses of $24,000 to increase circulation of newspapers and magazines that her agency distributes.For regular income tax purposes,she elected to expense the $24,000 in 2017.In addition,Vicki incurred $15,000 in circulation expenditures in 2018 and again elected expense treatment.What AMT adjustments will be required in 2017 and 2018 as a result of the circulation expenditures?

A)$16,000 positive in 2017, $2,000 positive in 2018.

B)$16,000 negative in 2017, $2,000 positive in 2018.

C)$16,000 negative in 2017, $10,000 positive in 2018.

D)$16,000 positive in 2017, $10,000 positive in 2018.

E)None of the above.

A)$16,000 positive in 2017, $2,000 positive in 2018.

B)$16,000 negative in 2017, $2,000 positive in 2018.

C)$16,000 negative in 2017, $10,000 positive in 2018.

D)$16,000 positive in 2017, $10,000 positive in 2018.

E)None of the above.

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

54

Dale owns and operates Dale's Emporium as a sole proprietorship.On January 30,2003,Dale's Emporium acquired a warehouse for $100,000.For regular income tax purposes in 2017,depreciation was deducted under MACRS using a 2.564% rate.Determine the AMT adjustment for depreciation and indicate whether it is positive or negative.

A)$64 negative adjustment.

B)$64 positive adjustment.

C)No adjustment is required because Dale's Emporium used the Alternative Depreciation System (ADS) to compute depreciation on the property for AMT purposes.

D)No adjustment is required because Dale's Emporium used MACRS to compute the depreciation of the property for regular income tax purposes.

A)$64 negative adjustment.

B)$64 positive adjustment.

C)No adjustment is required because Dale's Emporium used the Alternative Depreciation System (ADS) to compute depreciation on the property for AMT purposes.

D)No adjustment is required because Dale's Emporium used MACRS to compute the depreciation of the property for regular income tax purposes.

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

55

The corporate AMT does not apply to "small" C corporations.

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

56

Which of the following statements is correct?

A)If the tentative minimum tax is $10,000 and the regular income tax liability is $12,000, AMT is $2,000.

B)If the tentative minimum tax is $12,000 and the regular income tax liability is $10,000, AMT is $12,000.

C)If the tentative minimum tax is $10,000 and the regular income tax liability is $12,000, AMT is a negative $2,000.

D)If the tentative minimum tax is $12,000, and the regular income tax liability is $10,000, AMT is $2,000.

A)If the tentative minimum tax is $10,000 and the regular income tax liability is $12,000, AMT is $2,000.

B)If the tentative minimum tax is $12,000 and the regular income tax liability is $10,000, AMT is $12,000.

C)If the tentative minimum tax is $10,000 and the regular income tax liability is $12,000, AMT is a negative $2,000.

D)If the tentative minimum tax is $12,000, and the regular income tax liability is $10,000, AMT is $2,000.

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

57

Certain adjustments apply in calculating the corporate AMT that do not apply in calculating the noncorporate AMT and certain adjustments apply in calculating the noncorporate AMT that do not apply in calculating the corporate AMT.

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

58

Interest income on private activity bonds issued before 2009 and after 2010,reduced by expenses incurred in carrying the bonds,is a preference item that is included in computing AMTI.

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

59

The AMT exemption for a corporation with $225,000 of AMTI is $18,750.

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

60

If the taxpayer elects to capitalize and to amortize intangible drilling costs over a 3-year period for regular income tax purposes,there is no adjustment or preference for AMT purposes.

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

61

Factors that can cause the adjusted basis for AMT purposes to be different from the adjusted basis for regular income tax purposes include:

A)A different amount of depreciation has been deducted for AMT purposes and regular income tax purposes.

B)The spread on the exercise of an incentive stock option (ISO) is recognized for AMT purposes,but is not recognized for regular income tax purposes.

C)A different amount has been deducted for circulation expenditures for AMT purposes and for regular income tax purposes.

D)Only a.and b.

E)a.,b.,and c.

A)A different amount of depreciation has been deducted for AMT purposes and regular income tax purposes.

B)The spread on the exercise of an incentive stock option (ISO) is recognized for AMT purposes,but is not recognized for regular income tax purposes.

C)A different amount has been deducted for circulation expenditures for AMT purposes and for regular income tax purposes.

D)Only a.and b.

E)a.,b.,and c.

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

62

Which of the following amounts generally produce positive AMT adjustments?

A)Real property taxes deduction.

B)Personal exemption deduction.

C)Charitable contribution deduction.

D)Only a.and b.are correct.

E)a.,b.,and c.are correct.

A)Real property taxes deduction.

B)Personal exemption deduction.

C)Charitable contribution deduction.

D)Only a.and b.are correct.

E)a.,b.,and c.are correct.

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

63

Wallace owns a construction company that builds both commercial and residential buildings.He contracts to build a residential building for $800,000,and for which he is eligible to use the completed contract method of accounting.In the current year for regular income tax purposes,Wallace does not recognize any gross income on the contract.Under the percentage of completion method,the income recognized under the contract would have been $60,000.Wallace's AMT effect is:

A)$0.

B)$60,000 negative adjustment.

C)$60,000 positive adjustment.

D)$800,000 positive adjustment.

A)$0.

B)$60,000 negative adjustment.

C)$60,000 positive adjustment.

D)$800,000 positive adjustment.

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

64

Which of the following statements concerning capital gains and losses and the AMT is correct?

A)The lower tax rate on net capital gain is not allowed in the calculation of tentative minimum tax.

B)Net capital losses disallowed for regular tax purposes are deductible in the calculation of AMTI

C)The lower tax rate on net capital gain applies in calculating both regular income tax and the tentative minimum tax.

D)Net capital gain is taxed at the maximum 28% AMT rate

A)The lower tax rate on net capital gain is not allowed in the calculation of tentative minimum tax.

B)Net capital losses disallowed for regular tax purposes are deductible in the calculation of AMTI

C)The lower tax rate on net capital gain applies in calculating both regular income tax and the tentative minimum tax.

D)Net capital gain is taxed at the maximum 28% AMT rate

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

65

In 2017,Glenn recorded a $108,000 loss on a passive activity.None of the loss is attributable to AMT adjustments or preferences.She has no other passive activities.Which of the following statements is correct?

A)In 2017, Glenn can deduct $108,000 for regular income tax purposes and for AMT purposes.

B)Glenn reports a $108,000 tax preference in 2017 as a result of the passive activity.

C)For regular income tax purposes, none of the passive activity loss is allowed in 2017.

D)In 2017, Glenn reports a positive adjustment of $25,000 as a result of the passive activity loss.

A)In 2017, Glenn can deduct $108,000 for regular income tax purposes and for AMT purposes.

B)Glenn reports a $108,000 tax preference in 2017 as a result of the passive activity.

C)For regular income tax purposes, none of the passive activity loss is allowed in 2017.

D)In 2017, Glenn reports a positive adjustment of $25,000 as a result of the passive activity loss.

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

66

Eula owns a mineral property that had a basis of $23,000 at the beginning of the year.Cost depletion is $19,000.The property qualifies for a 15% depletion rate.Gross income from the property was $200,000,and net income before the percentage depletion deduction was $50,000.What is Eula's AMT preference for excess depletion,if she maximized her regular-tax depletion deduction?

A)$15,000

B)$23,000

C)$25,000

D)$2,000

A)$15,000

B)$23,000

C)$25,000

D)$2,000

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

67

Which of the following statements is correct?

A)The deduction for personal and dependency exemptions is not permitted in calculating the AMT.Therefore,in converting regular taxable income to AMTI,a positive adjustment is required.

B)To the extent that itemized deductions exceed the standard deduction for regular income tax purposes,a positive AMT adjustment is required in converting regular taxable income to AMTI.

C)The charitable contribution deduction for AMT purposes and for regular income tax purposes can be different.In this situation,a positive AMT adjustment is required for the amount of the difference.

D)Only a.and b.are correct.

E)a.,b.,and c.are correct.

A)The deduction for personal and dependency exemptions is not permitted in calculating the AMT.Therefore,in converting regular taxable income to AMTI,a positive adjustment is required.

B)To the extent that itemized deductions exceed the standard deduction for regular income tax purposes,a positive AMT adjustment is required in converting regular taxable income to AMTI.

C)The charitable contribution deduction for AMT purposes and for regular income tax purposes can be different.In this situation,a positive AMT adjustment is required for the amount of the difference.

D)Only a.and b.are correct.

E)a.,b.,and c.are correct.

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

68

Ted,who is single,owns a personal residence in the city.He also owns a condo near the ocean.He uses the condo as a vacation home.In March 2017,he borrowed $50,000 on a home equity loan and used the proceeds to acquire a luxury automobile.During 2017,he paid the following amounts of interest.

What amount,if any,must Ted recognize as an AMT adjustment in 2017?

A)$0

B)$4,800

C)$6,200

D)$11,000

What amount,if any,must Ted recognize as an AMT adjustment in 2017?

A)$0

B)$4,800

C)$6,200

D)$11,000

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

69

Which of the following can produce an AMT preference rather than an AMT adjustment?

A)Interest on private activity bonds issued in 2015.

B)Percentage depletion.

C)Incentive stock options (ISOs).

D)Only a.and b.

E)a.,b.,and c.

A)Interest on private activity bonds issued in 2015.

B)Percentage depletion.

C)Incentive stock options (ISOs).

D)Only a.and b.

E)a.,b.,and c.

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

70

In 2017,Zachary incurs no AMT adjustments,and his only AMT preference (which is also his only itemized deduction) is $42,000 of state and local and real property taxes.

If Zachary were a single taxpayer who itemized deductions and had taxable income of $95,000,his regular tax liability would be $19,582 and his AMT liability would be $22,555.

Assume instead that Zachary is a married taxpayer filing jointly in 2017.The couple's taxable income amount is changed only by the additional personal exemption.In comparison to the tax liability amounts presented above,the couple's regular and AMT tax liabilities would be:

A)Higher, Higher

B)Higher, Lower

C)Lower, Higher

D)Lower, Lower

If Zachary were a single taxpayer who itemized deductions and had taxable income of $95,000,his regular tax liability would be $19,582 and his AMT liability would be $22,555.

Assume instead that Zachary is a married taxpayer filing jointly in 2017.The couple's taxable income amount is changed only by the additional personal exemption.In comparison to the tax liability amounts presented above,the couple's regular and AMT tax liabilities would be:

A)Higher, Higher

B)Higher, Lower

C)Lower, Higher

D)Lower, Lower

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

71

Akeem,who does not itemize,incurred a net operating loss (NOL) of $50,000 in 2016.His deductions in 2016 included AMT tax preference items of $20,000,and he had no AMT adjustments.Assuming the NOL is not carried back,what is Akeem's ATNOLD carryover to 2017?

A)$50,000

B)$30,000

C)$20,000

D)$40,000

E)None of the above

A)$50,000

B)$30,000

C)$20,000

D)$40,000

E)None of the above

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

72

Marvin,the vice president of Lavender,Inc.,exercises stock options for 100 shares of stock in March 2017.The stock options are incentive stock options (ISOs).Their exercise price is $20 and the fair market value on the date of exercise is $28.The options were granted in March 2013 and all restrictions on the free transferability had lapsed by the exercise date.

A)If Marvin sells the stock in December 2017 for $3,000, his AMT adjustment in 2017 is a positive adjustment of $800.

B)If Marvin sells the stock in December 2018 for $3,000, his AMT adjustment in 2018 is $0.

C)If Marvin sells the stock in December 2017 for $3,000, his AMT adjustment in 2017 is a negative adjustment of $800.

D)If Marvin sells the stock in December 2018 for $3,000, his AMT adjustment in 2018 is a negative adjustment of $1,000.

E)None of the above.

A)If Marvin sells the stock in December 2017 for $3,000, his AMT adjustment in 2017 is a positive adjustment of $800.

B)If Marvin sells the stock in December 2018 for $3,000, his AMT adjustment in 2018 is $0.

C)If Marvin sells the stock in December 2017 for $3,000, his AMT adjustment in 2017 is a negative adjustment of $800.

D)If Marvin sells the stock in December 2018 for $3,000, his AMT adjustment in 2018 is a negative adjustment of $1,000.

E)None of the above.

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

73

Vinny's AGI is $250,000.He contributed $200,000 in cash to the Boy Scouts,a public charity.What is Vinny's charitable contribution deduction for AMT purposes?

A)$0

B)$50,000

C)$75,000

D)$125,000

A)$0

B)$50,000

C)$75,000

D)$125,000

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

74

In 2017,Blake incurs $270,000 of mining exploration expenditures,and deducts the entire amount for regular income tax purposes.Which of the following statements is correct?

A)For AMT purposes,Blake will have a positive adjustment of $243,000 in 2017.

B)Blake will have a negative AMT adjustment of $27,000 in 2021.

C)Over a 10-year period,positive and negative adjustments for mining exploration expenditures will net to zero.

D)Only a.and c.are correct.

E)a.,b.,and c.are correct.

A)For AMT purposes,Blake will have a positive adjustment of $243,000 in 2017.

B)Blake will have a negative AMT adjustment of $27,000 in 2021.

C)Over a 10-year period,positive and negative adjustments for mining exploration expenditures will net to zero.

D)Only a.and c.are correct.

E)a.,b.,and c.are correct.

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

75

For regular income tax purposes,Yolanda,who is single,is in the 35% tax bracket.Her AMT base is $220,000.Her tentative AMT is:

A)$57,200.

B)$57,844.

C)$61,600.

D)$77,650.

E)None of the above.

A)$57,200.

B)$57,844.

C)$61,600.

D)$77,650.

E)None of the above.

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

76

Celia and Christian,who are married filing jointly,have one dependent and do not itemize deductions.They report taxable income of $192,000 and tax preferences of $53,000 in 2017.What is their AMT base for 2017?

A)$0.

B)$212,587.

C)$215,550.

D)$269,850.

A)$0.

B)$212,587.

C)$215,550.

D)$269,850.

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

77

Prior to the effect of the tax credits,Justin's regular income tax liability is $200,000.and his tentative minimum tax is $195,000.Justin reports the following credits.

Calculate Justin's tax liability after credits.

A)$190,000

B)$194,000

C)$195,000

D)$200,000

Calculate Justin's tax liability after credits.

A)$190,000

B)$194,000

C)$195,000

D)$200,000

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

78

Prior to the effect of tax credits,Eunice's regular income tax liability is $325,000 and her tentative minimum tax is $312,000.Eunice has general business credits available of $20,000.Calculate Eunice's tax liability after tax credits.

A)$0

B)$305,000

C)$312,000

D)$325,000

A)$0

B)$305,000

C)$312,000

D)$325,000

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

79

Which of the following itemized deductions are allowed in full for AMT purposes?

A)Real property taxes.

B)Casualty losses.

C)Charitable contributions.

D)Only b.and c.

E)a.,b.,and c.

A)Real property taxes.

B)Casualty losses.

C)Charitable contributions.

D)Only b.and c.

E)a.,b.,and c.

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

80

Mitch,who is single and age 46 and has no dependents,had AGI of $100,000 this year.His potential itemized deductions were as follows.

What is the amount of Mitch's AMT adjustment for itemized deductions for 2017?

A)$10,000.

B)$12,300.

C)$16,300.

D)$34,300.

What is the amount of Mitch's AMT adjustment for itemized deductions for 2017?

A)$10,000.

B)$12,300.

C)$16,300.

D)$34,300.

Unlock Deck

Unlock for access to all 132 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 132 flashcards in this deck.