Deck 17: Capital Structure: Limits to the Use of Debt

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

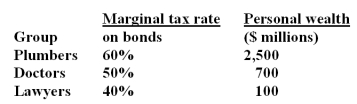

Consider an economy in which there are three groups of investors and no others.

There are no personal taxes on income from stocks.An investment is available that pays a tax-free 4%.The corporate tax rate is 50%.Total corporate income before earnings and taxes (EBIT) is $224 million forever.What is the maximum debt-to-equity ratio for the economy as a whole?

There are no personal taxes on income from stocks.An investment is available that pays a tax-free 4%.The corporate tax rate is 50%.Total corporate income before earnings and taxes (EBIT) is $224 million forever.What is the maximum debt-to-equity ratio for the economy as a whole?

There are no personal taxes on income from stocks.An investment is available that pays a tax-free 4%.The corporate tax rate is 50%.Total corporate income before earnings and taxes (EBIT) is $224 million forever.What is the maximum debt-to-equity ratio for the economy as a whole? Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/69

Play

Full screen (f)

Deck 17: Capital Structure: Limits to the Use of Debt

1

In a world with taxes and financial distress, when a firm is operating with the optimal capital structure:

I.the debt-equity ratio will also be optimal.

II.the weighted average cost of capital will be at its minimal point.

III.the required return on assets will be at its maximum point.

IV.the increased benefit from additional debt is equal to the increased bankruptcy costs of that debt.

A)I and IV only

B)II and III only

C)I and II only

D)II, III, and IV only

E)I, II, and IV only

I.the debt-equity ratio will also be optimal.

II.the weighted average cost of capital will be at its minimal point.

III.the required return on assets will be at its maximum point.

IV.the increased benefit from additional debt is equal to the increased bankruptcy costs of that debt.

A)I and IV only

B)II and III only

C)I and II only

D)II, III, and IV only

E)I, II, and IV only

I, II, and IV only

2

Although the use of debt provides tax benefits to the firm, debt also puts pressure on the firm to:

A)meet interest and principal payments which, if not met, can put the company into financial distress.

B)make dividend payments which if not met can put the company into financial distress.

C)meet both interest and dividend payments which when met increase the firm cash flow.

D)meet increased tax payments thereby increasing firm value.

E)None of the above.

A)meet interest and principal payments which, if not met, can put the company into financial distress.

B)make dividend payments which if not met can put the company into financial distress.

C)meet both interest and dividend payments which when met increase the firm cash flow.

D)meet increased tax payments thereby increasing firm value.

E)None of the above.

meet interest and principal payments which, if not met, can put the company into financial distress.

3

The MM theory with taxes implies that firms should issue maximum debt.In practice, this is not true because:

A)debt is more risky than equity.

B)bankruptcy is a disadvantage to debt.

C)firms will incur large agency costs of short term debt by issuing long term debt.

D)Both A and B.

E)Both B and C.

A)debt is more risky than equity.

B)bankruptcy is a disadvantage to debt.

C)firms will incur large agency costs of short term debt by issuing long term debt.

D)Both A and B.

E)Both B and C.

bankruptcy is a disadvantage to debt.

4

Given realistic estimates of the probability and cost of bankruptcy, the future costs of a possible bankruptcy are borne by:

A)all investors in the firm.

B)debtholders only because if default occurs interest and principal payments are not made.

C)shareholders because debtholders will pay less for the debt providing less cash for the shareholders.

D)management because if the firm defaults they will lose their jobs.

E)None of the above.

A)all investors in the firm.

B)debtholders only because if default occurs interest and principal payments are not made.

C)shareholders because debtholders will pay less for the debt providing less cash for the shareholders.

D)management because if the firm defaults they will lose their jobs.

E)None of the above.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

5

The value of a firm is maximized when the:

A)cost of equity is maximized.

B)tax rate is zero.

C)levered cost of capital is maximized.

D)weighted average cost of capital is minimized.

E)debt-equity ratio is minimized.

A)cost of equity is maximized.

B)tax rate is zero.

C)levered cost of capital is maximized.

D)weighted average cost of capital is minimized.

E)debt-equity ratio is minimized.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

6

One of the indirect costs of bankruptcy is the incentive for managers to take large risks.When following this strategy:

A)the firm will rank all projects and take the project which results in the highest expected value of the firm.

B)bondholders expropriate value from stockholders by selecting high risk projects.

C)stockholders expropriate value from bondholders by selecting high risk projects.

D)the firm will always take the low risk project.

E)Both A and B.

A)the firm will rank all projects and take the project which results in the highest expected value of the firm.

B)bondholders expropriate value from stockholders by selecting high risk projects.

C)stockholders expropriate value from bondholders by selecting high risk projects.

D)the firm will always take the low risk project.

E)Both A and B.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

7

The optimal capital structure:

A)will be the same for all firms in the same industry.

B)will remain constant over time unless the firm makes an acquisition.

C)of a firm will vary over time as taxes and market conditions change.

D)places more emphasis on the operations of a firm rather than the financing of a firm.

E)is unaffected by changes in the financial markets.

A)will be the same for all firms in the same industry.

B)will remain constant over time unless the firm makes an acquisition.

C)of a firm will vary over time as taxes and market conditions change.

D)places more emphasis on the operations of a firm rather than the financing of a firm.

E)is unaffected by changes in the financial markets.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

8

Conflicts of interest between stockholders and bondholders are known as:

A)trustee costs.

B)financial distress costs.

C)dealer costs.

D)agency costs.

E)underwriting costs.

A)trustee costs.

B)financial distress costs.

C)dealer costs.

D)agency costs.

E)underwriting costs.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

9

Corporations in the U.S.tend to:

A)minimize taxes.

B)underutilize debt.

C)rely less on equity financing than they should.

D)have extremely high debt-equity ratios.

E)rely more heavily on bonds than stocks as the major source of financing.

A)minimize taxes.

B)underutilize debt.

C)rely less on equity financing than they should.

D)have extremely high debt-equity ratios.

E)rely more heavily on bonds than stocks as the major source of financing.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

10

In general, the capital structures used by U.S.firms:

A)tend to overweigh debt in relation to equity.

B)are easily explained in terms of earnings volatility.

C)are easily explained by analyzing the types of assets owned by the various firms.

D)tend to be those which maximize the use of the firm's available tax shelters.

E)vary significantly across industries.

A)tend to overweigh debt in relation to equity.

B)are easily explained in terms of earnings volatility.

C)are easily explained by analyzing the types of assets owned by the various firms.

D)tend to be those which maximize the use of the firm's available tax shelters.

E)vary significantly across industries.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

11

The explicit and implicit costs associated with corporate default are referred to as the _____ costs of a firm.

A)flotation

B)default beta

C)direct bankruptcy

D)indirect bankruptcy

E)financial distress

A)flotation

B)default beta

C)direct bankruptcy

D)indirect bankruptcy

E)financial distress

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

12

The optimal capital structure has been achieved when the:

A)debt-equity ratio is equal to 1.

B)weight of equity is equal to the weight of debt.

C)cost of equity is maximized given a pre-tax cost of debt.

D)debt-equity ratio is such that the cost of debt exceeds the cost of equity.

E)debt-equity ratio selected results in the lowest possible weighed average cost of capital.

A)debt-equity ratio is equal to 1.

B)weight of equity is equal to the weight of debt.

C)cost of equity is maximized given a pre-tax cost of debt.

D)debt-equity ratio is such that the cost of debt exceeds the cost of equity.

E)debt-equity ratio selected results in the lowest possible weighed average cost of capital.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

13

The optimal capital structure of a firm _____ the marketed claims and _____ the nonmarketed claims against the cash flows of the firm.

A)minimizes; minimizes

B)minimizes; maximizes

C)maximizes; minimizes

D)maximizes; maximizes

E)equates; (leave blank)

A)minimizes; minimizes

B)minimizes; maximizes

C)maximizes; minimizes

D)maximizes; maximizes

E)equates; (leave blank)

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

14

The legal proceeding for liquidating or reorganizing a firm operating in default is called a:

A)tender offer.

B)bankruptcy.

C)merger.

D)takeover.

E)proxy fight.

A)tender offer.

B)bankruptcy.

C)merger.

D)takeover.

E)proxy fight.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

15

The costs of avoiding a bankruptcy filing by a financially distressed firm are classified as _____ costs.

A)flotation

B)direct bankruptcy

C)indirect bankruptcy

D)financial solvency

E)capital structure

A)flotation

B)direct bankruptcy

C)indirect bankruptcy

D)financial solvency

E)capital structure

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

16

One of the indirect costs to bankruptcy is the incentive toward underinvestment.Following this strategy may result in:

A)the firm always choosing projects with the positive NPVs.

B)the firm turning down positive NPV projects that it would clearly accept in an all equity firm.

C)stockholders contributing the full amount of the investment, but both stockholders and bondholders sharing in the benefits of the project.

D)Both A and C.

E)Both B and C.

A)the firm always choosing projects with the positive NPVs.

B)the firm turning down positive NPV projects that it would clearly accept in an all equity firm.

C)stockholders contributing the full amount of the investment, but both stockholders and bondholders sharing in the benefits of the project.

D)Both A and C.

E)Both B and C.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

17

Indirect costs of financial distress:

A)effectively limit the amount of equity a firm issues.

B)serve as an incentive to increase the financial leverage of a firm.

C)include direct costs such as legal and accounting fees.

D)tend to increase as the debt-equity ratio decreases.

E)include the costs incurred by a firm as it tries to avoid seeking bankruptcy protection.

A)effectively limit the amount of equity a firm issues.

B)serve as an incentive to increase the financial leverage of a firm.

C)include direct costs such as legal and accounting fees.

D)tend to increase as the debt-equity ratio decreases.

E)include the costs incurred by a firm as it tries to avoid seeking bankruptcy protection.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

18

The optimal capital structure will tend to include more debt for firms with:

A)the highest depreciation deductions.

B)the lowest marginal tax rate.

C)substantial tax shields from other sources.

D)lower probability of financial distress.

E)less taxable income.

A)the highest depreciation deductions.

B)the lowest marginal tax rate.

C)substantial tax shields from other sources.

D)lower probability of financial distress.

E)less taxable income.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

19

The explicit costs, such as the legal expenses, associated with corporate default are classified as _____ costs.

A)flotation

B)beta conversion

C)direct bankruptcy

D)indirect bankruptcy

E)unlevered

A)flotation

B)beta conversion

C)direct bankruptcy

D)indirect bankruptcy

E)unlevered

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

20

The basic lesson of MM theory is that the value of a firm is dependent upon the:

A)capital structure of the firm.

B)total cash flows of the firm.

C)percentage of a firm to which the bondholders have a claim.

D)tax claim placed on the firm by the government.

E)size of the stockholders claims on the firm.

A)capital structure of the firm.

B)total cash flows of the firm.

C)percentage of a firm to which the bondholders have a claim.

D)tax claim placed on the firm by the government.

E)size of the stockholders claims on the firm.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

21

Growth opportunities _______ the _____ of debt financing.

A)increase; advantage

B)decrease; advantage

C)decrease; disadvantage

D)Both A and C

E)None of the above

A)increase; advantage

B)decrease; advantage

C)decrease; disadvantage

D)Both A and C

E)None of the above

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

22

The introduction of personal taxes may reveal a disadvantage to the use of debt if the:

A)personal tax rate on the distribution of income to stockholders is less than the personal tax rate on interest income.

B)personal tax rate on the distribution of income to stockholders is greater than the personal tax rate on interest income.

C)personal tax rate on the distribution of income to stockholders is equal to the personal tax rate on interest income.

D)personal tax rate on interest income is zero.

E)None of the above.

A)personal tax rate on the distribution of income to stockholders is less than the personal tax rate on interest income.

B)personal tax rate on the distribution of income to stockholders is greater than the personal tax rate on interest income.

C)personal tax rate on the distribution of income to stockholders is equal to the personal tax rate on interest income.

D)personal tax rate on interest income is zero.

E)None of the above.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

23

Which of the following industries would tend to have the highest leverage?

A)Drugs

B)Computer

C)Paper

D)Electronics

E)Biological products

A)Drugs

B)Computer

C)Paper

D)Electronics

E)Biological products

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

24

Covenants restricting the use of leasing and additional borrowings primarily protect:

A)the equityholders from added risk of default.

B)the debtholders from the added risk of dilution of their claims.

C)the debtholders from the transfer of assets.

D)the management from having to pay agency costs.

E)None of the above.

A)the equityholders from added risk of default.

B)the debtholders from the added risk of dilution of their claims.

C)the debtholders from the transfer of assets.

D)the management from having to pay agency costs.

E)None of the above.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

25

Which of the following is not empirically true when formulating capital structure policy?

A)Some firms use no debt.

B)Most corporations have low debt-asset ratios.

C)There are no differences in the capital-structure of different industries.

D)Debt levels across industries vary widely.

E)Debt ratios in most countries are considerably less than 100%.

A)Some firms use no debt.

B)Most corporations have low debt-asset ratios.

C)There are no differences in the capital-structure of different industries.

D)Debt levels across industries vary widely.

E)Debt ratios in most countries are considerably less than 100%.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

26

The free cash flow hypothesis states:

A)that firms with greater free cash flow will pay more in dividends reducing the risk of financial distress.

B)that firms with greater free cash flow should issue new equity to force managers to minimize wasting resources and to work harder.

C)that issuing debt requires interest and principal payments reducing the potential of management to waste resources.

D)Both A and C.

E)Both B and C.

A)that firms with greater free cash flow will pay more in dividends reducing the risk of financial distress.

B)that firms with greater free cash flow should issue new equity to force managers to minimize wasting resources and to work harder.

C)that issuing debt requires interest and principal payments reducing the potential of management to waste resources.

D)Both A and C.

E)Both B and C.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

27

The pecking order states how financing should be raised.In order to avoid asymmetric information problems and misinterpretation of whether management is sending a signal on security overvaluation, the firm's first rule is to:

A)finance with internally generated funds.

B)always issue debt then the market won't know when management thinks the security is overvalued.

C)issue new equity first.

D)issue debt first.

E)None of the above.

A)finance with internally generated funds.

B)always issue debt then the market won't know when management thinks the security is overvalued.

C)issue new equity first.

D)issue debt first.

E)None of the above.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

28

When graphing firm value against debt levels, the debt level that maximizes the value of the firm is the level where:

A)the increase in the present value of distress costs from an additional dollar of debt is greater than the increase in the present value of the debt tax shield.

B)the increase in the present value of distress costs from an additional dollar of debt is equal to the increase in the present value of the debt tax shield.

C)the increase in the present value of distress costs from an additional dollar of debt is less than the increase of the present value of the debt tax shield.

D)distress costs as well as debt tax shields are zero.

E)distress costs as well as debt tax shields are maximized.

A)the increase in the present value of distress costs from an additional dollar of debt is greater than the increase in the present value of the debt tax shield.

B)the increase in the present value of distress costs from an additional dollar of debt is equal to the increase in the present value of the debt tax shield.

C)the increase in the present value of distress costs from an additional dollar of debt is less than the increase of the present value of the debt tax shield.

D)distress costs as well as debt tax shields are zero.

E)distress costs as well as debt tax shields are maximized.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

29

When shareholders pursue selfish strategies such as taking large risks or paying excessive dividends, these will result in:

A)no action by debtholders since these are equity holder concerns.

B)positive agency costs, as bondholders impose various restrictions and covenants which will diminish firm value.

C)investments of the same risk class that the firm is in.

D)undertaking scale enhancing projects.

E)lower agency costs, as shareholders have more control over the firm's assets.

A)no action by debtholders since these are equity holder concerns.

B)positive agency costs, as bondholders impose various restrictions and covenants which will diminish firm value.

C)investments of the same risk class that the firm is in.

D)undertaking scale enhancing projects.

E)lower agency costs, as shareholders have more control over the firm's assets.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

30

Studies have found that firms with high proportions of intangible assets are likely to use ____________ debt compared with firms with low proportions of intangible assets.

A)more

B)the same amount of

C)less

D)either more or the same amount of

E)any amount of debt

A)more

B)the same amount of

C)less

D)either more or the same amount of

E)any amount of debt

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

31

If a firm issues debt but writes protective and restrictive covenants into the loan contract, then the firm's debt may be issued at a _____ interest rate compared with otherwise similar debt.

A)significantly higher

B)slightly higher

C)equal

D)lower

E)Either A or B

A)significantly higher

B)slightly higher

C)equal

D)lower

E)Either A or B

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

32

What three factors are important to consider in determining a target debt to equity ratio?

A)Taxes, asset types, and pecking order and financial slack

B)Asset types, uncertainty of operating income, and pecking order and financial slack

C)Taxes, financial slack and pecking order, and uncertainty of operating income

D)Taxes, asset types, and uncertainty of operating income

E)None of the above.

A)Taxes, asset types, and pecking order and financial slack

B)Asset types, uncertainty of operating income, and pecking order and financial slack

C)Taxes, financial slack and pecking order, and uncertainty of operating income

D)Taxes, asset types, and uncertainty of operating income

E)None of the above.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

33

In a Miller equilibrium, what type of investments do high tax bracket investors tend to hold?

A)Bonds

B)Stocks

C)Debentures

D)Both stocks and bonds.

E)Neither stocks nor bonds.

A)Bonds

B)Stocks

C)Debentures

D)Both stocks and bonds.

E)Neither stocks nor bonds.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

34

In Miller's model, when the quantity [(1 - Tc)(1 - Ts) = (1 - Tb)], then:

A)the firm should hold no debt.

B)the value of the levered firm is greater than the value of the unlevered firm.

C)the tax shield on debt is exactly offset by higher personal taxes paid on interest income.

D)the tax shield on debt is exactly offset by higher levels of dividends.

E)the tax shield on debt is exactly offset by higher capital gains.

A)the firm should hold no debt.

B)the value of the levered firm is greater than the value of the unlevered firm.

C)the tax shield on debt is exactly offset by higher personal taxes paid on interest income.

D)the tax shield on debt is exactly offset by higher levels of dividends.

E)the tax shield on debt is exactly offset by higher capital gains.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

35

Which of the following is true?

A)A firm with low anticipated profit will likely take on a high level of debt.

B)A successful firm will probably take on zero debt.

C)Rational firms raise debt levels when profits are expected to decline.

D)Rational investors are likely to infer a higher firm value from a zero debt level.

E)Investors will generally view an increase in debt as a positive sign for the firm's value.

A)A firm with low anticipated profit will likely take on a high level of debt.

B)A successful firm will probably take on zero debt.

C)Rational firms raise debt levels when profits are expected to decline.

D)Rational investors are likely to infer a higher firm value from a zero debt level.

E)Investors will generally view an increase in debt as a positive sign for the firm's value.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

36

The value of a firm in financial distress is diminished if the firm:

A)is declared bankrupt and proceeds to be liquidated.

B)is declared insolvent and undergoes financial reorganization.

C)is a partnership.

D)Both A and C.

E)Both A and B.

A)is declared bankrupt and proceeds to be liquidated.

B)is declared insolvent and undergoes financial reorganization.

C)is a partnership.

D)Both A and C.

E)Both A and B.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

37

Issuing debt instead of new equity in a closely held firm more likely:

A)causes the owner-manager to work less hard and shirk their duties as they have less capital at risk.

B)causes the owner-manager to consume more perquisites because the cost is passed to the debtholders.

C)causes both more shirking and perquisite consumption since the government provides a tax shield on debt.

D)causes agency costs to fall as owner-managers do not need to worry about other shareholders.

E)causes the owner-manager to reduce shirking and perquisite consumption as the excess cash flow must be used to meet debt payments.

A)causes the owner-manager to work less hard and shirk their duties as they have less capital at risk.

B)causes the owner-manager to consume more perquisites because the cost is passed to the debtholders.

C)causes both more shirking and perquisite consumption since the government provides a tax shield on debt.

D)causes agency costs to fall as owner-managers do not need to worry about other shareholders.

E)causes the owner-manager to reduce shirking and perquisite consumption as the excess cash flow must be used to meet debt payments.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

38

When firms issue more debt, the tax shield on debt _____, the agency costs on debt (i.e., costs of financial distress) _____, and the agency costs on equity _____.

A)increases; increase; increase

B)decreases; decrease; decrease

C)increases; increase; decrease

D)decreases; decrease; increase

E)increases; decrease; decrease

A)increases; increase; increase

B)decreases; decrease; decrease

C)increases; increase; decrease

D)decreases; decrease; increase

E)increases; decrease; decrease

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

39

Indirect costs of bankruptcy are born principally by:

A)bondholders.

B)stockholders.

C)managers.

D)the federal government.

E)the firm's suppliers.

A)bondholders.

B)stockholders.

C)managers.

D)the federal government.

E)the firm's suppliers.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

40

An exchange may offer:

A)allow customers a 30 day money-back guarantee on the firm's product.

B)allow customers a 90 day warranty on the firm's product from defects.

C)allow bondholders to exchange some debt for stock.

D)allow stockholders to exchange some of their stock for debt.

E)Both C and D.

A)allow customers a 30 day money-back guarantee on the firm's product.

B)allow customers a 90 day warranty on the firm's product from defects.

C)allow bondholders to exchange some debt for stock.

D)allow stockholders to exchange some of their stock for debt.

E)Both C and D.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

41

An investment is available that pays a tax-free 7%.The corporate tax rate is 40%.Ignoring risk, what is the pre-tax return on taxable bonds?

A)4.20%

B)7.00%

C)7.47%

D)11.67%

E)None of the above

A)4.20%

B)7.00%

C)7.47%

D)11.67%

E)None of the above

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

42

The TrunkLine Company will earn $60 in one year if it does well.The debtholders are promised payments of $35 in one year if the firm does well.If the firm does poorly, expected earnings in one year will be $30 and the repayment will be $20 because of the dead weight cost of bankruptcy.The probability of the firm performing poorly or well is 50%.If bondholders are fully aware of these costs what will they pay for the debt? The interest rate on the bonds is 10%.

A)$25.00

B)$27.50

C)$29.55

D)$32.50

E)$35.00

A)$25.00

B)$27.50

C)$29.55

D)$32.50

E)$35.00

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

43

An investment is available that pays a tax-free 6%.The corporate tax rate is 30%.Ignoring risk, what is the pre-tax return on taxable bonds?

A)4.20%

B)6.00%

C)7.67%

D)8.57%

E)None of the above.

A)4.20%

B)6.00%

C)7.67%

D)8.57%

E)None of the above.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

44

What are the advantages of a prepackaged bankruptcy for a firm? What are the disadvantages?

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

45

Given the following information, leverage will add how much value to the unlevered firm per dollar of debt? Corporate tax rate: 30%

Personal tax rate on income from bonds: 20%

Personal tax rate on income from stocks: 0%

A)$0.125

B)$0.472

C)$0.528

D)$0.825

E)None of the above

Personal tax rate on income from bonds: 20%

Personal tax rate on income from stocks: 0%

A)$0.125

B)$0.472

C)$0.528

D)$0.825

E)None of the above

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

46

Given the following information, leverage will add how much value to the unlevered firm per dollar of debt? Corporate tax rate: 34%

Personal tax rate on income from bonds: 20%

Personal tax rate on income from stocks: 0%

A)$0.175

B)$0.472

C)$0.528

D)$0.825

E)None of the above

Personal tax rate on income from bonds: 20%

Personal tax rate on income from stocks: 0%

A)$0.175

B)$0.472

C)$0.528

D)$0.825

E)None of the above

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

47

Given the following information, leverage will add how much value to the unlevered firm per dollar of debt? Corporate tax rate: 34%

Personal tax rate on income from bonds: 50%

Personal tax rate on income from stocks: 10%

A)$-0.050

B)$-0.188

C)$0.188

D)$0.633

E)None of the above

Personal tax rate on income from bonds: 50%

Personal tax rate on income from stocks: 10%

A)$-0.050

B)$-0.188

C)$0.188

D)$0.633

E)None of the above

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

48

The Aggie Company has EBIT of $70,000 and market value debt of $100,000 outstanding with a 9% coupon rate.The cost of equity for an all equity firm would be 14%.Aggie has a 35% corporate tax rate.Investors face a 20% tax rate on debt receipts and a 15% rate on equity.Determine the value of Aggie.

A)$120,000

B)$162,948

C)$258,537

D)$263,080

E)$355,938

A)$120,000

B)$162,948

C)$258,537

D)$263,080

E)$355,938

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

49

Given the following information, leverage will add how much value to the unlevered firm per dollar of debt? Corporate tax rate: 34%

Personal tax rate on income from bonds: 10%

Personal tax rate on income from stocks: 50%

A)$-0.050

B)$-0.188

C)$0.367

D)$0.633

E)None of the above

Personal tax rate on income from bonds: 10%

Personal tax rate on income from stocks: 50%

A)$-0.050

B)$-0.188

C)$0.367

D)$0.633

E)None of the above

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

50

Given the following information, leverage will add how much value to the unlevered firm per dollar of debt? Corporate tax rate: 34%

Personal tax rate on income from bonds: 20%

Personal tax rate on income from stocks: 30%

A)$-0.050

B)$0.006

C)$0.246

D)$0.340

E)$0.423

Personal tax rate on income from bonds: 20%

Personal tax rate on income from stocks: 30%

A)$-0.050

B)$0.006

C)$0.246

D)$0.340

E)$0.423

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

51

Given the following information, leverage will add how much value to the unlevered firm per dollar of debt? Corporate tax rate: 34%

Personal tax rate on income from bonds: 20%

Personal tax rate on income from stocks: 50%

A)$-0.050

B)$-0.188

C)$0.367

D)$0.588

E)None of the above

Personal tax rate on income from bonds: 20%

Personal tax rate on income from stocks: 50%

A)$-0.050

B)$-0.188

C)$0.367

D)$0.588

E)None of the above

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

52

Is there an easily identifiable debt-equity ratio that will maximize the value of a firm? Why or why not?

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

53

Holly Berry Incorporated will earn $40 in one year if it does well.The debtholders are promised payments of $25 in one year if the firm does well.If the firm does poorly, expected earnings in one year will be $20 and the repayment will be $15 because of the dead weight cost of bankruptcy.The probability of the firm performing poorly or well is 50%.If bondholders are fully aware of these costs what will they pay for the debt? The interest rate on the bonds is 8%.

A)$18.52

B)$30.00

C)$32.55

D)$35.75

E)$37.04

A)$18.52

B)$30.00

C)$32.55

D)$35.75

E)$37.04

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

54

Given the following information, leverage will add how much value to the unlevered firm per dollar of debt? Corporate tax rate: 34%

Personal tax rate on income from bonds: 30%

Personal tax rate on income from stocks: 30%

A)$-0.050

B)$0.006

C)$0.246

D)$0.340

E)$0.660

Personal tax rate on income from bonds: 30%

Personal tax rate on income from stocks: 30%

A)$-0.050

B)$0.006

C)$0.246

D)$0.340

E)$0.660

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

55

Given the following information, leverage will add how much value to the unlevered firm per dollar of debt? Corporate tax rate: 40%

Personal tax rate on income from bonds: 20%

Personal tax rate on income from stocks: 30%

A)$-0.475

B)$0.475

C)$0.525

D)$0.633

E)None of the above

Personal tax rate on income from bonds: 20%

Personal tax rate on income from stocks: 30%

A)$-0.475

B)$0.475

C)$0.525

D)$0.633

E)None of the above

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

56

The TrunkLine Company debtholders are promised payments of $35 if the firm does well, but will receive only $20 if the firm does poorly.Bondholders are willing to pay $25.The promised return to the bondholders is approximately:

A)2.9%

B)16.9%

C)27.3%

D)40.0%

E)100%

A)2.9%

B)16.9%

C)27.3%

D)40.0%

E)100%

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

57

Holly Berry Incorporated debtholders are promised payments of $25 if the firm does well, but will receive only $20 if the firm does poorly.Bondholders are willing to pay $15.The promised return to the bondholders is approximately:

A)5.65%

B)45.65%

C)50.00%

D)66.67%

E)100.00%

A)5.65%

B)45.65%

C)50.00%

D)66.67%

E)100.00%

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

58

Your firm has a debt-equity ratio of .60.Your cost of equity is 11% and your after-tax cost of debt is 7%.What will your cost of equity be if the target capital structure becomes a 50/50 mix of debt and equity?

A)9.50%

B)10.50%

C)11.00%

D)11.25%

E)12.00%

A)9.50%

B)10.50%

C)11.00%

D)11.25%

E)12.00%

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

59

Suppose a Miller equilibrium exists with a corporate tax rate of 30% and a personal tax rate on income from bonds of 35%.What is the personal tax rate on income from stocks?

A)0.0%

B)7.1%

C)10.05%

D)45.5%

E)None of the above

A)0.0%

B)7.1%

C)10.05%

D)45.5%

E)None of the above

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

60

The Aggie Company has EBIT of $50,000 and market value debt of $100,000 outstanding with a 9% coupon rate.The cost of equity for an all equity firm would be 14%.Aggie has a 35% corporate tax rate.Investors face a 20% tax rate on debt receipts and a 15% rate on equity.Determine the value of Aggie.

A)$120,000

B)$162,948

C)$258,537

D)$263,080

E)$332,143

A)$120,000

B)$162,948

C)$258,537

D)$263,080

E)$332,143

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

61

What is the pecking order theory and what are the implications that arise from this theory?

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

62

Consider an economy in which there are three groups of investors and no others.

There are no personal taxes on income from stocks.An investment is available that pays a tax-free 4%.The corporate tax rate is 50%.Total corporate income before earnings and taxes (EBIT) is $224 million forever.What is the maximum debt-to-equity ratio for the economy as a whole?

There are no personal taxes on income from stocks.An investment is available that pays a tax-free 4%.The corporate tax rate is 50%.Total corporate income before earnings and taxes (EBIT) is $224 million forever.What is the maximum debt-to-equity ratio for the economy as a whole? Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

63

The All-Mine Corporation is deciding whether to invest in a new project.The project would have to be financed by equity, the cost is $2,000 and will return $2,500 or 25% in one year.The discount rate for both bonds and stock is 15% and the tax rate is zero.The predicted cash flows are $4,500 in a good economy, $3,000 in an average economy and $1,000 in a poor economy.Each economic outcome is equally likely and the promised debt repayment is $3,000.Should the company take the project? What is the value of firm and its components before and after the project addition?

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

64

Define and describe the direct and indirect costs of bankruptcy.Give three examples of each.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

65

If the firm were to convert $4 million of equity into debt at a cost of 10%, what would be the total cash flow to Louis if he holds all the debt? Compare this to Louis' total cash flow if the firm remains unlevered.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

66

Assume that all earnings are paid out as dividends.Now consider the fact that Louis must pay personal tax on the firm's cash flow.Louis pays taxes on interest at a rate of 33%, but pays taxes on dividends at a rate of 28%.Calculate the total cash flow to Louis after he pays personal taxes.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

67

Establishing a capital structure for a firm is not simple.Although financial theory guides the process, there is no simple formula.List and explain four main items that one should consider in determining the capital structure.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

68

The Do-All-Right Marketing Research firm has promised payments to its bondholders that total $100.The company believes that there is a 85% chance that the cash flow will be sufficient to meet these claims.However, there is a 15% chance that cash flows will fall short, in which case total earnings are expected to be $65.If the bonds sell in the market for $84, what is an estimate of the bankruptcy costs for Do-All-Right? Assume a cost of debt of 10%.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

69

Describe some of the sources of business risk and financial risk.Do financial decision makers have the ability to "trade off" one type of risk for the other?

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 69 flashcards in this deck.