Deck 12: Reporting Segment and Related Information

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

_____ Which amounts does FAS 131 require to be disclosed for each reportable segment?

Question

_____ Which separate segment amounts does FAS 131 require to be disclosed for each reportable segment when the amounts are used in the measure of segment profitability used by the CODM?

Question

_____ Which separate segment amounts does FAS 131 require to be disclosed for each reportable segment even though the amounts are not used in the measure of segment profitability used by the CODM?

Question

Question

Question

Question

Question

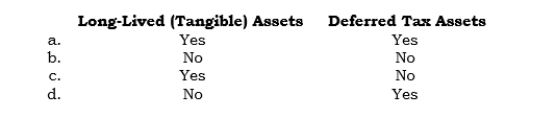

_____ The assets test used for determining reportable segments uses an asset amount that includes:

Question

_____ The assets test used for determining reportable segments uses an asset

amount that excludes:

amount that excludes:

Question

Question

Question

Question

Question

Question

Question

Question

Question

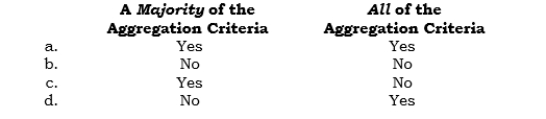

_____ For segment reporting purposes, aggregation of operating segments (for which no determination has been made as to whether they are reportable segments) is allowed only if they satisfy

Question

Question

Question

Question

Question

Question

Question

Question

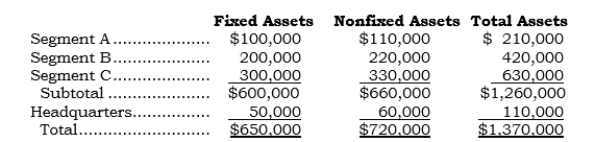

_____ Punex has three operating segments and a headquarters office. Information for the assets of these units at 12/31/06 follows:

In applying the 10% of assets test used to determine reportable segments, the 10% is applied to

In applying the 10% of assets test used to determine reportable segments, the 10% is applied to

A) $ 600,000

B) $ 650,000

C) $ 660,000

D) $1,260,000

E) $1,370,000

In applying the 10% of assets test used to determine reportable segments, the 10% is applied toA) $ 600,000

B) $ 650,000

C) $ 660,000

D) $1,260,000

E) $1,370,000

Question

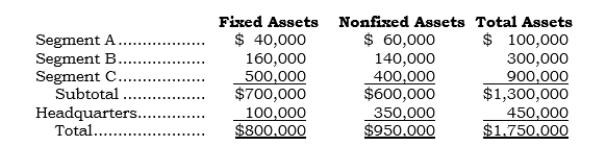

_____ Pinex has three operating segments and a headquarters office. Information for the assets of these units at 12/31/06 follows:

In applying the 10% of assets test used to determine reportable segments, the 10% is applied to

In applying the 10% of assets test used to determine reportable segments, the 10% is applied to

A) $ 700,000

B) $ 800,000

C) $ 950,000

D) $1,300,000

E) $1,750,000

In applying the 10% of assets test used to determine reportable segments, the 10% is applied toA) $ 700,000

B) $ 800,000

C) $ 950,000

D) $1,300,000

E) $1,750,000

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/90

Play

Full screen (f)

Deck 12: Reporting Segment and Related Information

1

The basis of segmentation required by FAS 131 is called the ____________________ _____________________________ approach.

management

2

Intercompany sales that occur within a vertically integrated segment are called _______________________________ sales.

intrasegment

3

Intercompany sales that occur between operating segments are called __________ __________________________ sales.

intersegment

4

The two major disclosures for reportable operating segments are (a) a measure of _______________________ and (b) a measure of ___________________________.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

5

Items that must be disclosed for a reportable segment if those items are included in the measure of profitability used by the CODM are (a)_______________________, (b)______________________, (c) _____________________, (d)______________________, (e) ______________________, (f) ______________________, (g) _______________________, (h) ______________________, and (i) ______________________.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

6

Three items that need not be disclosed for reportable operating segments are _______________________, _________________________, and ______________________.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

7

Segment profitability for all reportable segments must be reconciled to ________ ___________________________ ________________________________ income.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

8

Segment assets for all reportable segments must be reconciled to ______________ ___________________________ assets.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

9

Segment revenues for all reportable segments must be reconciled to __________ ___________________________ revenues.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

10

To determine whether an operating segment is a reportable segment, it is necessary to perform a test based on ____________________________, a test based on _________________________, and a test based on ________________________.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

11

In performing the revenues test to determine reportable segments, one includes any _________________________ sales but excludes any ____________________ sales.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

12

Enough operating segments must be presented so that at least 75% of all sales to ___________________________ of all operating segments is shown by reportable operating segments.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

13

Aggregation may be performed immediately after all operating segments have been _______________________. It may also be performed later immediately after all ________________________ segments have been determined.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

14

Entity-wide disclosures pertain to (a) _____________________________________, (b) ______________________________, and (c) _________________________________.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

15

Segment reporting is required of publicly owned companies and privately owned companies.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

16

Segment reporting is required for interim period financial statements of publicly owned companies.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

17

Segment reporting is not required in the separately issued financial statements of a subsidiary if the parent has also issued consolidated statements in a separate report.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

18

Segment reporting applies to not-for-profit entities.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

19

FAS 131 requires a single basis of segmentation-one based on products and services.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

20

All foreign subsidiaries are automatically operating segments (though some may not be reportable segments).

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

21

A start-up operation cannot be an operating segment until it has significant revenues.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

22

A central research and development facility (having no revenues) could not be an operating segment.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

23

FAS 131 does not require that GAAP methods be used in determining amounts reported for segment profitability.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

24

FAS 131 does not require that common costs that benefit two or more segments be allocated to the individual segments.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

25

The term chief operating decision maker refers to a particular individual-not a function.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

26

A vertically integrated business cannot be disaggregated.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

27

Intersegment revenues must be disclosed for reportable segments only if those revenues are included in the measure of profitability used by the CODM.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

28

Reporting segment cash flows is prohibited.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

29

Reporting segment liabilities is optional.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

30

Reporting segment research and development costs is not required only for domestic segments.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

31

FAS 131 requires use of quantitative thresholds to establish a measure of profitability.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

32

FAS 131 permits asymmetrical allocations to segments.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

33

In presenting segment data, eliminations and adjustments (that pertain to reportable segments) made in consolidation must be allocated to reportable segments.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

34

In presenting segment data, costs accounted for at a consolidated level need not be allocated to segments.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

35

A reconciliation must be presented that reconciles the total revenues of the reportable segments to consolidated pretax income.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

36

Aggregation of segments is allowed only of reportable operating segments and only if a majority of the aggregation criteria are satisfied.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

37

Aggregation of segments is allowed of reportable operating segments only if a majority of the aggregation criteria are satisfied.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

38

Aggregation of segments is mandatory if the aggregation criteria are satisfied.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

39

Before aggregation of segments can occur, the three quantitative thres-holds tests must be performed.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

40

Aggregation of segments can occur before or after performing the three quantitative thresholds tests.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

41

To qualify as an operating segment, an entity need satisfy only one of the three 10% or more quantitative thresholds tests.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

42

All reportable segments are operating segments but not all operating segments are reportable segments.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

43

All operating segments are reportable segments but not all reportable segments are operating segments.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

44

Aggregation of segments is allowed only if the 75% test is satisfied.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

45

More than one segment may operate in the same geographic area and one segment may include operations in several geographic areas.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

46

A company manufacturing widgets both domestically and overseas could have two reportable segments.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

47

In disclosing information about major customers, it is necessary to disclose the identity of each such customer.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

48

_____ FAS 131 defines an operating segment as a component of an enterprise that has:

A) Assets that are 10% or more of consolidated assets.

B) Assets that are 10% or more of the combined assets of all segments.

C) Revenues that are 10% or more of consolidated revenues.

D) Revenues that are 10% or more of combined revenues of all segments.

E) None of the above.

A) Assets that are 10% or more of consolidated assets.

B) Assets that are 10% or more of the combined assets of all segments.

C) Revenues that are 10% or more of consolidated revenues.

D) Revenues that are 10% or more of combined revenues of all segments.

E) None of the above.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

49

_____ To qualify as an operating segment under FAS 131, a component of an enterprise must

A) Have business activities with external parties or other components of the same enterprise.

B) Be a separate legal entity.

C) Have revenues with unaffiliated customers.

D) Have profitable operations or expectations of having profitable operations.

E) Not be part of a vertically integrated operation.

A) Have business activities with external parties or other components of the same enterprise.

B) Be a separate legal entity.

C) Have revenues with unaffiliated customers.

D) Have profitable operations or expectations of having profitable operations.

E) Not be part of a vertically integrated operation.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

50

_____ A component of a vertically integrated operation

A) Is always a separate operating segment.

B) Is always a reportable operating segment.

C) Can never be a separate operating segment.

D) Can never be a reportable operating segment.

E) None of the above.

A) Is always a separate operating segment.

B) Is always a reportable operating segment.

C) Can never be a separate operating segment.

D) Can never be a reportable operating segment.

E) None of the above.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

51

_____ Which of the following items are not required to be disclosed for reportable operating segments even though the items are included in the measure of profitability used by the CODM in managing segments?

A) Goodwill amortization expense.

B) Research and development costs.

C) Income tax expense (or benefit).

D) Interest revenues.

E) Extraordinary items.

A) Goodwill amortization expense.

B) Research and development costs.

C) Income tax expense (or benefit).

D) Interest revenues.

E) Extraordinary items.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

52

_____ Which of the following items does FAS 131 require to be included in the measure of profitability used by the CODM in managing segments?

A) Goodwill amortization expense.

B) Extraordinary items.

C) Interest revenues.

D) Interest expense.

E) None of the above.

A) Goodwill amortization expense.

B) Extraordinary items.

C) Interest revenues.

D) Interest expense.

E) None of the above.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

53

_____ Which of the following items does FAS 131 require to be excluded from the measure of profitability to be disclosed for reportable segments?

A) Unusual items.

B) Extraordinary items.

C) Income tax expense (or benefit).

D) Interest expense.

E) None of the above.

A) Unusual items.

B) Extraordinary items.

C) Income tax expense (or benefit).

D) Interest expense.

E) None of the above.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

54

_____ Which amounts does FAS 131 require to be disclosed for each reportable segment?

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

55

_____ Which separate segment amounts does FAS 131 require to be disclosed for each reportable segment when the amounts are used in the measure of segment profitability used by the CODM?

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

56

_____ Which separate segment amounts does FAS 131 require to be disclosed for each reportable segment even though the amounts are not used in the measure of segment profitability used by the CODM?

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

57

_____ Under FAS 131, revenues could include:

A) Intersegment interest income.

B) Intersegment lease income.

C) Intersegment management fee income.

D) Royalty income.

E) All of the above.

A) Intersegment interest income.

B) Intersegment lease income.

C) Intersegment management fee income.

D) Royalty income.

E) All of the above.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

58

_____ The revenues to be disclosed for identified operating segments do not include

A) Intrasegment sales.

B) Intersegment sales.

C) Intersegment interest income.

D) Domestic export sales.

E) None of the above.

A) Intrasegment sales.

B) Intersegment sales.

C) Intersegment interest income.

D) Domestic export sales.

E) None of the above.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

59

_____ The 10% revenues test used to determine reportable segments uses a revenues amount that includes

A) Intersegment sales.

B) Intersegment interest income.

C) External interest income.

D) a, b, and c.

E) None of the above.

A) Intersegment sales.

B) Intersegment interest income.

C) External interest income.

D) a, b, and c.

E) None of the above.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

60

_____ The revenue amounts for a reportable segment that are included in the revenues amount used in the revenues test used to determine reportable segments

A) Could be more than the sum of the revenues amounts that must be disclosed for that reportable segment.

B) Could be less than the sum of the revenues amounts that must be disclosed for that reportable segment.

C) Are always the same as the sum of the revenues amounts that must be disclosed for that reportable segment.

D) Are always different from the sum of the revenues amounts that must be disclosed for that reportable segment.

A) Could be more than the sum of the revenues amounts that must be disclosed for that reportable segment.

B) Could be less than the sum of the revenues amounts that must be disclosed for that reportable segment.

C) Are always the same as the sum of the revenues amounts that must be disclosed for that reportable segment.

D) Are always different from the sum of the revenues amounts that must be disclosed for that reportable segment.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

61

_____ The assets test used for determining reportable segments uses an asset amount that includes:

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

62

_____ The assets test used for determining reportable segments uses an asset

amount that excludes:

amount that excludes:

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

63

_____ To qualify as a reportable segment (disregard the requirements of the 75% test), the segment must satisfy

A) One of the three 10% tests.

B) Two of the three 10% tests.

C) All of the three 10% tests.

D) None of the above.

A) One of the three 10% tests.

B) Two of the three 10% tests.

C) All of the three 10% tests.

D) None of the above.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

64

_____ The 75% test is based on

A) Consolidated revenues.

B) Consolidated revenues minus intersegment revenues.

C) Consolidated revenues minus intrasegment revenues.

D) Consolidated revenues plus intersegment revenues minus intrasegment revenues.

E) None of the above.

A) Consolidated revenues.

B) Consolidated revenues minus intersegment revenues.

C) Consolidated revenues minus intrasegment revenues.

D) Consolidated revenues plus intersegment revenues minus intrasegment revenues.

E) None of the above.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

65

_____ Which of the following disclosed segment items need not be reconciled to the corresponding consolidated amount even though the item is included in the measure of profitability used by the CODM to manage the segment?

A) Interest expense.

B) Extraordinary items.

C) Depreciation expense.

D) Goodwill amortization expense.

E) None of the above.

A) Interest expense.

B) Extraordinary items.

C) Depreciation expense.

D) Goodwill amortization expense.

E) None of the above.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

66

_____ Which of the following mandatory or voluntarily disclosed segment items need not be reconciled to the corresponding consolidated amount?

A) Segment cash flows from operations.

B) Segment interest income.

C) Segment fixed assets.

D) Extraordinary items.

E) None of the above.

A) Segment cash flows from operations.

B) Segment interest income.

C) Segment fixed assets.

D) Extraordinary items.

E) None of the above.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

67

For segment reporting purposes, the components of a vertically integrated business

A) Cannot be reported separately.

B) Must be reported separately.

C) May or may not be reported separately depending on the circumstances.

D) None of the above.

A) Cannot be reported separately.

B) Must be reported separately.

C) May or may not be reported separately depending on the circumstances.

D) None of the above.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

68

_____ Aggregation of operating segments is allowed

A) Only of nonreportable segments.

B) Only of reportable segments.

C) Only of components of a vertically integrated business.

D) Of both reportable and nonreportable segments

E) None of the above.

A) Only of nonreportable segments.

B) Only of reportable segments.

C) Only of components of a vertically integrated business.

D) Of both reportable and nonreportable segments

E) None of the above.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

69

_____ Aggregation of two or more operating segments (not two or more reportable operating segments) having (1) similar economic characteristics and (2) a majority-not all-of other FAS 131 specified similarities is

A) Mandatory.

B) Prohibited.

C) Optional.

D) None of the above.

A) Mandatory.

B) Prohibited.

C) Optional.

D) None of the above.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

70

_____ Aggregation of two or more reportable operating segments (not two or more operating segments) having (1) similar economic characteristics and (2) a majority-not all-of other FAS 131 specified similarities is

A) Mandatory.

B) Prohibited.

C) Optional.

D) None of the above.

A) Mandatory.

B) Prohibited.

C) Optional.

D) None of the above.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

71

_____ For segment reporting purposes, aggregation of operating segments (for which no determination has been made as to whether they are reportable segments) is allowed only if they satisfy

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

72

_____ Which of the following items is not required to be disclosed under FAS 131?

A) Export sales.

B) Major customers.

C) Geographic areas in which sales occur.

D) Types of products and services.

E) None of the above.

A) Export sales.

B) Major customers.

C) Geographic areas in which sales occur.

D) Types of products and services.

E) None of the above.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

73

_____ An entity that operates in several industries has (a) external sales of $40,000,000, (b) intrasegment sales of $3,000,000, and (c) intersegment sales of $7,000,000. In performing the 10% of revenues test to determine reportable segments, the 10% is applied to

A) $3,000,000

B) $40,000,000

C) $43,000,000

D) $47,000,000

E) $50,000,000

A) $3,000,000

B) $40,000,000

C) $43,000,000

D) $47,000,000

E) $50,000,000

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

74

_____ An entity that operates in several industries has (a) external sales of $40,000,000, (b) intrasegment sales of $3,000,000, and (c) intersegment sales of $7,000,000. In performing the 75% test, the 75% is applied to

A) $3,000,000

B) $40,000,000

C) $43,000,000

D) $47,000,000

E) $50,000,000

A) $3,000,000

B) $40,000,000

C) $43,000,000

D) $47,000,000

E) $50,000,000

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

75

_____ An entity that operates in several industries has (a) external sales of $50,000,000, (b) intrasegment sales of $5,000,000, and (c) intersegment sales of $4,000,000. In performing the 10% of revenues test to determine reportable segments, the 10% is applied to

A) $4,000,000

B) $50,000,000

C) $54,000,000

D) $55,000,000

E) $59,000,000

A) $4,000,000

B) $50,000,000

C) $54,000,000

D) $55,000,000

E) $59,000,000

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

76

_____ An entity that operates in several industries has (a) external sales of $50,000,000, (b) intrasegment sales of $5,000,000, and (c) intersegment sales of $4,000,000. In performing the 75% test, the 75% is applied to

A) $4,000,000

B) $50,000,000

C) $54,000,000

D) $55,000,000

E) $59,000,000

A) $4,000,000

B) $50,000,000

C) $54,000,000

D) $55,000,000

E) $59,000,000

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

77

_____ An entity has four operating segments. For 2006, their measures of profitability are $300,000, $200,000, $(100,000), and $(50,000). In applying the 10% profitability test to determine reportable segments, the 10% is applied to:

A) $(150,000)

B) $ 350,000

C) $ 500,000

D) $ 650,000

A) $(150,000)

B) $ 350,000

C) $ 500,000

D) $ 650,000

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

78

_____ An entity has four operating segments. For 2006, their measures of profitability are $100,000, $200,000, and $(550,000), and $(5,000). In applying the 10% profitability test to determine reportable segments, the 10% is applied to:

A) $(555,000)

B) $(550,000)

C) $(255,000)

D) $ 300,000

E) $ 855,000

A) $(555,000)

B) $(550,000)

C) $(255,000)

D) $ 300,000

E) $ 855,000

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

79

_____ Punex has three operating segments and a headquarters office. Information for the assets of these units at 12/31/06 follows:

In applying the 10% of assets test used to determine reportable segments, the 10% is applied to

A) $ 600,000

B) $ 650,000

C) $ 660,000

D) $1,260,000

E) $1,370,000

In applying the 10% of assets test used to determine reportable segments, the 10% is applied toA) $ 600,000

B) $ 650,000

C) $ 660,000

D) $1,260,000

E) $1,370,000

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

80

_____ Pinex has three operating segments and a headquarters office. Information for the assets of these units at 12/31/06 follows:

In applying the 10% of assets test used to determine reportable segments, the 10% is applied to

A) $ 700,000

B) $ 800,000

C) $ 950,000

D) $1,300,000

E) $1,750,000

In applying the 10% of assets test used to determine reportable segments, the 10% is applied toA) $ 700,000

B) $ 800,000

C) $ 950,000

D) $1,300,000

E) $1,750,000

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 90 flashcards in this deck.