Deck 7: Additional Topics in Product Costing

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

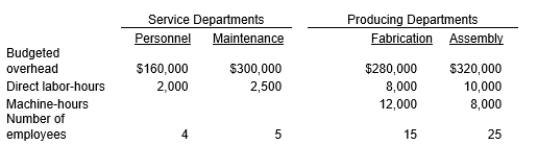

The following information pertains to Blaze Company:

Blaze Company does not divide costs into fixed and variable components. Personnel costs are allocated based on the number of employees, and maintenance costs are allocated based on machine-hours. Predetermined overhead rates for Fabrication and Assembly are based on direct labor-hours (round amounts to dollars).

Blaze Company does not divide costs into fixed and variable components. Personnel costs are allocated based on the number of employees, and maintenance costs are allocated based on machine-hours. Predetermined overhead rates for Fabrication and Assembly are based on direct labor-hours (round amounts to dollars).

If the direct method is used to allocate service department costs, the predetermined overhead rate for the Fabrication Department (rounded to 2 decimal places) would be:

A) $42.00

B) $65.00

C) $64.10

D) $69.55

Blaze Company does not divide costs into fixed and variable components. Personnel costs are allocated based on the number of employees, and maintenance costs are allocated based on machine-hours. Predetermined overhead rates for Fabrication and Assembly are based on direct labor-hours (round amounts to dollars).If the direct method is used to allocate service department costs, the predetermined overhead rate for the Fabrication Department (rounded to 2 decimal places) would be:

A) $42.00

B) $65.00

C) $64.10

D) $69.55

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

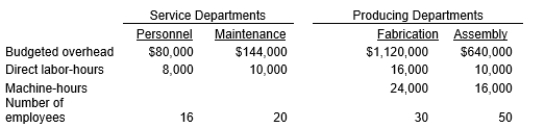

The following information pertains to Weiss Corporation:

Weiss Corporation does not divide costs into fixed and variable components. Personnel costs are allocated based on the number of employees, and maintenance costs are allocated based on machine-hours. Predetermined overhead rates for Fabrication and Assembly are based on direct labor-hours.

Weiss Corporation does not divide costs into fixed and variable components. Personnel costs are allocated based on the number of employees, and maintenance costs are allocated based on machine-hours. Predetermined overhead rates for Fabrication and Assembly are based on direct labor-hours.

If the direct method is used to allocate service department costs, what is the predetermined overhead rate for the Assembly Department (rounded to 2 decimal places)?

Weiss Corporation does not divide costs into fixed and variable components. Personnel costs are allocated based on the number of employees, and maintenance costs are allocated based on machine-hours. Predetermined overhead rates for Fabrication and Assembly are based on direct labor-hours.If the direct method is used to allocate service department costs, what is the predetermined overhead rate for the Assembly Department (rounded to 2 decimal places)?

Question

Question

Ed & Sons Auto Company incurred $60,000 of indirect advertising costs for its operations. The following 2017 data have been collected for its three departments:

Required:

Required:

Determine the costs allocated to each department using the following allocation bases:

a. Direct advertising costs

b. Newspaper ad space

c. Sales

Required:Determine the costs allocated to each department using the following allocation bases:

a. Direct advertising costs

b. Newspaper ad space

c. Sales

Question

Question

Question

Eastern Springs Company uses two producing departments (A and B) and two service departments (S1 and S2). The costs incurred in S1 and S2 are allocated to Departments A and B and included in their factory overhead rates for costing products. S1 costs are allocated based on the number of employees, S2 costs are allocated based on direct labor-hours, and the production departmental overhead rates are also based on direct labor hours.

The following data are available for a recent period:

Required:

Required:

a. Prepare a schedule allocating the service department costs to the producing departments using the step allocation method. The department providing the greatest percentage of interdepartmental services to other service departments should be allocated first.

b. Determine the overhead rates per direct labor hour for Departments A and B.

The following data are available for a recent period:

Required:a. Prepare a schedule allocating the service department costs to the producing departments using the step allocation method. The department providing the greatest percentage of interdepartmental services to other service departments should be allocated first.

b. Determine the overhead rates per direct labor hour for Departments A and B.

Question

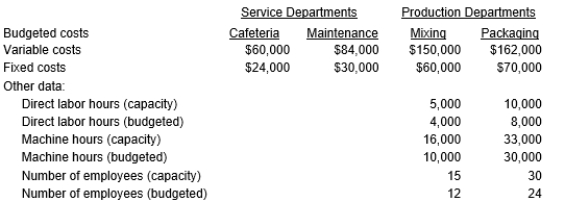

Glenwood Company applies factory overhead in its two producing departments using a predetermined rate based on budgeted machine hours in the Mixing Department and based on budgeted labor-hours in the Packaging Department. Variable cafeteria costs are allocated to the producing departments based on budgeted number of employees, and fixed costs are allocated based on the capacity number of employees. Variable maintenance costs are allocated on the budgeted number of direct labor-hours, and fixed costs are allocated on direct labor hour capacity.

The data concerning next year's operations are as follows:

Required:

Required:

a. Prepare a schedule showing a direct allocation of budgeted service department costs to producing departments.

b. Determine the predetermined overhead rate for the producing departments.

The data concerning next year's operations are as follows:

Required:a. Prepare a schedule showing a direct allocation of budgeted service department costs to producing departments.

b. Determine the predetermined overhead rate for the producing departments.

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/57

Play

Full screen (f)

Deck 7: Additional Topics in Product Costing

1

A cost that is assigned to a department as a result of an indirect allocation, or reassignment, from another department, such as a service department, would be classified as an indirect departmental cost.

True

2

Service departments within the context of management accounting typically provide services, such as repairs to products under warranty, directly to customers.

False

3

The linear algebra method of allocating service department costs does not recognize any interdepartmental services?

False

4

The step method of allocating service department costs gives only partial recognition to interdepartmental services.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

5

The reciprocal method of allocating service department costs is also known as linear algebra method.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

6

The purpose of dual cost allocation rates is to provide one set of numbers for managers' internal use and one for external investors.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

7

Inventory storage costs are reduced in just-in-time (JIT) inventory management.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

8

Cycle time is a perfect measure of value added to a product.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

9

Which of the following cost categories would most likely use the price of orders placed with suppliers as its allocation base?

A) Accounting

B) Maintenance and repairs

C) Personnel

D) Purchasing

A) Accounting

B) Maintenance and repairs

C) Personnel

D) Purchasing

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

10

Which of the following cost categories would most likely use the number of orders placed with suppliers as its allocation base?

A) Accounting

B) Maintenance and repairs

C) Personnel

D) Purchasing

A) Accounting

B) Maintenance and repairs

C) Personnel

D) Purchasing

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

11

Which of the following costs are most difficult to trace to specific units of production or other cost objectives?

A) Direct labor costs

B) Indirect costs

C) Prime costs

D) Raw materials costs

A) Direct labor costs

B) Indirect costs

C) Prime costs

D) Raw materials costs

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

12

Which of the following is not a key element of any indirect cost allocation system?

A) An accurate measurement of direct labor hours

B) A cost allocation base

C) A cost objective

D) A cost pool

A) An accurate measurement of direct labor hours

B) A cost allocation base

C) A cost objective

D) A cost pool

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

13

The following information pertains to Blaze Company:

Blaze Company does not divide costs into fixed and variable components. Personnel costs are allocated based on the number of employees, and maintenance costs are allocated based on machine-hours. Predetermined overhead rates for Fabrication and Assembly are based on direct labor-hours (round amounts to dollars).

If the direct method is used to allocate service department costs, the predetermined overhead rate for the Fabrication Department (rounded to 2 decimal places) would be:

A) $42.00

B) $65.00

C) $64.10

D) $69.55

Blaze Company does not divide costs into fixed and variable components. Personnel costs are allocated based on the number of employees, and maintenance costs are allocated based on machine-hours. Predetermined overhead rates for Fabrication and Assembly are based on direct labor-hours (round amounts to dollars).If the direct method is used to allocate service department costs, the predetermined overhead rate for the Fabrication Department (rounded to 2 decimal places) would be:

A) $42.00

B) $65.00

C) $64.10

D) $69.55

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

14

JD Company has two service departments whose direct department costs are $15,000 and $25,000, respectively, and two producing departments whose direct department costs are $210,000 and $200,000, respectively.

The combined total department costs for the producing departments after allocating the service departments are:

A) $460,000

B) $415,000

C) $400,000

D) $450,000

The combined total department costs for the producing departments after allocating the service departments are:

A) $460,000

B) $415,000

C) $400,000

D) $450,000

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

15

Realty Company allocates common Building Department costs to producing departments (A and and B) based on space occupied, and it allocates common Personnel Department costs based on the number of employees. Space occupancy and employee data are as follows: If Realty Company uses the direct allocation method, the ratio representing the portion of Personnel costs allocated to Department A is:

A) 40/83

B) 75/83

C) 45/75

D) None of the above

A) 40/83

B) 75/83

C) 45/75

D) None of the above

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

16

Jackson Company has two service departments (S1 and S2) and two producing departments (A and B) .

?Department S1 serves Departments S2, A, and B in the following percentages, respectively: 15%, 25%, and 60%.

?Department S2 serves Departments S1, A, and B in the following percentages, respectively: 0%, 70%, and 30%.

?Direct department costs for S1, S2, A, and B are $200,000, $16,000, $210,000, and $185,000, respectively.

If Jackson uses the step method of allocating service department costs beginning with Department S1, what is the total amount of cost that will be allocated from S2 to Department A?

A) $ 12,800

B) $105,000

C) $ 32,200

D) $-0-

?Department S1 serves Departments S2, A, and B in the following percentages, respectively: 15%, 25%, and 60%.

?Department S2 serves Departments S1, A, and B in the following percentages, respectively: 0%, 70%, and 30%.

?Direct department costs for S1, S2, A, and B are $200,000, $16,000, $210,000, and $185,000, respectively.

If Jackson uses the step method of allocating service department costs beginning with Department S1, what is the total amount of cost that will be allocated from S2 to Department A?

A) $ 12,800

B) $105,000

C) $ 32,200

D) $-0-

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

17

Which of the following allocation methods fully recognizes services that service departments provide to each other?

A) The direct method

B) The linear algebra method

C) The step method

D) None of the above

A) The direct method

B) The linear algebra method

C) The step method

D) None of the above

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

18

An element of just-in-time processing is:

A) Dependable suppliers who are willing to deliver on short notice.

B) A multi-skilled workforce

C) A total quality control system.

D) All of these apply.

A) Dependable suppliers who are willing to deliver on short notice.

B) A multi-skilled workforce

C) A total quality control system.

D) All of these apply.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

19

Which of the following statements describes just-in-time (JIT) inventory management?

A) JIT is an effective approach for shifting inventory costs to vendors.

B) JIT is a comprehensive management philosophy that stresses attitudes that lead to minimum level inventories.

C) JIT is a customer service driven strategy that seeks to strategically produce some excess inventory to guarantee inventories are always available to customers in a timely manner.

D) JIT is only used when a company's vendors ship goods when they are ordered.

A) JIT is an effective approach for shifting inventory costs to vendors.

B) JIT is a comprehensive management philosophy that stresses attitudes that lead to minimum level inventories.

C) JIT is a customer service driven strategy that seeks to strategically produce some excess inventory to guarantee inventories are always available to customers in a timely manner.

D) JIT is only used when a company's vendors ship goods when they are ordered.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

20

Which of the following is not a just-in-time inventory management approach?

A) Developing long-term relationships with vendors

B) Accepting vendor deliveries directly to the shop floor

C) Establishing procedures for production employees to order raw materials from vendors

D) Selecting only the vendors who can provide inventory at the lowest price

A) Developing long-term relationships with vendors

B) Accepting vendor deliveries directly to the shop floor

C) Establishing procedures for production employees to order raw materials from vendors

D) Selecting only the vendors who can provide inventory at the lowest price

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

21

Cycle time is comprised of each of the following components except:

A) Planning time

B) Set-up time

C) Waiting time

D) Inspection time

A) Planning time

B) Set-up time

C) Waiting time

D) Inspection time

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

22

The Kanban system developed by the Japanese is also known as:

A) The material pull system

B) The weighted average system

C) The activity driven system

D) The automated ordering system

A) The material pull system

B) The weighted average system

C) The activity driven system

D) The automated ordering system

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

23

Lowering cycle times reduces the need for:

A) Raw materials

B) Speculative inventories

C) Inspection

D) Materials handling

A) Raw materials

B) Speculative inventories

C) Inspection

D) Materials handling

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

24

Just-in-time is an approach toward managing:

A) Production efficiency

B) Inventories

C) Labor

D) Costs of production inputs

A) Production efficiency

B) Inventories

C) Labor

D) Costs of production inputs

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

25

Which of the following is not an element of just-in-time management philosophy?

A) Securing long-term contracts with suppliers

B) Reducing set-up time

C) Seeking to eliminate maintenance expense

D) Creating value for the end user

A) Securing long-term contracts with suppliers

B) Reducing set-up time

C) Seeking to eliminate maintenance expense

D) Creating value for the end user

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

26

Which of the following is an anticipated result of implementing a just-in-time management philosophy?

A) A smaller number of raw material orders will be placed.

B) Inventory carrying costs will be lowered.

C) The purchasing manager will have an increased role in ordering raw materials.

D) Inventory carrying costs will be eliminated.

A) A smaller number of raw material orders will be placed.

B) Inventory carrying costs will be lowered.

C) The purchasing manager will have an increased role in ordering raw materials.

D) Inventory carrying costs will be eliminated.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

27

All of the following are key elements of a just-in-time philosophy, except:

A) Increased coordination throughout the value chain

B) Reduced inventory

C) Reduced production times

D) Lack of a need for accurate product cost information

A) Increased coordination throughout the value chain

B) Reduced inventory

C) Reduced production times

D) Lack of a need for accurate product cost information

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

28

Which of the following components of cycle time add value to the product?

A) Setup time

B) Processing time

C) Movement time

D) Inspection time

A) Setup time

B) Processing time

C) Movement time

D) Inspection time

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

29

Which of the following elements of cycle time do not add value to the product?

A) Setup time

B) Move time

C) Wait time

D) All of the above

A) Setup time

B) Move time

C) Wait time

D) All of the above

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

30

The use of flexible manufacturing systems, properly sequencing jobs, and properly placing tools will minimize:

A) Setup time

B) Process time

C) Move time

D) Inspection time

A) Setup time

B) Process time

C) Move time

D) Inspection time

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

31

The ratio of value-added manufacturing time to the total of both value and non-value-added manufacturing times is known as:

A) Cycle efficiency.

B) Cycle time processing.

C) The value ratio.

D) Productivity turnover.

A) Cycle efficiency.

B) Cycle time processing.

C) The value ratio.

D) Productivity turnover.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

32

Which of the following is not a just-in-time supportive performance measure?

A) Inventory turnover

B) Cycle time

C) Unitized cost of goods sold

D) Cycle efficiency

A) Inventory turnover

B) Cycle time

C) Unitized cost of goods sold

D) Cycle efficiency

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

33

Ideally, cycle time would consist of only which of the following components?

A) Process time

B) Sales time

C) Move time

D) Just-in-time

A) Process time

B) Sales time

C) Move time

D) Just-in-time

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

34

The total time required to produce a unit or batch is known as:

A) Process time

B) Productivity

C) Cycle time

D) Work-in-process turnover

A) Process time

B) Productivity

C) Cycle time

D) Work-in-process turnover

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

35

Traditional costing systems often commit the cardinal sin of overproduction in a lean production company if managers are:

A) Ordering excess inventory, to achieve quantity discounts and favorable prices

B) Refusing to halt production to determine the cause of a quality problem, in order to avoid having idle employees and equipment

C) Trying to obtain lower fixed costs per unit under absorption

D) All of the above

A) Ordering excess inventory, to achieve quantity discounts and favorable prices

B) Refusing to halt production to determine the cause of a quality problem, in order to avoid having idle employees and equipment

C) Trying to obtain lower fixed costs per unit under absorption

D) All of the above

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

36

Which lean accounting model assigns all manufacturing costs to Cost of Goods Sold and then subtracts inventory costs from the Cost of Goods Sold account?

A) Absorption costing

B) Backflush costing

C) Electronic Data Interchange

D) Value-added inventory accounting

A) Absorption costing

B) Backflush costing

C) Electronic Data Interchange

D) Value-added inventory accounting

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

37

A goal of performance reporting in a lean accounting system is:

A) To provide information to managers for constant improvement in cost efficiency and quality.

B) To meet the reporting standards for generally accepted accounting principles.

C) To provide full disclosure to the public about manufacturing costs and efficiencies.

D) To show which producing departments are using approximately the same or different percentage of services.

A) To provide information to managers for constant improvement in cost efficiency and quality.

B) To meet the reporting standards for generally accepted accounting principles.

C) To provide full disclosure to the public about manufacturing costs and efficiencies.

D) To show which producing departments are using approximately the same or different percentage of services.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

38

Amber Company uses two producing departments (A and B) and two service departments (S1 and S2). The costs incurred in S1 and S2 are allocated to Departments A and B and included in their factory overhead rates for costing products. S1 costs are allocated based on the number of employees, S2 costs are allocated based on direct labor-hours, and the production departmental overhead rates are also based on direct labor-hours. The following data are available for a recent period: What is the order of allocation under the step cost allocation method?

A) Service department S1 is allocated first and Service department S2 allocated second.

B) Service department S2 is allocated first and Service department S1 allocated second.

C) Service department S1 and S2 are allocated equally, so order does not matter.

D) None of above

A) Service department S1 is allocated first and Service department S2 allocated second.

B) Service department S2 is allocated first and Service department S1 allocated second.

C) Service department S1 and S2 are allocated equally, so order does not matter.

D) None of above

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

39

Ballistic Company uses two producing departments (A and B) and two service departments (S1 and S2). The costs incurred in S1 and S2 are allocated to Departments A and B and included in their factory overhead rates for costing products. S1 costs are allocated based on the number of employees, S2 costs are allocated based on direct labor hours, and the production departmental overhead rates are also based on direct labor hours. The following data are available for a recent period: Assuming S2 Service Department is allocated first, what is the cost allocated to S1 Service Department, Department A, and Department B?

A) Service department S1 = $3,600, Department A = $18,000, Department B = $14,400

B) Service department S1 = $7,200, Department A = $36,000, Department B = $28,800

C) Service department S1 = $1,800, Department A = $ 9,000, Department B = $ 7,200

D) Service department S1 = $3,800, Department A = $16,000, Department B = $13,600

A) Service department S1 = $3,600, Department A = $18,000, Department B = $14,400

B) Service department S1 = $7,200, Department A = $36,000, Department B = $28,800

C) Service department S1 = $1,800, Department A = $ 9,000, Department B = $ 7,200

D) Service department S1 = $3,800, Department A = $16,000, Department B = $13,600

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

40

Callaway Company uses two producing departments (A and B) and two service departments (S1 and S2). The costs incurred in S1 and S2 are allocated to Departments A and B and included in their factory overhead rates for costing products. S1 costs are allocated based on the number of employees, S2 costs are allocated based on direct labor hours, and the production departmental overhead rates are also based on direct labor hours. The following data are available for a recent period: Assume S2 Service Department costs are allocated first and the cost allocated to S1 Service Department from S2 is $3,600.

What is the cost allocated to each of the two producing departments by Service Department S1?

A) Department A = $15,360, Department B = $ 8,640

B) Department A = $36,000, Department B = $28,800

C) Department A = $ 9,000, Department B = $ 7,200

D) Department A = $17,644, Department B = $ 9,936

What is the cost allocated to each of the two producing departments by Service Department S1?

A) Department A = $15,360, Department B = $ 8,640

B) Department A = $36,000, Department B = $28,800

C) Department A = $ 9,000, Department B = $ 7,200

D) Department A = $17,644, Department B = $ 9,936

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

41

Kent Inc. provided the following data for 2016 and 2017:

What are the inventory turnover ratio and the gross margin return on inventory investment for 2017?

A) Inventory turnover ratio = 3.00 times and the Gross margin return on inventory investment = 2%

B) Inventory turnover ratio = 2.00 times and the Gross margin return on inventory investment = 300%

C) Inventory turnover ratio = 3.09 times and the Gross margin return on inventory investment = 20%

D) Inventory turnover ratio = 3.00 times and the Gross margin return on inventory investment = 200%

What are the inventory turnover ratio and the gross margin return on inventory investment for 2017?

A) Inventory turnover ratio = 3.00 times and the Gross margin return on inventory investment = 2%

B) Inventory turnover ratio = 2.00 times and the Gross margin return on inventory investment = 300%

C) Inventory turnover ratio = 3.09 times and the Gross margin return on inventory investment = 20%

D) Inventory turnover ratio = 3.00 times and the Gross margin return on inventory investment = 200%

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

42

Buckhannon Jewelry Company is in the process of selecting cost drivers that could be used as the bases for allocating various service department costs to its three production divisions: Cutting, Milling and Finishing.

Required: Select the most appropriate allocation base for each type of service department cost described in (a) through (j). Select from among the four allocation bases in the following list. In recording your answer, use the abbreviations provided in the list. Some allocation bases will be used for more than one answer.

List of Possible Choices of Allocation Bases

EMP = Number of Employees

UPC = Units of Production Capacity

SQF = Square Footage Occupied

POH = Budgeted Production Department Overhead

Type of Service Department Cost to be Allocated to the Producing Divisions

Required: Select the most appropriate allocation base for each type of service department cost described in (a) through (j). Select from among the four allocation bases in the following list. In recording your answer, use the abbreviations provided in the list. Some allocation bases will be used for more than one answer.

List of Possible Choices of Allocation Bases

EMP = Number of Employees

UPC = Units of Production Capacity

SQF = Square Footage Occupied

POH = Budgeted Production Department Overhead

Type of Service Department Cost to be Allocated to the Producing Divisions

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

43

Alpine Company has two service departments (S1 and S2) and two producing departments (P1 and P2). Department S1 costs are allocated on the basis of number of employees, and Department S2 costs are allocated on the basis of space occupied expressed in square feet. Data on direct department costs, number of employees, and space occupied are as follows:

If Alpine uses the direct method, what is the ratio representing the portion of Department S2 allocated to P2?

If Alpine uses the direct method, what is the ratio representing the portion of Department S2 allocated to P2?

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

44

Jacklyn Company has three service departments whose direct department costs are $20,000, $40,000, and $60,000, respectively, and two producing departments whose direct department costs are $400,000 and $600,000, respectively.

Calculate the combined total department costs for the producing departments after allocation of the service departments.

Calculate the combined total department costs for the producing departments after allocation of the service departments.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

45

York Company has two service departments, Maintenance Department and Personnel Department, and two producing departments, X and Y. The Maintenance Department costs of $120,000 are allocated on the basis of standard service hours used. The Personnel Department costs of $18,000 are allocated on the basis of number of employees. The direct costs of Departments X and Y are $18,000 and $30,000, respectively. Data on standard service-hours and number of employees are as follows:

Using the direct method, calculate the cost of the Personnel Department allocated to Department X and to Department Y.

Using the direct method, calculate the cost of the Personnel Department allocated to Department X and to Department Y.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

46

York Company has two service departments, Maintenance Department and Personnel Department, and two producing departments, X and Y. The Maintenance Department costs of $120,000 are allocated on the basis of standard service hours used. The Personnel Department costs of $18,000 are allocated on the basis of number of employees. The direct costs of Departments X and Y are $18,000 and $30,000, respectively. Data on standard service-hours and number of employees are as follows:

Using the step method, if Personnel Department costs are allocated first, calculate the cost of Maintenance Department allocation to Department X.

Using the step method, if Personnel Department costs are allocated first, calculate the cost of Maintenance Department allocation to Department X.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

47

York Company has two service departments, Maintenance Department and Personnel Department, and two producing departments, X and Y. The Maintenance Department costs of $120,000 are allocated on the basis of standard service hours used. The Personnel Department costs of $18,000 are allocated on the basis of number of employees. The direct costs of Departments X and Y are $18,000 and $30,000, respectively. Data on standard service hours and number of employees are as follows:

Calculate the total overhead costs associated with Departments X and Y after allocating the Maintenance and Personnel Departments using the direct method.

Calculate the total overhead costs associated with Departments X and Y after allocating the Maintenance and Personnel Departments using the direct method.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

48

Rapport Manufacturing Company has two service departments, Maintenance Department and Personnel Department, and two producing departments, X and Y. The Maintenance Department costs of $60,000 are allocated on the basis of standard service used. The Personnel Department costs of $9,000 are allocated on the basis of number of employees. The direct costs of Departments X and Y are $72,000 and $120,000, respectively. Data on standard service-hours and number of employees are as follows:

Calculate the total overhead costs associated with Department Y after allocating the Maintenance and Personnel Departments using the direct method.

Calculate the total overhead costs associated with Department Y after allocating the Maintenance and Personnel Departments using the direct method.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

49

The following information pertains to Weiss Corporation:

Weiss Corporation does not divide costs into fixed and variable components. Personnel costs are allocated based on the number of employees, and maintenance costs are allocated based on machine-hours. Predetermined overhead rates for Fabrication and Assembly are based on direct labor-hours.

If the direct method is used to allocate service department costs, what is the predetermined overhead rate for the Assembly Department (rounded to 2 decimal places)?

Weiss Corporation does not divide costs into fixed and variable components. Personnel costs are allocated based on the number of employees, and maintenance costs are allocated based on machine-hours. Predetermined overhead rates for Fabrication and Assembly are based on direct labor-hours.If the direct method is used to allocate service department costs, what is the predetermined overhead rate for the Assembly Department (rounded to 2 decimal places)?

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

50

The Helix Manufacturing Company has two Production Departments: Mixing and Molding. Each of these two departments uses the services provided by the Utilities and Human Resources Departments, which both support the production functions and each other's functions as well. Helix uses the direct method of allocating these service department costs to the production departments. Utilities are allocated on the basis of hours of department operations and Human Resources is allocated on the basis of departmental direct labor hours. Last period the following costs were recorded:

Production Department data:

Required:

a. Determine the amount of Utilities costs allocated to the Mixing and Molding Departments using the direct method of allocating service department costs.

b. Determine the amount of Human Resource costs allocated to the Mixing and Molding Departments using the direct method of allocating service department costs.

c. Determine the total overhead costs of the Mixing and Molding Departments if the direct method of allocating department costs is used.

Production Department data:

Required:

a. Determine the amount of Utilities costs allocated to the Mixing and Molding Departments using the direct method of allocating service department costs.

b. Determine the amount of Human Resource costs allocated to the Mixing and Molding Departments using the direct method of allocating service department costs.

c. Determine the total overhead costs of the Mixing and Molding Departments if the direct method of allocating department costs is used.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

51

Ed & Sons Auto Company incurred $60,000 of indirect advertising costs for its operations. The following 2017 data have been collected for its three departments:

Required:

Determine the costs allocated to each department using the following allocation bases:

a. Direct advertising costs

b. Newspaper ad space

c. Sales

Required:Determine the costs allocated to each department using the following allocation bases:

a. Direct advertising costs

b. Newspaper ad space

c. Sales

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

52

The Woodridge Manufacturing Company has two Production Departments: Cutting and Pasting. Each of these two departments uses the services provided by the Computing and Maintenance Departments, which both support the production functions and each other's functions as well. Woodridge uses the step method of allocating these service department costs to the production departments. Computing is allocated on the basis of hours of department operations and Maintenance is allocated on the basis of departmental direct labor hours. Last period the following costs were recorded:

Production Department data:

Required:

a. Determine the amount of Maintenance costs allocated to the Cutting and Pasting Departments using the step method of allocating service department costs.

b. Determine the amount of Computing costs allocated to the Cutting and Pasting Departments using the step method of allocating service department costs.

c. Determine the total overhead costs of the Cutting and Pasting Departments when this method of allocating service department costs is used.

Production Department data:

Required:

a. Determine the amount of Maintenance costs allocated to the Cutting and Pasting Departments using the step method of allocating service department costs.

b. Determine the amount of Computing costs allocated to the Cutting and Pasting Departments using the step method of allocating service department costs.

c. Determine the total overhead costs of the Cutting and Pasting Departments when this method of allocating service department costs is used.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

53

BWT Company has two service departments (S1 and S2) and two producing departments (P1 and P2). Estimated direct costs and percentages of services used by other departments are as follows:

Required:

a. Prepare a schedule allocating the service department costs to the producing departments using the direct allocation method.

b. Prepare a schedule allocating the service department costs to the producing departments using the step allocation method.

Required:

a. Prepare a schedule allocating the service department costs to the producing departments using the direct allocation method.

b. Prepare a schedule allocating the service department costs to the producing departments using the step allocation method.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

54

Eastern Springs Company uses two producing departments (A and B) and two service departments (S1 and S2). The costs incurred in S1 and S2 are allocated to Departments A and B and included in their factory overhead rates for costing products. S1 costs are allocated based on the number of employees, S2 costs are allocated based on direct labor-hours, and the production departmental overhead rates are also based on direct labor hours.

The following data are available for a recent period:

Required:

a. Prepare a schedule allocating the service department costs to the producing departments using the step allocation method. The department providing the greatest percentage of interdepartmental services to other service departments should be allocated first.

b. Determine the overhead rates per direct labor hour for Departments A and B.

The following data are available for a recent period:

Required:a. Prepare a schedule allocating the service department costs to the producing departments using the step allocation method. The department providing the greatest percentage of interdepartmental services to other service departments should be allocated first.

b. Determine the overhead rates per direct labor hour for Departments A and B.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

55

Glenwood Company applies factory overhead in its two producing departments using a predetermined rate based on budgeted machine hours in the Mixing Department and based on budgeted labor-hours in the Packaging Department. Variable cafeteria costs are allocated to the producing departments based on budgeted number of employees, and fixed costs are allocated based on the capacity number of employees. Variable maintenance costs are allocated on the budgeted number of direct labor-hours, and fixed costs are allocated on direct labor hour capacity.

The data concerning next year's operations are as follows:

Required:

a. Prepare a schedule showing a direct allocation of budgeted service department costs to producing departments.

b. Determine the predetermined overhead rate for the producing departments.

The data concerning next year's operations are as follows:

Required:a. Prepare a schedule showing a direct allocation of budgeted service department costs to producing departments.

b. Determine the predetermined overhead rate for the producing departments.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

56

Explain the concept of just-in-time inventory management and its relationship to the lean production concept.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

57

Explain how traditional performance evaluation/performance systems such as standard costing conflict with the lean production concept.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 57 flashcards in this deck.