Deck 14: Quality and Environmental Cost Management

Full screen (f)

Question

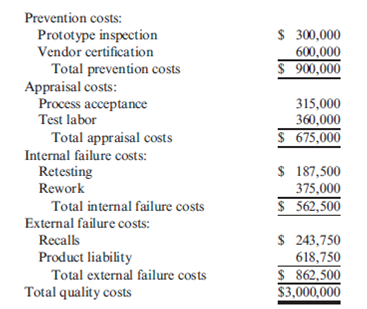

Quality Cost Report

Evans Company had total sales of $3,000,000 for fiscal 2013. The costs of quality-related activities are given below.

Required:

1. Prepare a quality cost report, classifying costs by category and expressing each category as a percentage of sales. What message does the cost report provide?

2. Prepare a bar graph and pie chart that illustrate each category's contribution to total quality costs. Comment on the significance of the distribution.

3. What if , five years from now, quality costs are 7.5 percent of sales, with control costs being 65 percent of the total quality costs? What would your conclusion be?

Evans Company had total sales of $3,000,000 for fiscal 2013. The costs of quality-related activities are given below.

Required:

1. Prepare a quality cost report, classifying costs by category and expressing each category as a percentage of sales. What message does the cost report provide?

2. Prepare a bar graph and pie chart that illustrate each category's contribution to total quality costs. Comment on the significance of the distribution.

3. What if , five years from now, quality costs are 7.5 percent of sales, with control costs being 65 percent of the total quality costs? What would your conclusion be?

Question

Question

Question

Question

Environmental Financial Reporting, Ecoefficiency, Improving Environmental Performance

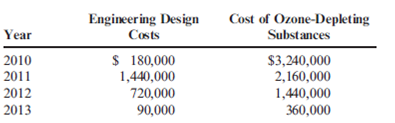

Refer to Problem 14.41. In the environmental benefits section of the report, three types of benefits are listed: income, savings, and cost avoidance. Now, consider the following data for selected items for a four-year period:

The engineering design costs were incurred to redesign the production processes and products. Redesign of the product allowed the substitution of a material that produced less ozonedepleting substances. Modifications in the design of the processes also accomplished the same objective. Because of the improvements, the company was able to reduce the demand for pollution control equipment (with its attendant depreciation and operating costs) and avoid fines and litigation costs. All of the savings generated in a given year represent costs avoided for future years. The engineering costs are investments in design projects. Once the results of the project are realized, design costs can be reduced to lower levels. However, since some ongoing design activity is required for maintaining the system and improving it as needed, the environmental engineering cost will not be reduced lower than the $90,000 reported in 2013.

Required:

1. Prepare a partial environmental financial statement, divided into benefit and cost sections for 2011, 2012, and 2013.

2. Evaluate and explain the outcomes. Does this result support or challenge ecoefficiency? Explain.

Refer to Problem 14.41. In the environmental benefits section of the report, three types of benefits are listed: income, savings, and cost avoidance. Now, consider the following data for selected items for a four-year period:

The engineering design costs were incurred to redesign the production processes and products. Redesign of the product allowed the substitution of a material that produced less ozonedepleting substances. Modifications in the design of the processes also accomplished the same objective. Because of the improvements, the company was able to reduce the demand for pollution control equipment (with its attendant depreciation and operating costs) and avoid fines and litigation costs. All of the savings generated in a given year represent costs avoided for future years. The engineering costs are investments in design projects. Once the results of the project are realized, design costs can be reduced to lower levels. However, since some ongoing design activity is required for maintaining the system and improving it as needed, the environmental engineering cost will not be reduced lower than the $90,000 reported in 2013.

Required:

1. Prepare a partial environmental financial statement, divided into benefit and cost sections for 2011, 2012, and 2013.

2. Evaluate and explain the outcomes. Does this result support or challenge ecoefficiency? Explain.

Question

Question

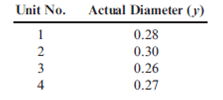

Taguchi Loss Function

Stahman, Inc., estimates its hidden external failure costs using the Taguchi loss function. Stahlman produces plastic sheets that vary in thickness and grade. For one of its large-volume products, it was determined that k = $30,000 and T = 0.28 inches in diameter. A sample of four units produced the following values:

Required:

1. Calculate the average loss per unit.

2. Assuming that 100,000 units were produced, what is the total hidden cost?

3. Assume that the multiplier for Stahman's hidden external failure costs is six. What are the measured external costs? Explain the difference between measured costs and hidden costs.

Stahman, Inc., estimates its hidden external failure costs using the Taguchi loss function. Stahlman produces plastic sheets that vary in thickness and grade. For one of its large-volume products, it was determined that k = $30,000 and T = 0.28 inches in diameter. A sample of four units produced the following values:

Required:

1. Calculate the average loss per unit.

2. Assuming that 100,000 units were produced, what is the total hidden cost?

3. Assume that the multiplier for Stahman's hidden external failure costs is six. What are the measured external costs? Explain the difference between measured costs and hidden costs.

Question

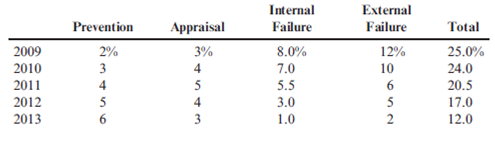

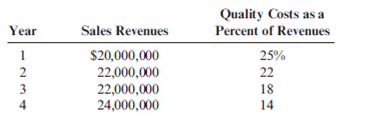

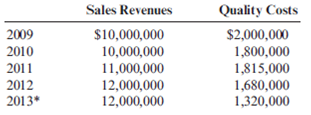

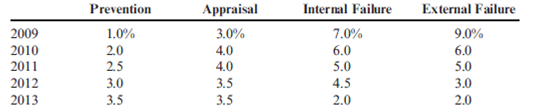

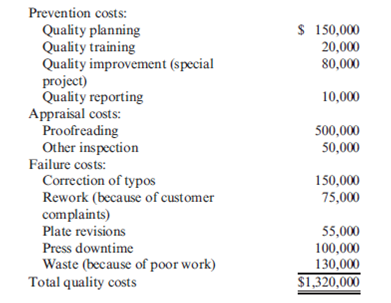

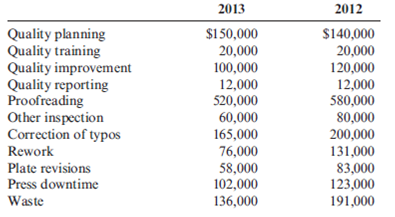

Multiple-Year Trend Reports

The controller of Willson Company has computed quality costs as a percentage of sales for the past five years (2009 was the first year the company implemented a quality improvement program). This information is as follows:

Required:

1. Prepare a trend graph for total quality costs. Comment on what the graph has to say about the success of the quality improvement program.

2. Prepare a graph that shows the trend for each quality cost category. What does the graph have to say about the success of the quality improvement program? Does this graph supply more insight than the total cost trend graph does?

3. Prepare a graph that compares the trend in relative quality costs. What does this graph tell you?

The controller of Willson Company has computed quality costs as a percentage of sales for the past five years (2009 was the first year the company implemented a quality improvement program). This information is as follows:

Required:

1. Prepare a trend graph for total quality costs. Comment on what the graph has to say about the success of the quality improvement program.

2. Prepare a graph that shows the trend for each quality cost category. What does the graph have to say about the success of the quality improvement program? Does this graph supply more insight than the total cost trend graph does?

3. Prepare a graph that compares the trend in relative quality costs. What does this graph tell you?

Question

Question

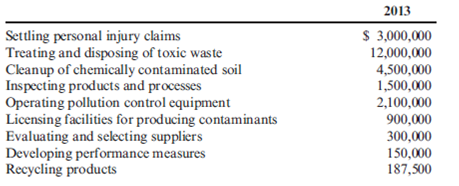

Environmental Financial Report

The following environmental cost reports for 2011, 2012, and 2013 (year end December 31) are for the Communications Products Division of Kartel, a telecommunications company. In 2011, Kartel committed itself to a continuous environmental improvement program, which was implemented throughout the company.

At the beginning of 2013, Kartel began a new program of recycling nonhazardous scrap. The effort produced recycling income totaling $25,000. The marketing vice president and the environmental manager estimated that sales revenue had increased by $200,000 per year since 2011 because of an improved public image relative to environmental performance. The company's Finance Department also estimated that Kartel saved $80,000 in 2013 because of reduced finance and insurance costs, all attributable to improved environmental performance. All reductions in environmental costs from 2011 to 2013 are attributable to improvement efforts. Furthermore, any reductions represent ongoing savings.

Required:

1. Prepare an environmental financial statement for 2013 (for the Products Division). In the cost section, classify environmental costs by category (prevention, detection, etc.).

2. Evaluate the changes in environmental performance.

The following environmental cost reports for 2011, 2012, and 2013 (year end December 31) are for the Communications Products Division of Kartel, a telecommunications company. In 2011, Kartel committed itself to a continuous environmental improvement program, which was implemented throughout the company.

At the beginning of 2013, Kartel began a new program of recycling nonhazardous scrap. The effort produced recycling income totaling $25,000. The marketing vice president and the environmental manager estimated that sales revenue had increased by $200,000 per year since 2011 because of an improved public image relative to environmental performance. The company's Finance Department also estimated that Kartel saved $80,000 in 2013 because of reduced finance and insurance costs, all attributable to improved environmental performance. All reductions in environmental costs from 2011 to 2013 are attributable to improvement efforts. Furthermore, any reductions represent ongoing savings.

Required:

1. Prepare an environmental financial statement for 2013 (for the Products Division). In the cost section, classify environmental costs by category (prevention, detection, etc.).

2. Evaluate the changes in environmental performance.

Question

Interim Quality Performance Report

Davis, Inc., had the following quality costs for the years ended December 31, 2012 and 2013:

At the end of 2012, management decided to increase its investment in control costs by 50 percent for each category's items with the expectation that failure costs would decrease by 20 percent for each item of the failure categories. Sales were $12,000,000 for both 2012 and 2013.

Required:

1. Calculate the budgeted costs for 2013, and prepare an interim quality performance report.

2. Comment on the significance of the report. How much progress has Davis made?

3. What if sales were $12,000,000 for 2012 and $15,000,000 for 2013? What adjustment to budgeted rework costs would be made? Budgeted quality audits? Assuming the actual costs for 2013 do not change, what does this adjustment say about Davis's performance?

Davis, Inc., had the following quality costs for the years ended December 31, 2012 and 2013:

At the end of 2012, management decided to increase its investment in control costs by 50 percent for each category's items with the expectation that failure costs would decrease by 20 percent for each item of the failure categories. Sales were $12,000,000 for both 2012 and 2013.

Required:

1. Calculate the budgeted costs for 2013, and prepare an interim quality performance report.

2. Comment on the significance of the report. How much progress has Davis made?

3. What if sales were $12,000,000 for 2012 and $15,000,000 for 2013? What adjustment to budgeted rework costs would be made? Budgeted quality audits? Assuming the actual costs for 2013 do not change, what does this adjustment say about Davis's performance?

Question

Question

Question

Question

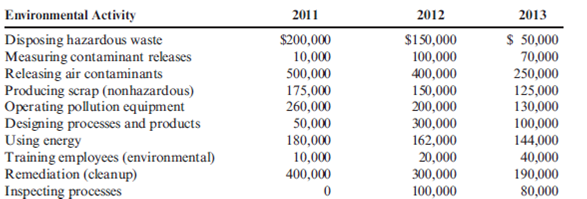

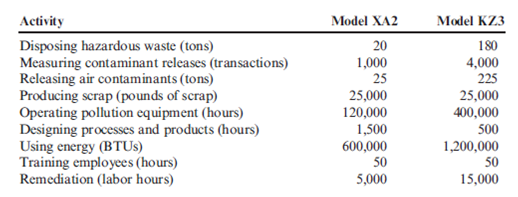

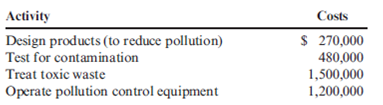

Assignment of Environmental Costs

Refer to Problem 14.43. In 2011, Jack Carter, president of Kartel, requested that environmental costs be assigned to the two major products produced by the company. He felt that knowledge of the environmental product costs would help guide the design decisions that would be necessary to improve environmental performance. The products represent two different models of a cellular phone (Model XA2 and Model KZ3). The models use different processes and materials. To assign the costs, the following data were gathered for 2011:

During 2011, Kartel's division produced 200,000 units of Model XA2 and 300,000 units of Model KZ3.

Required:

1. Using the activity data, calculate the environmental cost per unit for each model. How will this information be useful?

2. Upon examining the cost data produced in Requirement 1, an environmental engineer made the following suggestions: (1) substitute a new plastic for a material that appeared to be the source of much of the hazardous waste (the new material actually cost less than the contaminating material it would replace), and (2) redesign the processes to reduce the amount of air contaminants produced.

As a result of the first suggestion, by 2013, the amount of hazardous waste produced had diminished to 50 tons, 10 tons for Model XA2 and 40 tons for Model KZ3. The second suggestion reduced the contaminants released by 50 percent by 2013 (15 tons for Model XA2 and 110 tons for Model KZ3). The need for pollution equipment also diminished, and the hours required for operating this equipment for Model XA2 and Model KZ3 were reduced to 60,000 and 200,000, respectively. Calculate the unit cost reductions for the two models associated with the actions and outcomes described (assume the same production as in 2011). Do you think the efforts to reduce the environmental cost per unit were economically justified? Explain.

Refer to Problem 14.43. In 2011, Jack Carter, president of Kartel, requested that environmental costs be assigned to the two major products produced by the company. He felt that knowledge of the environmental product costs would help guide the design decisions that would be necessary to improve environmental performance. The products represent two different models of a cellular phone (Model XA2 and Model KZ3). The models use different processes and materials. To assign the costs, the following data were gathered for 2011:

During 2011, Kartel's division produced 200,000 units of Model XA2 and 300,000 units of Model KZ3.

Required:

1. Using the activity data, calculate the environmental cost per unit for each model. How will this information be useful?

2. Upon examining the cost data produced in Requirement 1, an environmental engineer made the following suggestions: (1) substitute a new plastic for a material that appeared to be the source of much of the hazardous waste (the new material actually cost less than the contaminating material it would replace), and (2) redesign the processes to reduce the amount of air contaminants produced.

As a result of the first suggestion, by 2013, the amount of hazardous waste produced had diminished to 50 tons, 10 tons for Model XA2 and 40 tons for Model KZ3. The second suggestion reduced the contaminants released by 50 percent by 2013 (15 tons for Model XA2 and 110 tons for Model KZ3). The need for pollution equipment also diminished, and the hours required for operating this equipment for Model XA2 and Model KZ3 were reduced to 60,000 and 200,000, respectively. Calculate the unit cost reductions for the two models associated with the actions and outcomes described (assume the same production as in 2011). Do you think the efforts to reduce the environmental cost per unit were economically justified? Explain.

Question

Question

Question

Question

Two products, Product A and Product B, are associated with the following environmental activities and associated data:

Which of the two products has the greatest environmental impact?

A) Product A because its total environmental cost is $400,000.

B) Product A because it causes more waste and pollution control than Product B.

C) Product B because its total environmental cost is $400,000.

D) Product B because its environmental cost per unit is five times more than Product A's unit environmental cost.

Which of the two products has the greatest environmental impact?

A) Product A because its total environmental cost is $400,000.

B) Product A because it causes more waste and pollution control than Product B.

C) Product B because its total environmental cost is $400,000.

D) Product B because its environmental cost per unit is five times more than Product A's unit environmental cost.

Question

Quality Trend Report Objective

Ross Company implemented a quality improvement program and tracked the following for the five years:

By cost category as a percentage of sales for the same period of time:

Required:

1. Prepare a bar graph that reveals the trend in quality cost as a percentage of sales (time on the horizontal axis and percentages on the vertical). Comment on the message of the graph.

2. Prepare a bar graph for each cost category as a percentage of sales. What does this graph tell you?

3. What if management would like to have the trend in relative distribution of quality costs? Express this as a bar graph and comment on its significance.

Ross Company implemented a quality improvement program and tracked the following for the five years:

By cost category as a percentage of sales for the same period of time:

Required:

1. Prepare a bar graph that reveals the trend in quality cost as a percentage of sales (time on the horizontal axis and percentages on the vertical). Comment on the message of the graph.

2. Prepare a bar graph for each cost category as a percentage of sales. What does this graph tell you?

3. What if management would like to have the trend in relative distribution of quality costs? Express this as a bar graph and comment on its significance.

Question

Question

Question

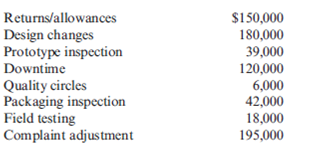

Quality Cost Report, Taguchi Loss Function

Kathy Shorts, president of Oliver Company, was concerned with the trend in sales and profitability. The company had been losing customers at an alarming rate. Furthermore, the company was barely breaking even. Investigation revealed that poor quality was at the root of the problem. At the end of 2013, Kathy decided to begin a quality improvement program. As a first step, she identified the following costs in the accounting records as quality related:

Required:

1. Prepare a quality cost report by quality cost category.

2. Calculate the relative distribution percentages for each quality cost category. Comment on the distribution.

3. Using the Taguchi loss function, an average loss per unit is computed to be $15 per unit. What are the hidden costs of external failure? How does this affect the relative distribution?

4. Shorts's quality manager decided not to bother with the hidden costs. What do you think was his reasoning? Any efforts to reduce measured external failure costs will also reduce the hidden costs. Do you agree or disagree? Explain.

Kathy Shorts, president of Oliver Company, was concerned with the trend in sales and profitability. The company had been losing customers at an alarming rate. Furthermore, the company was barely breaking even. Investigation revealed that poor quality was at the root of the problem. At the end of 2013, Kathy decided to begin a quality improvement program. As a first step, she identified the following costs in the accounting records as quality related:

Required:

1. Prepare a quality cost report by quality cost category.

2. Calculate the relative distribution percentages for each quality cost category. Comment on the distribution.

3. Using the Taguchi loss function, an average loss per unit is computed to be $15 per unit. What are the hidden costs of external failure? How does this affect the relative distribution?

4. Shorts's quality manager decided not to bother with the hidden costs. What do you think was his reasoning? Any efforts to reduce measured external failure costs will also reduce the hidden costs. Do you agree or disagree? Explain.

Question

Question

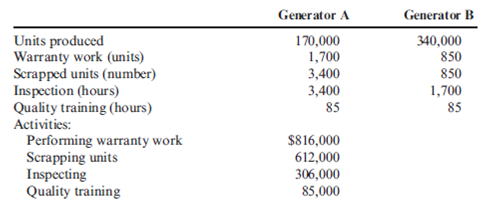

Activity-Based Quality Costing

Abernathy, Inc., produces two different generators and is concerned about their quality. The company has identified the following quality activities and costs associated with the two products:

Required:

1. Calculate the quality cost per unit for each product, and break this unit cost into quality cost categories. Which of the two seems to have the lowest quality?

2. How might a manager use the unit quality cost information?

Abernathy, Inc., produces two different generators and is concerned about their quality. The company has identified the following quality activities and costs associated with the two products:

Required:

1. Calculate the quality cost per unit for each product, and break this unit cost into quality cost categories. Which of the two seems to have the lowest quality?

2. How might a manager use the unit quality cost information?

Question

Question

Taguchi Loss Function

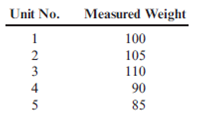

Panguitch Company manufactures a component for tablet computers. Weight and durability of the component are the two most important quality characteristics for the tablet manufacturers. With respect to the weight dimension, the component has a target value of 100 grams. Specification limits are 100 grams, plus or minus five grams. Products produced at the lower specification limit of 95 grams lose $20. A sample of five units produced the following weight measures:

During the first quarter, 100,000 units were produced.

Required:

1. Calculate the loss for each unit. Calculate the average loss for the sample of five.

2. Using the average loss, calculate the hidden quality costs for the first quarter.

3. Durability is another important quality characteristic. The target value is 20,000 hours of operation before failure. The lower specification limit set by engineering and marketing is 19,000 hours. They agreed that there should be no upper specification limit. They also noted that there is a $750 loss at the lower specification limit. Explain why there would be no upper specification limit. Use the lower limit and the left half of the Taguchi quadratic loss function to estimate the loss for components with the following lives: 6,500 hours, 11,000 hours, and 15,500 hours. What does this reveal about the importance of durability?

Panguitch Company manufactures a component for tablet computers. Weight and durability of the component are the two most important quality characteristics for the tablet manufacturers. With respect to the weight dimension, the component has a target value of 100 grams. Specification limits are 100 grams, plus or minus five grams. Products produced at the lower specification limit of 95 grams lose $20. A sample of five units produced the following weight measures:

During the first quarter, 100,000 units were produced.

Required:

1. Calculate the loss for each unit. Calculate the average loss for the sample of five.

2. Using the average loss, calculate the hidden quality costs for the first quarter.

3. Durability is another important quality characteristic. The target value is 20,000 hours of operation before failure. The lower specification limit set by engineering and marketing is 19,000 hours. They agreed that there should be no upper specification limit. They also noted that there is a $750 loss at the lower specification limit. Explain why there would be no upper specification limit. Use the lower limit and the left half of the Taguchi quadratic loss function to estimate the loss for components with the following lives: 6,500 hours, 11,000 hours, and 15,500 hours. What does this reveal about the importance of durability?

Question

Long-Term Performance Report

Nabors Company had actual quality costs for the year ended June 30, 2013, as given below.

At the zero-defect state, Nabors expects to spend $375,000 on quality engineering, $75,000 on vendor certification, and $50,000 on packaging inspection. Assume sales to be $25,000,000.

Required:

1. Prepare a long-range performance report for 2013. What does this report tell the management of Nabors?

2. Explain why quality costs still are present for the zero-defect state.

3. What if Nabors achieves the zero-defect state reflected in the report? What are some of the implications of this achievement?

Nabors Company had actual quality costs for the year ended June 30, 2013, as given below.

At the zero-defect state, Nabors expects to spend $375,000 on quality engineering, $75,000 on vendor certification, and $50,000 on packaging inspection. Assume sales to be $25,000,000.

Required:

1. Prepare a long-range performance report for 2013. What does this report tell the management of Nabors?

2. Explain why quality costs still are present for the zero-defect state.

3. What if Nabors achieves the zero-defect state reflected in the report? What are some of the implications of this achievement?

Question

Question

Question

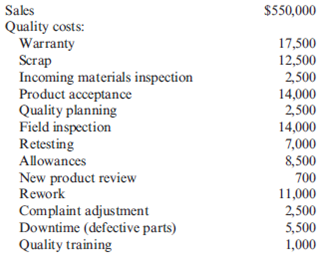

Quality Costs, Pricing Decisions, Market Share

Gaston Company manufactures furniture. One of its product lines is an economy-line kitchen table. During the last year, Gaston produced and sold 100,000 units for $100 per unit. Sales of the table are on a bid basis, but Gaston has always been able to win sufficient bids using the $100 price. This year, however, Gaston was losing more than its share of bids. Concerned, Larry Franklin, owner and president of the company, called a meeting of his executive committee (Megan Johnson, marketing manager; Fred Davis, quality manager; Kevin Jones, production manager; and Helen Jackson, controller).

LARRY : I don't understand why we're losing bids. Megan, do you have an explanation?

MEGAN : Yes, as a matter of fact. Two competitors have lowered their price to $92 per unit. That's too big a difference for most of our buyers to ignore. If we want to keep selling our 100,000 units per year, we will need to lower our price to $92. Otherwise, our sales will drop to about 20,000 to 25,000 per year.

HELEN : The unit contribution margin on the table is $10. Lowering the price to $92 will cost us $8 per unit. Based on a sales volume of 100,000, we'd make $200,000 in contribution margin. If we keep the price at $100, our contribution margin would be $200,000 to $250,000. If we have to lose, let's just take the lower market share. It's better than lowering our prices.

MEGAN : Perhaps. But the same thing could happen to some of our other product lines. My sources tell me that these two companies are on the tail end of a major quality improvement program-one that allows them significant savings. We need to rethink our whole competitive strategy-at least if we want to stay in business. Ideally, we should match the price reduction and work to reduce the costs to recapture the lost contribution margin.

FRED : I think I have something to offer. We are about to embark on a new quality improvement program of our own. I have brought the following estimates of the current quality costs for this economy line. As you can see, these costs run about 16 percent of current sales. That's excessive, and we believe that they can be reduced to about 4 percent of sales over time.

LARRY : This sounds good. Fred, how long will it take for you to achieve this reduction?

FRED : All these costs vary with sales level, so I'll express their reduction rate in those terms. Our best guess is that we can reduce these costs by about 1 percent of sales per quarter. So it should take about 12 quarters, or three years, to achieve the full benefit. Keep in mind that this is with an improvement in quality.

MEGAN : This offers us some hope. If we meet the price immediately, we can maintain our market share. Furthermore, if we can ever reach the point of reducing the price below the $92 level, then we can increase our market share. I estimate that we can increase sales by about 10,000 units for every $1 of price reduction beyond the $92 level. Kevin, how much extra capacity for this line do we have?

KEVIN : We can handle an extra 30,000 or 40,000 tables per year.

Required:

1. Assume that Gaston immediately reduces the bid price to $92. How long will it be before the unit contribution margin is restored to $10, assuming that quality costs are reduced as expected and that sales are maintained at 100,000 units per year (25,000 per quarter)?

2. Assume that Gaston holds the price at $92 until the 4 percent target is achieved. At this new level of quality costs, should the price be reduced? If so, by how much should the price be reduced, and what is the increase in contribution margin? Assume that price can be reduced only in $1 increments.

3. Assume that Gaston immediately reduces the price to $92 and begins the quality improvement program. Now, suppose that Gaston does not wait until the end of the three-year period before reducing prices. Instead, prices will be reduced when profitable to do so. Assume that prices can be reduced only by $1 increments. Identify when the first future price change should occur (if any).

4. Discuss the differences in viewpoints concerning the decision to decrease prices and the short-run contribution margin analysis done by Helen, the controller. Did quality cost information play an important role in the strategic decision making illustrated by the problem?

Gaston Company manufactures furniture. One of its product lines is an economy-line kitchen table. During the last year, Gaston produced and sold 100,000 units for $100 per unit. Sales of the table are on a bid basis, but Gaston has always been able to win sufficient bids using the $100 price. This year, however, Gaston was losing more than its share of bids. Concerned, Larry Franklin, owner and president of the company, called a meeting of his executive committee (Megan Johnson, marketing manager; Fred Davis, quality manager; Kevin Jones, production manager; and Helen Jackson, controller).

LARRY : I don't understand why we're losing bids. Megan, do you have an explanation?

MEGAN : Yes, as a matter of fact. Two competitors have lowered their price to $92 per unit. That's too big a difference for most of our buyers to ignore. If we want to keep selling our 100,000 units per year, we will need to lower our price to $92. Otherwise, our sales will drop to about 20,000 to 25,000 per year.

HELEN : The unit contribution margin on the table is $10. Lowering the price to $92 will cost us $8 per unit. Based on a sales volume of 100,000, we'd make $200,000 in contribution margin. If we keep the price at $100, our contribution margin would be $200,000 to $250,000. If we have to lose, let's just take the lower market share. It's better than lowering our prices.

MEGAN : Perhaps. But the same thing could happen to some of our other product lines. My sources tell me that these two companies are on the tail end of a major quality improvement program-one that allows them significant savings. We need to rethink our whole competitive strategy-at least if we want to stay in business. Ideally, we should match the price reduction and work to reduce the costs to recapture the lost contribution margin.

FRED : I think I have something to offer. We are about to embark on a new quality improvement program of our own. I have brought the following estimates of the current quality costs for this economy line. As you can see, these costs run about 16 percent of current sales. That's excessive, and we believe that they can be reduced to about 4 percent of sales over time.

LARRY : This sounds good. Fred, how long will it take for you to achieve this reduction?

FRED : All these costs vary with sales level, so I'll express their reduction rate in those terms. Our best guess is that we can reduce these costs by about 1 percent of sales per quarter. So it should take about 12 quarters, or three years, to achieve the full benefit. Keep in mind that this is with an improvement in quality.

MEGAN : This offers us some hope. If we meet the price immediately, we can maintain our market share. Furthermore, if we can ever reach the point of reducing the price below the $92 level, then we can increase our market share. I estimate that we can increase sales by about 10,000 units for every $1 of price reduction beyond the $92 level. Kevin, how much extra capacity for this line do we have?

KEVIN : We can handle an extra 30,000 or 40,000 tables per year.

Required:

1. Assume that Gaston immediately reduces the bid price to $92. How long will it be before the unit contribution margin is restored to $10, assuming that quality costs are reduced as expected and that sales are maintained at 100,000 units per year (25,000 per quarter)?

2. Assume that Gaston holds the price at $92 until the 4 percent target is achieved. At this new level of quality costs, should the price be reduced? If so, by how much should the price be reduced, and what is the increase in contribution margin? Assume that price can be reduced only in $1 increments.

3. Assume that Gaston immediately reduces the price to $92 and begins the quality improvement program. Now, suppose that Gaston does not wait until the end of the three-year period before reducing prices. Instead, prices will be reduced when profitable to do so. Assume that prices can be reduced only by $1 increments. Identify when the first future price change should occur (if any).

4. Discuss the differences in viewpoints concerning the decision to decrease prices and the short-run contribution margin analysis done by Helen, the controller. Did quality cost information play an important role in the strategic decision making illustrated by the problem?

Question

Question

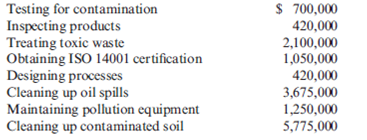

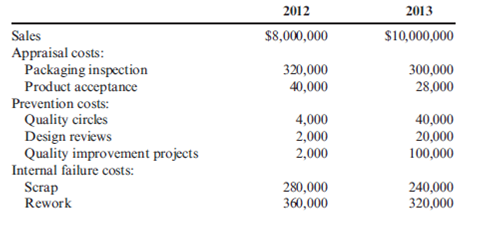

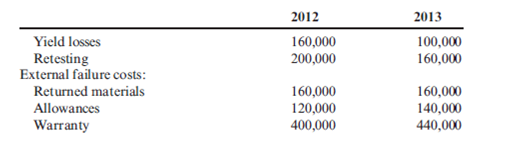

Quality Cost Report

Kang Company reported sales of $3,240,000 in 2013. At the end of the calendar year, the following quality costs were reported:

Required:

1. Prepare a quality cost report.

2. Prepare a graph (pie chart or bar graph) that shows the relative distribution of quality costs, and comment on the distribution.

Kang Company reported sales of $3,240,000 in 2013. At the end of the calendar year, the following quality costs were reported:

Required:

1. Prepare a quality cost report.

2. Prepare a graph (pie chart or bar graph) that shows the relative distribution of quality costs, and comment on the distribution.

Question

Question

Question

Environmental Cost Report

Verde Company reported operating costs of $50,000,000 as of December 31, 2013, with the following environmental costs:

Required:

1. Prepare an environmental cost report, classifying costs by quality category and expressing each as a percentage of total operating costs. What is the message of this report?

2. Prepare a pie chart that shows the relative distribution of environmental costs by category. What does this report tell you?

3. What if Verde deliberately did not include the cost of damaging the ecosystem because of solid waste disposal in its environmental cost report? Offer possible reasons for this decision. If consciously avoided, is this decision unethical?

Verde Company reported operating costs of $50,000,000 as of December 31, 2013, with the following environmental costs:

Required:

1. Prepare an environmental cost report, classifying costs by quality category and expressing each as a percentage of total operating costs. What is the message of this report?

2. Prepare a pie chart that shows the relative distribution of environmental costs by category. What does this report tell you?

3. What if Verde deliberately did not include the cost of damaging the ecosystem because of solid waste disposal in its environmental cost report? Offer possible reasons for this decision. If consciously avoided, is this decision unethical?

Question

Question

Question

Question

Question

Quality Improvement and Profitability Objective

Gagnon Company reported the following sales and quality costs for the past four years. Assume that all quality costs are variable and that all changes in the quality cost ratios are due to a quality improvement program.

Required:

1. Compute the quality costs for all four years. By how much did net income increase from Year 1 to Year 2 because of quality improvements? From Year 2 to Year 3? From Year 3 to Year 4?

2. The management of Gagnon Company believes it is possible to reduce quality costs to 2.5 percent of sales. Assuming sales will continue at the Year 4 level, calculate the additional profit potential facing Gagnon. Is the expectation of improving quality and reducing costs to 2.5 percent of sales realistic? Explain.

3. Assume that Gagnon produces one type of product, which is sold on a bid basis. In Years 1 and 2, the average bid was $400. In Year 1, total variable costs were $250 per unit. In Year 3, competition forced the bid to drop to $380. Compute the total contribution margin in Year 3 assuming the same quality costs as in Year 1. Now, compute the total contribution margin in Year 3 using the actual quality costs for Year 3. What is the increase in profitability resulting from the quality improvements made from Year 1 to Year 3?

Gagnon Company reported the following sales and quality costs for the past four years. Assume that all quality costs are variable and that all changes in the quality cost ratios are due to a quality improvement program.

Required:

1. Compute the quality costs for all four years. By how much did net income increase from Year 1 to Year 2 because of quality improvements? From Year 2 to Year 3? From Year 3 to Year 4?

2. The management of Gagnon Company believes it is possible to reduce quality costs to 2.5 percent of sales. Assuming sales will continue at the Year 4 level, calculate the additional profit potential facing Gagnon. Is the expectation of improving quality and reducing costs to 2.5 percent of sales realistic? Explain.

3. Assume that Gagnon produces one type of product, which is sold on a bid basis. In Years 1 and 2, the average bid was $400. In Year 1, total variable costs were $250 per unit. In Year 3, competition forced the bid to drop to $380. Compute the total contribution margin in Year 3 assuming the same quality costs as in Year 1. Now, compute the total contribution margin in Year 3 using the actual quality costs for Year 3. What is the increase in profitability resulting from the quality improvements made from Year 1 to Year 3?

Question

Environmental Cost Report

At the end of 2013, Bing Pharmaceuticals began to implement an environmental quality management program. As a first step, it identified the following costs in its accounting records as environmentally related for the calendar year just ended:

Required:

1. Prepare an environmental cost report by category. Assume that total operating costs are $150,000,000.

2. Use a pie chart to illustrate the relative distribution percentages for each environmental cost category. Comment on what this distribution communicates to a manager.

At the end of 2013, Bing Pharmaceuticals began to implement an environmental quality management program. As a first step, it identified the following costs in its accounting records as environmentally related for the calendar year just ended:

Required:

1. Prepare an environmental cost report by category. Assume that total operating costs are $150,000,000.

2. Use a pie chart to illustrate the relative distribution percentages for each environmental cost category. Comment on what this distribution communicates to a manager.

Question

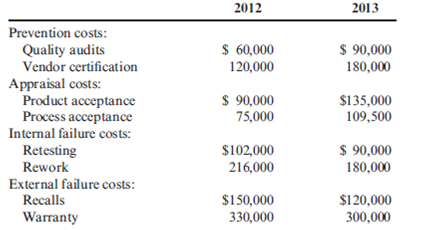

Quality Cost Report, Interim Performance Report

Recently, Ulrich Company received a report from an external consulting group on its quality costs. The consultants reported that the company's quality costs total about 21 percent of its sales revenues. Somewhat shocked by the magnitude of the costs, Rob Rustin, president of Ulrich Company, decided to launch a major quality improvement program. For the coming year, management decided to reduce quality costs to 17 percent of sales revenues. Although the amount of reduction was ambitious, most company officials believed that the goal could be realized. To improve the monitoring of the quality improvement program, Rob directed Pamela Golding, the controller, to prepare monthly performance reports comparing budgeted and actual quality costs. Budgeted costs and sales for the first two months of the year are as follows:

The following actual sales and actual quality costs were reported for January:

Required:

1. Reorganize the monthly budgets so that quality costs are grouped in one of four categories: appraisal, prevention, internal failure, or external failure. (Essentially, prepare a budgeted cost of quality report.) Also, identify each cost as variable (V) or fixed (F). (Assume that no costs are mixed.)

2. Prepare a performance report for January that compares actual costs with budgeted costs. Comment on the company's progress in improving quality and reducing its quality costs.

Recently, Ulrich Company received a report from an external consulting group on its quality costs. The consultants reported that the company's quality costs total about 21 percent of its sales revenues. Somewhat shocked by the magnitude of the costs, Rob Rustin, president of Ulrich Company, decided to launch a major quality improvement program. For the coming year, management decided to reduce quality costs to 17 percent of sales revenues. Although the amount of reduction was ambitious, most company officials believed that the goal could be realized. To improve the monitoring of the quality improvement program, Rob directed Pamela Golding, the controller, to prepare monthly performance reports comparing budgeted and actual quality costs. Budgeted costs and sales for the first two months of the year are as follows:

The following actual sales and actual quality costs were reported for January:

Required:

1. Reorganize the monthly budgets so that quality costs are grouped in one of four categories: appraisal, prevention, internal failure, or external failure. (Essentially, prepare a budgeted cost of quality report.) Also, identify each cost as variable (V) or fixed (F). (Assume that no costs are mixed.)

2. Prepare a performance report for January that compares actual costs with budgeted costs. Comment on the company's progress in improving quality and reducing its quality costs.

Question

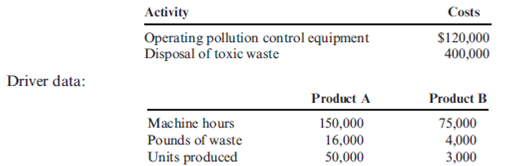

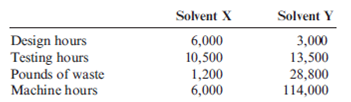

Activity-Based Environmental Cost Assignments

Pinter Company had the following environmental activities and product information:

1. Environmental activity costs

2. Driver data

3. Other production data

Required:

1. Calculate the activity rates that will be used to assign environmental costs to products.

2. Determine the unit environmental and unit costs of each product using ABC.

3. What if the design costs increased to $360,000 and the cost of toxic waste decreased to $750,000? Assume that Solvent Y uses 6,000 out of 12,000 design hours. Also assume that waste is cut by 50 percent and that Solvent Y is responsible for 14,250 of 15,000 pounds of toxic waste. What is the new environmental cost for Solvent Y?

Pinter Company had the following environmental activities and product information:

1. Environmental activity costs

2. Driver data

3. Other production data

Required:

1. Calculate the activity rates that will be used to assign environmental costs to products.

2. Determine the unit environmental and unit costs of each product using ABC.

3. What if the design costs increased to $360,000 and the cost of toxic waste decreased to $750,000? Assume that Solvent Y uses 6,000 out of 12,000 design hours. Also assume that waste is cut by 50 percent and that Solvent Y is responsible for 14,250 of 15,000 pounds of toxic waste. What is the new environmental cost for Solvent Y?

Question

Question

Question

Quality Cost Performance Reporting: One-Year Trend, Long-Range Analysis

In 2013, Major Company initiated a full-scale, quality improvement program. At the end of the year, Jack Aldredge, the president, noted with some satisfaction that the defects per unit of product had dropped significantly compared to the prior year. He was also pleased that relationships with suppliers had improved and defective materials had declined. The new quality training program was also well accepted by employees. Of most interest to the president, however, was the impact of the quality improvements on profitability. To help assess the dollar impact of the quality improvements, the actual sales and the actual quality costs for 2012 and 2013 are as follows by quality category:

All prevention costs are fixed (by discretion). Assume all other quality costs are unit-level variable.

Required:

1. Compute the relative distribution of quality costs for each year and prepare a pie chart. Do you believe that the company is moving in the right direction in terms of the balance among the quality cost categories? Explain.

2. Prepare a one-year trend performance report for 2013 (compare the actual costs of 2013 with those of 2012, adjusted for differences in sales volume). How much have profits increased because of the quality improvements made by Major Company?

3. Estimate the additional improvement in profits if Major Company ultimately reduces its quality costs to 2.5 percent of sales revenues (assume sales of $10 million).

In 2013, Major Company initiated a full-scale, quality improvement program. At the end of the year, Jack Aldredge, the president, noted with some satisfaction that the defects per unit of product had dropped significantly compared to the prior year. He was also pleased that relationships with suppliers had improved and defective materials had declined. The new quality training program was also well accepted by employees. Of most interest to the president, however, was the impact of the quality improvements on profitability. To help assess the dollar impact of the quality improvements, the actual sales and the actual quality costs for 2012 and 2013 are as follows by quality category:

All prevention costs are fixed (by discretion). Assume all other quality costs are unit-level variable.

Required:

1. Compute the relative distribution of quality costs for each year and prepare a pie chart. Do you believe that the company is moving in the right direction in terms of the balance among the quality cost categories? Explain.

2. Prepare a one-year trend performance report for 2013 (compare the actual costs of 2013 with those of 2012, adjusted for differences in sales volume). How much have profits increased because of the quality improvements made by Major Company?

3. Estimate the additional improvement in profits if Major Company ultimately reduces its quality costs to 2.5 percent of sales revenues (assume sales of $10 million).

Question

Question

Quality Costs: Profit Improvement and Distribution Across Categories, Gainsharing

Muskogee Company had sales of $60,000,000 in 2009. In 2013, sales had increased to $75,000,000. A quality improvement program was implemented at the beginning of 2009. Overall conformance quality was targeted for improvement. The quality costs for 2009 and 2013 follow. Assume any changes in quality costs are attributable to improvements in quality.

Required:

1. Compute the quality cost-to-sales ratio for each year. Is this type of improvement possible?

2. Calculate the relative distribution of costs by category for 2009. What do you think of the way costs are distributed? (A pie chart or bar graph may be of some help.) How do you think they will be distributed as the company approaches a zero-defects state?

3. Calculate the relative distribution of costs by category for 2013. What do you think of the level and distribution of quality costs? (A pie chart or bar graph may be of some help.) Do you think further reductions are possible?

4. The quality manager for Muskogee indicated that the external failure costs reported are only the measured costs. He argued that the 2013 external costs were much higher than those reported and that additional investment ought to be made in control costs. Discuss the validity of his viewpoint.

5. Suppose that the manager of Muskogee received a bonus equal to 10 percent of the quality cost savings each year. Do you think that gainsharing is a good or a bad idea? Discuss the risks of gainsharing.

Muskogee Company had sales of $60,000,000 in 2009. In 2013, sales had increased to $75,000,000. A quality improvement program was implemented at the beginning of 2009. Overall conformance quality was targeted for improvement. The quality costs for 2009 and 2013 follow. Assume any changes in quality costs are attributable to improvements in quality.

Required:

1. Compute the quality cost-to-sales ratio for each year. Is this type of improvement possible?

2. Calculate the relative distribution of costs by category for 2009. What do you think of the way costs are distributed? (A pie chart or bar graph may be of some help.) How do you think they will be distributed as the company approaches a zero-defects state?

3. Calculate the relative distribution of costs by category for 2013. What do you think of the level and distribution of quality costs? (A pie chart or bar graph may be of some help.) Do you think further reductions are possible?

4. The quality manager for Muskogee indicated that the external failure costs reported are only the measured costs. He argued that the 2013 external costs were much higher than those reported and that additional investment ought to be made in control costs. Discuss the validity of his viewpoint.

5. Suppose that the manager of Muskogee received a bonus equal to 10 percent of the quality cost savings each year. Do you think that gainsharing is a good or a bad idea? Discuss the risks of gainsharing.

Question

Question

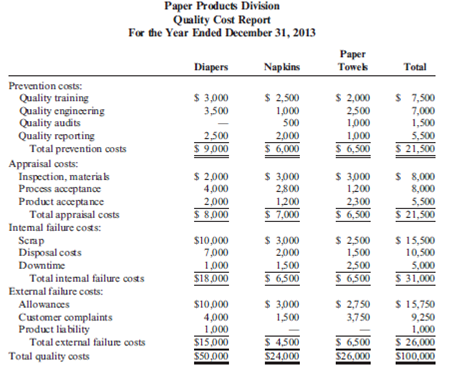

Distribution of Quality Costs

Paper Products Division produces paper diapers, napkins, and paper towels. The divisional manager has decided that quality costs can be minimized by distributing quality costs evenly among the four quality categories and reducing them to no more than 5 percent of sales. He has just received the following quality cost report:

Assume that all prevention costs are fixed and that the remaining quality costs are variable (unit-level).

Required:

1. Assume that the sales revenue for the year totaled $2 million, with sales for each product as follows: diapers, $1 million; napkins, $600,000; and paper towels, $400,000. Evaluate the distribution of costs for the division as a whole and for each product line. What recommendations do you have for the divisional manager?

2. Now, assume that total sales are $1 million and have this breakdown: diapers, $500,000; napkins, $300,000; and paper towels, $200,000. Evaluate the distribution of costs for the division as a whole and for each product line in this case. Do you think it is possible to reduce the quality costs to 5 percent of sales for each product line and for the division as a whole and, simultaneously, achieve an equal distribution of the quality costs? What recommendations do you have?

3. Assume total sales of $1 million with this breakdown: diapers, $500,000; napkins, $180,000; and paper towels, $320,000. Evaluate the distribution of quality costs. What recommendations do you have for the divisional manager?

4. Discuss the value of having quality costs reported by segment.

Paper Products Division produces paper diapers, napkins, and paper towels. The divisional manager has decided that quality costs can be minimized by distributing quality costs evenly among the four quality categories and reducing them to no more than 5 percent of sales. He has just received the following quality cost report:

Assume that all prevention costs are fixed and that the remaining quality costs are variable (unit-level).

Required:

1. Assume that the sales revenue for the year totaled $2 million, with sales for each product as follows: diapers, $1 million; napkins, $600,000; and paper towels, $400,000. Evaluate the distribution of costs for the division as a whole and for each product line. What recommendations do you have for the divisional manager?

2. Now, assume that total sales are $1 million and have this breakdown: diapers, $500,000; napkins, $300,000; and paper towels, $200,000. Evaluate the distribution of costs for the division as a whole and for each product line in this case. Do you think it is possible to reduce the quality costs to 5 percent of sales for each product line and for the division as a whole and, simultaneously, achieve an equal distribution of the quality costs? What recommendations do you have?

3. Assume total sales of $1 million with this breakdown: diapers, $500,000; napkins, $180,000; and paper towels, $320,000. Evaluate the distribution of quality costs. What recommendations do you have for the divisional manager?

4. Discuss the value of having quality costs reported by segment.

Question

Question

Question

Question

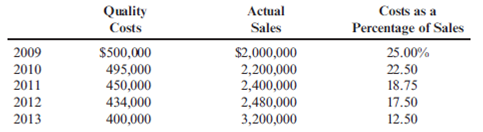

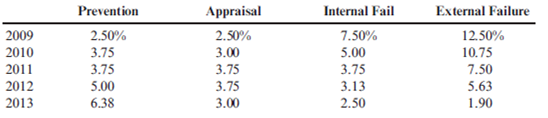

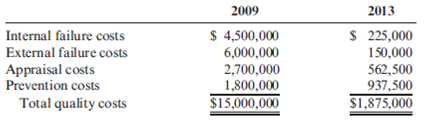

Trend Analysis, Quality Costs

In 2009, Milton Thayne, president of Carbondale Electronics, received a report indicating that quality costs were 31 percent of sales. Faced with increasing pressures from imported goods, Milton resolved to take measures to improve the overall quality of the company's products. After hiring a consultant in 2010, the company began an aggressive program of total quality control. At the end of 2013, Milton requested an analysis of the progress the company had made in reducing and controlling quality costs. The Accounting Department assembled the following data:

Required:

1. Compute the quality costs as a percentage of sales by category and in total for each year.

2. Prepare a multiple-year trend graph for quality costs, both by total costs and by category. Using the graph, assess the progress made in reducing and controlling quality costs. Does the graph provide evidence that quality has improved? Explain.

3. Using the 2009 quality cost relationships (assume all costs are variable), calculate the quality costs that would have prevailed in 2012. By how much did profits increase in 2012 because of the quality improvement program? Repeat for 2013.

In 2009, Milton Thayne, president of Carbondale Electronics, received a report indicating that quality costs were 31 percent of sales. Faced with increasing pressures from imported goods, Milton resolved to take measures to improve the overall quality of the company's products. After hiring a consultant in 2010, the company began an aggressive program of total quality control. At the end of 2013, Milton requested an analysis of the progress the company had made in reducing and controlling quality costs. The Accounting Department assembled the following data:

Required:

1. Compute the quality costs as a percentage of sales by category and in total for each year.

2. Prepare a multiple-year trend graph for quality costs, both by total costs and by category. Using the graph, assess the progress made in reducing and controlling quality costs. Does the graph provide evidence that quality has improved? Explain.

3. Using the 2009 quality cost relationships (assume all costs are variable), calculate the quality costs that would have prevailed in 2012. By how much did profits increase in 2012 because of the quality improvement program? Repeat for 2013.

Question

Question

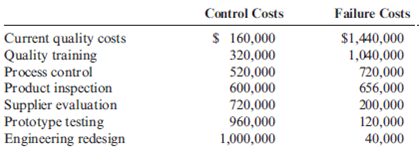

Trade-Offs Among Quality Cost Categories, Total Quality Control, Gainsharing

Javier Company has sales of $8 million and quality costs of $1,600,000. The company is embarking on a major quality improvement program. During the next three years, Javier intends to attack failure costs by increasing its appraisal and prevention costs. The "right" prevention activities will be selected, and appraisal costs will be reduced according to the results achieved. For the coming year, management is considering six specific activities: quality training, process control, product inspection, supplier evaluation, prototype testing, and redesign of two major products. To encourage managers to focus on reducing non-value-added quality costs and select the right activities, a bonus pool is established relating to reduction of quality costs. The bonus pool is equal to 10 percent of the total reduction in quality costs.

Current quality costs and the costs of these six activities are given in the following table. Each activity is added sequentially so that its effect on the cost categories can be assessed. For example, after quality training is added, the control costs increase to $320,000, and the failure costs drop to $1,040,000. Even though the activities are presented sequentially, they are totally independent of each other. Thus, only beneficial activities need be selected.

Required:

1. Identify the control activities that should be implemented, and calculate the total quality costs associated with this selection. Assume that an activity is selected only if it increases the bonus pool.

2. Given the activities selected in Requirement 1, calculate the following:

a. The reduction in total quality costs

b. The percentage distribution for control and failure costs

c. The amount for this year's bonus pool

3. Suppose that a quality engineer complained about the gainsharing incentive system. Basically, he argued that the bonus should be based only on reductions of failure and appraisal costs. In this way, investment in prevention activities would be encouraged, and eventually, failure and appraisal costs would be eliminated. After eliminating the non-value-added costs, focus could then be placed on the level of prevention costs. If this approach were adopted, what activities would be selected? Do you agree or disagree with this approach? Explain.

Javier Company has sales of $8 million and quality costs of $1,600,000. The company is embarking on a major quality improvement program. During the next three years, Javier intends to attack failure costs by increasing its appraisal and prevention costs. The "right" prevention activities will be selected, and appraisal costs will be reduced according to the results achieved. For the coming year, management is considering six specific activities: quality training, process control, product inspection, supplier evaluation, prototype testing, and redesign of two major products. To encourage managers to focus on reducing non-value-added quality costs and select the right activities, a bonus pool is established relating to reduction of quality costs. The bonus pool is equal to 10 percent of the total reduction in quality costs.

Current quality costs and the costs of these six activities are given in the following table. Each activity is added sequentially so that its effect on the cost categories can be assessed. For example, after quality training is added, the control costs increase to $320,000, and the failure costs drop to $1,040,000. Even though the activities are presented sequentially, they are totally independent of each other. Thus, only beneficial activities need be selected.

Required:

1. Identify the control activities that should be implemented, and calculate the total quality costs associated with this selection. Assume that an activity is selected only if it increases the bonus pool.

2. Given the activities selected in Requirement 1, calculate the following:

a. The reduction in total quality costs

b. The percentage distribution for control and failure costs

c. The amount for this year's bonus pool

3. Suppose that a quality engineer complained about the gainsharing incentive system. Basically, he argued that the bonus should be based only on reductions of failure and appraisal costs. In this way, investment in prevention activities would be encouraged, and eventually, failure and appraisal costs would be eliminated. After eliminating the non-value-added costs, focus could then be placed on the level of prevention costs. If this approach were adopted, what activities would be selected? Do you agree or disagree with this approach? Explain.

Question

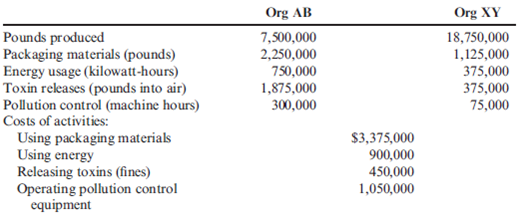

Environmental Cost Assignment

Coyle Pharmaceuticals produces two organic chemicals (Org AB and Org XY) used in the production of two of its most wide-selling anti-cancer drugs. The controller and environmental manager have identified the following environmental activities and costs associated with the two products:

Required:

1. Calculate the environmental cost per pound for each product. Which of the two products appears to cause the most degradation to the environment?

2. In which environmental category would you classify excessive use of materials and energy?

3. Suppose that the toxin releases cause health problems for those who live near the chemical plant. The costs, due to missed work and medical treatments, are estimated at $2,025,000 per year. How would assignment of these costs change the unit cost? Should they be assigned?

Coyle Pharmaceuticals produces two organic chemicals (Org AB and Org XY) used in the production of two of its most wide-selling anti-cancer drugs. The controller and environmental manager have identified the following environmental activities and costs associated with the two products:

Required:

1. Calculate the environmental cost per pound for each product. Which of the two products appears to cause the most degradation to the environment?

2. In which environmental category would you classify excessive use of materials and energy?

3. Suppose that the toxin releases cause health problems for those who live near the chemical plant. The costs, due to missed work and medical treatments, are estimated at $2,025,000 per year. How would assignment of these costs change the unit cost? Should they be assigned?

Question

Case on Quality Cost Performance Reports

Iona Company, a large printing company, is in its fourth year of a five-year, quality improvement program. The program began in 2009 with an internal study that revealed the quality costs being incurred. In that year, a five-year plan was developed to lower quality costs to 10 percent of sales by the end of 2013. Sales and quality costs for each year are as follows:

* Budgeted figures.

Quality costs by category are expressed as a percentage of sales as follows:

The detail of the 2013 budget for quality costs is also provided.

All prevention costs are fixed; all other quality costs are variable.

During 2013, the company had $12 million in sales. Actual quality costs for 2012 and 2013 are as follows:

Required:

1. Prepare an interim quality cost performance report for 2013 that compares actual quality costs with budgeted quality costs. Comment on the firm's ability to achieve its quality goals for the year.

2. Prepare a one-period quality performance report for 2013 that compares the actual quality costs of 2012 with the actual costs of 2013. How much did profits change because of improved quality?

3. Prepare a graph that shows the trend in total quality costs as a percentage of sales since the inception of the quality improvement program.

4. Prepare a graph that shows the trend for all four quality cost categories for 2009 through 2013. How does this graph help management know that the reduction in total quality costs is attributable to quality improvements?

5. Assume that the company is preparing a second five-year plan to reduce quality costs to 2.5 percent of sales. Prepare a long-range quality cost performance report assuming sales of $15 million at the end of five years. Assume that the final planned relative distribution of quality costs is as follows: proofreading, 50 percent; other inspection, 13 percent; quality training, 30 percent; and quality reporting, 7 percent.

Iona Company, a large printing company, is in its fourth year of a five-year, quality improvement program. The program began in 2009 with an internal study that revealed the quality costs being incurred. In that year, a five-year plan was developed to lower quality costs to 10 percent of sales by the end of 2013. Sales and quality costs for each year are as follows:

* Budgeted figures.

Quality costs by category are expressed as a percentage of sales as follows:

The detail of the 2013 budget for quality costs is also provided.

All prevention costs are fixed; all other quality costs are variable.

During 2013, the company had $12 million in sales. Actual quality costs for 2012 and 2013 are as follows:

Required:

1. Prepare an interim quality cost performance report for 2013 that compares actual quality costs with budgeted quality costs. Comment on the firm's ability to achieve its quality goals for the year.

2. Prepare a one-period quality performance report for 2013 that compares the actual quality costs of 2012 with the actual costs of 2013. How much did profits change because of improved quality?

3. Prepare a graph that shows the trend in total quality costs as a percentage of sales since the inception of the quality improvement program.

4. Prepare a graph that shows the trend for all four quality cost categories for 2009 through 2013. How does this graph help management know that the reduction in total quality costs is attributable to quality improvements?

5. Assume that the company is preparing a second five-year plan to reduce quality costs to 2.5 percent of sales. Prepare a long-range quality cost performance report assuming sales of $15 million at the end of five years. Assume that the final planned relative distribution of quality costs is as follows: proofreading, 50 percent; other inspection, 13 percent; quality training, 30 percent; and quality reporting, 7 percent.

Question

Question

Question

Question

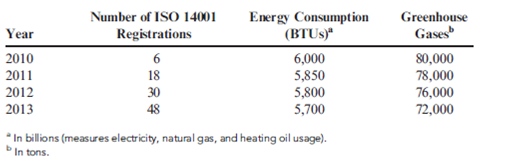

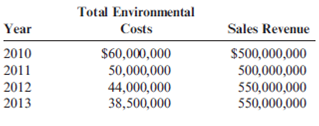

Environmental Responsibility Accounting, Cost Trends

At the beginning of 2010, Heber Company, an international telecommunications company, embarked on an environmental improvement program. The company set a goal to have all its facilities ISO 14001 registered by 2013. (There are 60 facilities worldwide.) To communicate the environmental progress made, management decided to issue, on a voluntary basis, an annual environmental progress report. Internally, the Accounting Department issued monthly progress reports and developed a number of measures that could be reported even more frequently to assess progress. Heber also asked an international CPA firm to prepare an auditor's report that would comment on the reasonableness and fairness of Heber's approach to assessing and measuring environmental performance.

At the end of 2013, the controller had gathered data that would be used in preparing the environmental progress report. A sample of the data collected is as follows:

As part of its environmental cost reporting system, Heber tracks its total environmental costs. Consider the following cost and sales data:

Required:

1. Using the data, prepare a bar graph for each of the three environmental variables provided (registrations, energy, and greenhouse gases). Comment on the progress made on these three dimensions.

2. Prepare a bar graph for environmental costs expressed as a percentage of sales. Assuming that environmental performance has improved, explain why environmental costs have decreased.

3. Normalize energy consumption by expressing it as a multiple of sales (BTUs/Sales). Now, prepare a bar graph for energy. Comment on the progress made in reducing energy consumption. How does this compare with the conclusion that would be reached using a nonnormalized measure of progress? Which is the best approach? Explain.

At the beginning of 2010, Heber Company, an international telecommunications company, embarked on an environmental improvement program. The company set a goal to have all its facilities ISO 14001 registered by 2013. (There are 60 facilities worldwide.) To communicate the environmental progress made, management decided to issue, on a voluntary basis, an annual environmental progress report. Internally, the Accounting Department issued monthly progress reports and developed a number of measures that could be reported even more frequently to assess progress. Heber also asked an international CPA firm to prepare an auditor's report that would comment on the reasonableness and fairness of Heber's approach to assessing and measuring environmental performance.

At the end of 2013, the controller had gathered data that would be used in preparing the environmental progress report. A sample of the data collected is as follows:

As part of its environmental cost reporting system, Heber tracks its total environmental costs. Consider the following cost and sales data:

Required:

1. Using the data, prepare a bar graph for each of the three environmental variables provided (registrations, energy, and greenhouse gases). Comment on the progress made on these three dimensions.

2. Prepare a bar graph for environmental costs expressed as a percentage of sales. Assuming that environmental performance has improved, explain why environmental costs have decreased.

3. Normalize energy consumption by expressing it as a multiple of sales (BTUs/Sales). Now, prepare a bar graph for energy. Comment on the progress made in reducing energy consumption. How does this compare with the conclusion that would be reached using a nonnormalized measure of progress? Which is the best approach? Explain.

Question

Question

Trend, Long-Range Performance Report

In 2012, Tru-Delite Frozen Desserts, Inc., instituted a quality improvement program. At the end of 2013, the management of the corporation requested a report to show the amount saved by the measures taken during the year. The actual sales and quality costs for 2012 and 2013 are as follows:

Tru-Delite's management believes that quality costs can be reduced to 2.5 percent of sales within the next five years. At the end of 2017, Tru-Delite's sales are projected to grow to $750,000. The projected relative distribution of quality costs at the end of 2017 is as follows:

Required:

1. Profits increased by what amount due to quality improvements made in 2013?

2. Prepare a long-range performance report that compares the quality costs incurred at the end of 2013 with the quality cost structure expected at the end of 2017.

3. Are the targeted costs in the year 2017 all value-added costs? How would you interpret the variances if the targeted costs are value-added costs?

4. What would be the profit increase in 2017 if the 2.5 percent performance standard is met in that year?

In 2012, Tru-Delite Frozen Desserts, Inc., instituted a quality improvement program. At the end of 2013, the management of the corporation requested a report to show the amount saved by the measures taken during the year. The actual sales and quality costs for 2012 and 2013 are as follows:

Tru-Delite's management believes that quality costs can be reduced to 2.5 percent of sales within the next five years. At the end of 2017, Tru-Delite's sales are projected to grow to $750,000. The projected relative distribution of quality costs at the end of 2017 is as follows:

Required:

1. Profits increased by what amount due to quality improvements made in 2013?

2. Prepare a long-range performance report that compares the quality costs incurred at the end of 2013 with the quality cost structure expected at the end of 2017.

3. Are the targeted costs in the year 2017 all value-added costs? How would you interpret the variances if the targeted costs are value-added costs?

4. What would be the profit increase in 2017 if the 2.5 percent performance standard is met in that year?

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/67

Play

Full screen (f)

Deck 14: Quality and Environmental Cost Management

1

Quality Cost Report

Evans Company had total sales of $3,000,000 for fiscal 2013. The costs of quality-related activities are given below.

Required:

1. Prepare a quality cost report, classifying costs by category and expressing each category as a percentage of sales. What message does the cost report provide?

2. Prepare a bar graph and pie chart that illustrate each category's contribution to total quality costs. Comment on the significance of the distribution.

3. What if , five years from now, quality costs are 7.5 percent of sales, with control costs being 65 percent of the total quality costs? What would your conclusion be?

Evans Company had total sales of $3,000,000 for fiscal 2013. The costs of quality-related activities are given below.

Required:

1. Prepare a quality cost report, classifying costs by category and expressing each category as a percentage of sales. What message does the cost report provide?

2. Prepare a bar graph and pie chart that illustrate each category's contribution to total quality costs. Comment on the significance of the distribution.

3. What if , five years from now, quality costs are 7.5 percent of sales, with control costs being 65 percent of the total quality costs? What would your conclusion be?

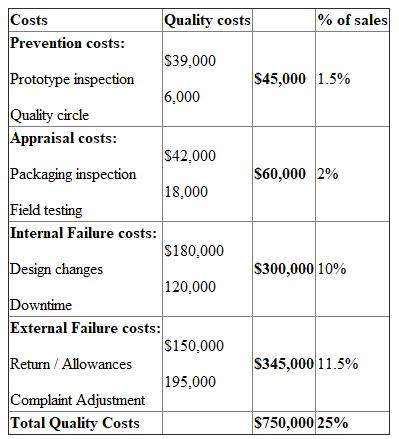

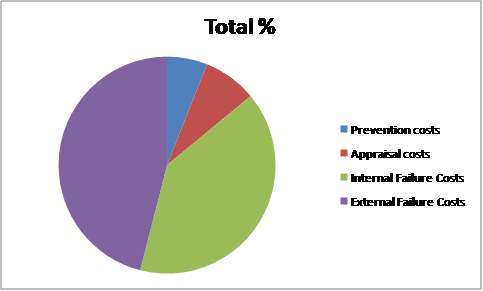

(1) Quality Cost Report:

Quality cost report is important for the organization regarding improving and controlling the quality costs.

First quality costs are categorized into four types:

(1) Prevention costs

(2) Detection (Appraisal) costs

(3) Internal failure costs

(4) External failure costs

Quality Costs Report of Evans Company

For the year ended 2013

Note:

Note:

• Total sales is $3,000,000

• Prevention costs is 1.5% ($45,000 / $$3,000,000) and like wise

• Percentage of sales is (Cost / Total Sales) 100

100

Therefore, the report clearly indicates that quality costs are too high 25% of sales which is much greater than the desired 2 to 4 percent of sales that prevails for companies with good quality performance.

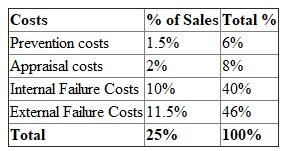

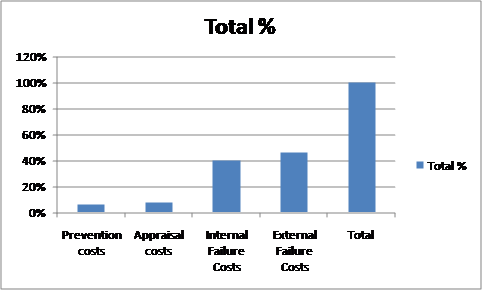

(2) Prepare the bar graph and pie chart:

Report Analysis:

• As per the data Failure Costs are 86% which is too high

• Compared to 14% relates to prevention cost and the appraisal costs

• It needs to invest more in control activities to drive down failure costs

• Total percentage is 6% (1.5 / 25) 100 and like wise

100 and like wise

• Total prevention cost and the appraisal costs is 14% (6% + 8%)• While Failure Costs are 86% (40% + 46%)Table showing total percent

(3) Conclusion:

(3) Conclusion:

• Reduction in the quality costs is due to the quality improvement, the 7.5% percent level reveals that the company is producing at a very high quality level.

• If quality costs are with the range of 2 to 4 percent than no failure costs, then the company has effectively and practically achieved Zero defects stage.

• It should be better to reduce the failure costs for the development of the firm.

Quality cost report is important for the organization regarding improving and controlling the quality costs.

First quality costs are categorized into four types:

(1) Prevention costs

(2) Detection (Appraisal) costs

(3) Internal failure costs

(4) External failure costs

Quality Costs Report of Evans Company

For the year ended 2013

Note: • Total sales is $3,000,000

• Prevention costs is 1.5% ($45,000 / $$3,000,000) and like wise

• Percentage of sales is (Cost / Total Sales)

100 Therefore, the report clearly indicates that quality costs are too high 25% of sales which is much greater than the desired 2 to 4 percent of sales that prevails for companies with good quality performance.

(2) Prepare the bar graph and pie chart:

Report Analysis:

• As per the data Failure Costs are 86% which is too high

• Compared to 14% relates to prevention cost and the appraisal costs

• It needs to invest more in control activities to drive down failure costs

• Total percentage is 6% (1.5 / 25)

100 and like wise• Total prevention cost and the appraisal costs is 14% (6% + 8%)• While Failure Costs are 86% (40% + 46%)Table showing total percent

(3) Conclusion: • Reduction in the quality costs is due to the quality improvement, the 7.5% percent level reveals that the company is producing at a very high quality level.

• If quality costs are with the range of 2 to 4 percent than no failure costs, then the company has effectively and practically achieved Zero defects stage.

• It should be better to reduce the failure costs for the development of the firm.

2

Describe the three types of quality performance reporting. How can managers use each report to help evaluate their quality improvement programs?

The three types of quality performance reporting are described below:

1. Interim quality reports: interim quality reports are prepared to determine the progress of quality in connection with current period standard. In fact, current reporting process takes in to account only the quality check of currently manufacturing products which are normally produced in current financial year and it is evaluated that how much these products are meeting the desired specifications.

2. Multiple-period reports : as far as multiple reporting is concerned it does not only take in account the current quality evaluation but compare it with former quality improvements as well, so as to boost the quality standard of the products manufactured.

3. Long-range reports: long range reporting is concerned with deterring the capability of the company to produce zero defected products. Hence this reporting is applied to evaluate the improvement of the company toward attaining the zero defect goal. This target can not be achieved in short run therefore it is considered as long range process.

1. Interim quality reports: interim quality reports are prepared to determine the progress of quality in connection with current period standard. In fact, current reporting process takes in to account only the quality check of currently manufacturing products which are normally produced in current financial year and it is evaluated that how much these products are meeting the desired specifications.