Deck 10: Decentralization: Responsibility Accounting, Performance

Full screen (f)

Question

Question

Question

Setting Transfer Prices-Market Price versus Full Cost

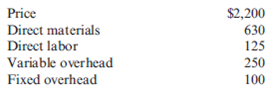

Ardmore, Inc., manufactures heating and air conditioning units in its six divisions. One division, the Components Division, produces electronic components that can be used by the other five. All the components produced by this division can be sold to outside customers; however, from the beginning, about 70 percent of its output has been used internally. The current policy requires that all internal transfers of components be transferred at full cost.

Recently, Cynthia Busby, the new chief executive officer of Ardmore, decided to investigate the transfer pricing policy. She was concerned that the current method of pricing internal transfers might force decisions by divisional managers that would be suboptimal for the firm. As part of her inquiry, she gathered some information concerning Part 4CM, used by the Small AC Division in its production of a window air conditioner, Model 7AC.

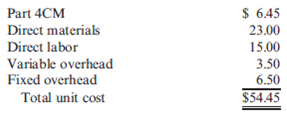

The Small AC Division sells 10,000 units of Model 7AC each year at a unit price of $58. Given current market conditions, this is the maximum price that the division can charge for Model 7AC. The cost of manufacturing the air conditioner is computed as follows:

The window unit is produced efficiently, and no further reduction in manufacturing costs is possible.

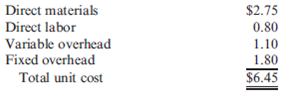

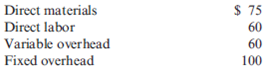

The manager of the Components Division indicated that he could sell 10,000 units (the division's capacity for this part) of Part 4CM to outside buyers at $12 per unit. The Small AC Division could also buy the part for $12 from external suppliers. The following detail on the manufacturing cost of the component was provided:

Required:

1. Compute the firmwide contribution margin associated with Part 4CM and Model 7AC. Also, compute the contribution margin earned by each division.

2. Suppose that Cynthia Busby abolishes the current transfer pricing policy and gives divisions autonomy in setting transfer prices. Can you predict what transfer price the manager of the Components Division will set? What should be the minimum transfer price for this part? The maximum transfer price?

3. Given the new transfer pricing policy, predict how this will affect the production decision for Model 7AC of the manager of the Small AC Division. How many units of Part 4CM will the manager of the Small AC Division purchase, either internally or externally?

4. Given the new transfer price set by the Components Division and your answer to Requirement 3, how many units of 4CM will be sold externally?

Ardmore, Inc., manufactures heating and air conditioning units in its six divisions. One division, the Components Division, produces electronic components that can be used by the other five. All the components produced by this division can be sold to outside customers; however, from the beginning, about 70 percent of its output has been used internally. The current policy requires that all internal transfers of components be transferred at full cost.

Recently, Cynthia Busby, the new chief executive officer of Ardmore, decided to investigate the transfer pricing policy. She was concerned that the current method of pricing internal transfers might force decisions by divisional managers that would be suboptimal for the firm. As part of her inquiry, she gathered some information concerning Part 4CM, used by the Small AC Division in its production of a window air conditioner, Model 7AC.

The Small AC Division sells 10,000 units of Model 7AC each year at a unit price of $58. Given current market conditions, this is the maximum price that the division can charge for Model 7AC. The cost of manufacturing the air conditioner is computed as follows:

The window unit is produced efficiently, and no further reduction in manufacturing costs is possible.

The manager of the Components Division indicated that he could sell 10,000 units (the division's capacity for this part) of Part 4CM to outside buyers at $12 per unit. The Small AC Division could also buy the part for $12 from external suppliers. The following detail on the manufacturing cost of the component was provided:

Required:

1. Compute the firmwide contribution margin associated with Part 4CM and Model 7AC. Also, compute the contribution margin earned by each division.

2. Suppose that Cynthia Busby abolishes the current transfer pricing policy and gives divisions autonomy in setting transfer prices. Can you predict what transfer price the manager of the Components Division will set? What should be the minimum transfer price for this part? The maximum transfer price?

3. Given the new transfer pricing policy, predict how this will affect the production decision for Model 7AC of the manager of the Small AC Division. How many units of Part 4CM will the manager of the Small AC Division purchase, either internally or externally?

4. Given the new transfer price set by the Components Division and your answer to Requirement 3, how many units of 4CM will be sold externally?

Question

Question

Question

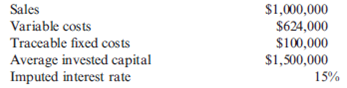

Transfer Pricing with Idle Capacity

Oriole, Inc., owns a number of food service companies. Two divisions are the Coffee Division and the Donut Shop Division. The Coffee Division purchases and roasts coffee beans for sale to supermarkets and specialty shops. The Donut Shop Division operates a chain of donut shops where the donuts are made on the premises. Coffee is an important item for sale along with the donuts and, to date, has been purchased from the Coffee Division. Company policy permits each manager the freedom to decide whether or not to buy or sell internally. Each divisional manager is evaluated on the basis of return on investment and residual income.

Recently, an outside supplier has offered to sell coffee beans, roasted and ground, to the Donut Shop Division for $4.30 per pound. Since the current price paid to the Coffee Division is $4.75 per pound, Ashleigh Tremont, the manager of the Donut Shop Division, was interested in the offer. However, before making the decision to switch to the outside supplier, she decided to approach Santigui Melendez, manager of the Coffee Division, to see if he wanted to offer an even better price. If not, then Ashleigh would buy from the outside supplier.

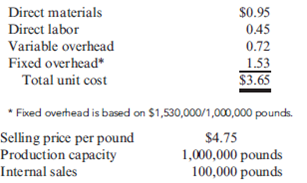

Upon receiving the information from Ashleigh about the outside offer, Santigui gathered the following information about the coffee:

Required:

1. Suppose that the Coffee Division is producing at capacity and can sell all that it produces to outside customers. How should Santigui respond to Ashleigh's request for a lower transfer price? What will be the effect on firmwide profits? Compute the effect of this response on each division's profits.

2. Now, assume that the Coffee Division is currently selling 950,000 pounds. If no units are sold internally, total coffee sales will drop to 850,000 pounds. Suppose that Santigui refuses to lower the transfer price from $4.75 and the Donut Division purchases from the external supplier. Compute the effect on each division's profits and on the profits of the firm as a whole.

3. Refer to Requirement 2. What are the minimum and maximum transfer prices? Suppose that the transfer price is set at the maximum price less $1. Will the two divisions accept this transfer price? Compute the effect on the firm's profits and on each division's profits.

4. Suppose that the Coffee Division has operating assets of $2,000,000. Assume that the Coffee Division sells 850,000 pounds to outsiders and 100,000 pounds to the Donut Division at a price of $4.75 per pound. What is divisional ROI (rounded to four significant digits) based on this situation? Now, refer to Requirement 3. What will divisional ROI (rounded to four significant digits) be if the transfer price of the maximum price less $1 is implemented? How will the change in ROI affect Santigui? What information has he gained as a result of the transfer pricing negotiations?

Oriole, Inc., owns a number of food service companies. Two divisions are the Coffee Division and the Donut Shop Division. The Coffee Division purchases and roasts coffee beans for sale to supermarkets and specialty shops. The Donut Shop Division operates a chain of donut shops where the donuts are made on the premises. Coffee is an important item for sale along with the donuts and, to date, has been purchased from the Coffee Division. Company policy permits each manager the freedom to decide whether or not to buy or sell internally. Each divisional manager is evaluated on the basis of return on investment and residual income.

Recently, an outside supplier has offered to sell coffee beans, roasted and ground, to the Donut Shop Division for $4.30 per pound. Since the current price paid to the Coffee Division is $4.75 per pound, Ashleigh Tremont, the manager of the Donut Shop Division, was interested in the offer. However, before making the decision to switch to the outside supplier, she decided to approach Santigui Melendez, manager of the Coffee Division, to see if he wanted to offer an even better price. If not, then Ashleigh would buy from the outside supplier.

Upon receiving the information from Ashleigh about the outside offer, Santigui gathered the following information about the coffee:

Required:

1. Suppose that the Coffee Division is producing at capacity and can sell all that it produces to outside customers. How should Santigui respond to Ashleigh's request for a lower transfer price? What will be the effect on firmwide profits? Compute the effect of this response on each division's profits.

2. Now, assume that the Coffee Division is currently selling 950,000 pounds. If no units are sold internally, total coffee sales will drop to 850,000 pounds. Suppose that Santigui refuses to lower the transfer price from $4.75 and the Donut Division purchases from the external supplier. Compute the effect on each division's profits and on the profits of the firm as a whole.

3. Refer to Requirement 2. What are the minimum and maximum transfer prices? Suppose that the transfer price is set at the maximum price less $1. Will the two divisions accept this transfer price? Compute the effect on the firm's profits and on each division's profits.

4. Suppose that the Coffee Division has operating assets of $2,000,000. Assume that the Coffee Division sells 850,000 pounds to outsiders and 100,000 pounds to the Donut Division at a price of $4.75 per pound. What is divisional ROI (rounded to four significant digits) based on this situation? Now, refer to Requirement 3. What will divisional ROI (rounded to four significant digits) be if the transfer price of the maximum price less $1 is implemented? How will the change in ROI affect Santigui? What information has he gained as a result of the transfer pricing negotiations?

Question

Question

Question

Question

ROI, Margin, Turnover

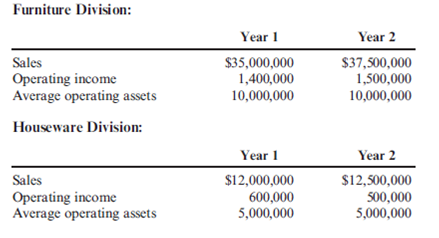

Jarriot, Inc., presented two years of data for its Furniture Division and its Houseware Division.

Required:

1. Compute the ROI and the margin and turnover ratios for each year for the Furniture Division. (Round your answers to four significant digits.)

2. Compute the ROI and the margin and turnover ratios for each year for the Houseware Division. (Round your answers to four significant digits.)

3. Explain the change in ROI from Year 1 to Year 2 for each division.

Jarriot, Inc., presented two years of data for its Furniture Division and its Houseware Division.

Required:

1. Compute the ROI and the margin and turnover ratios for each year for the Furniture Division. (Round your answers to four significant digits.)

2. Compute the ROI and the margin and turnover ratios for each year for the Houseware Division. (Round your answers to four significant digits.)

3. Explain the change in ROI from Year 1 to Year 2 for each division.

Question

Question

Question

Question

Question

Management Compensation

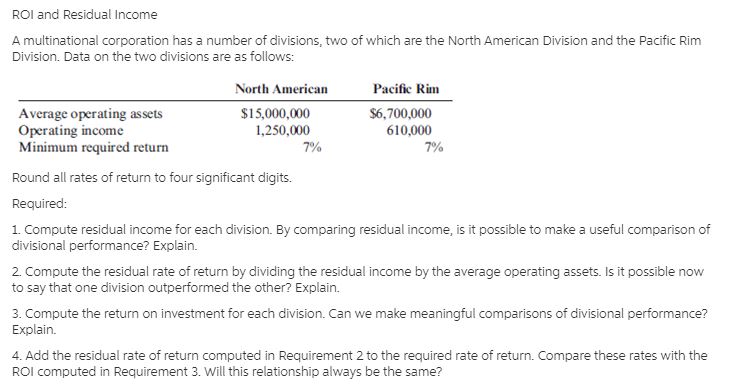

Renslen, Inc., a truck manufacturing conglomerate, has recently purchased two divisions: Meyers Service Company and Wellington Products, Inc. Meyers provides maintenance service on large truck cabs for 10-wheeler trucks, and Wellington produces air brakes for the 10-wheeler trucks.

The employees at Meyers take pride in their work, as Meyers is proclaimed to offer the best maintenance service in the trucking industry. The management of Meyers, as a group, has received additional compensation from a 10 percent bonus pool based on income before income taxes and bonus. Renslen plans to continue to compensate the Meyers management team on this basis as it is the same incentive plan used for all other Renslen divisions, except for the Wellington division.

Wellington offers a high-quality product to the trucking industry and is the premium choice even when compared to foreign competition. The management team at Wellington strives for zero defects and minimal scrap costs; current scrap levels are at 2 percent. The incentive compensation plan for Wellington management has been a 1 percent bonus based on gross margin.

Renslen plans to continue to compensate the Wellington management team on this basis. The following condensed income statements are for both divisions for the fiscal year ended May 31, 2012:

Renslen has invited the management teams of all its divisions to an off-site management workshop in July where the bonus checks will be presented. Renslen is concerned that the different bonus plans at the two divisions may cause some heated discussion.

Required:

1. Determine the 2012 bonus pool available for the management team at:

a. Meyers Service Company

b. Wellington Products, Inc.

2. Identify at least two advantages and disadvantages to Renslen, Inc., of the bonus pool incentive plan at:

a. Meyers Service Company

b. Wellington Products, Inc.

3. Having two different types of incentive plans for two operating divisions of the same corporation can create problems.

a. Discuss the behavioral problems that could arise within management for Meyers Service Company and Wellington Products, Inc., by having different types of incentive plans.

b. Present arguments that Renslen, Inc., can give to the management teams of both Meyers and Wellington to justify having two different incentive plans.

Renslen, Inc., a truck manufacturing conglomerate, has recently purchased two divisions: Meyers Service Company and Wellington Products, Inc. Meyers provides maintenance service on large truck cabs for 10-wheeler trucks, and Wellington produces air brakes for the 10-wheeler trucks.

The employees at Meyers take pride in their work, as Meyers is proclaimed to offer the best maintenance service in the trucking industry. The management of Meyers, as a group, has received additional compensation from a 10 percent bonus pool based on income before income taxes and bonus. Renslen plans to continue to compensate the Meyers management team on this basis as it is the same incentive plan used for all other Renslen divisions, except for the Wellington division.

Wellington offers a high-quality product to the trucking industry and is the premium choice even when compared to foreign competition. The management team at Wellington strives for zero defects and minimal scrap costs; current scrap levels are at 2 percent. The incentive compensation plan for Wellington management has been a 1 percent bonus based on gross margin.

Renslen plans to continue to compensate the Wellington management team on this basis. The following condensed income statements are for both divisions for the fiscal year ended May 31, 2012:

Renslen has invited the management teams of all its divisions to an off-site management workshop in July where the bonus checks will be presented. Renslen is concerned that the different bonus plans at the two divisions may cause some heated discussion.

Required:

1. Determine the 2012 bonus pool available for the management team at:

a. Meyers Service Company

b. Wellington Products, Inc.

2. Identify at least two advantages and disadvantages to Renslen, Inc., of the bonus pool incentive plan at:

a. Meyers Service Company

b. Wellington Products, Inc.

3. Having two different types of incentive plans for two operating divisions of the same corporation can create problems.

a. Discuss the behavioral problems that could arise within management for Meyers Service Company and Wellington Products, Inc., by having different types of incentive plans.

b. Present arguments that Renslen, Inc., can give to the management teams of both Meyers and Wellington to justify having two different incentive plans.

Question

ROI and Investment Decisions

Refer to Exercise 10.7 for data. At the end of Year 2, the manager of the Houseware Division is concerned about the division's performance. As a result, he is considering the opportunity to invest in two independent projects. The first is called the Espresso-Pro; it is an in-home espresso maker that can brew regular coffee as well as make espresso and latte drinks. While the market for espresso drinkers is small initially, he believes this market can grow, especially around giftgiving occasions. The second is the Mini-Prep appliance that can be used to do small chopping and dicing chores that do not require a full-sized food processor. Without the investments, the division expects that Year 2 data will remain unchanged. The expected operating incomes and the outlay required for each investment are as follows:

Jarriot's corporate headquarters has made available up to $500,000 of capital for this division. Any funds not invested by the division will be retained by headquarters and invested to earn the company's minimum required rate of return, 9 percent.

Required:

1. Compute the ROI for each investment.

2. Compute the divisional ROI (rounded to four significant digits) for each of the following four alternatives:

a. The Espresso-Pro is added.

b. The Mini-Prep is added.

c. Both investments are added.

d. Neither investment is made; the status quo is maintained.

Assuming that divisional managers are evaluated and rewarded on the basis of ROI performance, which alternative do you think the divisional manager will choose?

Refer to Exercise 10.7 for data. At the end of Year 2, the manager of the Houseware Division is concerned about the division's performance. As a result, he is considering the opportunity to invest in two independent projects. The first is called the Espresso-Pro; it is an in-home espresso maker that can brew regular coffee as well as make espresso and latte drinks. While the market for espresso drinkers is small initially, he believes this market can grow, especially around giftgiving occasions. The second is the Mini-Prep appliance that can be used to do small chopping and dicing chores that do not require a full-sized food processor. Without the investments, the division expects that Year 2 data will remain unchanged. The expected operating incomes and the outlay required for each investment are as follows:

Jarriot's corporate headquarters has made available up to $500,000 of capital for this division. Any funds not invested by the division will be retained by headquarters and invested to earn the company's minimum required rate of return, 9 percent.

Required:

1. Compute the ROI for each investment.

2. Compute the divisional ROI (rounded to four significant digits) for each of the following four alternatives:

a. The Espresso-Pro is added.

b. The Mini-Prep is added.

c. Both investments are added.

d. Neither investment is made; the status quo is maintained.

Assuming that divisional managers are evaluated and rewarded on the basis of ROI performance, which alternative do you think the divisional manager will choose?

Question

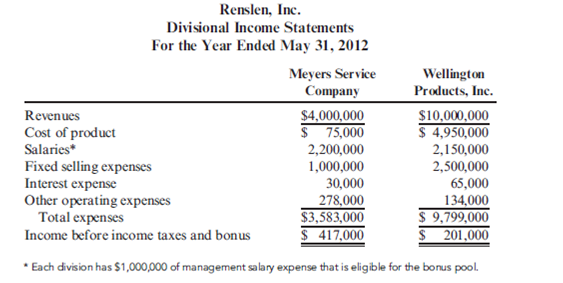

Margin, Turnover, ROI

Consider the data for each of the following four independent companies:

Required:

1. Calculate the missing values in the above table. (Round rates to four significant digits.)

2. Assume that the cost of capital is 9 percent for each of the four firms. Compute the residual income for each of the four firms.

Consider the data for each of the following four independent companies:

Required:

1. Calculate the missing values in the above table. (Round rates to four significant digits.)

2. Assume that the cost of capital is 9 percent for each of the four firms. Compute the residual income for each of the four firms.

Question

ROI, Residual Income, Behavioral Issues

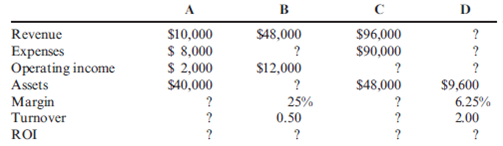

Jump Start Company (JSC), a subsidiary of Mason Industries, manufactures go-carts and other recreational vehicles. Family recreational centers that feature go-cart tracks along with miniature golf, batting cages, and arcade games have increased in popularity. As a result, JSC has been pressured by Mason management to diversify into some of these other recreational areas. Recreational Leasing, Inc. (RLI), one of the largest firms leasing arcade games to these family recreational centers, is looking for a friendly buyer. Mason's top management believes that RLI's assets could be acquired for an investment of $3.2 million and has strongly urged Bill Grieco, division manager of JSC, to consider acquiring RLI.

Bill has reviewed RLI's financial statements with his controller, Marie Donnelly, and they believe that the acquisition may not be in the best interest of JSC.

"If we decide not to do this, the Mason people are not going to be happy," said Bill. "If we could convince them to base our bonuses on something other than return on investment, maybe this acquisition would look more attractive. How would we do if the bonuses were based on residual income using the company's 15 percent cost of capital?"

Mason has traditionally evaluated all of its divisions on the basis of return on investment, which is defined as the ratio of operating income to total assets. The desired rate of return for each division is 20 percent. The management team of any division reporting an annual increase in the return on investment is automatically eligible for a bonus. The management of divisions reporting a decline in the return on investment must provide convincing explanations for the decline to be eligible for a bonus, and this bonus is limited to 50 percent of the bonus paid to divisions reporting an increase.

The following condensed financial statements are for both JSC and RLI for the fiscal year ended May 31:

Required:

1. If Mason Industries continues to use return on investment as the sole measure of division performance, explain why JSC would be reluctant to acquire RLI. Be sure to support your answer with appropriate calculations.

2. If Mason Industries could be persuaded to use residual income to measure the performance of JSC, explain why JSC would be more willing to acquire RLI. Be sure to support your answer with appropriate calculations.

3. Discuss how the behavior of division managers is likely to be affected by the use of:

a. Return on investment as a performance measure

b. Residual income as a performance measure (CMA adapted)

Jump Start Company (JSC), a subsidiary of Mason Industries, manufactures go-carts and other recreational vehicles. Family recreational centers that feature go-cart tracks along with miniature golf, batting cages, and arcade games have increased in popularity. As a result, JSC has been pressured by Mason management to diversify into some of these other recreational areas. Recreational Leasing, Inc. (RLI), one of the largest firms leasing arcade games to these family recreational centers, is looking for a friendly buyer. Mason's top management believes that RLI's assets could be acquired for an investment of $3.2 million and has strongly urged Bill Grieco, division manager of JSC, to consider acquiring RLI.

Bill has reviewed RLI's financial statements with his controller, Marie Donnelly, and they believe that the acquisition may not be in the best interest of JSC.

"If we decide not to do this, the Mason people are not going to be happy," said Bill. "If we could convince them to base our bonuses on something other than return on investment, maybe this acquisition would look more attractive. How would we do if the bonuses were based on residual income using the company's 15 percent cost of capital?"

Mason has traditionally evaluated all of its divisions on the basis of return on investment, which is defined as the ratio of operating income to total assets. The desired rate of return for each division is 20 percent. The management team of any division reporting an annual increase in the return on investment is automatically eligible for a bonus. The management of divisions reporting a decline in the return on investment must provide convincing explanations for the decline to be eligible for a bonus, and this bonus is limited to 50 percent of the bonus paid to divisions reporting an increase.

The following condensed financial statements are for both JSC and RLI for the fiscal year ended May 31:

Required:

1. If Mason Industries continues to use return on investment as the sole measure of division performance, explain why JSC would be reluctant to acquire RLI. Be sure to support your answer with appropriate calculations.

2. If Mason Industries could be persuaded to use residual income to measure the performance of JSC, explain why JSC would be more willing to acquire RLI. Be sure to support your answer with appropriate calculations.

3. Discuss how the behavior of division managers is likely to be affected by the use of:

a. Return on investment as a performance measure

b. Residual income as a performance measure (CMA adapted)

Question

Calculating Average Operating Assets, Margin, Turnover, Return on Investment (ROI)

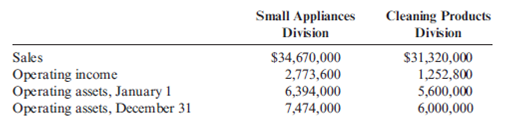

Forchen, Inc., provided the following information for two of its divisions for last year:

Required:

1. For the Small Appliances Division, calculate:

a. Average operating assets

b. Margin

c. Turnover

d. Return on investment (ROI)

2. For the Cleaning Products Division, calculate:

a. Average operating assets

b. Margin

c. Turnover

d. Return on investment (ROI)

3. What if operating income for the Small Appliances Division was $2,000,000? How would that affect average operating assets? Margin? Turnover? ROI? Calculate any changed ratios (round to four significant digits).

Forchen, Inc., provided the following information for two of its divisions for last year:

Required:

1. For the Small Appliances Division, calculate:

a. Average operating assets

b. Margin

c. Turnover

d. Return on investment (ROI)

2. For the Cleaning Products Division, calculate:

a. Average operating assets

b. Margin

c. Turnover

d. Return on investment (ROI)

3. What if operating income for the Small Appliances Division was $2,000,000? How would that affect average operating assets? Margin? Turnover? ROI? Calculate any changed ratios (round to four significant digits).

Question

Question

ROI, Residual Income

The following selected data pertain to the Argent Division for last year:

Required:

1. How much is the residual income?

2. How much is the return on investment? (Rounded to four significant digits.)

The following selected data pertain to the Argent Division for last year:

Required:

1. How much is the residual income?

2. How much is the return on investment? (Rounded to four significant digits.)

Question

Transfer Pricing in the MNC

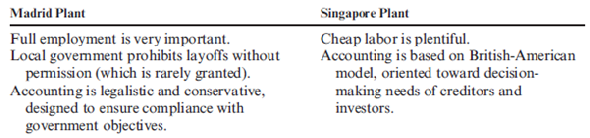

Carnover, Inc., manufactures a broad line of industrial and consumer products. One of its plants is located in Madrid, Spain, and another in Singapore. The Madrid plant is operating at 85 percent capacity. Its main product, electric motors, has experienced softness in the market, which has led to predictions of further softening of the market and predictions of a decline in production to 65 percent capacity. If that happens, workers will have to be laid off and one wing of the factory closed. The Singapore plant manufactures heavy-duty industrial mixers that use the motors manufactured by the Madrid plant as an integral component. Demand for the mixers is strong. Price and cost information for the mixers are as follows:

Fixed overhead is based on an annual budgeted amount of $3,500,000 and budgeted production of 35,000 mixers. The direct materials cost includes the cost of the motor at $200 (market price).

The Madrid plant capacity is 20,000 motors per year. Cost data are as follows:

Fixed overhead is based on budgeted fixed overhead of $2,000,000.

Required:

1. What is the maximum transfer price the Singapore plant would accept?

2. What is the minimum transfer price the Madrid plant would accept?

3. Consider the following environmental factors:

How might these environmental factors impact the transfer-pricing decision?

Carnover, Inc., manufactures a broad line of industrial and consumer products. One of its plants is located in Madrid, Spain, and another in Singapore. The Madrid plant is operating at 85 percent capacity. Its main product, electric motors, has experienced softness in the market, which has led to predictions of further softening of the market and predictions of a decline in production to 65 percent capacity. If that happens, workers will have to be laid off and one wing of the factory closed. The Singapore plant manufactures heavy-duty industrial mixers that use the motors manufactured by the Madrid plant as an integral component. Demand for the mixers is strong. Price and cost information for the mixers are as follows:

Fixed overhead is based on an annual budgeted amount of $3,500,000 and budgeted production of 35,000 mixers. The direct materials cost includes the cost of the motor at $200 (market price).

The Madrid plant capacity is 20,000 motors per year. Cost data are as follows:

Fixed overhead is based on budgeted fixed overhead of $2,000,000.

Required:

1. What is the maximum transfer price the Singapore plant would accept?

2. What is the minimum transfer price the Madrid plant would accept?

3. Consider the following environmental factors:

How might these environmental factors impact the transfer-pricing decision?

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

(2010 CPA Exam) SkyBound Airlines provided the following information about its two operating divisions:

Measuring performance using return on investment (ROI), which division performed better?

A) The Cargo division, with an ROI of 10%.

B) The Passenger division, with an ROI of 16%.

C) The Cargo division, with an ROI of 18%.

D) The Passenger division, with an ROI of 22%.

Measuring performance using return on investment (ROI), which division performed better?

A) The Cargo division, with an ROI of 10%.

B) The Passenger division, with an ROI of 16%.

C) The Cargo division, with an ROI of 18%.

D) The Passenger division, with an ROI of 22%.

Question

Question

Question

Question

Question

Operating Income for Segments

Xenold, Inc., manufactures and sells cooktops and ovens through three divisions: Home, Restaurant, and Specialty. Each division is evaluated as a profit center. Data for each division for last year are as follows (numbers in thousands):

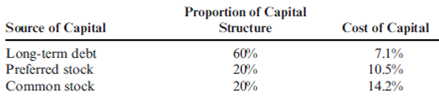

The income tax rate for Xenold, Inc., is 40 percent. Xenold, Inc., has two sources of financing: bonds paying 5 percent interest, which account for 25 percent of total investment, and equity accounting for the remaining 75 percent of total investment. Xenold, Inc., has been in business for over 15 years and is considered a relatively stable stock, despite its link to the cyclical construction industry. As a result, Xenold stock has an opportunity cost of 5 percent over the 4 percent long-term government bond rate. Xenold's total capital employed is $5.04 million ($2,600,000 for the Home Division, $1,700,000 for the Restaurant Division, and the remainder for the Specialty Division).

Required:

1. Prepare a segmented income statement for Xenold, Inc., for last year.

2. Calculate Xenold's weighted average cost of capital. (Round to four significant digits.)

3. Calculate EVA for each division and for Xenold, Inc.

4. Comment on the performance of each of the divisions.

Xenold, Inc., manufactures and sells cooktops and ovens through three divisions: Home, Restaurant, and Specialty. Each division is evaluated as a profit center. Data for each division for last year are as follows (numbers in thousands):

The income tax rate for Xenold, Inc., is 40 percent. Xenold, Inc., has two sources of financing: bonds paying 5 percent interest, which account for 25 percent of total investment, and equity accounting for the remaining 75 percent of total investment. Xenold, Inc., has been in business for over 15 years and is considered a relatively stable stock, despite its link to the cyclical construction industry. As a result, Xenold stock has an opportunity cost of 5 percent over the 4 percent long-term government bond rate. Xenold's total capital employed is $5.04 million ($2,600,000 for the Home Division, $1,700,000 for the Restaurant Division, and the remainder for the Specialty Division).

Required:

1. Prepare a segmented income statement for Xenold, Inc., for last year.

2. Calculate Xenold's weighted average cost of capital. (Round to four significant digits.)

3. Calculate EVA for each division and for Xenold, Inc.

4. Comment on the performance of each of the divisions.

Question

Question

Determining Market-Based and Negotiated Transfer Prices

Carreker, Inc., has a number of divisions, including the Alamosa Division, producer of surgical blades, and the Tavaris Division, a manufacturer of medical instruments. Alamosa Division produces a 2.6 cm steel blade that can be used by Tavaris Division in the production of scalpels. The market price of the blade is $21. Cost information for the blade is:

Tavaris needs 15,000 units of the 2.6 cm blade per year. Alamosa Division is at full capacity (90,000 units of the blade).

Required:

1. If Carreker, Inc., has a transfer pricing policy that requires transfer at market price, what would the transfer price be? Do you suppose that Alamosa and Tavaris divisions would choose to transfer at that price?

2. Now suppose that Carreker, Inc., allows negotiated transfer pricing and that Alamosa Division can avoid $1.75 of selling and distribution expense by selling to Tavaris Division. Which division sets the minimum transfer price, and what is it? Which division sets the maximum transfer price, and what is it? Do you suppose that Alamosa and Tavaris divisions would choose to transfer somewhere in the bargaining range?

3. What if Alamosa Division plans to produce and sell only 65,000 units of the 2.6 cm blade next year? Which division sets the minimum transfer price, and what is it? Which division sets the maximum transfer price, and what is it? Do you suppose that Alamosa and Tavaris divisions would choose to transfer somewhere in the bargaining range?

Carreker, Inc., has a number of divisions, including the Alamosa Division, producer of surgical blades, and the Tavaris Division, a manufacturer of medical instruments. Alamosa Division produces a 2.6 cm steel blade that can be used by Tavaris Division in the production of scalpels. The market price of the blade is $21. Cost information for the blade is:

Tavaris needs 15,000 units of the 2.6 cm blade per year. Alamosa Division is at full capacity (90,000 units of the blade).

Required:

1. If Carreker, Inc., has a transfer pricing policy that requires transfer at market price, what would the transfer price be? Do you suppose that Alamosa and Tavaris divisions would choose to transfer at that price?

2. Now suppose that Carreker, Inc., allows negotiated transfer pricing and that Alamosa Division can avoid $1.75 of selling and distribution expense by selling to Tavaris Division. Which division sets the minimum transfer price, and what is it? Which division sets the maximum transfer price, and what is it? Do you suppose that Alamosa and Tavaris divisions would choose to transfer somewhere in the bargaining range?

3. What if Alamosa Division plans to produce and sell only 65,000 units of the 2.6 cm blade next year? Which division sets the minimum transfer price, and what is it? Which division sets the maximum transfer price, and what is it? Do you suppose that Alamosa and Tavaris divisions would choose to transfer somewhere in the bargaining range?

Question

Question

(2009 CPA Exam) A company has the following financial information:

To maximize shareholder wealth, the company would most likely establish a hurdle rate that would limit acceptance of projects to only those with minimum returns greater than what percent?

A) 7.1%

B) 9.2%

C) 10.6%

D) 14.2%

To maximize shareholder wealth, the company would most likely establish a hurdle rate that would limit acceptance of projects to only those with minimum returns greater than what percent?

A) 7.1%

B) 9.2%

C) 10.6%

D) 14.2%

Question

Question

Transfer Pricing, Idle Capacity

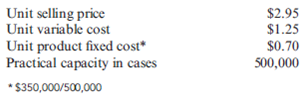

Mouton Perrier, Inc., has a number of divisions that produce liquors, bottled water, and glassware. The Glassware Division manufactures a variety of bottles that can be sold externally (to soft-drink and juice bottlers) or internally to Mouton Perrier's Bottled Water Division. Sales and cost data on a case of 24 basic 12-ounce bottles are as follows:

During the coming year, the Glassware Division expects to sell 390,000 cases of this bottle. The Bottled Water Division currently plans to buy 100,000 cases on the outside market for $2.95 each. Ellyn Burridge, manager of the Glassware Division, approached Justin Thomas, manager of the Bottled Water Division, and offered to sell the 100,000 cases for $2.89 each. Ellyn explained to Justin that she can avoid selling costs of $0.12 per case by selling internally and that she would split the savings by offering a $0.06 discount on the usual price.

Required:

1. What is the minimum transfer price that the Glassware Division would be willing to accept? What is the maximum transfer price that the Bottled Water Division would be willing to pay? Should an internal transfer take place? What would be the benefit (or loss) to the firm as a whole if the internal transfer takes place?

2. Suppose Justin knows that the Glassware Division has idle capacity. Do you think that he would agree to the transfer price of $2.89? Suppose he counters with an offer to pay $2.40. If you were Ellyn, would you be interested in this price? Explain with supporting computations.

3. Suppose that Mouton Perrier's policy is that all internal transfers take place at full manufacturing cost. What would the transfer price be? Would the transfer take place?

Mouton Perrier, Inc., has a number of divisions that produce liquors, bottled water, and glassware. The Glassware Division manufactures a variety of bottles that can be sold externally (to soft-drink and juice bottlers) or internally to Mouton Perrier's Bottled Water Division. Sales and cost data on a case of 24 basic 12-ounce bottles are as follows:

During the coming year, the Glassware Division expects to sell 390,000 cases of this bottle. The Bottled Water Division currently plans to buy 100,000 cases on the outside market for $2.95 each. Ellyn Burridge, manager of the Glassware Division, approached Justin Thomas, manager of the Bottled Water Division, and offered to sell the 100,000 cases for $2.89 each. Ellyn explained to Justin that she can avoid selling costs of $0.12 per case by selling internally and that she would split the savings by offering a $0.06 discount on the usual price.

Required:

1. What is the minimum transfer price that the Glassware Division would be willing to accept? What is the maximum transfer price that the Bottled Water Division would be willing to pay? Should an internal transfer take place? What would be the benefit (or loss) to the firm as a whole if the internal transfer takes place?

2. Suppose Justin knows that the Glassware Division has idle capacity. Do you think that he would agree to the transfer price of $2.89? Suppose he counters with an offer to pay $2.40. If you were Ellyn, would you be interested in this price? Explain with supporting computations.

3. Suppose that Mouton Perrier's policy is that all internal transfers take place at full manufacturing cost. What would the transfer price be? Would the transfer take place?

Question

Transfer Pricing

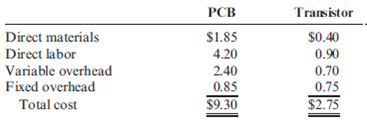

Fillmore Industries is a vertically integrated firm with several divisions that operate as decentralized profit centers. Fillmore's Systems Division manufactures scientific instruments and uses the products of two of Fillmore's other divisions. The Board Division manufactures printed circuit boards (PCBs). One PCB model is made exclusively for the Systems Division using proprietary designs, while less complex models are sold in outside markets. The products of the Transistor Division are sold in a well-developed competitive market; however, one transistor model is also used by the Systems Division. The costs per unit of the products used by the Systems Division are as follows:

The Board Division sells its commercial product at full cost plus a 30 percent markup and believes the proprietary board made for the Systems Division would sell for $12 per unit on the open market. The market price of the transistor used by the Systems Division is $3.45 per unit.

Required:

1. What is the minimum transfer price for the Transistor Division? What is the maximum transfer price of the transistor for the Systems Division?

2. Assume the Systems Division is able to purchase a large quantity of transistors from an outside source at $2.75 per unit. Further assume that the Transistor Division has excess capacity. Can the Transistor Division meet this price?

3. The Board and Systems divisions have negotiated a transfer price of $11 per printed circuit board. Discuss the impact this transfer price will have on each division. (CMA adapted)

Fillmore Industries is a vertically integrated firm with several divisions that operate as decentralized profit centers. Fillmore's Systems Division manufactures scientific instruments and uses the products of two of Fillmore's other divisions. The Board Division manufactures printed circuit boards (PCBs). One PCB model is made exclusively for the Systems Division using proprietary designs, while less complex models are sold in outside markets. The products of the Transistor Division are sold in a well-developed competitive market; however, one transistor model is also used by the Systems Division. The costs per unit of the products used by the Systems Division are as follows:

The Board Division sells its commercial product at full cost plus a 30 percent markup and believes the proprietary board made for the Systems Division would sell for $12 per unit on the open market. The market price of the transistor used by the Systems Division is $3.45 per unit.

Required:

1. What is the minimum transfer price for the Transistor Division? What is the maximum transfer price of the transistor for the Systems Division?

2. Assume the Systems Division is able to purchase a large quantity of transistors from an outside source at $2.75 per unit. Further assume that the Transistor Division has excess capacity. Can the Transistor Division meet this price?

3. The Board and Systems divisions have negotiated a transfer price of $11 per printed circuit board. Discuss the impact this transfer price will have on each division. (CMA adapted)

Question

Question

Question

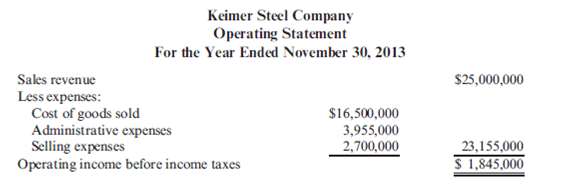

ROI, Residual Income

Raddington Industries produces tool and die machinery for manufacturers. The company expanded vertically in 2012 by acquiring one of its suppliers of alloy steel plates, Keimer Steel Company. To manage the two separate businesses, the operations of Keimer are reported separately as an investment center.

Raddington monitors its divisions on the basis of both unit contribution and return on average investment (ROI), with investment defined as average operating assets employed. Management bonuses are determined on ROI. All investments in operating assets are expected to earn a minimum return of 13 percent before income taxes.

Keimer's cost of goods sold is considered to be entirely variable, while the division's administrative expenses are not dependent on volume. Selling expenses are a mixed cost with 40 percent attributed to sales volume. Keimer contemplated a capital acquisition with an estimated ROI of 14.5 percent; however, division management decided against the investment because it believed that the investment would decrease Keimer's overall ROI.

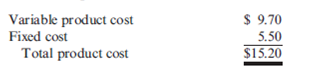

The 2013 operating statement for Keimer follows. The division's operating assets employed were $12,600,000 at November 30, 2013, a 5 percent increase over the 2012 year-end balance.

Required:

1. Calculate the unit contribution for Keimer Steel Company if 1,187,000 units were produced and sold during the year ended November 30, 2013.

2. Calculate the following performance measures for 2013 for Keimer Steel Company:

a. Pretax return on average investment in operating assets employed (ROI)

b. Residual income calculated on the basis of average operating assets employed

3. Explain why the management of Keimer Steel Company would have been more likely to accept the contemplated capital acquisition if residual income rather than ROI were used as a performance measure.

4. Keimer Steel Company is a separate investment center within Raddington Industries. Identify several items that Keimer should control if it is to be evaluated fairly by either the ROI or residual income performance measures. ( CMA adapted )

Raddington Industries produces tool and die machinery for manufacturers. The company expanded vertically in 2012 by acquiring one of its suppliers of alloy steel plates, Keimer Steel Company. To manage the two separate businesses, the operations of Keimer are reported separately as an investment center.

Raddington monitors its divisions on the basis of both unit contribution and return on average investment (ROI), with investment defined as average operating assets employed. Management bonuses are determined on ROI. All investments in operating assets are expected to earn a minimum return of 13 percent before income taxes.

Keimer's cost of goods sold is considered to be entirely variable, while the division's administrative expenses are not dependent on volume. Selling expenses are a mixed cost with 40 percent attributed to sales volume. Keimer contemplated a capital acquisition with an estimated ROI of 14.5 percent; however, division management decided against the investment because it believed that the investment would decrease Keimer's overall ROI.

The 2013 operating statement for Keimer follows. The division's operating assets employed were $12,600,000 at November 30, 2013, a 5 percent increase over the 2012 year-end balance.

Required:

1. Calculate the unit contribution for Keimer Steel Company if 1,187,000 units were produced and sold during the year ended November 30, 2013.

2. Calculate the following performance measures for 2013 for Keimer Steel Company:

a. Pretax return on average investment in operating assets employed (ROI)

b. Residual income calculated on the basis of average operating assets employed

3. Explain why the management of Keimer Steel Company would have been more likely to accept the contemplated capital acquisition if residual income rather than ROI were used as a performance measure.

4. Keimer Steel Company is a separate investment center within Raddington Industries. Identify several items that Keimer should control if it is to be evaluated fairly by either the ROI or residual income performance measures. ( CMA adapted )

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/50

Play

Full screen (f)

Deck 10: Decentralization: Responsibility Accounting, Performance

1

Determining Market-Based and Negotiated Transfer Prices

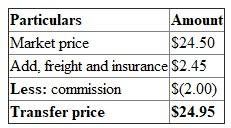

Clanahan, Inc., has a number of divisions around the world. Division US (in the United States) purchases a component from Division N (in the Netherlands). The component can be purchased externally for $24.50 each. The freight and insurance on the item amount to $2.45; however, commissions of $2.00 need not be paid.

Required:

1. Calculate the transfer price using the comparable uncontrolled price method.

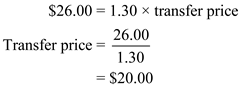

2. Suppose that there is no outside market for the component that Division N transfers to Division US. Further assume that Division US sells the component for $26.00 and normally receives a 30 percent markup on cost of goods sold. Calculate the transfer price using the resale price method.

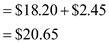

3. Now assume that there is no external market for the component transferred from Division N to Division US, and that the component is used in the manufacture of another product (i.e., it is not resold). Calculate the transfer price using the cost-plus method. Further assume that Division N's manufacturing cost for the component is $18.20.

4. What if commissions avoided were $2.25 per unit? How would that affect the comparable uncontrolled price? The resale price? The cost-plus price?

Clanahan, Inc., has a number of divisions around the world. Division US (in the United States) purchases a component from Division N (in the Netherlands). The component can be purchased externally for $24.50 each. The freight and insurance on the item amount to $2.45; however, commissions of $2.00 need not be paid.

Required:

1. Calculate the transfer price using the comparable uncontrolled price method.

2. Suppose that there is no outside market for the component that Division N transfers to Division US. Further assume that Division US sells the component for $26.00 and normally receives a 30 percent markup on cost of goods sold. Calculate the transfer price using the resale price method.

3. Now assume that there is no external market for the component transferred from Division N to Division US, and that the component is used in the manufacture of another product (i.e., it is not resold). Calculate the transfer price using the cost-plus method. Further assume that Division N's manufacturing cost for the component is $18.20.

4. What if commissions avoided were $2.25 per unit? How would that affect the comparable uncontrolled price? The resale price? The cost-plus price?

The information on the two divisions of C , Inc. is given in the question.

Given:

1.The transfer price using the comparable uncontrolled price method is calculated as follows:-

1.The transfer price using the comparable uncontrolled price method is calculated as follows:-

2.With no outside market for division N, and a resale price for division US, the transfer price is calculated as follows:-

2.With no outside market for division N, and a resale price for division US, the transfer price is calculated as follows:-

The transfer price is

The transfer price is

3.

3.

The cost plus transfer price is

The cost plus transfer price is

4.If the Commission is increased to

4.If the Commission is increased to

per unit, only the comparable uncontrolled price would be affected.

per unit, only the comparable uncontrolled price would be affected.

It would decrease to,

Given:

1.The transfer price using the comparable uncontrolled price method is calculated as follows:- 2.With no outside market for division N, and a resale price for division US, the transfer price is calculated as follows:- The transfer price is 3. The cost plus transfer price is 4.If the Commission is increased to per unit, only the comparable uncontrolled price would be affected. It would decrease to,

2

Identify three cost-based transfer prices. What are the disadvantages of cost-based transfer prices? When might it be appropriate to use cost-based transfer prices?

The three cost based transfer prices are as below:

1. Full cost

2. Full cost plus

3. Variable cost plus

• The main limitation of cost based transfer prices is that cost-based transfer prices cannot represent the preferable results for the division and the company.

• Peculiarly, transfer prices may adopt any one of the costing practice, to be grater than the maximum price or less than the minimum price.

• However, the prices can be used easily without any conflict.

1. Full cost

2. Full cost plus

3. Variable cost plus

• The main limitation of cost based transfer prices is that cost-based transfer prices cannot represent the preferable results for the division and the company.

• Peculiarly, transfer prices may adopt any one of the costing practice, to be grater than the maximum price or less than the minimum price.

• However, the prices can be used easily without any conflict.

3

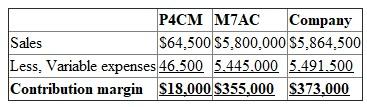

Setting Transfer Prices-Market Price versus Full Cost

Ardmore, Inc., manufactures heating and air conditioning units in its six divisions. One division, the Components Division, produces electronic components that can be used by the other five. All the components produced by this division can be sold to outside customers; however, from the beginning, about 70 percent of its output has been used internally. The current policy requires that all internal transfers of components be transferred at full cost.

Recently, Cynthia Busby, the new chief executive officer of Ardmore, decided to investigate the transfer pricing policy. She was concerned that the current method of pricing internal transfers might force decisions by divisional managers that would be suboptimal for the firm. As part of her inquiry, she gathered some information concerning Part 4CM, used by the Small AC Division in its production of a window air conditioner, Model 7AC.

The Small AC Division sells 10,000 units of Model 7AC each year at a unit price of $58. Given current market conditions, this is the maximum price that the division can charge for Model 7AC. The cost of manufacturing the air conditioner is computed as follows:

The window unit is produced efficiently, and no further reduction in manufacturing costs is possible.

The manager of the Components Division indicated that he could sell 10,000 units (the division's capacity for this part) of Part 4CM to outside buyers at $12 per unit. The Small AC Division could also buy the part for $12 from external suppliers. The following detail on the manufacturing cost of the component was provided:

Required:

1. Compute the firmwide contribution margin associated with Part 4CM and Model 7AC. Also, compute the contribution margin earned by each division.

2. Suppose that Cynthia Busby abolishes the current transfer pricing policy and gives divisions autonomy in setting transfer prices. Can you predict what transfer price the manager of the Components Division will set? What should be the minimum transfer price for this part? The maximum transfer price?

3. Given the new transfer pricing policy, predict how this will affect the production decision for Model 7AC of the manager of the Small AC Division. How many units of Part 4CM will the manager of the Small AC Division purchase, either internally or externally?

4. Given the new transfer price set by the Components Division and your answer to Requirement 3, how many units of 4CM will be sold externally?

Ardmore, Inc., manufactures heating and air conditioning units in its six divisions. One division, the Components Division, produces electronic components that can be used by the other five. All the components produced by this division can be sold to outside customers; however, from the beginning, about 70 percent of its output has been used internally. The current policy requires that all internal transfers of components be transferred at full cost.

Recently, Cynthia Busby, the new chief executive officer of Ardmore, decided to investigate the transfer pricing policy. She was concerned that the current method of pricing internal transfers might force decisions by divisional managers that would be suboptimal for the firm. As part of her inquiry, she gathered some information concerning Part 4CM, used by the Small AC Division in its production of a window air conditioner, Model 7AC.

The Small AC Division sells 10,000 units of Model 7AC each year at a unit price of $58. Given current market conditions, this is the maximum price that the division can charge for Model 7AC. The cost of manufacturing the air conditioner is computed as follows:

The window unit is produced efficiently, and no further reduction in manufacturing costs is possible.

The manager of the Components Division indicated that he could sell 10,000 units (the division's capacity for this part) of Part 4CM to outside buyers at $12 per unit. The Small AC Division could also buy the part for $12 from external suppliers. The following detail on the manufacturing cost of the component was provided:

Required:

1. Compute the firmwide contribution margin associated with Part 4CM and Model 7AC. Also, compute the contribution margin earned by each division.

2. Suppose that Cynthia Busby abolishes the current transfer pricing policy and gives divisions autonomy in setting transfer prices. Can you predict what transfer price the manager of the Components Division will set? What should be the minimum transfer price for this part? The maximum transfer price?

3. Given the new transfer pricing policy, predict how this will affect the production decision for Model 7AC of the manager of the Small AC Division. How many units of Part 4CM will the manager of the Small AC Division purchase, either internally or externally?

4. Given the new transfer price set by the Components Division and your answer to Requirement 3, how many units of 4CM will be sold externally?

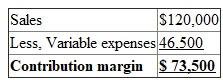

1.Computation of the contribution margin:

2.The transfer price is the market price of $12. This is the minimum price for the C Division and the maximum price for the S Division.

2.The transfer price is the market price of $12. This is the minimum price for the C Division and the maximum price for the S Division.

3.As soon as the manager of the S Division is capable of to increasing the price of Model 7, he will stop manufacturing and will not buy any of the components.

4.All 10,000 units of P4CM will be sold externally at the market price of $12 per unit.

5.

The contribution to profits rose by $55,500. Therefore, the CEO made the correct decision.

The contribution to profits rose by $55,500. Therefore, the CEO made the correct decision.

2.The transfer price is the market price of $12. This is the minimum price for the C Division and the maximum price for the S Division.3.As soon as the manager of the S Division is capable of to increasing the price of Model 7, he will stop manufacturing and will not buy any of the components.

4.All 10,000 units of P4CM will be sold externally at the market price of $12 per unit.

5.

The contribution to profits rose by $55,500. Therefore, the CEO made the correct decision. 4

What are two disadvantages of ROI? Explain how each can lead to decreased profitability.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

5

Transfer Pricing and Section 482

Sugarland, Inc., has a division in Indonesia that makes dyestuff in a variety of colors used to dye denim for jeans, and another division in the United States that manufactures denim clothing. The Dyestuff Division incurs manufacturing costs of $2.68 for one pound of powdered dye. The Clothing Division currently buys its dye powder from an outside supplier for $3.80 per pound. If the Clothing Division purchases the powder from the Indonesian division, the shipping costs will be $0.34 per pound, but sales commissions of $0.05 per pound will be avoided with an internal transfer.

Required:

1. Which Section 482 method should be used to calculate the allowable transfer price? Calculate the appropriate transfer price per pound.

2. Assume that the Clothing Division cannot buy this type of powder externally since it has an unusual formula that results in a color particular to Sugarland's jeans. Which Section 482 method should be used to calculate the allowable transfer price? Calculate the appropriate transfer price per pound.

Sugarland, Inc., has a division in Indonesia that makes dyestuff in a variety of colors used to dye denim for jeans, and another division in the United States that manufactures denim clothing. The Dyestuff Division incurs manufacturing costs of $2.68 for one pound of powdered dye. The Clothing Division currently buys its dye powder from an outside supplier for $3.80 per pound. If the Clothing Division purchases the powder from the Indonesian division, the shipping costs will be $0.34 per pound, but sales commissions of $0.05 per pound will be avoided with an internal transfer.

Required:

1. Which Section 482 method should be used to calculate the allowable transfer price? Calculate the appropriate transfer price per pound.

2. Assume that the Clothing Division cannot buy this type of powder externally since it has an unusual formula that results in a color particular to Sugarland's jeans. Which Section 482 method should be used to calculate the allowable transfer price? Calculate the appropriate transfer price per pound.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

6

Transfer Pricing with Idle Capacity

Oriole, Inc., owns a number of food service companies. Two divisions are the Coffee Division and the Donut Shop Division. The Coffee Division purchases and roasts coffee beans for sale to supermarkets and specialty shops. The Donut Shop Division operates a chain of donut shops where the donuts are made on the premises. Coffee is an important item for sale along with the donuts and, to date, has been purchased from the Coffee Division. Company policy permits each manager the freedom to decide whether or not to buy or sell internally. Each divisional manager is evaluated on the basis of return on investment and residual income.

Recently, an outside supplier has offered to sell coffee beans, roasted and ground, to the Donut Shop Division for $4.30 per pound. Since the current price paid to the Coffee Division is $4.75 per pound, Ashleigh Tremont, the manager of the Donut Shop Division, was interested in the offer. However, before making the decision to switch to the outside supplier, she decided to approach Santigui Melendez, manager of the Coffee Division, to see if he wanted to offer an even better price. If not, then Ashleigh would buy from the outside supplier.

Upon receiving the information from Ashleigh about the outside offer, Santigui gathered the following information about the coffee:

Required:

1. Suppose that the Coffee Division is producing at capacity and can sell all that it produces to outside customers. How should Santigui respond to Ashleigh's request for a lower transfer price? What will be the effect on firmwide profits? Compute the effect of this response on each division's profits.

2. Now, assume that the Coffee Division is currently selling 950,000 pounds. If no units are sold internally, total coffee sales will drop to 850,000 pounds. Suppose that Santigui refuses to lower the transfer price from $4.75 and the Donut Division purchases from the external supplier. Compute the effect on each division's profits and on the profits of the firm as a whole.

3. Refer to Requirement 2. What are the minimum and maximum transfer prices? Suppose that the transfer price is set at the maximum price less $1. Will the two divisions accept this transfer price? Compute the effect on the firm's profits and on each division's profits.

4. Suppose that the Coffee Division has operating assets of $2,000,000. Assume that the Coffee Division sells 850,000 pounds to outsiders and 100,000 pounds to the Donut Division at a price of $4.75 per pound. What is divisional ROI (rounded to four significant digits) based on this situation? Now, refer to Requirement 3. What will divisional ROI (rounded to four significant digits) be if the transfer price of the maximum price less $1 is implemented? How will the change in ROI affect Santigui? What information has he gained as a result of the transfer pricing negotiations?

Oriole, Inc., owns a number of food service companies. Two divisions are the Coffee Division and the Donut Shop Division. The Coffee Division purchases and roasts coffee beans for sale to supermarkets and specialty shops. The Donut Shop Division operates a chain of donut shops where the donuts are made on the premises. Coffee is an important item for sale along with the donuts and, to date, has been purchased from the Coffee Division. Company policy permits each manager the freedom to decide whether or not to buy or sell internally. Each divisional manager is evaluated on the basis of return on investment and residual income.

Recently, an outside supplier has offered to sell coffee beans, roasted and ground, to the Donut Shop Division for $4.30 per pound. Since the current price paid to the Coffee Division is $4.75 per pound, Ashleigh Tremont, the manager of the Donut Shop Division, was interested in the offer. However, before making the decision to switch to the outside supplier, she decided to approach Santigui Melendez, manager of the Coffee Division, to see if he wanted to offer an even better price. If not, then Ashleigh would buy from the outside supplier.

Upon receiving the information from Ashleigh about the outside offer, Santigui gathered the following information about the coffee:

Required:

1. Suppose that the Coffee Division is producing at capacity and can sell all that it produces to outside customers. How should Santigui respond to Ashleigh's request for a lower transfer price? What will be the effect on firmwide profits? Compute the effect of this response on each division's profits.

2. Now, assume that the Coffee Division is currently selling 950,000 pounds. If no units are sold internally, total coffee sales will drop to 850,000 pounds. Suppose that Santigui refuses to lower the transfer price from $4.75 and the Donut Division purchases from the external supplier. Compute the effect on each division's profits and on the profits of the firm as a whole.

3. Refer to Requirement 2. What are the minimum and maximum transfer prices? Suppose that the transfer price is set at the maximum price less $1. Will the two divisions accept this transfer price? Compute the effect on the firm's profits and on each division's profits.

4. Suppose that the Coffee Division has operating assets of $2,000,000. Assume that the Coffee Division sells 850,000 pounds to outsiders and 100,000 pounds to the Donut Division at a price of $4.75 per pound. What is divisional ROI (rounded to four significant digits) based on this situation? Now, refer to Requirement 3. What will divisional ROI (rounded to four significant digits) be if the transfer price of the maximum price less $1 is implemented? How will the change in ROI affect Santigui? What information has he gained as a result of the transfer pricing negotiations?

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

7

What is residual income? Explain how residual income overcomes one of ROI's disadvantages.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

8

What is the purpose of Internal Revenue Code Section 482? What four methods of transfer pricing are acceptable under this section?

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

9

Transfer Pricing: Various Computations

Corning Company has a decentralized organization with a divisional structure. Two of these divisions are the Appliance Division and the Manufactured Housing Division. Each divisional manager is evaluated on the basis of ROI.

The Appliance Division produces a small automatic dishwasher that the Manufactured Housing Division can use in one of its models. Appliance can produce up to 20,000 of these dishwashers per year. The variable costs of manufacturing the dishwashers are $98. The Manufactured Housing Division inserts the dishwasher into the model house and then sells the manufactured house to outside customers for $73,000 each. The division's capacity is 4,000 units. The variable costs of the manufactured house (in addition to the cost of the dishwasher itself) are $42,600.

Required:

Assume each part is independent, unless otherwise indicated.

1. Assume that all of the dishwashers produced can be sold to external customers for $320 each. The Manufactured Housing Division wants to buy 4,000 dishwashers per year. What should the transfer price be?

2. Refer to Requirement 1. Assume $24 of avoidable distribution costs. Identify the maximum and minimum transfer prices. Identify the actual transfer price, assuming that negotiation splits the difference.

3. Assume that the Appliance Division is operating at 75 percent capacity. The Manufactured Housing Division is currently buying 4,000 dishwashers from an outside supplier for $290 each. Assume that any joint benefit will be split evenly between the two divisions. What is the expected transfer price? How much will the profits of the firm increase under this arrangement? How much will the profits of the Appliance Division increase, assuming that it sells the extra 4,000 dishwashers internally?

Corning Company has a decentralized organization with a divisional structure. Two of these divisions are the Appliance Division and the Manufactured Housing Division. Each divisional manager is evaluated on the basis of ROI.

The Appliance Division produces a small automatic dishwasher that the Manufactured Housing Division can use in one of its models. Appliance can produce up to 20,000 of these dishwashers per year. The variable costs of manufacturing the dishwashers are $98. The Manufactured Housing Division inserts the dishwasher into the model house and then sells the manufactured house to outside customers for $73,000 each. The division's capacity is 4,000 units. The variable costs of the manufactured house (in addition to the cost of the dishwasher itself) are $42,600.

Required:

Assume each part is independent, unless otherwise indicated.

1. Assume that all of the dishwashers produced can be sold to external customers for $320 each. The Manufactured Housing Division wants to buy 4,000 dishwashers per year. What should the transfer price be?

2. Refer to Requirement 1. Assume $24 of avoidable distribution costs. Identify the maximum and minimum transfer prices. Identify the actual transfer price, assuming that negotiation splits the difference.

3. Assume that the Appliance Division is operating at 75 percent capacity. The Manufactured Housing Division is currently buying 4,000 dishwashers from an outside supplier for $290 each. Assume that any joint benefit will be split evenly between the two divisions. What is the expected transfer price? How much will the profits of the firm increase under this arrangement? How much will the profits of the Appliance Division increase, assuming that it sells the extra 4,000 dishwashers internally?

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

10

ROI, Margin, Turnover

Jarriot, Inc., presented two years of data for its Furniture Division and its Houseware Division.

Required:

1. Compute the ROI and the margin and turnover ratios for each year for the Furniture Division. (Round your answers to four significant digits.)

2. Compute the ROI and the margin and turnover ratios for each year for the Houseware Division. (Round your answers to four significant digits.)

3. Explain the change in ROI from Year 1 to Year 2 for each division.

Jarriot, Inc., presented two years of data for its Furniture Division and its Houseware Division.

Required:

1. Compute the ROI and the margin and turnover ratios for each year for the Furniture Division. (Round your answers to four significant digits.)

2. Compute the ROI and the margin and turnover ratios for each year for the Houseware Division. (Round your answers to four significant digits.)

3. Explain the change in ROI from Year 1 to Year 2 for each division.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

11

Transfer Pricing and Section 482

Mossfort, Inc., has a division in Canada that makes long-lasting exterior wood stain. Mossfort has another U.S. division, the Retail Division, that operates a chain of home improvement stores. The Retail Division would like to buy the unique, long-lasting wood stain from the Canadian division, since this type of stain is not currently available. The Exterior Stain Division incurs manufacturing costs of $13.45 for one gallon of stain.

If the Retail Division purchases the stain from the Canadian division, the shipping costs will be $1.40 per gallon, but sales commissions of $0.75 per gallon will be avoided with an internal transfer. The Retail Division plans to sell the stain for $32.80 per gallon. Normally, the Retail Division earns a gross margin of 35 percent above cost of goods sold.

Required:

1. Which Section 482 method should be used to calculate the allowable transfer price?

2. Calculate the appropriate transfer price per gallon. (Round to the nearest cent.)

Mossfort, Inc., has a division in Canada that makes long-lasting exterior wood stain. Mossfort has another U.S. division, the Retail Division, that operates a chain of home improvement stores. The Retail Division would like to buy the unique, long-lasting wood stain from the Canadian division, since this type of stain is not currently available. The Exterior Stain Division incurs manufacturing costs of $13.45 for one gallon of stain.

If the Retail Division purchases the stain from the Canadian division, the shipping costs will be $1.40 per gallon, but sales commissions of $0.75 per gallon will be avoided with an internal transfer. The Retail Division plans to sell the stain for $32.80 per gallon. Normally, the Retail Division earns a gross margin of 35 percent above cost of goods sold.

Required:

1. Which Section 482 method should be used to calculate the allowable transfer price?

2. Calculate the appropriate transfer price per gallon. (Round to the nearest cent.)

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

12

Managerial Performance Evaluation

Greg Peterson has recently been appointed vice president of operations for Webster Corporation. Greg has a manufacturing background and previously served as operations manager of Webster's Tractor Division. The business segments of Webster include the manufacture of heavy equipment, food processing, and financial services.

In a recent conversation with Carol Andrews, Webster's chief financial officer, Greg suggested that segment managers be evaluated on the basis of the segment data appearing in Webster's annual financial report. This report presents revenues, earnings, identifiable assets, and depreciation for each segment for a five-year period. Greg believes that evaluating segment managers by criteria similar to that used in evaluating the company's top management would be appropriate. Carol has expressed her reservations about using segment information from the annual financial report for this purpose and has suggested that Greg consider other ways to evaluate the performance of segment managers.

Required:

1. Explain why the segment information prepared for public reporting purposes may not be appropriate for the evaluation of segment management performance.

2. Describe the possible behavioral impact of Webster Corporation's segment managers if their performance is evaluated on the basis of the information in the annual financial report.

3. Identify and describe several types of financial information that would be more appropriate for Greg to review when evaluating the performance of segment managers. (CMA adapted)

Greg Peterson has recently been appointed vice president of operations for Webster Corporation. Greg has a manufacturing background and previously served as operations manager of Webster's Tractor Division. The business segments of Webster include the manufacture of heavy equipment, food processing, and financial services.

In a recent conversation with Carol Andrews, Webster's chief financial officer, Greg suggested that segment managers be evaluated on the basis of the segment data appearing in Webster's annual financial report. This report presents revenues, earnings, identifiable assets, and depreciation for each segment for a five-year period. Greg believes that evaluating segment managers by criteria similar to that used in evaluating the company's top management would be appropriate. Carol has expressed her reservations about using segment information from the annual financial report for this purpose and has suggested that Greg consider other ways to evaluate the performance of segment managers.

Required:

1. Explain why the segment information prepared for public reporting purposes may not be appropriate for the evaluation of segment management performance.