Deck 17: Audit Sampling for Tests of Details of Balances

Full screen (f)

Question

Question

Question

Question

Question

Tolerable misstatement is used to

A)

B)

C)

D)

A)

B)

C)

D)

Question

Question

Tests for rates of occurrence are appropriately used in all but which of the following situations?

A)

B)

C)

D)

A)

B)

C)

D)

Question

Question

Question

Question

Question

Question

Both sampling and nonsampling risks are associated with

A)

B)

C)

D)

A)

B)

C)

D)

Question

Question

Question

Question

Question

Question

What is the purpose of applying stratified sampling to a population?

A)

B)

C)

D)

A)

B)

C)

D)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

An auditor using nonstatistical sampling cannot formally measure sampling error and therefore must subjectively consider the possibility that the true population misstatement exceeds a tolerable amount. Which of the following factors should be considered by the auditor in making this assessment?

A)

B)

C)

D)

A)

B)

C)

D)

Question

Question

Question

Which of the following needs to be considered when the auditor generalizes from the sample to the population?

A)

B)

C)

D)

A)

B)

C)

D)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

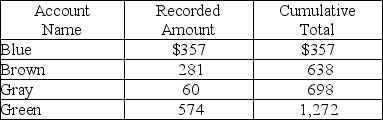

An accounts receivable population contains a total of four customers. The accounts, the amounts, and the cumulative total are shown below. Monetary unit sampling is to be used.  Based on the information above, the population size is

Based on the information above, the population size is

A) 4.

B) 574.

C) 1,272.

D) 2,684.

Based on the information above, the population size isA) 4.

B) 574.

C) 1,272.

D) 2,684.

Question

Question

Question

Question

Question

The auditor must consider the possibility that the true population misstatement is greater than the amount of misstatement that is tolerable when the auditor is performing

A)

B)

C)

D)

A)

B)

C)

D)

Question

Which of the following item(s) are needed to determine the sample size using MUS?

A)

B)

C)

D)

A)

B)

C)

D)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/130

Play

Full screen (f)

Deck 17: Audit Sampling for Tests of Details of Balances

1

If an auditor desires a greater level of assurance in auditing a balance, the acceptable risk of incorrect acceptance

A) is reduced.

B) is increased.

C) is not changed.

D) may be reduced or increased depending upon other circumstances.

A) is reduced.

B) is increased.

C) is not changed.

D) may be reduced or increased depending upon other circumstances.

A

2

When selecting a sample size for substantive tests of balances which factor, other factors being equal, would result in a larger sample?

A) a decrease in the tolerable misstatement

B) small expected misstatements

C) an increase in the tolerable misstatement

D) an increase in the acceptable risk of incorrect acceptance

A) a decrease in the tolerable misstatement

B) small expected misstatements

C) an increase in the tolerable misstatement

D) an increase in the acceptable risk of incorrect acceptance

A

3

The word below that best explains the relationship between required sample size and the acceptable risk of incorrect acceptance is

A) inverse.

B) direct.

C) proportional.

D) indeterminate.

A) inverse.

B) direct.

C) proportional.

D) indeterminate.

A

4

The auditor's principal objective when using a sample of tests of details of balances is whether the

A) account balance being audited is fairly stated.

B) transactions being audited are free of misstatements.

C) controls being tested are operating effectively.

D) transactions and account balances being audited are fairly stated.

A) account balance being audited is fairly stated.

B) transactions being audited are free of misstatements.

C) controls being tested are operating effectively.

D) transactions and account balances being audited are fairly stated.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

5

Tolerable misstatement is used to

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

6

In the test of details of balances, the auditor wants to make inferences about the entire population based on a sample.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

7

Tests for rates of occurrence are appropriately used in all but which of the following situations?

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

8

To address sampling risk, auditors can use either nonstatistical or statistical methods for tests of controls, substantive tests of transactions, and test of details of balances.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

9

Auditors perform test of controls and substantive tests of transactions for several reasons. Which of the following is not one of those reasons?

A) for larger public company audits, to conclude the control is operating effectively

B) to reduce assessed control risk and thereby reduce tests of details of balances

C) to determine whether the exception rate in the population is sufficiently low

D) to use rate of occurrence tests in the tests of details of balances

A) for larger public company audits, to conclude the control is operating effectively

B) to reduce assessed control risk and thereby reduce tests of details of balances

C) to determine whether the exception rate in the population is sufficiently low

D) to use rate of occurrence tests in the tests of details of balances

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

10

Auditors generally use rate of occurrence tests in tests of details of balances.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

11

The most important difference among tests of controls, substantive tests of transactions, and tests of details of balances lies in what the auditor wants to measure. Explain what each type of test attempts to measure.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

12

If an auditor concludes that internal controls are likely to be effective, the preliminary assessment of control risk can be reduced, leading to which of the following impacts on the acceptable risk of incorrect acceptance?

A) The acceptable risk of incorrect acceptance will be reduced.

B) The acceptable risk of incorrect acceptance will be increased.

C) The acceptable risk of incorrect acceptance will be eliminated.

D) The acceptable risk of incorrect acceptance will not be impacted.

A) The acceptable risk of incorrect acceptance will be reduced.

B) The acceptable risk of incorrect acceptance will be increased.

C) The acceptable risk of incorrect acceptance will be eliminated.

D) The acceptable risk of incorrect acceptance will not be impacted.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

13

Both sampling and nonsampling risks are associated with

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

14

If acceptable audit risk is increased, acceptable risk of incorrect acceptance should be

A) increased.

B) reduced.

C) unaffected.

D) modified.

A) increased.

B) reduced.

C) unaffected.

D) modified.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

15

Sampling, not nonsampling risks, are important for tests of controls, substantive tests of transaction, and test of details of balances.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

16

In estimating the population misstatement, the first step in projecting from the sample to the population is to

A) make a point estimate.

B) revise the upper error bound.

C) calculate the precision interval.

D) determine the population mean.

A) make a point estimate.

B) revise the upper error bound.

C) calculate the precision interval.

D) determine the population mean.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

17

The final step in the evaluation of the audit results is the decision to

A) accept the population as fairly stated or to require further action.

B) determine sampling error and calculate the estimated total population error.

C) project the point estimate.

D) determine the error in each sample.

A) accept the population as fairly stated or to require further action.

B) determine sampling error and calculate the estimated total population error.

C) project the point estimate.

D) determine the error in each sample.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

18

Which of the following does not have to be considered in determining the initial sample size of a test of details?

A) tolerable misstatement

B) acceptable risk of incorrect rejection

C) estimate of misstatements in the population

D) inherent risk

A) tolerable misstatement

B) acceptable risk of incorrect rejection

C) estimate of misstatements in the population

D) inherent risk

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

19

What is the purpose of applying stratified sampling to a population?

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

20

When using sampling methods, the auditor is focused on obtaining results in dollar terms.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

21

One of the steps involved in planning the sample for the tests of details of balances is to

A) select the sample.

B) perform the audit procedures.

C) define a misstatement.

D) analyze the misstatements.

A) select the sample.

B) perform the audit procedures.

C) define a misstatement.

D) analyze the misstatements.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

22

When errors are found in a sample, auditors in practice generally assume

A) that the population errors cannot be determined.

B) that the population errors are larger than the sample errors.

C) that the population errors are smaller than the sample errors.

D) that the actual sample errors are representative of the population errors.

A) that the population errors cannot be determined.

B) that the population errors are larger than the sample errors.

C) that the population errors are smaller than the sample errors.

D) that the actual sample errors are representative of the population errors.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

23

When analyzing misstatements, the auditor will determine

A) the implications of the misstatements on other audit areas.

B) the potential impact on the financial statements.

C) the effect on company operations.

D) all of the above.

A) the implications of the misstatements on other audit areas.

B) the potential impact on the financial statements.

C) the effect on company operations.

D) all of the above.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

24

Which of the following conditions would lead to a larger sample size?

A) larger tolerable misstatement

B) low inherent risk

C) high control risk

D) smaller account balance

A) larger tolerable misstatement

B) low inherent risk

C) high control risk

D) smaller account balance

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

25

If no exceptions were found in the substantive tests of transactions,

A) ARIA would stay the same.

B) the sample size would stay the same.

C) ARIA would increase.

D) the sample size would increase.

A) ARIA would stay the same.

B) the sample size would stay the same.

C) ARIA would increase.

D) the sample size would increase.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

26

Which of the following would lead to a larger sample size?

A) low inherent risk

B) low control risk

C) larger tolerable misstatement

D) unsatisfactory results in other related substantive procedures

A) low inherent risk

B) low control risk

C) larger tolerable misstatement

D) unsatisfactory results in other related substantive procedures

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

27

If the population is not considered acceptable, one step the auditor is likely to take is to

A) retest all internal controls.

B) ask the client to adjust the account balance.

C) test the entire population.

D) decrease inherent risk.

A) retest all internal controls.

B) ask the client to adjust the account balance.

C) test the entire population.

D) decrease inherent risk.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

28

While performing a substantive test of details during an audit, the auditor determined that the sample results supported the conclusion that the recorded account balance was not materially misstated. It was, in fact, materially misstated. This situation illustrates the risk of

A) incorrect rejection.

B) incorrect acceptance.

C) assessing control risk too low.

D) assessing control risk too high.

A) incorrect rejection.

B) incorrect acceptance.

C) assessing control risk too low.

D) assessing control risk too high.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

29

________ is a method of projecting from the sample to the population to estimate the population misstatement. It assumes that misstatements in the unaudited population are proportional to the misstatements found in the sample.

A) Mean-per-unit estimation

B) Point estimate

C) Monetary unit

D) Basic precision

A) Mean-per-unit estimation

B) Point estimate

C) Monetary unit

D) Basic precision

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

30

As the amount of misstatements expected in the population approaches tolerable misstatement, the planned sample size will

A) decrease.

B) increase.

C) vary based on characteristics of the population.

D) be unaffected.

A) decrease.

B) increase.

C) vary based on characteristics of the population.

D) be unaffected.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

31

Factors considered by an auditor to determine the possibility that the true population misstatement exceeds a tolerable amount in a nonstatistical sample include all of the following except for

A) the extent to which items in the population have been audited 100%.

B) the difference between the point estimate and acceptable control risk.

C) whether misstatements tend to be offsetting or in only one direction.

D) the amounts of individual misstatements.

A) the extent to which items in the population have been audited 100%.

B) the difference between the point estimate and acceptable control risk.

C) whether misstatements tend to be offsetting or in only one direction.

D) the amounts of individual misstatements.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

32

The risk the auditor is willing to take of accepting a balance as correct when the true misstatement in the balance under audit is greater than the tolerable misstatement is

A) the upper bound.

B) the tolerable risk.

C) the acceptable risk of incorrect acceptance.

D) the lower bound.

A) the upper bound.

B) the tolerable risk.

C) the acceptable risk of incorrect acceptance.

D) the lower bound.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

33

While performing a substantive test of details during an audit, the auditor determined that the sample results supported the conclusion that the recorded account balance was materially misstated. Which of the following is the least likely auditor reaction to this discovery?

A) perform expanded audit tests in the relevant areas

B) increase detection risk in the relevant areas

C) increase the sample size

D) take no action until tests of other audit areas are completed

A) perform expanded audit tests in the relevant areas

B) increase detection risk in the relevant areas

C) increase the sample size

D) take no action until tests of other audit areas are completed

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

34

When defining the population and the sampling unit for tests of details of balances,

A) the population is defined as all of the transactions in the journal for the period.

B) the sampling unit must be the same for all balance sheet accounts.

C) if sampling for completeness, the sampling unit will be customers with zero balances.

D) if sampling for completeness, the sampling unit will be the items making up the recorded population.

A) the population is defined as all of the transactions in the journal for the period.

B) the sampling unit must be the same for all balance sheet accounts.

C) if sampling for completeness, the sampling unit will be customers with zero balances.

D) if sampling for completeness, the sampling unit will be the items making up the recorded population.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

35

If analytical procedures are performed with no indications of likely misstatements, ARIA will ________ and the sample size will ________.

A) remain the same; increase

B) decrease; decrease

C) increase; decrease

D) decrease; increase

A) remain the same; increase

B) decrease; decrease

C) increase; decrease

D) decrease; increase

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

36

An auditor using nonstatistical sampling cannot formally measure sampling error and therefore must subjectively consider the possibility that the true population misstatement exceeds a tolerable amount. Which of the following factors should be considered by the auditor in making this assessment?

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

37

Which of the following is an accurate statement regarding how the acceptable risk of overreliance (ARO) and the acceptable risk of incorrect acceptance (ARIA) interact to affect evidence accumulation?

A) If internal controls are likely to be effective, preliminary control risk can be increased.

B) A lower control risk requires a lower ARO in testing the controls, which requires a smaller sample size.

C) If controls are found to be effective, control risk can remain low, which permits the auditor to increase ARIA, thereby requiring a smaller sample size in the substantive tests of details of balances.

D) If misstatements are considered unlikely, ARIA will decrease, and the sample size will also decrease.

A) If internal controls are likely to be effective, preliminary control risk can be increased.

B) A lower control risk requires a lower ARO in testing the controls, which requires a smaller sample size.

C) If controls are found to be effective, control risk can remain low, which permits the auditor to increase ARIA, thereby requiring a smaller sample size in the substantive tests of details of balances.

D) If misstatements are considered unlikely, ARIA will decrease, and the sample size will also decrease.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

38

You are auditing Raji and Company. You discover an item of inventory with an audited value of $5,000 with a recorded amount of $3,000. If this is the only error you discover, the projected misstatement for the sample would be

A) $5,000.

B) $2,000.

C) $3,000.

D) $4,000.

A) $5,000.

B) $2,000.

C) $3,000.

D) $4,000.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

39

Which of the following needs to be considered when the auditor generalizes from the sample to the population?

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

40

Which of the following is a correct statement?

A) When internal controls are effective, control risk can be reduced, and therefore the auditor will decrease the ARIA.

B) There is a direct relationship between ARIA and the required sample size.

C) A lower control risk requires a lower ARO in testing the controls.

D) ARO measures the auditor's desired assurance for an account balance.

A) When internal controls are effective, control risk can be reduced, and therefore the auditor will decrease the ARIA.

B) There is a direct relationship between ARIA and the required sample size.

C) A lower control risk requires a lower ARO in testing the controls.

D) ARO measures the auditor's desired assurance for an account balance.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

41

The primary factor affecting the auditor's decision about acceptable risk of incorrect acceptance (ARIA) is assessed inherent risk.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

42

An increased sample size will always cause the population to be accepted.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

43

Acceptable risk of incorrect acceptance (ARIA) and sample size are inversely related; that is, as ARIA increases, sample size decreases.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

44

The larger the sample size, the more confident the auditor can be that the point estimate is close to the true population value.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

45

If a population is not considered acceptable, and the analysis indicates an individual error is unique or most of the misstatements are of a specific type, it may be appropriate to restrict the additional audit effort to the problem area.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

46

Acceptable risk of incorrect acceptance is directly affected by acceptable audit risk.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

47

The auditor may be able to use computer software to test the accuracy of each customer's account balance by taking each customer's beginning balance, adding sales made on account, subtracting payments received, and adding/subtracting other account adjustments to calculate each customer's ending balance.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

48

Acceptable audit risk and acceptable risk of incorrect acceptance are inversely related; that is, as AAR increases, ARIA decreases.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

49

The auditor must do misstatement analysis to decide whether any modification of the audit risk model is needed.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

50

In stratified sampling, a maximum of four stratum can be used.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

51

An auditor using nonstatistical sampling cannot formally measure sampling error.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

52

Estimated misstatement in the population and sample size are inversely related; that is, as estimated misstatement increases, sample size decreases.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

53

Tolerable misstatement is inversely related to sample size.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

54

Auditors may find that the use of data analysis techniques allows them to test the entire population of an account balance for certain audit objectives.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

55

When using audit sampling for tests of details of balances, the acceptable risk of overreliance must be determined.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

56

There are 14 steps to audit sampling for tests of details of balances, divided into three sections: plan the sample, select the sample and perform the audit procedures, and evaluate the results. Discuss each of the steps included in the "evaluate the results" section for nonstatistical sampling.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

57

The purpose of stratification is to permit auditors to emphasize certain aspects of a population and deemphasize others.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

58

ARIA measures the auditor's desired assurance for an account balance.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

59

If the misstatement in a population is larger than tolerable misstatement without considering sampling error, the population will be considered unacceptable.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

60

Required sample size increases as the auditor's tolerable misstatement for an account balance or class of transactions decreases.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

61

When using monetary unit sampling, evaluating the likelihood of unrecorded items in the population is

A) unnecessary.

B) impossible.

C) possible but difficult.

D) an automatic outcome of the process.

A) unnecessary.

B) impossible.

C) possible but difficult.

D) an automatic outcome of the process.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

62

Identify each of the seven factors that influence sample size for nonstatistical tests of details of balances, and state whether each factor is directly or inversely related to sample size.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

63

Monetary unit sampling is not particularly effective at detecting

A) overstatements.

B) understatements.

C) errors in current assets.

D) errors in noncurrent assets.

A) overstatements.

B) understatements.

C) errors in current assets.

D) errors in noncurrent assets.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

64

An accounts receivable population contains a total of four customers. The accounts, the amounts, and the cumulative total are shown below. Monetary unit sampling is to be used. Based on the information above, the population size is

A) 4.

B) 574.

C) 1,272.

D) 2,684.

Based on the information above, the population size isA) 4.

B) 574.

C) 1,272.

D) 2,684.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

65

An auditor uses monetary unit sampling with a sampling interval of $20,000 and detects an item with a recorded amount of $10,000 with an audited value of $4,000. The projected misstatement of the sample is

A) $12,000.

B) $6,000.

C) $10,000.

D) $3,000.

A) $12,000.

B) $6,000.

C) $10,000.

D) $3,000.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

66

The most commonly used method of statistical sampling for tests of details of balances is

A) attributes sampling.

B) systematic sampling.

C) discovery sampling.

D) monetary unit sampling.

A) attributes sampling.

B) systematic sampling.

C) discovery sampling.

D) monetary unit sampling.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

67

Consider the steps in sampling for tests of details and for tests of controls. Explain the differences in applying sampling to these two types of tests.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

68

The statistical methods used to evaluate monetary unit samples

A) neither exclude nor include units twice.

B) may permit the inclusion of a unit in the sample more than once.

C) do not permit a unit to be included in the sample more than once.

D) ignore the possibility that a unit may be included in a sample more than once.

A) neither exclude nor include units twice.

B) may permit the inclusion of a unit in the sample more than once.

C) do not permit a unit to be included in the sample more than once.

D) ignore the possibility that a unit may be included in a sample more than once.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

69

The auditor must consider the possibility that the true population misstatement is greater than the amount of misstatement that is tolerable when the auditor is performing

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

70

Which of the following item(s) are needed to determine the sample size using MUS?

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

71

When the sample selection is done using probability proportional to size sample selection (PPS),

A) the actual number of units selected for testing may be more than the computed sample size.

B) the auditor must use systematic selection, rather than random selection of dollars.

C) population items with a zero recorded balance have no chance of being selected.

D) negative balances must be treated as positive balances.

A) the actual number of units selected for testing may be more than the computed sample size.

B) the auditor must use systematic selection, rather than random selection of dollars.

C) population items with a zero recorded balance have no chance of being selected.

D) negative balances must be treated as positive balances.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

72

PPS samples can be obtained in an efficient manner using all but which of the following?

A) hand selection by the auditor

B) computer software

C) random number tables

D) systematic sampling techniques

A) hand selection by the auditor

B) computer software

C) random number tables

D) systematic sampling techniques

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

73

An auditor is confirming a population of accounts receivable for monetary correctness. The population totals $2,000,000 and a sample of 200 confirmations is obtained. Upon audit, no misstatements are uncovered in the sample. Assuming an ARIA of 10%, the confidence factor would be 2.31. Applied to a sampling interval of $10,000, the upper misstatement bound is calculated as

A) $462.

B) $4,329.

C) $23,100.

D) $865,801.

A) $462.

B) $4,329.

C) $23,100.

D) $865,801.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

74

Which balance-related audit objective cannot be assessed using monetary unit sampling?

A) accuracy

B) completeness

C) existence

D) All of the above can be assessed using monetary unit sampling.

A) accuracy

B) completeness

C) existence

D) All of the above can be assessed using monetary unit sampling.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

75

In monetary unit sampling, a sampling interval of 900 means that

A) every 900th item will be selected.

B) every 900th dollar in the account will be sampled.

C) expected misstatement is 900.

D) tolerable misstatement is 900.

A) every 900th item will be selected.

B) every 900th dollar in the account will be sampled.

C) expected misstatement is 900.

D) tolerable misstatement is 900.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

76

When using nonstatistical sampling, the auditor must subjectively consider whether the true population misstatement exceeds a tolerable amount. This is done by considering five factors. One factor is the difference between the point estimate and tolerable misstatement. State the other four factors the auditor must consider.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

77

There are 14 steps to audit sampling for tests of details of balances, divided into three sections: plan the sample, select the sample and perform the audit procedures, and evaluate the results. Discuss 5 of the 9 steps included in the "plan the sample" section for nonstatistical sampling.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

78

When using monetary unit sampling, the recorded dollar population is a definition of all the items in the

A) population.

B) population which the auditor has included in the sample.

C) population which contain errors.

D) sample which contain errors.

A) population.

B) population which the auditor has included in the sample.

C) population which contain errors.

D) sample which contain errors.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

79

An estimate of the largest likely overstatement in a population at a given ARIA, using monetary unit sampling is the

A) point estimates.

B) precision intervals.

C) confidence intervals.

D) misstatement bound.

A) point estimates.

B) precision intervals.

C) confidence intervals.

D) misstatement bound.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

80

Discuss each of the six possible courses of action the auditor can take when he or she has concluded that the population is misstated by more than a tolerable amount.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 130 flashcards in this deck.