Deck 18: Pricing and Profitability Analysis

Full screen (f)

Question

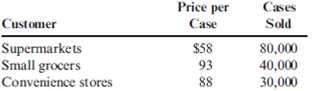

Costs of Different Customer Classes

Kaune Food Products Company manufactures canned mixed nuts with an average manufacturing cost of $52 per case (a case contains 24 cans of nuts). Kaune sold 150,000 cases last year to the following three classes of customer:

The supermarkets require special labeling on each can costing $0.04 per can. They order through electronic data interchange (EDI), which costs Kaune about $61,000 annually in operating expenses and depreciation. Kaune delivers the nuts to the stores and stocks them on the shelves. This distribution costs $45,000 per year.

The small grocers order in smaller lots that require special picking and packing in the factory; the special handling adds $25 to the cost of each case sold. Sales commissions to the independent jobbers who sell Kaune products to the grocers average 8 percent of sales. Bad debts expense amounts to 9 percent of sales.

Convenience stores also require special handling that costs $30 per case. In addition, Kaune is required to co-pay advertising costs with the convenience stores at a cost of $15,000 per year. Frequent stops are made to each convenience store by Kaune delivery trucks at a cost of $30,000 per year.

Required:

1. Calculate the total cost per case for each of the three customer classes. (Round unit costs to four significant digits.)

2. Using the costs from Requirement 1, calculate the profit per case per customer class. Does the cost analysis support the charging of different prices? Why or why not?

3. What if Kaune charged the average price per case to all customer classes? How would that affect the profit percentages?

Kaune Food Products Company manufactures canned mixed nuts with an average manufacturing cost of $52 per case (a case contains 24 cans of nuts). Kaune sold 150,000 cases last year to the following three classes of customer:

The supermarkets require special labeling on each can costing $0.04 per can. They order through electronic data interchange (EDI), which costs Kaune about $61,000 annually in operating expenses and depreciation. Kaune delivers the nuts to the stores and stocks them on the shelves. This distribution costs $45,000 per year.

The small grocers order in smaller lots that require special picking and packing in the factory; the special handling adds $25 to the cost of each case sold. Sales commissions to the independent jobbers who sell Kaune products to the grocers average 8 percent of sales. Bad debts expense amounts to 9 percent of sales.

Convenience stores also require special handling that costs $30 per case. In addition, Kaune is required to co-pay advertising costs with the convenience stores at a cost of $15,000 per year. Frequent stops are made to each convenience store by Kaune delivery trucks at a cost of $30,000 per year.

Required:

1. Calculate the total cost per case for each of the three customer classes. (Round unit costs to four significant digits.)

2. Using the costs from Requirement 1, calculate the profit per case per customer class. Does the cost analysis support the charging of different prices? Why or why not?

3. What if Kaune charged the average price per case to all customer classes? How would that affect the profit percentages?

Question

Question

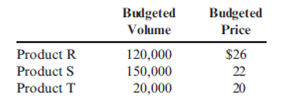

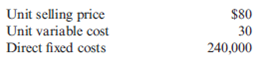

Pricing Strategy, Sales Variances

Eastman, Inc., manufactures and sells three products: R, S, and T. In January, Eastman, Inc., budgeted sales of the following.

At the end of the year, actual sales revenue for Product R and Product S was $3,075,000 and $3,254,000, respectively. The actual price charged for Product R was $25 and for Product S was $20. Only $10 was charged for Product T to encourage more consumers to buy it, and actual sales revenue equaled $540,000 for this product.

Required:

1. Calculate the sales price and sales volume variances for each of the three products based on the original budget.

2. Suppose that Product T is a new product just introduced during the year. What pricing strategy is Eastman, Inc., following for this product?

Eastman, Inc., manufactures and sells three products: R, S, and T. In January, Eastman, Inc., budgeted sales of the following.

At the end of the year, actual sales revenue for Product R and Product S was $3,075,000 and $3,254,000, respectively. The actual price charged for Product R was $25 and for Product S was $20. Only $10 was charged for Product T to encourage more consumers to buy it, and actual sales revenue equaled $540,000 for this product.

Required:

1. Calculate the sales price and sales volume variances for each of the three products based on the original budget.

2. Suppose that Product T is a new product just introduced during the year. What pricing strategy is Eastman, Inc., following for this product?

Question

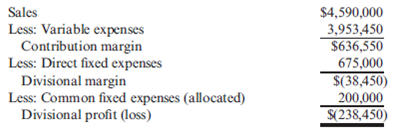

Segmented Income Statements, Adding and Dropping Product Lines

Dantrell Palmer has just been appointed manager of Kirchner Glass Products Division. He has two years to make the division profitable. If the division is still showing a loss after two years, it will be eliminated, and Dantrell will be reassigned as an assistant divisional manager in another division. The divisional income statement for the most recent year is as follows:

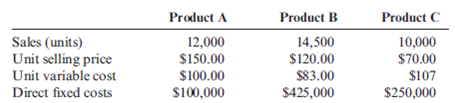

Upon arriving at the division, Dantrell requested the following data on the division's three products:

He also gathered data on a proposed new product (Product D). If this product is added, it would displace one of the current products; the quantity that could be produced and sold would equal the quantity sold of the product it displaces, although demand limits the maximum quantity that could be sold to 20,000 units. Because of specialized production equipment, it is not possible for the new product to displace part of the production of a second product. The information on Product D is as follows:

Required:

1. Prepare segmented income statements for Products A, B, and C.

2. Determine the products that Dantrell should produce for the coming year. Prepare segmented income statements that prove your combination is the best for the division. By how much will profits improve given the combination that you selected? (Hint: Your combination may include one, two, or three products.)

Dantrell Palmer has just been appointed manager of Kirchner Glass Products Division. He has two years to make the division profitable. If the division is still showing a loss after two years, it will be eliminated, and Dantrell will be reassigned as an assistant divisional manager in another division. The divisional income statement for the most recent year is as follows:

Upon arriving at the division, Dantrell requested the following data on the division's three products:

He also gathered data on a proposed new product (Product D). If this product is added, it would displace one of the current products; the quantity that could be produced and sold would equal the quantity sold of the product it displaces, although demand limits the maximum quantity that could be sold to 20,000 units. Because of specialized production equipment, it is not possible for the new product to displace part of the production of a second product. The information on Product D is as follows:

Required:

1. Prepare segmented income statements for Products A, B, and C.

2. Determine the products that Dantrell should produce for the coming year. Prepare segmented income statements that prove your combination is the best for the division. By how much will profits improve given the combination that you selected? (Hint: Your combination may include one, two, or three products.)

Question

Question

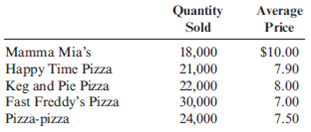

Elasticity of Demand and Market Structure

Janet Gordon and Phil Hopkins graduated several years ago with M.S. degrees in accounting and set up a full-service accounting firm. Janet and Phil have many small business clients and have noticed some pricing trends while compiling annual financial statements. The following data are for five of the pizza parlors that are Janet and Phil's clients.

Required:

1. Is the demand for pizza relatively more elastic or inelastic?

2. What type of market structure characterizes the pizza industry? How do you suppose that Mamma Mia's can charge so much more per pizza than Fast Freddy's does?

Janet Gordon and Phil Hopkins graduated several years ago with M.S. degrees in accounting and set up a full-service accounting firm. Janet and Phil have many small business clients and have noticed some pricing trends while compiling annual financial statements. The following data are for five of the pizza parlors that are Janet and Phil's clients.

Required:

1. Is the demand for pizza relatively more elastic or inelastic?

2. What type of market structure characterizes the pizza industry? How do you suppose that Mamma Mia's can charge so much more per pizza than Fast Freddy's does?

Question

Question

Operating Income for Segments

Alydar, Inc., manufactures and sells automotive tools through three divisions: Eastern, Southern, and International. Each division is evaluated as a profit center. Data for each division for last year are as follows:

Alydar, Inc., had corporate administrative expenses equal to $585,000; these were not allocated to the divisions.

Required:

1. Prepare a segmented income statement for Alydar, Inc., for last year.

2. Comment on the performance of each of the divisions.

Alydar, Inc., manufactures and sells automotive tools through three divisions: Eastern, Southern, and International. Each division is evaluated as a profit center. Data for each division for last year are as follows:

Alydar, Inc., had corporate administrative expenses equal to $585,000; these were not allocated to the divisions.

Required:

1. Prepare a segmented income statement for Alydar, Inc., for last year.

2. Comment on the performance of each of the divisions.

Question

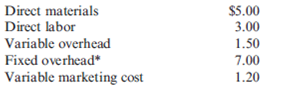

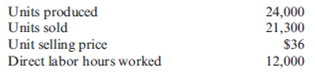

Absorption Costing, Value of Ending Inventory, Operating Income

Pattison Products, Inc., began operations in October and manufactured 40,000 units during the month with the following unit costs:

* Fixed overhead per unit = $280,000/40,000 units produced = $7

Total fixed factory overhead is $280,000 per month. During October, 38,400 units were sold at a price of $24, and fixed marketing and administrative expenses were $130,500.

Required:

1. Calculate the cost of each unit using absorption costing.

2. How many units remain in ending inventory? What is the cost of ending inventory using absorption costing?

3. Prepare an absorption-costing income statement for Pattison Products, Inc., for the month of October.

4. What if November production was 40,000 units, costs were stable, and sales were 41,000 units? What is the cost of ending inventory? What is operating income for November?

Pattison Products, Inc., began operations in October and manufactured 40,000 units during the month with the following unit costs:

* Fixed overhead per unit = $280,000/40,000 units produced = $7

Total fixed factory overhead is $280,000 per month. During October, 38,400 units were sold at a price of $24, and fixed marketing and administrative expenses were $130,500.

Required:

1. Calculate the cost of each unit using absorption costing.

2. How many units remain in ending inventory? What is the cost of ending inventory using absorption costing?

3. Prepare an absorption-costing income statement for Pattison Products, Inc., for the month of October.

4. What if November production was 40,000 units, costs were stable, and sales were 41,000 units? What is the cost of ending inventory? What is operating income for November?

Question

Question

Question

Product Profitability

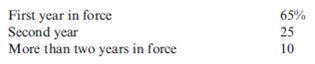

Porter Insurance Company has three lines of insurance: automobile, property, and life. The life insurance segment has been losing money for the past five quarters, and Leah Harper, Porter's controller, has done an analysis of that segment. She has discovered that the commission paid to the agent for the first year the policy is in place is 55 percent of the first-year premium. The second-year commission is 20 percent, and all succeeding years a commission equal to 5 percent of premiums is paid. No salaries are paid to agents; however, Porter does advertise on television and in magazines. Last year, the advertising expense was $500,000. The loss rate (payout on claims) averages 50 percent. Administrative expenses equal $450,000 per year. Revenue last year was $10,000,000 (premiums). The percentage of policies of various lengths is as follows:

Experience has shown that if a policy remains in effect for more than two years, it is rarely cancelled.

Leah is considering two alternative plans to turn this segment around. Plan 1 requires spending $250,000 on improved customer claim service in hopes that the percentage of policies in effect will take on the following distribution:

Total premiums would remain constant at $10,000,000, and there are no other changes in fixed or variable cost behavior.

Plan 2 involves dropping the independent agent and commission system and having potential policyholders phone in requests for coverage. Leah estimates that revenue would drop to $7,000,000. Commissions would be zero, but administrative expenses would rise by $1,200,000, and advertising (including direct mail solicitation) would increase by $1,000,000.

Required:

1. Prepare a variable-costing income statement for last year for the life insurance segment of Porter Insurance Company.

2. What impact would Plan 1 have on income?

3. What impact would Plan 2 have on income?

Porter Insurance Company has three lines of insurance: automobile, property, and life. The life insurance segment has been losing money for the past five quarters, and Leah Harper, Porter's controller, has done an analysis of that segment. She has discovered that the commission paid to the agent for the first year the policy is in place is 55 percent of the first-year premium. The second-year commission is 20 percent, and all succeeding years a commission equal to 5 percent of premiums is paid. No salaries are paid to agents; however, Porter does advertise on television and in magazines. Last year, the advertising expense was $500,000. The loss rate (payout on claims) averages 50 percent. Administrative expenses equal $450,000 per year. Revenue last year was $10,000,000 (premiums). The percentage of policies of various lengths is as follows:

Experience has shown that if a policy remains in effect for more than two years, it is rarely cancelled.

Leah is considering two alternative plans to turn this segment around. Plan 1 requires spending $250,000 on improved customer claim service in hopes that the percentage of policies in effect will take on the following distribution:

Total premiums would remain constant at $10,000,000, and there are no other changes in fixed or variable cost behavior.

Plan 2 involves dropping the independent agent and commission system and having potential policyholders phone in requests for coverage. Leah estimates that revenue would drop to $7,000,000. Commissions would be zero, but administrative expenses would rise by $1,200,000, and advertising (including direct mail solicitation) would increase by $1,000,000.

Required:

1. Prepare a variable-costing income statement for last year for the life insurance segment of Porter Insurance Company.

2. What impact would Plan 1 have on income?

3. What impact would Plan 2 have on income?

Question

Question

Question

Question

Question

Question

Question

Question

Customer Profitability

Olin Company manufactures and distributes carpentry tools. Production of the tools is in the mature portion of the product life cycle. Olin has a sales force of 20. Salespeople are paid a commission of 7 percent of sales, plus expenses of $35 per day for days spent on the road away from home, plus $0.50 per mile. They deliver products in addition to making the sales, and each salesperson is required to own a truck suitable for making deliveries.

For the coming quarter, Olin estimates the following:

On average, a salesperson travels 6,000 miles per quarter and spends 38 days on the road. The fixed marketing and administrative expenses total $400,000 per quarter.

Required:

1. Prepare an income statement for Olin Company for the next quarter.

2. Suppose that a large hardware chain, MegaHardware, Inc., wants Olin Company to produce its new SuperTool line. This would require Olin Company to sell 80 percent of total output to the chain. The tools will be imprinted with the SuperTool brand, requiring Olin to purchase new equipment, use somewhat different materials, and reconfigure the production line. Olin's industrial engineers estimate that cost of goods sold for the SuperTool line would increase by 15 percent. No sales commission would be incurred, and MegaHardware would link Olin to its EDI system. This would require an annual cost of $100,000 on the part of Olin. MegaHardware would pay shipping. As a result, the sales force would shrink by 80 percent. Should Olin accept MegaHardware's offer? Support your answer with appropriate calculations.

Olin Company manufactures and distributes carpentry tools. Production of the tools is in the mature portion of the product life cycle. Olin has a sales force of 20. Salespeople are paid a commission of 7 percent of sales, plus expenses of $35 per day for days spent on the road away from home, plus $0.50 per mile. They deliver products in addition to making the sales, and each salesperson is required to own a truck suitable for making deliveries.

For the coming quarter, Olin estimates the following:

On average, a salesperson travels 6,000 miles per quarter and spends 38 days on the road. The fixed marketing and administrative expenses total $400,000 per quarter.

Required:

1. Prepare an income statement for Olin Company for the next quarter.

2. Suppose that a large hardware chain, MegaHardware, Inc., wants Olin Company to produce its new SuperTool line. This would require Olin Company to sell 80 percent of total output to the chain. The tools will be imprinted with the SuperTool brand, requiring Olin to purchase new equipment, use somewhat different materials, and reconfigure the production line. Olin's industrial engineers estimate that cost of goods sold for the SuperTool line would increase by 15 percent. No sales commission would be incurred, and MegaHardware would link Olin to its EDI system. This would require an annual cost of $100,000 on the part of Olin. MegaHardware would pay shipping. As a result, the sales force would shrink by 80 percent. Should Olin accept MegaHardware's offer? Support your answer with appropriate calculations.

Question

Question

Question

Question

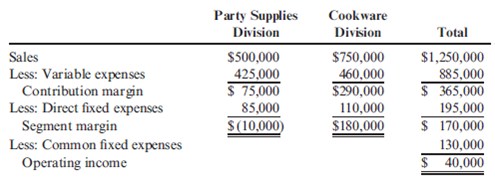

Segmented Income Statements: Analysis of Proposals to Improve Profits

Shannon, Inc., has two divisions. One produces and sells paper party supplies (napkins, paper plates, invitations); the other produces and sells cookware. A segmented income statement for the most recent quarter is given below:

On seeing the quarterly statement, Madge Shannon, president of Shannon, Inc., was distressed and discussed her disappointment with Bob Ferguson, the company's vice president of finance.

MADGE : "The Party Supplies Division is killing us. It's not even covering its own fixed costs. I'm beginning to believe that we should shut down that division. This is the seventh consecutive quarter it has failed to provide a positive segment margin. I was certain that Paula Kelly could turn it around. But this is her third quarter, and she hasn't done much better than the previous divisional manager."

BOB : "Well, before you get too excited about the situation, perhaps you should evaluate Paula's most recent proposals. She wants to spend $10,000 per quarter for the right to use familiar cartoon figures on a new series of invitations, plates, and napkins and at the same time increase the advertising budget by $25,000 per quarter to let the public know about them. According to her marketing people, sales should increase by 10 percent if the right advertising is done-and done quickly. In addition, Paula wants to lease some new production machinery that will increase the rate of production, lower labor costs, and result in less waste of materials. Paula claims that variable costs will be reduced by 30 percent. The cost of the lease is $95,000 per quarter."

Upon hearing this news, Madge calmed considerably and, in fact, was somewhat pleased. After all, she was the one who had selected Paula and had a great deal of confidence in Paula's judgment and abilities.

Required:

1. Assuming that Paula's proposals are sound, should Madge Shannon be pleased with the prospects for the Party Supplies Division? Prepare a segmented income statement for the next quarter that reflects the implementation of Paula's proposals. Assume that the Cookware Division's sales increase by 5 percent for the next quarter and that the same cost relationships hold.

2. Suppose that everything materializes as Paula projected except for the 10 percent increase in sales-no change in sales revenues takes place. Are the proposals still sound? What if the variable costs are reduced by 40 percent instead of 30 percent with no change in sales?

Shannon, Inc., has two divisions. One produces and sells paper party supplies (napkins, paper plates, invitations); the other produces and sells cookware. A segmented income statement for the most recent quarter is given below:

On seeing the quarterly statement, Madge Shannon, president of Shannon, Inc., was distressed and discussed her disappointment with Bob Ferguson, the company's vice president of finance.

MADGE : "The Party Supplies Division is killing us. It's not even covering its own fixed costs. I'm beginning to believe that we should shut down that division. This is the seventh consecutive quarter it has failed to provide a positive segment margin. I was certain that Paula Kelly could turn it around. But this is her third quarter, and she hasn't done much better than the previous divisional manager."

BOB : "Well, before you get too excited about the situation, perhaps you should evaluate Paula's most recent proposals. She wants to spend $10,000 per quarter for the right to use familiar cartoon figures on a new series of invitations, plates, and napkins and at the same time increase the advertising budget by $25,000 per quarter to let the public know about them. According to her marketing people, sales should increase by 10 percent if the right advertising is done-and done quickly. In addition, Paula wants to lease some new production machinery that will increase the rate of production, lower labor costs, and result in less waste of materials. Paula claims that variable costs will be reduced by 30 percent. The cost of the lease is $95,000 per quarter."

Upon hearing this news, Madge calmed considerably and, in fact, was somewhat pleased. After all, she was the one who had selected Paula and had a great deal of confidence in Paula's judgment and abilities.

Required:

1. Assuming that Paula's proposals are sound, should Madge Shannon be pleased with the prospects for the Party Supplies Division? Prepare a segmented income statement for the next quarter that reflects the implementation of Paula's proposals. Assume that the Cookware Division's sales increase by 5 percent for the next quarter and that the same cost relationships hold.

2. Suppose that everything materializes as Paula projected except for the 10 percent increase in sales-no change in sales revenues takes place. Are the proposals still sound? What if the variable costs are reduced by 40 percent instead of 30 percent with no change in sales?

Question

Question

Question

Price Discrimination, Customer Costs

Jorell, Inc., manufactures and distributes a variety of labelers. Annual production of labelers averages 340,000 units. A large chain store purchases about 30 percent of Jorell's production. Several thousand independent retail office supply stores purchase the other 70 percent. Jorell incurs the following costs of production per labeler:

Jorell has two salespeople assigned to the chain store account at a cost of $55,000 each per year. Delivery is made in 1,500 unit batches about three times a month at a delivery cost of $750 per batch. Eight salespeople service the remaining accounts. They call on the stores and incur salary and mileage expenses of approximately $41,000 each. Delivery costs vary from store to store, averaging $0.60 per unit.

Jorell charges the chain store $16.50 per labeler and the independent office supply stores $20 per labeler.

Required:

Is Jorell's pricing policy supported by cost differences in serving the two different classes of customer? Support your answer with relevant calculations. (Round unit costs to the nearest cent.)

Jorell, Inc., manufactures and distributes a variety of labelers. Annual production of labelers averages 340,000 units. A large chain store purchases about 30 percent of Jorell's production. Several thousand independent retail office supply stores purchase the other 70 percent. Jorell incurs the following costs of production per labeler:

Jorell has two salespeople assigned to the chain store account at a cost of $55,000 each per year. Delivery is made in 1,500 unit batches about three times a month at a delivery cost of $750 per batch. Eight salespeople service the remaining accounts. They call on the stores and incur salary and mileage expenses of approximately $41,000 each. Delivery costs vary from store to store, averaging $0.60 per unit.

Jorell charges the chain store $16.50 per labeler and the independent office supply stores $20 per labeler.

Required:

Is Jorell's pricing policy supported by cost differences in serving the two different classes of customer? Support your answer with relevant calculations. (Round unit costs to the nearest cent.)

Question

Segmented Reporting and Variances

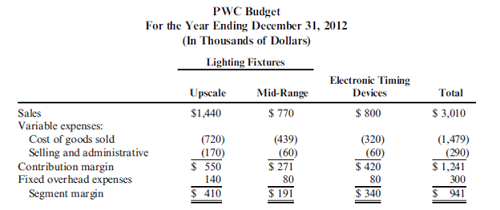

Pittsburgh-Walsh Company (PWC) is a manufacturing company whose product line consists of lighting fixtures and electronic timing devices. The Lighting Fixtures Division assembles units for the upscale and mid-range markets. The Electronic Timing Devices Division manufactures instrument panels that allow electronic systems to be activated and deactivated at scheduled times for both efficiency and safety purposes. Both divisions operate out of the same manufacturing facilities and share production equipment.

PWC's budget for the year ending December 31, 2012, follows and was prepared on a business segment basis under the following guidelines:

a. Variable expenses are directly assigned to the incurring division.

b. Fixed overhead expenses are directly assigned to the incurring division.

c. The production plan is for 8,000 upscale fixtures, 22,000 mid-range fixtures, and 20,000 electronic timing devices. Production equals sales.

PWC established a bonus plan for division management that required meeting the budget's planned operating income by product line, with a bonus increment if the division exceeds the planned product line operating income by 10 percent or more.

Shortly before the year began, the CEO, Jack Parkow, suffered a heart attack and retired. After reviewing the 2012 budget, the new CEO, Joe Kelly, decided to close the lighting fixtures mid-range product line by the end of the first quarter and use the available production capacity to grow the remaining two product lines. The marketing staff advised that electronic timing devices could grow by 40 percent with increased direct sales support. Increases above that level and increasing sales of upscale lighting fixtures would require expanded advertising expenditures to increase consumer awareness of PWC as an electronics and upscale lighting fixtures company. Kelly approved the increased sales support and advertising expenditures to achieve the revised plan. Kelly advised the divisions that for bonus purposes the original product-line operating income objectives must be met, but he did allow the Lighting Fixtures Division to combine the operating income objectives for both product lines for bonus purposes.

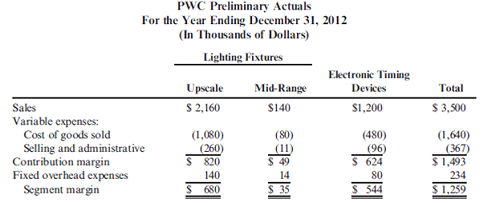

Prior to the close of the fiscal year, the division controllers were furnished with preliminary actual data for review and adjustment, as appropriate. These preliminary year-end data reflect the revised units of production amounting to 12,000 upscale fixtures, 4,000 mid-range fixtures, and 30,000 electronic timing devices and are presented as follows:

The controller of the Lighting Fixtures Division, anticipating a similar bonus plan for 2013, is contemplating deferring some revenues to the next year on the pretext that the sales are not yet final and accruing in the current year expenditures that will be applicable to the first quarter of 2013. The corporation would meet its annual plan, and the division would exceed the 10 percent incremental bonus plateau in 2012 despite the deferred revenues and accrued expenses contemplated.

Required:

1. Outline the benefits that an organization realizes from segment reporting. Evaluate segment reporting on a variable-costing basis versus an absorption-costing basis.

2. Calculate the contribution margin, contribution margin volume, and sales mix variances.

3. Explain why the variances occurred. ( CMA adapted )

Pittsburgh-Walsh Company (PWC) is a manufacturing company whose product line consists of lighting fixtures and electronic timing devices. The Lighting Fixtures Division assembles units for the upscale and mid-range markets. The Electronic Timing Devices Division manufactures instrument panels that allow electronic systems to be activated and deactivated at scheduled times for both efficiency and safety purposes. Both divisions operate out of the same manufacturing facilities and share production equipment.

PWC's budget for the year ending December 31, 2012, follows and was prepared on a business segment basis under the following guidelines:

a. Variable expenses are directly assigned to the incurring division.

b. Fixed overhead expenses are directly assigned to the incurring division.

c. The production plan is for 8,000 upscale fixtures, 22,000 mid-range fixtures, and 20,000 electronic timing devices. Production equals sales.

PWC established a bonus plan for division management that required meeting the budget's planned operating income by product line, with a bonus increment if the division exceeds the planned product line operating income by 10 percent or more.

Shortly before the year began, the CEO, Jack Parkow, suffered a heart attack and retired. After reviewing the 2012 budget, the new CEO, Joe Kelly, decided to close the lighting fixtures mid-range product line by the end of the first quarter and use the available production capacity to grow the remaining two product lines. The marketing staff advised that electronic timing devices could grow by 40 percent with increased direct sales support. Increases above that level and increasing sales of upscale lighting fixtures would require expanded advertising expenditures to increase consumer awareness of PWC as an electronics and upscale lighting fixtures company. Kelly approved the increased sales support and advertising expenditures to achieve the revised plan. Kelly advised the divisions that for bonus purposes the original product-line operating income objectives must be met, but he did allow the Lighting Fixtures Division to combine the operating income objectives for both product lines for bonus purposes.

Prior to the close of the fiscal year, the division controllers were furnished with preliminary actual data for review and adjustment, as appropriate. These preliminary year-end data reflect the revised units of production amounting to 12,000 upscale fixtures, 4,000 mid-range fixtures, and 30,000 electronic timing devices and are presented as follows:

The controller of the Lighting Fixtures Division, anticipating a similar bonus plan for 2013, is contemplating deferring some revenues to the next year on the pretext that the sales are not yet final and accruing in the current year expenditures that will be applicable to the first quarter of 2013. The corporation would meet its annual plan, and the division would exceed the 10 percent incremental bonus plateau in 2012 despite the deferred revenues and accrued expenses contemplated.

Required:

1. Outline the benefits that an organization realizes from segment reporting. Evaluate segment reporting on a variable-costing basis versus an absorption-costing basis.

2. Calculate the contribution margin, contribution margin volume, and sales mix variances.

3. Explain why the variances occurred. ( CMA adapted )

Question

Question

Markup on Cost, Cost-Based Pricing

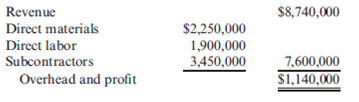

Arthur Quillen Construction Company is a general contractor that specializes in custom residential housing. Each job requires a bid that includes Quillen's direct costs and subcontractor costs as well as an amount referred to as "overhead and profit." Quillen's bidding policy is to estimate the costs of direct materials, direct labor, and subcontractors' costs. These are totaled, and a markup is applied to cover overhead and profit. In the coming year, the company believes it will be the successful bidder on 10 jobs with the following total revenues and costs:

Required:

1. Given the preceding information, what is the markup percentage on total direct costs?

2. Suppose Quillen is asked to bid on a job with estimated direct costs of $570,000. What is the bid? If the customer complains that the profit seems pretty high, how might Quillen counter that accusation?

Arthur Quillen Construction Company is a general contractor that specializes in custom residential housing. Each job requires a bid that includes Quillen's direct costs and subcontractor costs as well as an amount referred to as "overhead and profit." Quillen's bidding policy is to estimate the costs of direct materials, direct labor, and subcontractors' costs. These are totaled, and a markup is applied to cover overhead and profit. In the coming year, the company believes it will be the successful bidder on 10 jobs with the following total revenues and costs:

Required:

1. Given the preceding information, what is the markup percentage on total direct costs?

2. Suppose Quillen is asked to bid on a job with estimated direct costs of $570,000. What is the bid? If the customer complains that the profit seems pretty high, how might Quillen counter that accusation?

Question

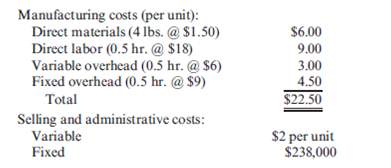

Unit Costs, Inventory Valuation, Variable and Absorption Costing

Snyder Company produced 90,000 units during its first year of operations and sold 87,000 at $21.80 per unit. The company chose practical activity-at 90,000 units-to compute its predetermined overhead rate. Manufacturing costs are as follows:

Required:

1. Calculate the unit cost and the cost of finished goods inventory under absorption costing.

2. Calculate the unit cost and the cost of finished goods inventory under variable costing.

3. What is the dollar amount that would be used to report the cost of finished goods inventory to external parties. Why?

Snyder Company produced 90,000 units during its first year of operations and sold 87,000 at $21.80 per unit. The company chose practical activity-at 90,000 units-to compute its predetermined overhead rate. Manufacturing costs are as follows:

Required:

1. Calculate the unit cost and the cost of finished goods inventory under absorption costing.

2. Calculate the unit cost and the cost of finished goods inventory under variable costing.

3. What is the dollar amount that would be used to report the cost of finished goods inventory to external parties. Why?

Question

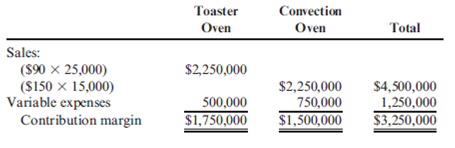

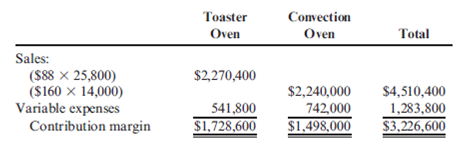

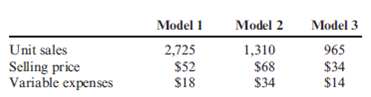

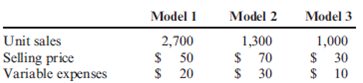

Contribution Margin Variance

Iliff, Inc., produces and sells two types of countertop ovens-the toaster oven and the convection oven. Budgeted and actual data for the two models are shown below.

Budgeted Amounts:

Actual Amounts:

Required:

1. Calculate the contribution margin variance.

2. What if actual units sold of the convection oven increased? How would that affect the contribution margin variance? What if actual units sold of the convection oven decreased? How would that affect the contribution margin variance?

Iliff, Inc., produces and sells two types of countertop ovens-the toaster oven and the convection oven. Budgeted and actual data for the two models are shown below.

Budgeted Amounts:

Actual Amounts:

Required:

1. Calculate the contribution margin variance.

2. What if actual units sold of the convection oven increased? How would that affect the contribution margin variance? What if actual units sold of the convection oven decreased? How would that affect the contribution margin variance?

Question

Question

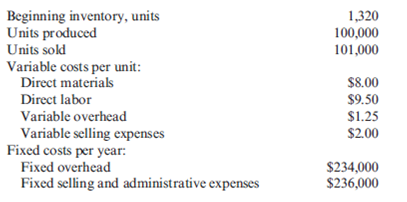

Income Statements, Variable and Absorption Costing

The following information pertains to Vladamir, Inc., for last year:

There are no work-in-process inventories. Normal activity is 100,000 units. Expected and actual overhead costs are the same. Costs have not changed from one year to the next.

Required:

1. How many units are in ending inventory?

2. Without preparing an income statement, indicate what the difference will be between variable-costing income and absorption-costing income.

3. Assume the selling price per unit is $29. Prepare an income statement using (a) variable costing and (b) absorption costing.

The following information pertains to Vladamir, Inc., for last year:

There are no work-in-process inventories. Normal activity is 100,000 units. Expected and actual overhead costs are the same. Costs have not changed from one year to the next.

Required:

1. How many units are in ending inventory?

2. Without preparing an income statement, indicate what the difference will be between variable-costing income and absorption-costing income.

3. Assume the selling price per unit is $29. Prepare an income statement using (a) variable costing and (b) absorption costing.

Question

Question

Question

Income Statements and Firm Performance: Variable and Absorption Costing

Jellison Company had the following operating data for its first two years of operations: Variable costs

Jellison produced 90,000 units in the first year and sold 80,000. In the second year, it produced 80,000 units and sold 90,000 units. The selling price per unit each year was $12. Jellison uses an actual costing system for product costing.

Required:

1. Prepare income statements for both years using absorption costing. Has firm performance, as measured by income, improved or declined from Year 1 to Year 2?

2. Prepare income statements for both years using variable costing. Has firm performance, as measured by income, improved or declined from Year 1 to Year 2?

3. Which method do you think most accurately measures firm performance? Why?

Jellison Company had the following operating data for its first two years of operations: Variable costs

Jellison produced 90,000 units in the first year and sold 80,000. In the second year, it produced 80,000 units and sold 90,000 units. The selling price per unit each year was $12. Jellison uses an actual costing system for product costing.

Required:

1. Prepare income statements for both years using absorption costing. Has firm performance, as measured by income, improved or declined from Year 1 to Year 2?

2. Prepare income statements for both years using variable costing. Has firm performance, as measured by income, improved or declined from Year 1 to Year 2?

3. Which method do you think most accurately measures firm performance? Why?

Question

Question

Question

Absorption- and Variable-Costing Income Statements

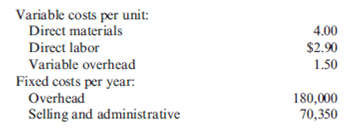

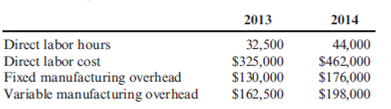

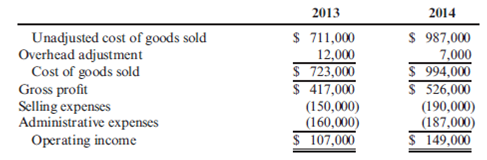

San Mateo Optics, Inc., specializes in manufacturing lenses for large telescopes and cameras used in space exploration. As the specifications for the lenses are determined by the customer and vary considerably, the company uses a job-order costing system.

Manufacturing overhead is applied to jobs on the basis of direct labor hours, utilizing the absorption- or full-costing method. San Mateo's predetermined overhead rates for 2013 and 2014 were based on the following estimates.

Jim Cimino, San Mateo's controller, would like to use variable (direct) costing for internal reporting purposes as he believes statements prepared using variable costing are more appropriate for making product decisions. In order to explain the benefits of variable costing to the other members of San Mateo's management team, Cimino plans to convert the company's income statement from absorption costing to variable costing. He has gathered the following information for this purpose, along with a copy of San Mateo's 2013 and 2014 comparative income statement.

San Mateo's actual manufacturing data for the two years are as follows:

The company's actual inventory balances were as follows:

For both years, all administrative expenses were fixed, while a portion of the selling expenses resulting from an 8 percent commission on net sales was variable. San Mateo reports any overor underapplied overhead as an adjustment to the cost of goods sold.

Required:

1. For the year ended December 31, 2014, prepare the revised income statement for San Mateo Optics, Inc., utilizing the variable-costing method. Be sure to include the contribution margin on the revised income statement.

2. Describe two advantages of using variable costing rather than absorption costing. ( CMA adapted )

San Mateo Optics, Inc., specializes in manufacturing lenses for large telescopes and cameras used in space exploration. As the specifications for the lenses are determined by the customer and vary considerably, the company uses a job-order costing system.

Manufacturing overhead is applied to jobs on the basis of direct labor hours, utilizing the absorption- or full-costing method. San Mateo's predetermined overhead rates for 2013 and 2014 were based on the following estimates.

Jim Cimino, San Mateo's controller, would like to use variable (direct) costing for internal reporting purposes as he believes statements prepared using variable costing are more appropriate for making product decisions. In order to explain the benefits of variable costing to the other members of San Mateo's management team, Cimino plans to convert the company's income statement from absorption costing to variable costing. He has gathered the following information for this purpose, along with a copy of San Mateo's 2013 and 2014 comparative income statement.

San Mateo's actual manufacturing data for the two years are as follows:

The company's actual inventory balances were as follows:

For both years, all administrative expenses were fixed, while a portion of the selling expenses resulting from an 8 percent commission on net sales was variable. San Mateo reports any overor underapplied overhead as an adjustment to the cost of goods sold.

Required:

1. For the year ended December 31, 2014, prepare the revised income statement for San Mateo Optics, Inc., utilizing the variable-costing method. Be sure to include the contribution margin on the revised income statement.

2. Describe two advantages of using variable costing rather than absorption costing. ( CMA adapted )

Question

Question

Absorption and Variable Costing with Over- and Underapplied Overhead

Flaherty, Inc., has just completed its first year of operations. The unit costs on a normal costing basis are as follows:

During the year, the company had the following activity:

Actual fixed overhead was $12,000 less than budgeted fixed overhead. Budgeted variable overhead was $5,000 less than the actual variable overhead. The company used an expected actual activity level of 12,000 direct labor hours to compute the predetermined overhead rates. Any overhead variances are closed to Cost of Goods Sold.

Required:

1. Compute the unit cost using (a) absorption costing and (b) variable costing.

2. Prepare an absorption-costing income statement.

3. Prepare a variable-costing income statement.

4. Reconcile the difference between the two income statements.

Flaherty, Inc., has just completed its first year of operations. The unit costs on a normal costing basis are as follows:

During the year, the company had the following activity:

Actual fixed overhead was $12,000 less than budgeted fixed overhead. Budgeted variable overhead was $5,000 less than the actual variable overhead. The company used an expected actual activity level of 12,000 direct labor hours to compute the predetermined overhead rates. Any overhead variances are closed to Cost of Goods Sold.

Required:

1. Compute the unit cost using (a) absorption costing and (b) variable costing.

2. Prepare an absorption-costing income statement.

3. Prepare a variable-costing income statement.

4. Reconcile the difference between the two income statements.

Question

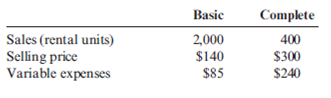

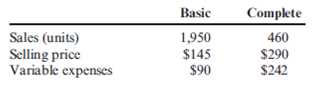

Contribution Margin Variance, Contribution Margin Volume Variance, Sales Mix Variance

Haysbert Company provides management services for apartments and rental units. In general, Haysbert packages its services into two groups: basic and complete. The basic package includes advertising vacant units, showing potential renters through them, and collecting monthly rent and remitting it to the owner. The complete package adds maintenance of units and bookkeeping to the basic package. Packages are priced on a per-rental unit basis. Actual results from last year are as follows:

Haysbert had budgeted the following amounts:

Required:

1. Calculate the contribution margin variance.

2. Calculate the contribution margin volume variance.

3. Calculate the sales mix variance.

Haysbert Company provides management services for apartments and rental units. In general, Haysbert packages its services into two groups: basic and complete. The basic package includes advertising vacant units, showing potential renters through them, and collecting monthly rent and remitting it to the owner. The complete package adds maintenance of units and bookkeeping to the basic package. Packages are priced on a per-rental unit basis. Actual results from last year are as follows:

Haysbert had budgeted the following amounts:

Required:

1. Calculate the contribution margin variance.

2. Calculate the contribution margin volume variance.

3. Calculate the sales mix variance.

Question

Question

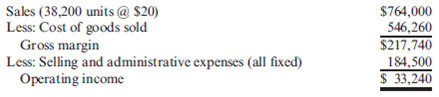

Variable Costing, Absorption Costing

During its first year of operations, Snobegon, Inc. (located in Lake Snobegon, Minnesota), produced 40,000 plastic snow scoops. Snow scoops are oversized shovel-type scoops that are used to push snow away. Unit sales were 38,200 scoops. Fixed overhead was applied at $0.75 per unit produced. Fixed overhead was underapplied by $2,900. This fixed overhead variance was closed to Cost of Goods Sold. There was no variable overhead variance. The results of the year's operations are as follows (on an absorption-costing basis):

Required:

1. Calculate the cost of the firm's ending inventory under absorption costing. What is the cost of the ending inventory under variable costing? (Round unit costs to five significant digits.)

2. Prepare a variable-costing income statement. Reconcile the difference between the two income figures.

During its first year of operations, Snobegon, Inc. (located in Lake Snobegon, Minnesota), produced 40,000 plastic snow scoops. Snow scoops are oversized shovel-type scoops that are used to push snow away. Unit sales were 38,200 scoops. Fixed overhead was applied at $0.75 per unit produced. Fixed overhead was underapplied by $2,900. This fixed overhead variance was closed to Cost of Goods Sold. There was no variable overhead variance. The results of the year's operations are as follows (on an absorption-costing basis):

Required:

1. Calculate the cost of the firm's ending inventory under absorption costing. What is the cost of the ending inventory under variable costing? (Round unit costs to five significant digits.)

2. Prepare a variable-costing income statement. Reconcile the difference between the two income figures.

Question

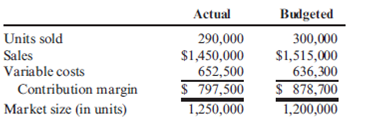

Contribution Margin Variance, Contribution Margin Volume Variance, Market Share Variance, Market Size Variance

Sulert, Inc., produces and sells gel-filled ice packs. Sulert's performance report for April follows:

Required:

1. Calculate the contribution margin variance and the contribution margin volume variance.

2. Calculate the market share variance and the market size variance. ( CMA adapted )

Sulert, Inc., produces and sells gel-filled ice packs. Sulert's performance report for April follows:

Required:

1. Calculate the contribution margin variance and the contribution margin volume variance.

2. Calculate the market share variance and the market size variance. ( CMA adapted )

Question

Question

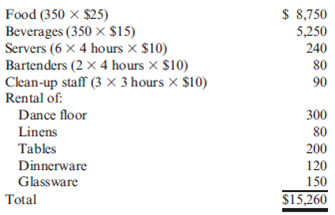

Cost-Based Pricing, Target Pricing

Carina Franks operates a catering company in Austin, Texas. Carina provides food and servers for parties. She also rents tables, chairs, dinnerware, glassware, and linens. Estefan and Maria Montero have contacted Carina about plans for their daughter's Quinceanera (a festive party thrown by Hispanic parents to celebrate their daughters' fifteenth birthdays). The Monteros would like a catered affair on the lawn of a rural church. They have requested an open bar, a sit-down dinner for 350 people, a large tent, and a dance floor. Of course, they expect Carina to supply serving staff, tables with linens, dinnerware, and glassware. They will handle the flowers, the decorations, and hiring the band on their own. Carina put together this bid:

Required:

1. Explain where costs for Carina's services and profit are calculated in the preceding bid.

2. Suppose that the Monteros blanch when they see the preceding bid. One of them suggests that they had hoped to spend no more than $10,000 or so on the party. How could Carina work with the Monteros to achieve a target cost of that amount?

3. Estefan Montero protests the cost of dance floor rental. He said, "I've seen those for rent at U-Rent-It for $75." How would you respond to this remark if you were Carina? (Hint: You want this job and so telling him, "Go ahead and do it yourself, Cheapskate!" is not an option.)

Carina Franks operates a catering company in Austin, Texas. Carina provides food and servers for parties. She also rents tables, chairs, dinnerware, glassware, and linens. Estefan and Maria Montero have contacted Carina about plans for their daughter's Quinceanera (a festive party thrown by Hispanic parents to celebrate their daughters' fifteenth birthdays). The Monteros would like a catered affair on the lawn of a rural church. They have requested an open bar, a sit-down dinner for 350 people, a large tent, and a dance floor. Of course, they expect Carina to supply serving staff, tables with linens, dinnerware, and glassware. They will handle the flowers, the decorations, and hiring the band on their own. Carina put together this bid:

Required:

1. Explain where costs for Carina's services and profit are calculated in the preceding bid.

2. Suppose that the Monteros blanch when they see the preceding bid. One of them suggests that they had hoped to spend no more than $10,000 or so on the party. How could Carina work with the Monteros to achieve a target cost of that amount?

3. Estefan Montero protests the cost of dance floor rental. He said, "I've seen those for rent at U-Rent-It for $75." How would you respond to this remark if you were Carina? (Hint: You want this job and so telling him, "Go ahead and do it yourself, Cheapskate!" is not an option.)

Question

Contribution Margin Variance, Contribution Margin Volume Variance, Sales Mix Variance

Gasconia Company produces three models of a product. Actual results from last year are as follows:

Gasconia had budgeted the following amounts:

Required:

1. Calculate the contribution margin variance.

2. Calculate the contribution margin volume variance.

3. Calculate the sales mix variance.

Gasconia Company produces three models of a product. Actual results from last year are as follows:

Gasconia had budgeted the following amounts:

Required:

1. Calculate the contribution margin variance.

2. Calculate the contribution margin volume variance.

3. Calculate the sales mix variance.

Question

Markup on Cost, Job Pricing

Ventana Window and Wall Treatments Company provides draperies, shades, and various window treatments. Ventana works with the customer to design the appropriate window treatment, places the order, and installs the finished product. Direct materials and direct labor costs are easy to trace to the jobs. Ventana's income statement for last year is as follows:

Ventana wants to find a markup on cost of goods sold that will allow them to earn about the same amount of profit on each job as was earned last year.

Required:

1. What is the markup on cost of goods sold (COGS) that will maintain the same profit as last year? (Round the percentage to two significant digits.)

2. A customer orders draperies and shades for a remodeling job. The job will have the following costs:

What is the price that Ventana will quote given the markup percentage calculated in Requirement 1? (Round the price to the nearest dollar.)

3. What if Ventana wants to calculate a markup on direct materials cost, since it is the largest cost of doing business? What is the markup on direct materials cost that will maintain the same profit as last year? (Round the percentage to two significant digits.) What is the bid price Ventana will use for the job given in Requirement 2 if the markup percentage is calculated on the basis of direct materials cost? (Round to the nearest dollar.)

Ventana Window and Wall Treatments Company provides draperies, shades, and various window treatments. Ventana works with the customer to design the appropriate window treatment, places the order, and installs the finished product. Direct materials and direct labor costs are easy to trace to the jobs. Ventana's income statement for last year is as follows:

Ventana wants to find a markup on cost of goods sold that will allow them to earn about the same amount of profit on each job as was earned last year.

Required:

1. What is the markup on cost of goods sold (COGS) that will maintain the same profit as last year? (Round the percentage to two significant digits.)

2. A customer orders draperies and shades for a remodeling job. The job will have the following costs:

What is the price that Ventana will quote given the markup percentage calculated in Requirement 1? (Round the price to the nearest dollar.)

3. What if Ventana wants to calculate a markup on direct materials cost, since it is the largest cost of doing business? What is the markup on direct materials cost that will maintain the same profit as last year? (Round the percentage to two significant digits.) What is the bid price Ventana will use for the job given in Requirement 2 if the markup percentage is calculated on the basis of direct materials cost? (Round to the nearest dollar.)

Question

Market Share Variance, Market Size Variance

Budgeted unit sales for the entire countertop oven industry were 2,500,000 (of all model types), and actual unit sales for the industry were 2,550,000. Recall from Cornerstone Exercise 18.6 that Iliff, Inc., provided the following information:

Required:

1. Calculate the market share variance (take percentages out to four significant digits).

2. Calculate the market size variance.

3. What if Iliff actually sold a total of 41,000 units (in total of the two models)? How would that affect the market share variance? The market size variance?

Budgeted unit sales for the entire countertop oven industry were 2,500,000 (of all model types), and actual unit sales for the industry were 2,550,000. Recall from Cornerstone Exercise 18.6 that Iliff, Inc., provided the following information:

Required:

1. Calculate the market share variance (take percentages out to four significant digits).

2. Calculate the market size variance.

3. What if Iliff actually sold a total of 41,000 units (in total of the two models)? How would that affect the market share variance? The market size variance?

Question

Cost-Based Pricing

Otero Fibers, Inc., specializes in the manufacture of synthetic fibers that the company uses in many products such as blankets, coats, and uniforms for police and firefighters. Otero has been in business since 1985 and has been profitable every year since 1993. The company uses a standard cost system and applies overhead on the basis of direct labor hours.

Otero has recently received a request to bid on the manufacture of 800,000 blankets scheduled for delivery to several military bases. The bid must be stated at full cost per unit plus a return on full cost of no more than 10 percent after income taxes. Full cost has been defined as including all variable costs of manufacturing the product, a reasonable amount of fixed overhead, and reasonable incremental administrative costs associated with the manufacture and sale of the product. The contractor has indicated that bids in excess of $30 per blanket are not likely to be considered.

In order to prepare the bid for the 800,000 blankets, Andrea Lightner, cost accountant, has gathered the following information about the costs associated with the production of the blankets.

* Direct machine costs consist of items such as special lubricants, replacement of needles used in stitching, and maintenance costs. These costs are not included in the normal overhead rates.

** Otero recently developed a new blanket fiber at a cost of $750,000. In an effort to recover this cost, Otero has instituted a policy of adding a $0.50 fee to the cost of each blanket using the new fiber. To date, the company has recovered $125,000. Lightner knows that this fee does not fit within the definition of full cost, as it is not a cost of manufacturing the product.

Required:

1. Calculate the minimum price per blanket that Otero Fibers could bid without reducing the company's operating income.

2. Using the full-cost criteria and the maximum allowable return specified, calculate Otero Fibers' bid price per blanket.

3. Without prejudice to your answer to Requirement 2, assume that the price per blanket that Otero Fibers calculated using the cost-plus criteria specified is greater than the maximum bid of $30 per blanket allowed. Discuss the factors that Otero Fibers should consider before deciding whether or not to submit a bid at the maximum acceptable price of $30 per blanket. (CMA adapted)

Otero Fibers, Inc., specializes in the manufacture of synthetic fibers that the company uses in many products such as blankets, coats, and uniforms for police and firefighters. Otero has been in business since 1985 and has been profitable every year since 1993. The company uses a standard cost system and applies overhead on the basis of direct labor hours.

Otero has recently received a request to bid on the manufacture of 800,000 blankets scheduled for delivery to several military bases. The bid must be stated at full cost per unit plus a return on full cost of no more than 10 percent after income taxes. Full cost has been defined as including all variable costs of manufacturing the product, a reasonable amount of fixed overhead, and reasonable incremental administrative costs associated with the manufacture and sale of the product. The contractor has indicated that bids in excess of $30 per blanket are not likely to be considered.

In order to prepare the bid for the 800,000 blankets, Andrea Lightner, cost accountant, has gathered the following information about the costs associated with the production of the blankets.

* Direct machine costs consist of items such as special lubricants, replacement of needles used in stitching, and maintenance costs. These costs are not included in the normal overhead rates.

** Otero recently developed a new blanket fiber at a cost of $750,000. In an effort to recover this cost, Otero has instituted a policy of adding a $0.50 fee to the cost of each blanket using the new fiber. To date, the company has recovered $125,000. Lightner knows that this fee does not fit within the definition of full cost, as it is not a cost of manufacturing the product.

Required:

1. Calculate the minimum price per blanket that Otero Fibers could bid without reducing the company's operating income.

2. Using the full-cost criteria and the maximum allowable return specified, calculate Otero Fibers' bid price per blanket.

3. Without prejudice to your answer to Requirement 2, assume that the price per blanket that Otero Fibers calculated using the cost-plus criteria specified is greater than the maximum bid of $30 per blanket allowed. Discuss the factors that Otero Fibers should consider before deciding whether or not to submit a bid at the maximum acceptable price of $30 per blanket. (CMA adapted)

Question

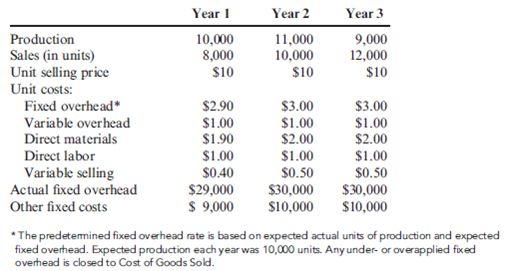

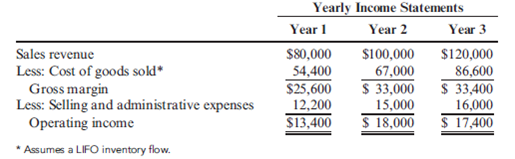

Impact of Inventory Changes on Absorption-Costing Income: Divisional Profitability

Dana Baird was manager of a new Medical Supplies Division. She had just finished her second year and had been visiting with the company's vice president of operations. In the first year, the operating income for the division had shown a substantial increase over the prior year. Her second year saw an even greater increase. The vice president was extremely pleased and promised Dana a $5,000 bonus if the division showed a similar increase in profits for the upcoming year. Dana was elated. She was completely confident that the goal could be met. Sales contracts were already well ahead of last year's performance, and she knew that there would be no increases in costs.

At the end of the third year, Dana received the following data regarding operations for the first three years:

Upon examining the operating data, Dana was pleased. Sales had increased by 20 percent over the previous year, and costs had remained stable. However, when she saw the yearly income statements, she was dismayed and perplexed. Instead of seeing a significant increase in income for the third year, she saw a small decrease. Surely, the Accounting Department had made an error.

Required:

1. Explain to Dana why she lost her $5,000 bonus.

2. Prepare variable-costing income statements for each of the three years. Reconcile the differences between the absorption-costing and variable-costing incomes.

3. If you were the vice president of Dana's company, which income statement (variable-costing or absorption-costing) would you prefer to use for evaluating Dana's performance? Why?

Dana Baird was manager of a new Medical Supplies Division. She had just finished her second year and had been visiting with the company's vice president of operations. In the first year, the operating income for the division had shown a substantial increase over the prior year. Her second year saw an even greater increase. The vice president was extremely pleased and promised Dana a $5,000 bonus if the division showed a similar increase in profits for the upcoming year. Dana was elated. She was completely confident that the goal could be met. Sales contracts were already well ahead of last year's performance, and she knew that there would be no increases in costs.

At the end of the third year, Dana received the following data regarding operations for the first three years:

Upon examining the operating data, Dana was pleased. Sales had increased by 20 percent over the previous year, and costs had remained stable. However, when she saw the yearly income statements, she was dismayed and perplexed. Instead of seeing a significant increase in income for the third year, she saw a small decrease. Surely, the Accounting Department had made an error.

Required:

1. Explain to Dana why she lost her $5,000 bonus.

2. Prepare variable-costing income statements for each of the three years. Reconcile the differences between the absorption-costing and variable-costing incomes.

3. If you were the vice president of Dana's company, which income statement (variable-costing or absorption-costing) would you prefer to use for evaluating Dana's performance? Why?

Question

Question

Question

Life-Cycle Pricing, Sales Price and Sales Volume Variances

Data for Torleson Company are as follows:

Required:

1. Calculate the sales price variance.

2. Calculate the sales volume variance.

3. Suppose that the product is in the introductory stage of the product life cycle. What information do these two variances provide to Torleson's managers?

Data for Torleson Company are as follows:

Required:

1. Calculate the sales price variance.

2. Calculate the sales volume variance.

3. Suppose that the product is in the introductory stage of the product life cycle. What information do these two variances provide to Torleson's managers?

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/57

Play

Full screen (f)

Deck 18: Pricing and Profitability Analysis

1

Costs of Different Customer Classes

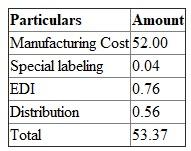

Kaune Food Products Company manufactures canned mixed nuts with an average manufacturing cost of $52 per case (a case contains 24 cans of nuts). Kaune sold 150,000 cases last year to the following three classes of customer:

The supermarkets require special labeling on each can costing $0.04 per can. They order through electronic data interchange (EDI), which costs Kaune about $61,000 annually in operating expenses and depreciation. Kaune delivers the nuts to the stores and stocks them on the shelves. This distribution costs $45,000 per year.

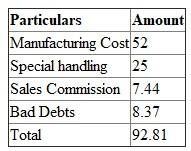

The small grocers order in smaller lots that require special picking and packing in the factory; the special handling adds $25 to the cost of each case sold. Sales commissions to the independent jobbers who sell Kaune products to the grocers average 8 percent of sales. Bad debts expense amounts to 9 percent of sales.

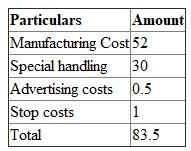

Convenience stores also require special handling that costs $30 per case. In addition, Kaune is required to co-pay advertising costs with the convenience stores at a cost of $15,000 per year. Frequent stops are made to each convenience store by Kaune delivery trucks at a cost of $30,000 per year.

Required:

1. Calculate the total cost per case for each of the three customer classes. (Round unit costs to four significant digits.)

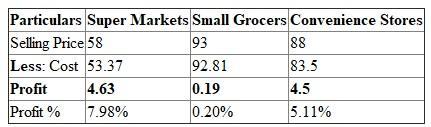

2. Using the costs from Requirement 1, calculate the profit per case per customer class. Does the cost analysis support the charging of different prices? Why or why not?

3. What if Kaune charged the average price per case to all customer classes? How would that affect the profit percentages?

Kaune Food Products Company manufactures canned mixed nuts with an average manufacturing cost of $52 per case (a case contains 24 cans of nuts). Kaune sold 150,000 cases last year to the following three classes of customer:

The supermarkets require special labeling on each can costing $0.04 per can. They order through electronic data interchange (EDI), which costs Kaune about $61,000 annually in operating expenses and depreciation. Kaune delivers the nuts to the stores and stocks them on the shelves. This distribution costs $45,000 per year.

The small grocers order in smaller lots that require special picking and packing in the factory; the special handling adds $25 to the cost of each case sold. Sales commissions to the independent jobbers who sell Kaune products to the grocers average 8 percent of sales. Bad debts expense amounts to 9 percent of sales.

Convenience stores also require special handling that costs $30 per case. In addition, Kaune is required to co-pay advertising costs with the convenience stores at a cost of $15,000 per year. Frequent stops are made to each convenience store by Kaune delivery trucks at a cost of $30,000 per year.

Required:

1. Calculate the total cost per case for each of the three customer classes. (Round unit costs to four significant digits.)

2. Using the costs from Requirement 1, calculate the profit per case per customer class. Does the cost analysis support the charging of different prices? Why or why not?

3. What if Kaune charged the average price per case to all customer classes? How would that affect the profit percentages?

1. The total cost per case for each of the 3 customers shall be calculated in following manner:

Super Markets: The cost shall be calculated in following manner:

Explanations:

Explanations:

a. Price per case is $ 52

b. Labeling cost is.04

c. EDI cost is calculated in following manner:

The EDI cost is

The EDI cost is

d. The distribution costs are calculated in following manner:

d. The distribution costs are calculated in following manner:

Hence, the distribution cost is

Hence, the distribution cost is

Small Grocers: The calculation shall be made in following manner:

Small Grocers: The calculation shall be made in following manner:

Explanations:

Explanations:

a. Price Per case is $ 52

b. Special handling cost is $ 25

c. Sales Commission is calculated in following manner:

d. The Bad debts are calculated in following manner:

d. The Bad debts are calculated in following manner:

Convenience Stores: The Calculation shall be made in following manner:

Convenience Stores: The Calculation shall be made in following manner:

Explanations:

Explanations:

a. Price Per case is $ 52

b. Special handling cost is $ 30

c. Sales Commission is calculated in following manner:

d.

d.

The Stop Costs are calculated in following manner:

2. The profit per case shall be calculated as a difference between sales price and cost price hence it shall be calculated in following manner:

2. The profit per case shall be calculated as a difference between sales price and cost price hence it shall be calculated in following manner:

Profit % for supermarkets:

Profit % for supermarkets:

Profit % for small grocers:

Profit % for small grocers:

Profit % for convenience stores:

Profit % for convenience stores:

3. The Average selling price is $ 79.67 and if average price is charged from each customer then in that case the profits in super markets will increase significantly while the profits in small grocers and convenience stores will fall down and henceforth the profit percentage will fall for small grocery and convenience stores.

3. The Average selling price is $ 79.67 and if average price is charged from each customer then in that case the profits in super markets will increase significantly while the profits in small grocers and convenience stores will fall down and henceforth the profit percentage will fall for small grocery and convenience stores.

Super Markets: The cost shall be calculated in following manner:

Explanations:a. Price per case is $ 52

b. Labeling cost is.04

c. EDI cost is calculated in following manner:

The EDI cost is d. The distribution costs are calculated in following manner: Hence, the distribution cost is Small Grocers: The calculation shall be made in following manner: Explanations:a. Price Per case is $ 52

b. Special handling cost is $ 25

c. Sales Commission is calculated in following manner:

d. The Bad debts are calculated in following manner: Convenience Stores: The Calculation shall be made in following manner: Explanations:a. Price Per case is $ 52

b. Special handling cost is $ 30

c. Sales Commission is calculated in following manner:

d. The Stop Costs are calculated in following manner:

2. The profit per case shall be calculated as a difference between sales price and cost price hence it shall be calculated in following manner: Profit % for supermarkets: Profit % for small grocers: Profit % for convenience stores: 3. The Average selling price is $ 79.67 and if average price is charged from each customer then in that case the profits in super markets will increase significantly while the profits in small grocers and convenience stores will fall down and henceforth the profit percentage will fall for small grocery and convenience stores. 2

Suppose that Alpha Company has four product lines, three of which are profitable and one (let's call it "Loser") of which generally incurs a loss. Give several reasons why Alpha Company may choose not to drop the Loser product line.

Identify some reasons for why A Company may not choose to drop the loser product line:

Following are the possible reasons:

• This loser product line is very essential to run remaining three product lines. It means that these products are using as materials in remaining product lines.

• Cost classification may not don perfectly between these four product lines.

• Company has huge fixed cost, if this product line is dropped remaining product lines will suffer due to high fixed cost.

Following are the possible reasons:

• This loser product line is very essential to run remaining three product lines. It means that these products are using as materials in remaining product lines.

• Cost classification may not don perfectly between these four product lines.

• Company has huge fixed cost, if this product line is dropped remaining product lines will suffer due to high fixed cost.

3

Pricing Strategy, Sales Variances

Eastman, Inc., manufactures and sells three products: R, S, and T. In January, Eastman, Inc., budgeted sales of the following.

At the end of the year, actual sales revenue for Product R and Product S was $3,075,000 and $3,254,000, respectively. The actual price charged for Product R was $25 and for Product S was $20. Only $10 was charged for Product T to encourage more consumers to buy it, and actual sales revenue equaled $540,000 for this product.

Required:

1. Calculate the sales price and sales volume variances for each of the three products based on the original budget.

2. Suppose that Product T is a new product just introduced during the year. What pricing strategy is Eastman, Inc., following for this product?

Eastman, Inc., manufactures and sells three products: R, S, and T. In January, Eastman, Inc., budgeted sales of the following.

At the end of the year, actual sales revenue for Product R and Product S was $3,075,000 and $3,254,000, respectively. The actual price charged for Product R was $25 and for Product S was $20. Only $10 was charged for Product T to encourage more consumers to buy it, and actual sales revenue equaled $540,000 for this product.

Required:

1. Calculate the sales price and sales volume variances for each of the three products based on the original budget.

2. Suppose that Product T is a new product just introduced during the year. What pricing strategy is Eastman, Inc., following for this product?

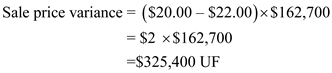

The impact of actual and budgeted units sold on the revenue of the company refers to the sales revenue. Sales price variance reflects the impact of difference of budgeted sales and actual sales on the revenue of the company.

1.Sales price variance can be calculated using following formulae:

Product R

Product R

Hence, the Sales Price Variance for the Product R is

Hence, the Sales Price Variance for the Product R is

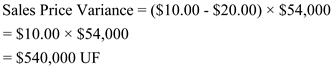

Product S

Product S

Hence, the Sales Price Variance for the Product S is

Hence, the Sales Price Variance for the Product S is

Product T

Product T

Hence, the Sales Price Variance for the Product T is

Hence, the Sales Price Variance for the Product T is

.

.

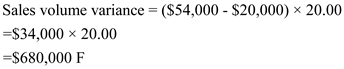

Sales volume variance can be calculated using following formulae:

Product R

Hence, the sales volume variance for the Product R is

Hence, the sales volume variance for the Product R is

Product S

Product S

Hence, the Sales Volume Variance for the Product S is

Hence, the Sales Volume Variance for the Product S is

Product T

Product T

Hence, the Sales Volume Variance for the Product T is

Hence, the Sales Volume Variance for the Product T is

2.Introductory stage of a product in its life cycle means, the product is recently introduced in the market. The price of the product will be kept low as compared to the budgeted. Also the quantity sold will be higher since the product is new to the customer.

2.Introductory stage of a product in its life cycle means, the product is recently introduced in the market. The price of the product will be kept low as compared to the budgeted. Also the quantity sold will be higher since the product is new to the customer.

The variances like sales price variance provide the information that due to low price the revenue generation will be negative. However, if the quantity sales are more, the sales volume variance proves that the profitability would be favorable.

1.Sales price variance can be calculated using following formulae:

Product R Hence, the Sales Price Variance for the Product R is Product S Hence, the Sales Price Variance for the Product S is Product T Hence, the Sales Price Variance for the Product T is .Sales volume variance can be calculated using following formulae:

Product R