Deck 11: Risk and Return: the Capital Asset Pricing Model

Full screen (f)

Question

Question

Question

Question

Question

Question

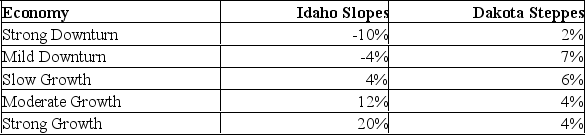

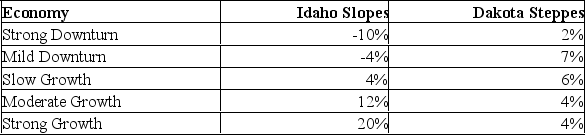

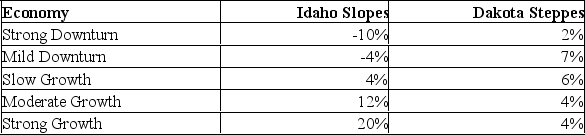

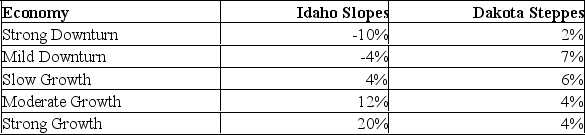

Idaho Slopes (IS) and Dakota Steppes (DS) are both seasonal businesses. IS is a downhill skiing facility, while DS is a tour company that specializes in walking tours and camping. The equally likely returns on each company over the next year is expected to be:  The correlation between the returns of IS and DS is:

The correlation between the returns of IS and DS is:

A) +1.00

B) -1.10

C) +0.30

D) -0.03

E) 0.03

The correlation between the returns of IS and DS is:A) +1.00

B) -1.10

C) +0.30

D) -0.03

E) 0.03

Question

Idaho Slopes (IS) and Dakota Steppes (DS) are both seasonal businesses. IS is a downhill skiing facility, while DS is a tour company that specializes in walking tours and camping. The equally likely returns on each company over the next year is expected to be:  The variances of IS and DS are:

The variances of IS and DS are:

A) .0145; .00038.

B) .011584; .000304.

C) .006454; .000154.

D) .0008068; .000193.

The variances of IS and DS are:A) .0145; .00038.

B) .011584; .000304.

C) .006454; .000154.

D) .0008068; .000193.

Question

Question

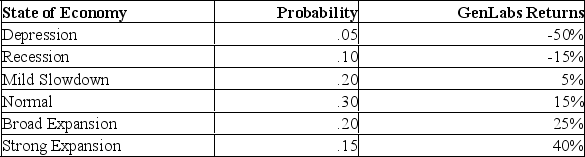

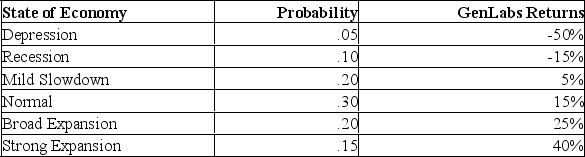

GenLabs has been a hot stock the last few years, but is risky. The expected returns for GenLabs are highly dependent on the state of the economy as follows:  The variance and standard deviation of GenLabs returns are:

The variance and standard deviation of GenLabs returns are:

A) 0.042875; 0.2070628.

B) 0.0714612; 8.450.845142.

C) 0.093958; 0.3065169.

D) 0.112750; 0.335809.

The variance and standard deviation of GenLabs returns are:A) 0.042875; 0.2070628.

B) 0.0714612; 8.450.845142.

C) 0.093958; 0.3065169.

D) 0.112750; 0.335809.

Question

Question

Question

Question

Idaho Slopes (IS) and Dakota Steppes (DS) are both seasonal businesses. IS is a downhill skiing facility, while DS is a tour company that specializes in walking tours and camping. The equally likely returns on each company over the next year is expected to be:  The covariance between the IS and DS returns is:

The covariance between the IS and DS returns is:

A) .00187.

B) .00240.

C) .00028.

D) .000056.

The covariance between the IS and DS returns is:A) .00187.

B) .00240.

C) .00028.

D) .000056.

Question

GenLabs has been a hot stock the last few years, but is risky. The expected returns for GenLabs are highly dependent on the state of the economy as follows:  The expected return on GenLabs is:

The expected return on GenLabs is:

A) 20.5%

B) 12.5%

C) 8.5%

D) 3.3%

The expected return on GenLabs is:A) 20.5%

B) 12.5%

C) 8.5%

D) 3.3%

Question

Question

Idaho Slopes (IS) and Dakota Steppes (DS) are both seasonal businesses. IS is a downhill skiing facility, while DS is a tour company that specializes in walking tours and camping. The equally likely returns on each company over the next year is expected to be:  If IS and DS are combined in a portfolio with 50% invested in each, the expected return and risk would be:

If IS and DS are combined in a portfolio with 50% invested in each, the expected return and risk would be:

A) 5.625%; 37.2%.

B) 4.5%; 5.48%.

C) 8.0%; 8.2%.

D) 5.0%; 0%.

E) 4.5%; 0%.

If IS and DS are combined in a portfolio with 50% invested in each, the expected return and risk would be:A) 5.625%; 37.2%.

B) 4.5%; 5.48%.

C) 8.0%; 8.2%.

D) 5.0%; 0%.

E) 4.5%; 0%.

Question

Question

Idaho Slopes (IS) and Dakota Steppes (DS) are both seasonal businesses. IS is a downhill skiing facility, while DS is a tour company that specializes in walking tours and camping. The equally likely returns on each company over the next year is expected to be:  The means of IS and DS are:

The means of IS and DS are:

A) 4.4%; 4.6%.

B) 5.5%; 5.75%.

C) 10%; 6%.

D) 4%; 6%.

The means of IS and DS are:A) 4.4%; 4.6%.

B) 5.5%; 5.75%.

C) 10%; 6%.

D) 4%; 6%.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

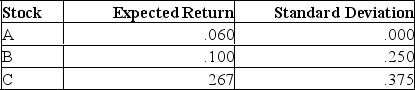

Given the following information on 3 stocks:

Using the CAPM, calculate the expected return for Stock's A, B, and

Using the CAPM, calculate the expected return for Stock's A, B, and

C. Which stocks would you recommend purchasing?

BA = .0070/.0064 = 1.094; ra = .07 + (.18-.07)1.094 = .1903

BB = .0045/.0064 = 0.703; rb = .07 + (.18-.07)0.703 = .1473

BC = .0013/.0064 = 0.203; rc = .07 + (.18-.07)0.203 = .0923

Indifferent on A as .1903 _.19.

Would buy B as.15 > .1473.

Would not buy C as.09 < .0923.

Using the CAPM, calculate the expected return for Stock's A, B, and C. Which stocks would you recommend purchasing?

BA = .0070/.0064 = 1.094; ra = .07 + (.18-.07)1.094 = .1903

BB = .0045/.0064 = 0.703; rb = .07 + (.18-.07)0.703 = .1473

BC = .0013/.0064 = 0.203; rc = .07 + (.18-.07)0.203 = .0923

Indifferent on A as .1903 _.19.

Would buy B as.15 > .1473.

Would not buy C as.09 < .0923.

Question

Question

Question

Question

Question

Question

Question

Question

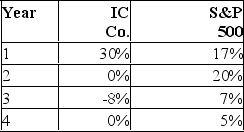

Returns for the IC Company and for the S&P 500 Index over the previous 4-year period are given below:

What are the average returns on IC and on the S&P 500 index? If you had invested $1.00 in IC, how much would you have had after 4 years? What is the correlation between the returns on IC and the S&P?

What are the average returns on IC and on the S&P 500 index? If you had invested $1.00 in IC, how much would you have had after 4 years? What is the correlation between the returns on IC and the S&P?

What are the average returns on IC and on the S&P 500 index? If you had invested $1.00 in IC, how much would you have had after 4 years? What is the correlation between the returns on IC and the S&P? Question

Question

Question

Given the following information on three stocks:

= -.05333

= -.05333

bc

Suppose you desire to invest in any one of the stocks listed above. Can any be recommended?

= -.05333bc

Suppose you desire to invest in any one of the stocks listed above. Can any be recommended?

Question

Question

Question

Given the following information on three stocks:

= -.05333

= -.05333

bc

Now suppose you diversify into two securities. Given all choices, can any portfolio be eliminated? Assume equal weights.

= -.05333bc

Now suppose you diversify into two securities. Given all choices, can any portfolio be eliminated? Assume equal weights.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/65

Play

Full screen (f)

Deck 11: Risk and Return: the Capital Asset Pricing Model

1

If the covariance of stock 1 with stock 2 is -.0065, then what is the covariance of stock 2 with stock 1?

A) -.0065.

B) less than -.0065.

C) greater than +.0065.

D) +.0065.

A) -.0065.

B) less than -.0065.

C) greater than +.0065.

D) +.0065.

-.0065.

2

A portfolio is entirely invested into Buzz's Bauxite Boring Equity, which is expected to return 16%, and Zum's Inc. bonds, which are expected to return 8%. Sixty percent of the funds are invested in Buzz's and the rest in Zum's. What is the expected return on the portfolio?

A) 9.6%.

B) 12.8%.

C) 24.1%.

D) 6.4%.

A) 9.6%.

B) 12.8%.

C) 24.1%.

D) 6.4%.

12.8%.

3

A portfolio will usually contain:

A) only one riskless asset.

B) only one risky asset.

C) two or more assets.

D) no assets.

A) only one riskless asset.

B) only one risky asset.

C) two or more assets.

D) no assets.

two or more assets.

4

Stock A has an expected return of 20%, and stock B has an expected return of 4%. However, the risk of stock A as measured by its variance is 3 times that of stock B. If the two stocks are combined equally in a portfolio, what would be the portfolio's expected return?

A) 20.0%.

B) 4.0%.

C) 12.0%.

D) Greater than 20%.

A) 20.0%.

B) 4.0%.

C) 12.0%.

D) Greater than 20%.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

5

Systematic risk is measured by:

A) the mean.

B) beta.

C) the geometric average.

D) the standard deviation.

A) the mean.

B) beta.

C) the geometric average.

D) the standard deviation.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

6

Idaho Slopes (IS) and Dakota Steppes (DS) are both seasonal businesses. IS is a downhill skiing facility, while DS is a tour company that specializes in walking tours and camping. The equally likely returns on each company over the next year is expected to be: The correlation between the returns of IS and DS is:

A) +1.00

B) -1.10

C) +0.30

D) -0.03

E) 0.03

The correlation between the returns of IS and DS is:A) +1.00

B) -1.10

C) +0.30

D) -0.03

E) 0.03

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

7

Idaho Slopes (IS) and Dakota Steppes (DS) are both seasonal businesses. IS is a downhill skiing facility, while DS is a tour company that specializes in walking tours and camping. The equally likely returns on each company over the next year is expected to be: The variances of IS and DS are:

A) .0145; .00038.

B) .011584; .000304.

C) .006454; .000154.

D) .0008068; .000193.

The variances of IS and DS are:A) .0145; .00038.

B) .011584; .000304.

C) .006454; .000154.

D) .0008068; .000193.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

8

When stocks with the same expected return are combined into a portfolio:

A) the expected return of the portfolio is less than the average expected return of the stocks.

B) the expected return of the portfolio is greater than the average expected return of the stocks.

C) the expected return of the portfolio is equal to the average expected return of the stocks.

D) there is no relationship between the expected return of the portfolio and the expected return of the stocks.

A) the expected return of the portfolio is less than the average expected return of the stocks.

B) the expected return of the portfolio is greater than the average expected return of the stocks.

C) the expected return of the portfolio is equal to the average expected return of the stocks.

D) there is no relationship between the expected return of the portfolio and the expected return of the stocks.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

9

GenLabs has been a hot stock the last few years, but is risky. The expected returns for GenLabs are highly dependent on the state of the economy as follows: The variance and standard deviation of GenLabs returns are:

A) 0.042875; 0.2070628.

B) 0.0714612; 8.450.845142.

C) 0.093958; 0.3065169.

D) 0.112750; 0.335809.

The variance and standard deviation of GenLabs returns are:A) 0.042875; 0.2070628.

B) 0.0714612; 8.450.845142.

C) 0.093958; 0.3065169.

D) 0.112750; 0.335809.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

10

The rate of return on the common stock of Flowers by Flo is expected to be 14% in a boom economy, 8% in a normal economy, and only 2% in a recessionary economy. The probabilities of these economic states are 20% for a boom, 70% for a normal economy, and 10% for a recession. What is the variance of the returns on the common stock of Flowers by Flo?

A) 0.001044

B) 0.001280

C) 0.001863

D) 0.002001

E) 0.002471

A) 0.001044

B) 0.001280

C) 0.001863

D) 0.002001

E) 0.002471

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

11

You have plotted the data for two securities over time on the same graph, ie., the month return of each security for the last 5 years. If the pattern of the movements of the two securities rose and fell as the other did, these two securities would have:

A) no correlation at all.

B) a weak negative correlation.

C) a strong negative correlation.

D) a strong positive correlation.

A) no correlation at all.

B) a weak negative correlation.

C) a strong negative correlation.

D) a strong positive correlation.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

12

If you have a portfolio of two risky stocks which turns out to have no diversification. The reason you have no diversification is:

A) the returns are too small.

B) the returns move perfectly opposite of one another.

C) the returns are too large to offset.

D) the returns move perfectly with one another.

E) the returns are completely unrelated to one another.

A) the returns are too small.

B) the returns move perfectly opposite of one another.

C) the returns are too large to offset.

D) the returns move perfectly with one another.

E) the returns are completely unrelated to one another.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

13

Idaho Slopes (IS) and Dakota Steppes (DS) are both seasonal businesses. IS is a downhill skiing facility, while DS is a tour company that specializes in walking tours and camping. The equally likely returns on each company over the next year is expected to be: The covariance between the IS and DS returns is:

A) .00187.

B) .00240.

C) .00028.

D) .000056.

The covariance between the IS and DS returns is:A) .00187.

B) .00240.

C) .00028.

D) .000056.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

14

GenLabs has been a hot stock the last few years, but is risky. The expected returns for GenLabs are highly dependent on the state of the economy as follows: The expected return on GenLabs is:

A) 20.5%

B) 12.5%

C) 8.5%

D) 3.3%

The expected return on GenLabs is:A) 20.5%

B) 12.5%

C) 8.5%

D) 3.3%

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

15

Standard deviation measures ________________ risk.

A) total

B) nondiversifiable

C) unsystematic risk

D) systematic risk

A) total

B) nondiversifiable

C) unsystematic risk

D) systematic risk

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

16

Idaho Slopes (IS) and Dakota Steppes (DS) are both seasonal businesses. IS is a downhill skiing facility, while DS is a tour company that specializes in walking tours and camping. The equally likely returns on each company over the next year is expected to be: If IS and DS are combined in a portfolio with 50% invested in each, the expected return and risk would be:

A) 5.625%; 37.2%.

B) 4.5%; 5.48%.

C) 8.0%; 8.2%.

D) 5.0%; 0%.

E) 4.5%; 0%.

If IS and DS are combined in a portfolio with 50% invested in each, the expected return and risk would be:A) 5.625%; 37.2%.

B) 4.5%; 5.48%.

C) 8.0%; 8.2%.

D) 5.0%; 0%.

E) 4.5%; 0%.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

17

If the correlation between two stocks is -1, the returns:

A) generally move in the same direction.

B) move perfectly opposite one another.

C) are unrelated to one another as it is <0.

D) have standard deviations of equal size but opposite signs.

A) generally move in the same direction.

B) move perfectly opposite one another.

C) are unrelated to one another as it is <0.

D) have standard deviations of equal size but opposite signs.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

18

Idaho Slopes (IS) and Dakota Steppes (DS) are both seasonal businesses. IS is a downhill skiing facility, while DS is a tour company that specializes in walking tours and camping. The equally likely returns on each company over the next year is expected to be: The means of IS and DS are:

A) 4.4%; 4.6%.

B) 5.5%; 5.75%.

C) 10%; 6%.

D) 4%; 6%.

The means of IS and DS are:A) 4.4%; 4.6%.

B) 5.5%; 5.75%.

C) 10%; 6%.

D) 4%; 6%.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

19

Covariance measures the interrelationship between two securities in terms of:

A) both expected return and direction of return movement.

B) both size and direction of return movement.

C) the standard deviation of returns.

D) both expected return and size of return movements.

E) the correlations of returns.

A) both expected return and direction of return movement.

B) both size and direction of return movement.

C) the standard deviation of returns.

D) both expected return and size of return movements.

E) the correlations of returns.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

20

When a security is added to a portfolio the appropriate return and risk contributions are:

A) the expected return of the asset and its standard deviation.

B) the most probable return and the beta.

C) the expected return and the beta.

D) the most probable return and its standard deviation.

A) the expected return of the asset and its standard deviation.

B) the most probable return and the beta.

C) the expected return and the beta.

D) the most probable return and its standard deviation.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

21

If the correlation between two stocks is +1, then a portfolio combining these two stocks will have a variance that is:

A) less than the weighted average of the two individual variances.

B) greater than the weighted average of the two individual variances.

C) equal to the weighted average of the two individual variances.

D) less than or equal to average variance of the two weighted variances, depending on other information.

A) less than the weighted average of the two individual variances.

B) greater than the weighted average of the two individual variances.

C) equal to the weighted average of the two individual variances.

D) less than or equal to average variance of the two weighted variances, depending on other information.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

22

The opportunity set of portfolios is:

A) all possible return combinations of those securities.

B) all possible risk combinations of those securities.

C) all possible risk-return combinations of those securities.

D) the best or highest risk-return combination.

E) the lowest risk-return combination.

A) all possible return combinations of those securities.

B) all possible risk combinations of those securities.

C) all possible risk-return combinations of those securities.

D) the best or highest risk-return combination.

E) the lowest risk-return combination.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

23

An efficient set of portfolios is:

A) the complete opportunity set.

B) the portion of the opportunity set below the minimum variance portfolio.

C) only the minimum variance portfolio.

D) the dominant portion of the opportunity set.

E) only the maximum return portfolio.

A) the complete opportunity set.

B) the portion of the opportunity set below the minimum variance portfolio.

C) only the minimum variance portfolio.

D) the dominant portion of the opportunity set.

E) only the maximum return portfolio.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

24

Total risk can be divided into:

A) standard deviation and variance.

B) standard deviation and covariance.

C) portfolio risk and beta.

D) portfolio risk and unsystematic risk.

E) portfolio risk and covariance.

A) standard deviation and variance.

B) standard deviation and covariance.

C) portfolio risk and beta.

D) portfolio risk and unsystematic risk.

E) portfolio risk and covariance.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

25

The total number of variance and covariance terms in portfolio is N2. How many of these would be (including non-unique) covariances?

A) N.

B) N2.

C) N2- N.

D) N2- N/2.

A) N.

B) N2.

C) N2- N.

D) N2- N/2.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

26

Diversification can effectively reduce risk. Once a portfolio is diversified the type of risk remaining is:

A) individual security risk.

B) riskless security risk.

C) risk related to the market portfolio.

D) total standard deviations.

A) individual security risk.

B) riskless security risk.

C) risk related to the market portfolio.

D) total standard deviations.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

27

As we add more securities to a portfolio, the ____ will decrease:

A) total risk

B) systematic risk

C) unsystematic risk

D) standard error

A) total risk

B) systematic risk

C) unsystematic risk

D) standard error

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

28

For a highly diversified equally weighted portfolio, the portfolio variance is:

A) the average covariance.

B) the average expected value.

C) the average variance.

D) the weighted average expected value.

E) the weighted average variance.

A) the average covariance.

B) the average expected value.

C) the average variance.

D) the weighted average expected value.

E) the weighted average variance.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

29

The CML is the pricing relationship between:

A) efficient portfolios and beta.

B) the risk-free asset and standard deviation of the portfolio return.

C) the optimal portfolio and the standard deviation of portfolio return.

D) beta and the standard deviation of portfolio return.

A) efficient portfolios and beta.

B) the risk-free asset and standard deviation of the portfolio return.

C) the optimal portfolio and the standard deviation of portfolio return.

D) beta and the standard deviation of portfolio return.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

30

A portfolio has 25% of its funds invested in Security C and 75% of its funds invested in Security D. Security C has an expected return of 8% and a standard deviation of 6%. Security B has an expected return of 10% and a standard deviation of 10%. The securities have a coefficient of correlation of.6. Which of the following values is closest to portfolio return and variance?

A) .095; .001675.

B) .095; .0072.

C) .100; .00849.

D) .090;.0081.

A) .095; .001675.

B) .095; .0072.

C) .100; .00849.

D) .090;.0081.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

31

The standard deviation of a portfolio will tend to increase when:

A) a risky asset in the portfolio is replaced with Treasury bills.

B) short-term bonds are replaced with Treasury Bills.

C) the portfolio concentration in a single cyclical industry increases.

D) the weights of the various diverse securities become more evenly distributed.

A) a risky asset in the portfolio is replaced with Treasury bills.

B) short-term bonds are replaced with Treasury Bills.

C) the portfolio concentration in a single cyclical industry increases.

D) the weights of the various diverse securities become more evenly distributed.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

32

Beta measures:

A) the ability to diversify risk.

B) how an asset covaries with the market.

C) the actual return on an asset.

D) the standard of the assets' returns.

A) the ability to diversify risk.

B) how an asset covaries with the market.

C) the actual return on an asset.

D) the standard of the assets' returns.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

33

The dominant portfolio with the lowest possible risk measures is:

A) the efficient frontier.

B) the minimum variance portfolio.

C) the upper tail of the efficient set.

D) the tangency portfolio.

A) the efficient frontier.

B) the minimum variance portfolio.

C) the upper tail of the efficient set.

D) the tangency portfolio.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

34

A portfolio has 35% of its funds invested in Security One and 65% of its funds invested in Security Two. Security One has a standard deviation of 6. Security Two has a standard deviation of 12. The securities have a coefficient of correlation of.5. Which of the following values is closest to portfolio variance?

A) 81.

B) 90.

C) 27.

D) 6561.

A) 81.

B) 90.

C) 27.

D) 6561.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

35

When many assets are included in a portfolio or index the risk of the portfolio or index will be:

A) less than the risk of the securities because the correlations are greater than 1.

B) equal to the risk of the securities because the correlations are equal to 1.

C) less than the risk of the securities because the correlations are usually less than 1.

D) unaffected by the risk of securities because their correlations are less than 1.

A) less than the risk of the securities because the correlations are greater than 1.

B) equal to the risk of the securities because the correlations are equal to 1.

C) less than the risk of the securities because the correlations are usually less than 1.

D) unaffected by the risk of securities because their correlations are less than 1.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

36

The diversification effect of a portfolio of two stocks:

A) increases as the correlation between the stocks declines.

B) increases as the correlation between the stocks rises.

C) decreases as the correlation between the stocks rises.

D) Both increases as the correlation between the stocks declines; and decreases as the correlation between the stocks rises.

A) increases as the correlation between the stocks declines.

B) increases as the correlation between the stocks rises.

C) decreases as the correlation between the stocks rises.

D) Both increases as the correlation between the stocks declines; and decreases as the correlation between the stocks rises.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

37

The measure of beta associates most closely with:

A) idiosyncratic risk.

B) risk-free return.

C) systematic risk.

D) unexpected risk.

E) unsystematic risk.

A) idiosyncratic risk.

B) risk-free return.

C) systematic risk.

D) unexpected risk.

E) unsystematic risk.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

38

You've owned a share of stock for 6 years. It returned 5% in 3 of those years and -5% in the other 3. What was the variance?

A) 0.15%.

B) 0.16%.

C) 0.25%.

D) 0%.

A) 0.15%.

B) 0.16%.

C) 0.25%.

D) 0%.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

39

Which one of the following would indicate a portfolio is being effectively diversified?

A) An increase in the portfolio beta.

B) A decrease in the portfolio beta.

C) An increase in the portfolio rate of return.

D) A decrease in the portfolio standard deviation.

A) An increase in the portfolio beta.

B) A decrease in the portfolio beta.

C) An increase in the portfolio rate of return.

D) A decrease in the portfolio standard deviation.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

40

A well-diversified portfolio has negligible:

A) expected return.

B) systematic risk.

C) unsystematic risk.

D) variance.

A) expected return.

B) systematic risk.

C) unsystematic risk.

D) variance.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

41

Given the following information on 3 stocks:

Using the CAPM, calculate the expected return for Stock's A, B, and

C. Which stocks would you recommend purchasing?

BA = .0070/.0064 = 1.094; ra = .07 + (.18-.07)1.094 = .1903

BB = .0045/.0064 = 0.703; rb = .07 + (.18-.07)0.703 = .1473

BC = .0013/.0064 = 0.203; rc = .07 + (.18-.07)0.203 = .0923

Indifferent on A as .1903 _.19.

Would buy B as.15 > .1473.

Would not buy C as.09 < .0923.

Using the CAPM, calculate the expected return for Stock's A, B, and C. Which stocks would you recommend purchasing?

BA = .0070/.0064 = 1.094; ra = .07 + (.18-.07)1.094 = .1903

BB = .0045/.0064 = 0.703; rb = .07 + (.18-.07)0.703 = .1473

BC = .0013/.0064 = 0.203; rc = .07 + (.18-.07)0.203 = .0923

Indifferent on A as .1903 _.19.

Would buy B as.15 > .1473.

Would not buy C as.09 < .0923.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

42

The characteristic line is graphically depicted as:

A) the plot of the relationship between beta and expected return.

B) the plot of the returns of the security against the beta.

C) the plot of the security against the market index returns.

D) the plot of the beta against the market index returns.

A) the plot of the relationship between beta and expected return.

B) the plot of the returns of the security against the beta.

C) the plot of the security against the market index returns.

D) the plot of the beta against the market index returns.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

43

According to the CAPM, the expected return on a risky asset depends on three components. Describe each component, and explain its role in determining expected return.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

44

A security that is fairly priced will have a return _____ the Security Market Line.

A) below

B) on or below

C) on

D) on or above

E) above

A) below

B) on or below

C) on

D) on or above

E) above

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

45

The combination of the efficient set of portfolios with a riskless lending and borrowing rate results in:

A) the capital market line which shows that all investors will only invest in the riskless asset.

B) the capital market line which shows that all investors will invest in a combination of the riskless asset and the tangency portfolio.

C) the security market line which shows that all investors will invest in the riskless asset only.

D) the security market line which shows that all investors will invest in a combination of the riskless asset and the tangency portfolio.

A) the capital market line which shows that all investors will only invest in the riskless asset.

B) the capital market line which shows that all investors will invest in a combination of the riskless asset and the tangency portfolio.

C) the security market line which shows that all investors will invest in the riskless asset only.

D) the security market line which shows that all investors will invest in a combination of the riskless asset and the tangency portfolio.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

46

Suppose the MiniCD Corporation's common stock has a return of 12%. Assume the risk-free rate is 4%, the expected market return is 9%, and no unsystematic influence affected Mini's return. The beta for MiniCD is:

A) 0.89.

B) 1.60.

C) 2.40.

D) 3.00.

A) 0.89.

B) 1.60.

C) 2.40.

D) 3.00.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

47

The separation principle states that an investor will:

A) choose any efficient portfolio and invest some amount in the riskless asset to generate the expected return.

B) choose an efficient portfolio based on individual risk tolerance or utility.

C) never choose to invest in the riskless asset because the expected return on the riskless asset is lower over time.

D) invest only in the riskless asset and tangency portfolio choosing the weights based on individual risk tolerance.

A) choose any efficient portfolio and invest some amount in the riskless asset to generate the expected return.

B) choose an efficient portfolio based on individual risk tolerance or utility.

C) never choose to invest in the riskless asset because the expected return on the riskless asset is lower over time.

D) invest only in the riskless asset and tangency portfolio choosing the weights based on individual risk tolerance.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

48

You want your portfolio beta to be 1.20. Currently, your portfolio consists of $100 invested in stock A with a beta of 1.4 and $300 in stock B with a beta of.6. You have another $400 to invest and want to divide it between an asset with a beta of 1.6 and a risk-free asset. How much should you invest in the risk-free asset?

A) $0

B) $140

C) $200

D) $320

A) $0

B) $140

C) $200

D) $320

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

49

Returns for the IC Company and for the S&P 500 Index over the previous 4-year period are given below:

What are the average returns on IC and on the S&P 500 index? If you had invested $1.00 in IC, how much would you have had after 4 years? What is the correlation between the returns on IC and the S&P?

What are the average returns on IC and on the S&P 500 index? If you had invested $1.00 in IC, how much would you have had after 4 years? What is the correlation between the returns on IC and the S&P? Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

50

Suppose the JumpStart Corporation's common stock has a beta of 0.8. If the risk-free rate is 4% and the expected market return is 9%, the expected return for JumpStart's common is:

A) 3.2%.

B) 4.0%.

C) 7.2%.

D) 8.0%.

E) 9.0%.

A) 3.2%.

B) 4.0%.

C) 7.2%.

D) 8.0%.

E) 9.0%.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

51

A portfolio exists containing stocks D, E, and F held in proportions 30%, 40%, and 30% respectively. The expected returns on the three stocks are given by 12%, 20%, and 28% respectively. Calculate the portfolio's expected return.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

52

Given the following information on three stocks:

= -.05333

bc

Suppose you desire to invest in any one of the stocks listed above. Can any be recommended?

= -.05333bc

Suppose you desire to invest in any one of the stocks listed above. Can any be recommended?

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

53

The elements in the off-diagonal positions of the Variance Covariance matrix are:

A) covariances.

B) security selections.

C) variances.

D) security weights.

A) covariances.

B) security selections.

C) variances.

D) security weights.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

54

The beta of a security is calculated by:

A) dividing the covariance of the security with the market by the variance of the market.

B) dividing the correlation of the security with the market by the variance of the market.

C) dividing the variance of the market by the covariance of the security with the market.

D) dividing the variance of the market by the correlation of the security with the market.

A) dividing the covariance of the security with the market by the variance of the market.

B) dividing the correlation of the security with the market by the variance of the market.

C) dividing the variance of the market by the covariance of the security with the market.

D) dividing the variance of the market by the correlation of the security with the market.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

55

Given the following information on three stocks:

= -.05333

bc

Now suppose you diversify into two securities. Given all choices, can any portfolio be eliminated? Assume equal weights.

= -.05333bc

Now suppose you diversify into two securities. Given all choices, can any portfolio be eliminated? Assume equal weights.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

56

Explain in words what beta is and why it is an important tool of security valuation.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

57

A stock with a beta of zero would be expected to:

A) have a rate of return equal to the risk-free rate.

B) have a rate of return equal to the market rate.

C) have a rate of return equal to zero.

D) have a rate of return equal to the one.

A) have a rate of return equal to the risk-free rate.

B) have a rate of return equal to the market rate.

C) have a rate of return equal to zero.

D) have a rate of return equal to the one.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

58

A portfolio is made up of 75% of stock 1, and 25% of stock 2. Stock 1 has a variance of.08, and stock 2 has a variance of.035. The covariance between the stocks is -.001. Calculate both the variance and the standard deviation of the portfolio.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

59

The elements along the diagonal of the Variance Covariance matrix are:

A) covariances.

B) security weights.

C) security selections.

D) variances.

A) covariances.

B) security weights.

C) security selections.

D) variances.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

60

A portfolio contains four assets. Asset 1 has a beta of.8 and comprises 30% of the portfolio. Asset 2 has a beta of 1.1 and comprises 30% of the portfolio. Asset 3 has a beta of 1.5 and comprises 20% of the portfolio. Asset 4 has a beta of 1.6 and comprises the remaining 20% of the portfolio. If the riskless rate is expected to be 3% and the market risk premium is 6%, what is the beta of the portfolio, the expected return on the portfolio and the market?

A) 1.19; 6.57%; 6.00%

B) 1.19; 7.14%; 6.00%

C) 1.19; 10.14%; 9.00%

D) 1.25; 10.50%; 6.00%

E) 1.25; 10.50%; 9.00%

A) 1.19; 6.57%; 6.00%

B) 1.19; 7.14%; 6.00%

C) 1.19; 10.14%; 9.00%

D) 1.25; 10.50%; 6.00%

E) 1.25; 10.50%; 9.00%

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

61

Draw and explain the relationship between the opportunity set for a two asset portfolio when the correlation is: [Choose from -1, -.5, 0, +.5, and +1]

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

62

Why are some risks diversifiable and some nondiversifiable? Give an example of each.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

63

Draw the SML and plot asset C such that it has less risk than the market but plots above the SML, and asset D such that it has more risk than the market and plots below the SML. (Be sure to indicate where the market portfolio is on your graph.) Explain how assets like C or D can plot as they do and explain why such pricing cannot persist in a market that is in equilibrium.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

64

We routinely assume that investors are risk-averse return-seekers; i.e., they like returns and dislike risk. If so, why do we contend that only systematic risk and not total risk is important?

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

65

The diagram below represents an opportunity set for a two asset combination. Indicate the correct efficient set with labels; explain why it is so.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 65 flashcards in this deck.