Deck 9: Standard Costing: a Functional-Based Control Approach

Full screen (f)

Question

Question

Calculating the Direct Labor Mix Variance

Mangia Pizza Company makes frozen pizzas that are sold through grocery stores. Mangia uses two types of direct labor: machine operators and packers. Mangia developed the following standard mix for spreading on premade pizza shells to produce 16 giant-size sausage pizzas.

Mangia's recent batch (designed to produce 400 pizzas) used 400 direct labor hours. Of the total, 160 were for machine operators, and the remaining 240 hours were for packers. The actual yield was 780 pizzas.

Required:

1. Calculate the standard mix (SM) in hours for machine operators and for packers.

2. Calculate the mix variance.

3. Calculate the actual proportion of hours worked by machine operators and by packers. Use these results to explain the direction (favorable or unfavorable) of the mix variance.

4. What if of the total 400 direct labor hours worked, 200 were worked by each type of direct labor? How would that affect the mix variance?

Mangia Pizza Company makes frozen pizzas that are sold through grocery stores. Mangia uses two types of direct labor: machine operators and packers. Mangia developed the following standard mix for spreading on premade pizza shells to produce 16 giant-size sausage pizzas.

Mangia's recent batch (designed to produce 400 pizzas) used 400 direct labor hours. Of the total, 160 were for machine operators, and the remaining 240 hours were for packers. The actual yield was 780 pizzas.

Required:

1. Calculate the standard mix (SM) in hours for machine operators and for packers.

2. Calculate the mix variance.

3. Calculate the actual proportion of hours worked by machine operators and by packers. Use these results to explain the direction (favorable or unfavorable) of the mix variance.

4. What if of the total 400 direct labor hours worked, 200 were worked by each type of direct labor? How would that affect the mix variance?

Question

Direct Labor and Direct Materials Variances, Journal Entries

Jameson Company produces paper towels. The company has established the following direct materials and direct labor standards for one case of paper towels:

During the first quarter of the year, Jameson produced 45,000 cases of paper towels. The company purchased and used 135,700 pounds of paper pulp at $0.38 per pound. Actual direct labor used was 91,000 hours at $12.10 per hour.

Required:

1. Calculate the direct materials price and usage variances.

2. Calculate the direct labor rate and efficiency variances.

3. Prepare the journal entries for the direct materials and direct labor variances.

4. Describe how flexible budgeting variances relate to the direct materials and direct labor variances computed in Requirements 1 and 2.

Jameson Company produces paper towels. The company has established the following direct materials and direct labor standards for one case of paper towels:

During the first quarter of the year, Jameson produced 45,000 cases of paper towels. The company purchased and used 135,700 pounds of paper pulp at $0.38 per pound. Actual direct labor used was 91,000 hours at $12.10 per hour.

Required:

1. Calculate the direct materials price and usage variances.

2. Calculate the direct labor rate and efficiency variances.

3. Prepare the journal entries for the direct materials and direct labor variances.

4. Describe how flexible budgeting variances relate to the direct materials and direct labor variances computed in Requirements 1 and 2.

Question

Direct Materials Usage Variances: Direct Materials Mix and Yield Variances

Energy Products Company produces a gasoline additive, Gas Gain. This product increases engine efficiency and improves gasoline mileage by creating a more complete burn in the combustion process.

Careful controls are required during the production process to ensure that the proper mix of input chemicals is achieved and that evaporation is controlled. If the controls are not effective, there can be a loss of output and efficiency.

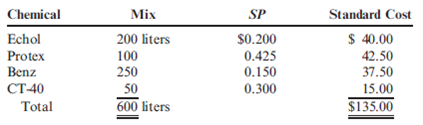

The standard cost of producing a 500-liter batch of Gas Gain is $135. The standard direct materials mix and related standard cost of each chemical used in a 500-liter batch are as follows:

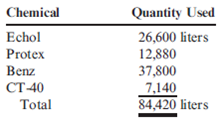

The quantities of chemicals purchased and used during the current production period are shown in the following schedule. A total of 140 batches of Gas Gain were manufactured during the current production period. Energy Products determines its cost and chemical usage variations at the end of each production period.

Required:

Compute the total direct materials usage variance, and then break down this variance into its mix and yield components. (CMA adapted)

Energy Products Company produces a gasoline additive, Gas Gain. This product increases engine efficiency and improves gasoline mileage by creating a more complete burn in the combustion process.

Careful controls are required during the production process to ensure that the proper mix of input chemicals is achieved and that evaporation is controlled. If the controls are not effective, there can be a loss of output and efficiency.

The standard cost of producing a 500-liter batch of Gas Gain is $135. The standard direct materials mix and related standard cost of each chemical used in a 500-liter batch are as follows:

The quantities of chemicals purchased and used during the current production period are shown in the following schedule. A total of 140 batches of Gas Gain were manufactured during the current production period. Energy Products determines its cost and chemical usage variations at the end of each production period.

Required:

Compute the total direct materials usage variance, and then break down this variance into its mix and yield components. (CMA adapted)

Question

Question

Question

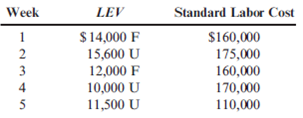

Investigation of Variances

Madison Company uses the following rule to determine whether direct labor efficiency variances ought to be investigated. A direct labor efficiency variance will be investigated anytime the amount exceeds the lesser of $12,000 or 10 percent of the standard labor cost. Reports for the past five weeks provided the following information:

Required:

1. Using the rule provided, identify the cases that will be investigated.

2. Suppose that investigation reveals that the cause of an unfavorable direct labor efficiency variance is the use of lower quality direct materials than are usually used. Who is responsi-ble? What corrective action would likely be taken?

3. Suppose that investigation reveals that the cause of a significant favorable direct labor efficiency variance is attributable to a new approach to manufacturing that takes less labor time but causes more direct materials waste. Upon examining the direct materials usage variance, it is discovered to be unfavorable, and it is larger than the favorable direct labor efficiency variance. Who is responsible? What action should be taken? How would your answer change if the unfavorable variance were smaller than the favorable?

Madison Company uses the following rule to determine whether direct labor efficiency variances ought to be investigated. A direct labor efficiency variance will be investigated anytime the amount exceeds the lesser of $12,000 or 10 percent of the standard labor cost. Reports for the past five weeks provided the following information:

Required:

1. Using the rule provided, identify the cases that will be investigated.

2. Suppose that investigation reveals that the cause of an unfavorable direct labor efficiency variance is the use of lower quality direct materials than are usually used. Who is responsi-ble? What corrective action would likely be taken?

3. Suppose that investigation reveals that the cause of a significant favorable direct labor efficiency variance is attributable to a new approach to manufacturing that takes less labor time but causes more direct materials waste. Upon examining the direct materials usage variance, it is discovered to be unfavorable, and it is larger than the favorable direct labor efficiency variance. Who is responsible? What action should be taken? How would your answer change if the unfavorable variance were smaller than the favorable?

Question

Question

Question

Question

Question

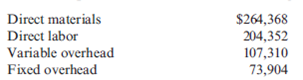

Flexible Budget, Standard Cost Variances, T-Accounts

Ingles Company manufactures external hard drives. At the beginning of the period, the following plans for production and costs were revealed:

During the year, 24,800 units were produced and sold. The following actual costs were incurred:

There were no beginning or ending inventories of direct materials. The direct materials price variance was $10,168 unfavorable. In producing the 24,800 units, a total of 12,772 hours were worked, 3 percent more hours than the standard allowed for the actual output. Overhead costs are applied to production using direct labor hours.

Required:

1. Prepare a performance report comparing expected costs to actual costs.

2. Determine the following:

a. Direct materials usage variance

b. Direct labor rate variance

c. Direct labor usage variance

d. Fixed overhead spending and volume variances

e. Variable overhead spending and efficiency variances

3. Use T-accounts to show the flow of costs through the system. In showing the flow, you do not need to show detailed overhead variances. Show only the over- and underapplied variances for fixed and variable overhead.

Ingles Company manufactures external hard drives. At the beginning of the period, the following plans for production and costs were revealed:

During the year, 24,800 units were produced and sold. The following actual costs were incurred:

There were no beginning or ending inventories of direct materials. The direct materials price variance was $10,168 unfavorable. In producing the 24,800 units, a total of 12,772 hours were worked, 3 percent more hours than the standard allowed for the actual output. Overhead costs are applied to production using direct labor hours.

Required:

1. Prepare a performance report comparing expected costs to actual costs.

2. Determine the following:

a. Direct materials usage variance

b. Direct labor rate variance

c. Direct labor usage variance

d. Fixed overhead spending and volume variances

e. Variable overhead spending and efficiency variances

3. Use T-accounts to show the flow of costs through the system. In showing the flow, you do not need to show detailed overhead variances. Show only the over- and underapplied variances for fixed and variable overhead.

Question

Question

Question

Question

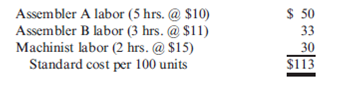

Standard Costing: Planned Variances

As part of its cost control program, Tracer Company uses a standard costing system for all manufactured items. The standard cost for each item is established at the beginning of the fiscal year, and the standards are not revised until the beginning of the next fiscal year. Changes in costs, caused during the year by changes in direct materials or direct labor inputs or by changes in the manufacturing process, are recognized as they occur by the inclusion of planned variances in Tracer's monthly operating budgets.

The following direct labor standard was established for one of Tracer's products, effective June 1, 2012, the beginning of the fiscal year:

The standard was based on the direct labor being performed by a team consisting of five persons with Assembler A skills, three persons with Assembler B skills, and two persons with machinist skills; this team represents the most efficient use of the company's skilled employees. The standard also assumed that the quality of direct materials that had been used in prior years would be available for the coming year.

For the first seven months of the fiscal year, actual manufacturing costs at Tracer have been within the standards established. However, the company has received a significant increase in orders, and there is an insufficient number of skilled workers to meet the increased production. Therefore, beginning in January, the production teams will consist of eight persons with Assembler A skills, one person with Assembler B skills, and one person with machinist skills. The reorganized teams will work more slowly than the normal teams, and as a result, only 80 units will be produced in the same time period in which 100 units would normally be produced. Faulty work has never been a cause for units to be rejected in the final inspection process, and it is not expected to be a cause for rejection with the reorganized teams.

Furthermore, Tracer has been notified by its direct materials supplier that lower-quality direct materials will be supplied beginning January 1. Normally, one unit of direct materials is required for each good unit produced, and no units are lost due to defective direct materials. Tracer estimates that 6 percent of the units manufactured after January 1 will be rejected in the final inspection process due to defective direct materials.

Required:

1. Determine the number of units of lower quality direct materials that Tracer Company must enter into production in order to produce 47,000 good finished units.

2. How many hours of each class of direct labor must be used to manufacture 47,000 good finished units?

3. Determine the amount that should be included in Tracer's January operating budget for the planned direct labor variance caused by the reorganization of the direct labor teams and the lower quality direct materials. ( CMA adapted )

As part of its cost control program, Tracer Company uses a standard costing system for all manufactured items. The standard cost for each item is established at the beginning of the fiscal year, and the standards are not revised until the beginning of the next fiscal year. Changes in costs, caused during the year by changes in direct materials or direct labor inputs or by changes in the manufacturing process, are recognized as they occur by the inclusion of planned variances in Tracer's monthly operating budgets.

The following direct labor standard was established for one of Tracer's products, effective June 1, 2012, the beginning of the fiscal year:

The standard was based on the direct labor being performed by a team consisting of five persons with Assembler A skills, three persons with Assembler B skills, and two persons with machinist skills; this team represents the most efficient use of the company's skilled employees. The standard also assumed that the quality of direct materials that had been used in prior years would be available for the coming year.

For the first seven months of the fiscal year, actual manufacturing costs at Tracer have been within the standards established. However, the company has received a significant increase in orders, and there is an insufficient number of skilled workers to meet the increased production. Therefore, beginning in January, the production teams will consist of eight persons with Assembler A skills, one person with Assembler B skills, and one person with machinist skills. The reorganized teams will work more slowly than the normal teams, and as a result, only 80 units will be produced in the same time period in which 100 units would normally be produced. Faulty work has never been a cause for units to be rejected in the final inspection process, and it is not expected to be a cause for rejection with the reorganized teams.

Furthermore, Tracer has been notified by its direct materials supplier that lower-quality direct materials will be supplied beginning January 1. Normally, one unit of direct materials is required for each good unit produced, and no units are lost due to defective direct materials. Tracer estimates that 6 percent of the units manufactured after January 1 will be rejected in the final inspection process due to defective direct materials.

Required:

1. Determine the number of units of lower quality direct materials that Tracer Company must enter into production in order to produce 47,000 good finished units.

2. How many hours of each class of direct labor must be used to manufacture 47,000 good finished units?

3. Determine the amount that should be included in Tracer's January operating budget for the planned direct labor variance caused by the reorganization of the direct labor teams and the lower quality direct materials. ( CMA adapted )

Question

Using Control Limits to Determine When to Investigate a Variance

Kavallia Company set a standard cost for one item at $328,000; allowable deviation is ±$14,500. Actual costs for the past six months are as follows:

Required:

1. Calculate the variance from standard for each month. Which months should be investigated?

2. What if the company uses a two-part rule for investigating variances? The allowable deviation is the lesser of 4 percent of the standard amount or $14,500. Now which months should be investigated?

Kavallia Company set a standard cost for one item at $328,000; allowable deviation is ±$14,500. Actual costs for the past six months are as follows:

Required:

1. Calculate the variance from standard for each month. Which months should be investigated?

2. What if the company uses a two-part rule for investigating variances? The allowable deviation is the lesser of 4 percent of the standard amount or $14,500. Now which months should be investigated?

Question

Question

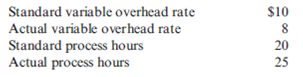

(2011 CPA Exam) A company has gathered the following information from a recent production run:

What is the company's variable overhead spending variance?

A) $50 unfavorable

B) $50 favorable

C) $40 unfavorable

D) $40 favorable

What is the company's variable overhead spending variance?

A) $50 unfavorable

B) $50 favorable

C) $40 unfavorable

D) $40 favorable

Question

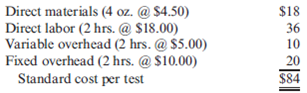

Variance Analysis in a Process-Costing Setting (Chapter 6 Required), Service Firm

Aspen Medical Laboratory performs comprehensive blood tests for physicians and clinics throughout the Southwest. Aspen uses a standard process-costing system for its comprehensive blood work. Skilled technicians perform the blood tests. Because Aspen uses a standard costing system, equivalent units are calculated using the FIFO method. The standard cost sheet for the blood test follows (these standards were used throughout the calendar year):

For the month of November, Aspen reported the following actual results:

a. Beginning work in process: 1,250 tests, 60 percent complete

b. Tests started: 25,000

c. Ending work in process: 2,500 tests, 40 percent complete

d. Direct labor: 47,000 hours at $19 per hour

e. Direct materials purchased and used: 102,000 at $4.25 per ounce

f. Variable overhead: $144,000

g. Fixed overhead: $300,000

h. Direct materials are added at the beginning of the process.

Required:

1. Explain why the FIFO method is used for process costing when a standard costing system has been adopted.

2. Calculate the cost of goods transferred out (tests completed and transferred out) for the month of November. Does standard costing simplify process costing? Explain.

3. Calculate price and quantity variances for direct materials and direct labor.

Aspen Medical Laboratory performs comprehensive blood tests for physicians and clinics throughout the Southwest. Aspen uses a standard process-costing system for its comprehensive blood work. Skilled technicians perform the blood tests. Because Aspen uses a standard costing system, equivalent units are calculated using the FIFO method. The standard cost sheet for the blood test follows (these standards were used throughout the calendar year):

For the month of November, Aspen reported the following actual results:

a. Beginning work in process: 1,250 tests, 60 percent complete

b. Tests started: 25,000

c. Ending work in process: 2,500 tests, 40 percent complete

d. Direct labor: 47,000 hours at $19 per hour

e. Direct materials purchased and used: 102,000 at $4.25 per ounce

f. Variable overhead: $144,000

g. Fixed overhead: $300,000

h. Direct materials are added at the beginning of the process.

Required:

1. Explain why the FIFO method is used for process costing when a standard costing system has been adopted.

2. Calculate the cost of goods transferred out (tests completed and transferred out) for the month of November. Does standard costing simplify process costing? Explain.

3. Calculate price and quantity variances for direct materials and direct labor.

Question

Question

Question

A company uses a standard costing system. At the end of the current year, the company provides the following overhead information.

What amount is the volume variance?

A) $2,500 favorable

B) $2,500 unfavorable

C) $5,000 unfavorable

D) $5,000 favorable

What amount is the volume variance?

A) $2,500 favorable

B) $2,500 unfavorable

C) $5,000 unfavorable

D) $5,000 favorable

Question

Setting Standards, Calculating and Using Variances

Leather Works is a family-owned maker of leather travel bags and briefcases located in the northeastern part of the United States. Foreign competition has forced its owner, Heather Gray, to explore new ways to meet the competition. One of her cousins, Wallace Hayes, who recently graduated from college with a major in accounting, told her about the use of cost variance analysis to learn about efficiencies of production.

In May 2012, Heather asked Matt Jones, chief accountant, and Alfred Prudest, production manager, to implement a standard costing system. Matt and Alfred, in turn, retained Shannon Leikam, an accounting professor at Harding's College, to set up a standard costing system by using information supplied to her by Matt's and Alfred's staff. To verify that the information was accurate, Shannon visited the plant and measured workers' output using time and motion studies. During those visits, she was not accompanied by either Matt or Alfred, and the workers knew about Shannon's schedule in advance. The cost system was implemented in June 2012.

Recently, the following dialogue took place among Heather, Matt, and Alfred:

HEATHER : How is the business performing?

ALFRED : You know, we are producing a lot more than we used to, thanks to the contract that you helped obtain from Lean, Inc., for laptop covers. (Lean is a national supplier of computer accessories.)

MATT : Thank goodness for that new product. It has kept us from sinking even more due to the inroads into our business made by those foreign suppliers of leather goods.

HEATHER : What about the standard costing system?

MATT : The variances are mostly favorable, except for the first few months when the supplier of leather started charging more.

HEATHER : How did the union members take to the standards?

ALFRED : Not bad. They grumbled a bit at first, but they have taken it in stride. We've consistently shown favorable direct labor efficiency variances and direct materials usage variances. The direct labor rate variance has been flat.

MATT : It should be since direct labor rates are negotiated by the union representative at the start of the year and remain the same for the entire year.

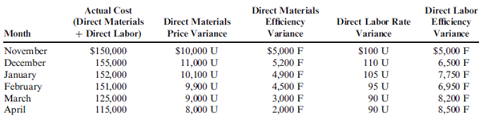

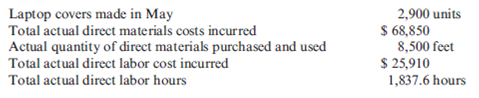

HEATHER : Matt, would you send me the variance report for laptop covers immediately?

The following chart summarizes the direct materials and direct labor variances from November 2012 through April 2013 (extracted from the report provided by Matt). Standards for each laptop cover are as follows:

a. Three feet of direct materials at $7.50 per foot

b. Forty-five minutes of direct labor at $14 per hour

In addition, the data for May 2013, but not the variances for the month, are as follows:

Actual direct labor cost per hour exceeded the budgeted rate by $0.10 per hour.

Required:

1. For May 2013, calculate the price and quantity variances for direct labor and direct materials.

2. Discuss the trend of the direct materials and labor variances.

3. What type of actions must the workers have taken during the period they were being observed for the setting of standards?

4. What can be done to ensure that the standards are set correctly? ( CMA adapted )

Leather Works is a family-owned maker of leather travel bags and briefcases located in the northeastern part of the United States. Foreign competition has forced its owner, Heather Gray, to explore new ways to meet the competition. One of her cousins, Wallace Hayes, who recently graduated from college with a major in accounting, told her about the use of cost variance analysis to learn about efficiencies of production.

In May 2012, Heather asked Matt Jones, chief accountant, and Alfred Prudest, production manager, to implement a standard costing system. Matt and Alfred, in turn, retained Shannon Leikam, an accounting professor at Harding's College, to set up a standard costing system by using information supplied to her by Matt's and Alfred's staff. To verify that the information was accurate, Shannon visited the plant and measured workers' output using time and motion studies. During those visits, she was not accompanied by either Matt or Alfred, and the workers knew about Shannon's schedule in advance. The cost system was implemented in June 2012.

Recently, the following dialogue took place among Heather, Matt, and Alfred:

HEATHER : How is the business performing?

ALFRED : You know, we are producing a lot more than we used to, thanks to the contract that you helped obtain from Lean, Inc., for laptop covers. (Lean is a national supplier of computer accessories.)

MATT : Thank goodness for that new product. It has kept us from sinking even more due to the inroads into our business made by those foreign suppliers of leather goods.

HEATHER : What about the standard costing system?

MATT : The variances are mostly favorable, except for the first few months when the supplier of leather started charging more.

HEATHER : How did the union members take to the standards?

ALFRED : Not bad. They grumbled a bit at first, but they have taken it in stride. We've consistently shown favorable direct labor efficiency variances and direct materials usage variances. The direct labor rate variance has been flat.

MATT : It should be since direct labor rates are negotiated by the union representative at the start of the year and remain the same for the entire year.

HEATHER : Matt, would you send me the variance report for laptop covers immediately?

The following chart summarizes the direct materials and direct labor variances from November 2012 through April 2013 (extracted from the report provided by Matt). Standards for each laptop cover are as follows:

a. Three feet of direct materials at $7.50 per foot

b. Forty-five minutes of direct labor at $14 per hour

In addition, the data for May 2013, but not the variances for the month, are as follows:

Actual direct labor cost per hour exceeded the budgeted rate by $0.10 per hour.

Required:

1. For May 2013, calculate the price and quantity variances for direct labor and direct materials.

2. Discuss the trend of the direct materials and labor variances.

3. What type of actions must the workers have taken during the period they were being observed for the setting of standards?

4. What can be done to ensure that the standards are set correctly? ( CMA adapted )

Question

Closing the Balances in the Variance Accounts at the End of the Year

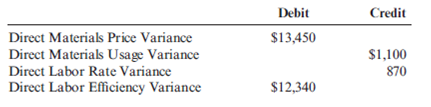

Yohan Company has the following balances in its direct materials and direct labor variance accounts at year-end:

Unadjusted Cost of Goods Sold equals $1,500,000, unadjusted Work in Process equals $236,000, and unadjusted Finished Goods equals $180,000.

Required:

1. Assume that the ending balances in the variance accounts are immaterial and prepare the journal entries to close them to Cost of Goods Sold. What is the adjusted balance in Cost of Goods Sold after closing out the variances?

2. What if any ending balance in a variance account that exceeds $10,000 is considered material? Close the immaterial variance accounts to Cost of Goods Sold and prorate the material variances among Cost of Goods Sold, Work in Process, and Finished Goods on the basis of prime costs in these accounts. The prime cost in Cost of Goods Sold is $1,050,000, the prime cost in Work in Process is $165,200, and the prime cost in Finished Goods is $126,000. What are the adjusted balances in Work in Process, Finished Goods, and Cost of Goods Sold after closing out all variances? (Round ratios to four significant digits. Round journal entries to the nearest dollar.)

Yohan Company has the following balances in its direct materials and direct labor variance accounts at year-end:

Unadjusted Cost of Goods Sold equals $1,500,000, unadjusted Work in Process equals $236,000, and unadjusted Finished Goods equals $180,000.

Required:

1. Assume that the ending balances in the variance accounts are immaterial and prepare the journal entries to close them to Cost of Goods Sold. What is the adjusted balance in Cost of Goods Sold after closing out the variances?

2. What if any ending balance in a variance account that exceeds $10,000 is considered material? Close the immaterial variance accounts to Cost of Goods Sold and prorate the material variances among Cost of Goods Sold, Work in Process, and Finished Goods on the basis of prime costs in these accounts. The prime cost in Cost of Goods Sold is $1,050,000, the prime cost in Work in Process is $165,200, and the prime cost in Finished Goods is $126,000. What are the adjusted balances in Work in Process, Finished Goods, and Cost of Goods Sold after closing out all variances? (Round ratios to four significant digits. Round journal entries to the nearest dollar.)

Question

Question

(2010 CPA Exam) Relevant information for material A follows:

What was the direct material quantity variance for material A?

A) $2,000 favorable

B) $1,900 favorable

C) $1,900 unfavorable

D) $2,000 unfavorable

What was the direct material quantity variance for material A?

A) $2,000 favorable

B) $1,900 favorable

C) $1,900 unfavorable

D) $2,000 unfavorable

Question

Question

Computation of Inputs Allowed, Direct Materials and Direct Labor

During the year, Dorner Company produced 280,000 lathe components for industrial metal working machinery. Dorner's direct materials and direct labor standards per unit are as follows:

Required:

1. Compute the standard pounds of direct materials allowed for the production of 280,000 units.

2. Compute the standard direct labor hours allowed for the production of 280,000 units.

During the year, Dorner Company produced 280,000 lathe components for industrial metal working machinery. Dorner's direct materials and direct labor standards per unit are as follows:

Required:

1. Compute the standard pounds of direct materials allowed for the production of 280,000 units.

2. Compute the standard direct labor hours allowed for the production of 280,000 units.

Question

Question

Calculating the Total Overhead Variance

Standish Company manufactures consumer products and provided the following information for the month of February:

Required:

1. Calculate the total variable overhead variance.

2. What if actual production had been 129,600 units? How would that affect the total variable overhead variance?

Standish Company manufactures consumer products and provided the following information for the month of February:

Required:

1. Calculate the total variable overhead variance.

2. What if actual production had been 129,600 units? How would that affect the total variable overhead variance?

Question

Question

Standard Costs, Decomposition of Budget Variances, Direct Materials and Direct Labor

Haversham Corporation produces dress shirts. The company uses a standard costing system and has set the following standards for direct materials and direct labor (for one shirt):

During the year, Haversham produced 9,800 shirts. The actual fabric purchased was 14,600 yards at $2.74 per yard. There were no beginning or ending inventories of fabric. Actual direct labor was 10,900 hours at $19.60 per hour.

Required:

1. Compute the costs of fabric and direct labor that should have been incurred for the production of 9,800 shirts.

2. Compute the total budget variances for direct materials and direct labor.

3. Break down the total budget variance for direct materials into a price variance and a usage variance. Prepare the journal entries associated with these variances.

4. Break down the total budget variance for direct labor into a rate variance and an efficiency variance. Prepare the journal entries associated with these variances.

Haversham Corporation produces dress shirts. The company uses a standard costing system and has set the following standards for direct materials and direct labor (for one shirt):

During the year, Haversham produced 9,800 shirts. The actual fabric purchased was 14,600 yards at $2.74 per yard. There were no beginning or ending inventories of fabric. Actual direct labor was 10,900 hours at $19.60 per hour.

Required:

1. Compute the costs of fabric and direct labor that should have been incurred for the production of 9,800 shirts.

2. Compute the total budget variances for direct materials and direct labor.

3. Break down the total budget variance for direct materials into a price variance and a usage variance. Prepare the journal entries associated with these variances.

4. Break down the total budget variance for direct labor into a rate variance and an efficiency variance. Prepare the journal entries associated with these variances.

Question

Question

Direct Materials and Direct Labor Variances

Zoller Company produces a dark chocolate candy bar. Recently, the company adopted the following standards for one bar of the candy:

During the first week of operation, the company experienced the following actual results:

a. Bars produced: 143,000.

b. Ounces of direct materials purchased: 901,200 ounces at $0.21 per ounce.

c. There are no beginning or ending inventories of direct materials.

d. Direct labor: 11,300 hours at $17.30.

Required:

1. Compute price and usage variances for direct materials.

2. Compute the rate variance and the efficiency variance for direct labor.

3. Prepare the journal entries associated with direct materials and direct labor.

Zoller Company produces a dark chocolate candy bar. Recently, the company adopted the following standards for one bar of the candy:

During the first week of operation, the company experienced the following actual results:

a. Bars produced: 143,000.

b. Ounces of direct materials purchased: 901,200 ounces at $0.21 per ounce.

c. There are no beginning or ending inventories of direct materials.

d. Direct labor: 11,300 hours at $17.30.

Required:

1. Compute price and usage variances for direct materials.

2. Compute the rate variance and the efficiency variance for direct labor.

3. Prepare the journal entries associated with direct materials and direct labor.

Question

Overhead Application, Overhead Variances, Journal Entries

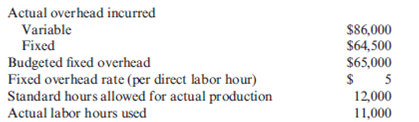

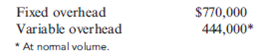

Plimpton Company produces countertop ovens. Plimpton uses a standard costing system. The standard costing system relies on direct labor hours to assign overhead costs to production. The direct labor standard indicates that two direct labor hours should be used for every oven produced. The normal production volume is 100,000 units. The budgeted overhead for the coming year is as follows:

Plimpton applies overhead on the basis of direct labor hours.

During the year, Plimpton produced 97,000 units, worked 196,000 direct labor hours, and incurred actual fixed overhead costs of $780,000 and actual variable overhead costs of $435,600.

Required:

1. Calculate the standard fixed overhead rate and the standard variable overhead rate.

2. Compute the applied fixed overhead and the applied variable overhead. What is the total fixed overhead variance? Total variable overhead variance?

3. Break down the total fixed overhead variance into a spending variance and a volume variance. Discuss the significance of each.

4. Compute the variable overhead spending and efficiency variances. Discuss the significance of each.

5. Now assume that Plimpton's cost accounting system reveals only the total actual overhead. In this case, a three-variance analysis can be performed. Using the relationships between a three- and four-variance analysis, indicate the values for the three overhead variances.

6. Prepare the journal entries that would be related to fixed and variable overhead during the year and at the end of the year. Assume variances are closed to Cost of Goods Sold.

Plimpton Company produces countertop ovens. Plimpton uses a standard costing system. The standard costing system relies on direct labor hours to assign overhead costs to production. The direct labor standard indicates that two direct labor hours should be used for every oven produced. The normal production volume is 100,000 units. The budgeted overhead for the coming year is as follows:

Plimpton applies overhead on the basis of direct labor hours.

During the year, Plimpton produced 97,000 units, worked 196,000 direct labor hours, and incurred actual fixed overhead costs of $780,000 and actual variable overhead costs of $435,600.

Required:

1. Calculate the standard fixed overhead rate and the standard variable overhead rate.

2. Compute the applied fixed overhead and the applied variable overhead. What is the total fixed overhead variance? Total variable overhead variance?

3. Break down the total fixed overhead variance into a spending variance and a volume variance. Discuss the significance of each.

4. Compute the variable overhead spending and efficiency variances. Discuss the significance of each.

5. Now assume that Plimpton's cost accounting system reveals only the total actual overhead. In this case, a three-variance analysis can be performed. Using the relationships between a three- and four-variance analysis, indicate the values for the three overhead variances.

6. Prepare the journal entries that would be related to fixed and variable overhead during the year and at the end of the year. Assume variances are closed to Cost of Goods Sold.

Question

Question

Question

Direct Materials, Direct Labor, and Overhead Variances, Journal Entries

Algers Company produces dry fertilizer. At the beginning of the year, Algers had the following standard cost sheet:

Algers computes its overhead rates using practical volume, which is 54,000 units. The actual results for the year are as follows:

a. Units produced: 53,000

b. Direct materials purchased: 274,000 pounds at $2.50 per pound

c. Direct materials used: 270,300 pounds

d. Direct labor: 40,100 hours at $17.95 per hour

e. Fixed overhead: $161,700

f. Variable overhead: $122,000

Required:

1. Compute price and usage variances for direct materials.

2. Compute the direct labor rate and labor efficiency variances.

3. Compute the fixed overhead spending and volume variances. Interpret the volume variance.

4. Compute the variable overhead spending and efficiency variances.

5. Prepare journal entries for the following:

a. The purchase of direct materials

b. The issuance of direct materials to production (Work in Process)

c. The addition of direct labor to Work in Process

d. The addition of overhead to Work in Process

e. The incurrence of actual overhead costs

f. Closing out of variances to Cost of Goods Sold

Algers Company produces dry fertilizer. At the beginning of the year, Algers had the following standard cost sheet:

Algers computes its overhead rates using practical volume, which is 54,000 units. The actual results for the year are as follows:

a. Units produced: 53,000

b. Direct materials purchased: 274,000 pounds at $2.50 per pound

c. Direct materials used: 270,300 pounds

d. Direct labor: 40,100 hours at $17.95 per hour

e. Fixed overhead: $161,700

f. Variable overhead: $122,000

Required:

1. Compute price and usage variances for direct materials.

2. Compute the direct labor rate and labor efficiency variances.

3. Compute the fixed overhead spending and volume variances. Interpret the volume variance.

4. Compute the variable overhead spending and efficiency variances.

5. Prepare journal entries for the following:

a. The purchase of direct materials

b. The issuance of direct materials to production (Work in Process)

c. The addition of direct labor to Work in Process

d. The addition of overhead to Work in Process

e. The incurrence of actual overhead costs

f. Closing out of variances to Cost of Goods Sold

Question

Question

Question

Solving for Unknowns

Misterio Company uses a standard costing system. During the past quarter, the following variances were computed:

Misterio applies variable overhead using a standard rate of $2 per direct labor hour allowed. Two direct labor hours are allowed per unit produced. (Only one type of product is manufactured.) During the quarter, Misterio used 30 percent more direct labor hours than should have been used.

Required:

1. What were the actual direct labor hours worked? The total hours allowed?

2. What is the standard hourly rate for direct labor? The actual hourly rate?

3. How many actual units were produced?

Misterio Company uses a standard costing system. During the past quarter, the following variances were computed:

Misterio applies variable overhead using a standard rate of $2 per direct labor hour allowed. Two direct labor hours are allowed per unit produced. (Only one type of product is manufactured.) During the quarter, Misterio used 30 percent more direct labor hours than should have been used.

Required:

1. What were the actual direct labor hours worked? The total hours allowed?

2. What is the standard hourly rate for direct labor? The actual hourly rate?

3. How many actual units were produced?

Question

Calculating the Fixed Overhead Spending and Volume Variances

Standish Company manufactures consumer products and provided the following information for the month of February:

Required:

1. Calculate the fixed overhead spending variance using the formula approach.

2. Calculate the volume variance using the formula approach.

3. Calculate the fixed overhead spending variance and volume variance using the three-pronged graphical approach.

4. What if 129,600 units had actually been produced in February? What impact would that have had on the fixed overhead spending variance? On the volume variance?

Standish Company manufactures consumer products and provided the following information for the month of February:

Required:

1. Calculate the fixed overhead spending variance using the formula approach.

2. Calculate the volume variance using the formula approach.

3. Calculate the fixed overhead spending variance and volume variance using the three-pronged graphical approach.

4. What if 129,600 units had actually been produced in February? What impact would that have had on the fixed overhead spending variance? On the volume variance?

Question

Question

Basic Variance Analysis, Revision of Standards, Journal Entries

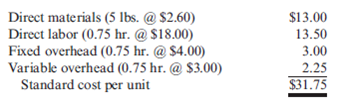

Petrillo Company produces engine parts for large motors. The company uses a standard cost system for production costing and control. The standard cost sheet for one of its higher volume products (a valve) is as follows:

During the year, Petrillo had the following activity related to valve production:

a. Production of valves totaled 20,600 units.

b. A total of 135,400 pounds of direct materials was purchased at $5.36 per pound.

c. There were 10,000 pounds of direct materials in beginning inventory (carried at $5.40 per pound). There was no ending inventory.

d. The company used 36,500 direct labor hours at a total cost of $656,270.

e. Actual fixed overhead totaled $110,000.

f. Actual variable overhead totaled $168,000.

Petrillo produces all of its valves in a single plant. Normal activity is 20,000 units per year. Standard overhead rates are computed based on normal activity measured in standard direct labor hours.

Required:

1. Compute the direct materials price and usage variances.

2. Compute the direct labor rate and efficiency variances.

3. Compute overhead variances using a two-variance analysis.

4. Compute overhead variances using a four-variance analysis.

5. Assume that the purchasing agent for the valve plant purchased a lower-quality direct material from a new supplier. Would you recommend that the company continue to use this cheaper direct material? If so, what standards would likely need revision to reflect this decision? Assume that the end product's quality is not significantly affected.

6. Prepare all possible journal entries (assuming a four-variance analysis of overhead variances).

Petrillo Company produces engine parts for large motors. The company uses a standard cost system for production costing and control. The standard cost sheet for one of its higher volume products (a valve) is as follows:

During the year, Petrillo had the following activity related to valve production:

a. Production of valves totaled 20,600 units.

b. A total of 135,400 pounds of direct materials was purchased at $5.36 per pound.

c. There were 10,000 pounds of direct materials in beginning inventory (carried at $5.40 per pound). There was no ending inventory.

d. The company used 36,500 direct labor hours at a total cost of $656,270.

e. Actual fixed overhead totaled $110,000.

f. Actual variable overhead totaled $168,000.

Petrillo produces all of its valves in a single plant. Normal activity is 20,000 units per year. Standard overhead rates are computed based on normal activity measured in standard direct labor hours.

Required:

1. Compute the direct materials price and usage variances.

2. Compute the direct labor rate and efficiency variances.

3. Compute overhead variances using a two-variance analysis.

4. Compute overhead variances using a four-variance analysis.

5. Assume that the purchasing agent for the valve plant purchased a lower-quality direct material from a new supplier. Would you recommend that the company continue to use this cheaper direct material? If so, what standards would likely need revision to reflect this decision? Assume that the end product's quality is not significantly affected.

6. Prepare all possible journal entries (assuming a four-variance analysis of overhead variances).

Question

Question

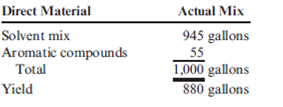

Direct Materials Mix and Yield Variances

Chypre, Inc., produces a cologne mist using a solvent mix (water and pure alcohol) and aromatic compounds (the scent base) that it sells to other companies for bottling and sale to consumers. Chypre developed the following standard cost sheet:

On May 2, Chypre produced a batch of 1,000 gallons with the following actual results:

Required:

1. Calculate the yield ratio.

2. Calculate the standard cost per unit of the yield. (Round to the nearest cent.)

3. Calculate the direct materials yield variance. (Round to the nearest cent.)

4. Calculate the direct materials mix variance. (Round to the nearest cent.)

Chypre, Inc., produces a cologne mist using a solvent mix (water and pure alcohol) and aromatic compounds (the scent base) that it sells to other companies for bottling and sale to consumers. Chypre developed the following standard cost sheet:

On May 2, Chypre produced a batch of 1,000 gallons with the following actual results:

Required:

1. Calculate the yield ratio.

2. Calculate the standard cost per unit of the yield. (Round to the nearest cent.)

3. Calculate the direct materials yield variance. (Round to the nearest cent.)

4. Calculate the direct materials mix variance. (Round to the nearest cent.)

Question

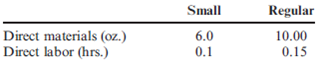

Unit Costs, Multiple Products, Variance Analysis, Journal Entries

Business Specialty, Inc., manufactures two staplers: small and regular. The standard quantities of direct labor and direct materials per unit for the year are as follows:

The standard price paid per pound of direct materials is $1.60. The standard rate for labor is $8.00. Overhead is applied on the basis of direct labor hours. A plantwide rate is used. Budgeted overhead for the year is as follows:

The company expects to work 12,000 direct labor hours during the year; standard overhead rates are computed using this activity level. For every small stapler produced, the company produces two regular staplers.

Actual operating data for the year are as follows:

a. Units produced: small staplers, 35,000; regular staplers, 70,000.

b. Direct materials purchased and used: 56,000 pounds at $1.55-13,000 for the small stapler and 43,000 for the regular stapler. There were no beginning or ending direct materials inventories.

c. Direct labor: 14,800 hours-3,600 hours for the small stapler and 11,200 hours for the regular stapler. Total cost of direct labor: $114,700.

d. Variable overhead: $607,500.

e. Fixed overhead: $350,000.

Required:

1. Prepare a standard cost sheet showing the unit cost for each product.

2. Compute the direct materials price and usage variances for each product. Prepare journal entries to record direct materials activity.

3. Compute the direct labor rate and efficiency variances for each product. Prepare journal entries to record direct labor activity.

4. Compute the variances for fixed and variable overhead. Prepare journal entries to record overhead activity. All variances are closed to Cost of Goods Sold.

5. Assume that you know only the total direct materials used for both products and the total direct labor hours used for both products. Can you compute the total direct materials and direct labor usage variances? Explain.

Business Specialty, Inc., manufactures two staplers: small and regular. The standard quantities of direct labor and direct materials per unit for the year are as follows:

The standard price paid per pound of direct materials is $1.60. The standard rate for labor is $8.00. Overhead is applied on the basis of direct labor hours. A plantwide rate is used. Budgeted overhead for the year is as follows:

The company expects to work 12,000 direct labor hours during the year; standard overhead rates are computed using this activity level. For every small stapler produced, the company produces two regular staplers.

Actual operating data for the year are as follows:

a. Units produced: small staplers, 35,000; regular staplers, 70,000.

b. Direct materials purchased and used: 56,000 pounds at $1.55-13,000 for the small stapler and 43,000 for the regular stapler. There were no beginning or ending direct materials inventories.

c. Direct labor: 14,800 hours-3,600 hours for the small stapler and 11,200 hours for the regular stapler. Total cost of direct labor: $114,700.

d. Variable overhead: $607,500.

e. Fixed overhead: $350,000.

Required:

1. Prepare a standard cost sheet showing the unit cost for each product.

2. Compute the direct materials price and usage variances for each product. Prepare journal entries to record direct materials activity.

3. Compute the direct labor rate and efficiency variances for each product. Prepare journal entries to record direct labor activity.

4. Compute the variances for fixed and variable overhead. Prepare journal entries to record overhead activity. All variances are closed to Cost of Goods Sold.

5. Assume that you know only the total direct materials used for both products and the total direct labor hours used for both products. Can you compute the total direct materials and direct labor usage variances? Explain.

Question

Question

Calculating the Direct Materials Mix Variance

Mangia Pizza Company makes frozen pizzas that are sold through grocery stores. Mangia developed the following standard mix for spreading on premade pizza shells to produce 16 giant-size sausage pizzas.

Mangia put a batch of 2,000 pounds of direct materials (enough for 800 frozen sausage pizzas) into process. Of the total, 700 pounds were tomato sauce, 840 pounds were cheese, and the remaining 460 pounds were sausage. The actual yield was 780 pizzas.

Required:

1. Calculate the standard mix (SM) in pounds for tomato sauce, for cheese, and for sausage.

2. Calculate the mix variance.

3. Calculate the actual proportion used of tomato sauce, cheese, and sausage. Use these results to explain the direction (favorable or unfavorable) of the mix variance.

4. What if of the total 2,000 pounds of ingredients put into process, 700 pounds were tomato sauce, 700 pounds were cheese, and 600 pounds were sausage? How would that affect themix variance?

Mangia Pizza Company makes frozen pizzas that are sold through grocery stores. Mangia developed the following standard mix for spreading on premade pizza shells to produce 16 giant-size sausage pizzas.

Mangia put a batch of 2,000 pounds of direct materials (enough for 800 frozen sausage pizzas) into process. Of the total, 700 pounds were tomato sauce, 840 pounds were cheese, and the remaining 460 pounds were sausage. The actual yield was 780 pizzas.

Required:

1. Calculate the standard mix (SM) in pounds for tomato sauce, for cheese, and for sausage.

2. Calculate the mix variance.

3. Calculate the actual proportion used of tomato sauce, cheese, and sausage. Use these results to explain the direction (favorable or unfavorable) of the mix variance.

4. What if of the total 2,000 pounds of ingredients put into process, 700 pounds were tomato sauce, 700 pounds were cheese, and 600 pounds were sausage? How would that affect themix variance?

Question

Question

Direct Materials Usage Variance, Direct Materials Mix and Yield Variances

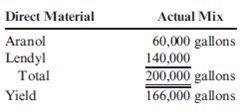

Vet-Pro, Inc., produces a veterinary grade anti-anxiety mixture for pets with behavioral problems. Two chemical solutions, Aranol and Lendyl, are mixed and heated to produce a chemical that is sold to companies that produce the anti-anxiety pills. The mixture is produced in batches and has the following standards:

During March, the following actual production information was provided:

Required:

1. Compute the direct materials mix and yield variances.

2. Compute the total direct materials usage variance for Aranol and Lendyl. Show that the total direct materials usage variance is equal to the sum of the direct materials mix and yield variances.

Vet-Pro, Inc., produces a veterinary grade anti-anxiety mixture for pets with behavioral problems. Two chemical solutions, Aranol and Lendyl, are mixed and heated to produce a chemical that is sold to companies that produce the anti-anxiety pills. The mixture is produced in batches and has the following standards:

During March, the following actual production information was provided:

Required:

1. Compute the direct materials mix and yield variances.

2. Compute the total direct materials usage variance for Aranol and Lendyl. Show that the total direct materials usage variance is equal to the sum of the direct materials mix and yield variances.

Question

Question

Question

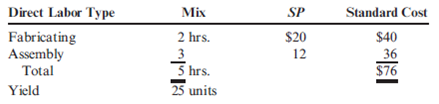

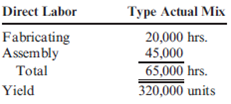

Direct Labor Mix and Yield Variances

Delano Company uses two types of direct labor for the manufacturing of its products: fabricating and assembly. Delano has developed the following standard mix for direct labor, where output is measured in number of circuit boards.

During the second week in April, Delano produced the following results:

Required:

1. Calculate the yield ratio.

2. Calculate the standard cost per unit of the yield.

3. Calculate the direct labor yield variance.

4. Calculate the direct labor mix variance.

Delano Company uses two types of direct labor for the manufacturing of its products: fabricating and assembly. Delano has developed the following standard mix for direct labor, where output is measured in number of circuit boards.

During the second week in April, Delano produced the following results:

Required:

1. Calculate the yield ratio.

2. Calculate the standard cost per unit of the yield.

3. Calculate the direct labor yield variance.

4. Calculate the direct labor mix variance.

Question

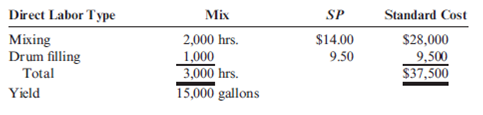

Direct Labor Efficiency Variance, Direct Labor Mix and Yield Variances

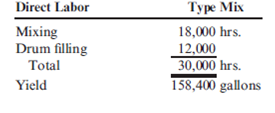

Refer to the data in Problem 9.34. Vet-Pro, Inc., also uses two different types of direct labor in producing the anti-anxiety mixture: mixing and drum-filling labor (the completed product is placed into 50-gallon drums). For each batch of 20,000 gallons of direct materials input, the following standards have been developed for direct labor:

The actual direct labor hours used for the output produced in March are also provided:

Required:

1. Compute the direct labor mix and yield variances.

2. Compute the total direct labor efficiency variance. Show that the total direct labor efficiency variance is equal to the sum of the direct labor mix and yield variances.

Refer to the data in Problem 9.34. Vet-Pro, Inc., also uses two different types of direct labor in producing the anti-anxiety mixture: mixing and drum-filling labor (the completed product is placed into 50-gallon drums). For each batch of 20,000 gallons of direct materials input, the following standards have been developed for direct labor:

The actual direct labor hours used for the output produced in March are also provided:

Required:

1. Compute the direct labor mix and yield variances.

2. Compute the total direct labor efficiency variance. Show that the total direct labor efficiency variance is equal to the sum of the direct labor mix and yield variances.

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/56

Play

Full screen (f)

Deck 9: Standard Costing: a Functional-Based Control Approach

1

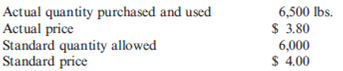

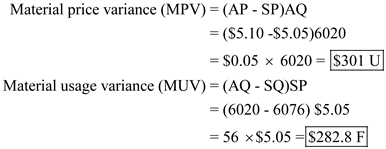

Calculating the Direct Materials Price Variance and the Direct Materials Usage Variance

Refer to Cornerstone Exercise 9.1. Guillermo's Oil and Lube Company provided the following information for the production of oil changes during the month of June:

Actual number of oil changes performed: 980

Actual number of quarts of oil used: 6,020 quarts

Actual price paid per quart of oil: $5.10

Standard price per quart of oil: $5.05

Required:

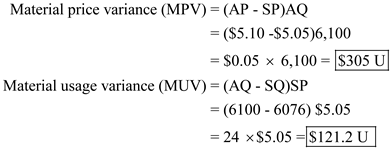

1. Calculate the direct materials price variance ( MPV ) and the direct materials usage variance ( MUV ) for June using the formula approach.

2. Calculate the direct materials price variance ( MPV ) and the direct materials usage variance ( MUV ) for June using the graphical approach.

3. Calculate the total direct materials variance for oil for June.

4. What if the actual number of quarts of oil purchased in June had been 6,100 quarts, and the materials price variance was calculated at the time of purchase? What would be the materials price variance ( MPV )? The materials usage variance ( MUV )?

Refer to Cornerstone Exercise 9.1. Guillermo's Oil and Lube Company provided the following information for the production of oil changes during the month of June:

Actual number of oil changes performed: 980

Actual number of quarts of oil used: 6,020 quarts

Actual price paid per quart of oil: $5.10

Standard price per quart of oil: $5.05

Required:

1. Calculate the direct materials price variance ( MPV ) and the direct materials usage variance ( MUV ) for June using the formula approach.

2. Calculate the direct materials price variance ( MPV ) and the direct materials usage variance ( MUV ) for June using the graphical approach.

3. Calculate the total direct materials variance for oil for June.

4. What if the actual number of quarts of oil purchased in June had been 6,100 quarts, and the materials price variance was calculated at the time of purchase? What would be the materials price variance ( MPV )? The materials usage variance ( MUV )?

1.To get material price variance, the difference between the actual price and standard price is to be multiplied with actual quantity. To compute material usage variance, the difference between the actual quantity and standard quantity is to be multiplied with standard price.

2.The graphical representation for the computation of MPV and MUV is as follows:

2.The graphical representation for the computation of MPV and MUV is as follows:

3.To compute total material variance, we need to take out the difference between actual price to produce actual quantity and standard price to produce the standard quantity.

3.To compute total material variance, we need to take out the difference between actual price to produce actual quantity and standard price to produce the standard quantity.

4.If the actual number of quarts purchased in June had been 6,100 quarts, and when the material price variance is calculated at the time of purchase, then AQ needs to be redefined as the actual quantity of direct material purchased, rather than actual direct material used. So,

4.If the actual number of quarts purchased in June had been 6,100 quarts, and when the material price variance is calculated at the time of purchase, then AQ needs to be redefined as the actual quantity of direct material purchased, rather than actual direct material used. So,

2.The graphical representation for the computation of MPV and MUV is as follows: 3.To compute total material variance, we need to take out the difference between actual price to produce actual quantity and standard price to produce the standard quantity. 4.If the actual number of quarts purchased in June had been 6,100 quarts, and when the material price variance is calculated at the time of purchase, then AQ needs to be redefined as the actual quantity of direct material purchased, rather than actual direct material used. So, 2

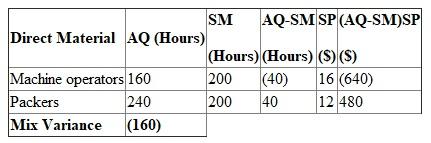

Calculating the Direct Labor Mix Variance

Mangia Pizza Company makes frozen pizzas that are sold through grocery stores. Mangia uses two types of direct labor: machine operators and packers. Mangia developed the following standard mix for spreading on premade pizza shells to produce 16 giant-size sausage pizzas.

Mangia's recent batch (designed to produce 400 pizzas) used 400 direct labor hours. Of the total, 160 were for machine operators, and the remaining 240 hours were for packers. The actual yield was 780 pizzas.

Required:

1. Calculate the standard mix (SM) in hours for machine operators and for packers.

2. Calculate the mix variance.

3. Calculate the actual proportion of hours worked by machine operators and by packers. Use these results to explain the direction (favorable or unfavorable) of the mix variance.

4. What if of the total 400 direct labor hours worked, 200 were worked by each type of direct labor? How would that affect the mix variance?

Mangia Pizza Company makes frozen pizzas that are sold through grocery stores. Mangia uses two types of direct labor: machine operators and packers. Mangia developed the following standard mix for spreading on premade pizza shells to produce 16 giant-size sausage pizzas.

Mangia's recent batch (designed to produce 400 pizzas) used 400 direct labor hours. Of the total, 160 were for machine operators, and the remaining 240 hours were for packers. The actual yield was 780 pizzas.

Required:

1. Calculate the standard mix (SM) in hours for machine operators and for packers.

2. Calculate the mix variance.

3. Calculate the actual proportion of hours worked by machine operators and by packers. Use these results to explain the direction (favorable or unfavorable) of the mix variance.

4. What if of the total 400 direct labor hours worked, 200 were worked by each type of direct labor? How would that affect the mix variance?

1.To calculate the standard mix, standard mix proportion is to be multiplied with actual input quantity.

2.To compute the mix variance the following formula can be used:

2.To compute the mix variance the following formula can be used:

3.To compute actual mix proportion, actual quantity is to be multiplied with total actual input quantity.

3.To compute actual mix proportion, actual quantity is to be multiplied with total actual input quantity.

The mix variance is favorable because a large percentage of less expensive labor i.e. packers is used.

The mix variance is favorable because a large percentage of less expensive labor i.e. packers is used.

4.If the proportions of the ingredients are changed, the actual mix proportion can be computed as:

The mix variance will be unfavorable because relatively expensive labor (machine operators) is used in the same proportion as less expensive labor i.e. packers.

The mix variance will be unfavorable because relatively expensive labor (machine operators) is used in the same proportion as less expensive labor i.e. packers.

2.To compute the mix variance the following formula can be used: 3.To compute actual mix proportion, actual quantity is to be multiplied with total actual input quantity. The mix variance is favorable because a large percentage of less expensive labor i.e. packers is used.4.If the proportions of the ingredients are changed, the actual mix proportion can be computed as:

The mix variance will be unfavorable because relatively expensive labor (machine operators) is used in the same proportion as less expensive labor i.e. packers. 3

Direct Labor and Direct Materials Variances, Journal Entries

Jameson Company produces paper towels. The company has established the following direct materials and direct labor standards for one case of paper towels:

During the first quarter of the year, Jameson produced 45,000 cases of paper towels. The company purchased and used 135,700 pounds of paper pulp at $0.38 per pound. Actual direct labor used was 91,000 hours at $12.10 per hour.

Required:

1. Calculate the direct materials price and usage variances.

2. Calculate the direct labor rate and efficiency variances.

3. Prepare the journal entries for the direct materials and direct labor variances.

4. Describe how flexible budgeting variances relate to the direct materials and direct labor variances computed in Requirements 1 and 2.

Jameson Company produces paper towels. The company has established the following direct materials and direct labor standards for one case of paper towels:

During the first quarter of the year, Jameson produced 45,000 cases of paper towels. The company purchased and used 135,700 pounds of paper pulp at $0.38 per pound. Actual direct labor used was 91,000 hours at $12.10 per hour.

Required:

1. Calculate the direct materials price and usage variances.

2. Calculate the direct labor rate and efficiency variances.

3. Prepare the journal entries for the direct materials and direct labor variances.

4. Describe how flexible budgeting variances relate to the direct materials and direct labor variances computed in Requirements 1 and 2.

1.Direct materials price variance =

i.e.

i.e.

Paper pulp =

= 2,714 favorable

= 2,714 favorable

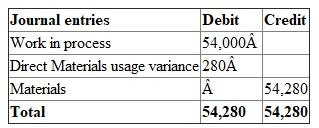

Direct materials usage variance =

Before arrive at usage variance, we need to arrive at the standard quantity and standard labor hours.

Before arrive at usage variance, we need to arrive at the standard quantity and standard labor hours.

One case of paper towel requires 3 lbs of paper pulps, so in order to produce 45,000 cases we need 135,000 paper pulps as shown below

Standard quantity =

i.e. 135,000

i.e. 135,000

One case of paper towel requires 2 hrs of direct labor, so in order to produce 45,000 cases we need 90,000 labor hours as calculated below

Standard labor hours =

i.e. 90,000 hours

i.e. 90,000 hours

Direct materials usage variance =

Direct materials usage variance =

Direct materials usage variance =

Direct materials usage variance = 280 unfavorable

Direct materials usage variance = 280 unfavorable

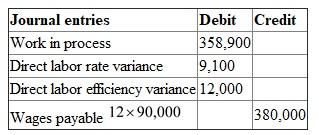

2. Direct labor rate variance =

Direct labor rate variance =

Direct labor rate variance =

Direct labor rate variance = 9,100 unfavorable

Direct labor rate variance = 9,100 unfavorable

Direct labor efficiency variance =

Direct labor efficiency variance =

Direct labor efficiency variance =

Direct labor efficiency variance = 12,000 unfavorable

Direct labor efficiency variance = 12,000 unfavorable

3. Before journalizing the material and labor variances, we need to arrive at the total materials used.

Materials =

i.e.

i.e.

which is equal to 54,280.

which is equal to 54,280.

Journal entries for direct materials price variance

Journal entries for direct materials usage variance

Journal entries for direct materials usage variance

Journal entries for direct labor rate and efficiency variance

Journal entries for direct labor rate and efficiency variance

Wages payable is nothing but standard rate multiplied by actual labor hours.

Wages payable is nothing but standard rate multiplied by actual labor hours.

4.Flexible budgets are prepared for different levels of production needs and the variance occurs when there is a difference to the budgeted and actual results. Direct material and direct labor variances are as well calculated for different output levels for standard and actual levels.

i.e. Paper pulp =

= 2,714 favorableDirect materials usage variance =

Before arrive at usage variance, we need to arrive at the standard quantity and standard labor hours.One case of paper towel requires 3 lbs of paper pulps, so in order to produce 45,000 cases we need 135,000 paper pulps as shown below

Standard quantity =

i.e. 135,000One case of paper towel requires 2 hrs of direct labor, so in order to produce 45,000 cases we need 90,000 labor hours as calculated below

Standard labor hours =

i.e. 90,000 hoursDirect materials usage variance =

Direct materials usage variance = Direct materials usage variance = 280 unfavorable2. Direct labor rate variance =

Direct labor rate variance = Direct labor rate variance = 9,100 unfavorableDirect labor efficiency variance =

Direct labor efficiency variance = Direct labor efficiency variance = 12,000 unfavorable3. Before journalizing the material and labor variances, we need to arrive at the total materials used.

Materials =

i.e. which is equal to 54,280.Journal entries for direct materials price variance

Journal entries for direct materials usage variance Journal entries for direct labor rate and efficiency variance Wages payable is nothing but standard rate multiplied by actual labor hours.4.Flexible budgets are prepared for different levels of production needs and the variance occurs when there is a difference to the budgeted and actual results. Direct material and direct labor variances are as well calculated for different output levels for standard and actual levels.

4

Direct Materials Usage Variances: Direct Materials Mix and Yield Variances

Energy Products Company produces a gasoline additive, Gas Gain. This product increases engine efficiency and improves gasoline mileage by creating a more complete burn in the combustion process.

Careful controls are required during the production process to ensure that the proper mix of input chemicals is achieved and that evaporation is controlled. If the controls are not effective, there can be a loss of output and efficiency.

The standard cost of producing a 500-liter batch of Gas Gain is $135. The standard direct materials mix and related standard cost of each chemical used in a 500-liter batch are as follows:

The quantities of chemicals purchased and used during the current production period are shown in the following schedule. A total of 140 batches of Gas Gain were manufactured during the current production period. Energy Products determines its cost and chemical usage variations at the end of each production period.

Required:

Compute the total direct materials usage variance, and then break down this variance into its mix and yield components. (CMA adapted)

Energy Products Company produces a gasoline additive, Gas Gain. This product increases engine efficiency and improves gasoline mileage by creating a more complete burn in the combustion process.

Careful controls are required during the production process to ensure that the proper mix of input chemicals is achieved and that evaporation is controlled. If the controls are not effective, there can be a loss of output and efficiency.

The standard cost of producing a 500-liter batch of Gas Gain is $135. The standard direct materials mix and related standard cost of each chemical used in a 500-liter batch are as follows:

The quantities of chemicals purchased and used during the current production period are shown in the following schedule. A total of 140 batches of Gas Gain were manufactured during the current production period. Energy Products determines its cost and chemical usage variations at the end of each production period.

Required:

Compute the total direct materials usage variance, and then break down this variance into its mix and yield components. (CMA adapted)

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

5

What is the quantity decision? The pricing decision?

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

6

Suggest some possible causes of an unfavorable direct labor efficiency variance.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

7

Investigation of Variances

Madison Company uses the following rule to determine whether direct labor efficiency variances ought to be investigated. A direct labor efficiency variance will be investigated anytime the amount exceeds the lesser of $12,000 or 10 percent of the standard labor cost. Reports for the past five weeks provided the following information:

Required:

1. Using the rule provided, identify the cases that will be investigated.

2. Suppose that investigation reveals that the cause of an unfavorable direct labor efficiency variance is the use of lower quality direct materials than are usually used. Who is responsi-ble? What corrective action would likely be taken?

3. Suppose that investigation reveals that the cause of a significant favorable direct labor efficiency variance is attributable to a new approach to manufacturing that takes less labor time but causes more direct materials waste. Upon examining the direct materials usage variance, it is discovered to be unfavorable, and it is larger than the favorable direct labor efficiency variance. Who is responsible? What action should be taken? How would your answer change if the unfavorable variance were smaller than the favorable?

Madison Company uses the following rule to determine whether direct labor efficiency variances ought to be investigated. A direct labor efficiency variance will be investigated anytime the amount exceeds the lesser of $12,000 or 10 percent of the standard labor cost. Reports for the past five weeks provided the following information:

Required:

1. Using the rule provided, identify the cases that will be investigated.

2. Suppose that investigation reveals that the cause of an unfavorable direct labor efficiency variance is the use of lower quality direct materials than are usually used. Who is responsi-ble? What corrective action would likely be taken?

3. Suppose that investigation reveals that the cause of a significant favorable direct labor efficiency variance is attributable to a new approach to manufacturing that takes less labor time but causes more direct materials waste. Upon examining the direct materials usage variance, it is discovered to be unfavorable, and it is larger than the favorable direct labor efficiency variance. Who is responsible? What action should be taken? How would your answer change if the unfavorable variance were smaller than the favorable?

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

8

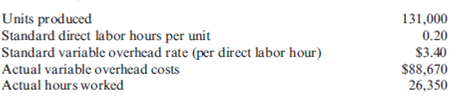

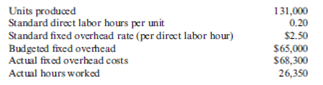

Solving for Unknowns, Overhead Analysis OBJECTIVE OO

Nuevo Company produces a single product. Nuevo employs a standard cost system and uses a flexible budget to predict overhead costs at various levels of activity. For the most recent year, Nuevo used a standard overhead rate equal to $6.25 per direct labor hour. The rate was computed using expected activity. Budgeted overhead costs are $80,000 for 10,000 direct labor hours and $120,000 for 20,000 direct labor hours. During the past year, Nuevo generated the following data:

a. Actual production: 4,000 units

b. Fixed overhead volume variance: $1,750 U

c. Variable overhead efficiency variance: $3,200 F

d. Actual fixed overhead costs: $41,335

e. Actual variable overhead costs: $70,000

Required:

1. Determine the fixed overhead spending variance.

2. Determine the variable overhead spending variance.