Deck 6: Revaluations and Impairment Testing of Non-Current Assets

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

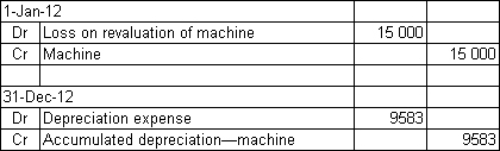

Mendelssons Ltd has a machine that has been revaluing over a number of years.The valuation as at 1 January 2012 is $130 000.The previous valuation was $145 000 and the accumulated depreciation is $40 000.The revised salvage value is $15 000 and the estimated useful life remaining is 12 years.The benefits from the machine are expected to be derived evenly over its life.In the previous year,the machine had been devalued by $15 000 and this amount written off to the income statement.What are the entries at 1 January 2012 to record the revaluation using the net method and at 31 December 2012 to record depreciation?

A)

B)

C)

D)

A)

B)

C)

D)

Question

Question

Question

Question

Question

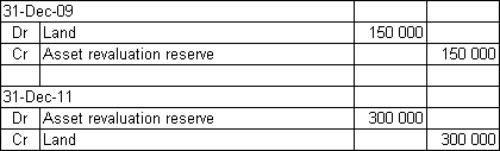

Pigeon Ltd purchased land for $750 000 6 years ago.It was revalued on 31 December 2009 to $600 000.A subsequent revaluation on 31 December 2011 found the market value to be $900 000 due to a change in council zoning for the area.What are the journal entries required to record the revaluations on 31 December 2009 and 31 December 2011?

A)

B)

C)

D)

A)

B)

C)

D)

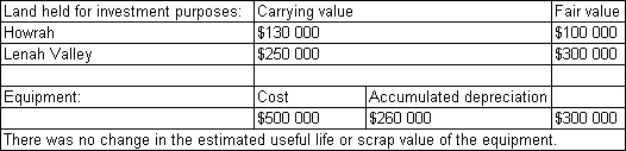

Question

Question

Question

Question

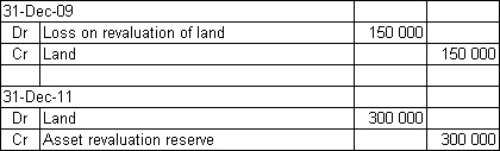

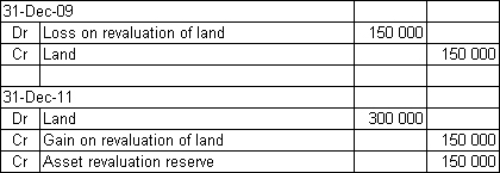

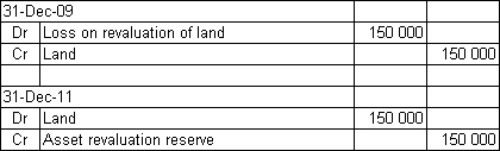

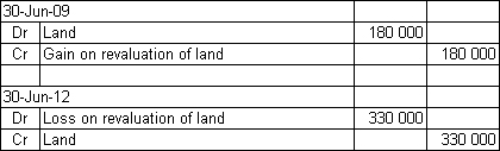

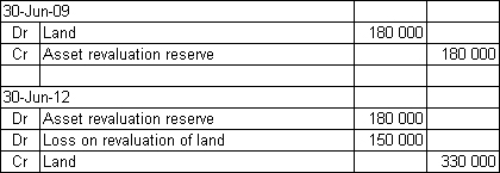

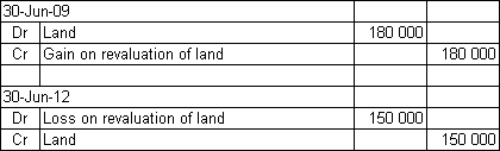

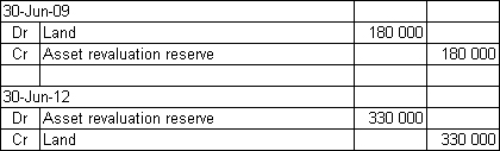

Seagull Marinas Ltd owns land that was purchased for $300 000 to be used as the future site of a boat shed.Due to the development of a resort in the vicinity,the land's fair market value had risen to $480 000 and was revalued on 30 June 2009.A revaluation undertaken on 30 June 2012 of $150,000 reflects the effect of the failure of resort development and local concerns about the protection of the nesting sites of endangered sea birds located near the land.What are the journal entries required to record the revaluations on 30 June 2009 and 30 June 2012?

A)

B)

C)

D)

A)

B)

C)

D)

Question

Burchells Ltd owns a machine that originally cost $36 000.It has been depreciated using the straight-line method for 3 years,giving an accumulated depreciation of $15 000 (the salvage value was estimated at $6000 and the useful life at 6 years).At the beginning of the current financial year its carrying value is therefore $21 000.It has been decided by the directors to revalue it to fair value,which is assessed to be $38 000.The salvage value and useful life are considered to be unchanged.What are the appropriate entries to record the revaluation using the net method and the depreciation expense for the current year (rounded to the nearest dollar)?

A)

B)

C)

D)

A)

B)

C)

D)

Question

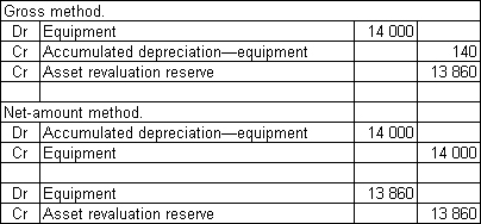

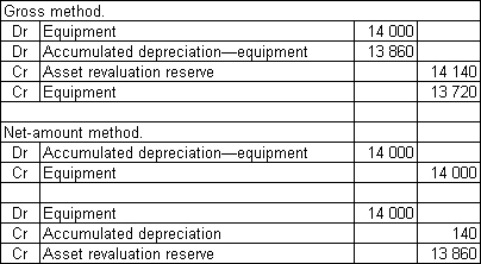

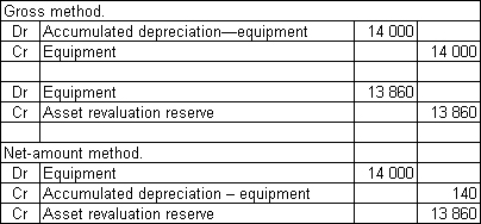

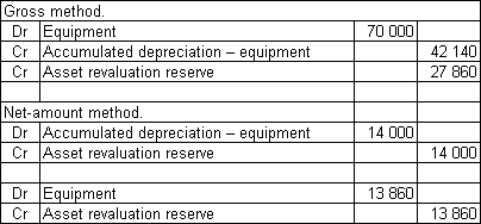

Smith & Jones Ltd owns equipment that was purchased for $56 000 and has accumulated depreciation of $14 000.The following market value information was gathered about the equipment

The equipment has a remaining useful life to the entity of 10 years.What are the appropriate journal entries to record the revaluation under the gross method and the net-amount method?

A)

B)

C)

D)

The equipment has a remaining useful life to the entity of 10 years.What are the appropriate journal entries to record the revaluation under the gross method and the net-amount method?

A)

B)

C)

D)

Question

Bears and Things acquired a toy-stuffing machine at a cost of $150 000 on 1 July 2009.The machine had a useful life of 10 years and a residual value of $30 000.The benefits from the machine are expected to be derived evenly over its life.On 1 July 2011 the asset's fair value is $110 000 and the salvage value and useful life are expected to be unchanged (that is,there is 8 years of remaining life).On 30 June 2009 the machine is sold for $60 000 cash.What are the journal entries required to record the depreciation for the year ended 30 June 2009 and the sale of the machine in accordance with AASB 116 if: (a)the revaluation is undertaken and (b)the revaluation is not recorded?

A)

B)

C)

D)

A)

B)

C)

D)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Stairway Ltd is undertaking its regular review of the fair value of its assets.It has discovered the following material changes

What are the journal entries required to record the revaluations in accordance with relevant accounting standards?

A)

B)

C)

D)

What are the journal entries required to record the revaluations in accordance with relevant accounting standards?

A)

B)

C)

D)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/76

Play

Full screen (f)

Deck 6: Revaluations and Impairment Testing of Non-Current Assets

1

Once an entity elects to value a class of assets using fair value it can switch back to cost basis measurement as long as there is justifiable reason.

True

2

Entities that elect to report plant and equipment at cost less accumulated depreciation are required to disclose a valuation of plant and equipment every 3 years in a note to the accounts.

False

3

Positive Accounting Theory suggests that the revalution model is income increasing because the credit is asset revaluation reserve.

False

4

AASB 138 will permit some intangible assets to be revalued upwards only when there is an 'active market' for the asset.

Unlock Deck

Unlock for access to all 76 flashcards in this deck.

Unlock Deck

k this deck

5

The process of discounting future cash flows in calculating the recoverable amount of an asset will result in a higher recoverable amount than if the cash flows are not discounted.

Unlock Deck

Unlock for access to all 76 flashcards in this deck.

Unlock Deck

k this deck

6

If an asset is subject to depreciation or amortization there is no longer a need to test the asset for impairment.

Unlock Deck

Unlock for access to all 76 flashcards in this deck.

Unlock Deck

k this deck

7

The concept of conservatism requires that if a class of non-current assets is revalued a revaluation decrement should be treated as an expense of the period,whereas a revaluation increment should be treated as an increase in a reserve.

Unlock Deck

Unlock for access to all 76 flashcards in this deck.

Unlock Deck

k this deck

8

AASB 116 requires that if it has been decided to revalue a class of non-current assets,the valuations must be kept up to date.

Unlock Deck

Unlock for access to all 76 flashcards in this deck.

Unlock Deck

k this deck

9

AASB 116 requires entities to review at least at the end of each annual reporting period to assess if the fair value of the non-current assets has changed.

Unlock Deck

Unlock for access to all 76 flashcards in this deck.

Unlock Deck

k this deck

10

The fair value of a non-current asset is defined in AASB 116 as the gross amount for which the asset can be sold when the entity is preparing to liquidate.

Unlock Deck

Unlock for access to all 76 flashcards in this deck.

Unlock Deck

k this deck

11

A sale of property plant and equipment requires the derecognition of the carrying amount of the asset and any cost of replacement part capitalised.

Unlock Deck

Unlock for access to all 76 flashcards in this deck.

Unlock Deck

k this deck

12

AASB 116 requires that revaluation increments and decrements must be offset recorded directly to equity and not be recorded as a gain or loss.

Unlock Deck

Unlock for access to all 76 flashcards in this deck.

Unlock Deck

k this deck

13

Australia is the only country that allows upward revaluations of non-current assets.

Unlock Deck

Unlock for access to all 76 flashcards in this deck.

Unlock Deck

k this deck

14

The revaluation model is a tool used by managers to reduce political costs.

Unlock Deck

Unlock for access to all 76 flashcards in this deck.

Unlock Deck

k this deck

15

If an asset's carrying amount is impaired,AASB 116 requires all assets in the same class to be revalued.

Unlock Deck

Unlock for access to all 76 flashcards in this deck.

Unlock Deck

k this deck

16

An entity that elects the revaluation model to measure a class of asset is permitted to revert back to the cost model provided that this will provide more relevant and reliable information.

Unlock Deck

Unlock for access to all 76 flashcards in this deck.

Unlock Deck

k this deck

17

AASB 116 requires that where the replacement cost of a non-current asset is less than its carrying value,the asset should be written down to its replacement cost.

Unlock Deck

Unlock for access to all 76 flashcards in this deck.

Unlock Deck

k this deck

18

Depreciation method used and depreciation rates are required to be disclosed for taxation purposes.

Unlock Deck

Unlock for access to all 76 flashcards in this deck.

Unlock Deck

k this deck

19

AASB 136 does not require the use of present values when determining the recoverable amount of an asset.

Unlock Deck

Unlock for access to all 76 flashcards in this deck.

Unlock Deck

k this deck

20

Recoverable amount is the amount expected to be recovered through the ongoing use and subsequent disposal of an asset.

Unlock Deck

Unlock for access to all 76 flashcards in this deck.

Unlock Deck

k this deck

21

Cars and Trucks Ltd owns an engine testing machine which was purchased for $120 000.After 3 years of use the machine had accumulated depreciation of $58 560 but was revalued to $80 000.Two years later the machine was sold for $60 000 and had accumulated depreciation at the time of sale of $36 800.What journal entries would be required to record the sale of the machine in accordance with AASB 116 requirements?

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 76 flashcards in this deck.

Unlock Deck

k this deck

22

By permitting some classes of assets to be valued at cost and others at fair value the AASB has:

A) removed any confusion regarding the total balance of non-current assets.

B) forced entities to accurately reflect their true financial position at any point in time.

C) created a situation where the total asset figure may be a combination of cost and fair value assessments, reducing its meaningfulness.

D) removed the opportunity for managers to act in their own self-interest as suggested by Positive Accounting Theory.

A) removed any confusion regarding the total balance of non-current assets.

B) forced entities to accurately reflect their true financial position at any point in time.

C) created a situation where the total asset figure may be a combination of cost and fair value assessments, reducing its meaningfulness.

D) removed the opportunity for managers to act in their own self-interest as suggested by Positive Accounting Theory.

Unlock Deck

Unlock for access to all 76 flashcards in this deck.

Unlock Deck

k this deck

23

Where an asset's carrying amount based on its cost is written down to its recoverable amount,AASB 136 specifies that:

A) Since this constitutes a revaluation of the asset, all assets in that class must be revalued.

B) The amount written down is to be treated as an adjustment to the asset revaluation reserve.

C) The write-down is not considered to be a revaluation and so the entity is not obliged to revalue that whole class of non-current assets.

D) To the extent that the asset was revalued upward in the past, the amount of the write-off may be transferred to the asset revaluation reserve and any remaining amount should be expensed.

A) Since this constitutes a revaluation of the asset, all assets in that class must be revalued.

B) The amount written down is to be treated as an adjustment to the asset revaluation reserve.

C) The write-down is not considered to be a revaluation and so the entity is not obliged to revalue that whole class of non-current assets.

D) To the extent that the asset was revalued upward in the past, the amount of the write-off may be transferred to the asset revaluation reserve and any remaining amount should be expensed.

Unlock Deck

Unlock for access to all 76 flashcards in this deck.

Unlock Deck

k this deck

24

A class of non-current assets as defined by AASB 116 is a category of non-current assets that:

A) were all purchased at the same time by the reporting entity.

B) all have a similar nature or function in the operations of the entity.

C) are disclosed as a single item without supplementary dissection in the financial report.

D) all have a similar nature or function in the operations of the entity, and are disclosed as a single item without supplementary dissection in the financial report.

A) were all purchased at the same time by the reporting entity.

B) all have a similar nature or function in the operations of the entity.

C) are disclosed as a single item without supplementary dissection in the financial report.

D) all have a similar nature or function in the operations of the entity, and are disclosed as a single item without supplementary dissection in the financial report.

Unlock Deck

Unlock for access to all 76 flashcards in this deck.

Unlock Deck

k this deck

25

Peters Ltd has a machine that originally cost $20 000 and has accumulated depreciation of $5000.Its remaining life is assessed to be 5 years with no salvage value.The directors of Peters Ltd decide on 1 July 2003 to revalue the machine.They are unable to find market information on a machine in a similar state to theirs,so the market value of a new machine of the same type,$30 000,is used as a basis.What is/are the appropriate journal entry(ies)using the gross method to record the revaluation?

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 76 flashcards in this deck.

Unlock Deck

k this deck

26

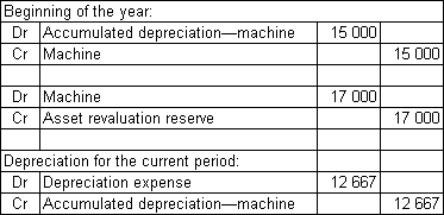

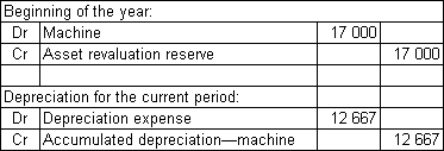

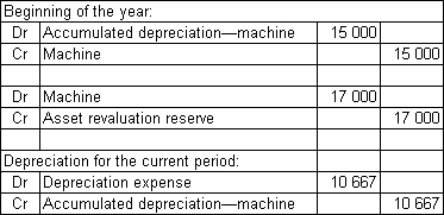

Mendelssons Ltd has a machine that has been revaluing over a number of years.The valuation as at 1 January 2012 is $130 000.The previous valuation was $145 000 and the accumulated depreciation is $40 000.The revised salvage value is $15 000 and the estimated useful life remaining is 12 years.The benefits from the machine are expected to be derived evenly over its life.In the previous year,the machine had been devalued by $15 000 and this amount written off to the income statement.What are the entries at 1 January 2012 to record the revaluation using the net method and at 31 December 2012 to record depreciation?

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 76 flashcards in this deck.

Unlock Deck

k this deck

27

A machine purchased by White Ltd had a cost of $670 000 and an accumulated depreciation balance of $120 000 at 30 June 2012.Its fair value is assessed at this time,with its first revaluation as $450 000.What is/are the appropriate journal entry(ies)to record the revaluation using the net method?

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 76 flashcards in this deck.

Unlock Deck

k this deck

28

Manchester Ltd has a building that originally cost $850 000 and has accumulated depreciation of $120 000 as at 30 June 2012.It is decided on 1 July 2012 that the building should be revalued to $820 000.What are the appropriate entries to record the revaluation using the net method?

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 76 flashcards in this deck.

Unlock Deck

k this deck

29

Purple Co Ltd purchased an item of land 3 years ago at a cost of $700 000.Two years ago the recoverable value of the land was considered to be $550 000.In the current period the land is revalued and the fair value is now $750 000.What is the treatment of the change in value in each of the periods?

A) Two years ago: a loss of $150 000 is recognised. The current period: a gain of $150 000 and an increase in the asset revaluation reserve of $50 000 is recognised.

B) Two years ago: $150 000 is debited to the asset revaluation reserve. The current period: $200 000 is credited to the asset revaluation reserve.

C) Two years ago: $150 000 is expensed in the period. The current period: $200 000 is transferred to the asset revaluation reserve.

D) Two years ago: $150 000 is written off to the asset revaluation reserve. The current period: $200 000 revenue is recognised.

A) Two years ago: a loss of $150 000 is recognised. The current period: a gain of $150 000 and an increase in the asset revaluation reserve of $50 000 is recognised.

B) Two years ago: $150 000 is debited to the asset revaluation reserve. The current period: $200 000 is credited to the asset revaluation reserve.

C) Two years ago: $150 000 is expensed in the period. The current period: $200 000 is transferred to the asset revaluation reserve.

D) Two years ago: $150 000 is written off to the asset revaluation reserve. The current period: $200 000 revenue is recognised.

Unlock Deck

Unlock for access to all 76 flashcards in this deck.

Unlock Deck

k this deck

30

AASB 116 provides guidance on fair values which states:

A) Where an active and liquid market exists for an asset, the market price represents evidence of the asset's fair value.

B) Fair values are determined on the basis that an entity is a going concern.

C) Where no market exists the price should be based on the amount for which an asset could be exchanged between knowledgeable, willing parties in an arm's length transaction.

D) All of the given answers are correct.

A) Where an active and liquid market exists for an asset, the market price represents evidence of the asset's fair value.

B) Fair values are determined on the basis that an entity is a going concern.

C) Where no market exists the price should be based on the amount for which an asset could be exchanged between knowledgeable, willing parties in an arm's length transaction.

D) All of the given answers are correct.

Unlock Deck

Unlock for access to all 76 flashcards in this deck.

Unlock Deck

k this deck

31

Pigeon Ltd purchased land for $750 000 6 years ago.It was revalued on 31 December 2009 to $600 000.A subsequent revaluation on 31 December 2011 found the market value to be $900 000 due to a change in council zoning for the area.What are the journal entries required to record the revaluations on 31 December 2009 and 31 December 2011?

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 76 flashcards in this deck.

Unlock Deck

k this deck

32

Once a class of non-current assets has been revalued,AASB 116 requires that:

A) Directors continue to revalue the class of assets on an ad hoc basis.

B) Revaluations must be undertaken regularly enough to ensure that the carrying amount of each asset in the class of assets does not differ materially from its fair value at reporting date.

C) All assets in the class must be revalued every 3 years.

D) Revaluations must be undertaken regularly enough to ensure that the carrying amount of the class of assets does not differ from its fair value at reporting date.

A) Directors continue to revalue the class of assets on an ad hoc basis.

B) Revaluations must be undertaken regularly enough to ensure that the carrying amount of each asset in the class of assets does not differ materially from its fair value at reporting date.

C) All assets in the class must be revalued every 3 years.

D) Revaluations must be undertaken regularly enough to ensure that the carrying amount of the class of assets does not differ from its fair value at reporting date.

Unlock Deck

Unlock for access to all 76 flashcards in this deck.

Unlock Deck

k this deck

33

Where the value of revalued non-current assets does not change frequently and is not material,AASB 116 suggests that revaluations:

A) may be undertaken when next convenient.

B) should be undertaken every 3 to 5 years.

C) may be undertaken for individual assets within a class.

D) should be suspended and the entity should switch back to cost.

A) may be undertaken when next convenient.

B) should be undertaken every 3 to 5 years.

C) may be undertaken for individual assets within a class.

D) should be suspended and the entity should switch back to cost.

Unlock Deck

Unlock for access to all 76 flashcards in this deck.

Unlock Deck

k this deck

34

Revaluations increments are often a source of discussion because:

A) Historical-cost accounting has traditionally stated that unrealised holding gains should generally be treated as income.

B) A transaction with an external party is always required to recognise income.

C) Revaluation increments can be used to offset previous decrements across all asset classes.

D) This model loosens debt covenant restrictions.

A) Historical-cost accounting has traditionally stated that unrealised holding gains should generally be treated as income.

B) A transaction with an external party is always required to recognise income.

C) Revaluation increments can be used to offset previous decrements across all asset classes.

D) This model loosens debt covenant restrictions.

Unlock Deck

Unlock for access to all 76 flashcards in this deck.

Unlock Deck

k this deck

35

Seagull Marinas Ltd owns land that was purchased for $300 000 to be used as the future site of a boat shed.Due to the development of a resort in the vicinity,the land's fair market value had risen to $480 000 and was revalued on 30 June 2009.A revaluation undertaken on 30 June 2012 of $150,000 reflects the effect of the failure of resort development and local concerns about the protection of the nesting sites of endangered sea birds located near the land.What are the journal entries required to record the revaluations on 30 June 2009 and 30 June 2012?

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 76 flashcards in this deck.

Unlock Deck

k this deck

36

Burchells Ltd owns a machine that originally cost $36 000.It has been depreciated using the straight-line method for 3 years,giving an accumulated depreciation of $15 000 (the salvage value was estimated at $6000 and the useful life at 6 years).At the beginning of the current financial year its carrying value is therefore $21 000.It has been decided by the directors to revalue it to fair value,which is assessed to be $38 000.The salvage value and useful life are considered to be unchanged.What are the appropriate entries to record the revaluation using the net method and the depreciation expense for the current year (rounded to the nearest dollar)?

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 76 flashcards in this deck.

Unlock Deck

k this deck

37

Smith & Jones Ltd owns equipment that was purchased for $56 000 and has accumulated depreciation of $14 000.The following market value information was gathered about the equipment

The equipment has a remaining useful life to the entity of 10 years.What are the appropriate journal entries to record the revaluation under the gross method and the net-amount method?

A)

B)

C)

D)

The equipment has a remaining useful life to the entity of 10 years.What are the appropriate journal entries to record the revaluation under the gross method and the net-amount method?

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 76 flashcards in this deck.

Unlock Deck

k this deck

38

Bears and Things acquired a toy-stuffing machine at a cost of $150 000 on 1 July 2009.The machine had a useful life of 10 years and a residual value of $30 000.The benefits from the machine are expected to be derived evenly over its life.On 1 July 2011 the asset's fair value is $110 000 and the salvage value and useful life are expected to be unchanged (that is,there is 8 years of remaining life).On 30 June 2009 the machine is sold for $60 000 cash.What are the journal entries required to record the depreciation for the year ended 30 June 2009 and the sale of the machine in accordance with AASB 116 if: (a)the revaluation is undertaken and (b)the revaluation is not recorded?

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 76 flashcards in this deck.

Unlock Deck

k this deck

39

Hendersons Ltd has just begun to revalue its plant and equipment.The following information about the items included in this class of non-current assets shows their carrying value,and most recent revaluation.

What is/are the appropriate journal entry(ies)to record the revaluations using the net method?

A)

B)

C)

D)

What is/are the appropriate journal entry(ies)to record the revaluations using the net method?

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 76 flashcards in this deck.

Unlock Deck

k this deck

40

AASB 136 requires that:

A) If a non-current asset is revalued, the revalued amount may be less than the recoverable amount.

B) If a non-current asset is revalued, it must be revalued to the lower of current replacement cost or net realisable value.

C) If a non-current asset is revalued, it must be revalued to the amount for which an asset could be exchanged between knowledgeable, willing parties in an arm's length transaction.

D) If a non-current asset is revalued, it must be revalued to the amount for which the asset could be realised in an active market in a liquidation sale.

A) If a non-current asset is revalued, the revalued amount may be less than the recoverable amount.

B) If a non-current asset is revalued, it must be revalued to the lower of current replacement cost or net realisable value.

C) If a non-current asset is revalued, it must be revalued to the amount for which an asset could be exchanged between knowledgeable, willing parties in an arm's length transaction.

D) If a non-current asset is revalued, it must be revalued to the amount for which the asset could be realised in an active market in a liquidation sale.

Unlock Deck

Unlock for access to all 76 flashcards in this deck.

Unlock Deck

k this deck

41

Brown,Izan and Loh (1992)found that revaluations are more likely to take place:

A) in small firms with low value assets that wished to borrow more.

B) in industries that are strike prone.

C) in entities that are highly geared.

D) in industries that are strike prone and in entities that are highly geared.

A) in small firms with low value assets that wished to borrow more.

B) in industries that are strike prone.

C) in entities that are highly geared.

D) in industries that are strike prone and in entities that are highly geared.

Unlock Deck

Unlock for access to all 76 flashcards in this deck.

Unlock Deck

k this deck

42

AASB 116 permits which of the following with respect to measurement of non-current assets using revaluation model?

A) Net revaluation decrements for each class of asset are initially debited to asset revaluation reserve.

B) Use of cost model to measure other assets in the same class.

C) All increments arising from revaluation are credited to asset revaluation reserve.

D) None of the given answers are correct.

A) Net revaluation decrements for each class of asset are initially debited to asset revaluation reserve.

B) Use of cost model to measure other assets in the same class.

C) All increments arising from revaluation are credited to asset revaluation reserve.

D) None of the given answers are correct.

Unlock Deck

Unlock for access to all 76 flashcards in this deck.

Unlock Deck

k this deck

43

AASB 116 prescribes that,if assets within the same class are revalued and some assets increased in value while others decreased in value:

A) the net decrement for the class of asset should be recognised as loss in the income statement.

B) the net increment for the class of asset should be credited to revaluation reserve.

C) the total increment for all assets in the same class that increased in value should be credited to revaluation reserve and total decrement for all assets in the same class of asset should be recognised as loss in the income statement.

D) All of the given answers are correct.

A) the net decrement for the class of asset should be recognised as loss in the income statement.

B) the net increment for the class of asset should be credited to revaluation reserve.

C) the total increment for all assets in the same class that increased in value should be credited to revaluation reserve and total decrement for all assets in the same class of asset should be recognised as loss in the income statement.

D) All of the given answers are correct.

Unlock Deck

Unlock for access to all 76 flashcards in this deck.

Unlock Deck

k this deck

44

Which of the following statement is true of accumulated depreciation?

A) It is the difference between acquisition costs and residual value.

B) It is the difference between acquisition costs and revalued amount.

C) It is initially derecognised on first time revaluations.

D) It is restated proportionately to the carrying amount and the revalued amount of the asset.

A) It is the difference between acquisition costs and residual value.

B) It is the difference between acquisition costs and revalued amount.

C) It is initially derecognised on first time revaluations.

D) It is restated proportionately to the carrying amount and the revalued amount of the asset.

Unlock Deck

Unlock for access to all 76 flashcards in this deck.

Unlock Deck

k this deck

45

When an entity adopts the valuation model to account for its property,plant and equipment,which of the following statement(s)is/are correct?

A) If an item is revalued, all assets in the same class shall be revalued.

B) If an asset's carrying amount is decreased as a result of a revaluation, the decrease is always recognised in profit and loss.

C) If an asset's carrying amount is increased as a result of a revaluation, the increase is always credited directly to equity.

D) All of the given answers.

A) If an item is revalued, all assets in the same class shall be revalued.

B) If an asset's carrying amount is decreased as a result of a revaluation, the decrease is always recognised in profit and loss.

C) If an asset's carrying amount is increased as a result of a revaluation, the increase is always credited directly to equity.

D) All of the given answers.

Unlock Deck

Unlock for access to all 76 flashcards in this deck.

Unlock Deck

k this deck

46

Under AASB 116 when an asset is revalued and the net method is used,accumulated depreciation:

A) must be written back to profit.

B) must be closed off to the equity account.

C) should be eliminated against the gross carrying amount of the asset before revaluation.

D) should be increased by the same proportion as the gross carrying amount of the asset so that the carrying amount of the asset after revaluation equals the revalued amount.

A) must be written back to profit.

B) must be closed off to the equity account.

C) should be eliminated against the gross carrying amount of the asset before revaluation.

D) should be increased by the same proportion as the gross carrying amount of the asset so that the carrying amount of the asset after revaluation equals the revalued amount.

Unlock Deck

Unlock for access to all 76 flashcards in this deck.

Unlock Deck

k this deck

47

Which of the following statements is true of revaluation model in AASB 116?

A) It is the preferred model of managers with bonus based payments.

B) It is required under AASB 116.

C) Once adopted the firm can no longer revert back to cost model.

D) None of the statements are correct.

A) It is the preferred model of managers with bonus based payments.

B) It is required under AASB 116.

C) Once adopted the firm can no longer revert back to cost model.

D) None of the statements are correct.

Unlock Deck

Unlock for access to all 76 flashcards in this deck.

Unlock Deck

k this deck

48

Stairway Ltd is undertaking its regular review of the fair value of its assets.It has discovered the following material changes

What are the journal entries required to record the revaluations in accordance with relevant accounting standards?

A)

B)

C)

D)

What are the journal entries required to record the revaluations in accordance with relevant accounting standards?

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 76 flashcards in this deck.

Unlock Deck

k this deck

49

Chopin Ltd has a debt contract and is close to violating the return on equity ratio as stipulated in the debt agreement.What is the most appropriate action to take?

A) Negotiate a loan to increase cash balance.

B) Accelerate collection of receivables.

C) Negotiate to prepay long-term debt.

D) Revalue a class of asset.

A) Negotiate a loan to increase cash balance.

B) Accelerate collection of receivables.

C) Negotiate to prepay long-term debt.

D) Revalue a class of asset.

Unlock Deck

Unlock for access to all 76 flashcards in this deck.

Unlock Deck

k this deck

50

Where management's bonuses are tied to profit-based performance measures management may have an incentive not to revalue assets because:

A) When revaluing assets, the value of the asset base increases, consequently the return on assets will fall.

B) A revaluation may result in a decrease in the value of the asset base.

C) A revaluation that increases the value of the asset base will increase profit measures.

D) When revaluing assets, the value of the asset base increases, consequently the debt to equity ratio will fall.

A) When revaluing assets, the value of the asset base increases, consequently the return on assets will fall.

B) A revaluation may result in a decrease in the value of the asset base.

C) A revaluation that increases the value of the asset base will increase profit measures.

D) When revaluing assets, the value of the asset base increases, consequently the debt to equity ratio will fall.

Unlock Deck

Unlock for access to all 76 flashcards in this deck.

Unlock Deck

k this deck

51

Staples Ltd has invested in two parcels of land that are treated as belonging to the same class of assets.The first parcel of land was purchased for $500 000 and has been valued this period at $650 000.The second parcel of land has a carrying value of $340 000 and has been valued this period at $100 000.What is the appropriate journal entry to record the revaluations?

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 76 flashcards in this deck.

Unlock Deck

k this deck

52

When an item of property,plant and equipment is derecognised the treatment of any asset revaluation reserve that relates to an asset include:

A) debiting the asset revaluation reserve in the journal entry to record the profit or loss on sale of the asset.

B) transferring the relevant amount out of the asset revaluation reserve and showing it as revenue in the income statement.

C) transferring the asset revaluation reserve to retained earnings.

D) writing off the amount out of the asset revaluation reserve against the remaining assets in the class of assets to which the asset that was sold belonged.

A) debiting the asset revaluation reserve in the journal entry to record the profit or loss on sale of the asset.

B) transferring the relevant amount out of the asset revaluation reserve and showing it as revenue in the income statement.

C) transferring the asset revaluation reserve to retained earnings.

D) writing off the amount out of the asset revaluation reserve against the remaining assets in the class of assets to which the asset that was sold belonged.

Unlock Deck

Unlock for access to all 76 flashcards in this deck.

Unlock Deck

k this deck

53

Palm Beach Ltd has elected to adopt the allowed alternative treatment to account for some of its property,plant and equipment.The information available for the class of assets the entity wishes to covert to revaluation model follows.

Which of the following statements is correct if Palm Beach Ltd is to comply with AASB 116?

A) When office equipment is revalued, net profit will increase $10 000.

B) When machinery is revalued, net profit will increase by $2500.

C) When motor vehicles are revalued, net profit will decrease by $16 000.

D) When all assets are revalued, net profit will increase by $8500.

Which of the following statements is correct if Palm Beach Ltd is to comply with AASB 116?

A) When office equipment is revalued, net profit will increase $10 000.

B) When machinery is revalued, net profit will increase by $2500.

C) When motor vehicles are revalued, net profit will decrease by $16 000.

D) When all assets are revalued, net profit will increase by $8500.

Unlock Deck

Unlock for access to all 76 flashcards in this deck.

Unlock Deck

k this deck

54

Research using the Positive Accounting Theory approach investigated public trust deeds and found that in relation to revaluations they:

A) allowed revaluations but imposed very low debt/asset limits.

B) specified which assets may be revalued and who may conduct the revaluations.

C) generally did not permit revaluations.

D) allowed revaluations but specified the period between revaluations as being no longer than 2 years.

A) allowed revaluations but imposed very low debt/asset limits.

B) specified which assets may be revalued and who may conduct the revaluations.

C) generally did not permit revaluations.

D) allowed revaluations but specified the period between revaluations as being no longer than 2 years.

Unlock Deck

Unlock for access to all 76 flashcards in this deck.

Unlock Deck

k this deck

55

Casey Co Ltd is assessing the recoverable amount of some land it invested in 5 years ago at a cost $600 000.Management has sought independent valuation advice that indicates that the land may be sold in 6 years' time for $800 000.Since the land is not generating any cash flows,this is its undiscounted recoverable amount.The appropriate discount rate is estimated to be 7%.The present value of $1 received in 6 years' time at a discount rate of 7% is 0.6663.What is the effect of using the discount rate on the need to write down the value of the asset?

A) Since the recoverable amount of $800 000 is greater than the cost of $600 000, there is no need to write down the asset.

B) The undiscounted amount may not be used according to AASB 136 so the asset should be written down by $66 960.

C) There is no need to write down the asset in either case since the undiscounted amount is greater than the cost and the discounted amount of $900 438 is also greater than the cost.

D) The undiscounted amount may be used in this case as the asset will not be continually in use, and therefore 'value in use' cannot be calculated. As this amount is higher than the cost there is no need to write down the asset.

A) Since the recoverable amount of $800 000 is greater than the cost of $600 000, there is no need to write down the asset.

B) The undiscounted amount may not be used according to AASB 136 so the asset should be written down by $66 960.

C) There is no need to write down the asset in either case since the undiscounted amount is greater than the cost and the discounted amount of $900 438 is also greater than the cost.

D) The undiscounted amount may be used in this case as the asset will not be continually in use, and therefore 'value in use' cannot be calculated. As this amount is higher than the cost there is no need to write down the asset.

Unlock Deck

Unlock for access to all 76 flashcards in this deck.

Unlock Deck

k this deck

56

The costs associated with revaluing assets include:

A) additional audit fees.

B) fees charged by the valuer.

C) opportunity costs associated with the directors' time to review the valuations.

D) all of the given answers.

A) additional audit fees.

B) fees charged by the valuer.

C) opportunity costs associated with the directors' time to review the valuations.

D) all of the given answers.

Unlock Deck

Unlock for access to all 76 flashcards in this deck.

Unlock Deck

k this deck

57

On disposal of an asset a gain or loss is the difference between the proceeds from sale and:

A) the cost of an asset.

B) residual value of the asset.

C) carrying amount of the asset.

D) revalued amount of the asset.

A) the cost of an asset.

B) residual value of the asset.

C) carrying amount of the asset.

D) revalued amount of the asset.

Unlock Deck

Unlock for access to all 76 flashcards in this deck.

Unlock Deck

k this deck

58

Where there are debt covenants in place to restrict the level of debt to assets then management may be motivated to:

A) avoid revaluations because an increase in asset values increases depreciation and therefore reduces profit.

B) undertake revaluations where the expectation is that asset values have fallen.

C) avoid revaluations because of their effect on the cash flows of the business and therefore its ability to pay interest under the debt covenant.

D) undertake revaluations where the expectation is that asset values are rising.

A) avoid revaluations because an increase in asset values increases depreciation and therefore reduces profit.

B) undertake revaluations where the expectation is that asset values have fallen.

C) avoid revaluations because of their effect on the cash flows of the business and therefore its ability to pay interest under the debt covenant.

D) undertake revaluations where the expectation is that asset values are rising.

Unlock Deck

Unlock for access to all 76 flashcards in this deck.

Unlock Deck

k this deck

59

Under AASB 116 when an asset is revalued and the gross method is used,accumulated depreciation:

A) must be written back to profit.

B) must be closed off to reduce the asset account.

C) is ignored during revaluation as it has not effect on carrying amount.

D) should be increased by the same proportion as the gross carrying amount of the asset so that the carrying amount of the asset after revaluation equals the revalued amount.

A) must be written back to profit.

B) must be closed off to reduce the asset account.

C) is ignored during revaluation as it has not effect on carrying amount.

D) should be increased by the same proportion as the gross carrying amount of the asset so that the carrying amount of the asset after revaluation equals the revalued amount.

Unlock Deck

Unlock for access to all 76 flashcards in this deck.

Unlock Deck

k this deck

60

According to Positive Accounting Theory,the size of the entity may have an impact on management's decision to revalue because of management's motivation to reduce political costs.There is more than one possible view regarding the effect of revaluation on political visibility,including which of the following?

A) Since revaluations may increase the variability of asset size, they will increase political costs.

B) Where increases in asset size are expected to result from revaluations, the increase in the size of the entity may reduce political costs.

C) Where revaluations increase the size of the asset base, the return on assets will be lower and this will potentially lower political costs.

D) Where revaluations result in an increase in the asset base, depreciation expense will increase and lead to greater political costs.

A) Since revaluations may increase the variability of asset size, they will increase political costs.

B) Where increases in asset size are expected to result from revaluations, the increase in the size of the entity may reduce political costs.

C) Where revaluations increase the size of the asset base, the return on assets will be lower and this will potentially lower political costs.

D) Where revaluations result in an increase in the asset base, depreciation expense will increase and lead to greater political costs.

Unlock Deck

Unlock for access to all 76 flashcards in this deck.

Unlock Deck

k this deck

61

Explain the process that an entity must undertake when converting from the cost model to the valuation model basis of accounting for its non-current assets.

Unlock Deck

Unlock for access to all 76 flashcards in this deck.

Unlock Deck

k this deck

62

Explain why discounting future cash flows will have direct implications for the calculated value of the recoverable amount.

Unlock Deck

Unlock for access to all 76 flashcards in this deck.

Unlock Deck

k this deck

63

A firm that has both compensation and debt contracts will prefer the revaluation model over the cost model to measure its property,plant and equipment.Discuss.

Unlock Deck

Unlock for access to all 76 flashcards in this deck.

Unlock Deck

k this deck

64

Compare the accounting treatment for investment properties with that of property,plant and equipment using the valuation model.

Unlock Deck

Unlock for access to all 76 flashcards in this deck.

Unlock Deck

k this deck

65

Discuss the potential usefulness of the gross method in revaluation of non-current assets.

Unlock Deck

Unlock for access to all 76 flashcards in this deck.

Unlock Deck

k this deck

66

Brahms Ltd acquired a property of land and building for $1.5 million.Management estimates the value of land to be 40% of cost.The building is estimated to have a useful life of 50 years.After 25 years,the property was revalued at 1.2 million.It is expected that the life of the building will remain the same and salvage value is expected to be $100 000.What is the revaluation gain(loss)for the building and the depreciation expense one year after revaluation?

A) $120 000; $24 800

B) ($120 000); $28 800

C) $220 000; $24 800

D) ($220 000); $28 800

A) $120 000; $24 800

B) ($120 000); $28 800

C) $220 000; $24 800

D) ($220 000); $28 800

Unlock Deck

Unlock for access to all 76 flashcards in this deck.

Unlock Deck

k this deck

67

Mozart Ltd acquired a building for $1.5 million.Management estimates the value of land to be 40% of cost.The building is estimated to have a useful life of 50 years.After 25 years,the property's fair value is estimated at 1.2 million.It is expected that the life of the building will remain the same and salvage value is expected to be $100 000.Which of the following statements is correct at end of year 25 with respect to the revaluation?

A) Net profit will increase by $100 000.

B) Net profit will increase by $120 000.

C) Net profit will decrease by $220 000.

D) Net profit is unaffected as the credit is through the asset revaluation reserve.

A) Net profit will increase by $100 000.

B) Net profit will increase by $120 000.

C) Net profit will decrease by $220 000.

D) Net profit is unaffected as the credit is through the asset revaluation reserve.

Unlock Deck

Unlock for access to all 76 flashcards in this deck.

Unlock Deck

k this deck

68

If an asset's carrying amount is increased due to an initial revaluation that increase shall be recognised in:

A) other comprehensive income.

B) the profit and loss.

C) in the disclosures.

D) None of the given answers are correct.

A) other comprehensive income.

B) the profit and loss.

C) in the disclosures.

D) None of the given answers are correct.

Unlock Deck

Unlock for access to all 76 flashcards in this deck.

Unlock Deck

k this deck

69

Differentiate depreciation expense from impairment loss.

Unlock Deck

Unlock for access to all 76 flashcards in this deck.

Unlock Deck

k this deck

70

What is the rationale for revaluing the entire class of assets when an item of property,plant and equipment is revalued?

Unlock Deck

Unlock for access to all 76 flashcards in this deck.

Unlock Deck

k this deck

71

Discuss the process for the reversal of revaluation decrements and increments.

Unlock Deck

Unlock for access to all 76 flashcards in this deck.

Unlock Deck

k this deck

72

Which of the following statements is a valid reason to select cost model over the revaluation model?

A) to report relevant information

B) to reduce taxes

C) to properly match costs with expenses

D) to simplify the measurement accounting policy

A) to report relevant information

B) to reduce taxes

C) to properly match costs with expenses

D) to simplify the measurement accounting policy

Unlock Deck

Unlock for access to all 76 flashcards in this deck.

Unlock Deck

k this deck

73

According to AASB 136 the recoverable amount of an asset or cash-generating unit is the:

A) lower of its fair value less costs of disposal and its value in use.

B) lower of its fair value plus costs of disposal and its value in use.

C) higher of its fair value less costs of disposal and its value in use.

D) higher of its fair value plus costs of disposal and its value in use.

A) lower of its fair value less costs of disposal and its value in use.

B) lower of its fair value plus costs of disposal and its value in use.

C) higher of its fair value less costs of disposal and its value in use.

D) higher of its fair value plus costs of disposal and its value in use.

Unlock Deck

Unlock for access to all 76 flashcards in this deck.

Unlock Deck

k this deck

74

AASB 136 defines the smallest identifiable group of assets that generates cash inflows that are largely independent of the cash inflows from other assets or groups of assets as a:

A) class of assets.

B) asset portfolio.

C) value in use asset group.

D) cash-generating unit.

A) class of assets.

B) asset portfolio.

C) value in use asset group.

D) cash-generating unit.

Unlock Deck

Unlock for access to all 76 flashcards in this deck.

Unlock Deck

k this deck

75

Explain why the accounting treatment from increments and decrements are not symmetrical with respect to the revaluation of property,plant and equipment.

Unlock Deck

Unlock for access to all 76 flashcards in this deck.

Unlock Deck

k this deck

76

An investment property is considered to generate cash flows that are:

A) dependent on the other assets of the entity.

B) designed to reduce taxes.

C) largely independent of the other assets of the entity.

D) all of the given answers.

A) dependent on the other assets of the entity.

B) designed to reduce taxes.

C) largely independent of the other assets of the entity.

D) all of the given answers.

Unlock Deck

Unlock for access to all 76 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 76 flashcards in this deck.