Deck 27: Accounting for Group Structures

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

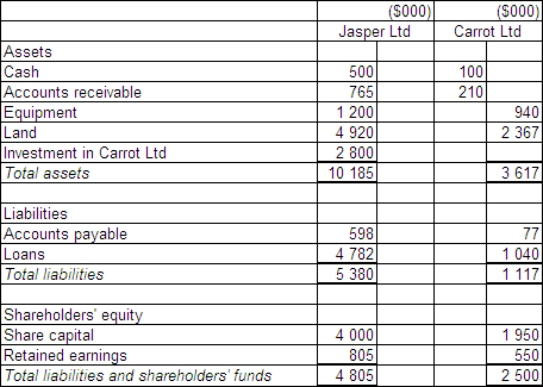

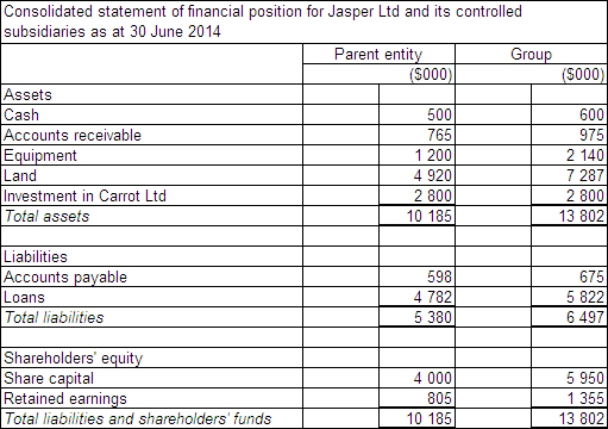

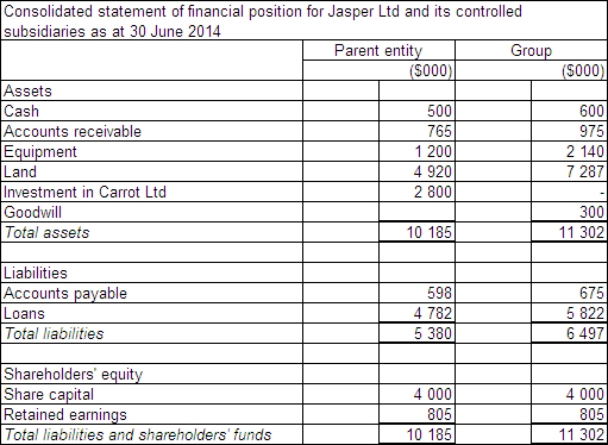

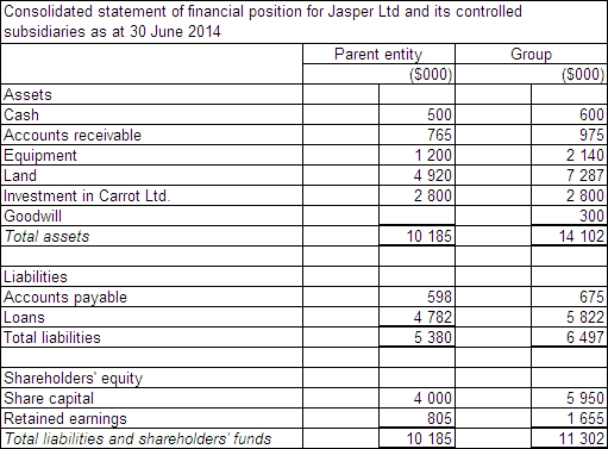

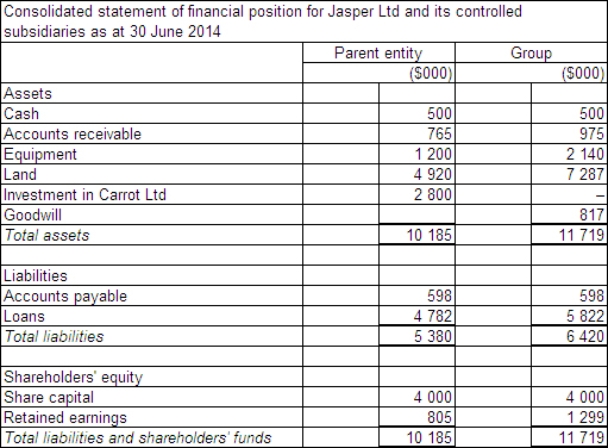

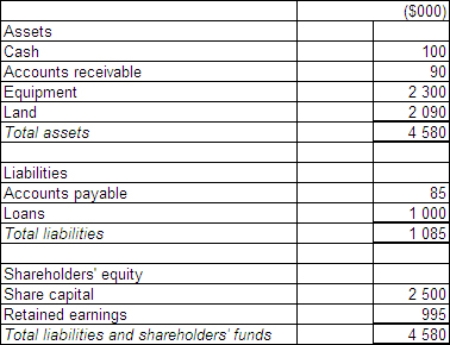

Jasper Ltd acquires all the issued capital of Carrot Ltd for a cash payment of $2 800 000 on 30 June 2014.The statement of financial position of both entities at purchase date is:  Assuming the assets of Carrot Ltd are recorded at fair value,what is the consolidated statement of financial position at the date of purchase?

Assuming the assets of Carrot Ltd are recorded at fair value,what is the consolidated statement of financial position at the date of purchase?

A)

B)

C)

D)

Assuming the assets of Carrot Ltd are recorded at fair value,what is the consolidated statement of financial position at the date of purchase?A)

B)

C)

D)

Question

Question

Question

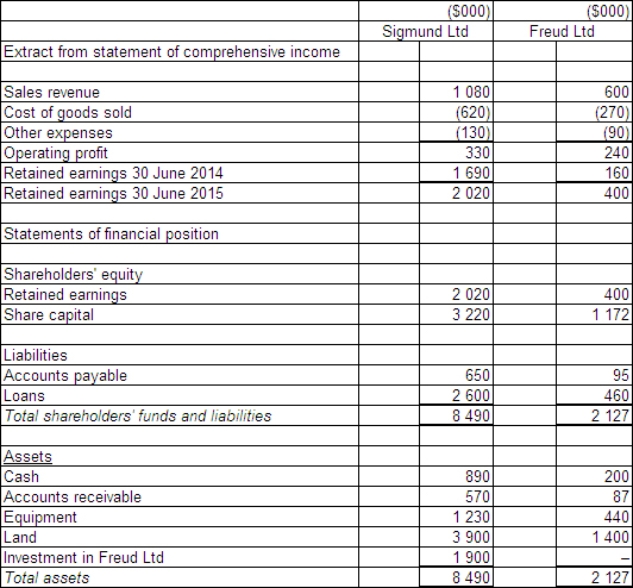

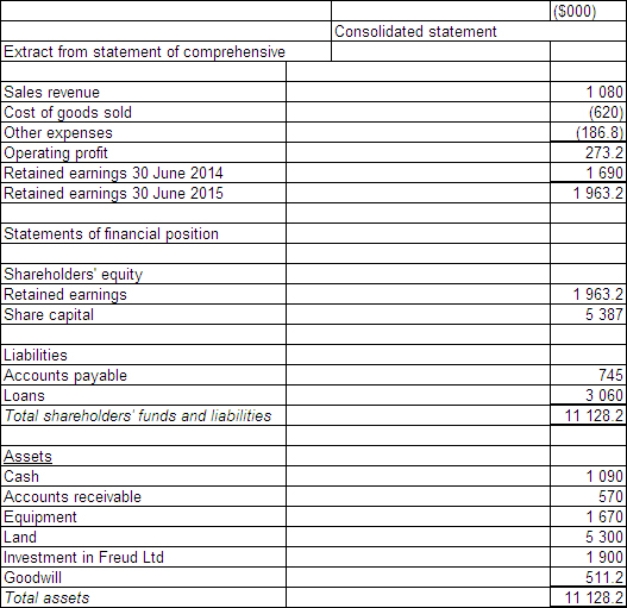

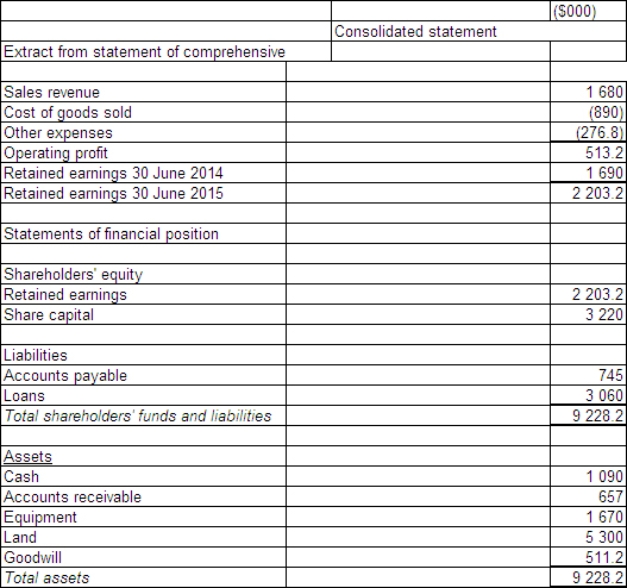

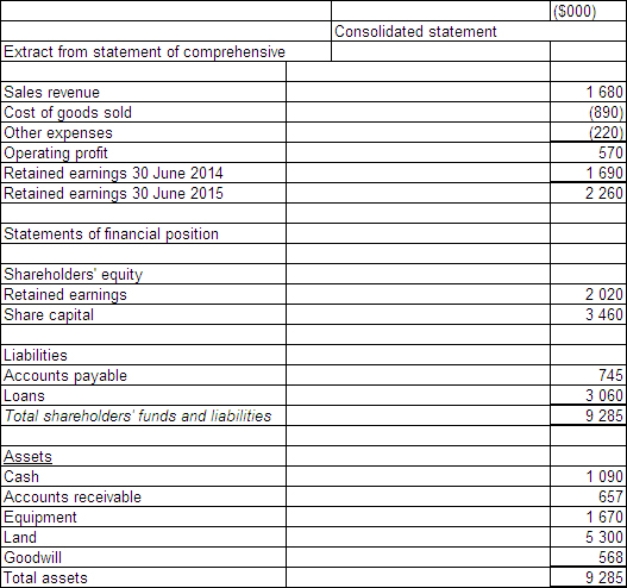

Sigmund Ltd acquires all the issued capital of Freud Ltd for a cash payment of $1 900 000 on 30 June 2014.The financial statements of both entities on 30 June 2105 are:  The fair value of the net tangible assets of Freud Ltd on 30 June 2014 was $1 332 000.The equity of Freud at that time was made up of share capital of $1 172 000 and retained earnings of $160 000.Goodwill had been determined to have been impaired by $56 800 during the period.During the period ended 30 June 2015 there were no intragroup transactions.Which of the following consolidated financial statements is correct?

The fair value of the net tangible assets of Freud Ltd on 30 June 2014 was $1 332 000.The equity of Freud at that time was made up of share capital of $1 172 000 and retained earnings of $160 000.Goodwill had been determined to have been impaired by $56 800 during the period.During the period ended 30 June 2015 there were no intragroup transactions.Which of the following consolidated financial statements is correct?

A)

B)

C)

D)

The fair value of the net tangible assets of Freud Ltd on 30 June 2014 was $1 332 000.The equity of Freud at that time was made up of share capital of $1 172 000 and retained earnings of $160 000.Goodwill had been determined to have been impaired by $56 800 during the period.During the period ended 30 June 2015 there were no intragroup transactions.Which of the following consolidated financial statements is correct?A)

B)

C)

D)

Question

Question

Question

Question

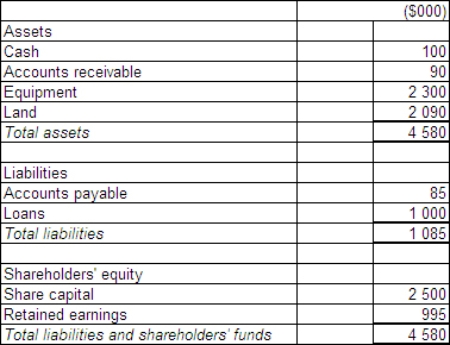

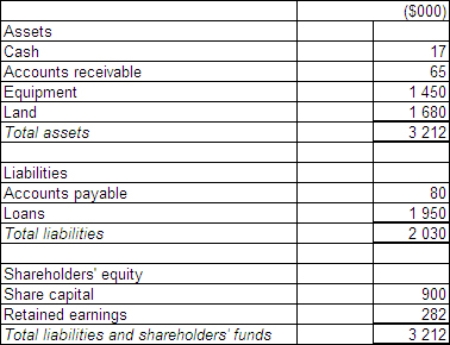

Arthur Ltd acquires all the issued capital of Martha Ltd for a cash payment of $3 000 000 on 30 June 2015.The statement of financial position of Martha Ltd at purchase date is:  Assuming the assets are at fair value,what is the goodwill or excess on consolidation?

Assuming the assets are at fair value,what is the goodwill or excess on consolidation?

A) $500 000 goodwill

B) $1 580 000 excess

C) $510 000 goodwill

D) $495 000 excess

Assuming the assets are at fair value,what is the goodwill or excess on consolidation?A) $500 000 goodwill

B) $1 580 000 excess

C) $510 000 goodwill

D) $495 000 excess

Question

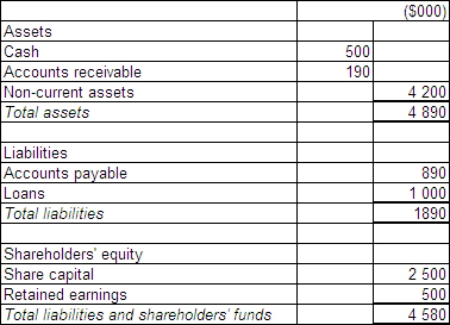

Candle Ltd acquires all the issued capital of Wick Ltd for a cash payment of $4 500 000 on 30 June 2014.The statement of financial position of Wick Ltd at purchase date is:  The fair value of the net assets of Wick Ltd as at 30 June 2014 is $3 800 000.What is the consolidation entry to eliminate the investment in Wick Ltd?

The fair value of the net assets of Wick Ltd as at 30 June 2014 is $3 800 000.What is the consolidation entry to eliminate the investment in Wick Ltd?

A)

B)

C)

D)

The fair value of the net assets of Wick Ltd as at 30 June 2014 is $3 800 000.What is the consolidation entry to eliminate the investment in Wick Ltd?A)

B)

C)

D)

Question

Question

Question

Question

Question

Banderas Ltd acquires all the issued capital of Ryan Ltd for a cash payment of $2 900 000 on 30 June 2014.The statement of financial position of Ryan Ltd at purchase date is:  Assuming the assets are at fair value,what is the consolidation entry to eliminate the investment in Ryan Ltd?

Assuming the assets are at fair value,what is the consolidation entry to eliminate the investment in Ryan Ltd?

A)

B)

C)

D)

Assuming the assets are at fair value,what is the consolidation entry to eliminate the investment in Ryan Ltd?A)

B)

C)

D)

Question

Question

Question

Question

Fresco Ltd acquires all the issued capital of Indoor Ltd for a cash payment of $1 000 000 on 30 June 2015.The statement of financial position of Indoor Ltd at purchase date is:

Assuming the assets of Indoor Ltd are at fair value,what is the entry to eliminate the investment in Fresco Ltd?

A)

B)

C)

D)

Assuming the assets of Indoor Ltd are at fair value,what is the entry to eliminate the investment in Fresco Ltd?

A)

B)

C)

D)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/87

Play

Full screen (f)

Deck 27: Accounting for Group Structures

1

Sullivan (1985)argued that the preparation of group accounts can proceed to the fulfilment of the true and fair notion only when partitioning is fully enforced.

False

2

As prescribed in AASB 3 Business Combinations,when an acquirer makes a bargain purchase,the acquirer recognises the excess as goodwill on acquisition date.

False

3

When an acquirer makes a bargain purchase in a business combination,the excess that remains is recognised in profit or loss of the acquirer on acquisition date.

True

4

In the consolidated financial statements of the parent entity and its controlled entities only transactions with assets and liabilities relating to parties external to the economic entity will be reflected.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

5

AASB 10 notes that in preparing consolidated financial statements,an entity combines the financial statements of the parent and the subsidiaries line by line by adding together,in proportion to the degree of ownership,like items of assets,liabilities,income and expenses; but not equity balances.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

6

It is possible for one entity to control another entity under the AASB 10 definition without the controlling entity having any equity-ownership interest in the other entity.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

7

The first step in the consolidation process is substituting the assets and liabilities of the subsidiary for the investment account that currently exists in the parent company.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

8

Non-controlling interests (minority interests)are defined as the equity in the parent company that is not provided by the group shareholders.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

9

The consolidation process does not involve any adjustments to the financial statements of the individual entities making up the group.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

10

Where separate entities in a group do not apply the same accounting methods,AASB 10 Consolidated Financial Statements prescribes adjustments to be made on consolidation to remove the effects of different accounting policies.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

11

Control is defined in AASB 10 as the 'capacity to manage the policies of another entity'.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

12

A company may own more than 50 per cent of the capital of another entity and not have effective control of that entity as defined in AASB 10.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

13

'Control' over a subsidiary,once determined as being in existence,can only be lost with a change in the level of ownership.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

14

AASB 10 Consolidated Financial Statements permits the reporting periods of entities in the group to be dissimilar as long as adjustments are made on consolidation to remove the effects of different reporting periods.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

15

A subsidiary is an entity that is controlled by a parent entity.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

16

The purpose of providing consolidated statements is to show the results and financial position of a group as if it were operating with a single source of finance.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

17

Goodwill arises at acquisition date when the purchase price exceeds the identifiable assets acquired and the liabilities assumed.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

18

The consolidation concept adopted in AASB 10 is to include all the assets and liabilities of the parent entity and subsidiaries in the consolidation and to treat non-controlling interests as part of the equity of the group.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

19

Under AASB 10 parent companies may choose whether to present one set of consolidated accounts or to provide two or more sub-sets of the consolidated accounts to cover the whole group.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

20

AASB 10 requires the parent company to have control of another entity in order for that entity's consolidation into the group accounts to be required.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

21

Richer Ltd is owed a material amount by Poorer Partnership.Poorer is heavily in debt to Richer Ltd,but due to an unexpected economic downturn is unable to make repayments according to schedule.The board of Richer Ltd believes that Poorer has a good chance of trading out of its current economic difficulties as its management and product are sound and the current problems stem from external factors that are expected to pass within the next 12 to 18 months.Richer Ltd enters into an arrangement with Poorer to manage its finances until the economic situation reverses.At this stage it is not perceived as necessary for Richer Ltd to be otherwise involved in the running of Poorer.Given the situation described,what is Richer Ltd most likely to be required to do to account for Poorer under AASB 10?

A) As the control achieved is only temporary, under AASB 10 Richer would not be required to consolidate Poorer.

B) Richer Ltd should consolidate Poorer under AASB 10 because it has control over it by the definition of 'control' in AASB.

C) Richer Ltd should not be required to consolidate Poorer as it does not have control as defined in AASB 10.

D) Richer Ltd does have temporary control of Poorer, but since Poorer is a partnership Richer is not required to include it in a consolidated set of financial statements.

A) As the control achieved is only temporary, under AASB 10 Richer would not be required to consolidate Poorer.

B) Richer Ltd should consolidate Poorer under AASB 10 because it has control over it by the definition of 'control' in AASB.

C) Richer Ltd should not be required to consolidate Poorer as it does not have control as defined in AASB 10.

D) Richer Ltd does have temporary control of Poorer, but since Poorer is a partnership Richer is not required to include it in a consolidated set of financial statements.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

22

A consolidated entity is defined as:

A) the company and its subsidiaries at the end of the financial year. Subsidiaries are companies and trusts as defined in terms of the Corporations Act.

B) a combined entity constituted by a parent entity and its controlled entities.

C) a trust or partnership registered as a management investment scheme and all the entities it controls at the end of the financial year.

D) the parent company, non-controlling interests and subsidiaries owned by that parent company as at the end of the financial year.

A) the company and its subsidiaries at the end of the financial year. Subsidiaries are companies and trusts as defined in terms of the Corporations Act.

B) a combined entity constituted by a parent entity and its controlled entities.

C) a trust or partnership registered as a management investment scheme and all the entities it controls at the end of the financial year.

D) the parent company, non-controlling interests and subsidiaries owned by that parent company as at the end of the financial year.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

23

Which of the following statements is an accurate description of the difference between a legal entity and an economic entity?

A) An economic entity is one that combines one or more legal entities with synergy such that they each make higher returns than they would individually. If an entity ceases to effectively produce increased returns in this way it becomes uneconomic. A legal entity is one that is recognised in law as having a separate existence from its owners.

B) A legal entity is one that uses appropriate corporate governance measures to ensure that it abides by legislative requirements and other legal regulations. An economic entity may span more than one legal entity, but is not a legal entity in itself.

C) An economic entity is one that is formed for the purpose of generating a profit and therefore a return to owners. A legal entity is one that is circumscribed by legal constitution or accounting standards as constituting a reporting entity.

D) A legal entity refers to an entity that has its own particular legal status such as a company, trust or partnership. The concept of an economic entity emphasises substance over legal form. It may operate as a coordinated entity and contain more than one legal entity.

A) An economic entity is one that combines one or more legal entities with synergy such that they each make higher returns than they would individually. If an entity ceases to effectively produce increased returns in this way it becomes uneconomic. A legal entity is one that is recognised in law as having a separate existence from its owners.

B) A legal entity is one that uses appropriate corporate governance measures to ensure that it abides by legislative requirements and other legal regulations. An economic entity may span more than one legal entity, but is not a legal entity in itself.

C) An economic entity is one that is formed for the purpose of generating a profit and therefore a return to owners. A legal entity is one that is circumscribed by legal constitution or accounting standards as constituting a reporting entity.

D) A legal entity refers to an entity that has its own particular legal status such as a company, trust or partnership. The concept of an economic entity emphasises substance over legal form. It may operate as a coordinated entity and contain more than one legal entity.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

24

'Passive' control implies that it is possible to exert control over another entity even though the option to exert such control may never be exercised.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

25

AASB 10 defines control as:

A) governing the financial, operating and sustainability policies of an entity so as to benefit from its activities.

B) the capacity of an entity to dominate the decision making of another entity by virtue of a majority shareholding or controlling ownership interest in some form.

C) the capacity and willingness to direct the decision making of another entity with respect to its financial and operating policies to improve the performance and position of the controlling entity.

D) the power to govern the financial and operating policies of an entity so as to benefit from its activities.

A) governing the financial, operating and sustainability policies of an entity so as to benefit from its activities.

B) the capacity of an entity to dominate the decision making of another entity by virtue of a majority shareholding or controlling ownership interest in some form.

C) the capacity and willingness to direct the decision making of another entity with respect to its financial and operating policies to improve the performance and position of the controlling entity.

D) the power to govern the financial and operating policies of an entity so as to benefit from its activities.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

26

Which of the following statements accurately describes the elimination entry to eliminate pre-acquisition shareholders' funds?

A) It is made once at the time of the first consolidation of the economic entity's accounts in order to eliminate the parent entity's investment in the subsidiary against the non-monetary assets of the controlled entity.

B) It is made each time the consolidation is performed in order to adjust the carrying value of the controlled entity's non-current assets to their fair value.

C) It is carried out once at the date that control of the subsidiary is achieved in order to create the goodwill or discount and eliminate the parent entity's equity against the controlled entity's investment.

D) It is made each time the consolidation is performed in order to eliminate the parent entity's investment in the controlled entity against the equity of the controlled entity. Any adjustments necessary to bring the non-current assets of the controlled entity to fair value are made before the elimination entry and any difference between the consideration paid and the fair value of the net assets of the controlled entity are recognised.

A) It is made once at the time of the first consolidation of the economic entity's accounts in order to eliminate the parent entity's investment in the subsidiary against the non-monetary assets of the controlled entity.

B) It is made each time the consolidation is performed in order to adjust the carrying value of the controlled entity's non-current assets to their fair value.

C) It is carried out once at the date that control of the subsidiary is achieved in order to create the goodwill or discount and eliminate the parent entity's equity against the controlled entity's investment.

D) It is made each time the consolidation is performed in order to eliminate the parent entity's investment in the controlled entity against the equity of the controlled entity. Any adjustments necessary to bring the non-current assets of the controlled entity to fair value are made before the elimination entry and any difference between the consideration paid and the fair value of the net assets of the controlled entity are recognised.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

27

Which of the following consolidation concepts are described correctly?

A) The entity concept requires the inclusion of all the parent entity assets and the proportionate share of the assets and liabilities of the subsidiaries where the proportion is based on the direct ownership of the capital of the subsidiary by parent companies within the group.

B) The proprietary concept includes all the assets and liabilities of the parent company and subsidiaries as assets and liabilities of the group. Non-controlling interest is treated as a liability of the group.

C) The parent-entity concept includes all assets and liabilities of the parent and its subsidiaries in the consolidated accounts. The non-controlling interest is treated as a liability of the group.

D) The proprietary concept includes all the assets and liabilities of the parent company and subsidiaries as assets and liabilities of the group. Non-controlling interest is treated as a liability of the group; the parent-entity concept includes all assets and liabilities of the parent and its subsidiaries in the consolidated accounts. The non-controlling interest is treated as a liability of the group.

A) The entity concept requires the inclusion of all the parent entity assets and the proportionate share of the assets and liabilities of the subsidiaries where the proportion is based on the direct ownership of the capital of the subsidiary by parent companies within the group.

B) The proprietary concept includes all the assets and liabilities of the parent company and subsidiaries as assets and liabilities of the group. Non-controlling interest is treated as a liability of the group.

C) The parent-entity concept includes all assets and liabilities of the parent and its subsidiaries in the consolidated accounts. The non-controlling interest is treated as a liability of the group.

D) The proprietary concept includes all the assets and liabilities of the parent company and subsidiaries as assets and liabilities of the group. Non-controlling interest is treated as a liability of the group; the parent-entity concept includes all assets and liabilities of the parent and its subsidiaries in the consolidated accounts. The non-controlling interest is treated as a liability of the group.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

28

Post-acquisition earnings of the subsidiary are included in the economic entity's earnings.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

29

Gigi Ltd is acting as a trustee for Bonberre trust.Gigi has complete control of the operating and financing decisions of the trust.The nominated beneficiaries of the trust are Mr and Mrs Bonberre,who each receive 50 per cent of the trust profits.Given the situation described,what is Gigi Ltd most likely to be required to do to account for the Bonberre trust under AASB 10?

A) Gigi Ltd should be required to consolidate the trust as it controls the operating and financing decisions.

B) Gigi Ltd should not be required to consolidate Bonberre trust because a trust cannot be a subsidiary under The Corporations Law.

C) Gigi Ltd should treat the trust as an investment in its books, valued at the present value of any future income streams expected to be received in return for managing the trust.

D) Gigi Ltd should not consolidate the trust because, while it does control the financing and operating decisions of the trust, it cannot do so in a way to benefit Gigi Ltd.

A) Gigi Ltd should be required to consolidate the trust as it controls the operating and financing decisions.

B) Gigi Ltd should not be required to consolidate Bonberre trust because a trust cannot be a subsidiary under The Corporations Law.

C) Gigi Ltd should treat the trust as an investment in its books, valued at the present value of any future income streams expected to be received in return for managing the trust.

D) Gigi Ltd should not consolidate the trust because, while it does control the financing and operating decisions of the trust, it cannot do so in a way to benefit Gigi Ltd.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

30

The degree of control over an investee determines how the investor accounts for the investment.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

31

At acquisition date which of the following is not required to be recognised by the acquirer?

A) Liabilities assumed.

B) non-controlling interest in the acquiree.

C) goodwill separately from the identified assets acquired

D) Retained earnings of the acquiree.

A) Liabilities assumed.

B) non-controlling interest in the acquiree.

C) goodwill separately from the identified assets acquired

D) Retained earnings of the acquiree.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

32

In the situation in which a subsidiary is only controlled temporarily,AASB 10 requires:

A) the investment be recorded at fair market value and any gain or loss on acquisition recognised immediately in the statement of comprehensive income.

B) the subsidiary to be treated as an associate and equity accounting applied.

C) the results of the subsidiary for the period of time that it was controlled to be included in the consolidated accounts.

D) the investment to be reported at cost and dividends be accrued when declared.

A) the investment be recorded at fair market value and any gain or loss on acquisition recognised immediately in the statement of comprehensive income.

B) the subsidiary to be treated as an associate and equity accounting applied.

C) the results of the subsidiary for the period of time that it was controlled to be included in the consolidated accounts.

D) the investment to be reported at cost and dividends be accrued when declared.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

33

What are the major consolidation concepts?

A) entity, partnership and parent

B) equity, control and ownership

C) parent-entity, ownership and proprietary

D) entity, parent-entity and proprietary

A) entity, partnership and parent

B) equity, control and ownership

C) parent-entity, ownership and proprietary

D) entity, parent-entity and proprietary

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

34

Panda Ltd acquires all the issued capital of Bear Ltd for a cash payment of $2 545 000 on 30 June 2015.The statement of financial position of Bear Ltd at purchase date is: Assuming the assets are at fair value,what amount of goodwill would be recorded in the books of Bear Ltd and what amount would be recorded in the consolidated statements at the date of purchase?

A) Bear's books $0; consolidated statements $0

B) Bear's books $0; consolidated statements $545 000

C) Bear's books $545 000; consolidated statements $270 000

D) Bear's books $270 000; consolidated statements $270 000

A) Bear's books $0; consolidated statements $0

B) Bear's books $0; consolidated statements $545 000

C) Bear's books $545 000; consolidated statements $270 000

D) Bear's books $270 000; consolidated statements $270 000

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

35

The partition effect in relation to a group of companies arose when:

A) It was not permitted under The Corporations Law to consolidate an entity that was not a company. This resulted not only in the non-company entity not being consolidated, but also all the entities (company or otherwise) that it controlled not being consolidated.

B) The non-controlling shareholders in a number of companies controlled by a parent entity organised themselves to block the transfer of funds within a group.

C) Companies in a group coordinated to transfer assets in such a way as to protect part of the group from being taxed, thus reducing the total tax owing for the group as a whole.

D) Dividends were declared and paid in such a way as to manage cash reserves within a group.

A) It was not permitted under The Corporations Law to consolidate an entity that was not a company. This resulted not only in the non-company entity not being consolidated, but also all the entities (company or otherwise) that it controlled not being consolidated.

B) The non-controlling shareholders in a number of companies controlled by a parent entity organised themselves to block the transfer of funds within a group.

C) Companies in a group coordinated to transfer assets in such a way as to protect part of the group from being taxed, thus reducing the total tax owing for the group as a whole.

D) Dividends were declared and paid in such a way as to manage cash reserves within a group.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

36

The factors that are taken into consideration in determining whether or not an entity should be consolidated under AASB 10 include:

A) the nature of the legal form of the entity and whether or not the 'parent' entity owns enough of the equity in the entity to effectively control the benefits that flow from the relationship with the other entity.

B) whether or not the potential 'parent' entity controls the other entity.

C) the number of members on the board under the control of the potential 'parent' entity, and whether or not the other entity has been partitioned by the potential 'parent' entity.

D) whether or not the potential 'parent' entity controls the other entity and whether or not it is in a significantly different business to the potential 'parent'.

A) the nature of the legal form of the entity and whether or not the 'parent' entity owns enough of the equity in the entity to effectively control the benefits that flow from the relationship with the other entity.

B) whether or not the potential 'parent' entity controls the other entity.

C) the number of members on the board under the control of the potential 'parent' entity, and whether or not the other entity has been partitioned by the potential 'parent' entity.

D) whether or not the potential 'parent' entity controls the other entity and whether or not it is in a significantly different business to the potential 'parent'.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

37

One important aim of releasing AAS 24 in 1991 and amendments made to The Corporations Law in the same year was to:

A) require parent entities to consolidate companies that they controlled into one set of financial statements for the first time.

B) change the treatment of non-controlling interests to be reflected in the accounts as a liability.

C) prevent companies from keeping debt off the statement of financial position consolidated statement of financial position by interposing partnerships or trusts in the group structure.

D) require the consolidation of the cash-flow statement as well as the statement of financial position and statement of comprehensive income.

A) require parent entities to consolidate companies that they controlled into one set of financial statements for the first time.

B) change the treatment of non-controlling interests to be reflected in the accounts as a liability.

C) prevent companies from keeping debt off the statement of financial position consolidated statement of financial position by interposing partnerships or trusts in the group structure.

D) require the consolidation of the cash-flow statement as well as the statement of financial position and statement of comprehensive income.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

38

Growl Ltd acquires all the issued capital of Tiger Ltd for a cash payment of $5 000 000 on 30 June 2015.The statement of financial position of Tiger Ltd at purchase date is: The fair value of the net assets at the date of purchase was $4 200 000.What amount of goodwill or excess would be recorded in the consolidated statements at the date of purchase?

A) $500 000 goodwill

B) $300 000 discount

C) $800 000 goodwill

D) $389 000 discount

A) $500 000 goodwill

B) $300 000 discount

C) $800 000 goodwill

D) $389 000 discount

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

39

AASB 10 identifies a number of factors that may indicate the existence of control.These include:

A) the ability to appoint the CEO of another entity.

B) the power to dominate the composition of the board of directors or governing body of another entity.

C) the power to require another entity to purchase goods and services from an entity that results in a benefit to the controlling entity.

D) the ability to appoint the CEO of another entity and the power to dominate the composition of the board of directors or governing body of another entity.

A) the ability to appoint the CEO of another entity.

B) the power to dominate the composition of the board of directors or governing body of another entity.

C) the power to require another entity to purchase goods and services from an entity that results in a benefit to the controlling entity.

D) the ability to appoint the CEO of another entity and the power to dominate the composition of the board of directors or governing body of another entity.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

40

Which consolidation concept mainly underlies the approach adopted in AASB 10?

A) proprietary concept

B) accrual concept

C) entity concept

D) parent-entity concept

A) proprietary concept

B) accrual concept

C) entity concept

D) parent-entity concept

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

41

A subsidiary:

A) is excluded from consolidation because the investor is a venture capital organisation.

B) is not excluded from consolidation simply because the investor is a venture capital organisation.

C) is excluded from consolidation because its business activities are dissimilar from those of other entities within the group.

D) is not excluded from consolidation simply because the investor only has significant influence, and not control, over it.

A) is excluded from consolidation because the investor is a venture capital organisation.

B) is not excluded from consolidation simply because the investor is a venture capital organisation.

C) is excluded from consolidation because its business activities are dissimilar from those of other entities within the group.

D) is not excluded from consolidation simply because the investor only has significant influence, and not control, over it.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

42

Jasper Ltd acquires all the issued capital of Carrot Ltd for a cash payment of $2 800 000 on 30 June 2014.The statement of financial position of both entities at purchase date is: Assuming the assets of Carrot Ltd are recorded at fair value,what is the consolidated statement of financial position at the date of purchase?

A)

B)

C)

D)

Assuming the assets of Carrot Ltd are recorded at fair value,what is the consolidated statement of financial position at the date of purchase?A)

B)

C)

D)

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

43

The preparation of consolidated financial statements:

A) obviates the need for separate entities to prepare and release their own separate financial statements.

B) does not obviate the need for separate entities to prepare and release their own separate financial statements.

C) should be done in accordance with AASB 10.

D) does not obviate the need for separate entities to prepare and release their own separate financial statements and should be done in accordance with AASB 10.

A) obviates the need for separate entities to prepare and release their own separate financial statements.

B) does not obviate the need for separate entities to prepare and release their own separate financial statements.

C) should be done in accordance with AASB 10.

D) does not obviate the need for separate entities to prepare and release their own separate financial statements and should be done in accordance with AASB 10.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

44

A former loophole (now closed)that existed under the former s.9 of The Corporations Law:

A) required the preparation of one set of consolidated accounts for the group.

B) required the preparation of separate accounts for each body corporate in the group.

C) gave the choice of using full consolidation, proportional consolidation or the equity method of accounting.

D) gave the choice of one set, or two or more sets, of consolidated accounts; or separate accounts for each body corporate; or a combination.

A) required the preparation of one set of consolidated accounts for the group.

B) required the preparation of separate accounts for each body corporate in the group.

C) gave the choice of using full consolidation, proportional consolidation or the equity method of accounting.

D) gave the choice of one set, or two or more sets, of consolidated accounts; or separate accounts for each body corporate; or a combination.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

45

Sigmund Ltd acquires all the issued capital of Freud Ltd for a cash payment of $1 900 000 on 30 June 2014.The financial statements of both entities on 30 June 2105 are: The fair value of the net tangible assets of Freud Ltd on 30 June 2014 was $1 332 000.The equity of Freud at that time was made up of share capital of $1 172 000 and retained earnings of $160 000.Goodwill had been determined to have been impaired by $56 800 during the period.During the period ended 30 June 2015 there were no intragroup transactions.Which of the following consolidated financial statements is correct?

A)

B)

C)

D)

The fair value of the net tangible assets of Freud Ltd on 30 June 2014 was $1 332 000.The equity of Freud at that time was made up of share capital of $1 172 000 and retained earnings of $160 000.Goodwill had been determined to have been impaired by $56 800 during the period.During the period ended 30 June 2015 there were no intragroup transactions.Which of the following consolidated financial statements is correct?A)

B)

C)

D)

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

46

'Control' exists when the parent owns less than half of the voting power of an entity when:

A) No other entity owns more than half either.

B) There is power to govern the financial and operating policies of the entity under a statute.

C) There is power to govern the financial and operating policies of the entity under an agreement.

D) There is power to govern the financial and operating policies of the entity under a statute and there is power to govern the financial and operating policies of the entity under an agreement.

A) No other entity owns more than half either.

B) There is power to govern the financial and operating policies of the entity under a statute.

C) There is power to govern the financial and operating policies of the entity under an agreement.

D) There is power to govern the financial and operating policies of the entity under a statute and there is power to govern the financial and operating policies of the entity under an agreement.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

47

In a situation where the net assets acquired in the controlled entity are not recorded at fair value,approaches that may be taken to account for this include:

A) Adjust the excess or goodwill so that the elimination entry balances.

B) Revalue the assets in the parent entity's books.

C) Revalue the assets during the consolidation process each period.

D) Adjust the depreciation on the assets to bring them to fair value in the consolidated accounts.

A) Adjust the excess or goodwill so that the elimination entry balances.

B) Revalue the assets in the parent entity's books.

C) Revalue the assets during the consolidation process each period.

D) Adjust the depreciation on the assets to bring them to fair value in the consolidated accounts.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

48

Non-controlling interests are defined is AASB 10 as:

A) that portion of profit or loss and net assets of a subsidiary attributable to equity interests that are not owned directly by the parent.

B) that portion of net assets of a subsidiary attributable to equity interests that are not owned, directly or indirectly through subsidiaries, by the parent.

C) that portion of profit or loss and net assets of a subsidiary attributable to equity interests that are not owned, directly or indirectly through subsidiaries, by the parent.

D) the largest single shareholding, less fifty per cent, not owned, directly or indirectly through subsidiaries, by the parent.

A) that portion of profit or loss and net assets of a subsidiary attributable to equity interests that are not owned directly by the parent.

B) that portion of net assets of a subsidiary attributable to equity interests that are not owned, directly or indirectly through subsidiaries, by the parent.

C) that portion of profit or loss and net assets of a subsidiary attributable to equity interests that are not owned, directly or indirectly through subsidiaries, by the parent.

D) the largest single shareholding, less fifty per cent, not owned, directly or indirectly through subsidiaries, by the parent.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

49

Arthur Ltd acquires all the issued capital of Martha Ltd for a cash payment of $3 000 000 on 30 June 2015.The statement of financial position of Martha Ltd at purchase date is: Assuming the assets are at fair value,what is the goodwill or excess on consolidation?

A) $500 000 goodwill

B) $1 580 000 excess

C) $510 000 goodwill

D) $495 000 excess

Assuming the assets are at fair value,what is the goodwill or excess on consolidation?A) $500 000 goodwill

B) $1 580 000 excess

C) $510 000 goodwill

D) $495 000 excess

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

50

Candle Ltd acquires all the issued capital of Wick Ltd for a cash payment of $4 500 000 on 30 June 2014.The statement of financial position of Wick Ltd at purchase date is: The fair value of the net assets of Wick Ltd as at 30 June 2014 is $3 800 000.What is the consolidation entry to eliminate the investment in Wick Ltd?

A)

B)

C)

D)

The fair value of the net assets of Wick Ltd as at 30 June 2014 is $3 800 000.What is the consolidation entry to eliminate the investment in Wick Ltd?A)

B)

C)

D)

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

51

Where the controlled entity's non-current assets were not at fair value at the date of purchase and they have not been revalued in the controlled entity's accounts,the treatment in the consolidation entry may include which of the following entries?

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

52

In what situation does an excess on acquisition arise and how does AASB 3 require it to be treated?

A) An excess arises when the fair value of the purchase consideration is greater than the nominal value of the assets purchased. AASB 3 requires an excess to be eliminated by recognising it as a gain in the period in which the entity was purchased.

B) An excess arises when the fair value of the purchase consideration is greater than the nominal value of the assets purchased. AASB 3 requires the fair values of the monetary assets acquired to be proportionately decreased until the excess is eliminated. If an excess balance remains it must be recognised as an expense in the statement of comprehensive income.

C) An excess arises when the cost of acquisition exceeds the fair value of the identifiable net assets purchased. AASB 3 requires the equity of the purchased entity to be proportionately decreased until the excess is eliminated.

D) An excess arises when the fair value of the identifiable net assets acquired by the entity exceeds the fair value of the consideration paid. AASB 3 requires a reassessment of the identification and measurement of the identifiable net assets, and a reassessment of the measurement of the fair value of the consideration paid. If an excess remains after the reassessment it must be recognised as income in profit or loss.

A) An excess arises when the fair value of the purchase consideration is greater than the nominal value of the assets purchased. AASB 3 requires an excess to be eliminated by recognising it as a gain in the period in which the entity was purchased.

B) An excess arises when the fair value of the purchase consideration is greater than the nominal value of the assets purchased. AASB 3 requires the fair values of the monetary assets acquired to be proportionately decreased until the excess is eliminated. If an excess balance remains it must be recognised as an expense in the statement of comprehensive income.

C) An excess arises when the cost of acquisition exceeds the fair value of the identifiable net assets purchased. AASB 3 requires the equity of the purchased entity to be proportionately decreased until the excess is eliminated.

D) An excess arises when the fair value of the identifiable net assets acquired by the entity exceeds the fair value of the consideration paid. AASB 3 requires a reassessment of the identification and measurement of the identifiable net assets, and a reassessment of the measurement of the fair value of the consideration paid. If an excess remains after the reassessment it must be recognised as income in profit or loss.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

53

Gingimup Ltd purchased all the equity of Kindawansa Ltd on 30 June 2015.At that time the carrying value of the net assets of Kindawansa was $1 200 000.This amount was made up in equity as follows: share capital $1 000 000; retained earnings $200 000.Kindawansa has held some valuable land for a long time (purchased at $ 1 200 000),but has not revalued it.Its fair value at 30 June 2015 was $2 800 000 (all other non-current assets are recorded at fair value).Gingimup Ltd paid cash consideration of $3 000 000 for Kindawansa Ltd.Assuming that the land has not been revalued in the controlled entity's books,what are the elimination entries required to reflect the purchase of Kindawansa Ltd?

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

54

Gouda Ltd acquires all the issued capital of Cheese Ltd for a cash payment of $2 545 000 on 30 June 2015.The statement of financial position of Cheese Ltd at purchase date is: Assuming the assets are at fair value,what would be the consolidation entry to eliminate the investment in Cheese Ltd?

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

55

Banderas Ltd acquires all the issued capital of Ryan Ltd for a cash payment of $2 900 000 on 30 June 2014.The statement of financial position of Ryan Ltd at purchase date is: Assuming the assets are at fair value,what is the consolidation entry to eliminate the investment in Ryan Ltd?

A)

B)

C)

D)

Assuming the assets are at fair value,what is the consolidation entry to eliminate the investment in Ryan Ltd?A)

B)

C)

D)

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

56

Which of the following statements is not correct?

A) A group comprises a parent and all of its subsidiaries.

B) Consolidated financial statements are financial statements of a group of entities presented as if that group was acting as a single economic entity.

C) A subsidiary is an entity that is controlled by another entity.

D) A parent is an entity that has more than one subsidiary.

A) A group comprises a parent and all of its subsidiaries.

B) Consolidated financial statements are financial statements of a group of entities presented as if that group was acting as a single economic entity.

C) A subsidiary is an entity that is controlled by another entity.

D) A parent is an entity that has more than one subsidiary.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

57

Which of the following statements accurately describes important aspects of consolidation after the date of acquisition?

A) The elimination entry is made only the first time the consolidation is conducted. Any goodwill arising from the purchase is amortised over the appropriate period (not more than 20 years) and any excess will have been written off in the first year's elimination entry. Post-acquisition earnings are considered to be part of the group's earnings.

B) The elimination entry will be made each time the consolidation is undertaken. Goodwill arising on consolidation will be recognised. If the controlled entity was purchased at a discount the excess is recognised as a gain in the profit or loss on the acquisition date

C) The elimination entry is made each time the consolidation is undertaken. If an excess arises on consolidation it is completely written off in the first year and is not included in the consolidation worksheet entries again. If goodwill arises it is recognised for the full amount at acquisition and amortised over a period not exceeding 20 years. Any earnings made by the controlled entity after acquisition belongs to the parent entity and should be reflected in the consolidated accounts and the parent entity's books.

D) The elimination entry will be made each time the consolidation is undertaken, but the amount of goodwill or excess recognised each time will change. The excess will be written off in the first period and the goodwill amortised over an appropriate period (not exceeding 20 years). The goodwill expense will be recognised in the books of the parent company and matched against the post-acquisition earnings of the controlled entity. Any remaining surplus is treated as income in the consolidated accounts.

A) The elimination entry is made only the first time the consolidation is conducted. Any goodwill arising from the purchase is amortised over the appropriate period (not more than 20 years) and any excess will have been written off in the first year's elimination entry. Post-acquisition earnings are considered to be part of the group's earnings.

B) The elimination entry will be made each time the consolidation is undertaken. Goodwill arising on consolidation will be recognised. If the controlled entity was purchased at a discount the excess is recognised as a gain in the profit or loss on the acquisition date

C) The elimination entry is made each time the consolidation is undertaken. If an excess arises on consolidation it is completely written off in the first year and is not included in the consolidation worksheet entries again. If goodwill arises it is recognised for the full amount at acquisition and amortised over a period not exceeding 20 years. Any earnings made by the controlled entity after acquisition belongs to the parent entity and should be reflected in the consolidated accounts and the parent entity's books.

D) The elimination entry will be made each time the consolidation is undertaken, but the amount of goodwill or excess recognised each time will change. The excess will be written off in the first period and the goodwill amortised over an appropriate period (not exceeding 20 years). The goodwill expense will be recognised in the books of the parent company and matched against the post-acquisition earnings of the controlled entity. Any remaining surplus is treated as income in the consolidated accounts.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

58

The lack of a direct link between levels of ownership and control (i.e.the degree of ownership does not,of itself,determine if an entity has control of another):

A) is consistent with the AASB Framework's definition of assets, which relies on control and not legal ownership.

B) is consistent with the AASB Framework's definition of assets, which relies on legal ownership and not control.

C) is consistent with the AASB Framework's definition of equity, which recognises investments in other entities.

D) is consistent with the AASB Framework's definition of equity, which relies on control and not legal ownership.

A) is consistent with the AASB Framework's definition of assets, which relies on control and not legal ownership.

B) is consistent with the AASB Framework's definition of assets, which relies on legal ownership and not control.

C) is consistent with the AASB Framework's definition of equity, which recognises investments in other entities.

D) is consistent with the AASB Framework's definition of equity, which relies on control and not legal ownership.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

59

Fresco Ltd acquires all the issued capital of Indoor Ltd for a cash payment of $1 000 000 on 30 June 2015.The statement of financial position of Indoor Ltd at purchase date is:

Assuming the assets of Indoor Ltd are at fair value,what is the entry to eliminate the investment in Fresco Ltd?

A)

B)

C)

D)

Assuming the assets of Indoor Ltd are at fair value,what is the entry to eliminate the investment in Fresco Ltd?

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

60

In the situation in which a subsidiary revalues its non-current assets to fair value in its books as part of being acquired by a parent entity,the accounting treatment is:

A) to treat the revaluation according to AASB 116 Property, Plant and Equipment in the books of the subsidiary entity.

B) to create a revaluation surplus in the consolidated accounts and write it off against the parent entity's investment in the subsidiary.

C) to adjust the investment recorded by the parent entity so that the entry balances in the elimination entry.

D) to write off the adjustment to fair value to the statement of comprehensive income, as determined by AASB 10 Consolidated Financial Statements, which is concerned with the treatment of the revaluation in the books of the controlled entity.

A) to treat the revaluation according to AASB 116 Property, Plant and Equipment in the books of the subsidiary entity.

B) to create a revaluation surplus in the consolidated accounts and write it off against the parent entity's investment in the subsidiary.

C) to adjust the investment recorded by the parent entity so that the entry balances in the elimination entry.

D) to write off the adjustment to fair value to the statement of comprehensive income, as determined by AASB 10 Consolidated Financial Statements, which is concerned with the treatment of the revaluation in the books of the controlled entity.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

61

Discuss,and provide an example of the 'partition' effect that existed under the previous Corporations Law,prior to 1991.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

62

After initial recognition,goodwill is measured in which of the following ways?

A) at cost

B) at fair value

C) at cost less accumulated impairment losses

D) at cost less accumulated amortisation

A) at cost

B) at fair value

C) at cost less accumulated impairment losses

D) at cost less accumulated amortisation

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

63

On consolidation,the investment in subsidiary,shown in the investor's books,shall be eliminated in full against which of the following?

A) assets and liabilities of the subsidiary

B) post-acquisition shareholders' funds of the subsidiary

C) share capital of the subsidiary acquired by the parent only

D) none of the given answers

A) assets and liabilities of the subsidiary

B) post-acquisition shareholders' funds of the subsidiary

C) share capital of the subsidiary acquired by the parent only

D) none of the given answers

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

64

AASB 12 Disclosure of Interests in Other Entities requires an entity to disclose for each of its subsidiaries that have non-controlling interests that are material to the reporting entity:

A) summarised financial information about the subsidiary

B) the profit or loss allocated to non-controlling interests of the subsidiary during the reporting period.

C) accumulated non-controlling interests of the subsidiary at the end of the reporting period.

D) All of the given answers are required to be disclosed.

A) summarised financial information about the subsidiary

B) the profit or loss allocated to non-controlling interests of the subsidiary during the reporting period.

C) accumulated non-controlling interests of the subsidiary at the end of the reporting period.

D) All of the given answers are required to be disclosed.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

65

Which of the following statements is not in accordance with AASB 3 Business Combinations?

A) An entity shall account for each business combination by applying the acquisition method.

B) For each business combination, one of the combining entities shall be identified as the acquirer.

C) The acquirer is required to recognise, separately from goodwill, the identifiable assets acquired, the liabilities assumed and any non-controlling interest in the acquiree.

D) The acquirer shall measure the identifiable assets acquired and the liabilities assumed at their acquisition-date agreed values.

A) An entity shall account for each business combination by applying the acquisition method.

B) For each business combination, one of the combining entities shall be identified as the acquirer.

C) The acquirer is required to recognise, separately from goodwill, the identifiable assets acquired, the liabilities assumed and any non-controlling interest in the acquiree.

D) The acquirer shall measure the identifiable assets acquired and the liabilities assumed at their acquisition-date agreed values.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

66

On 1 July 2012,Goliath Ltd acquires all shares in David Ltd for $800 000.The fair value of net assets acquired is $920 000 comprised of $600 000 in share capital and $320 000 in retained earnings.What is the appropriate elimination entry for this investment that is in accordance with AASB 3 Business Combinations and AASB 10 Consolidated Financial Statements?

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

67

On 1 July 2012,Mawson Ltd acquires all shares in Mountain Ltd for $400 000.The fair value of net assets acquired is $320 000 comprising $200 000 in share capital and $120 000 in retained earnings.On the date of purchase,successful publishing title is not recorded in the books of the acquiree but assumed by the acquirer.The publishing title is estimated at $20 000 and likely to eventuate after acquisition.What is the appropriate elimination entry for this investment that is in accordance with AASB 3 Business Combinations and AASB 10 Consolidated Financial Statements?

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

68

Which of the following statements about post-acquisition earnings is incorrect?

A) They form part of earnings of the economic entity.

B) They are the earnings produced subsequent to the acquisition date by members of the group.

C) They are eliminated against the parent's earnings, in a similar fashion to pre-acquisition earnings.

D) They form part of earnings of the economic entity and they are eliminated against the parent's earnings, in a similar fashion to pre-acquisition earnings.

A) They form part of earnings of the economic entity.

B) They are the earnings produced subsequent to the acquisition date by members of the group.

C) They are eliminated against the parent's earnings, in a similar fashion to pre-acquisition earnings.

D) They form part of earnings of the economic entity and they are eliminated against the parent's earnings, in a similar fashion to pre-acquisition earnings.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

69

On 1 July 2012,Felix Ltd acquires all shares in Oscar Ltd for $800 000.The fair value of net assets acquired is $620 000 comprising $400 000 in share capital and $220 000 in retained earnings.What is the appropriate elimination entry for this investment that is in accordance with AASB 3 Business Combinations and AASB 10 Consolidated Financial Statements?

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

70

Discuss the reason for recognising non-controlling interests as part of equity,rather than as a liability.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

71

Which of the following would not be classified as an identifiable intangible asset in accordance with AASB 138 Intangible assets?

A) mastheads

B) goodwill

C) customer lists

D) patent

A) mastheads

B) goodwill

C) customer lists

D) patent

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

72

Goodwill is:

A) an intangible asset, as defined in AASB 138.

B) future economic benefits arising from assets that are not capable of being separately recognised or individually identified

C) determined as being the excess of the fair value of the identifiable net assets acquired over the cost of an acquisition.

D) recognised by the acquirer, at acquisition date, as an asset in its own books.

A) an intangible asset, as defined in AASB 138.

B) future economic benefits arising from assets that are not capable of being separately recognised or individually identified

C) determined as being the excess of the fair value of the identifiable net assets acquired over the cost of an acquisition.

D) recognised by the acquirer, at acquisition date, as an asset in its own books.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

73

In determining control,'potential voting rights':

A) include those rights embedded in such instruments as share call options and share warrants.

B) which are currently exercisable should be taken into account.

C) even if they are not currently exercisable should be taken into account.

D) include those rights embedded in such instruments as share call options and share warrants and which are currently exercisable.

A) include those rights embedded in such instruments as share call options and share warrants.

B) which are currently exercisable should be taken into account.

C) even if they are not currently exercisable should be taken into account.

D) include those rights embedded in such instruments as share call options and share warrants and which are currently exercisable.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

74

On 1 July 2012,Carol Ltd acquires all shares in Alice Ltd for $400 000.The fair value of net assets acquired is $320 000 comprising $200 000 in share capital and $120 000 in retained earnings.On the date of purchase,a contingent liability is not recorded in the books of the acquiree but assumed by the acquirer.The contingent liability is estimated at $20 000 and likely to eventuate after acquisition.What is the appropriate elimination entry for this investment that is in accordance with AASB 3 Business Combinations and AASB 10 Consolidated Financial Statements?

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

75

What are the three key elements of the definition of control?

Enumerate several factors that may provide an indication of control.

Enumerate several factors that may provide an indication of control.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

76

Directors have determined that goodwill acquired in 2014 has been impaired by $5000.What is the appropriate elimination entry for this impairment?

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

77

Briefly outline the three main concepts of consolidation and how they differ.Identify the concept used in Australia and the implications this has for the consolidation accounting process.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

78

When an investee is classified as an associate which method of accounting is used to account for the investment?

A) proprietary method

B) acquisition method

C) equity method

D) parent-entity method

A) proprietary method

B) acquisition method

C) equity method

D) parent-entity method

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

79

When group members do not apply the same accounting methods,the consolidation process requires which of the following to be done?

A) All group members must change their accounting policies to be consistent.

B) Adjustments must be made on consolidation to remove the effects of the different policies.

C) Two sets of consolidated accounts need to be presented; the first done on the basis of the inconsistent policies, the second done after the subsidiaries have adjusted their policies in line with the parent.

D) A choice is to be made by the parent's management between any of the three other given answers.

A) All group members must change their accounting policies to be consistent.

B) Adjustments must be made on consolidation to remove the effects of the different policies.

C) Two sets of consolidated accounts need to be presented; the first done on the basis of the inconsistent policies, the second done after the subsidiaries have adjusted their policies in line with the parent.

D) A choice is to be made by the parent's management between any of the three other given answers.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

80

On 1 July 2012,Bob Ltd acquires all shares in Ted Ltd for $600 000.The fair value of net assets acquired is $500 000 comprising $400 000 in share capital and $100 000 in retained earnings.What is the appropriate elimination entry for this investment that is in accordance with AASB 3 Business Combinations and AASB 10 Consolidated Financial Statements?

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 87 flashcards in this deck.