Deck 5: Cost Allocation and Activity-Based Costing Systems

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Stumbo Company has two production departments, Cutting and Assembling, served by one maintenance department. Budgeted fixed costs for the maintenance department for 20X3 were $60,000, and the variable cost per labour hour was $2.00. Other relevant data for 20X3 are as follows:

Actual maintenance department costs for 20X3 were $64,000 fixed and $120,000 variable.

Actual maintenance department costs for 20X3 were $64,000 fixed and $120,000 variable.

*in labour hours

The amount of fixed maintenance costs allocated to the Assembling Department should be

A) $36,000.

B) $24,000.

C) $28,000.

D) $22,500.

Actual maintenance department costs for 20X3 were $64,000 fixed and $120,000 variable.*in labour hours

The amount of fixed maintenance costs allocated to the Assembling Department should be

A) $36,000.

B) $24,000.

C) $28,000.

D) $22,500.

Question

Stohr Company has two departments, New and Old. Central costs are allocated to the two departments in various ways. Relevant information is presented below:

If total advertising expense is $240,000 and it is allocated on the basis of sales, the amount allocated to the New Department should be

A) $40,000.

B) $60,000.

C) $168,000.

D) $200,000.

If total advertising expense is $240,000 and it is allocated on the basis of sales, the amount allocated to the New Department should be

A) $40,000.

B) $60,000.

C) $168,000.

D) $200,000.

Question

Boone Manufacturing has two production departments, Mixing and Finishing, served by one maintenance department. Budgeted fixed costs for the maintenance department for 20X3 were $20,000, and the variable cost per labour hour was $3.00. Other relevant data for 20X3 are as follows:

Actual maintenance department costs for 20X3 were $24,000 fixed and $50,000 variable.

Actual maintenance department costs for 20X3 were $24,000 fixed and $50,000 variable.

*in labour hours

The amount of variable maintenance costs allocated to the Finishing Department should be

A) $21,000.

B) $24,000.

C) $18,750.

D) $18,000.

Actual maintenance department costs for 20X3 were $24,000 fixed and $50,000 variable.*in labour hours

The amount of variable maintenance costs allocated to the Finishing Department should be

A) $21,000.

B) $24,000.

C) $18,750.

D) $18,000.

Question

Stumbo Company has two production departments, Cutting and Assembling, served by one maintenance department. Budgeted fixed costs for the maintenance department for 20X3 were $60,000, and the variable cost per labour hour was $2.00. Other relevant data for 20X3 are as follows:

Actual maintenance department costs for 20X3 were $64,000 fixed and $120,000 variable.

*in labour hours

The amount of variable maintenance costs allocated to the Cutting Department should be

A) $80,000.

B) $96,000.

C) $64,000.

D) $83,333.

Actual maintenance department costs for 20X3 were $64,000 fixed and $120,000 variable.*in labour hours

The amount of variable maintenance costs allocated to the Cutting Department should be

A) $80,000.

B) $96,000.

C) $64,000.

D) $83,333.

Question

Stohr Company has two departments, New and Old. Central costs are allocated to the two departments in various ways. Relevant information is presented below:

If total payroll processing costs are $40,000 and they are allocated on the basis of number of employees, the amount allocated to the Old Department should be

A) $28,000.

B) $12,000.

C) $30,000.

D) $33,333.

If total payroll processing costs are $40,000 and they are allocated on the basis of number of employees, the amount allocated to the Old Department should be

A) $28,000.

B) $12,000.

C) $30,000.

D) $33,333.

Question

Boone Manufacturing has two production departments, Mixing and Finishing, served by one maintenance department. Budgeted fixed costs for the maintenance department for 20X3 were $20,000, and the variable cost per labour hour was $3.00. Other relevant data for 20X3 are as follows:

Actual maintenance department costs for 20X3 were $24,000 fixed and $50,000 variable.

*in labour hours

The amount of variable maintenance costs allocated to the Mixing Department should be

A) $30,000.

B) $36,000.

C) $24,000.

D) $31,250.

Actual maintenance department costs for 20X3 were $24,000 fixed and $50,000 variable.*in labour hours

The amount of variable maintenance costs allocated to the Mixing Department should be

A) $30,000.

B) $36,000.

C) $24,000.

D) $31,250.

Question

Stohr Company has two departments, New and Old. Central costs are allocated to the two departments in various ways. Relevant information is presented below:

If total rent expense is $192,000 and it is allocated on the basis of square footage, the amount allocated to the Old Department should be

A) $57,600.

B) $160,000.

C) $144,000.

D) $48,000.

If total rent expense is $192,000 and it is allocated on the basis of square footage, the amount allocated to the Old Department should be

A) $57,600.

B) $160,000.

C) $144,000.

D) $48,000.

Question

Question

Stumbo Company has two production departments, Cutting and Assembling, served by one maintenance department. Budgeted fixed costs for the maintenance department for 20X3 were $60,000, and the variable cost per labour hour was $2.00. Other relevant data for 20X3 are as follows:

Actual maintenance department costs for 20X3 were $64,000 fixed and $120,000 variable.

*in labour hours

The amount of fixed maintenance costs allocated to the Cutting Department should be

A) $40,000.

B) $24,000.

C) $36,000.

D) $28,000.

Actual maintenance department costs for 20X3 were $64,000 fixed and $120,000 variable.*in labour hours

The amount of fixed maintenance costs allocated to the Cutting Department should be

A) $40,000.

B) $24,000.

C) $36,000.

D) $28,000.

Question

Stumbo Company has two production departments, Cutting and Assembling, served by one maintenance department. Budgeted fixed costs for the maintenance department for 20X3 were $60,000, and the variable cost per labour hour was $2.00. Other relevant data for 20X3 are as follows:

Actual maintenance department costs for 20X3 were $64,000 fixed and $120,000 variable.

*in labour hours

The amount of variable maintenance costs allocated to the Assembling Department should be

A) $56,000.

B) $64,000.

C) $50,000.

D) $48,000.

Actual maintenance department costs for 20X3 were $64,000 fixed and $120,000 variable.*in labour hours

The amount of variable maintenance costs allocated to the Assembling Department should be

A) $56,000.

B) $64,000.

C) $50,000.

D) $48,000.

Question

Stohr Company has two departments, New and Old. Central costs are allocated to the two departments in various ways. Relevant information is presented below:

If total advertising expense is $120,000 and it is allocated on the basis of sales, the amount allocated to the Old Department should be

A) $90,000.

B) $36,000.

C) $100,000.

D) $ 20,000.

If total advertising expense is $120,000 and it is allocated on the basis of sales, the amount allocated to the Old Department should be

A) $90,000.

B) $36,000.

C) $100,000.

D) $ 20,000.

Question

Question

Question

Question

Boone Manufacturing has two production departments, Mixing and Finishing, served by one maintenance department. Budgeted fixed costs for the maintenance department for 20X3 were $20,000, and the variable cost per labour hour was $3.00. Other relevant data for 20X3 are as follows:

Actual maintenance department costs for 20X3 were $24,000 fixed and $50,000 variable.

*in labour hours

The amount of fixed maintenance costs allocated to the Finishing Department should be

A) $12,000.

B) $ 8,000.

C) $ 9,333.

D) $ 7,500.

Actual maintenance department costs for 20X3 were $24,000 fixed and $50,000 variable.*in labour hours

The amount of fixed maintenance costs allocated to the Finishing Department should be

A) $12,000.

B) $ 8,000.

C) $ 9,333.

D) $ 7,500.

Question

Stohr Company has two departments, New and Old. Central costs are allocated to the two departments in various ways. Relevant information is presented below:

If total rent expense is $80,000 and it is allocated on the basis of square footage, the amount allocated to the New Department should be

A) $13,333.

B) $20,000.

C) $56,000.

D) $60,000.

If total rent expense is $80,000 and it is allocated on the basis of square footage, the amount allocated to the New Department should be

A) $13,333.

B) $20,000.

C) $56,000.

D) $60,000.

Question

Boone Manufacturing has two production departments, Mixing and Finishing, served by one maintenance department. Budgeted fixed costs for the maintenance department for 20X3 were $20,000, and the variable cost per labour hour was $3.00. Other relevant data for 20X3 are as follows:

Actual maintenance department costs for 20X3 were $24,000 fixed and $50,000 variable.

*in labour hours

The amount of fixed maintenance costs allocated to the Mixing Department should be

A) $13,333.

B) $8,000.

C) $12,000.

D) $9,333.

Actual maintenance department costs for 20X3 were $24,000 fixed and $50,000 variable.*in labour hours

The amount of fixed maintenance costs allocated to the Mixing Department should be

A) $13,333.

B) $8,000.

C) $12,000.

D) $9,333.

Question

Question

Stohr Company has two departments, New and Old. Central costs are allocated to the two departments in various ways. Relevant information is presented below:

If total payroll processing costs are $64,000 and they are allocated on the basis of number of employees, the amount allocated to the New Department should be

A) $44,800.

B) $16,000.

C) $10,667.

D) $19,200.

If total payroll processing costs are $64,000 and they are allocated on the basis of number of employees, the amount allocated to the New Department should be

A) $44,800.

B) $16,000.

C) $10,667.

D) $19,200.

Question

Question

County Company has two service departments, Maintenance and Personnel, as well as two production departments, Mixing and Finishing. Maintenance costs are allocated based on square footage, while personnel costs are allocated based on number of employees. The following information has been gathered for the current year:

If the direct method is used to allocate costs, the total cost of the Mixing Department after allocation would be

A) $121,714.

B) $41,143.

C) $20,571.

D) $60,000.

If the direct method is used to allocate costs, the total cost of the Mixing Department after allocation would be

A) $121,714.

B) $41,143.

C) $20,571.

D) $60,000.

Question

City Company has two service departments, Maintenance and Personnel, as well as two production departments, Mixing and Finishing. Maintenance costs are allocated based on square footage while personnel costs are allocated based on number of employees. The following information has been gathered for the current year:

If the direct method is used to allocate costs, the total cost of the Finishing Department after allocation would be

A) $7,714.

B) $6,858.

C) $39,571.

D) $25,000.

If the direct method is used to allocate costs, the total cost of the Finishing Department after allocation would be

A) $7,714.

B) $6,858.

C) $39,571.

D) $25,000.

Question

City Company has two service departments, Maintenance and Personnel, as well as two production departments, Mixing and Finishing. Maintenance costs are allocated based on square footage while personnel costs are allocated based on number of employees. The following information has been gathered for the current year:

If the step-down method of allocating costs is used, and the Personnel Department renders the greatest service, then the total amount of overhead that would be allocated from Maintenance to Mixing is

A) $4,500.

B) $8,357.

C) $9,000.

D) $11,143.

If the step-down method of allocating costs is used, and the Personnel Department renders the greatest service, then the total amount of overhead that would be allocated from Maintenance to Mixing is

A) $4,500.

B) $8,357.

C) $9,000.

D) $11,143.

Question

County Company has two service departments, Maintenance and Personnel, as well as two production departments, Mixing and Finishing. Maintenance costs are allocated based on square footage, while personnel costs are allocated based on number of employees. The following information has been gathered for the current year:

If the step-down method is used to allocate costs, and the Maintenance Department renders the greatest service, then the total cost of the Mixing Department after allocation would be

A) $120,429.

B) $122,571.

C) $121,712.

D) $ 60,000.

If the step-down method is used to allocate costs, and the Maintenance Department renders the greatest service, then the total cost of the Mixing Department after allocation would be

A) $120,429.

B) $122,571.

C) $121,712.

D) $ 60,000.

Question

Question

City Company has two service departments, Maintenance and Personnel, as well as two production departments, Mixing and Finishing. Maintenance costs are allocated based on square footage while personnel costs are allocated based on number of employees. The following information has been gathered for the current year:

If the step-down method is used to allocate costs, and the Maintenance Department renders the greatest service, then the total cost of the Mixing Department after allocation would be

A) $30,107.

B) $30,642.

C) $30,428.

D) $15,000.

If the step-down method is used to allocate costs, and the Maintenance Department renders the greatest service, then the total cost of the Mixing Department after allocation would be

A) $30,107.

B) $30,642.

C) $30,428.

D) $15,000.

Question

Question

City Company has two service departments, Maintenance and Personnel, as well as two production departments, Mixing and Finishing. Maintenance costs are allocated based on square footage while personnel costs are allocated based on number of employees. The following information has been gathered for the current year:

If the direct method is used to allocate costs, the total cost of the Mixing Department after allocation would be

A) $30,429.

B) $10,286.

C) $5,143.

D) $15,000.

If the direct method is used to allocate costs, the total cost of the Mixing Department after allocation would be

A) $30,429.

B) $10,286.

C) $5,143.

D) $15,000.

Question

County Company has two service departments, Maintenance and Personnel, as well as two production departments, Mixing and Finishing. Maintenance costs are allocated based on square footage, while personnel costs are allocated based on number of employees. The following information has been gathered for the current year:

If the step-down method is used to allocate costs, and the Personnel Department renders the greatest service, then the total cost of the Finishing Department after allocation would be

A) $100,000.

B) $158,288.

C) $159,571.

D) $157,429.

If the step-down method is used to allocate costs, and the Personnel Department renders the greatest service, then the total cost of the Finishing Department after allocation would be

A) $100,000.

B) $158,288.

C) $159,571.

D) $157,429.

Question

County Company has two service departments, Maintenance and Personnel, as well as two production departments, Mixing and Finishing. Maintenance costs are allocated based on square footage, while personnel costs are allocated based on number of employees. The following information has been gathered for the current year:

If the step-down method of allocating costs is used, and the Personnel Department renders the greatest service, then the total amount of overhead that would be allocated from Maintenance to Mixing is

A) $18,000.

B) $33,428.

C) $36,000.

D) $44,571.

If the step-down method of allocating costs is used, and the Personnel Department renders the greatest service, then the total amount of overhead that would be allocated from Maintenance to Mixing is

A) $18,000.

B) $33,428.

C) $36,000.

D) $44,571.

Question

Question

County Company has two service departments, Maintenance and Personnel, as well as two production departments, Mixing and Finishing. Maintenance costs are allocated based on square footage, while personnel costs are allocated based on number of employees. The following information has been gathered for the current year:

If the step-down method of allocating costs is used, and the Personnel Department renders the greatest service, then the total amount of overhead that would be allocated from Maintenance to Finishing is

A) $24,000.

B) $33,429.

C) $27,000.

D) $32,568.

If the step-down method of allocating costs is used, and the Personnel Department renders the greatest service, then the total amount of overhead that would be allocated from Maintenance to Finishing is

A) $24,000.

B) $33,429.

C) $27,000.

D) $32,568.

Question

County Company has two service departments, Maintenance and Personnel, as well as two production departments, Mixing and Finishing. Maintenance costs are allocated based on square footage, while personnel costs are allocated based on number of employees. The following information has been gathered for the current year:

If the direct method is used to allocate costs, the total cost of the Finishing Department after allocation would be

A) $30,857.

B) $27,429.

C) $158,286.

D) $100,000.

If the direct method is used to allocate costs, the total cost of the Finishing Department after allocation would be

A) $30,857.

B) $27,429.

C) $158,286.

D) $100,000.

Question

City Company has two service departments, Maintenance and Personnel, as well as two production departments, Mixing and Finishing. Maintenance costs are allocated based on square footage while personnel costs are allocated based on number of employees. The following information has been gathered for the current year:

If the step-down method is used to allocate costs, and the Maintenance Department renders the greatest service, the total amount of overhead that would be allocated from Personnel to Mixing is

A) $5,143.

B) $6,107.

C) $6,000.

D) $9,000.

If the step-down method is used to allocate costs, and the Maintenance Department renders the greatest service, the total amount of overhead that would be allocated from Personnel to Mixing is

A) $5,143.

B) $6,107.

C) $6,000.

D) $9,000.

Question

County Company has two service departments, Maintenance and Personnel, as well as two production departments, Mixing and Finishing. Maintenance costs are allocated based on square footage, while personnel costs are allocated based on number of employees. The following information has been gathered for the current year:

If the step-down method is used to allocate costs, and the Maintenance Department renders the greatest service, the total amount of overhead that would be allocated from Personnel to Mixing is

A) $20,572.

B) $24,429.

C) $24,000.

D) $36,000.

If the step-down method is used to allocate costs, and the Maintenance Department renders the greatest service, the total amount of overhead that would be allocated from Personnel to Mixing is

A) $20,572.

B) $24,429.

C) $24,000.

D) $36,000.

Question

City Company has two service departments, Maintenance and Personnel, as well as two production departments, Mixing and Finishing. Maintenance costs are allocated based on square footage while personnel costs are allocated based on number of employees. The following information has been gathered for the current year:

If the step-down method is used to allocate costs, and the Maintenance Department renders the greatest service, then the total amount of overhead that would be allocated from Personnel to Finishing is

A) $6,107.

B) $4,500.

C) $8,143.

D) $6,750.

If the step-down method is used to allocate costs, and the Maintenance Department renders the greatest service, then the total amount of overhead that would be allocated from Personnel to Finishing is

A) $6,107.

B) $4,500.

C) $8,143.

D) $6,750.

Question

City Company has two service departments, Maintenance and Personnel, as well as two production departments, Mixing and Finishing. Maintenance costs are allocated based on square footage while personnel costs are allocated based on number of employees. The following information has been gathered for the current year:

If the step-down method of allocating costs is used, and the Personnel Department renders the greatest service, then the total amount of overhead that would be allocated from Maintenance to Finishing is

A) $6,000.

B) $8,357.

C) $6,750.

D) $8,142.

If the step-down method of allocating costs is used, and the Personnel Department renders the greatest service, then the total amount of overhead that would be allocated from Maintenance to Finishing is

A) $6,000.

B) $8,357.

C) $6,750.

D) $8,142.

Question

City Company has two service departments, Maintenance and Personnel, as well as two production departments, Mixing and Finishing. Maintenance costs are allocated based on square footage while personnel costs are allocated based on number of employees. The following information has been gathered for the current year:

If the step-down method is used to allocate costs, and the Personnel Department renders the greatest service, then the total cost of the Finishing Department after allocation would be

A) $25,000.

B) $39,572.

C) $39,892.

D) $39,357.

If the step-down method is used to allocate costs, and the Personnel Department renders the greatest service, then the total cost of the Finishing Department after allocation would be

A) $25,000.

B) $39,572.

C) $39,892.

D) $39,357.

Question

County Company has two service departments, Maintenance and Personnel, as well as two production departments, Mixing and Finishing. Maintenance costs are allocated based on square footage, while personnel costs are allocated based on number of employees. The following information has been gathered for the current year:

If the step-down method is used to allocate costs, and the Maintenance Department renders the greatest service, then the total amount of overhead that would be allocated from Personnel to Finishing is

A) $24,429.

B) $18,000.

C) $32,571.

D) $27,000.

If the step-down method is used to allocate costs, and the Maintenance Department renders the greatest service, then the total amount of overhead that would be allocated from Personnel to Finishing is

A) $24,429.

B) $18,000.

C) $32,571.

D) $27,000.

Question

Question

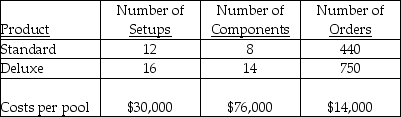

Stanley Corp. manufactures two models of its roasting pans, a standard and a deluxe model. Three activities have been identified as cost drivers and the related costs pooled together to arrive at the following information:

If activity-based costing is used, then the product setup cost for the standard model would be

A) $12,857.

B) $17,143.

C) $1,071.

D) $1,866.

If activity-based costing is used, then the product setup cost for the standard model would be

A) $12,857.

B) $17,143.

C) $1,071.

D) $1,866.

Question

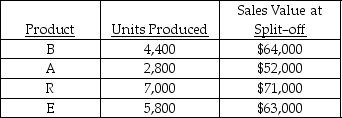

Bare Company manufactures four products from a joint process. Joint costs for the year amounted to $140,000. The following data are also available:

Assuming the relative-sales-value method of allocating joint costs, the amount of joint costs allocated to product E would be

A) $40,600.00.

B) $64,444.40.

C) $58,000.00.

D) $35,280.00.

Assuming the relative-sales-value method of allocating joint costs, the amount of joint costs allocated to product E would be

A) $40,600.00.

B) $64,444.40.

C) $58,000.00.

D) $35,280.00.

Question

Bare Company manufactures four products from a joint process. Joint costs for the year amounted to $140,000. The following data are also available:

Assuming the relative-sales-value method of allocating joint costs, the amount of joint costs allocated to product A would be

A) $19,600.

B) $37,692.

C) $29,120.

D) $16,640.

Assuming the relative-sales-value method of allocating joint costs, the amount of joint costs allocated to product A would be

A) $19,600.

B) $37,692.

C) $29,120.

D) $16,640.

Question

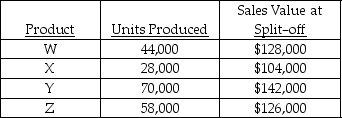

Upjohn Company manufactures four products from a joint process. Joint costs for the year amounted to $350,000. The following data are also available:

Assuming the physical-units method of allocating joint costs, the amount of joint costs allocated to product Y would be

A) $172,536.

B) $99,400.

C) $122,500.

D) $24,648.

Assuming the physical-units method of allocating joint costs, the amount of joint costs allocated to product Y would be

A) $172,536.

B) $99,400.

C) $122,500.

D) $24,648.

Question

Bare Company manufactures four products from a joint process. Joint costs for the year amounted to $140,000. The following data are also available:

Assuming the relative-sales-value method of allocating joint costs, the amount of joint costs allocated to product B would be

A) $35,840.00.

B) $48,124.80.

C) $30,800.00.

D) $20,160.00.

Assuming the relative-sales-value method of allocating joint costs, the amount of joint costs allocated to product B would be

A) $35,840.00.

B) $48,124.80.

C) $30,800.00.

D) $20,160.00.

Question

Question

Question

Stanley Corp. manufactures two models of its roasting pans, a standard and a deluxe model. Three activities have been identified as cost drivers and the related costs pooled together to arrive at the following information:

If activity-based costing is used, then the total amount of overhead allocated to the standard model would be

A) $74,330.

B) $120,000.

C) $40,000.

D) $45,670.

If activity-based costing is used, then the total amount of overhead allocated to the standard model would be

A) $74,330.

B) $120,000.

C) $40,000.

D) $45,670.

Question

Stanley Corp. manufactures two models of its roasting pans, a standard and a deluxe model. Three activities have been identified as cost drivers and the related costs pooled together to arrive at the following information:

If activity-based costing is used, then the total amount of overhead allocated to the deluxe model would be

A) $45,670.

B) $74,330.

C) $120,000.

D) $ 80,000.

If activity-based costing is used, then the total amount of overhead allocated to the deluxe model would be

A) $45,670.

B) $74,330.

C) $120,000.

D) $ 80,000.

Question

Question

Question

Upjohn Company manufactures four products from a joint process. Joint costs for the year amounted to $350,000. The following data are also available:

Assuming the relative-sales-value method of allocating joint costs, the amount of joint costs allocated to product W would be

A) $89,600.

B) $120,312.

C) $77,000.

D) $50,400.

Assuming the relative-sales-value method of allocating joint costs, the amount of joint costs allocated to product W would be

A) $89,600.

B) $120,312.

C) $77,000.

D) $50,400.

Question

Bare Company manufactures four products from a joint process. Joint costs for the year amounted to $140,000. The following data are also available:

Assuming the relative-sales-value method of allocating joint costs, the amount of joint costs allocated to product R would be

A) $49,000.00.

B) $39,760.00.

C) $69,014.40.

D) $22,720.00.

Assuming the relative-sales-value method of allocating joint costs, the amount of joint costs allocated to product R would be

A) $49,000.00.

B) $39,760.00.

C) $69,014.40.

D) $22,720.00.

Question

Question

Upjohn Company manufactures four products from a joint process. Joint costs for the year amounted to $350,000. The following data are also available:

Assuming the physical-units method of allocating joint costs, the amount of joint costs allocated to product W would be

A) $120,312.

B) $62,858.

C) $122,500.

D) $77,000.

Assuming the physical-units method of allocating joint costs, the amount of joint costs allocated to product W would be

A) $120,312.

B) $62,858.

C) $122,500.

D) $77,000.

Question

Upjohn Company manufactures four products from a joint process. Joint costs for the year amounted to $350,000. The following data are also available:

Assuming the physical-units method of allocating joint costs, the amount of joint costs allocated to product Z would be

A) $101,500.

B) $89,600.

C) $161,111.

D) $82,858.

Assuming the physical-units method of allocating joint costs, the amount of joint costs allocated to product Z would be

A) $101,500.

B) $89,600.

C) $161,111.

D) $82,858.

Question

Stanley Corp. manufactures two models of its roasting pans, a standard and a deluxe model. Three activities have been identified as cost drivers and the related costs pooled together to arrive at the following information:

If activity-based costing is used, then the total cost of the components used in the deluxe model would be

A) $3,455.

B) $27,636.

C) $48,364.

D) $76,000.

If activity-based costing is used, then the total cost of the components used in the deluxe model would be

A) $3,455.

B) $27,636.

C) $48,364.

D) $76,000.

Question

Question

Upjohn Company manufactures four products from a joint process. Joint costs for the year amounted to $350,000. The following data are also available:

Assuming the physical-units method of allocating joint costs, the amount of joint costs allocated to product X would be

A) $94,230.

B) $72,800.

C) $122,500.

D) $49,000.

Assuming the physical-units method of allocating joint costs, the amount of joint costs allocated to product X would be

A) $94,230.

B) $72,800.

C) $122,500.

D) $49,000.

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/128

Play

Full screen (f)

Deck 5: Cost Allocation and Activity-Based Costing Systems

1

Activity-based accounting systems classify more costs as direct, thus simplifying and reducing the cost of a traditional system.

False

2

The goal of activity-based costing is to trace costs to products or services instead of arbitrarily allocating them.

True

3

In activity-based costing, costs are classified as either direct or indirect.

False

4

Producing departments are responsible for producing the products sold to customers.

Unlock Deck

Unlock for access to all 128 flashcards in this deck.

Unlock Deck

k this deck

5

The goal of a just-in-time production system is to have zero inventory.

Unlock Deck

Unlock for access to all 128 flashcards in this deck.

Unlock Deck

k this deck

6

One of the main objectives of cost allocation is to motivate managers.

Unlock Deck

Unlock for access to all 128 flashcards in this deck.

Unlock Deck

k this deck

7

The cost pool should be a quantifiable measure of what causes costs.

Unlock Deck

Unlock for access to all 128 flashcards in this deck.

Unlock Deck

k this deck

8

Service departments are responsible for providing services directly to customers.

Unlock Deck

Unlock for access to all 128 flashcards in this deck.

Unlock Deck

k this deck

9

Packaging is an example of a service department.

Unlock Deck

Unlock for access to all 128 flashcards in this deck.

Unlock Deck

k this deck

10

If the allocation is for performance evaluation, variable service department costs should be allocated based on the actual rate and actual usage.

Unlock Deck

Unlock for access to all 128 flashcards in this deck.

Unlock Deck

k this deck

11

The company cafeteria is an example of a producing department.

Unlock Deck

Unlock for access to all 128 flashcards in this deck.

Unlock Deck

k this deck

12

One of the main objectives of cost allocation is to value inventory.

Unlock Deck

Unlock for access to all 128 flashcards in this deck.

Unlock Deck

k this deck

13

Accounting is an example of a producing department.

Unlock Deck

Unlock for access to all 128 flashcards in this deck.

Unlock Deck

k this deck

14

Service department costs should be allocated directly to units of product.

Unlock Deck

Unlock for access to all 128 flashcards in this deck.

Unlock Deck

k this deck

15

The goal of a cost accounting system is to measure the cost of developing, producing, selling and distributing particular products or services.

Unlock Deck

Unlock for access to all 128 flashcards in this deck.

Unlock Deck

k this deck

16

The reciprocal method of allocating service department costs fully recognizes services that service departments provide to each other.

Unlock Deck

Unlock for access to all 128 flashcards in this deck.

Unlock Deck

k this deck

17

Direct-labour hours are not a very good measure of the cause of costs in modern, highly automated departments.

Unlock Deck

Unlock for access to all 128 flashcards in this deck.

Unlock Deck

k this deck

18

Actual costs should always be used when allocating service department costs.

Unlock Deck

Unlock for access to all 128 flashcards in this deck.

Unlock Deck

k this deck

19

The direct method of allocating service department costs partially recognizes services that service departments provide to each other.

Unlock Deck

Unlock for access to all 128 flashcards in this deck.

Unlock Deck

k this deck

20

Maintenance is an example of a service department.

Unlock Deck

Unlock for access to all 128 flashcards in this deck.

Unlock Deck

k this deck

21

To allocate central costs, a company could use all of the following cost drivers EXCEPT the

A) revenue of each division.

B) cost of goods sold by each division.

C) total assets of each division.

D) total period costs of each division.

A) revenue of each division.

B) cost of goods sold by each division.

C) total assets of each division.

D) total period costs of each division.

Unlock Deck

Unlock for access to all 128 flashcards in this deck.

Unlock Deck

k this deck

22

Stumbo Company has two production departments, Cutting and Assembling, served by one maintenance department. Budgeted fixed costs for the maintenance department for 20X3 were $60,000, and the variable cost per labour hour was $2.00. Other relevant data for 20X3 are as follows:

Actual maintenance department costs for 20X3 were $64,000 fixed and $120,000 variable.

*in labour hours

The amount of fixed maintenance costs allocated to the Assembling Department should be

A) $36,000.

B) $24,000.

C) $28,000.

D) $22,500.

Actual maintenance department costs for 20X3 were $64,000 fixed and $120,000 variable.*in labour hours

The amount of fixed maintenance costs allocated to the Assembling Department should be

A) $36,000.

B) $24,000.

C) $28,000.

D) $22,500.

Unlock Deck

Unlock for access to all 128 flashcards in this deck.

Unlock Deck

k this deck

23

Stohr Company has two departments, New and Old. Central costs are allocated to the two departments in various ways. Relevant information is presented below:

If total advertising expense is $240,000 and it is allocated on the basis of sales, the amount allocated to the New Department should be

A) $40,000.

B) $60,000.

C) $168,000.

D) $200,000.

If total advertising expense is $240,000 and it is allocated on the basis of sales, the amount allocated to the New Department should be

A) $40,000.

B) $60,000.

C) $168,000.

D) $200,000.

Unlock Deck

Unlock for access to all 128 flashcards in this deck.

Unlock Deck

k this deck

24

Boone Manufacturing has two production departments, Mixing and Finishing, served by one maintenance department. Budgeted fixed costs for the maintenance department for 20X3 were $20,000, and the variable cost per labour hour was $3.00. Other relevant data for 20X3 are as follows:

Actual maintenance department costs for 20X3 were $24,000 fixed and $50,000 variable.

*in labour hours

The amount of variable maintenance costs allocated to the Finishing Department should be

A) $21,000.

B) $24,000.

C) $18,750.

D) $18,000.

Actual maintenance department costs for 20X3 were $24,000 fixed and $50,000 variable.*in labour hours

The amount of variable maintenance costs allocated to the Finishing Department should be

A) $21,000.

B) $24,000.

C) $18,750.

D) $18,000.

Unlock Deck

Unlock for access to all 128 flashcards in this deck.

Unlock Deck

k this deck

25

Stumbo Company has two production departments, Cutting and Assembling, served by one maintenance department. Budgeted fixed costs for the maintenance department for 20X3 were $60,000, and the variable cost per labour hour was $2.00. Other relevant data for 20X3 are as follows:

Actual maintenance department costs for 20X3 were $64,000 fixed and $120,000 variable.

*in labour hours

The amount of variable maintenance costs allocated to the Cutting Department should be

A) $80,000.

B) $96,000.

C) $64,000.

D) $83,333.

Actual maintenance department costs for 20X3 were $64,000 fixed and $120,000 variable.*in labour hours

The amount of variable maintenance costs allocated to the Cutting Department should be

A) $80,000.

B) $96,000.

C) $64,000.

D) $83,333.

Unlock Deck

Unlock for access to all 128 flashcards in this deck.

Unlock Deck

k this deck

26

Stohr Company has two departments, New and Old. Central costs are allocated to the two departments in various ways. Relevant information is presented below:

If total payroll processing costs are $40,000 and they are allocated on the basis of number of employees, the amount allocated to the Old Department should be

A) $28,000.

B) $12,000.

C) $30,000.

D) $33,333.

If total payroll processing costs are $40,000 and they are allocated on the basis of number of employees, the amount allocated to the Old Department should be

A) $28,000.

B) $12,000.

C) $30,000.

D) $33,333.

Unlock Deck

Unlock for access to all 128 flashcards in this deck.

Unlock Deck

k this deck

27

Boone Manufacturing has two production departments, Mixing and Finishing, served by one maintenance department. Budgeted fixed costs for the maintenance department for 20X3 were $20,000, and the variable cost per labour hour was $3.00. Other relevant data for 20X3 are as follows:

Actual maintenance department costs for 20X3 were $24,000 fixed and $50,000 variable.

*in labour hours

The amount of variable maintenance costs allocated to the Mixing Department should be

A) $30,000.

B) $36,000.

C) $24,000.

D) $31,250.

Actual maintenance department costs for 20X3 were $24,000 fixed and $50,000 variable.*in labour hours

The amount of variable maintenance costs allocated to the Mixing Department should be

A) $30,000.

B) $36,000.

C) $24,000.

D) $31,250.

Unlock Deck

Unlock for access to all 128 flashcards in this deck.

Unlock Deck

k this deck

28

Stohr Company has two departments, New and Old. Central costs are allocated to the two departments in various ways. Relevant information is presented below:

If total rent expense is $192,000 and it is allocated on the basis of square footage, the amount allocated to the Old Department should be

A) $57,600.

B) $160,000.

C) $144,000.

D) $48,000.

If total rent expense is $192,000 and it is allocated on the basis of square footage, the amount allocated to the Old Department should be

A) $57,600.

B) $160,000.

C) $144,000.

D) $48,000.

Unlock Deck

Unlock for access to all 128 flashcards in this deck.

Unlock Deck

k this deck

29

Which of the following departments is NOT a service department?

A) Facilities management

B) Personnel

C) Accounting

D) Finishing

A) Facilities management

B) Personnel

C) Accounting

D) Finishing

Unlock Deck

Unlock for access to all 128 flashcards in this deck.

Unlock Deck

k this deck

30

Stumbo Company has two production departments, Cutting and Assembling, served by one maintenance department. Budgeted fixed costs for the maintenance department for 20X3 were $60,000, and the variable cost per labour hour was $2.00. Other relevant data for 20X3 are as follows:

Actual maintenance department costs for 20X3 were $64,000 fixed and $120,000 variable.

*in labour hours

The amount of fixed maintenance costs allocated to the Cutting Department should be

A) $40,000.

B) $24,000.

C) $36,000.

D) $28,000.

Actual maintenance department costs for 20X3 were $64,000 fixed and $120,000 variable.*in labour hours

The amount of fixed maintenance costs allocated to the Cutting Department should be

A) $40,000.

B) $24,000.

C) $36,000.

D) $28,000.

Unlock Deck

Unlock for access to all 128 flashcards in this deck.

Unlock Deck

k this deck

31

Stumbo Company has two production departments, Cutting and Assembling, served by one maintenance department. Budgeted fixed costs for the maintenance department for 20X3 were $60,000, and the variable cost per labour hour was $2.00. Other relevant data for 20X3 are as follows:

Actual maintenance department costs for 20X3 were $64,000 fixed and $120,000 variable.

*in labour hours

The amount of variable maintenance costs allocated to the Assembling Department should be

A) $56,000.

B) $64,000.

C) $50,000.

D) $48,000.

Actual maintenance department costs for 20X3 were $64,000 fixed and $120,000 variable.*in labour hours

The amount of variable maintenance costs allocated to the Assembling Department should be

A) $56,000.

B) $64,000.

C) $50,000.

D) $48,000.

Unlock Deck

Unlock for access to all 128 flashcards in this deck.

Unlock Deck

k this deck

32

Stohr Company has two departments, New and Old. Central costs are allocated to the two departments in various ways. Relevant information is presented below:

If total advertising expense is $120,000 and it is allocated on the basis of sales, the amount allocated to the Old Department should be

A) $90,000.

B) $36,000.

C) $100,000.

D) $ 20,000.

If total advertising expense is $120,000 and it is allocated on the basis of sales, the amount allocated to the Old Department should be

A) $90,000.

B) $36,000.

C) $100,000.

D) $ 20,000.

Unlock Deck

Unlock for access to all 128 flashcards in this deck.

Unlock Deck

k this deck

33

A group of individual costs that is allocated to cost objectives using a single cost driver is known as a

A) cost allocation base.

B) cost pool.

C) joint cost.

D) by-product.

A) cost allocation base.

B) cost pool.

C) joint cost.

D) by-product.

Unlock Deck

Unlock for access to all 128 flashcards in this deck.

Unlock Deck

k this deck

34

Which of the following is NOT a type of cost allocation?

A) Allocation of costs to the appropriate organizational unit

B) Reallocation of costs from service departments to production departments

C) Allocation of costs of a particular organizational unit to products or services

D) Reallocation of costs from production departments to service departments

A) Allocation of costs to the appropriate organizational unit

B) Reallocation of costs from service departments to production departments

C) Allocation of costs of a particular organizational unit to products or services

D) Reallocation of costs from production departments to service departments

Unlock Deck

Unlock for access to all 128 flashcards in this deck.

Unlock Deck

k this deck

35

The preferred guidelines for allocating service department costs include all of the following EXCEPT

A) identify the direct and indirect costs.

B) evaluate performance using budgets for each service department.

C) establish part or all of the details regarding cost allocation in advance of rendering the service.

D) allocate variable- and fixed-cost pools separately.

A) identify the direct and indirect costs.

B) evaluate performance using budgets for each service department.

C) establish part or all of the details regarding cost allocation in advance of rendering the service.

D) allocate variable- and fixed-cost pools separately.

Unlock Deck

Unlock for access to all 128 flashcards in this deck.

Unlock Deck

k this deck

36

Boone Manufacturing has two production departments, Mixing and Finishing, served by one maintenance department. Budgeted fixed costs for the maintenance department for 20X3 were $20,000, and the variable cost per labour hour was $3.00. Other relevant data for 20X3 are as follows:

Actual maintenance department costs for 20X3 were $24,000 fixed and $50,000 variable.

*in labour hours

The amount of fixed maintenance costs allocated to the Finishing Department should be

A) $12,000.

B) $ 8,000.

C) $ 9,333.

D) $ 7,500.

Actual maintenance department costs for 20X3 were $24,000 fixed and $50,000 variable.*in labour hours

The amount of fixed maintenance costs allocated to the Finishing Department should be

A) $12,000.

B) $ 8,000.

C) $ 9,333.

D) $ 7,500.

Unlock Deck

Unlock for access to all 128 flashcards in this deck.

Unlock Deck

k this deck

37

Stohr Company has two departments, New and Old. Central costs are allocated to the two departments in various ways. Relevant information is presented below:

If total rent expense is $80,000 and it is allocated on the basis of square footage, the amount allocated to the New Department should be

A) $13,333.

B) $20,000.

C) $56,000.

D) $60,000.

If total rent expense is $80,000 and it is allocated on the basis of square footage, the amount allocated to the New Department should be

A) $13,333.

B) $20,000.

C) $56,000.

D) $60,000.

Unlock Deck

Unlock for access to all 128 flashcards in this deck.

Unlock Deck

k this deck

38

Boone Manufacturing has two production departments, Mixing and Finishing, served by one maintenance department. Budgeted fixed costs for the maintenance department for 20X3 were $20,000, and the variable cost per labour hour was $3.00. Other relevant data for 20X3 are as follows:

Actual maintenance department costs for 20X3 were $24,000 fixed and $50,000 variable.

*in labour hours

The amount of fixed maintenance costs allocated to the Mixing Department should be

A) $13,333.

B) $8,000.

C) $12,000.

D) $9,333.

Actual maintenance department costs for 20X3 were $24,000 fixed and $50,000 variable.*in labour hours

The amount of fixed maintenance costs allocated to the Mixing Department should be

A) $13,333.

B) $8,000.

C) $12,000.

D) $9,333.

Unlock Deck

Unlock for access to all 128 flashcards in this deck.

Unlock Deck

k this deck

39

Costs are allocated for all the following purposes EXCEPT to

A) predict the economic effects of planning and control decisions.

B) obtain desired motivation.

C) determine the sales volume.

D) compute income and asset valuation.

A) predict the economic effects of planning and control decisions.

B) obtain desired motivation.

C) determine the sales volume.

D) compute income and asset valuation.

Unlock Deck

Unlock for access to all 128 flashcards in this deck.

Unlock Deck

k this deck

40

Stohr Company has two departments, New and Old. Central costs are allocated to the two departments in various ways. Relevant information is presented below:

If total payroll processing costs are $64,000 and they are allocated on the basis of number of employees, the amount allocated to the New Department should be

A) $44,800.

B) $16,000.

C) $10,667.

D) $19,200.

If total payroll processing costs are $64,000 and they are allocated on the basis of number of employees, the amount allocated to the New Department should be

A) $44,800.

B) $16,000.

C) $10,667.

D) $19,200.

Unlock Deck

Unlock for access to all 128 flashcards in this deck.

Unlock Deck

k this deck

41

A method for allocating service department costs that ignores other service departments when any given service department's costs are allocated to the revenue-producing departments is called the

A) direct method.

B) indirect method.

C) step-down method.

D) step-up method.

A) direct method.

B) indirect method.

C) step-down method.

D) step-up method.

Unlock Deck

Unlock for access to all 128 flashcards in this deck.

Unlock Deck

k this deck

42

County Company has two service departments, Maintenance and Personnel, as well as two production departments, Mixing and Finishing. Maintenance costs are allocated based on square footage, while personnel costs are allocated based on number of employees. The following information has been gathered for the current year:

If the direct method is used to allocate costs, the total cost of the Mixing Department after allocation would be

A) $121,714.

B) $41,143.

C) $20,571.

D) $60,000.

If the direct method is used to allocate costs, the total cost of the Mixing Department after allocation would be

A) $121,714.

B) $41,143.

C) $20,571.

D) $60,000.

Unlock Deck

Unlock for access to all 128 flashcards in this deck.

Unlock Deck

k this deck

43

City Company has two service departments, Maintenance and Personnel, as well as two production departments, Mixing and Finishing. Maintenance costs are allocated based on square footage while personnel costs are allocated based on number of employees. The following information has been gathered for the current year:

If the direct method is used to allocate costs, the total cost of the Finishing Department after allocation would be

A) $7,714.

B) $6,858.

C) $39,571.

D) $25,000.

If the direct method is used to allocate costs, the total cost of the Finishing Department after allocation would be

A) $7,714.

B) $6,858.

C) $39,571.

D) $25,000.

Unlock Deck

Unlock for access to all 128 flashcards in this deck.

Unlock Deck

k this deck

44

City Company has two service departments, Maintenance and Personnel, as well as two production departments, Mixing and Finishing. Maintenance costs are allocated based on square footage while personnel costs are allocated based on number of employees. The following information has been gathered for the current year:

If the step-down method of allocating costs is used, and the Personnel Department renders the greatest service, then the total amount of overhead that would be allocated from Maintenance to Mixing is

A) $4,500.

B) $8,357.

C) $9,000.

D) $11,143.

If the step-down method of allocating costs is used, and the Personnel Department renders the greatest service, then the total amount of overhead that would be allocated from Maintenance to Mixing is

A) $4,500.

B) $8,357.

C) $9,000.

D) $11,143.

Unlock Deck

Unlock for access to all 128 flashcards in this deck.

Unlock Deck

k this deck

45

County Company has two service departments, Maintenance and Personnel, as well as two production departments, Mixing and Finishing. Maintenance costs are allocated based on square footage, while personnel costs are allocated based on number of employees. The following information has been gathered for the current year:

If the step-down method is used to allocate costs, and the Maintenance Department renders the greatest service, then the total cost of the Mixing Department after allocation would be

A) $120,429.

B) $122,571.

C) $121,712.

D) $ 60,000.

If the step-down method is used to allocate costs, and the Maintenance Department renders the greatest service, then the total cost of the Mixing Department after allocation would be

A) $120,429.

B) $122,571.

C) $121,712.

D) $ 60,000.

Unlock Deck

Unlock for access to all 128 flashcards in this deck.

Unlock Deck

k this deck

46

In the step-down method, the last service department in the sequence is the one that renders the

A) most service to all other service departments.

B) most service to the least number of other service departments.

C) least service to the least number of other service departments.

D) least service to the most other service departments.

A) most service to all other service departments.

B) most service to the least number of other service departments.

C) least service to the least number of other service departments.

D) least service to the most other service departments.

Unlock Deck

Unlock for access to all 128 flashcards in this deck.

Unlock Deck

k this deck

47

City Company has two service departments, Maintenance and Personnel, as well as two production departments, Mixing and Finishing. Maintenance costs are allocated based on square footage while personnel costs are allocated based on number of employees. The following information has been gathered for the current year:

If the step-down method is used to allocate costs, and the Maintenance Department renders the greatest service, then the total cost of the Mixing Department after allocation would be

A) $30,107.

B) $30,642.

C) $30,428.

D) $15,000.

If the step-down method is used to allocate costs, and the Maintenance Department renders the greatest service, then the total cost of the Mixing Department after allocation would be

A) $30,107.

B) $30,642.

C) $30,428.

D) $15,000.

Unlock Deck

Unlock for access to all 128 flashcards in this deck.

Unlock Deck

k this deck

48

Which of the following is the least likely alternative to be used to allocate costs?

A) Use a different cost driver for each cost pool.

B) Allocate all costs evenly to all other departments.

C) Allocate some cost pools using cost drivers and leave other cost pools unallocated.

D) Use one cost driver to allocate all department costs.

A) Use a different cost driver for each cost pool.

B) Allocate all costs evenly to all other departments.

C) Allocate some cost pools using cost drivers and leave other cost pools unallocated.

D) Use one cost driver to allocate all department costs.

Unlock Deck

Unlock for access to all 128 flashcards in this deck.

Unlock Deck

k this deck

49

City Company has two service departments, Maintenance and Personnel, as well as two production departments, Mixing and Finishing. Maintenance costs are allocated based on square footage while personnel costs are allocated based on number of employees. The following information has been gathered for the current year:

If the direct method is used to allocate costs, the total cost of the Mixing Department after allocation would be

A) $30,429.

B) $10,286.

C) $5,143.

D) $15,000.

If the direct method is used to allocate costs, the total cost of the Mixing Department after allocation would be

A) $30,429.

B) $10,286.

C) $5,143.

D) $15,000.

Unlock Deck

Unlock for access to all 128 flashcards in this deck.

Unlock Deck

k this deck

50

County Company has two service departments, Maintenance and Personnel, as well as two production departments, Mixing and Finishing. Maintenance costs are allocated based on square footage, while personnel costs are allocated based on number of employees. The following information has been gathered for the current year:

If the step-down method is used to allocate costs, and the Personnel Department renders the greatest service, then the total cost of the Finishing Department after allocation would be

A) $100,000.

B) $158,288.

C) $159,571.

D) $157,429.

If the step-down method is used to allocate costs, and the Personnel Department renders the greatest service, then the total cost of the Finishing Department after allocation would be

A) $100,000.

B) $158,288.

C) $159,571.

D) $157,429.

Unlock Deck

Unlock for access to all 128 flashcards in this deck.

Unlock Deck

k this deck

51

County Company has two service departments, Maintenance and Personnel, as well as two production departments, Mixing and Finishing. Maintenance costs are allocated based on square footage, while personnel costs are allocated based on number of employees. The following information has been gathered for the current year:

If the step-down method of allocating costs is used, and the Personnel Department renders the greatest service, then the total amount of overhead that would be allocated from Maintenance to Mixing is

A) $18,000.

B) $33,428.

C) $36,000.

D) $44,571.

If the step-down method of allocating costs is used, and the Personnel Department renders the greatest service, then the total amount of overhead that would be allocated from Maintenance to Mixing is

A) $18,000.

B) $33,428.

C) $36,000.

D) $44,571.

Unlock Deck

Unlock for access to all 128 flashcards in this deck.

Unlock Deck

k this deck

52

The greatest virtue of the direct method is

A) its simplicity.

B) the lack of understandability by managers.

C) the recognition of reciprocal relationships between service departments.

D) its ability to allocate production department costs to service departments.

A) its simplicity.

B) the lack of understandability by managers.

C) the recognition of reciprocal relationships between service departments.

D) its ability to allocate production department costs to service departments.

Unlock Deck

Unlock for access to all 128 flashcards in this deck.

Unlock Deck

k this deck

53

County Company has two service departments, Maintenance and Personnel, as well as two production departments, Mixing and Finishing. Maintenance costs are allocated based on square footage, while personnel costs are allocated based on number of employees. The following information has been gathered for the current year:

If the step-down method of allocating costs is used, and the Personnel Department renders the greatest service, then the total amount of overhead that would be allocated from Maintenance to Finishing is

A) $24,000.

B) $33,429.

C) $27,000.

D) $32,568.

If the step-down method of allocating costs is used, and the Personnel Department renders the greatest service, then the total amount of overhead that would be allocated from Maintenance to Finishing is

A) $24,000.

B) $33,429.

C) $27,000.

D) $32,568.

Unlock Deck

Unlock for access to all 128 flashcards in this deck.

Unlock Deck

k this deck

54

County Company has two service departments, Maintenance and Personnel, as well as two production departments, Mixing and Finishing. Maintenance costs are allocated based on square footage, while personnel costs are allocated based on number of employees. The following information has been gathered for the current year:

If the direct method is used to allocate costs, the total cost of the Finishing Department after allocation would be

A) $30,857.

B) $27,429.

C) $158,286.

D) $100,000.

If the direct method is used to allocate costs, the total cost of the Finishing Department after allocation would be

A) $30,857.

B) $27,429.

C) $158,286.

D) $100,000.

Unlock Deck

Unlock for access to all 128 flashcards in this deck.

Unlock Deck

k this deck

55

City Company has two service departments, Maintenance and Personnel, as well as two production departments, Mixing and Finishing. Maintenance costs are allocated based on square footage while personnel costs are allocated based on number of employees. The following information has been gathered for the current year:

If the step-down method is used to allocate costs, and the Maintenance Department renders the greatest service, the total amount of overhead that would be allocated from Personnel to Mixing is

A) $5,143.

B) $6,107.

C) $6,000.

D) $9,000.

If the step-down method is used to allocate costs, and the Maintenance Department renders the greatest service, the total amount of overhead that would be allocated from Personnel to Mixing is

A) $5,143.

B) $6,107.

C) $6,000.

D) $9,000.

Unlock Deck

Unlock for access to all 128 flashcards in this deck.

Unlock Deck

k this deck

56

County Company has two service departments, Maintenance and Personnel, as well as two production departments, Mixing and Finishing. Maintenance costs are allocated based on square footage, while personnel costs are allocated based on number of employees. The following information has been gathered for the current year:

If the step-down method is used to allocate costs, and the Maintenance Department renders the greatest service, the total amount of overhead that would be allocated from Personnel to Mixing is

A) $20,572.

B) $24,429.

C) $24,000.

D) $36,000.

If the step-down method is used to allocate costs, and the Maintenance Department renders the greatest service, the total amount of overhead that would be allocated from Personnel to Mixing is

A) $20,572.

B) $24,429.

C) $24,000.

D) $36,000.

Unlock Deck

Unlock for access to all 128 flashcards in this deck.

Unlock Deck

k this deck

57

City Company has two service departments, Maintenance and Personnel, as well as two production departments, Mixing and Finishing. Maintenance costs are allocated based on square footage while personnel costs are allocated based on number of employees. The following information has been gathered for the current year:

If the step-down method is used to allocate costs, and the Maintenance Department renders the greatest service, then the total amount of overhead that would be allocated from Personnel to Finishing is

A) $6,107.

B) $4,500.

C) $8,143.

D) $6,750.

If the step-down method is used to allocate costs, and the Maintenance Department renders the greatest service, then the total amount of overhead that would be allocated from Personnel to Finishing is

A) $6,107.

B) $4,500.

C) $8,143.

D) $6,750.

Unlock Deck

Unlock for access to all 128 flashcards in this deck.

Unlock Deck

k this deck

58

City Company has two service departments, Maintenance and Personnel, as well as two production departments, Mixing and Finishing. Maintenance costs are allocated based on square footage while personnel costs are allocated based on number of employees. The following information has been gathered for the current year:

If the step-down method of allocating costs is used, and the Personnel Department renders the greatest service, then the total amount of overhead that would be allocated from Maintenance to Finishing is

A) $6,000.

B) $8,357.

C) $6,750.

D) $8,142.

If the step-down method of allocating costs is used, and the Personnel Department renders the greatest service, then the total amount of overhead that would be allocated from Maintenance to Finishing is

A) $6,000.

B) $8,357.

C) $6,750.

D) $8,142.

Unlock Deck

Unlock for access to all 128 flashcards in this deck.

Unlock Deck

k this deck

59

City Company has two service departments, Maintenance and Personnel, as well as two production departments, Mixing and Finishing. Maintenance costs are allocated based on square footage while personnel costs are allocated based on number of employees. The following information has been gathered for the current year:

If the step-down method is used to allocate costs, and the Personnel Department renders the greatest service, then the total cost of the Finishing Department after allocation would be

A) $25,000.

B) $39,572.

C) $39,892.

D) $39,357.

If the step-down method is used to allocate costs, and the Personnel Department renders the greatest service, then the total cost of the Finishing Department after allocation would be

A) $25,000.

B) $39,572.

C) $39,892.

D) $39,357.

Unlock Deck

Unlock for access to all 128 flashcards in this deck.

Unlock Deck

k this deck

60

County Company has two service departments, Maintenance and Personnel, as well as two production departments, Mixing and Finishing. Maintenance costs are allocated based on square footage, while personnel costs are allocated based on number of employees. The following information has been gathered for the current year:

If the step-down method is used to allocate costs, and the Maintenance Department renders the greatest service, then the total amount of overhead that would be allocated from Personnel to Finishing is

A) $24,429.

B) $18,000.

C) $32,571.

D) $27,000.

If the step-down method is used to allocate costs, and the Maintenance Department renders the greatest service, then the total amount of overhead that would be allocated from Personnel to Finishing is

A) $24,429.

B) $18,000.

C) $32,571.

D) $27,000.

Unlock Deck

Unlock for access to all 128 flashcards in this deck.

Unlock Deck

k this deck

61

Which of the following is NOT likely to be a cost driver?

A) Production orders

B) Material requisitions

C) Cost accountant's labour hours

D) Product inspections

A) Production orders

B) Material requisitions

C) Cost accountant's labour hours

D) Product inspections

Unlock Deck

Unlock for access to all 128 flashcards in this deck.

Unlock Deck

k this deck

62

Stanley Corp. manufactures two models of its roasting pans, a standard and a deluxe model. Three activities have been identified as cost drivers and the related costs pooled together to arrive at the following information:

If activity-based costing is used, then the product setup cost for the standard model would be

A) $12,857.

B) $17,143.

C) $1,071.

D) $1,866.

If activity-based costing is used, then the product setup cost for the standard model would be

A) $12,857.

B) $17,143.

C) $1,071.

D) $1,866.

Unlock Deck

Unlock for access to all 128 flashcards in this deck.

Unlock Deck

k this deck

63

Bare Company manufactures four products from a joint process. Joint costs for the year amounted to $140,000. The following data are also available:

Assuming the relative-sales-value method of allocating joint costs, the amount of joint costs allocated to product E would be

A) $40,600.00.

B) $64,444.40.

C) $58,000.00.

D) $35,280.00.

Assuming the relative-sales-value method of allocating joint costs, the amount of joint costs allocated to product E would be

A) $40,600.00.

B) $64,444.40.

C) $58,000.00.

D) $35,280.00.

Unlock Deck

Unlock for access to all 128 flashcards in this deck.

Unlock Deck

k this deck

64

Bare Company manufactures four products from a joint process. Joint costs for the year amounted to $140,000. The following data are also available:

Assuming the relative-sales-value method of allocating joint costs, the amount of joint costs allocated to product A would be

A) $19,600.

B) $37,692.

C) $29,120.

D) $16,640.

Assuming the relative-sales-value method of allocating joint costs, the amount of joint costs allocated to product A would be

A) $19,600.

B) $37,692.

C) $29,120.

D) $16,640.

Unlock Deck

Unlock for access to all 128 flashcards in this deck.

Unlock Deck

k this deck

65

Upjohn Company manufactures four products from a joint process. Joint costs for the year amounted to $350,000. The following data are also available:

Assuming the physical-units method of allocating joint costs, the amount of joint costs allocated to product Y would be

A) $172,536.

B) $99,400.

C) $122,500.

D) $24,648.

Assuming the physical-units method of allocating joint costs, the amount of joint costs allocated to product Y would be

A) $172,536.

B) $99,400.

C) $122,500.

D) $24,648.

Unlock Deck

Unlock for access to all 128 flashcards in this deck.

Unlock Deck

k this deck

66

Bare Company manufactures four products from a joint process. Joint costs for the year amounted to $140,000. The following data are also available:

Assuming the relative-sales-value method of allocating joint costs, the amount of joint costs allocated to product B would be

A) $35,840.00.

B) $48,124.80.

C) $30,800.00.

D) $20,160.00.

Assuming the relative-sales-value method of allocating joint costs, the amount of joint costs allocated to product B would be

A) $35,840.00.

B) $48,124.80.

C) $30,800.00.

D) $20,160.00.

Unlock Deck

Unlock for access to all 128 flashcards in this deck.

Unlock Deck

k this deck

67

Which of the following statements regarding by-products is FALSE?

A) A by-product is not individually identifiable until the split-off point.

B) A by-product is the same as a joint product.

C) By-products have relatively insignificant total sales value.

D) Only separable costs are allocated to by-products.

A) A by-product is not individually identifiable until the split-off point.

B) A by-product is the same as a joint product.

C) By-products have relatively insignificant total sales value.

D) Only separable costs are allocated to by-products.

Unlock Deck

Unlock for access to all 128 flashcards in this deck.

Unlock Deck

k this deck

68

Activity-based costing is also known as

A) transaction-based costing.

B) motivation-based costing.

C) objective-based costing.

D) variable-based costing.

A) transaction-based costing.

B) motivation-based costing.

C) objective-based costing.

D) variable-based costing.

Unlock Deck

Unlock for access to all 128 flashcards in this deck.

Unlock Deck

k this deck

69

Stanley Corp. manufactures two models of its roasting pans, a standard and a deluxe model. Three activities have been identified as cost drivers and the related costs pooled together to arrive at the following information:

If activity-based costing is used, then the total amount of overhead allocated to the standard model would be

A) $74,330.

B) $120,000.

C) $40,000.

D) $45,670.

If activity-based costing is used, then the total amount of overhead allocated to the standard model would be

A) $74,330.

B) $120,000.

C) $40,000.

D) $45,670.

Unlock Deck

Unlock for access to all 128 flashcards in this deck.

Unlock Deck

k this deck

70

Stanley Corp. manufactures two models of its roasting pans, a standard and a deluxe model. Three activities have been identified as cost drivers and the related costs pooled together to arrive at the following information:

If activity-based costing is used, then the total amount of overhead allocated to the deluxe model would be

A) $45,670.

B) $74,330.

C) $120,000.

D) $ 80,000.

If activity-based costing is used, then the total amount of overhead allocated to the deluxe model would be

A) $45,670.

B) $74,330.

C) $120,000.

D) $ 80,000.

Unlock Deck

Unlock for access to all 128 flashcards in this deck.

Unlock Deck

k this deck

71

Another term for cost application is

A) cost pool.

B) cost driver.

C) cost objective.

D) cost attribution.

A) cost pool.

B) cost driver.

C) cost objective.

D) cost attribution.

Unlock Deck

Unlock for access to all 128 flashcards in this deck.

Unlock Deck

k this deck

72

Which of the following is NOT likely to be an activity in an activity-based costing system?

A) Materials handling

B) Inspection

C) Accounting

D) Assembly

A) Materials handling

B) Inspection

C) Accounting

D) Assembly

Unlock Deck

Unlock for access to all 128 flashcards in this deck.

Unlock Deck

k this deck

73

Upjohn Company manufactures four products from a joint process. Joint costs for the year amounted to $350,000. The following data are also available:

Assuming the relative-sales-value method of allocating joint costs, the amount of joint costs allocated to product W would be

A) $89,600.

B) $120,312.

C) $77,000.

D) $50,400.

Assuming the relative-sales-value method of allocating joint costs, the amount of joint costs allocated to product W would be

A) $89,600.

B) $120,312.

C) $77,000.

D) $50,400.

Unlock Deck

Unlock for access to all 128 flashcards in this deck.

Unlock Deck

k this deck

74

Bare Company manufactures four products from a joint process. Joint costs for the year amounted to $140,000. The following data are also available:

Assuming the relative-sales-value method of allocating joint costs, the amount of joint costs allocated to product R would be

A) $49,000.00.

B) $39,760.00.

C) $69,014.40.

D) $22,720.00.

Assuming the relative-sales-value method of allocating joint costs, the amount of joint costs allocated to product R would be

A) $49,000.00.

B) $39,760.00.

C) $69,014.40.

D) $22,720.00.

Unlock Deck

Unlock for access to all 128 flashcards in this deck.

Unlock Deck

k this deck

75

One conventional way of allocating joint costs to products is the

A) relative sales value method.

B) direct method.

C) indirect method.

D) abc method.

A) relative sales value method.

B) direct method.

C) indirect method.

D) abc method.

Unlock Deck