Deck 5: Overall Audit Strategy, Audit Program, Audit of the Sales and Collection Cycle, Audit Sampling for Tests of Controls and Substantive Tests of Transactions

Full screen (f)

Question

Question

Question

Tests of controls may include which of the following types of evidence?

Question

Question

Question

Question

Question

Question

Question

Which of the following types of procedures will be performed in an audit of internal control over financial reporting?

Question

Question

When an auditor believes that analytical procedures indicate a reasonable possibility of misstatement, the auditor usually would:

Question

Question

Question

Question

Which of the following is/are performed in an audit of internal control over financial reporting?

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

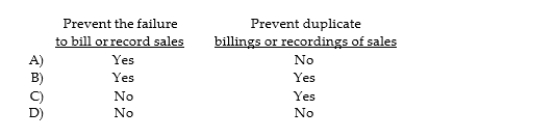

When posting items from the sales journal, details of the journal and journal totals are posted to which items?

Question

Question

Question

To prevent fraud, management should deny cash access to anyone responsible for:

Question

Which of the following is a point at which the auditor deems authorization to be critical?

Question

Prenumbered documents are intended to help:

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

An auditor can increase the likelihood that a sample is representative by using care in:

Question

Sampling risk may be controlled by:

Question

Question

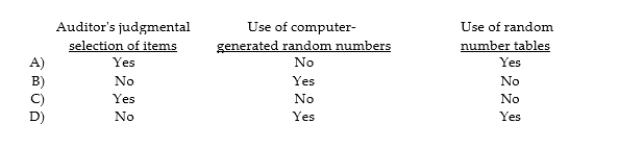

Which of the following methods of sample selection is appropriately used when selecting a random sample?

Question

Question

Question

Question

Question

Question

Question

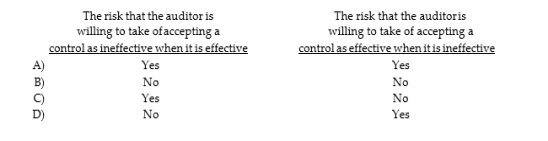

The acceptable risk of assessing control risk too low is:

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/63

Play

Full screen (f)

Deck 5: Overall Audit Strategy, Audit Program, Audit of the Sales and Collection Cycle, Audit Sampling for Tests of Controls and Substantive Tests of Transactions

1

Shown below (1 through 5) are the five types of tests which auditors use to determine whether financial statements are fairly stated. Which three are substantive tests?

A) 3, 4, and 5.

B) 2, 3, and 4.

C) 1, 2, and 3.

D) 2, 3, and 5.

A) 3, 4, and 5.

B) 2, 3, and 4.

C) 1, 2, and 3.

D) 2, 3, and 5.

3, 4, and 5.

2

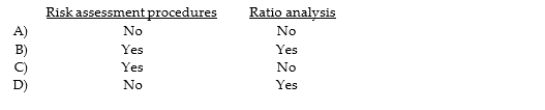

Which of the following procedures are frequently performed in response to the auditor's assessment of the risk of material misstatement?

A) Tests of controls.

B) Risk assessment procedures.

C) Tests of details of balances.

D) Ratio analysis.

A) Tests of controls.

B) Risk assessment procedures.

C) Tests of details of balances.

D) Ratio analysis.

Tests of details of balances.

3

Tests of controls may include which of the following types of evidence?

D

4

Which of the following is not a useful risk assessment procedure for obtaining an understanding of internal controls?

A) Make inquiries of the client's personnel.

B) Examine documents and records.

C) Read industry trade magazines.

D) Observe client activities and operations.

A) Make inquiries of the client's personnel.

B) Examine documents and records.

C) Read industry trade magazines.

D) Observe client activities and operations.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

5

Which of the following is not appropriate for purposes of testing the effectiveness of controls?

A) Reperform client procedures.

B) Evaluate prior experience with the client.

C) Observe control- related activities.

D) Make inquiries of client personnel.

A) Reperform client procedures.

B) Evaluate prior experience with the client.

C) Observe control- related activities.

D) Make inquiries of client personnel.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

6

Analytical procedures are defined in the auditing standards as:

A) helpful procedures not possessing the validity of other tests available to the auditor.

B) tests of controls.

C) substantive tests.

D) compliance tests.

A) helpful procedures not possessing the validity of other tests available to the auditor.

B) tests of controls.

C) substantive tests.

D) compliance tests.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

7

Tests of transactions are used to determine whether _ ________ have been satisfied.

A) compliance test requirements.

B) transaction- related audit objectives.

C) balance coverage requirements.

D) existence assertions.

A) compliance test requirements.

B) transaction- related audit objectives.

C) balance coverage requirements.

D) existence assertions.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

8

Which of the following audit tests is usually the least costly to perform?

A) Tests of controls.

B) Substantive tests of transactions.

C) Analytical procedures.

D) Tests of balances.

A) Tests of controls.

B) Substantive tests of transactions.

C) Analytical procedures.

D) Tests of balances.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

9

Which of the following relationships between types of tests and audit evidence is not correct?

A) Tests of controls and observation.

B) Tests of details and inspection.

C) Substantive tests of transactions and reperformance.

D) Tests of details and observation.

A) Tests of controls and observation.

B) Tests of details and inspection.

C) Substantive tests of transactions and reperformance.

D) Tests of details and observation.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

10

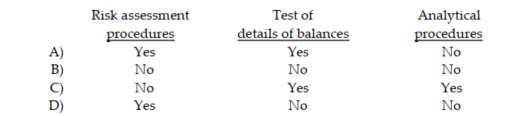

Which of the following types of procedures will be performed in an audit of internal control over financial reporting?

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

11

Tests of details of balances focus on:

A) end of the year balances.

B) beginning of the year balances.

C) accounting cycles.

D) transaction details for the period under audit.

A) end of the year balances.

B) beginning of the year balances.

C) accounting cycles.

D) transaction details for the period under audit.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

12

When an auditor believes that analytical procedures indicate a reasonable possibility of misstatement, the auditor usually would:

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

13

When controls are deemed ineffective and assessed control risk is at the maximum for a private company, there will be _ ________ emphasis placed on tests of controls.

A) heavy

B) moderate

C) no

D) relatively little

A) heavy

B) moderate

C) no

D) relatively little

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

14

Tests of controls address each of the following questions except:

A) Why were the procedures performed?

B) Who performed the procedures?

C) Were the necessary procedures performed?

D) How were the procedures performed?

A) Why were the procedures performed?

B) Who performed the procedures?

C) Were the necessary procedures performed?

D) How were the procedures performed?

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

15

At what point in the audit are tests of details most appropriately designed?

A) Testing.

B) Communication of material weaknesses.

C) Engagement evaluation.

D) Planning.

A) Testing.

B) Communication of material weaknesses.

C) Engagement evaluation.

D) Planning.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

16

Which of the following is/are performed in an audit of internal control over financial reporting?

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

17

Only ________ involve physical examination and confirmation.

A) tests of controls

B) tests of transactions

C) tests of balances

D) analytical procedures

A) tests of controls

B) tests of transactions

C) tests of balances

D) analytical procedures

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

18

Inspection is used in every type of test except:

A) analytical procedures.

B) tests of details.

C) tests of transactions.

D) tests of controls.

A) analytical procedures.

B) tests of details.

C) tests of transactions.

D) tests of controls.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

19

An exception in a test of control indicates the ________ of misstatements.

A) the amount, likelihood, and classification

B) the amount and the classification

C) the amount

D) the likelihood

A) the amount, likelihood, and classification

B) the amount and the classification

C) the amount

D) the likelihood

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

20

Must auditors always perform tests of controls?

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

21

Consider the audit risk model and the five types of audit tests. Which tests provide evidence pertinent to the various elements of the audit risk model?

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

22

Discuss the major determinants of the extent of tests of details of balances.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

23

Auditing standards encourage, but do not require, a written audit program.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

24

Substantive tests of transactions are the most expensive type of audit test to perform.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

25

Tests of details of balances focus on beginning and ending of the year balances.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

26

Substantive tests of transactions and substantive tests of details of balances are often conducted simultaneously.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

27

Which of the following is not an account affected by the sales and collection cycle?

A) Sales returns and allowances.

B) Cash receipts.

C) Allowance for uncollectible accounts.

D) Gross margin.

A) Sales returns and allowances.

B) Cash receipts.

C) Allowance for uncollectible accounts.

D) Gross margin.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

28

What critical event must take place before goods can be shipped?

A) Determination of correct delivery address.

B) Receipt of cash.

C) Credit approval.

D) Receipt of sales order from the customer.

A) Determination of correct delivery address.

B) Receipt of cash.

C) Credit approval.

D) Receipt of sales order from the customer.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

29

At what point in the sales and collection cycle does the company first give up assets?

A) Credit approval.

B) Shipment of goods.

C) Sales approval.

D) Cash collection.

A) Credit approval.

B) Shipment of goods.

C) Sales approval.

D) Cash collection.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

30

Most companies recognize sales revenue when:

A) customer orders are received.

B) sales are invoiced.

C) goods are shipped.

D) customer orders are approved.

A) customer orders are received.

B) sales are invoiced.

C) goods are shipped.

D) customer orders are approved.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

31

The document that supports reductions in accounts receivable is the:

A) bill of lading.

B) sales invoice.

C) monthly statement.

D) credit memo.

A) bill of lading.

B) sales invoice.

C) monthly statement.

D) credit memo.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

32

In which of the following will sales return and allowances not be recorded?

A) Sales returns and allowances transaction file.

B) Accounts receivable master file.

C) Cash receipts journal.

D) Sales returns and allowances will be recorded in all of the above.

A) Sales returns and allowances transaction file.

B) Accounts receivable master file.

C) Cash receipts journal.

D) Sales returns and allowances will be recorded in all of the above.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

33

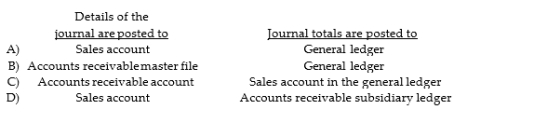

When posting items from the sales journal, details of the journal and journal totals are posted to which items?

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

34

A document used to indicate authority to write off an account receivable as uncollectible is the:

A) debit memo.

B) credit memo.

C) voucher.

D) uncollectible account authorization form.

A) debit memo.

B) credit memo.

C) voucher.

D) uncollectible account authorization form.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

35

Management's assertions for sales and collection activities are ________ when sales are generated via e- commerce activities.

A) expanded

B) mitigated

C) decreased

D) unchanged

A) expanded

B) mitigated

C) decreased

D) unchanged

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

36

To prevent fraud, management should deny cash access to anyone responsible for:

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

37

Which of the following is a point at which the auditor deems authorization to be critical?

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

38

Prenumbered documents are intended to help:

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

39

At which point in an ordinary sales transaction would a lack of specific authorization be of least concern to the auditor?

A) Determination of discounts.

B) Selling of goods for cash.

C) Granting of credit.

D) Shipment of goods.

A) Determination of discounts.

B) Selling of goods for cash.

C) Granting of credit.

D) Shipment of goods.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

40

Explain each of the following types of documents and indicate the class of transactions in which they are commonly used.1. Customer order2. Shipping document3. Remittance advice4. Sales returns and allowance journal5. Uncollectible account authorization form

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

41

When testing the occurrence objective for sales, the auditor is concerned with the possibility of three types of misstatements. One type is sales being included in the journal for which no shipment was made. Discuss the other two types of misstatements.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

42

When designing substantive tests of transaction for sales, the auditor is concerned with several types of misstatements. What are these types of misstatements and are they intentional or unintentional?

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

43

If sales invoices are automatically calculated and posted by a company's computer system, can the auditor reduce substantive tests of transactions for the accuracy objective?

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

44

Describe the three basic steps an auditor should follow when designing tests of controls and substantive tests of transactions.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

45

Match each of the descriptions with the following terms for each of the documents and records

-A schedule prepared by an independent person when cash is received. It is used to verify whether cash received was recorded and deposited at the correct amounts and on a timely basis.

A) Customer order form

B) Sales order

C) Bill of lading

D) Sales invoice

E) Summary sales report

F) Accounts receivable master file

G) Monthly statement

H) Remittance advice

I) Prelisting of cash receipts

J) Credit memo

K) Uncollectible account authorization form

-A schedule prepared by an independent person when cash is received. It is used to verify whether cash received was recorded and deposited at the correct amounts and on a timely basis.

A) Customer order form

B) Sales order

C) Bill of lading

D) Sales invoice

E) Summary sales report

F) Accounts receivable master file

G) Monthly statement

H) Remittance advice

I) Prelisting of cash receipts

J) Credit memo

K) Uncollectible account authorization form

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

46

Match each of the descriptions with the following terms for each of the documents and records

-An internal document for communicating the description, quantity, and related information for goods ordered by a customer. This is frequently used to indicate credit approval and authorization for shipment.

A) Customer order form

B) Sales order

C) Bill of lading

D) Sales invoice

E) Summary sales report

F) Accounts receivable master file

G) Monthly statement

H) Remittance advice

I) Prelisting of cash receipts

J) Credit memo

K) Uncollectible account authorization form

-An internal document for communicating the description, quantity, and related information for goods ordered by a customer. This is frequently used to indicate credit approval and authorization for shipment.

A) Customer order form

B) Sales order

C) Bill of lading

D) Sales invoice

E) Summary sales report

F) Accounts receivable master file

G) Monthly statement

H) Remittance advice

I) Prelisting of cash receipts

J) Credit memo

K) Uncollectible account authorization form

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

47

Match each of the descriptions with the following terms for each of the documents and records

-A document that accompanies the sales invoice mailed to the customer and which can be returned to the seller with the cash payment.

A) Customer order form

B) Sales order

C) Bill of lading

D) Sales invoice

E) Summary sales report

F) Accounts receivable master file

G) Monthly statement

H) Remittance advice

I) Prelisting of cash receipts

J) Credit memo

K) Uncollectible account authorization form

-A document that accompanies the sales invoice mailed to the customer and which can be returned to the seller with the cash payment.

A) Customer order form

B) Sales order

C) Bill of lading

D) Sales invoice

E) Summary sales report

F) Accounts receivable master file

G) Monthly statement

H) Remittance advice

I) Prelisting of cash receipts

J) Credit memo

K) Uncollectible account authorization form

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

48

Testing from source documents to the journal is useful for testing nonexistent transactions.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

49

In practice, auditors ________ know if a sample is truly a representative one.

A) sometimes

B) often

C) routinely

D) never

A) sometimes

B) often

C) routinely

D) never

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

50

One cause of nonsampling risk is:

A) testing less than the entire population.

B) use of extensive tests of controls.

C) the possibility that a properly- selected sample still may not be representative.

D) ineffective use of audit procedures.

A) testing less than the entire population.

B) use of extensive tests of controls.

C) the possibility that a properly- selected sample still may not be representative.

D) ineffective use of audit procedures.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

51

An auditor can increase the likelihood that a sample is representative by using care in:

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

52

Sampling risk may be controlled by:

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

53

Which of the following is not one of the basic phases in audit sampling?

A) Selecting the sample and performing the tests.

B) Evaluating the results of the sample.

C) Planning the sample.

D) Each of the above is a phase in audit sampling.

A) Selecting the sample and performing the tests.

B) Evaluating the results of the sample.

C) Planning the sample.

D) Each of the above is a phase in audit sampling.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

54

Which of the following methods of sample selection is appropriately used when selecting a random sample?

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

55

The acceptable risk of assessing control risk too low will normally be assessed at a ________ level when auditing a public company.

A) nominal

B) higher

C) lower

D) compensating

A) nominal

B) higher

C) lower

D) compensating

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

56

Which of the following is not one of the types of computer tools used to generate random samples?

A) Random application search software.

B) Random number generators.

C) Generalized audit software.

D) Electronic spreadsheet programs.

A) Random application search software.

B) Random number generators.

C) Generalized audit software.

D) Electronic spreadsheet programs.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

57

In using audit sampling for exception rates, the auditor is primarily interested in determining the

A) average range in which

B) lowest

C) highest

D) none of the above

A) average range in which

B) lowest

C) highest

D) none of the above

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

58

Place the following steps in their proper order:1. Analyze exceptions2. Select the sample3. Define attributes and exception conditions4. State the objectives of the audit test5. Specify the tolerable exception rate

A) 4,3,5,2,1.

B) 1,3,2,4,5.

C) 1,2,3,4,5.

D) 4,3,1,2,5.

A) 4,3,5,2,1.

B) 1,3,2,4,5.

C) 1,2,3,4,5.

D) 4,3,1,2,5.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

59

________ represents the auditor's measure of sampling risk.

A) SER

B) EPER

C) ARACR

D) TER

A) SER

B) EPER

C) ARACR

D) TER

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

60

Which of the following is not determined until after a sample is tested and evaluated?

A) Tolerable exception rate.

B) Computed exception rate.

C) Sample exception rate.

D) Estimated population exception rate.

A) Tolerable exception rate.

B) Computed exception rate.

C) Sample exception rate.

D) Estimated population exception rate.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

61

The acceptable risk of assessing control risk too low is:

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

62

A means of reducing the potential bias in systematic sample selection is to:

A) include a large block of the population.

B) use multiple starts.

C) include only the high- dollar- value items.

D) use a random number table.

A) include a large block of the population.

B) use multiple starts.

C) include only the high- dollar- value items.

D) use a random number table.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

63

When selecting a sample, random numbers may be obtained either with replacement or without replacement. Although both selection methods are theoretically sound, auditors rarely use replacement sampling.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 63 flashcards in this deck.