Deck 3: Partially Owned Created Subsidiaries & Variable Interest Entities

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

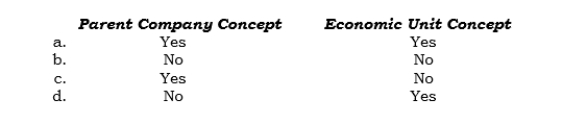

_____ The noncontrolling interest in a created subsidiary's net income is based on the subsidiary's reported net income under which of the following concepts?

Question

Question

Question

Question

Question

Question

Question

_____ The NCI in a created subsidiary's net assets is based on the subsidiary's book values under which of the following concepts?

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

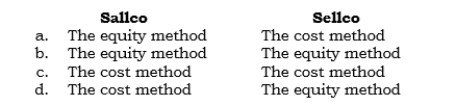

_____ Pallco justifiably does not consolidate two of its 100%-owned subsidiaries (Sallco and Sellco). Sallco is (a) a foreign subsidiary and (b) prohibited by the foreign government from paying dividends. Sellco is (a) a domestic subsidiary acquired two months ago in the purchase of a conglomerate and (b) in process of being sold. What would be the most likely method of accounting for each of these unconsolidated subsidiaries?

Question

Question

Question

Question

matching

based on the information given.

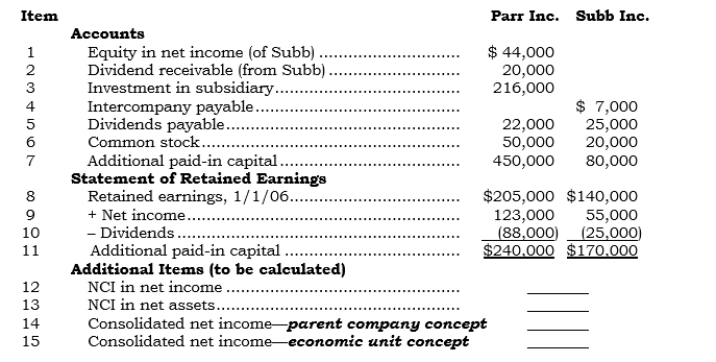

The following (a) seven account balances and (b) statements of retained earnings were obtained from the separate company statements of Parr Inc. and its 80%-owned created sub-sidiary, Subb Inc. (Parr's only subsidiary), at the end of 2006:

When Subb was created (in 2004, 20% of the common shares it issued were sold to private investors.

When Subb was created (in 2004, 20% of the common shares it issued were sold to private investors.

Requirement 1:

How is each of the first 11 preceding items reported in Parr's 2006 consolidated statements? Use the following list of possible answer codes in the answer columns:

-_____(item 1)

A) Report at the amount shown in Subb's separate statements.

B) Report at the amount shown in Parr's separate statements.

C) Report at less than the sum of the amounts shown in Parr's and Subb's separate statements.

D) Report at the sum of the amounts shown in Parr's and Subb's separate statements.

E) Do not report this item in the consolidated statements or in the separate statements of either Parr or Subb.

F) Do not report this item in the consolidated statements.

G) Create this item in the consolidation process.

based on the information given.

The following (a) seven account balances and (b) statements of retained earnings were obtained from the separate company statements of Parr Inc. and its 80%-owned created sub-sidiary, Subb Inc. (Parr's only subsidiary), at the end of 2006:

When Subb was created (in 2004, 20% of the common shares it issued were sold to private investors.Requirement 1:

How is each of the first 11 preceding items reported in Parr's 2006 consolidated statements? Use the following list of possible answer codes in the answer columns:

-_____(item 1)

A) Report at the amount shown in Subb's separate statements.

B) Report at the amount shown in Parr's separate statements.

C) Report at less than the sum of the amounts shown in Parr's and Subb's separate statements.

D) Report at the sum of the amounts shown in Parr's and Subb's separate statements.

E) Do not report this item in the consolidated statements or in the separate statements of either Parr or Subb.

F) Do not report this item in the consolidated statements.

G) Create this item in the consolidation process.

Question

matching

based on the information given.

The following (a) seven account balances and (b) statements of retained earnings were obtained from the separate company statements of Parr Inc. and its 80%-owned created sub-sidiary, Subb Inc. (Parr's only subsidiary), at the end of 2006:

When Subb was created (in 2004, 20% of the common shares it issued were sold to private investors.

Requirement 1:

How is each of the first 11 preceding items reported in Parr's 2006 consolidated statements? Use the following list of possible answer codes in the answer columns:

-_____(item 2)

A) Report at the amount shown in Subb's separate statements.

B) Report at the amount shown in Parr's separate statements.

C) Report at less than the sum of the amounts shown in Parr's and Subb's separate statements.

D) Report at the sum of the amounts shown in Parr's and Subb's separate statements.

E) Do not report this item in the consolidated statements or in the separate statements of either Parr or Subb.

F) Do not report this item in the consolidated statements.

G) Create this item in the consolidation process.

based on the information given.

The following (a) seven account balances and (b) statements of retained earnings were obtained from the separate company statements of Parr Inc. and its 80%-owned created sub-sidiary, Subb Inc. (Parr's only subsidiary), at the end of 2006:

When Subb was created (in 2004, 20% of the common shares it issued were sold to private investors.Requirement 1:

How is each of the first 11 preceding items reported in Parr's 2006 consolidated statements? Use the following list of possible answer codes in the answer columns:

-_____(item 2)

A) Report at the amount shown in Subb's separate statements.

B) Report at the amount shown in Parr's separate statements.

C) Report at less than the sum of the amounts shown in Parr's and Subb's separate statements.

D) Report at the sum of the amounts shown in Parr's and Subb's separate statements.

E) Do not report this item in the consolidated statements or in the separate statements of either Parr or Subb.

F) Do not report this item in the consolidated statements.

G) Create this item in the consolidation process.

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/138

Play

Full screen (f)

Deck 3: Partially Owned Created Subsidiaries & Variable Interest Entities

1

Another term for the noncontrolling interest is the ____________________________.

minority interest

2

A manner of consolidation in which the noncontrolling interest is not presented in the consolidated statements is called _________________________________.

proportional consolidation

3

Under current GAAP, ________________________________________ consolidation is required.

full

4

A concept of viewing the noncontrolling interest that assumes that a new reporting entity does not result from the consolidation process is the ______________________________________concept.

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

5

A concept of viewing the noncontrolling interest that assumes that a new reporting entity results from the consolidation process is the _________________________ concept.

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

6

Dividends paid to noncontrolling shareholders are treated as a(n) _______________ __________________ of the noncontrolling interest from a consolidated perspective.

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

7

The three allowable methods of valuing an investment in an unconsolidated subsidiary are the _________________________ method, the _________________________ method, and the __________________________ method.

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

8

The fair value method of valuing an investment in an unconsolidated subsidiary can be used only if the subsidiary is _________________________________.

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

9

The fair value method of valuing an investment in an unconsolidated partially owned subsidiary can be used only if the subsidiary's common stock has a _______________________________________ fair value.

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

10

Controlling an entity by means of a voting majority interest is referred to as having ________________________________________ control.

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

11

Controlling an entity by means other than a voting majority interest is referred to as having ________________________________________ control.

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

12

An entity that is subject to consolidation pursuant to FASB FIN 46 is called a __________________________________ .

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

13

The company that must consolidate a variable interest entity is called the __________________________________ .

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

14

An entity that is created to serve a specific, predetermined, limited purpose by a sponsoring entity is usually referred to, in practice, as a ____________________________ .

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

15

FIN 46 allows an exception to consolidation for _____________________________ .

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

16

Events that cause a reassessment of determining the primary beneficiary are called _______________________________ .

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

17

Proportional consolidation is not allowed under current GAAP.

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

18

Under proportional consolidation, no amounts are presented in the consolidated statements for the noncontrolling interest.

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

19

Both proportional consolidation and full consolidation are allowed under current GAAP.

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

20

For partially owned subsidiaries, part of the rationale of full consolidation is that the parent has a separable percentage interest in each individual asset, liability, and income statement account of the subsidiary.

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

21

For partially owned subsidiaries, part of the rationale of full consolidation is that the parent controls the subsidiary and therefore should include (a) all the assets and liabilities under its control and (b) all income statement activities resulting from its control.

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

22

The rationale underlying the parent company concept is that the reporting entity does not change as a result of the consolidation process.

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

23

Under the parent company concept, the interest of the noncontrolling shareholders is considered to be an equity interest of the consolidated reporting entity.

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

24

The rationale of the economic unit concept is that the reporting entity does change as a result of the consolidation process.

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

25

Under the economic unit concept, the interest of the noncontrolling shareholders is considered to be an equity interest of the consolidated reporting entity.

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

26

Both the parent company concept and the economic unit concept are full consolidation approaches.

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

27

Under current GAAP, both the parent company concept and the economic unit concept are allowed.

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

28

Under current GAAP, only the parent company concept is allowed.

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

29

Under the parent company concept, the NCI in the subsidiary's net income is presented as a deduction in arriving at consolidated net income.

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

30

Under the economic unit concept, the NCI in the subsidiary's net income is presented as a deduction in arriving at consolidated net income.

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

31

Under the parent company concept, the NCI in the subsidiary's net assets is presented as part of consolidated stockholders' equity.

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

32

Under the economic unit concept, the NCI in the subsidiary's net assets is presented as part of consolidated stockholders' equity.

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

33

If a subsidiary is not consolidated, the parent can arbitrarily choose between either the equity method or the cost method.

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

34

If a subsidiary is not consolidated, the equity method can be used only if significant influence exists.

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

35

A foreign subsidiary is not consolidated because the foreign government has imposed dividend payment restrictions. The cost method would usually be used instead of the equity method in accounting for the investment in the subsidiary.

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

36

An 80% owned subsidiary is not consolidated because control has been lost. The cost method cannot be used to account for the investment in the subsidiary.

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

37

An 80% owned subsidiary is not consolidated because control has been lost. The cost method cannot be used to account for the investment in the subsidiary if the subsidiary's common stock has a readily determinable fair value.

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

38

An 80% owned subsidiary is not consolidated because control has been lost. The cost method cannot be used to account for the investment in the subsidiary if the parent has significant influence.

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

39

The equity method can be used in lieu of consolidation.

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

40

Having certain financial arrangements with another entity that result in control is having effective legal control.

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

41

Effective control encompasses legal control.

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

42

All VIEs, by definition, have a primary beneficiary.

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

43

An SPE can be a VIE.

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

44

All VIEs must be SPEs as well.

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

45

The variable interest holder having the highest percentage interest of all of the variable interest holders must consolidate the VIE.

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

46

A loan guarantee to a VIE's lenders could be a potential variable interest.

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

47

A call option held by Entity A on Entity B's assets could be a potential variable interest.

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

48

All VIEs must be consolidated.

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

49

If Entity A will absorb a majority of a VIE's expected losses and Entity B will receive a majority of that VIE's expected residual returns, both entities must consolidate the VIE.

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

50

The consolidation procedures for a VIE are similar to those for consolidating a created subsidiary.

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

51

In consolidating a VIE, the VIEs assets and liabilities must be initially valued at their book values-not their fair values.

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

52

In consolidating a VIE, goodwill can never be reported.

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

53

In consolidating a VIE, the noncontrolling interest is initially valued at its fair value-not its book value.

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

54

The concept of legal control encompasses the concept of effective control.

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

55

_____ Which of the following methods does not report any amounts for the noncontrolling interest in the consolidated statements?

A) The parent company concept.

B) The economic unit concept.

C) Proportional consolidation.

D) None of the above.

A) The parent company concept.

B) The economic unit concept.

C) Proportional consolidation.

D) None of the above.

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

56

_____ The noncontrolling interest in a created subsidiary's net income is based on the subsidiary's reported net income under which of the following concepts?

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

57

_____Which of the following statements is false concerning the parent company concept?

A) The NCI in the subsidiary's net income is shown as a deduction in arriving at consolidated net income.

B) The NCI in the subsidiary's net assets is classified outside the consolidated stockholders' equity.

C) Primacy is given to presenting information for the parent's shareholders.

D) All of the above.

E) None of the above.

A) The NCI in the subsidiary's net income is shown as a deduction in arriving at consolidated net income.

B) The NCI in the subsidiary's net assets is classified outside the consolidated stockholders' equity.

C) Primacy is given to presenting information for the parent's shareholders.

D) All of the above.

E) None of the above.

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

58

_____ Which of the following statements is false concerning the economic unit concept?

A) The NCI in the subsidiary's net income is shown as a deduction in arriving at consolidated net income.

B) The NCI in the subsidiary's net assets is classified as part of the consolidated stockholders' equity.

C) The NCI in the subsidiary's net income is shown as a division of the consolidated net income.

D) All of the above.

E) None of the above.

A) The NCI in the subsidiary's net income is shown as a deduction in arriving at consolidated net income.

B) The NCI in the subsidiary's net assets is classified as part of the consolidated stockholders' equity.

C) The NCI in the subsidiary's net income is shown as a division of the consolidated net income.

D) All of the above.

E) None of the above.

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

59

_____ Under the FASB's 1999 exposure draft on consolidation policy, which of the following methods or concepts must be used in reporting consolidated amounts?

A) The economic unit concept.

B) The parent company concept.

C) Proportional consolidation.

D) Full proportional consolidation.

E) Either a or b.

A) The economic unit concept.

B) The parent company concept.

C) Proportional consolidation.

D) Full proportional consolidation.

E) Either a or b.

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

60

When a partially owned created subsidiary reports profits, the amount reported for consolidated net income would be the highest under which of the following methods?

A) The parent company concept.

B) The economic unit concept.

C) Proportional consolidation.

D) None of the above.

A) The parent company concept.

B) The economic unit concept.

C) Proportional consolidation.

D) None of the above.

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

61

_____ The amount to be reported for the NCI in the net assets of a created subsidiary would be the lowest amount under which of the following methods?

A) The parent company concept.

B) The economic unit concept.

C) Proportional consolidation.

D) None of the above.

A) The parent company concept.

B) The economic unit concept.

C) Proportional consolidation.

D) None of the above.

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

62

_____ Which of the following methods reports the NCI in the subsidiary's net income as a deduction in arriving at consolidated net income in the consolidated income statement?

A) The parent company concept.

B) The economic unit concept.

C) Proportional consolidation.

D) None of the above.

A) The parent company concept.

B) The economic unit concept.

C) Proportional consolidation.

D) None of the above.

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

63

_____ The NCI in a created subsidiary's net assets is based on the subsidiary's book values under which of the following concepts?

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

64

_____ Which of the following methods reports the noncontrolling interest as a division or sharing of the consolidated net income?

A) The parent company concept.

B) The economic unit concept.

C) Proportional consolidation.

D) None of the above.

A) The parent company concept.

B) The economic unit concept.

C) Proportional consolidation.

D) None of the above.

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

65

_____ Paxel owns 80% of Saxel's outstanding common stock. For 2006, Saxel reported $60,000 of net income and declared dividends of $10,000. What is the carrying value of Paxel's investment using the equity method at 12/31/06 if the investment's carrying value on 1/1/06 was $200,000?

A) $200,000

B) $208,000

C) $240,000

D) $248,000

E) $256,000

A) $200,000

B) $208,000

C) $240,000

D) $248,000

E) $256,000

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

66

_____ Paxel owns 80% of Saxel's outstanding common stock. For 2006, Saxel reported $60,000 of net income and declared dividends of $10,000. What amount appears in Paxel's 2006 income statement if Paxel accounts for its investment using the equity method?

A) $ -0-

B) $8,000

C) $40,000

D) $48,000

E) $56,000

A) $ -0-

B) $8,000

C) $40,000

D) $48,000

E) $56,000

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

67

_____ For 2006, Pyna reported $500,000 of net income from its own separate operations. This amount excludes income relating to Syna, its 80%-owned created subsidiary, which reported $100,000 of net income and declared $55,000 of dividends in 2006. What is the consolidated net income under the economic unit concept?

A) $536,000

B) $544,000

C) $580,000

D) $600,000

E) $644,000

A) $536,000

B) $544,000

C) $580,000

D) $600,000

E) $644,000

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

68

_____ For 2006, Pyna reported $500,000 of net income from its own separate operations. This amount excludes income relating to Syna, its 80%-owned created subsidiary, which reported $100,000 of net income and declared $55,000 of dividends in 2006. What is the consolidated net income under the parent company concept?

A) $536,000

B) $544,000

C) $580,000

D) $600,000

E) $644,000

A) $536,000

B) $544,000

C) $580,000

D) $600,000

E) $644,000

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

69

_____ Parco, a publicly owned company, could properly not consolidate Sarco, which is

A) Controlled only by having a majority voting interest and unable to distribute dividends because of long-term currency transfer restrictions imposed by a foreign government.

B) Controlled only by having a majority voting interest and has recently emerged from bankruptcy proceedings.

C) Controlled by means other than by having a majority voting interest.

D) Controlled only by having a majority voting interest and has total assets that are less than 10% of the parent's total assets and earnings, respectively.

E) None of the above.

A) Controlled only by having a majority voting interest and unable to distribute dividends because of long-term currency transfer restrictions imposed by a foreign government.

B) Controlled only by having a majority voting interest and has recently emerged from bankruptcy proceedings.

C) Controlled by means other than by having a majority voting interest.

D) Controlled only by having a majority voting interest and has total assets that are less than 10% of the parent's total assets and earnings, respectively.

E) None of the above.

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

70

_____ Prell's 100%-owned domestic subsidiary has filed for bankruptcy protection. How should Prell value its investment in its unconsolidated statements if Prell can exercise significant influence?

A) The cost method.

B) The equity method.

C) The cost method or the equity method, as most appropriate.

D) The equity method or the fair market value.

E) The cost method or the fair market value.

A) The cost method.

B) The equity method.

C) The cost method or the equity method, as most appropriate.

D) The equity method or the fair market value.

E) The cost method or the fair market value.

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

71

_____ Prell's 100%-owned domestic subsidiary has filed for bankruptcy protection. How should Prell value its investment in its unconsolidated statements if Prell cannot exercise significant influence?

A) The cost method.

B) The equity method.

C) The cost method or the equity method, as most appropriate.

D) The equity method or the fair market value.

E) The cost method or the fair market value.

A) The cost method.

B) The equity method.

C) The cost method or the equity method, as most appropriate.

D) The equity method or the fair market value.

E) The cost method or the fair market value.

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

72

_____ Which of the following valuation techniques could not be used to value an investment in an unconsolidated 100%-owned subsidiary?

A) The cost method.

B) The equity method.

C) The fair market value.

D) The cost method and the fair market value.

E) The equity method and the fair market value.

A) The cost method.

B) The equity method.

C) The fair market value.

D) The cost method and the fair market value.

E) The equity method and the fair market value.

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

73

_____ Which of the following valuation techniques could not be used to value an investment in an unconsolidated 90%-owned subsidiary that has its unowned shares publicly traded?

A) The cost method.

B) The equity method.

C) The fair market value.

D) The cost method and the fair market value.

E) The equity method and the fair market value.

A) The cost method.

B) The equity method.

C) The fair market value.

D) The cost method and the fair market value.

E) The equity method and the fair market value.

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

74

_____ What would be the effect on parent-company-only financial statements-not the consolidated statements-if an unconsolidated subsidiary is accounted for under the cost method?

A) All of the unconsolidated subsidiary's accounts will be included individually in the parent company's statements.

B) The retained earnings in the parent company's statements will reflect the earnings of the unconsolidated subsidiary.

C) Dividend income from the unconsolidated subsidiary will be reported in the parent company's income statement.

D) The parent company's retained earnings will be the same as if the subsidiary had been consolidated.

E) None of the above.

A) All of the unconsolidated subsidiary's accounts will be included individually in the parent company's statements.

B) The retained earnings in the parent company's statements will reflect the earnings of the unconsolidated subsidiary.

C) Dividend income from the unconsolidated subsidiary will be reported in the parent company's income statement.

D) The parent company's retained earnings will be the same as if the subsidiary had been consolidated.

E) None of the above.

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

75

_____ Pallco justifiably does not consolidate two of its 100%-owned subsidiaries (Sallco and Sellco). Sallco is (a) a foreign subsidiary and (b) prohibited by the foreign government from paying dividends. Sellco is (a) a domestic subsidiary acquired two months ago in the purchase of a conglomerate and (b) in process of being sold. What would be the most likely method of accounting for each of these unconsolidated subsidiaries?

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

76

_____Under the FASB's consolidation rules, an entity that is controlled by financial arrangements (rather than by a majority voting interest)

A) Must be consolidated.

B) Must be consolidated if the parent is publicly owned.

C) Must be consolidated if the parent has significant influence.

D) Must be consolidated only if the subsidiary is partially owned.

A) Must be consolidated.

B) Must be consolidated if the parent is publicly owned.

C) Must be consolidated if the parent has significant influence.

D) Must be consolidated only if the subsidiary is partially owned.

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

77

_____Entity A will absorb a majority of a VIE's expected losses and Entity B will receive a majority of that VIE's expected residual returns.

A) Entity A must consolidate the VIE.

B) Entity B must consolidate the VIE.

C) Neither entity must consolidate the VIE.

D) Both entities must consolidate the VIE.

A) Entity A must consolidate the VIE.

B) Entity B must consolidate the VIE.

C) Neither entity must consolidate the VIE.

D) Both entities must consolidate the VIE.

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

78

_____ In general, an entity's equity at risk is deemed sufficient to permit the entity to finance its activities without additional subordinated financial support if the equity at risk is

A) At least 10% of the entity's total liabilities.

B) At least 10% of the entity's total long-term debt.

C) At least 10% of the entity's total assets.

D) More than $1,000,000.

E) More than $5,000,000.

A) At least 10% of the entity's total liabilities.

B) At least 10% of the entity's total long-term debt.

C) At least 10% of the entity's total assets.

D) More than $1,000,000.

E) More than $5,000,000.

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

79

matching

based on the information given.

The following (a) seven account balances and (b) statements of retained earnings were obtained from the separate company statements of Parr Inc. and its 80%-owned created sub-sidiary, Subb Inc. (Parr's only subsidiary), at the end of 2006:

When Subb was created (in 2004, 20% of the common shares it issued were sold to private investors.

Requirement 1:

How is each of the first 11 preceding items reported in Parr's 2006 consolidated statements? Use the following list of possible answer codes in the answer columns:

-_____(item 1)

A) Report at the amount shown in Subb's separate statements.

B) Report at the amount shown in Parr's separate statements.

C) Report at less than the sum of the amounts shown in Parr's and Subb's separate statements.

D) Report at the sum of the amounts shown in Parr's and Subb's separate statements.

E) Do not report this item in the consolidated statements or in the separate statements of either Parr or Subb.

F) Do not report this item in the consolidated statements.

G) Create this item in the consolidation process.

based on the information given.

The following (a) seven account balances and (b) statements of retained earnings were obtained from the separate company statements of Parr Inc. and its 80%-owned created sub-sidiary, Subb Inc. (Parr's only subsidiary), at the end of 2006:

When Subb was created (in 2004, 20% of the common shares it issued were sold to private investors.Requirement 1:

How is each of the first 11 preceding items reported in Parr's 2006 consolidated statements? Use the following list of possible answer codes in the answer columns:

-_____(item 1)

A) Report at the amount shown in Subb's separate statements.

B) Report at the amount shown in Parr's separate statements.

C) Report at less than the sum of the amounts shown in Parr's and Subb's separate statements.

D) Report at the sum of the amounts shown in Parr's and Subb's separate statements.

E) Do not report this item in the consolidated statements or in the separate statements of either Parr or Subb.

F) Do not report this item in the consolidated statements.

G) Create this item in the consolidation process.

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

80

matching

based on the information given.

The following (a) seven account balances and (b) statements of retained earnings were obtained from the separate company statements of Parr Inc. and its 80%-owned created sub-sidiary, Subb Inc. (Parr's only subsidiary), at the end of 2006:

When Subb was created (in 2004, 20% of the common shares it issued were sold to private investors.

Requirement 1:

How is each of the first 11 preceding items reported in Parr's 2006 consolidated statements? Use the following list of possible answer codes in the answer columns:

-_____(item 2)

A) Report at the amount shown in Subb's separate statements.

B) Report at the amount shown in Parr's separate statements.

C) Report at less than the sum of the amounts shown in Parr's and Subb's separate statements.

D) Report at the sum of the amounts shown in Parr's and Subb's separate statements.

E) Do not report this item in the consolidated statements or in the separate statements of either Parr or Subb.

F) Do not report this item in the consolidated statements.

G) Create this item in the consolidation process.

based on the information given.

The following (a) seven account balances and (b) statements of retained earnings were obtained from the separate company statements of Parr Inc. and its 80%-owned created sub-sidiary, Subb Inc. (Parr's only subsidiary), at the end of 2006:

When Subb was created (in 2004, 20% of the common shares it issued were sold to private investors.Requirement 1:

How is each of the first 11 preceding items reported in Parr's 2006 consolidated statements? Use the following list of possible answer codes in the answer columns:

-_____(item 2)

A) Report at the amount shown in Subb's separate statements.

B) Report at the amount shown in Parr's separate statements.

C) Report at less than the sum of the amounts shown in Parr's and Subb's separate statements.

D) Report at the sum of the amounts shown in Parr's and Subb's separate statements.

E) Do not report this item in the consolidated statements or in the separate statements of either Parr or Subb.

F) Do not report this item in the consolidated statements.

G) Create this item in the consolidation process.

Unlock Deck

Unlock for access to all 138 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 138 flashcards in this deck.