Deck 11: Strategic Cost Management

Full screen (f)

Question

Question

Question

External Linkages, Activity-Based Customer Costing, and Strategic Decision Making

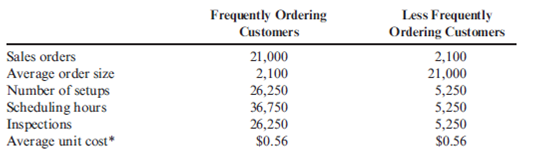

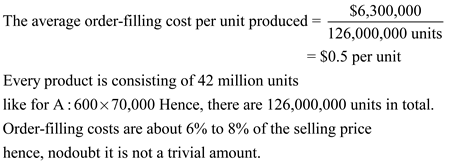

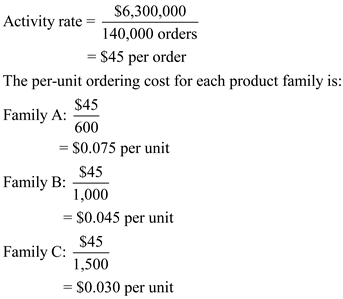

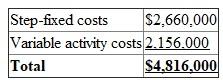

Moss Manufacturing produces several types of bolts. The products are produced in batches according to customer order. Although there are a variety of bolts, they can be grouped into three product families. The number of units sold is the same for each family. The selling prices for the three families range from $0.50 to $0.80 per unit. Because the product families are used in different kinds of products, customers also can be grouped into three categories, corresponding to the product family they purchase. Historically, the costs of order entry, processing, and handling were expensed and not traced to individual products. These costs are not trivial and totaled $6,300,000 for the most recent year. Furthermore, these costs had been increasing over time. Recently, the company had begun to emphasize a cost reduction strategy; however, any cost reduction decisions had to contribute to the creation of a competitive advantage.

Because of the magnitude and growth of order-filling costs, management decided to explore the causes of these costs. They discovered that order-filling costs were driven by the number of customer orders processed. Further investigation revealed the following cost behavior:

Step-fixed cost component: $70,000 per step; 2,000 orders define a step*

Variable cost component: $28 per order

*Moss currently has sufficient steps to process 100,000 orders.

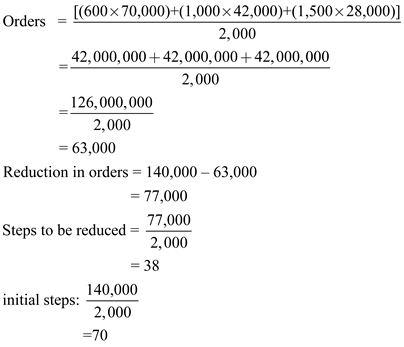

The expected customer orders for the year total 140,000. The expected usage of the order- filling activity and the average size of an order by product family are as follows:

As a result of the cost behavior analysis, the marketing manager recommended the imposition of a charge per customer order. The president of the company concurred. The charge was implemented by adding the cost per order to the price of each order (computed using the projected ordering costs and expected orders). This ordering cost was then reduced as the size of the order increased and eliminated as the order size reached 2,000 units. (The marketing manager indicated that any penalties imposed for orders greater than this size would lose sales from some of the smaller customers.) Within a short period of communicating this new price information to customers, the average order size for all three product families increased to 2,000 units.

Required:

1. Moss traditionally has expensed order-filling costs (following GAAP guidelines). Under this approach, how much cost is assigned to customers? Do you agree with this practice?

Explain.

2. Consider the following claim: by expensing the order-filling costs, all products were undercosted; furthermore, products ordered in small batches are significantly undercosted.

Explain, with supporting computations where possible. Explain how this analysis also reveals the costs of various customer categories.

3. Calculate the reduction in order-filling costs produced by the change in pricing strategy. (Assume that resource spending is reduced as much as possible and that the total units sold remain unchanged.) Explain how exploiting customer linkages produced this cost reduction. Moss also noticed that other activity costs, such as those for setups, scheduling, and materials handling costs, were reduced significantly as a result of this new policy. Explain this outcome, and discuss its implications.

4. Suppose that one of the customers complains about the new pricing policy. This buyer is a lean, JIT firm that relies on small, frequent orders. In fact, this customer accounted for 30 percent of the Family A orders. How should Moss deal with this customer?

5. One of Moss's goals is to reduce costs so that a competitive advantage might be created. Describe how the management of Moss might use this outcome to help create a competitive advantage.

Moss Manufacturing produces several types of bolts. The products are produced in batches according to customer order. Although there are a variety of bolts, they can be grouped into three product families. The number of units sold is the same for each family. The selling prices for the three families range from $0.50 to $0.80 per unit. Because the product families are used in different kinds of products, customers also can be grouped into three categories, corresponding to the product family they purchase. Historically, the costs of order entry, processing, and handling were expensed and not traced to individual products. These costs are not trivial and totaled $6,300,000 for the most recent year. Furthermore, these costs had been increasing over time. Recently, the company had begun to emphasize a cost reduction strategy; however, any cost reduction decisions had to contribute to the creation of a competitive advantage.

Because of the magnitude and growth of order-filling costs, management decided to explore the causes of these costs. They discovered that order-filling costs were driven by the number of customer orders processed. Further investigation revealed the following cost behavior:

Step-fixed cost component: $70,000 per step; 2,000 orders define a step*

Variable cost component: $28 per order

*Moss currently has sufficient steps to process 100,000 orders.

The expected customer orders for the year total 140,000. The expected usage of the order- filling activity and the average size of an order by product family are as follows:

As a result of the cost behavior analysis, the marketing manager recommended the imposition of a charge per customer order. The president of the company concurred. The charge was implemented by adding the cost per order to the price of each order (computed using the projected ordering costs and expected orders). This ordering cost was then reduced as the size of the order increased and eliminated as the order size reached 2,000 units. (The marketing manager indicated that any penalties imposed for orders greater than this size would lose sales from some of the smaller customers.) Within a short period of communicating this new price information to customers, the average order size for all three product families increased to 2,000 units.

Required:

1. Moss traditionally has expensed order-filling costs (following GAAP guidelines). Under this approach, how much cost is assigned to customers? Do you agree with this practice?

Explain.

2. Consider the following claim: by expensing the order-filling costs, all products were undercosted; furthermore, products ordered in small batches are significantly undercosted.

Explain, with supporting computations where possible. Explain how this analysis also reveals the costs of various customer categories.

3. Calculate the reduction in order-filling costs produced by the change in pricing strategy. (Assume that resource spending is reduced as much as possible and that the total units sold remain unchanged.) Explain how exploiting customer linkages produced this cost reduction. Moss also noticed that other activity costs, such as those for setups, scheduling, and materials handling costs, were reduced significantly as a result of this new policy. Explain this outcome, and discuss its implications.

4. Suppose that one of the customers complains about the new pricing policy. This buyer is a lean, JIT firm that relies on small, frequent orders. In fact, this customer accounted for 30 percent of the Family A orders. How should Moss deal with this customer?

5. One of Moss's goals is to reduce costs so that a competitive advantage might be created. Describe how the management of Moss might use this outcome to help create a competitive advantage.

Question

Question

Question

Internal and External Linkages, Strategic Cost Management

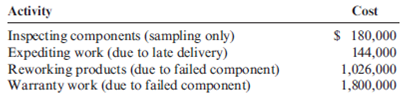

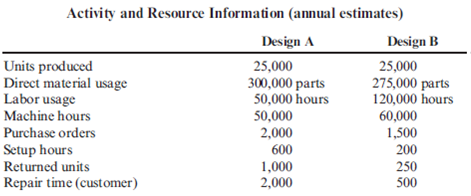

Maxwell Company produces a variety of kitchen appliances, including cooking ranges and dishwashers. Over the past several years, competition has intensified. In order to maintain-and perhaps increase-its market share, Maxwell's management decided that the overall quality of its products had to be increased. Furthermore, costs needed to be reduced so that the selling prices of its products could be reduced. After some investigation, Maxwell concluded that many of its problems could be traced to the unreliability of the parts that were purchased from outside suppliers. Many of these components failed to work as intended, causing performance problems.

Over the years, the company had increased its inspection activity of the final products. If a problem could be detected internally, then it was usually possible to rework the appliance so that the desired performance was achieved. Management also had increased its warranty coverage; warranty work had been increasing over the years.

David Haight, president of Maxwell Company, called a meeting with his executive committee. Lee Linsenmeyer, chief engineer; Kit Applegate, controller; and Jeannie Mitchell, purchasing manager, were all in attendance. How to improve the company's competitive position was the meeting's topic. The conversation of the meeting was recorded as seen on the following page:

DAVID : We need to find a way to improve the quality of our products and at the same time reduce costs. Lee, you said that you have done some research in this area. Would you share your findings?

LEE : As you know, a major source of our quality problems relates to the poor quality of the parts we acquire from the outside. We have a lot of different parts, and this adds to the complexity of the problem. What I thought would be helpful would be to redesign our products so that they can use as many interchangeable parts as possible. This will cut down the number of different parts, make it easier to inspect, and cheaper to repair when it comes to warranty work. My engineering staff has already come up with some new designs that will do this for us.

JEANNIE : I like this idea. It will simplify the purchasing activity significantly. With fewer parts, I can envision some significant savings for my area. Lee has shown me the designs so I know exactly what parts would be needed. I also have a suggestion. We need to embark on a supplier evaluation program. We have too many suppliers. By reducing the number of different parts, we will need fewer suppliers. And we really don't need to use all the suppliers that produce the parts demanded by the new designs. We should pick suppliers that will work with us and provide the quality of parts that we need. I have done some preliminary research and have identified five suppliers that seem willing to work with us and assure us of the quality we need. Lee may need to send some of his engineers into their plants to make sure that they can do what they are claiming.

DAVID : This sounds promising. Kit, can you look over the proposals and their estimates and give us some idea if this approach will save us any money? And if so, how much can we expect to save?

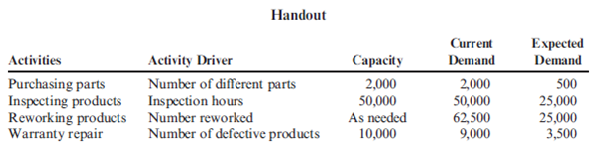

KIT : Actually, I am ahead of the game here. Lee and Jeannie have both been in contact with me and have provided me with some estimates on how these actions would affect different activities. I have prepared a handout that includes an activity table revealing what I think are the key activities affected. I have also assembled some tentative information about activity costs. The table gives the current demand and the expected demand after the changes are implemented. With this information, we should be able to assess the expected cost savings.

Additionally, the following activity cost data are provided:

Purchasing parts: Variable activity cost: $30 per part number; 20 salaried clerks, each earning a $45,000 annual salary. Each clerk is capable of processing orders associated with 100 part numbers.

Inspecting parts: Twenty-five inspectors, each earning a salary of $40,000 per year. Each inspector is capable of 2,000 hours of inspection.

Reworking products: Variable activity cost: $25 per unit reworked (labor and parts).

Warranty: Twenty repair agents, each paid a salary of $35,000 per year. Each repair agent is capable of repairing 500 units per year. Variable activity costs: $15 per product repaired.

Required:

1. Compute the total savings possible as reflected by Kit's handout. Assume that resource spending is reduced where possible.

2. Explain how redesign and supplier evaluation are linked to the savings computed in Requirement 1. Discuss the importance of recognizing and exploiting internal and external linkages.

3. Identify the organizational and operational activities involved in the strategy being considered by Maxwell Company. What is the relationship between organizational and operational activities?

Maxwell Company produces a variety of kitchen appliances, including cooking ranges and dishwashers. Over the past several years, competition has intensified. In order to maintain-and perhaps increase-its market share, Maxwell's management decided that the overall quality of its products had to be increased. Furthermore, costs needed to be reduced so that the selling prices of its products could be reduced. After some investigation, Maxwell concluded that many of its problems could be traced to the unreliability of the parts that were purchased from outside suppliers. Many of these components failed to work as intended, causing performance problems.

Over the years, the company had increased its inspection activity of the final products. If a problem could be detected internally, then it was usually possible to rework the appliance so that the desired performance was achieved. Management also had increased its warranty coverage; warranty work had been increasing over the years.

David Haight, president of Maxwell Company, called a meeting with his executive committee. Lee Linsenmeyer, chief engineer; Kit Applegate, controller; and Jeannie Mitchell, purchasing manager, were all in attendance. How to improve the company's competitive position was the meeting's topic. The conversation of the meeting was recorded as seen on the following page:

DAVID : We need to find a way to improve the quality of our products and at the same time reduce costs. Lee, you said that you have done some research in this area. Would you share your findings?

LEE : As you know, a major source of our quality problems relates to the poor quality of the parts we acquire from the outside. We have a lot of different parts, and this adds to the complexity of the problem. What I thought would be helpful would be to redesign our products so that they can use as many interchangeable parts as possible. This will cut down the number of different parts, make it easier to inspect, and cheaper to repair when it comes to warranty work. My engineering staff has already come up with some new designs that will do this for us.

JEANNIE : I like this idea. It will simplify the purchasing activity significantly. With fewer parts, I can envision some significant savings for my area. Lee has shown me the designs so I know exactly what parts would be needed. I also have a suggestion. We need to embark on a supplier evaluation program. We have too many suppliers. By reducing the number of different parts, we will need fewer suppliers. And we really don't need to use all the suppliers that produce the parts demanded by the new designs. We should pick suppliers that will work with us and provide the quality of parts that we need. I have done some preliminary research and have identified five suppliers that seem willing to work with us and assure us of the quality we need. Lee may need to send some of his engineers into their plants to make sure that they can do what they are claiming.

DAVID : This sounds promising. Kit, can you look over the proposals and their estimates and give us some idea if this approach will save us any money? And if so, how much can we expect to save?

KIT : Actually, I am ahead of the game here. Lee and Jeannie have both been in contact with me and have provided me with some estimates on how these actions would affect different activities. I have prepared a handout that includes an activity table revealing what I think are the key activities affected. I have also assembled some tentative information about activity costs. The table gives the current demand and the expected demand after the changes are implemented. With this information, we should be able to assess the expected cost savings.

Additionally, the following activity cost data are provided:

Purchasing parts: Variable activity cost: $30 per part number; 20 salaried clerks, each earning a $45,000 annual salary. Each clerk is capable of processing orders associated with 100 part numbers.

Inspecting parts: Twenty-five inspectors, each earning a salary of $40,000 per year. Each inspector is capable of 2,000 hours of inspection.

Reworking products: Variable activity cost: $25 per unit reworked (labor and parts).

Warranty: Twenty repair agents, each paid a salary of $35,000 per year. Each repair agent is capable of repairing 500 units per year. Variable activity costs: $15 per product repaired.

Required:

1. Compute the total savings possible as reflected by Kit's handout. Assume that resource spending is reduced where possible.

2. Explain how redesign and supplier evaluation are linked to the savings computed in Requirement 1. Discuss the importance of recognizing and exploiting internal and external linkages.

3. Identify the organizational and operational activities involved in the strategy being considered by Maxwell Company. What is the relationship between organizational and operational activities?

Question

Question

Question

External Linkages and Strategic Cost Management OBJECTIVE

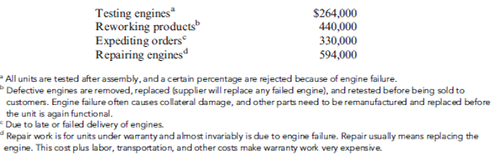

Pawnee Works makes machine parts for manufacturers of industrial equipment. Over the years, Pawnee has been a steady and reliable supplier of quality parts to medium- and small-machine manufacturers. Michael Murray, owner of Pawnee Works, once again was disappointed in the year-end income statement. Profits had again failed to meet expectations. The performance was particularly puzzling given that the shop was operating at 100 percent capacity and had been for two years-ever since it had landed a Fortune 500 firm as a regular customer. This firm currently supplies 40 percent of the business-a figure that had grown over the two years. Convinced that something was wrong, Michael called Brooke Harker, a partner in a large regional CPA firm. Brooke agreed to look into the matter.

A short time later, Brooke made an appointment to meet with Michael. Their conversation was recorded as follows:

BROOKE : Michael, I think I have pinpointed your problem. I think your main difficulty is poor pricing-you're undercharging your major customer. The firm is getting high-precision machined parts for much less than the cost to you. And I bet that you have been losing some of your smaller customers. You may want to rethink your strategic position. You are a small player in the industrial machine industry. This Fortune 500 customer has 40 percent of the industrial machine market. Over the years, you have carved out a good reputation among small- and medium-size manufacturers. Right?

MICHAEL : Well, you're right. Over the years, our customers have not been giants. But we saw this business with the Fortune 500 company as an opportunity to play in the big leagues. We thought it might mean the opportunity to expand the size of our operation. And we have expanded-at least we have added employees and some specialized engineering equipment. My engineering and programming costs have skyrocketed-resource increases we needed, though, to meet the specs of this larger customer. Profits have increased slightly, but nothing like I expected. You're also right about losing some of our smaller customers. Many have complained that the price of their jobs has increased. They have all indicated that they like the work we do and that we are conveniently located, but they argue that they simply cannot afford to keep paying the price we require. The small customers we have kept are also complaining and threatening to go elsewhere. I doubt we'll be able to hold onto their business for much longer-unless a change is made. So far, though, the business we have lost has been replaced with more orders from our large customer. I expect we could do even more business for the large customer. But how can the large buyer be getting the great deal you've described? It has the same markup as our regular jobs-full manufacturing cost plus 25 percent.

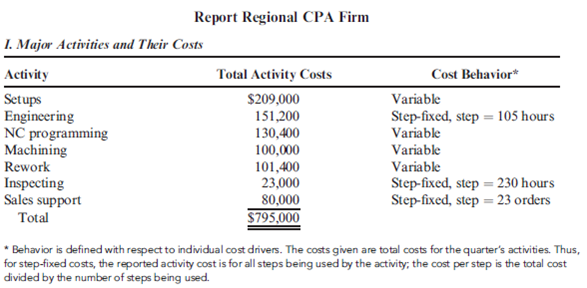

BROOKE : I have prepared a report illustrating the total overhead costs for a typical quarter.

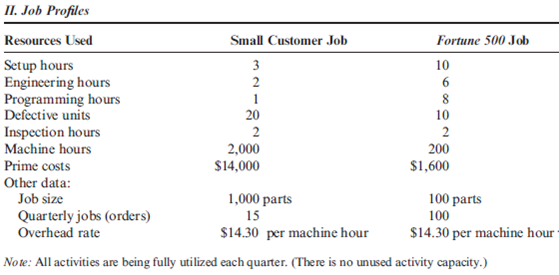

This report details your major activities and their associated costs. It also provides a comparison of a typical job for your small customers and the typical job for your large customer. Part of the problem is that your accounting system does not react to certain external events. It fails to show the effect of the large customer's activities on your activities and those that relate to your other customers. Given that you assign overhead costs using machine hours, I think you'll find it quite revealing.

MICHAEL : I'll have my controller examine the report for me. You know, if you are right about underpricing the large customer, I have a big problem. I'm not sure that I can increase the price of the parts without losing this big guy's business. After all, it can go to a dozen machine shops like mine and get the work done. A price increase may not work. Then I'd be faced with the loss of 40 percent of my jobs. I suppose, though, that I might be able to regain most of the business with the small customers. In fact, I am positive that we could get most of that business back. I wonder if that's what I ought to do.

Required:

1. Without any calculation, explain why the machining company is losing money. Discuss the strategic insights provided by knowledge of activities, their costs, and customer linkages. Comment on the observation made by Brooke that the current accounting system fails to reflect external events. What changes would be needed to correct this deficiency (if true)?

2. Compute the unit price currently being charged each customer type (using machine hours to assign overhead costs).

3. Compute the unit price that would be charged each customer assuming that overhead is assigned using an ABC approach. Was the CPA right? Is the large customer paying less than the cost of producing the unit? How is this conclusion affected if the sales support activity is traced to jobs? (Use orders-jobs-as the cost driver.)

4. Compute the quarterly profit that is currently being earned and the amount that would be earned if Pawnee Works sold only to small customers (a small customer strategy). For the second income statement, use ABC for cost assignments. For the second income statement, the large customer is replaced with 10 smaller customers with the same characteristics as the 15 currently buying parts from Pawnee. Assume that any opportunities to reduce resource spending and usage will be reflected in the profit associated with a small customer strategy. Also, only the cost of activity usage is assigned to jobs. Any cost of unused activity is reported as a separate item on the income statement. Report sales support as a period expense.

5. What change in strategy would you recommend? In making this recommendation, consider the firm's value-chain framework.

Pawnee Works makes machine parts for manufacturers of industrial equipment. Over the years, Pawnee has been a steady and reliable supplier of quality parts to medium- and small-machine manufacturers. Michael Murray, owner of Pawnee Works, once again was disappointed in the year-end income statement. Profits had again failed to meet expectations. The performance was particularly puzzling given that the shop was operating at 100 percent capacity and had been for two years-ever since it had landed a Fortune 500 firm as a regular customer. This firm currently supplies 40 percent of the business-a figure that had grown over the two years. Convinced that something was wrong, Michael called Brooke Harker, a partner in a large regional CPA firm. Brooke agreed to look into the matter.

A short time later, Brooke made an appointment to meet with Michael. Their conversation was recorded as follows:

BROOKE : Michael, I think I have pinpointed your problem. I think your main difficulty is poor pricing-you're undercharging your major customer. The firm is getting high-precision machined parts for much less than the cost to you. And I bet that you have been losing some of your smaller customers. You may want to rethink your strategic position. You are a small player in the industrial machine industry. This Fortune 500 customer has 40 percent of the industrial machine market. Over the years, you have carved out a good reputation among small- and medium-size manufacturers. Right?

MICHAEL : Well, you're right. Over the years, our customers have not been giants. But we saw this business with the Fortune 500 company as an opportunity to play in the big leagues. We thought it might mean the opportunity to expand the size of our operation. And we have expanded-at least we have added employees and some specialized engineering equipment. My engineering and programming costs have skyrocketed-resource increases we needed, though, to meet the specs of this larger customer. Profits have increased slightly, but nothing like I expected. You're also right about losing some of our smaller customers. Many have complained that the price of their jobs has increased. They have all indicated that they like the work we do and that we are conveniently located, but they argue that they simply cannot afford to keep paying the price we require. The small customers we have kept are also complaining and threatening to go elsewhere. I doubt we'll be able to hold onto their business for much longer-unless a change is made. So far, though, the business we have lost has been replaced with more orders from our large customer. I expect we could do even more business for the large customer. But how can the large buyer be getting the great deal you've described? It has the same markup as our regular jobs-full manufacturing cost plus 25 percent.

BROOKE : I have prepared a report illustrating the total overhead costs for a typical quarter.

This report details your major activities and their associated costs. It also provides a comparison of a typical job for your small customers and the typical job for your large customer. Part of the problem is that your accounting system does not react to certain external events. It fails to show the effect of the large customer's activities on your activities and those that relate to your other customers. Given that you assign overhead costs using machine hours, I think you'll find it quite revealing.

MICHAEL : I'll have my controller examine the report for me. You know, if you are right about underpricing the large customer, I have a big problem. I'm not sure that I can increase the price of the parts without losing this big guy's business. After all, it can go to a dozen machine shops like mine and get the work done. A price increase may not work. Then I'd be faced with the loss of 40 percent of my jobs. I suppose, though, that I might be able to regain most of the business with the small customers. In fact, I am positive that we could get most of that business back. I wonder if that's what I ought to do.

Required:

1. Without any calculation, explain why the machining company is losing money. Discuss the strategic insights provided by knowledge of activities, their costs, and customer linkages. Comment on the observation made by Brooke that the current accounting system fails to reflect external events. What changes would be needed to correct this deficiency (if true)?

2. Compute the unit price currently being charged each customer type (using machine hours to assign overhead costs).

3. Compute the unit price that would be charged each customer assuming that overhead is assigned using an ABC approach. Was the CPA right? Is the large customer paying less than the cost of producing the unit? How is this conclusion affected if the sales support activity is traced to jobs? (Use orders-jobs-as the cost driver.)

4. Compute the quarterly profit that is currently being earned and the amount that would be earned if Pawnee Works sold only to small customers (a small customer strategy). For the second income statement, use ABC for cost assignments. For the second income statement, the large customer is replaced with 10 smaller customers with the same characteristics as the 15 currently buying parts from Pawnee. Assume that any opportunities to reduce resource spending and usage will be reflected in the profit associated with a small customer strategy. Also, only the cost of activity usage is assigned to jobs. Any cost of unused activity is reported as a separate item on the income statement. Report sales support as a period expense.

5. What change in strategy would you recommend? In making this recommendation, consider the firm's value-chain framework.

Question

Question

JIT Features and Product Costing Accuracy

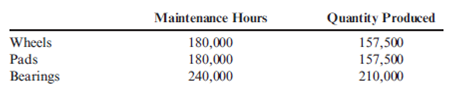

Prior to installing a JIT system, Barker Company, a producer of automobile parts, used maintenance hours to assign maintenance costs to its three products (wheels, brake pads, and ball bearings). The maintenance costs totaled $5,880,000 per year. The maintenance hours used by each product and the quantity of each product produced are as follows:

After installing JIT, three manufacturing cells were created, and cell workers were trained to perform preventive maintenance and minor repairs. A full-time maintenance person was also assigned to each cell. Maintenance costs for the three cells still totaled $5,880,000; however, these costs are now traceable to each cell as follows:

Required:

1. Compute the pre-JIT maintenance cost per unit for each product.

2. Compute the maintenance cost per unit for each product after installing JIT.

3. Explain why the JIT maintenance cost per unit is more accurate than the pre-JIT cost.

Prior to installing a JIT system, Barker Company, a producer of automobile parts, used maintenance hours to assign maintenance costs to its three products (wheels, brake pads, and ball bearings). The maintenance costs totaled $5,880,000 per year. The maintenance hours used by each product and the quantity of each product produced are as follows:

After installing JIT, three manufacturing cells were created, and cell workers were trained to perform preventive maintenance and minor repairs. A full-time maintenance person was also assigned to each cell. Maintenance costs for the three cells still totaled $5,880,000; however, these costs are now traceable to each cell as follows:

Required:

1. Compute the pre-JIT maintenance cost per unit for each product.

2. Compute the maintenance cost per unit for each product after installing JIT.

3. Explain why the JIT maintenance cost per unit is more accurate than the pre-JIT cost.

Question

Question

Question

Question

Life-Cycle Cost Management

Jolene Askew, manager of Feagan Company, has committed her company to a strategically sound cost reduction program. Emphasizing life-cycle cost management is a major part of this effort. Jolene is convinced that production costs can be reduced by paying more attention to the relationships between design and manufacturing. Design engineers need to know what causes manufacturing costs. She instructed her controller to develop a manufacturing cost formula for a newly proposed product. Marketing had already projected sales of 25,000 units for the new product. (The life cycle was estimated to be 18 months. The company expected to have 50 percent of the market and priced its product to achieve this goal.) The projected selling price was $20 per unit. The following cost formula was developed:

Y = $200,000 + $10 X 1

where

Upon seeing the cost formula, Jolene quickly calculated the projected gross profit to be $50,000. This produced a gross profit of $2 per unit, well below the targeted gross profit of $4 per unit. Jolene then sent a memo to the Engineering Department, instructing them to search for a new design that would lower the costs of production by at least $50,000 so that the target profit could be met.

Within two days, the Engineering Department proposed a new design that would reduce unit-variable cost from $10 per machine hour to $8 per machine hour (Design Z). The chief engineer, upon reviewing the design, questioned the validity of the controller's cost formula. He suggested a more careful assessment of the proposed design's effect on activities other than machining. Based on this suggestion, the following revised cost formula was developed. This cost formula reflected the cost relationships of the most recent design (Design Z).

Y = $140,000 + $8 X 1 + $5,000 X 2 + $2,000 X 3

where

X 1 = Machine hours

X 2 = Number of batches

X 3 = Number of engineering change orders

Based on scheduling and inventory considerations, the product would be produced in batches of 1,000; thus, 25 batches would be needed over the product's life cycle. Furthermore, based on past experience, the product would likely generate about 20 engineering change orders.

This new insight into the linkage of the product with its underlying activities led to a different design (Design W). This second design also lowered the unit-level cost by $2 per unit but decreased the number of design support requirements from 20 orders to 10 orders. Attention was also given to the setup activity, and the design engineer assigned to the product created a design that reduced setup time and lowered variable setup costs from $5,000 to $3,000 per setup. Furthermore, Design W also creates excess activity capacity for the setup activity, and resource spending for setup activity capacity can be decreased by $40,000, reducing the fixed cost component in the equation by this amount.

Design W was recommended and accepted. As prototypes of the design were tested, an additional benefit emerged. Based on test results, the post-purchase costs dropped from an estimated $0.70 per unit sold to $0.40 per unit sold. Using this information, the Marketing Department revised the projected market share upward from 50 percent to 60 percent (with no price decrease).

Required:

1. Calculate the expected gross profit per unit for Design Z using the controller's original cost formula. According to this outcome, does Design Z reach the targeted unit profit? Repeat, using the engineer's revised cost formula. Explain why Design Z failed to meet the targeted profit. What does this say about the use of unit-based costing for life-cycle cost management?

2. Calculate the expected profit per unit using Design W. Comment on the value of activity information for life-cycle cost management.

3. The benefit of the post-purchase cost reduction of Design W was discovered in testing. What direct benefit did it create for Feagan Company (in dollars)? Reducing post-purchase costs was not a specific design objective. Should it have been? Are there any other design objectives that should have been considered?

Jolene Askew, manager of Feagan Company, has committed her company to a strategically sound cost reduction program. Emphasizing life-cycle cost management is a major part of this effort. Jolene is convinced that production costs can be reduced by paying more attention to the relationships between design and manufacturing. Design engineers need to know what causes manufacturing costs. She instructed her controller to develop a manufacturing cost formula for a newly proposed product. Marketing had already projected sales of 25,000 units for the new product. (The life cycle was estimated to be 18 months. The company expected to have 50 percent of the market and priced its product to achieve this goal.) The projected selling price was $20 per unit. The following cost formula was developed:

Y = $200,000 + $10 X 1

where

Upon seeing the cost formula, Jolene quickly calculated the projected gross profit to be $50,000. This produced a gross profit of $2 per unit, well below the targeted gross profit of $4 per unit. Jolene then sent a memo to the Engineering Department, instructing them to search for a new design that would lower the costs of production by at least $50,000 so that the target profit could be met.

Within two days, the Engineering Department proposed a new design that would reduce unit-variable cost from $10 per machine hour to $8 per machine hour (Design Z). The chief engineer, upon reviewing the design, questioned the validity of the controller's cost formula. He suggested a more careful assessment of the proposed design's effect on activities other than machining. Based on this suggestion, the following revised cost formula was developed. This cost formula reflected the cost relationships of the most recent design (Design Z).

Y = $140,000 + $8 X 1 + $5,000 X 2 + $2,000 X 3

where

X 1 = Machine hours

X 2 = Number of batches

X 3 = Number of engineering change orders

Based on scheduling and inventory considerations, the product would be produced in batches of 1,000; thus, 25 batches would be needed over the product's life cycle. Furthermore, based on past experience, the product would likely generate about 20 engineering change orders.

This new insight into the linkage of the product with its underlying activities led to a different design (Design W). This second design also lowered the unit-level cost by $2 per unit but decreased the number of design support requirements from 20 orders to 10 orders. Attention was also given to the setup activity, and the design engineer assigned to the product created a design that reduced setup time and lowered variable setup costs from $5,000 to $3,000 per setup. Furthermore, Design W also creates excess activity capacity for the setup activity, and resource spending for setup activity capacity can be decreased by $40,000, reducing the fixed cost component in the equation by this amount.

Design W was recommended and accepted. As prototypes of the design were tested, an additional benefit emerged. Based on test results, the post-purchase costs dropped from an estimated $0.70 per unit sold to $0.40 per unit sold. Using this information, the Marketing Department revised the projected market share upward from 50 percent to 60 percent (with no price decrease).

Required:

1. Calculate the expected gross profit per unit for Design Z using the controller's original cost formula. According to this outcome, does Design Z reach the targeted unit profit? Repeat, using the engineer's revised cost formula. Explain why Design Z failed to meet the targeted profit. What does this say about the use of unit-based costing for life-cycle cost management?

2. Calculate the expected profit per unit using Design W. Comment on the value of activity information for life-cycle cost management.

3. The benefit of the post-purchase cost reduction of Design W was discovered in testing. What direct benefit did it create for Feagan Company (in dollars)? Reducing post-purchase costs was not a specific design objective. Should it have been? Are there any other design objectives that should have been considered?

Question

Question

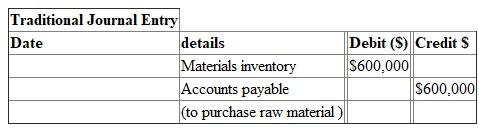

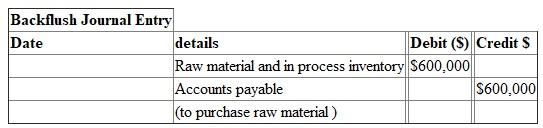

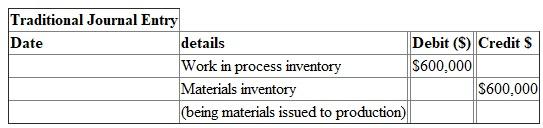

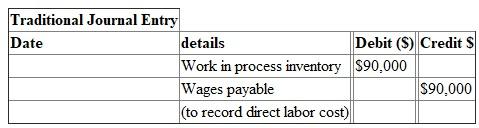

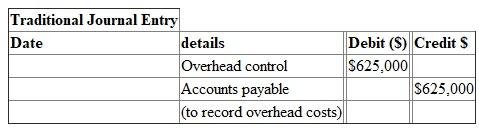

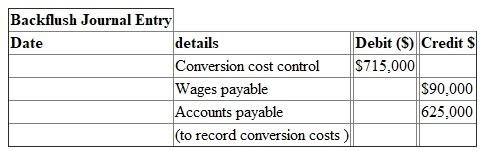

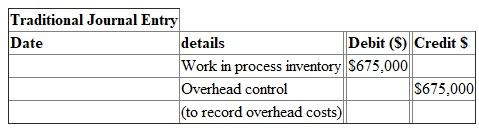

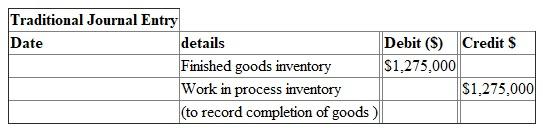

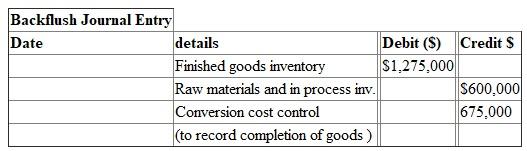

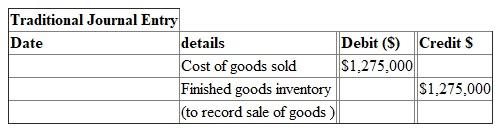

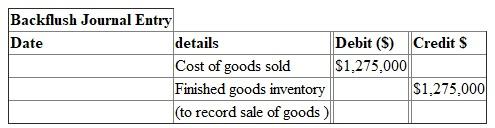

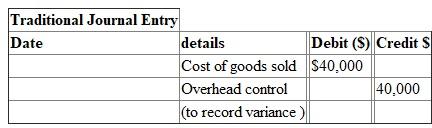

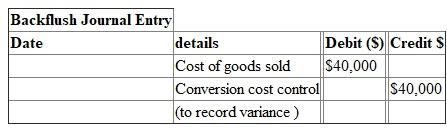

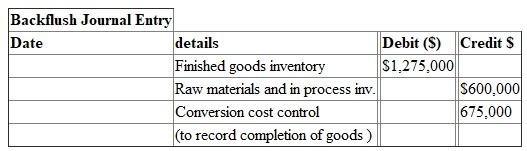

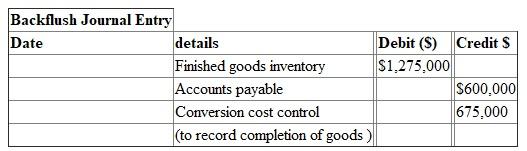

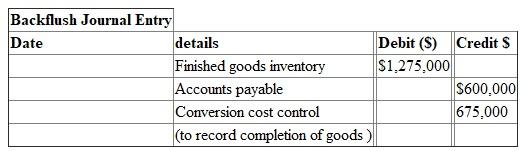

Backflush versus Traditional Costing: Variation 1

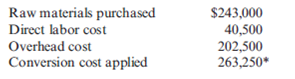

Potter Company has installed a JIT purchasing and manufacturing system and is using backflush accounting for its cost flows. It currently uses a two-trigger approach with the purchase of materials as the first trigger point and the completion of goods as the second trigger point. During the month of June, Potter had the following transactions:

* $40,500 labor plus $222,750 overhead.

There were no beginning or ending inventories. All goods produced were sold with a 60 percent markup. Any variance is closed to Cost of Goods Sold. (Variances are recognized monthly.)

Required:

1. Prepare the journal entries that would have been made using a traditional accounting approach for cost flows.

2. Prepare the journal entries for the month using backflush costing.

Potter Company has installed a JIT purchasing and manufacturing system and is using backflush accounting for its cost flows. It currently uses a two-trigger approach with the purchase of materials as the first trigger point and the completion of goods as the second trigger point. During the month of June, Potter had the following transactions:

* $40,500 labor plus $222,750 overhead.

There were no beginning or ending inventories. All goods produced were sold with a 60 percent markup. Any variance is closed to Cost of Goods Sold. (Variances are recognized monthly.)

Required:

1. Prepare the journal entries that would have been made using a traditional accounting approach for cost flows.

2. Prepare the journal entries for the month using backflush costing.

Question

JIT, Traceability of Costs, Product Costing Accuracy, JIT Effects on Cost Accounting Systems

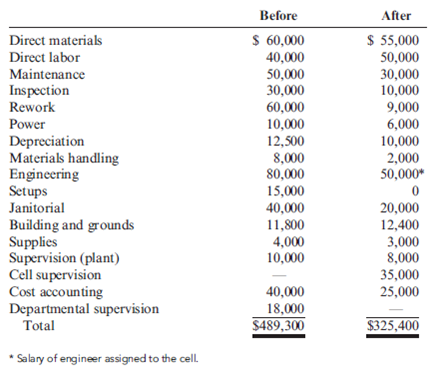

Homer Manufacturing produces different models of 22-calibre rifles. The manufacturing costs assigned to its economy model rifle before and after installing JIT are given in the following table. Cell workers do all maintenance and are also responsible for moving materials, cell janitorial work, and inspecting products. Janitorial work outside the cells is still handled by the Janitorial Department.

In both the pre- and post-JIT setting, 10,000 units of the economy model are manufactured. In the JIT setting, manufacturing cells are used to produce each product. The management of Homer Manufacturing reported a significant decrease in manufacturing costs for all of its rifles after JIT was installed. It also reported less inventory-related costs and a significant decrease in lead times. Accounting costs also decreased because Homer switched from a job-order costing system to a process-costing system.

Required:

1. Compute the unit cost of the product before and after JIT.

2. Explain why the JIT unit cost is more accurate. Also explain what JIT features may have produced a decrease in production costs. Use as many specific cost items as possible to illustrate your explanation.

3. Explain why Homer Manufacturing switched from a job-order costing system to a process- costing system after JIT was implemented.

4. Classify the costs in the JIT environment according to how they are assigned to the cell: direct tracing, driver tracing, or allocation. Which cost assignment method is most common? What does this imply regarding product-costing accuracy?

Homer Manufacturing produces different models of 22-calibre rifles. The manufacturing costs assigned to its economy model rifle before and after installing JIT are given in the following table. Cell workers do all maintenance and are also responsible for moving materials, cell janitorial work, and inspecting products. Janitorial work outside the cells is still handled by the Janitorial Department.

In both the pre- and post-JIT setting, 10,000 units of the economy model are manufactured. In the JIT setting, manufacturing cells are used to produce each product. The management of Homer Manufacturing reported a significant decrease in manufacturing costs for all of its rifles after JIT was installed. It also reported less inventory-related costs and a significant decrease in lead times. Accounting costs also decreased because Homer switched from a job-order costing system to a process-costing system.

Required:

1. Compute the unit cost of the product before and after JIT.

2. Explain why the JIT unit cost is more accurate. Also explain what JIT features may have produced a decrease in production costs. Use as many specific cost items as possible to illustrate your explanation.

3. Explain why Homer Manufacturing switched from a job-order costing system to a process- costing system after JIT was implemented.

4. Classify the costs in the JIT environment according to how they are assigned to the cell: direct tracing, driver tracing, or allocation. Which cost assignment method is most common? What does this imply regarding product-costing accuracy?

Question

Question

Question

JIT and Product Costing

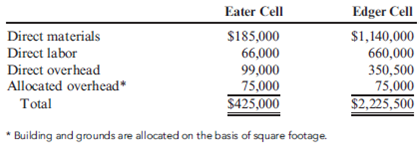

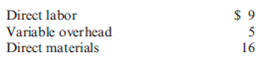

Mott Company recently implemented a JIT manufacturing system. After one year of operation, Heidi Burrows, president of the company, wanted to compare product cost under the JIT system with product cost under the old system. Mott's two products are weed eaters and lawn edgers. The unit prime costs under the old system are as follows:

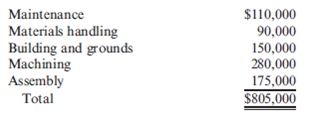

Under the old manufacturing system, the company operated three service centers and two production departments. Overhead was applied using departmental overhead rates. The direct overhead costs associated with each department for the year preceding the installation of JIT are as follows:

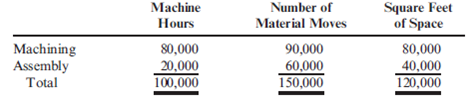

Under the old system, the overhead costs of the service departments were allocated directly to the producing departments and then to the products passing through them. (Both products passed through each producing department.) The overhead rate for the Machining Department was based on machine hours, and the overhead rate for assembly was based on direct labor hours. During the last year of operations for the old system, the Machining Department used 80,000 machine hours, and the Assembly Department used 20,000 direct labor hours. Each weed eater required 1.0 machine hour in Machining and 0.25 direct labor hour in Assembly. Each lawn edger required 2.0 machine hours in Machining and 0.5 hour in Assembly. Bases for allocation of the service costs are as follows:

Upon implementing JIT, a manufacturing cell for each product was created to replace the departmental structure. Each cell occupied 40,000 square feet. Maintenance and materials handling were both decentralized to the cell level. Essentially, cell workers were trained to operate the machines in each cell, assemble the components, maintain the machines, and move the partially completed units from one point to the next within the cell. During the first year of the JIT system, the company produced and sold 20,000 weed eaters and 30,000 lawn edgers. This output was identical to that for the last year of operations under the old system. The following costs have been assigned to the manufacturing cells:

Required:

1. Compute the unit cost for each product under the old manufacturing system.

2. Compute the unit cost for each product under the JIT system.

3. Which of the unit costs is more accurate? Explain. Include in your explanation a discussion of how the computational approaches differ.

4. Calculate the decrease in overhead costs under JIT, and provide some possible reasons that explain the decrease.

Mott Company recently implemented a JIT manufacturing system. After one year of operation, Heidi Burrows, president of the company, wanted to compare product cost under the JIT system with product cost under the old system. Mott's two products are weed eaters and lawn edgers. The unit prime costs under the old system are as follows:

Under the old manufacturing system, the company operated three service centers and two production departments. Overhead was applied using departmental overhead rates. The direct overhead costs associated with each department for the year preceding the installation of JIT are as follows:

Under the old system, the overhead costs of the service departments were allocated directly to the producing departments and then to the products passing through them. (Both products passed through each producing department.) The overhead rate for the Machining Department was based on machine hours, and the overhead rate for assembly was based on direct labor hours. During the last year of operations for the old system, the Machining Department used 80,000 machine hours, and the Assembly Department used 20,000 direct labor hours. Each weed eater required 1.0 machine hour in Machining and 0.25 direct labor hour in Assembly. Each lawn edger required 2.0 machine hours in Machining and 0.5 hour in Assembly. Bases for allocation of the service costs are as follows:

Upon implementing JIT, a manufacturing cell for each product was created to replace the departmental structure. Each cell occupied 40,000 square feet. Maintenance and materials handling were both decentralized to the cell level. Essentially, cell workers were trained to operate the machines in each cell, assemble the components, maintain the machines, and move the partially completed units from one point to the next within the cell. During the first year of the JIT system, the company produced and sold 20,000 weed eaters and 30,000 lawn edgers. This output was identical to that for the last year of operations under the old system. The following costs have been assigned to the manufacturing cells:

Required:

1. Compute the unit cost for each product under the old manufacturing system.

2. Compute the unit cost for each product under the JIT system.

3. Which of the unit costs is more accurate? Explain. Include in your explanation a discussion of how the computational approaches differ.

4. Calculate the decrease in overhead costs under JIT, and provide some possible reasons that explain the decrease.

Question

Question

Question

Backflush Costing, Conversion Rate

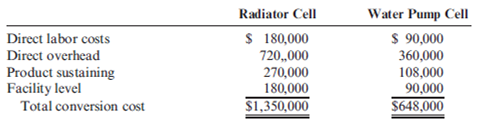

Southward Company has implemented a JIT flexible manufacturing system. John Richins, controller of the company, has decided to reduce the accounting requirements given the expectation of lower inventories. For one thing, he has decided to treat direct labor cost as a part of overhead and to discontinue the detailed direct labor accounting of the past. The company has created two manufacturing cells, each capable of producing a family of products: the radiator cell and the water pump cell. The output of both cells is sold to a sister division and to customers who use the radiators and water pumps for repair activity. Product-level overhead costs outside the cells are assigned to each cell using appropriate drivers. Facility-level costs are allocated to each cell on the basis of square footage. The budgeted direct labor and overhead costs are as follows:

The predetermined conversion cost rate is based on available production hours in each cell. The radiator cell has 45,000 hours available for production, and the water pump cell has 27,000 hours. Conversion costs are applied to the units produced by multiplying the conversion rate by the actual time required to produce the units. The radiator cell produced 81,000 units, taking 0.5 hour to produce one unit of product (on average). The water pump cell produced 90,000 units, taking 0.25 hour to produce one unit of product (on average).

Other actual results for the year are as follows:

All units produced were sold. Any conversion cost variance is closed to Cost of Goods Sold.

Required:

1. Calculate the predetermined conversion cost rates for each cell.

2. Prepare journal entries using backflush accounting. Assume two trigger points, with completion of goods as the second trigger point.

3. Repeat Requirement 2, assuming that the second trigger point is the sale of the goods.

4. Explain why there is no need to have a work-in-process inventory account.

5. Two variants of backflush costing were presented in which each used two trigger points, with the second trigger point differing. Suppose that the only trigger point for recognizing manufacturing costs occurs when the goods are sold. How would the entries be listed here? When would this backflush variant be considered appropriate?

Southward Company has implemented a JIT flexible manufacturing system. John Richins, controller of the company, has decided to reduce the accounting requirements given the expectation of lower inventories. For one thing, he has decided to treat direct labor cost as a part of overhead and to discontinue the detailed direct labor accounting of the past. The company has created two manufacturing cells, each capable of producing a family of products: the radiator cell and the water pump cell. The output of both cells is sold to a sister division and to customers who use the radiators and water pumps for repair activity. Product-level overhead costs outside the cells are assigned to each cell using appropriate drivers. Facility-level costs are allocated to each cell on the basis of square footage. The budgeted direct labor and overhead costs are as follows:

The predetermined conversion cost rate is based on available production hours in each cell. The radiator cell has 45,000 hours available for production, and the water pump cell has 27,000 hours. Conversion costs are applied to the units produced by multiplying the conversion rate by the actual time required to produce the units. The radiator cell produced 81,000 units, taking 0.5 hour to produce one unit of product (on average). The water pump cell produced 90,000 units, taking 0.25 hour to produce one unit of product (on average).

Other actual results for the year are as follows:

All units produced were sold. Any conversion cost variance is closed to Cost of Goods Sold.

Required:

1. Calculate the predetermined conversion cost rates for each cell.

2. Prepare journal entries using backflush accounting. Assume two trigger points, with completion of goods as the second trigger point.

3. Repeat Requirement 2, assuming that the second trigger point is the sale of the goods.

4. Explain why there is no need to have a work-in-process inventory account.

5. Two variants of backflush costing were presented in which each used two trigger points, with the second trigger point differing. Suppose that the only trigger point for recognizing manufacturing costs occurs when the goods are sold. How would the entries be listed here? When would this backflush variant be considered appropriate?

Question

Exploiting Internal Linkages

Woodruff Company is currently producing a snowmobile that uses five specialized parts. Engineering has proposed replacing these specialized parts with commodity parts, which will cost less and can be purchased in larger order quantities. Current activity capacity and demand (with specialized parts required) and expected activity demand (with only commodity parts required) are provided.

Additionally, the following activity cost data are provided:

Material usage : $20 per specialized part used; $16 per commodity part; no fixed activity cost. Installing parts : $14 per direct labor hour; no fixed activity cost. Purchasing parts: Four salaried clerks, each earning a $45,000 annual salary; each clerk is capable of processing 5,000 purchase orders. Variable activity costs: $0.80 per purchase order processed for forms, postage, etc.

Required:

1. Calculate the cost reduction produced by using commodity parts instead of specialized parts.

2. Suppose that 50,000 units are being produced and sold for $8,800 per unit and that the price per unit will be reduced by the per-unit savings. What is the new price for the configured product?

3. What if the expected activity demand for purchase orders was 8,500? How would this affect the answers to Requirements 1 and 2?

Woodruff Company is currently producing a snowmobile that uses five specialized parts. Engineering has proposed replacing these specialized parts with commodity parts, which will cost less and can be purchased in larger order quantities. Current activity capacity and demand (with specialized parts required) and expected activity demand (with only commodity parts required) are provided.

Additionally, the following activity cost data are provided:

Material usage : $20 per specialized part used; $16 per commodity part; no fixed activity cost. Installing parts : $14 per direct labor hour; no fixed activity cost. Purchasing parts: Four salaried clerks, each earning a $45,000 annual salary; each clerk is capable of processing 5,000 purchase orders. Variable activity costs: $0.80 per purchase order processed for forms, postage, etc.

Required:

1. Calculate the cost reduction produced by using commodity parts instead of specialized parts.

2. Suppose that 50,000 units are being produced and sold for $8,800 per unit and that the price per unit will be reduced by the per-unit savings. What is the new price for the configured product?

3. What if the expected activity demand for purchase orders was 8,500? How would this affect the answers to Requirements 1 and 2?

Question

Question

Cost Assignment and JIT

Bunker Company produces two types of glucose monitors (basic and advanced). Both pass through two producing departments: Fabrication and Assembly. Bunker also has an Inspection Department that is responsible for testing monitors to ensure that they perform within prespecified tolerance ranges (a sampling procedure is used). Budgeted data for the three departments are as follows:

In the Fabrication Department, the basic model requires 0.5 hour of direct labor and the advanced model requires 1.0 hour. In the Assembly Department, the basic model requires 0.7 hour of direct labor and the advanced model requires 1.25 hours. There are 45,000 basic units produced and 24,000 advanced units.

Immediately after preparing the budgeted data, a consultant suggests that two manufacturing cells be created: one for the manufacture of the basic model and the other for the manufacture of the advanced model. Raw materials would be delivered to each cell, and goods would be shipped immediately to customers upon completion. Workers within each cell would also be trained to perform monitor testing. The total direct overhead costs estimated for each cell would be $228,000 for the basic cell and $720,000 for the advanced cell.

Required:

1. Allocate the inspection costs to each department, and compute the overhead cost per unit for each monitor. (Overhead rates use direct labor hours.)

2. Compute the overhead cost per unit if manufacturing cells are created. Which unit overhead cost do you think is more accurate-the one computed with a departmental structure, or the one computed using a cell structure? Explain.

3. Note that the total overhead costs for the cell structure are lower. Explain why.

Bunker Company produces two types of glucose monitors (basic and advanced). Both pass through two producing departments: Fabrication and Assembly. Bunker also has an Inspection Department that is responsible for testing monitors to ensure that they perform within prespecified tolerance ranges (a sampling procedure is used). Budgeted data for the three departments are as follows:

In the Fabrication Department, the basic model requires 0.5 hour of direct labor and the advanced model requires 1.0 hour. In the Assembly Department, the basic model requires 0.7 hour of direct labor and the advanced model requires 1.25 hours. There are 45,000 basic units produced and 24,000 advanced units.

Immediately after preparing the budgeted data, a consultant suggests that two manufacturing cells be created: one for the manufacture of the basic model and the other for the manufacture of the advanced model. Raw materials would be delivered to each cell, and goods would be shipped immediately to customers upon completion. Workers within each cell would also be trained to perform monitor testing. The total direct overhead costs estimated for each cell would be $228,000 for the basic cell and $720,000 for the advanced cell.

Required:

1. Allocate the inspection costs to each department, and compute the overhead cost per unit for each monitor. (Overhead rates use direct labor hours.)

2. Compute the overhead cost per unit if manufacturing cells are created. Which unit overhead cost do you think is more accurate-the one computed with a departmental structure, or the one computed using a cell structure? Explain.

3. Note that the total overhead costs for the cell structure are lower. Explain why.

Question

JIT, Creation of Manufacturing Cells, Behavioral Considerations, Impact on Costing Practices

Reddy Heaters, Inc., produces insert heaters that can be used for various applications, ranging from coffeepots to submarines. Because of the wide variety of insert heaters produced, Reddy uses a job-order costing system. Product lines are differentiated by the size of the heater. In the early stages of the company's history, sales were strong and profits steadily increased. In recent years, however, profits have been declining, and the company has been losing market share. Alarmed by the deteriorating financial position of the company, President Doug Young requested a special study to identify the problems. Sheri Butler, the head of the Internal Audit Department, was put in charge of the study. After two months of investigation, Sheri was ready to report her findings.

SHERI : Doug, I think we have some real concerns that need to be addressed. Production is down, employee morale is low, and the number of defective units that we have to scrap is way up. In fact, over the past several years, our scrap rate has increased from 9 percent to 15 percent of total production. And scrap is expensive. We don't detect defective units until the end of the process. By that time, we lose everything. The nature of the product simply doesn't permit rework.

DOUG : I have a feeling that the increased scrap rate is related to the morale problem you've encountered. Do you have any feel for why morale is low?

SHERI : I get the feeling that boredom is a factor. Many employees don't feel challenged by their work. Also, with the decline in performance, they are receiving more pressure from their supervisors, which simply aggravates the problem.

DOUG : What other problems have you detected?

SHERI : Well, much of our market share has been lost to foreign competitors. The time it takes us to process an order, from time of receipt to delivery, has increased from 20 to 30 days. Some of the customers we have lost have switched to Japanese suppliers, from whom they receive heaters in less than 15 days. Added to this delay in our delivery is an increase in the number of complaints about poorly performing heaters. Our quality has definitely taken a nosedive over the past several years.

DOUG : It's amazing that it has taken us this long to spot these problems. It's incredible to me that the Japanese can deliver a part faster than we can, even in our more efficient days. I wonder what their secret is.

SHERI : I investigated that very issue. It appears that they can produce and deliver their heaters rapidly because they use a JIT purchasing and manufacturing system.

DOUG : Can we use this system to increase our competitive ability?

SHERI : I think so, but we'll need to hire a consultant to tell us how to do it. Also, it might be a good idea to try it out on only one of our major product lines. I suggest the small heater line. It is having the most problems and has been showing a loss for the past two years. If JIT can restore this line to a competitive mode, then it'll work for the other lines as well.

Within a week, Reddy Heaters hired the services of a large CPA firm. The firm sent Kim Burnham, one of its managers, to do the initial background work. After spending some time at the plant, Kim wrote up the following description of the small heater production process:

The various departments are scattered throughout the factory. Labor is specialized and trained to operate the machines in the respective departments. Additionally, the company has a centralized stores area that provides the raw materials for production, a centralized Maintenance Department that has responsibility for maintaining all production equipment, and a group of laborers responsible for moving the partially completed units from department to department.

Under the current method ofproduction, small heaters pass through several departments, where each department has a collection of similar machines. The first department cuts a metal pipe into one of three lengths: three, four, or five inches long. The cut pipe is then taken to the Laser Department, where the part number is printed on the pipe. In a second department, ceramic cylinders-cut to smaller lengths than the pipe-are wrapped with a fine wire (using a wrapping machine). The pipe and the wrapped ceramic cylinders are then taken to the Welding Department, where the wrapped ceramic cylinders are placed inside the pipe, centered, and filled with a substance that prevents electricity from reaching the metal pipe. Finally, the ends of the pipe are welded shut with two wire leads protruding from one end. This completed heater is then transferred to the Testing Department, which uses special equipment to see if the heater functions properly.

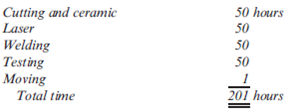

The small heaters are produced in batches of 300. It takes 50 hours to cut 300 metal pipes and prepare 300 ceramic cylinders (1/6 hour per unit, both processes occurring at the same time). After 50 hours of production time, the 300 metal pipes are transported to the Laser Department (20 minutes transport time), and the 300 ceramic cylinders are transported to the Welding Department (20 minutes transport time). In the Laser Department, it takes 50 hours to imprint the part number (1/6 hour per pipe). The 300 metal pipes are then transported to the Welding Department. In the Welding Department, the ceramic and metal pipes are joined and welded. The welding process takes 50 hours (1/6 hour per pipe). Finally, the 300 units are transported (20 minutes) to the Testing Department. Each unit requires 1/6 hour for testing, or a total of 50 hours for the 300 units. From start to finish, the total production time for the 300 units is as follows:

Notice that Laser must wait 50 hours before it can begin imprinting. Similarly, Welding must wait 100 hours before it can begin working on the batch, and finally, Testing must wait 150 hours before it can begin working on the batch.

Based on the information gathered, Kim estimated that the production time for 300 units could be cut from 201 hours to about 50 hours by creating a small heater manufacturing cell.

Required:

1. One of the first actions taken by Reddy Heaters was to organize a manufacturing cell for the small heater line. Describe how you would organize the manufacturing cell. How does it differ from the traditional arrangement? Will any training costs be associated with the transition to JIT? Explain.

2. Explain, with computational support, how the production time for 300 units can be reduced to about 50 hours. If this is a true reduction in production time, what implications does it have for Reddy's competitive position?

3. Describe the organizational and operational activities that must be managed to bring about the reduction in production time. What are the cost drivers associated with these activities? For operational drivers, indicate the expected effect on activity costs.

4. Initially, the employees resented the change to JIT. After a small period of time, however, morale improved significantly. Explain why the change to JIT increased employee morale.

5. Within a few months, Reddy was able to offer a lower price for its small heaters. Additionally, the number of complaints about the performance of the small heaters declined sharply. By the end of the second year, the product line was reporting profits greater than had ever been achieved. Discuss the JIT features that may have made the lower price and higher profits possible.

6. Within a year of the JIT installation, Reddy's controller remarked, "We have a much better idea than ever before of what it is costing us to produce these small insert heaters." Offer some justification for the controller's statement.

7. Discuss the impact that JIT has on other management accounting practices.

Reddy Heaters, Inc., produces insert heaters that can be used for various applications, ranging from coffeepots to submarines. Because of the wide variety of insert heaters produced, Reddy uses a job-order costing system. Product lines are differentiated by the size of the heater. In the early stages of the company's history, sales were strong and profits steadily increased. In recent years, however, profits have been declining, and the company has been losing market share. Alarmed by the deteriorating financial position of the company, President Doug Young requested a special study to identify the problems. Sheri Butler, the head of the Internal Audit Department, was put in charge of the study. After two months of investigation, Sheri was ready to report her findings.

SHERI : Doug, I think we have some real concerns that need to be addressed. Production is down, employee morale is low, and the number of defective units that we have to scrap is way up. In fact, over the past several years, our scrap rate has increased from 9 percent to 15 percent of total production. And scrap is expensive. We don't detect defective units until the end of the process. By that time, we lose everything. The nature of the product simply doesn't permit rework.

DOUG : I have a feeling that the increased scrap rate is related to the morale problem you've encountered. Do you have any feel for why morale is low?

SHERI : I get the feeling that boredom is a factor. Many employees don't feel challenged by their work. Also, with the decline in performance, they are receiving more pressure from their supervisors, which simply aggravates the problem.

DOUG : What other problems have you detected?

SHERI : Well, much of our market share has been lost to foreign competitors. The time it takes us to process an order, from time of receipt to delivery, has increased from 20 to 30 days. Some of the customers we have lost have switched to Japanese suppliers, from whom they receive heaters in less than 15 days. Added to this delay in our delivery is an increase in the number of complaints about poorly performing heaters. Our quality has definitely taken a nosedive over the past several years.

DOUG : It's amazing that it has taken us this long to spot these problems. It's incredible to me that the Japanese can deliver a part faster than we can, even in our more efficient days. I wonder what their secret is.

SHERI : I investigated that very issue. It appears that they can produce and deliver their heaters rapidly because they use a JIT purchasing and manufacturing system.

DOUG : Can we use this system to increase our competitive ability?

SHERI : I think so, but we'll need to hire a consultant to tell us how to do it. Also, it might be a good idea to try it out on only one of our major product lines. I suggest the small heater line. It is having the most problems and has been showing a loss for the past two years. If JIT can restore this line to a competitive mode, then it'll work for the other lines as well.

Within a week, Reddy Heaters hired the services of a large CPA firm. The firm sent Kim Burnham, one of its managers, to do the initial background work. After spending some time at the plant, Kim wrote up the following description of the small heater production process:

The various departments are scattered throughout the factory. Labor is specialized and trained to operate the machines in the respective departments. Additionally, the company has a centralized stores area that provides the raw materials for production, a centralized Maintenance Department that has responsibility for maintaining all production equipment, and a group of laborers responsible for moving the partially completed units from department to department.

Under the current method ofproduction, small heaters pass through several departments, where each department has a collection of similar machines. The first department cuts a metal pipe into one of three lengths: three, four, or five inches long. The cut pipe is then taken to the Laser Department, where the part number is printed on the pipe. In a second department, ceramic cylinders-cut to smaller lengths than the pipe-are wrapped with a fine wire (using a wrapping machine). The pipe and the wrapped ceramic cylinders are then taken to the Welding Department, where the wrapped ceramic cylinders are placed inside the pipe, centered, and filled with a substance that prevents electricity from reaching the metal pipe. Finally, the ends of the pipe are welded shut with two wire leads protruding from one end. This completed heater is then transferred to the Testing Department, which uses special equipment to see if the heater functions properly.

The small heaters are produced in batches of 300. It takes 50 hours to cut 300 metal pipes and prepare 300 ceramic cylinders (1/6 hour per unit, both processes occurring at the same time). After 50 hours of production time, the 300 metal pipes are transported to the Laser Department (20 minutes transport time), and the 300 ceramic cylinders are transported to the Welding Department (20 minutes transport time). In the Laser Department, it takes 50 hours to imprint the part number (1/6 hour per pipe). The 300 metal pipes are then transported to the Welding Department. In the Welding Department, the ceramic and metal pipes are joined and welded. The welding process takes 50 hours (1/6 hour per pipe). Finally, the 300 units are transported (20 minutes) to the Testing Department. Each unit requires 1/6 hour for testing, or a total of 50 hours for the 300 units. From start to finish, the total production time for the 300 units is as follows:

Notice that Laser must wait 50 hours before it can begin imprinting. Similarly, Welding must wait 100 hours before it can begin working on the batch, and finally, Testing must wait 150 hours before it can begin working on the batch.

Based on the information gathered, Kim estimated that the production time for 300 units could be cut from 201 hours to about 50 hours by creating a small heater manufacturing cell.

Required:

1. One of the first actions taken by Reddy Heaters was to organize a manufacturing cell for the small heater line. Describe how you would organize the manufacturing cell. How does it differ from the traditional arrangement? Will any training costs be associated with the transition to JIT? Explain.

2. Explain, with computational support, how the production time for 300 units can be reduced to about 50 hours. If this is a true reduction in production time, what implications does it have for Reddy's competitive position?

3. Describe the organizational and operational activities that must be managed to bring about the reduction in production time. What are the cost drivers associated with these activities? For operational drivers, indicate the expected effect on activity costs.

4. Initially, the employees resented the change to JIT. After a small period of time, however, morale improved significantly. Explain why the change to JIT increased employee morale.

5. Within a few months, Reddy was able to offer a lower price for its small heaters. Additionally, the number of complaints about the performance of the small heaters declined sharply. By the end of the second year, the product line was reporting profits greater than had ever been achieved. Discuss the JIT features that may have made the lower price and higher profits possible.

6. Within a year of the JIT installation, Reddy's controller remarked, "We have a much better idea than ever before of what it is costing us to produce these small insert heaters." Offer some justification for the controller's statement.

7. Discuss the impact that JIT has on other management accounting practices.

Question

Question

Operational and Organizational Activities

McConkie Company has decided to pursue a cost leadership strategy. This decision is prompted, in part, by increased competition from foreign firms. McConkie's management is confident that costs can be reduced by more efficient management of the firm's operational activities. Improving operational activity efficiency, however, often requires some strategic changes in organizational activities. McConkie currently uses a very traditional manufacturing approach. Plants are organized along departmental lines. Management follows a typical pyramid structure. Labor is specialized and located in departments. Quality management follows a conventional acceptable quality level approach. (Batches of products are accepted if the number of defective units is below some predetermined level.) Materials are purchased from a large number of suppliers, and sizable inventories of materials, work in process, and finished goods are maintained. The company produces many different products that use a variety of different parts, many of which are purchased from suppliers.

Required:

Given this brief description of the firm and its setting, for each of the following operational activities and their associated drivers, suggest some strategic changes in organizational activities (and drivers) that might reduce the cost of performing the indicated operational activity. Explain your reasoning.

McConkie Company has decided to pursue a cost leadership strategy. This decision is prompted, in part, by increased competition from foreign firms. McConkie's management is confident that costs can be reduced by more efficient management of the firm's operational activities. Improving operational activity efficiency, however, often requires some strategic changes in organizational activities. McConkie currently uses a very traditional manufacturing approach. Plants are organized along departmental lines. Management follows a typical pyramid structure. Labor is specialized and located in departments. Quality management follows a conventional acceptable quality level approach. (Batches of products are accepted if the number of defective units is below some predetermined level.) Materials are purchased from a large number of suppliers, and sizable inventories of materials, work in process, and finished goods are maintained. The company produces many different products that use a variety of different parts, many of which are purchased from suppliers.

Required: