Deck 21: Forward and Futures Contracts

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

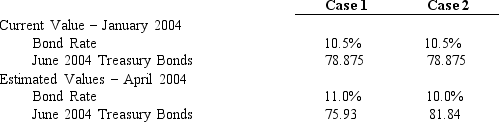

Exhibit 21.1

Use the Information Below for the Following Problem(S)

In late January 2004, The Union Cosmos Company is considering the sale of $100 million in 10-year debentures that will probably be rated AAA like the firm's other bond issues. The firm is anxious to proceed at today's rate of 10.5 percent. As treasurer, you know that it will take until sometime in April to get the issue registered and sold. Therefore, you suggest that the firm hedge the pending issue using Treasury bond futures contracts each representing $100,000.

Refer to Exhibit 21.1.Explain how you would go about hedging the bond issue?

A) Sell 1,000 contracts

B) Buy 1,000 contracts

C) Sell 100 contracts

D) Sell 10,000 contracts

E) None of the above

Use the Information Below for the Following Problem(S)

In late January 2004, The Union Cosmos Company is considering the sale of $100 million in 10-year debentures that will probably be rated AAA like the firm's other bond issues. The firm is anxious to proceed at today's rate of 10.5 percent. As treasurer, you know that it will take until sometime in April to get the issue registered and sold. Therefore, you suggest that the firm hedge the pending issue using Treasury bond futures contracts each representing $100,000.

Refer to Exhibit 21.1.Explain how you would go about hedging the bond issue?

A) Sell 1,000 contracts

B) Buy 1,000 contracts

C) Sell 100 contracts

D) Sell 10,000 contracts

E) None of the above

Question

Question

Question

Exhibit 21.1

Use the Information Below for the Following Problem(S)

In late January 2004, The Union Cosmos Company is considering the sale of $100 million in 10-year debentures that will probably be rated AAA like the firm's other bond issues. The firm is anxious to proceed at today's rate of 10.5 percent. As treasurer, you know that it will take until sometime in April to get the issue registered and sold. Therefore, you suggest that the firm hedge the pending issue using Treasury bond futures contracts each representing $100,000.

Refer to Exhibit 21.1.What is the dollar gain or loss assuming that future conditions described in Case 2 actually occur? (Ignore commissions and margin costs,and assume a naive hedge ratio.)

A) $2,965,000.00 gain

B) $45,500.00 gain

C) $2,965,000.00 loss

D) $45,500.00 loss

E) None of the above

Use the Information Below for the Following Problem(S)

In late January 2004, The Union Cosmos Company is considering the sale of $100 million in 10-year debentures that will probably be rated AAA like the firm's other bond issues. The firm is anxious to proceed at today's rate of 10.5 percent. As treasurer, you know that it will take until sometime in April to get the issue registered and sold. Therefore, you suggest that the firm hedge the pending issue using Treasury bond futures contracts each representing $100,000.

Refer to Exhibit 21.1.What is the dollar gain or loss assuming that future conditions described in Case 2 actually occur? (Ignore commissions and margin costs,and assume a naive hedge ratio.)

A) $2,965,000.00 gain

B) $45,500.00 gain

C) $2,965,000.00 loss

D) $45,500.00 loss

E) None of the above

Question

Question

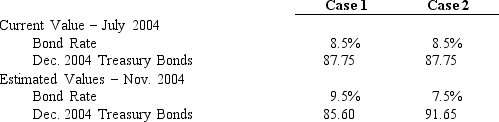

Exhibit 21.2

Use the Information Below for the Following Problem(S)

Assume you are the Treasurer for the Johnson Pharmaceutical Company and in late July 2004, the company is considering the sale of $500 million in 20-year debentures that will most likely be rated the same as the firm's other debt issues. The firm would like to proceed at the current rate of 8.5%, but you know that it will probably take until November to bring the issue to market. Therefore, you suggest that the firm hedge the pending issue using Treasury bond futures contracts which each represent $100,000.

Refer to Exhibit 21.2.What is the dollar gain or loss assuming that future conditions described in Case 1 actually occur? (Ignore commissions and margin costs,and assume a naive hedge ratio.)

A) $47,316,683.00 gain

B) $36,566,683.00 loss

C) $10,750,000.00 gain

D) $10,750,000.00 loss

E) None of the above

Use the Information Below for the Following Problem(S)

Assume you are the Treasurer for the Johnson Pharmaceutical Company and in late July 2004, the company is considering the sale of $500 million in 20-year debentures that will most likely be rated the same as the firm's other debt issues. The firm would like to proceed at the current rate of 8.5%, but you know that it will probably take until November to bring the issue to market. Therefore, you suggest that the firm hedge the pending issue using Treasury bond futures contracts which each represent $100,000.

Refer to Exhibit 21.2.What is the dollar gain or loss assuming that future conditions described in Case 1 actually occur? (Ignore commissions and margin costs,and assume a naive hedge ratio.)

A) $47,316,683.00 gain

B) $36,566,683.00 loss

C) $10,750,000.00 gain

D) $10,750,000.00 loss

E) None of the above

Question

Question

Exhibit 21.2

Use the Information Below for the Following Problem(S)

Assume you are the Treasurer for the Johnson Pharmaceutical Company and in late July 2004, the company is considering the sale of $500 million in 20-year debentures that will most likely be rated the same as the firm's other debt issues. The firm would like to proceed at the current rate of 8.5%, but you know that it will probably take until November to bring the issue to market. Therefore, you suggest that the firm hedge the pending issue using Treasury bond futures contracts which each represent $100,000.

Refer to Exhibit 21.2.How you would go about hedging the bond issue?

A) Buy 5,000 contracts

B) Buy 50,000 contracts

C) Sell 5,000,000 contracts

D) Sell 5,000 contracts

E) None of the above

Use the Information Below for the Following Problem(S)

Assume you are the Treasurer for the Johnson Pharmaceutical Company and in late July 2004, the company is considering the sale of $500 million in 20-year debentures that will most likely be rated the same as the firm's other debt issues. The firm would like to proceed at the current rate of 8.5%, but you know that it will probably take until November to bring the issue to market. Therefore, you suggest that the firm hedge the pending issue using Treasury bond futures contracts which each represent $100,000.

Refer to Exhibit 21.2.How you would go about hedging the bond issue?

A) Buy 5,000 contracts

B) Buy 50,000 contracts

C) Sell 5,000,000 contracts

D) Sell 5,000 contracts

E) None of the above

Question

Exhibit 21.2

Use the Information Below for the Following Problem(S)

Assume you are the Treasurer for the Johnson Pharmaceutical Company and in late July 2004, the company is considering the sale of $500 million in 20-year debentures that will most likely be rated the same as the firm's other debt issues. The firm would like to proceed at the current rate of 8.5%, but you know that it will probably take until November to bring the issue to market. Therefore, you suggest that the firm hedge the pending issue using Treasury bond futures contracts which each represent $100,000.

Refer to Exhibit 21.2.What is the dollar gain or loss assuming that future conditions described in Case 2 actually occur? (Ignore commissions and margin costs,and assume a naive hedge ratio.)

A) $19,500,000.00 gain

B) $27,816,683.04 gain

C) $27,816,683.04 loss

D) $19,500,000.00 loss

E) None of the above

Use the Information Below for the Following Problem(S)

Assume you are the Treasurer for the Johnson Pharmaceutical Company and in late July 2004, the company is considering the sale of $500 million in 20-year debentures that will most likely be rated the same as the firm's other debt issues. The firm would like to proceed at the current rate of 8.5%, but you know that it will probably take until November to bring the issue to market. Therefore, you suggest that the firm hedge the pending issue using Treasury bond futures contracts which each represent $100,000.

Refer to Exhibit 21.2.What is the dollar gain or loss assuming that future conditions described in Case 2 actually occur? (Ignore commissions and margin costs,and assume a naive hedge ratio.)

A) $19,500,000.00 gain

B) $27,816,683.04 gain

C) $27,816,683.04 loss

D) $19,500,000.00 loss

E) None of the above

Question

Question

Question

Question

Question

Question

Question

Question

Exhibit 21.1

Use the Information Below for the Following Problem(S)

In late January 2004, The Union Cosmos Company is considering the sale of $100 million in 10-year debentures that will probably be rated AAA like the firm's other bond issues. The firm is anxious to proceed at today's rate of 10.5 percent. As treasurer, you know that it will take until sometime in April to get the issue registered and sold. Therefore, you suggest that the firm hedge the pending issue using Treasury bond futures contracts each representing $100,000.

Refer to Exhibit 21.1.What is the dollar gain or loss assuming that future conditions described in Case 1 actually occur? (Ignore commissions and margin costs,and assume a naive hedge ratio.)

A) $2,945,000.00 gain

B) $65,500.00 gain

C) $2,945,000.00 loss

D) $65,500.00 loss

E) None of the above

Use the Information Below for the Following Problem(S)

In late January 2004, The Union Cosmos Company is considering the sale of $100 million in 10-year debentures that will probably be rated AAA like the firm's other bond issues. The firm is anxious to proceed at today's rate of 10.5 percent. As treasurer, you know that it will take until sometime in April to get the issue registered and sold. Therefore, you suggest that the firm hedge the pending issue using Treasury bond futures contracts each representing $100,000.

Refer to Exhibit 21.1.What is the dollar gain or loss assuming that future conditions described in Case 1 actually occur? (Ignore commissions and margin costs,and assume a naive hedge ratio.)

A) $2,945,000.00 gain

B) $65,500.00 gain

C) $2,945,000.00 loss

D) $65,500.00 loss

E) None of the above

Question

Question

Question

Exhibit 21.6

Use the Information Below for the Following Problem(S)

Assume that you observe the following prices in the T-Bill and Eurodollar futures markets

Refer to Exhibit 21.6.If you expected the TED spread to widen over the next month then an appropriate strategy would be to

A) Go long T-Bill futures and long Eurodollar futures.

B) Go short T-Bill futures and short Eurodollar futures.

C) Go long T-Bill futures and short Eurodollar futures.

D) Go short T-Bill futures and long Eurodollar futures.

E) None of the above.

Use the Information Below for the Following Problem(S)

Assume that you observe the following prices in the T-Bill and Eurodollar futures markets

Refer to Exhibit 21.6.If you expected the TED spread to widen over the next month then an appropriate strategy would be to

A) Go long T-Bill futures and long Eurodollar futures.

B) Go short T-Bill futures and short Eurodollar futures.

C) Go long T-Bill futures and short Eurodollar futures.

D) Go short T-Bill futures and long Eurodollar futures.

E) None of the above.

Question

Question

Question

Question

Question

Exhibit 21.6

Use the Information Below for the Following Problem(S)

Assume that you observe the following prices in the T-Bill and Eurodollar futures markets

Refer to Exhibit 21.6.Assume that a month later the price of the September T-Bill future is 93 and the price of the Eurodollar future is 90.25.Calculate the profit on the Eurodollar futures position.

A) 190 basis points.

B) 210 basis points.

C) -190 basis points.

D) -210 basis points.

E) 100 basis points.

Use the Information Below for the Following Problem(S)

Assume that you observe the following prices in the T-Bill and Eurodollar futures markets

Refer to Exhibit 21.6.Assume that a month later the price of the September T-Bill future is 93 and the price of the Eurodollar future is 90.25.Calculate the profit on the Eurodollar futures position.

A) 190 basis points.

B) 210 basis points.

C) -190 basis points.

D) -210 basis points.

E) 100 basis points.

Question

Question

Question

Question

Exhibit 21.6

Use the Information Below for the Following Problem(S)

Assume that you observe the following prices in the T-Bill and Eurodollar futures markets

Refer to Exhibit 21.6.Assume that a month later the price of the September T-Bill future is 93 and the price of the Eurodollar future is 90.25.Calculate the profit on the T-Bill futures position.

A) 25 basis points.

B) 110 basis points.

C) -25 basis points.

D) -110 basis points.

E) 50 basis points.

Use the Information Below for the Following Problem(S)

Assume that you observe the following prices in the T-Bill and Eurodollar futures markets

Refer to Exhibit 21.6.Assume that a month later the price of the September T-Bill future is 93 and the price of the Eurodollar future is 90.25.Calculate the profit on the T-Bill futures position.

A) 25 basis points.

B) 110 basis points.

C) -25 basis points.

D) -110 basis points.

E) 50 basis points.

Question

Question

Exhibit 21.7

Use the Information Below for the Following Problem(S)

Assume that you observe the following prices in the T-Bill and Eurodollar futures markets

Refer to Exhibit 21.7.Assume that a month later the price of the September T-Bill future is 96.25 and the price of the Eurodollar future is 95.9.Calculate the profit on the Eurodollar futures position.

A) 101 basis points.

B) 130 basis points.

C) -101 basis points.

D) -130 basis points.

E) 29 basis points.

Use the Information Below for the Following Problem(S)

Assume that you observe the following prices in the T-Bill and Eurodollar futures markets

Refer to Exhibit 21.7.Assume that a month later the price of the September T-Bill future is 96.25 and the price of the Eurodollar future is 95.9.Calculate the profit on the Eurodollar futures position.

A) 101 basis points.

B) 130 basis points.

C) -101 basis points.

D) -130 basis points.

E) 29 basis points.

Question

Question

Exhibit 21.7

Use the Information Below for the Following Problem(S)

Assume that you observe the following prices in the T-Bill and Eurodollar futures markets

Refer to Exhibit 21.7.If you expected the TED spread to narrow over the next month then an appropriate strategy would be to

A) Go long T-Bill futures and long Eurodollar futures.

B) Go short T-Bill futures and short Eurodollar futures.

C) Go long T-Bill futures and short Eurodollar futures.

D) Go short T-Bill futures and long Eurodollar futures.

E) None of the above.

Use the Information Below for the Following Problem(S)

Assume that you observe the following prices in the T-Bill and Eurodollar futures markets

Refer to Exhibit 21.7.If you expected the TED spread to narrow over the next month then an appropriate strategy would be to

A) Go long T-Bill futures and long Eurodollar futures.

B) Go short T-Bill futures and short Eurodollar futures.

C) Go long T-Bill futures and short Eurodollar futures.

D) Go short T-Bill futures and long Eurodollar futures.

E) None of the above.

Question

Exhibit 21.7

Use the Information Below for the Following Problem(S)

Assume that you observe the following prices in the T-Bill and Eurodollar futures markets

Refer to Exhibit 21.7.Assume that a month later the price of the September T-Bill future is 96.25 and the price of the Eurodollar future is 95.9.Calculate the profit on the T-Bill futures position.

A) 101 basis points.

B) 130 basis points.

C) -101 basis points.

D) -130 basis points.

E) 29 basis points.

Use the Information Below for the Following Problem(S)

Assume that you observe the following prices in the T-Bill and Eurodollar futures markets

Refer to Exhibit 21.7.Assume that a month later the price of the September T-Bill future is 96.25 and the price of the Eurodollar future is 95.9.Calculate the profit on the T-Bill futures position.

A) 101 basis points.

B) 130 basis points.

C) -101 basis points.

D) -130 basis points.

E) 29 basis points.

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/99

Play

Full screen (f)

Deck 21: Forward and Futures Contracts

1

Some forward contracts,particularly in the foreign exchange market,are quite standard and liquid.

True

2

According to the cost of carry model the futures price is the present value of the spot price discounted at the risk free rate.

False

3

Since futures contracts are "marked-to-market" daily,the gains and losses are settled daily.

True

4

The goal of a hedge transaction is to increase expected returns of a fundamental holding.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

5

Like hedging,arbitrage results in increased returns with a disproportional increase in risk.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

6

The inclusion of dividends in the cost of carry model will increase the futures price.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

7

The basis is the spot price minus the future price.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

8

A riskless stock index arbitrage profit is possible if the following condition holds: F₀,T = S₀(1 + rf - d)ᵀ,where spot price now is S₀,value now of a futures contract expiring at time T is (F₀,T),rf is the risk free rate and d is the dividend.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

9

The basis (Bt,T)at time t between the spot price (St)and a futures contract expiring at time T (t,T)is: St - Ft,T.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

10

In the cost of carry model the inclusion of storage costs will increase the futures price.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

11

The cost-of-carry model is useful for pricing future contracts.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

12

Forward contracts are individually designed agreements,and can be tailored to the specific needs of the ultimate end-user.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

13

Interest rate parity is a key concept in managing risk in the commodities market.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

14

If you were bearish on the near term outlook for the stock market but did not want to sell your portfolio,you could hedge against the decline by selling stock index futures.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

15

If you have entered into a currency futures hedge for the Japanese yen in connection with buying Japanese equipment,if the yen goes from 110 yen/$1 to 100 yen/$1,you will lose in the spot market but have an offsetting gain in the futures market.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

16

In the absence of arbitrage opportunities,the forward price should be equal to the spot price plus the cost of carry.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

17

Stock index futures are useful in providing a hedge against movements in an underlying financial asset.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

18

Like future contracts,all forward contracts are processed by a clearing corporation.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

19

The number of future contracts needed to hedge a unit of the spot assets is solely a function of the variance of the spot prices.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

20

The pure expectations hypothesis suggests futures prices serve as unbiased forecasts of future spot prices.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

21

A riskless stock index arbitrage profit is possible if the following condition holds:

A) F0,T = S0(1 + rf - d)T

B) F0,T > S0(1 + rf - d)T

C) F0,T < S0(1 + rf - d)T

D) a and b

E) b and c

A) F0,T = S0(1 + rf - d)T

B) F0,T > S0(1 + rf - d)T

C) F0,T < S0(1 + rf - d)T

D) a and b

E) b and c

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

22

The process by which invest on margin accounts are credited or debited to reflect daily trading gains or losses is referred to as the ____ process.

A) Hedge rationing

B) Daily settlement

C) Marked-to-market

D) Book-to-market

E) Account realization

A) Hedge rationing

B) Daily settlement

C) Marked-to-market

D) Book-to-market

E) Account realization

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

23

The bond that maximizes the difference between the invoice price and the delivery price is referred to as the

A) Cheapest-to-deliver.

B) Conversion bond.

C) Delivery bond.

D) Cheapest to substitute.

E) Cost-of-carry.

A) Cheapest-to-deliver.

B) Conversion bond.

C) Delivery bond.

D) Cheapest to substitute.

E) Cost-of-carry.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

24

The major difference between valuing futures versus forward contracts stems from the fact that future contracts are

A) Traded on exchange.

B) Backed by a clearinghouse.

C) Marked-to-market daily.

D) Less risky.

E) Relatively inflexible.

A) Traded on exchange.

B) Backed by a clearinghouse.

C) Marked-to-market daily.

D) Less risky.

E) Relatively inflexible.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

25

The Eurodollar futures contract is a popular hedging vehicle because it is based on the three-month LIBOR.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

26

Which of the following statements is true?

A) The buyer of a forward contract is said to be long forward.

B) The seller of a forward contract is said to be short forward.

C) The seller of a forward contract is said to be long forward.

D) The buyer of a forward contract is said to be short forward.

E) Choices a and b

A) The buyer of a forward contract is said to be long forward.

B) The seller of a forward contract is said to be short forward.

C) The seller of a forward contract is said to be long forward.

D) The buyer of a forward contract is said to be short forward.

E) Choices a and b

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

27

A backwardated futures market occurs when

A) F0,T < S0

B) F0,T = S0

C) F0,T > S0

D) F0,T > E( ST)

E) F0,T > ST

A) F0,T < S0

B) F0,T = S0

C) F0,T > S0

D) F0,T > E( ST)

E) F0,T > ST

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

28

The main tradeoff between forward and future contracts is

A) Design flexibility.

B) Credit risk.

C) Liquidity risk.

D) All of the above.

E) Choices a and b only

A) Design flexibility.

B) Credit risk.

C) Liquidity risk.

D) All of the above.

E) Choices a and b only

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

29

The inclusion of the following in the cost of carry model will increase the futures price

A) Dividends

B) Storage costs

C) Interest rate

D) a and b

E) None of the above

A) Dividends

B) Storage costs

C) Interest rate

D) a and b

E) None of the above

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

30

The most popular financial futures in terms of average daily volume is the

A) OEX contracts.

B) S&P 500 contracts.

C) LIBOR contracts.

D) T-bill contracts.

E) T-bond contracts.

A) OEX contracts.

B) S&P 500 contracts.

C) LIBOR contracts.

D) T-bill contracts.

E) T-bond contracts.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

31

Financial futures have become an increasingly attractive investment alternative since the Chicago Board of Trade (CBOT)began trading them in 1977,and their hedging function partly accounts for the growth in trading.Which of the following statements concerning financial futures is true?

A) Financial futures protect the investment portfolio against inflation in the economy.

B) Investors seek protection against the increasing volatility of interest rates.

C) Unlike commodity futures, factors that influence price shifts are not supply and demand of the commodity but buyer psychology.

D) A reason for their popularity is that trading is restricted to government obligations, which reduces risks.

E) All of the above are true statements

A) Financial futures protect the investment portfolio against inflation in the economy.

B) Investors seek protection against the increasing volatility of interest rates.

C) Unlike commodity futures, factors that influence price shifts are not supply and demand of the commodity but buyer psychology.

D) A reason for their popularity is that trading is restricted to government obligations, which reduces risks.

E) All of the above are true statements

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

32

In the absence of arbitrage opportunities,the forward contract price should be equal to the current price plus

A) Contract price.

B) The cost of carry.

C) Margin requirement.

D) The price discovery rate.

E) The convenience return.

A) Contract price.

B) The cost of carry.

C) Margin requirement.

D) The price discovery rate.

E) The convenience return.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

33

An investor in a hedge position is no longer exposed to the absolute price movement of the underlying asset,but the investor is still exposed to basis risk.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

34

The optimal hedge ratio is a function of all of the following except

A) The standard deviation of changes in spot prices.

B) The variance deviation of changes in forward prices.

C) The covariance between changes in spot and forward prices.

D) Choices a and b only

E) All of the above

A) The standard deviation of changes in spot prices.

B) The variance deviation of changes in forward prices.

C) The covariance between changes in spot and forward prices.

D) Choices a and b only

E) All of the above

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

35

Which of the following is not considered a "cost of carry"?

A) Commissions for physical storage

B) An opportunity cost for the net amount of invested capital

C) A premium for the convenience of consuming the asset now

D) A risk premium for uncertainty

E) All of the above are considered costs of carry.

A) Commissions for physical storage

B) An opportunity cost for the net amount of invested capital

C) A premium for the convenience of consuming the asset now

D) A risk premium for uncertainty

E) All of the above are considered costs of carry.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

36

As a contract approaches maturity,the spot price and forward price

A) Increase.

B) Diverge.

C) Maintain a fixed price differential.

D) Have a random relationship.

E) Converge.

A) Increase.

B) Diverge.

C) Maintain a fixed price differential.

D) Have a random relationship.

E) Converge.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

37

According to the cost of carry model the relationship between the spot (S₀)and futures price (F₀,T)is

A) S0 = F0,T/(1 + rf)T

B) S0 = F0,T(1 + rf)T

C) S0 + F0,T = (1 + rf)T

D) S0 = F0,T + (1 + rf)T

E) S0 - F0,T = (1 + rf)T

A) S0 = F0,T/(1 + rf)T

B) S0 = F0,T(1 + rf)T

C) S0 + F0,T = (1 + rf)T

D) S0 = F0,T + (1 + rf)T

E) S0 - F0,T = (1 + rf)T

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

38

The basis (Bt,T)at time t between the spot price (St)and a futures contract expiring at time T (Ft,T)is

A) Bt,T = St + Ft,T

B) Bt,T = St - Ft,T

C) Bt,T = St × Ft,T

D) Bt,T = St/Ft,T

E) None of the above

A) Bt,T = St + Ft,T

B) Bt,T = St - Ft,T

C) Bt,T = St × Ft,T

D) Bt,T = St/Ft,T

E) None of the above

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

39

The Chicago Board of Trade (CBT)uses conversion factors to correct for differences in deliverable bonds.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

40

In the absence of arbitrage opportunities,the forward contract price should be equal to the current spot price plus interest.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

41

An investor who wants a long position in a ____ must first place the order with a broker,who then passes it on to the trading pit or electronic network.Details of the order are then passed on to the exchange clearinghouse.

A) Call option

B) Put option

C) Forward contract

D) Futures contract

E) None of the above

A) Call option

B) Put option

C) Forward contract

D) Futures contract

E) None of the above

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

42

Exhibit 21.3

Use the Information Below for the Following Problem(S)

As a relationship officer for a money-center commercial bank, one of your corporate accounts has just approached you about a one-year loan for $3,000,000. The customer would pay a quarterly interest expense based on the prevailing level of LIBOR at the beginning of each quarter. As is the bank's convention on all such loans, the amount of the interest payment would then be paid at the end of the quarterly cycle when the new rate for the next cycle is determined. You observe the following LIBOR yield curve in the cash market:

-Refer to Exhibit 21.3.What is the implied 90-day forward rate at the beginning of the fourth quarter?

A) 6.19%

B) 5.10%

C) 6.07%

D) 5.68%

E) None of the above

Use the Information Below for the Following Problem(S)

As a relationship officer for a money-center commercial bank, one of your corporate accounts has just approached you about a one-year loan for $3,000,000. The customer would pay a quarterly interest expense based on the prevailing level of LIBOR at the beginning of each quarter. As is the bank's convention on all such loans, the amount of the interest payment would then be paid at the end of the quarterly cycle when the new rate for the next cycle is determined. You observe the following LIBOR yield curve in the cash market:

-Refer to Exhibit 21.3.What is the implied 90-day forward rate at the beginning of the fourth quarter?

A) 6.19%

B) 5.10%

C) 6.07%

D) 5.68%

E) None of the above

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

43

Exhibit 21.1

Use the Information Below for the Following Problem(S)

In late January 2004, The Union Cosmos Company is considering the sale of $100 million in 10-year debentures that will probably be rated AAA like the firm's other bond issues. The firm is anxious to proceed at today's rate of 10.5 percent. As treasurer, you know that it will take until sometime in April to get the issue registered and sold. Therefore, you suggest that the firm hedge the pending issue using Treasury bond futures contracts each representing $100,000.

Refer to Exhibit 21.1.Explain how you would go about hedging the bond issue?

A) Sell 1,000 contracts

B) Buy 1,000 contracts

C) Sell 100 contracts

D) Sell 10,000 contracts

E) None of the above

Use the Information Below for the Following Problem(S)

In late January 2004, The Union Cosmos Company is considering the sale of $100 million in 10-year debentures that will probably be rated AAA like the firm's other bond issues. The firm is anxious to proceed at today's rate of 10.5 percent. As treasurer, you know that it will take until sometime in April to get the issue registered and sold. Therefore, you suggest that the firm hedge the pending issue using Treasury bond futures contracts each representing $100,000.

Refer to Exhibit 21.1.Explain how you would go about hedging the bond issue?

A) Sell 1,000 contracts

B) Buy 1,000 contracts

C) Sell 100 contracts

D) Sell 10,000 contracts

E) None of the above

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

44

Exhibit 21.3

Use the Information Below for the Following Problem(S)

As a relationship officer for a money-center commercial bank, one of your corporate accounts has just approached you about a one-year loan for $3,000,000. The customer would pay a quarterly interest expense based on the prevailing level of LIBOR at the beginning of each quarter. As is the bank's convention on all such loans, the amount of the interest payment would then be paid at the end of the quarterly cycle when the new rate for the next cycle is determined. You observe the following LIBOR yield curve in the cash market:

-Refer to Exhibit 21.3.What is the implied 90-day forward rate at the beginning of the second quarter?

A) 4.70%

B) 4.85%

C) 4.60%

D) 4.94%

E) None of the above

Use the Information Below for the Following Problem(S)

As a relationship officer for a money-center commercial bank, one of your corporate accounts has just approached you about a one-year loan for $3,000,000. The customer would pay a quarterly interest expense based on the prevailing level of LIBOR at the beginning of each quarter. As is the bank's convention on all such loans, the amount of the interest payment would then be paid at the end of the quarterly cycle when the new rate for the next cycle is determined. You observe the following LIBOR yield curve in the cash market:

-Refer to Exhibit 21.3.What is the implied 90-day forward rate at the beginning of the second quarter?

A) 4.70%

B) 4.85%

C) 4.60%

D) 4.94%

E) None of the above

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

45

Exhibit 21.3

Use the Information Below for the Following Problem(S)

As a relationship officer for a money-center commercial bank, one of your corporate accounts has just approached you about a one-year loan for $3,000,000. The customer would pay a quarterly interest expense based on the prevailing level of LIBOR at the beginning of each quarter. As is the bank's convention on all such loans, the amount of the interest payment would then be paid at the end of the quarterly cycle when the new rate for the next cycle is determined. You observe the following LIBOR yield curve in the cash market:

-Refer to Exhibit 21.3.If 90-day LIBOR rises to the levels "predicted" by the implied forward rates,what will the dollar level of the bank's interest receipt be at the end of the fourth quarter?

A) $36,223.50

B) $40,500.00

C) $38,250.00

D) $36,375.00

E) None of the above

Use the Information Below for the Following Problem(S)

As a relationship officer for a money-center commercial bank, one of your corporate accounts has just approached you about a one-year loan for $3,000,000. The customer would pay a quarterly interest expense based on the prevailing level of LIBOR at the beginning of each quarter. As is the bank's convention on all such loans, the amount of the interest payment would then be paid at the end of the quarterly cycle when the new rate for the next cycle is determined. You observe the following LIBOR yield curve in the cash market:

-Refer to Exhibit 21.3.If 90-day LIBOR rises to the levels "predicted" by the implied forward rates,what will the dollar level of the bank's interest receipt be at the end of the fourth quarter?

A) $36,223.50

B) $40,500.00

C) $38,250.00

D) $36,375.00

E) None of the above

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

46

Exhibit 21.1

Use the Information Below for the Following Problem(S)

In late January 2004, The Union Cosmos Company is considering the sale of $100 million in 10-year debentures that will probably be rated AAA like the firm's other bond issues. The firm is anxious to proceed at today's rate of 10.5 percent. As treasurer, you know that it will take until sometime in April to get the issue registered and sold. Therefore, you suggest that the firm hedge the pending issue using Treasury bond futures contracts each representing $100,000.

Refer to Exhibit 21.1.What is the dollar gain or loss assuming that future conditions described in Case 2 actually occur? (Ignore commissions and margin costs,and assume a naive hedge ratio.)

A) $2,965,000.00 gain

B) $45,500.00 gain

C) $2,965,000.00 loss

D) $45,500.00 loss

E) None of the above

Use the Information Below for the Following Problem(S)

In late January 2004, The Union Cosmos Company is considering the sale of $100 million in 10-year debentures that will probably be rated AAA like the firm's other bond issues. The firm is anxious to proceed at today's rate of 10.5 percent. As treasurer, you know that it will take until sometime in April to get the issue registered and sold. Therefore, you suggest that the firm hedge the pending issue using Treasury bond futures contracts each representing $100,000.

Refer to Exhibit 21.1.What is the dollar gain or loss assuming that future conditions described in Case 2 actually occur? (Ignore commissions and margin costs,and assume a naive hedge ratio.)

A) $2,965,000.00 gain

B) $45,500.00 gain

C) $2,965,000.00 loss

D) $45,500.00 loss

E) None of the above

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

47

Exhibit 21.3

Use the Information Below for the Following Problem(S)

As a relationship officer for a money-center commercial bank, one of your corporate accounts has just approached you about a one-year loan for $3,000,000. The customer would pay a quarterly interest expense based on the prevailing level of LIBOR at the beginning of each quarter. As is the bank's convention on all such loans, the amount of the interest payment would then be paid at the end of the quarterly cycle when the new rate for the next cycle is determined. You observe the following LIBOR yield curve in the cash market:

-Refer to Exhibit 21.3.Assuming the yields inferred from the Eurodollar futures contract prices for the next three settlement periods are equal to the implied forward rates,calculate the dollar value of the annuity that would leave the bank indifferent between making the floating-rate loan and hedging it in the futures market,and making a one-year fixed-rate loan.

A) $49,312.36

B) $35,120.62

C) $39,036.45

D) $44,452.36

E) None of the above

Use the Information Below for the Following Problem(S)

As a relationship officer for a money-center commercial bank, one of your corporate accounts has just approached you about a one-year loan for $3,000,000. The customer would pay a quarterly interest expense based on the prevailing level of LIBOR at the beginning of each quarter. As is the bank's convention on all such loans, the amount of the interest payment would then be paid at the end of the quarterly cycle when the new rate for the next cycle is determined. You observe the following LIBOR yield curve in the cash market:

-Refer to Exhibit 21.3.Assuming the yields inferred from the Eurodollar futures contract prices for the next three settlement periods are equal to the implied forward rates,calculate the dollar value of the annuity that would leave the bank indifferent between making the floating-rate loan and hedging it in the futures market,and making a one-year fixed-rate loan.

A) $49,312.36

B) $35,120.62

C) $39,036.45

D) $44,452.36

E) None of the above

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

48

Exhibit 21.2

Use the Information Below for the Following Problem(S)

Assume you are the Treasurer for the Johnson Pharmaceutical Company and in late July 2004, the company is considering the sale of $500 million in 20-year debentures that will most likely be rated the same as the firm's other debt issues. The firm would like to proceed at the current rate of 8.5%, but you know that it will probably take until November to bring the issue to market. Therefore, you suggest that the firm hedge the pending issue using Treasury bond futures contracts which each represent $100,000.

Refer to Exhibit 21.2.What is the dollar gain or loss assuming that future conditions described in Case 1 actually occur? (Ignore commissions and margin costs,and assume a naive hedge ratio.)

A) $47,316,683.00 gain

B) $36,566,683.00 loss

C) $10,750,000.00 gain

D) $10,750,000.00 loss

E) None of the above

Use the Information Below for the Following Problem(S)

Assume you are the Treasurer for the Johnson Pharmaceutical Company and in late July 2004, the company is considering the sale of $500 million in 20-year debentures that will most likely be rated the same as the firm's other debt issues. The firm would like to proceed at the current rate of 8.5%, but you know that it will probably take until November to bring the issue to market. Therefore, you suggest that the firm hedge the pending issue using Treasury bond futures contracts which each represent $100,000.

Refer to Exhibit 21.2.What is the dollar gain or loss assuming that future conditions described in Case 1 actually occur? (Ignore commissions and margin costs,and assume a naive hedge ratio.)

A) $47,316,683.00 gain

B) $36,566,683.00 loss

C) $10,750,000.00 gain

D) $10,750,000.00 loss

E) None of the above

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

49

Financial futures include all of the following underlying securities except

A) Stock indexes

B) Treasury bonds

C) Bank deposits

D) Foreign currencies

E) All of the above are examples of underlying securities for financial futures

A) Stock indexes

B) Treasury bonds

C) Bank deposits

D) Foreign currencies

E) All of the above are examples of underlying securities for financial futures

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

50

Exhibit 21.2

Use the Information Below for the Following Problem(S)

Assume you are the Treasurer for the Johnson Pharmaceutical Company and in late July 2004, the company is considering the sale of $500 million in 20-year debentures that will most likely be rated the same as the firm's other debt issues. The firm would like to proceed at the current rate of 8.5%, but you know that it will probably take until November to bring the issue to market. Therefore, you suggest that the firm hedge the pending issue using Treasury bond futures contracts which each represent $100,000.

Refer to Exhibit 21.2.How you would go about hedging the bond issue?

A) Buy 5,000 contracts

B) Buy 50,000 contracts

C) Sell 5,000,000 contracts

D) Sell 5,000 contracts

E) None of the above

Use the Information Below for the Following Problem(S)

Assume you are the Treasurer for the Johnson Pharmaceutical Company and in late July 2004, the company is considering the sale of $500 million in 20-year debentures that will most likely be rated the same as the firm's other debt issues. The firm would like to proceed at the current rate of 8.5%, but you know that it will probably take until November to bring the issue to market. Therefore, you suggest that the firm hedge the pending issue using Treasury bond futures contracts which each represent $100,000.

Refer to Exhibit 21.2.How you would go about hedging the bond issue?

A) Buy 5,000 contracts

B) Buy 50,000 contracts

C) Sell 5,000,000 contracts

D) Sell 5,000 contracts

E) None of the above

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

51

Exhibit 21.2

Use the Information Below for the Following Problem(S)

Assume you are the Treasurer for the Johnson Pharmaceutical Company and in late July 2004, the company is considering the sale of $500 million in 20-year debentures that will most likely be rated the same as the firm's other debt issues. The firm would like to proceed at the current rate of 8.5%, but you know that it will probably take until November to bring the issue to market. Therefore, you suggest that the firm hedge the pending issue using Treasury bond futures contracts which each represent $100,000.

Refer to Exhibit 21.2.What is the dollar gain or loss assuming that future conditions described in Case 2 actually occur? (Ignore commissions and margin costs,and assume a naive hedge ratio.)

A) $19,500,000.00 gain

B) $27,816,683.04 gain

C) $27,816,683.04 loss

D) $19,500,000.00 loss

E) None of the above

Use the Information Below for the Following Problem(S)

Assume you are the Treasurer for the Johnson Pharmaceutical Company and in late July 2004, the company is considering the sale of $500 million in 20-year debentures that will most likely be rated the same as the firm's other debt issues. The firm would like to proceed at the current rate of 8.5%, but you know that it will probably take until November to bring the issue to market. Therefore, you suggest that the firm hedge the pending issue using Treasury bond futures contracts which each represent $100,000.

Refer to Exhibit 21.2.What is the dollar gain or loss assuming that future conditions described in Case 2 actually occur? (Ignore commissions and margin costs,and assume a naive hedge ratio.)

A) $19,500,000.00 gain

B) $27,816,683.04 gain

C) $27,816,683.04 loss

D) $19,500,000.00 loss

E) None of the above

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

52

In your portfolio you have $1 million of 20 year,8 5/8 percent bonds which are selling at 83.15 (or 83 15/32)against this position.Because you feel interest rates will rise you sell 10 bond futures at 81.15 (or 81 15/32)against this position.Two months later you decide to close your position.The bonds have fallen to 78 and the futures contracts are at 75.16 (75 16/32).Disregarding margin and transaction costs,what is your gain or loss?

A) $5,000 loss

B) $500 loss

C) Breakeven

D) $500 gain

E) $5,000 gain

A) $5,000 loss

B) $500 loss

C) Breakeven

D) $500 gain

E) $5,000 gain

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

53

Which of the following is true when F?,T < E(ST)?

A) Occurs when long hedgers outnumber short hedgers.

B) Occurs when short hedgers outnumber long hedgers.

C) The market is said to be in contango.

D) The market is said to be in normal contango.

E) The pure expectations hypothesis holds.

A) Occurs when long hedgers outnumber short hedgers.

B) Occurs when short hedgers outnumber long hedgers.

C) The market is said to be in contango.

D) The market is said to be in normal contango.

E) The pure expectations hypothesis holds.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

54

Exhibit 21.3

Use the Information Below for the Following Problem(S)

As a relationship officer for a money-center commercial bank, one of your corporate accounts has just approached you about a one-year loan for $3,000,000. The customer would pay a quarterly interest expense based on the prevailing level of LIBOR at the beginning of each quarter. As is the bank's convention on all such loans, the amount of the interest payment would then be paid at the end of the quarterly cycle when the new rate for the next cycle is determined. You observe the following LIBOR yield curve in the cash market:

-Refer to Exhibit 21.3.If 90-day LIBOR rises to the levels "predicted" by the implied forward rates,what will the dollar level of the bank's interest receipt be at the end of the first quarter?

A) $35,250.00

B) $36,375.00

C) $38,250.00

D) $40,500.00

E) None of the above

Use the Information Below for the Following Problem(S)

As a relationship officer for a money-center commercial bank, one of your corporate accounts has just approached you about a one-year loan for $3,000,000. The customer would pay a quarterly interest expense based on the prevailing level of LIBOR at the beginning of each quarter. As is the bank's convention on all such loans, the amount of the interest payment would then be paid at the end of the quarterly cycle when the new rate for the next cycle is determined. You observe the following LIBOR yield curve in the cash market:

-Refer to Exhibit 21.3.If 90-day LIBOR rises to the levels "predicted" by the implied forward rates,what will the dollar level of the bank's interest receipt be at the end of the first quarter?

A) $35,250.00

B) $36,375.00

C) $38,250.00

D) $40,500.00

E) None of the above

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

55

Exhibit 21.3

Use the Information Below for the Following Problem(S)

As a relationship officer for a money-center commercial bank, one of your corporate accounts has just approached you about a one-year loan for $3,000,000. The customer would pay a quarterly interest expense based on the prevailing level of LIBOR at the beginning of each quarter. As is the bank's convention on all such loans, the amount of the interest payment would then be paid at the end of the quarterly cycle when the new rate for the next cycle is determined. You observe the following LIBOR yield curve in the cash market:

-Refer to Exhibit 21.3.What is the implied 90-day forward rate at the beginning of the third quarter?

A) 5.10%

B) 5.47%

C) 4.70%

D) 4.85%

E) None of the above

Use the Information Below for the Following Problem(S)

As a relationship officer for a money-center commercial bank, one of your corporate accounts has just approached you about a one-year loan for $3,000,000. The customer would pay a quarterly interest expense based on the prevailing level of LIBOR at the beginning of each quarter. As is the bank's convention on all such loans, the amount of the interest payment would then be paid at the end of the quarterly cycle when the new rate for the next cycle is determined. You observe the following LIBOR yield curve in the cash market:

-Refer to Exhibit 21.3.What is the implied 90-day forward rate at the beginning of the third quarter?

A) 5.10%

B) 5.47%

C) 4.70%

D) 4.85%

E) None of the above

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

56

When F₀,T > E(ST)it is known as

A) Backwardation.

B) Normal backwardation.

C) Normal contango.

D) Inverted spread.

E) Pure expectations equilibrium.

A) Backwardation.

B) Normal backwardation.

C) Normal contango.

D) Inverted spread.

E) Pure expectations equilibrium.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

57

Exhibit 21.3

Use the Information Below for the Following Problem(S)

As a relationship officer for a money-center commercial bank, one of your corporate accounts has just approached you about a one-year loan for $3,000,000. The customer would pay a quarterly interest expense based on the prevailing level of LIBOR at the beginning of each quarter. As is the bank's convention on all such loans, the amount of the interest payment would then be paid at the end of the quarterly cycle when the new rate for the next cycle is determined. You observe the following LIBOR yield curve in the cash market:

-Refer to Exhibit 21.3.If the bank wanted to hedge its exposure to falling LIBOR on this loan commitment,describe the sequence of transactions in the futures markets it could undertake.

A) Buy 3 Eurodollar futures contracts that expire at the end of the first quarter.

B) Buy 3 Eurodollar futures contracts that expire at the end of the first quarter, 3 that expire at the end of the second quarter, and 3 that expire at the end of the third quarter.

C) Sell 3 Eurodollar futures contracts that expire at the end of the year.

D) Sell one Eurodollar futures contract that expires at the end of the first quarter, one that expires at the end of the second quarter, and one that expires at the end of the third quarter.

E) Buy 3 Eurodollar futures contracts that expire at the end of the year.

Use the Information Below for the Following Problem(S)

As a relationship officer for a money-center commercial bank, one of your corporate accounts has just approached you about a one-year loan for $3,000,000. The customer would pay a quarterly interest expense based on the prevailing level of LIBOR at the beginning of each quarter. As is the bank's convention on all such loans, the amount of the interest payment would then be paid at the end of the quarterly cycle when the new rate for the next cycle is determined. You observe the following LIBOR yield curve in the cash market:

-Refer to Exhibit 21.3.If the bank wanted to hedge its exposure to falling LIBOR on this loan commitment,describe the sequence of transactions in the futures markets it could undertake.

A) Buy 3 Eurodollar futures contracts that expire at the end of the first quarter.

B) Buy 3 Eurodollar futures contracts that expire at the end of the first quarter, 3 that expire at the end of the second quarter, and 3 that expire at the end of the third quarter.

C) Sell 3 Eurodollar futures contracts that expire at the end of the year.

D) Sell one Eurodollar futures contract that expires at the end of the first quarter, one that expires at the end of the second quarter, and one that expires at the end of the third quarter.

E) Buy 3 Eurodollar futures contracts that expire at the end of the year.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

58

Exhibit 21.3

Use the Information Below for the Following Problem(S)

As a relationship officer for a money-center commercial bank, one of your corporate accounts has just approached you about a one-year loan for $3,000,000. The customer would pay a quarterly interest expense based on the prevailing level of LIBOR at the beginning of each quarter. As is the bank's convention on all such loans, the amount of the interest payment would then be paid at the end of the quarterly cycle when the new rate for the next cycle is determined. You observe the following LIBOR yield curve in the cash market:

-Refer to Exhibit 21.3.If 90-day LIBOR rises to the levels "predicted" by the implied forward rates,what will the dollar level of the bank's interest receipt be at the end of the third quarter?

A) $35,250.00

B) $36,375.00

C) $38,250.00

D) $41,005.50

E) None of the above

Use the Information Below for the Following Problem(S)

As a relationship officer for a money-center commercial bank, one of your corporate accounts has just approached you about a one-year loan for $3,000,000. The customer would pay a quarterly interest expense based on the prevailing level of LIBOR at the beginning of each quarter. As is the bank's convention on all such loans, the amount of the interest payment would then be paid at the end of the quarterly cycle when the new rate for the next cycle is determined. You observe the following LIBOR yield curve in the cash market:

-Refer to Exhibit 21.3.If 90-day LIBOR rises to the levels "predicted" by the implied forward rates,what will the dollar level of the bank's interest receipt be at the end of the third quarter?

A) $35,250.00

B) $36,375.00

C) $38,250.00

D) $41,005.50

E) None of the above

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

59

Exhibit 21.1

Use the Information Below for the Following Problem(S)

In late January 2004, The Union Cosmos Company is considering the sale of $100 million in 10-year debentures that will probably be rated AAA like the firm's other bond issues. The firm is anxious to proceed at today's rate of 10.5 percent. As treasurer, you know that it will take until sometime in April to get the issue registered and sold. Therefore, you suggest that the firm hedge the pending issue using Treasury bond futures contracts each representing $100,000.

Refer to Exhibit 21.1.What is the dollar gain or loss assuming that future conditions described in Case 1 actually occur? (Ignore commissions and margin costs,and assume a naive hedge ratio.)

A) $2,945,000.00 gain

B) $65,500.00 gain

C) $2,945,000.00 loss

D) $65,500.00 loss

E) None of the above

Use the Information Below for the Following Problem(S)

In late January 2004, The Union Cosmos Company is considering the sale of $100 million in 10-year debentures that will probably be rated AAA like the firm's other bond issues. The firm is anxious to proceed at today's rate of 10.5 percent. As treasurer, you know that it will take until sometime in April to get the issue registered and sold. Therefore, you suggest that the firm hedge the pending issue using Treasury bond futures contracts each representing $100,000.

Refer to Exhibit 21.1.What is the dollar gain or loss assuming that future conditions described in Case 1 actually occur? (Ignore commissions and margin costs,and assume a naive hedge ratio.)

A) $2,945,000.00 gain

B) $65,500.00 gain

C) $2,945,000.00 loss

D) $65,500.00 loss

E) None of the above

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

60

Exhibit 21.3

Use the Information Below for the Following Problem(S)

As a relationship officer for a money-center commercial bank, one of your corporate accounts has just approached you about a one-year loan for $3,000,000. The customer would pay a quarterly interest expense based on the prevailing level of LIBOR at the beginning of each quarter. As is the bank's convention on all such loans, the amount of the interest payment would then be paid at the end of the quarterly cycle when the new rate for the next cycle is determined. You observe the following LIBOR yield curve in the cash market:

-Refer to Exhibit 21.3.If 90-day LIBOR rises to the levels "predicted" by the implied forward rates,what will the dollar level of the bank's interest receipt be at the end of the second quarter?

A) $40,500.00

B) $38,250.00

C) $35,250.00

D) $37,064.25

E) None of the above

Use the Information Below for the Following Problem(S)

As a relationship officer for a money-center commercial bank, one of your corporate accounts has just approached you about a one-year loan for $3,000,000. The customer would pay a quarterly interest expense based on the prevailing level of LIBOR at the beginning of each quarter. As is the bank's convention on all such loans, the amount of the interest payment would then be paid at the end of the quarterly cycle when the new rate for the next cycle is determined. You observe the following LIBOR yield curve in the cash market:

-Refer to Exhibit 21.3.If 90-day LIBOR rises to the levels "predicted" by the implied forward rates,what will the dollar level of the bank's interest receipt be at the end of the second quarter?

A) $40,500.00

B) $38,250.00

C) $35,250.00

D) $37,064.25

E) None of the above

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

61

Exhibit 21.4

Use the Information Below for the Following Problem(S)

A 3-month T-bond futures contract (maturity 20 years, coupon 6%, face $100,000) currently trades at $98,781.25 (implied yield 6.11%). A 3-month T-note futures contract (maturity 10 years, coupon 6%, face $100,000) currently trades at $101,468.80 (implied yield 5.80%). Assume semiannual compounding.

Refer to Exhibit 21.4.Suppose the yield curve changed so the that the new yield on the T-bond contract rose to 6.5% and the new yield on the T-note contract fell to 5.5%.Calculate the profit on the NOB futures spread.(Assume coupons are paid semiannually)

A) -$5850.92

B) -$6,671.42

C) $6,671.42

D) $5850.92

E) None of the above

Use the Information Below for the Following Problem(S)

A 3-month T-bond futures contract (maturity 20 years, coupon 6%, face $100,000) currently trades at $98,781.25 (implied yield 6.11%). A 3-month T-note futures contract (maturity 10 years, coupon 6%, face $100,000) currently trades at $101,468.80 (implied yield 5.80%). Assume semiannual compounding.

Refer to Exhibit 21.4.Suppose the yield curve changed so the that the new yield on the T-bond contract rose to 6.5% and the new yield on the T-note contract fell to 5.5%.Calculate the profit on the NOB futures spread.(Assume coupons are paid semiannually)

A) -$5850.92

B) -$6,671.42

C) $6,671.42

D) $5850.92

E) None of the above

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

62

Exhibit 21.6

Use the Information Below for the Following Problem(S)

Assume that you observe the following prices in the T-Bill and Eurodollar futures markets

Refer to Exhibit 21.6.If you expected the TED spread to widen over the next month then an appropriate strategy would be to

A) Go long T-Bill futures and long Eurodollar futures.

B) Go short T-Bill futures and short Eurodollar futures.

C) Go long T-Bill futures and short Eurodollar futures.

D) Go short T-Bill futures and long Eurodollar futures.

E) None of the above.

Use the Information Below for the Following Problem(S)

Assume that you observe the following prices in the T-Bill and Eurodollar futures markets

Refer to Exhibit 21.6.If you expected the TED spread to widen over the next month then an appropriate strategy would be to

A) Go long T-Bill futures and long Eurodollar futures.

B) Go short T-Bill futures and short Eurodollar futures.

C) Go long T-Bill futures and short Eurodollar futures.

D) Go short T-Bill futures and long Eurodollar futures.

E) None of the above.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

63

Exhibit 21.5

Use the Information Below for the Following Problem(S)

The S&P 500 stock index is at 1100. The annualized interest rate is 3.5% and the annualized dividend is 2%.

Refer to Exhibit 21.5.Calculate the price of the futures contract now.

A) 1108.59

B) 1102.75

C) 1139.79

D) 1123.19

E) None of the above

Use the Information Below for the Following Problem(S)

The S&P 500 stock index is at 1100. The annualized interest rate is 3.5% and the annualized dividend is 2%.

Refer to Exhibit 21.5.Calculate the price of the futures contract now.

A) 1108.59

B) 1102.75

C) 1139.79

D) 1123.19

E) None of the above

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

64

Exhibit 21.4

Use the Information Below for the Following Problem(S)

A 3-month T-bond futures contract (maturity 20 years, coupon 6%, face $100,000) currently trades at $98,781.25 (implied yield 6.11%). A 3-month T-note futures contract (maturity 10 years, coupon 6%, face $100,000) currently trades at $101,468.80 (implied yield 5.80%). Assume semiannual compounding.

Refer to Exhibit 21.4.If you expected the yield curve to steepen,the appropriate NOB futures spread strategy would be

A) Go long the T-bond and short the T-note

B) Go short the T-bond and long the T-note

C) Go long the T-bond and long the T-note

D) Go short the T-bond and short the T-note

E) None of the above

Use the Information Below for the Following Problem(S)

A 3-month T-bond futures contract (maturity 20 years, coupon 6%, face $100,000) currently trades at $98,781.25 (implied yield 6.11%). A 3-month T-note futures contract (maturity 10 years, coupon 6%, face $100,000) currently trades at $101,468.80 (implied yield 5.80%). Assume semiannual compounding.

Refer to Exhibit 21.4.If you expected the yield curve to steepen,the appropriate NOB futures spread strategy would be

A) Go long the T-bond and short the T-note

B) Go short the T-bond and long the T-note

C) Go long the T-bond and long the T-note

D) Go short the T-bond and short the T-note

E) None of the above

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

65

Exhibit 21.3

Use the Information Below for the Following Problem(S)

As a relationship officer for a money-center commercial bank, one of your corporate accounts has just approached you about a one-year loan for $3,000,000. The customer would pay a quarterly interest expense based on the prevailing level of LIBOR at the beginning of each quarter. As is the bank's convention on all such loans, the amount of the interest payment would then be paid at the end of the quarterly cycle when the new rate for the next cycle is determined. You observe the following LIBOR yield curve in the cash market:

-Refer to Exhibit 21.3.Assuming the yields inferred from the Eurodollar futures contract prices for the next three settlement periods are equal to the implied forward rates,calculate in annual (360-day)percentage terms,the annuity that would leave the bank indifferent between making the floating-rate loan and hedging it in the futures market,and making a one-year fixed-rate loan.

A) 20.86%

B) 5.10%

C) 4.91%

D) 5.20%

E) None of the above

Use the Information Below for the Following Problem(S)

As a relationship officer for a money-center commercial bank, one of your corporate accounts has just approached you about a one-year loan for $3,000,000. The customer would pay a quarterly interest expense based on the prevailing level of LIBOR at the beginning of each quarter. As is the bank's convention on all such loans, the amount of the interest payment would then be paid at the end of the quarterly cycle when the new rate for the next cycle is determined. You observe the following LIBOR yield curve in the cash market:

-Refer to Exhibit 21.3.Assuming the yields inferred from the Eurodollar futures contract prices for the next three settlement periods are equal to the implied forward rates,calculate in annual (360-day)percentage terms,the annuity that would leave the bank indifferent between making the floating-rate loan and hedging it in the futures market,and making a one-year fixed-rate loan.

A) 20.86%

B) 5.10%

C) 4.91%

D) 5.20%

E) None of the above

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

66

Exhibit 21.5

Use the Information Below for the Following Problem(S)

The S&P 500 stock index is at 1100. The annualized interest rate is 3.5% and the annualized dividend is 2%.

Refer to Exhibit 21.5.If the futures contract was currently available for 1250,calculate the arbitrage profit.

A) $0

B) $133.41

C) -$133.41

D) $147.25

E) -$147.25

Use the Information Below for the Following Problem(S)

The S&P 500 stock index is at 1100. The annualized interest rate is 3.5% and the annualized dividend is 2%.

Refer to Exhibit 21.5.If the futures contract was currently available for 1250,calculate the arbitrage profit.

A) $0

B) $133.41

C) -$133.41

D) $147.25

E) -$147.25

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

67

Exhibit 21.6

Use the Information Below for the Following Problem(S)

Assume that you observe the following prices in the T-Bill and Eurodollar futures markets

Refer to Exhibit 21.6.Assume that a month later the price of the September T-Bill future is 93 and the price of the Eurodollar future is 90.25.Calculate the profit on the Eurodollar futures position.

A) 190 basis points.

B) 210 basis points.

C) -190 basis points.

D) -210 basis points.

E) 100 basis points.

Use the Information Below for the Following Problem(S)

Assume that you observe the following prices in the T-Bill and Eurodollar futures markets

Refer to Exhibit 21.6.Assume that a month later the price of the September T-Bill future is 93 and the price of the Eurodollar future is 90.25.Calculate the profit on the Eurodollar futures position.

A) 190 basis points.

B) 210 basis points.

C) -190 basis points.

D) -210 basis points.

E) 100 basis points.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

68

Exhibit 21.5

Use the Information Below for the Following Problem(S)

The S&P 500 stock index is at 1100. The annualized interest rate is 3.5% and the annualized dividend is 2%.

Refer to Exhibit 21.5.If the futures contract was currently available for 1250,indicate the appropriate strategy that would earn an arbitrage profit.

A) Long futures, and short the index.

B) Short futures and long the index.

C) Long futures and long the index.

D) Short futures and short the index.

E) None of the above.

Use the Information Below for the Following Problem(S)

The S&P 500 stock index is at 1100. The annualized interest rate is 3.5% and the annualized dividend is 2%.

Refer to Exhibit 21.5.If the futures contract was currently available for 1250,indicate the appropriate strategy that would earn an arbitrage profit.

A) Long futures, and short the index.

B) Short futures and long the index.

C) Long futures and long the index.

D) Short futures and short the index.

E) None of the above.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

69

Exhibit 21.4

Use the Information Below for the Following Problem(S)

A 3-month T-bond futures contract (maturity 20 years, coupon 6%, face $100,000) currently trades at $98,781.25 (implied yield 6.11%). A 3-month T-note futures contract (maturity 10 years, coupon 6%, face $100,000) currently trades at $101,468.80 (implied yield 5.80%). Assume semiannual compounding.

Refer to Exhibit 21.4.If you expected the yield curve to flatten,the appropriate NOB futures spread strategy would be

A) Go long the T-bond and short the T-note

B) Go short the T-bond and long the T-note

C) Go long the T-bond and long the T-note

D) Go short the T-bond and short the T-note

E) None of the above

Use the Information Below for the Following Problem(S)

A 3-month T-bond futures contract (maturity 20 years, coupon 6%, face $100,000) currently trades at $98,781.25 (implied yield 6.11%). A 3-month T-note futures contract (maturity 10 years, coupon 6%, face $100,000) currently trades at $101,468.80 (implied yield 5.80%). Assume semiannual compounding.

Refer to Exhibit 21.4.If you expected the yield curve to flatten,the appropriate NOB futures spread strategy would be

A) Go long the T-bond and short the T-note

B) Go short the T-bond and long the T-note

C) Go long the T-bond and long the T-note

D) Go short the T-bond and short the T-note

E) None of the above

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

70

Assume that you manage an equity portfolio.The portfolio beta is 1.15.You anticipate a decline in equity values and wish to hedge $500 million of the portfolio.Calculate the number of contracts you would need to hedge your position and indicate whether you would go short or long.Assume that the price of the S&P 500 futures contract is 1105 and the multiplier is 250.

A) 2500 contracts short

B) 1810 contracts short

C) 1810 contracts long

D) 2081 contracts short

E) 2081 contracts long

A) 2500 contracts short

B) 1810 contracts short

C) 1810 contracts long

D) 2081 contracts short

E) 2081 contracts long

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

71

Exhibit 21.6

Use the Information Below for the Following Problem(S)

Assume that you observe the following prices in the T-Bill and Eurodollar futures markets

Refer to Exhibit 21.6.Assume that a month later the price of the September T-Bill future is 93 and the price of the Eurodollar future is 90.25.Calculate the profit on the T-Bill futures position.

A) 25 basis points.

B) 110 basis points.

C) -25 basis points.

D) -110 basis points.

E) 50 basis points.

Use the Information Below for the Following Problem(S)

Assume that you observe the following prices in the T-Bill and Eurodollar futures markets

Refer to Exhibit 21.6.Assume that a month later the price of the September T-Bill future is 93 and the price of the Eurodollar future is 90.25.Calculate the profit on the T-Bill futures position.

A) 25 basis points.