Deck 4: Activity-Based Costing

Full screen (f)

Question

Overhead Variances and Their Disposal

Warner Company has the following data for the past year:

Warner uses the overhead control account to accumulate both actual and applied overhead.

Required:

1. Calculate the overhead variance for the year and close it to cost of goods sold.

2. Assume the variance calculated is material. After prorating, close the variances to the appropriate accounts and provide the final ending balances of these accounts.

3. What if the variance is of the opposite sign calculated in Requirement 1? Provide the appropriate adjusting journal entries for Requirements 1 and 2.

Warner Company has the following data for the past year:

Warner uses the overhead control account to accumulate both actual and applied overhead.

Required:

1. Calculate the overhead variance for the year and close it to cost of goods sold.

2. Assume the variance calculated is material. After prorating, close the variances to the appropriate accounts and provide the final ending balances of these accounts.

3. What if the variance is of the opposite sign calculated in Requirement 1? Provide the appropriate adjusting journal entries for Requirements 1 and 2.

Question

Question

TDABC

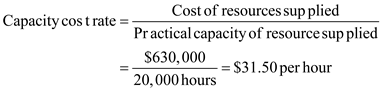

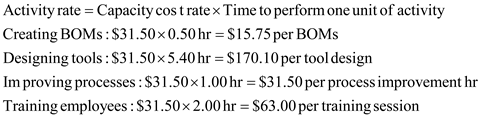

Bob Randall, cost accounting manager for Hemple Products, was asked to determine the costs of the activities performed within the company's Manufacturing Engineering Department. The department has the following activities: creating bills of materials (BOMs), studying manufacturing capabilities, improving manufacturing processes, training employees, and designing tools. The resource costs (from the general ledger) and the times to perform one unit of each activity are provided below.

Total machine and labor hours (at practical capacity):

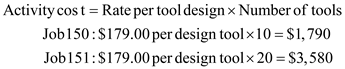

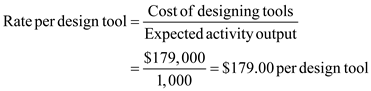

The activity, designing tools, uses the number of tools designed as the activity driver. Using a traditional approach, the cost of the designing tools activity was determined to be $179,000 (see Exercise 4.18) with an expected activity output of 1,000 for the coming year. During the first week of the year, two jobs (Job 150 and Job 151) had a demand for 10 and 20 new tools, respectively.

Required:

1. Calculate the capacity cost rate for the Manufacturing Engineering Department.

2. Using the capacity cost rate, determine the activity rates for each activity.

3. Calculate the cost of designing tools that would be assigned to each job using the TDABC- derived activity rate and then repeat using the traditional ABC rate. What might be the cause or causes that would explain the differences in the two approaches?

4. Now suppose that time for creating BOMs is 0.50 for a standard product but that creating a BOM for a custom product adds an additional 0.3 hour. Express the time equation for this added complexity and then calculate the activity rate for the activity of creating a BOM for custom products.

Bob Randall, cost accounting manager for Hemple Products, was asked to determine the costs of the activities performed within the company's Manufacturing Engineering Department. The department has the following activities: creating bills of materials (BOMs), studying manufacturing capabilities, improving manufacturing processes, training employees, and designing tools. The resource costs (from the general ledger) and the times to perform one unit of each activity are provided below.

Total machine and labor hours (at practical capacity):

The activity, designing tools, uses the number of tools designed as the activity driver. Using a traditional approach, the cost of the designing tools activity was determined to be $179,000 (see Exercise 4.18) with an expected activity output of 1,000 for the coming year. During the first week of the year, two jobs (Job 150 and Job 151) had a demand for 10 and 20 new tools, respectively.

Required:

1. Calculate the capacity cost rate for the Manufacturing Engineering Department.

2. Using the capacity cost rate, determine the activity rates for each activity.

3. Calculate the cost of designing tools that would be assigned to each job using the TDABC- derived activity rate and then repeat using the traditional ABC rate. What might be the cause or causes that would explain the differences in the two approaches?

4. Now suppose that time for creating BOMs is 0.50 for a standard product but that creating a BOM for a custom product adds an additional 0.3 hour. Express the time equation for this added complexity and then calculate the activity rate for the activity of creating a BOM for custom products.

Question

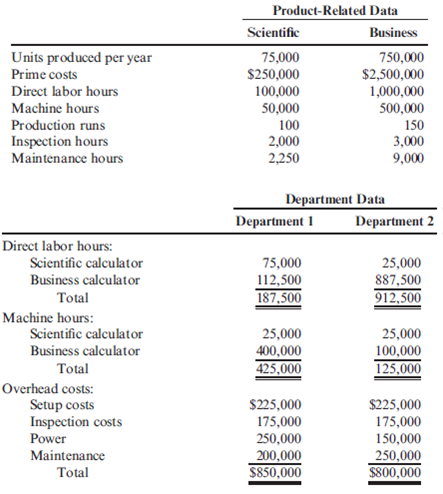

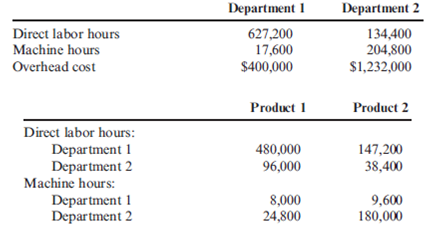

Product-Costing Accuracy, Plantwide and Departmental Rates, ABC

Escuha Company produces two type of calculators: scientific and business. Both products pass through two producing departments. The business calculator is by far the most popular. The following data have been gathered for these two products:

Required:

1. Compute the overhead cost per unit for each product using a plantwide, unit-based rate using direct labor hours.

2. Compute the overhead cost per unit for each product using departmental rates. In calculating departmental rates, use machine hours for Department 1 and direct labor hours for Department 2. Repeat using direct labor hours for Department 1 and machine hours for Department 2.

3. Compute the overhead cost per unit for each product using activity-based costing.

4. Comment on the ability of departmental rates to improve the accuracy of product costing.

Escuha Company produces two type of calculators: scientific and business. Both products pass through two producing departments. The business calculator is by far the most popular. The following data have been gathered for these two products:

Required:

1. Compute the overhead cost per unit for each product using a plantwide, unit-based rate using direct labor hours.

2. Compute the overhead cost per unit for each product using departmental rates. In calculating departmental rates, use machine hours for Department 1 and direct labor hours for Department 2. Repeat using direct labor hours for Department 1 and machine hours for Department 2.

3. Compute the overhead cost per unit for each product using activity-based costing.

4. Comment on the ability of departmental rates to improve the accuracy of product costing.

Question

Question

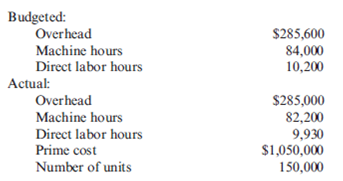

Predetermined Overhead Rate, Applied Overhead, Unit Cost

Ripley, Inc., costs products using a normal costing system. The following data are available for last year:

Overhead is applied on the basis of direct labor hours.

Required:

1. What was the predetermined overhead rate?

2. What was the applied overhead for last year?

3. Was overhead over- or underapplied, and by how much?

4. What was the total cost per unit produced (carry your answer to four significant digits)?

Ripley, Inc., costs products using a normal costing system. The following data are available for last year:

Overhead is applied on the basis of direct labor hours.

Required:

1. What was the predetermined overhead rate?

2. What was the applied overhead for last year?

3. Was overhead over- or underapplied, and by how much?

4. What was the total cost per unit produced (carry your answer to four significant digits)?

Question

Approximately Relevant ABC

Silven Company has identified the following overhead activities, costs, and activity drivers for the coming year:

Silven produces two models of cell phones with the following expected activity demands:

Required:

1. Determine the total overhead assigned to each product using the four activity drivers.

2. Determine the total overhead assigned to each model using the two most expensive activities. The costs of the two relatively inexpensive activities are allocated to the two expensive activities in proportion to their costs.

3. Using ABC as the benchmark, calculate the percentage error and comment on the accuracy of the reduced system. Explain why this approach may be desirable.

Silven Company has identified the following overhead activities, costs, and activity drivers for the coming year:

Silven produces two models of cell phones with the following expected activity demands:

Required:

1. Determine the total overhead assigned to each product using the four activity drivers.

2. Determine the total overhead assigned to each model using the two most expensive activities. The costs of the two relatively inexpensive activities are allocated to the two expensive activities in proportion to their costs.

3. Using ABC as the benchmark, calculate the percentage error and comment on the accuracy of the reduced system. Explain why this approach may be desirable.

Question

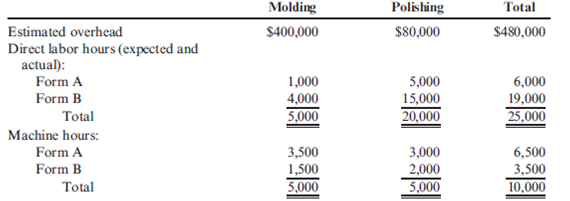

Departmental Overhead Rates

Lansing, Inc., provided the following data for its two producing departments:

Machine hours are used to assign the overhead of the Molding Department, and direct labor hours are used to assign the overhead of the Polishing Department. There are 30,000 units of Form A produced and sold and 50,000 of Form B.

Required:

1. Calculate the overhead rates for each department.

2. Using departmental rates, assign overhead to the two products and calculate the overhead cost per unit. How does this compare with the plantwide rate unit cost, using direct labor hours?

3. What if the machine hours in Molding were 1,200 for Form A and 3,800 for Form B and the direct labor hours used in Polishing were 5,000 and 15,000, respectively? Calculate the overhead cost per unit for each product using departmental rates, and compare with the plantwide rate unit costs calculated in Requirement 2. What can you conclude from this outcome?

Lansing, Inc., provided the following data for its two producing departments:

Machine hours are used to assign the overhead of the Molding Department, and direct labor hours are used to assign the overhead of the Polishing Department. There are 30,000 units of Form A produced and sold and 50,000 of Form B.

Required:

1. Calculate the overhead rates for each department.

2. Using departmental rates, assign overhead to the two products and calculate the overhead cost per unit. How does this compare with the plantwide rate unit cost, using direct labor hours?

3. What if the machine hours in Molding were 1,200 for Form A and 3,800 for Form B and the direct labor hours used in Polishing were 5,000 and 15,000, respectively? Calculate the overhead cost per unit for each product using departmental rates, and compare with the plantwide rate unit costs calculated in Requirement 2. What can you conclude from this outcome?

Question

Question

Question

Question

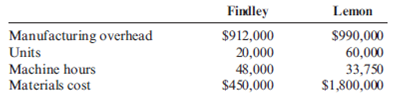

Predetermined Overhead Rate, Application of Overhead

Findley Company and Lemon Company both use predetermined overhead rates to apply manufacturing overhead to production. Findley's is based on machine hours, and Lemon's is based on materials cost. Budgeted production and cost data for Findley and Lemon are as follows:

At the end of the year, Findley Company had incurred overhead of $915,000 and had produced 19,600 units using 47,780 machine hours and materials costing $445,000. Lemon Company had incurred overhead of $972,000 and had produced 61,500 units using 32,650 machine hours and materials costing $1,777,500.

Required:

1. Compute the predetermined overhead rates for Findley Company and Lemon Company.

2. Was overhead over- or underapplied for each company, and by how much?

Findley Company and Lemon Company both use predetermined overhead rates to apply manufacturing overhead to production. Findley's is based on machine hours, and Lemon's is based on materials cost. Budgeted production and cost data for Findley and Lemon are as follows:

At the end of the year, Findley Company had incurred overhead of $915,000 and had produced 19,600 units using 47,780 machine hours and materials costing $445,000. Lemon Company had incurred overhead of $972,000 and had produced 61,500 units using 32,650 machine hours and materials costing $1,777,500.

Required:

1. Compute the predetermined overhead rates for Findley Company and Lemon Company.

2. Was overhead over- or underapplied for each company, and by how much?

Question

(2009 CPA Exam, adapted)

Merry Co. has two major categories of factory overhead: material handling and quality control. The costs expected for these categories for the coming year are:

The plant currently applies overhead based on direct labor hours. The estimated direct labor hours are 80,000 per year. The plant manager is asked to submit a bid and assembles the following data on a proposed job:

What amount is the estimated product cost on the proposed job?

a. $8,000

b. $10,000

c. $14,000

d. $18,000

Merry Co. has two major categories of factory overhead: material handling and quality control. The costs expected for these categories for the coming year are:

The plant currently applies overhead based on direct labor hours. The estimated direct labor hours are 80,000 per year. The plant manager is asked to submit a bid and assembles the following data on a proposed job:

What amount is the estimated product cost on the proposed job?

a. $8,000

b. $10,000

c. $14,000

d. $18,000

Question

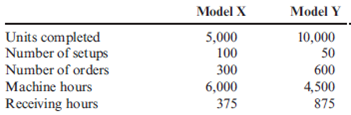

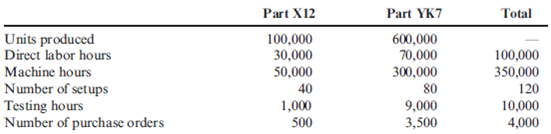

Consumption Ratios

Larsen, Inc., produces two types of electronic parts and has provided the following data:

There are four activities: machining, setting up, testing, and purchasing.

Required:

1. Calculate the activity consumption ratios for each product.

2. Calculate the consumption ratios for the plantwide rate (direct labor hours). When compared with the activity ratios, what can you say about the relative accuracy of a plantwide rate? Which product is undercosted?

3. What if the machine hours were used for the plantwide rate? Would this remove the cost distortion of a plantwide rate?

Larsen, Inc., produces two types of electronic parts and has provided the following data:

There are four activities: machining, setting up, testing, and purchasing.

Required:

1. Calculate the activity consumption ratios for each product.

2. Calculate the consumption ratios for the plantwide rate (direct labor hours). When compared with the activity ratios, what can you say about the relative accuracy of a plantwide rate? Which product is undercosted?

3. What if the machine hours were used for the plantwide rate? Would this remove the cost distortion of a plantwide rate?

Question

Question

Question

Question

Predetermined Overhead Rate, Overhead Variances, Journal Entries

Craig Company uses a predetermined overhead rate to assign overhead to jobs. Because Craig's production is machine intensive, overhead is applied on the basis of machine hours. The expected overhead for the year was $5.7 million, and the practical level of activity is 375,000 machine hours.

During the year, Craig used 382,500 machine hours and incurred actual overhead costs of $5.73 million. Craig also had the following balances of applied overhead in its accounts:

Required:

1. Compute a predetermined overhead rate for Craig.

2. Compute the overhead variance, and label it as under- or overapplied.

3. Assuming the overhead variance is immaterial, prepare the journal entry to dispose of the variance at the end of the year.

4. Assuming the overhead variance is material, prepare the journal entry that appropriately disposes of the overhead variance at the end of the year.

Craig Company uses a predetermined overhead rate to assign overhead to jobs. Because Craig's production is machine intensive, overhead is applied on the basis of machine hours. The expected overhead for the year was $5.7 million, and the practical level of activity is 375,000 machine hours.

During the year, Craig used 382,500 machine hours and incurred actual overhead costs of $5.73 million. Craig also had the following balances of applied overhead in its accounts:

Required:

1. Compute a predetermined overhead rate for Craig.

2. Compute the overhead variance, and label it as under- or overapplied.

3. Assuming the overhead variance is immaterial, prepare the journal entry to dispose of the variance at the end of the year.

4. Assuming the overhead variance is material, prepare the journal entry that appropriately disposes of the overhead variance at the end of the year.

Question

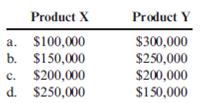

(2010 CPA Exam, adapted)

Boyle, Inc., makes two products, X and Y, that require allocation of indirect manufacturing costs. The following data were compiled by the accountant before making any allocations:

The total cost of setting up manufacturing processes and equipment is $400,000. The company uses a job-costing system with a single indirect cost rate. Under this system, allocated costs were $300,000 and $100,000 for X and Y, respectively. If an activity-based costing system is used, what would be the allocated costs for each product?

Boyle, Inc., makes two products, X and Y, that require allocation of indirect manufacturing costs. The following data were compiled by the accountant before making any allocations:

The total cost of setting up manufacturing processes and equipment is $400,000. The company uses a job-costing system with a single indirect cost rate. Under this system, allocated costs were $300,000 and $100,000 for X and Y, respectively. If an activity-based costing system is used, what would be the allocated costs for each product?

Question

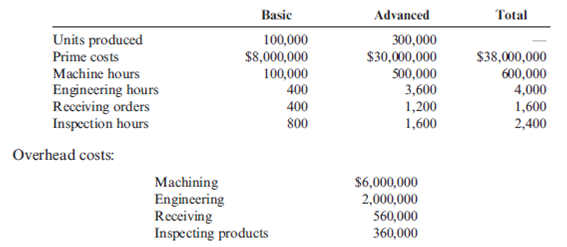

Activity-Based Product Costing

Roberts Company produces two weed eaters: basic and advanced. The company has four activities: machining, engineering, receiving, and packing. Information on these activities and their drivers is given below.

Required:

1. Calculate the four activity rates.

2. Calculate the unit costs using activity rates. Also, calculate the overhead cost per unit.

3. What if consumption ratios instead of activity rates were used to assign costs instead of activity rates? Show the cost assignment for the inspection activity.

Roberts Company produces two weed eaters: basic and advanced. The company has four activities: machining, engineering, receiving, and packing. Information on these activities and their drivers is given below.

Required:

1. Calculate the four activity rates.

2. Calculate the unit costs using activity rates. Also, calculate the overhead cost per unit.

3. What if consumption ratios instead of activity rates were used to assign costs instead of activity rates? Show the cost assignment for the inspection activity.

Question

Question

Question

Question

Departmental Overhead Rates

Mariposa, Inc., produces machine tools and currently uses a plantwide overhead rate, based on machine hours. Harry Whipple, the plant manager, has heard that departmental overhead rates can offer significantly better cost assignments than can a plantwide rate.

Mariposa has the following data for its two departments for the coming year:

Required:

1. Compute a predetermined overhead rate for the plant as a whole based on machine hours.

2. Compute predetermined overhead rates for each department using machine hours.

3. Suppose that a machine tool (Product X75) used 60 machine hours from Department A and 150 machine hours from Department B. A second machine tool (Product Y15) used 150 machine hours from Department A and 60 machine hours from Department B. Compute the overhead cost assigned to each product using the plantwide rate computed in Requirement 1. Repeat the computation using the departmental rates found in Requirement 2. Which of the two approaches gives the fairest assignment? Why?

4. Repeat Requirement 3 assuming the expected overhead cost for Department B is $360,000. Now would you recommend departmental rates over a plantwide rate?

Mariposa, Inc., produces machine tools and currently uses a plantwide overhead rate, based on machine hours. Harry Whipple, the plant manager, has heard that departmental overhead rates can offer significantly better cost assignments than can a plantwide rate.

Mariposa has the following data for its two departments for the coming year:

Required:

1. Compute a predetermined overhead rate for the plant as a whole based on machine hours.

2. Compute predetermined overhead rates for each department using machine hours.

3. Suppose that a machine tool (Product X75) used 60 machine hours from Department A and 150 machine hours from Department B. A second machine tool (Product Y15) used 150 machine hours from Department A and 60 machine hours from Department B. Compute the overhead cost assigned to each product using the plantwide rate computed in Requirement 1. Repeat the computation using the departmental rates found in Requirement 2. Which of the two approaches gives the fairest assignment? Why?

4. Repeat Requirement 3 assuming the expected overhead cost for Department B is $360,000. Now would you recommend departmental rates over a plantwide rate?

Question

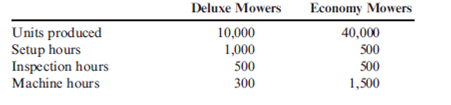

Consider the information given on two products and their usage of two overhead activities (setups and inspection):

Suppose that machine hours are used to assign all overhead costs to the two products. Which of the following is the best answer?

A) Deluxe mowers are undercosted, and regular mowers are overcosted.

B) Deluxe mowers and regular mowers are accurately costed.

C) Deluxe mowers are overcosted, and regular mowers are undercosted.

D) Using inspection hours to assign overhead costs is the best allocation approach.

Suppose that machine hours are used to assign all overhead costs to the two products. Which of the following is the best answer?

A) Deluxe mowers are undercosted, and regular mowers are overcosted.

B) Deluxe mowers and regular mowers are accurately costed.

C) Deluxe mowers are overcosted, and regular mowers are undercosted.

D) Using inspection hours to assign overhead costs is the best allocation approach.

Question

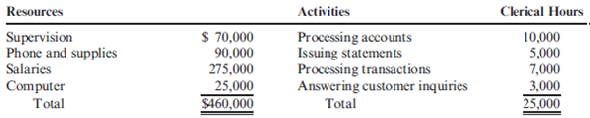

Assigning Cost of Resources to Activities, Unbundling the General Ledger

Golding Bank provided the following data about its resources and activities for its checking account process:

• Computers are used only by the issuing (30 percent) and processing transaction (70 percent) activities.

• Phone and supplies are 60 percent customer inquiries with the other 40 percent divided equally among the remaining activities, including supervising the checking operation.

• The supervisor spends 100 percent of his time on supervision. In addition to the 25,000 clerical hours, there are 2,000 hours of supervision used (the hours used by the supervising clerks activity, which is not listed above).

Required:

1. Prepare a work distribution matrix for the five primary activities.

2. Calculate the cost of each activity.

3. What if the cost of the supervising activity is assigned to the other four activities? Why would this be done? If it is done, what is the final cost of these four primary activities?

Golding Bank provided the following data about its resources and activities for its checking account process:

• Computers are used only by the issuing (30 percent) and processing transaction (70 percent) activities.

• Phone and supplies are 60 percent customer inquiries with the other 40 percent divided equally among the remaining activities, including supervising the checking operation.

• The supervisor spends 100 percent of his time on supervision. In addition to the 25,000 clerical hours, there are 2,000 hours of supervision used (the hours used by the supervising clerks activity, which is not listed above).

Required:

1. Prepare a work distribution matrix for the five primary activities.

2. Calculate the cost of each activity.

3. What if the cost of the supervising activity is assigned to the other four activities? Why would this be done? If it is done, what is the final cost of these four primary activities?

Question

Question

Predetermined Overhead Rates, Overhead Variances, Unit Costs

Primera Company produces two products and uses a predetermined overhead rate to apply overhead. Primera currently applies overhead using a plantwide rate based on direct labor hours. Consideration is being given to the use of departmental overhead rates where overhead would be applied on the basis of direct labor hours in Department 1 and on the basis of machine hours in Department 2. At the beginning of the year, the following estimates are provided:

Actual results reported by department and product during the year are as follows:

Required:

1. Compute the plantwide predetermined overhead rate and calculate the overhead assigned to each product.

2. Calculate the predetermined departmental overhead rates and calculate the overhead assigned to each product.

3. Using departmental rates, compute the applied overhead for the year. What is the under- or over applied overhead for the firm?

4. Prepare the journal entry that disposes of the overhead variance calculated in Requirement 3, assuming it is not material in amount. What additional information would you need if the variance is material to make the appropriate journal entry?

Primera Company produces two products and uses a predetermined overhead rate to apply overhead. Primera currently applies overhead using a plantwide rate based on direct labor hours. Consideration is being given to the use of departmental overhead rates where overhead would be applied on the basis of direct labor hours in Department 1 and on the basis of machine hours in Department 2. At the beginning of the year, the following estimates are provided:

Actual results reported by department and product during the year are as follows:

Required:

1. Compute the plantwide predetermined overhead rate and calculate the overhead assigned to each product.

2. Calculate the predetermined departmental overhead rates and calculate the overhead assigned to each product.

3. Using departmental rates, compute the applied overhead for the year. What is the under- or over applied overhead for the firm?

4. Prepare the journal entry that disposes of the overhead variance calculated in Requirement 3, assuming it is not material in amount. What additional information would you need if the variance is material to make the appropriate journal entry?

Question

Question

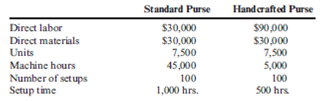

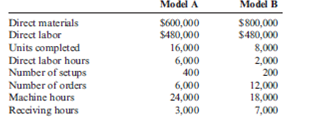

Drivers and Product-Costing Accuracy

McCourt Company produces two types of leather purses: standard and handcrafted. Both purses use equipment for cutting and stitching. The equipment also has the capability of creating standard designs. The standard purses use only these standard designs. They are all of the same size to accommodate the design features of the equipment. The handcrafted purses can be cut to any size because the designs are created manually. Many of the manually produced designs are in response to specific requests of retailers. The equipment must be specially configured to accommodate the production of a batch of purses that will receive a handcrafted design. McCourt Company assigns overhead using direct labor dollars. Muggs Clark, sales manager, is convinced that the purses are not being costed correctly.

To illustrate his point, he decided to focus on the expected annual setup and machine-related costs, which are as follows:

* Computed on a straight-line basis; book value at the beginning of the year was $250,000.

The machine has the capability of supplying 250,000 machine hours over its remaining life. Muggs also collected the expected annual prime costs for each purse, the machine hours, and the expected production (which is the normal output for the company).

Required:

1. Do you think that the direct labor costs and direct materials costs are accurately traced to each type of purse? Explain.

2. The controller has suggested that overhead costs be assigned to each product using a plantwide rate based on direct labor dollars. Machine costs and setup costs are overhead costs. Assume that these are the only overhead costs. For each type of purse, calculate the overhead per unit that would be assigned using a direct labor dollars overhead rate. Do you think that these costs are traced accurately to each purse? Explain.

3. Now calculate the overhead cost per unit per purse using two overhead rates: one for the setup activity and one for the machining activity. In choosing a driver to assign the setup costs, did you use number of setups or setup hours? Why? As part of your explanation, define transaction and duration drivers. Do you think machine costs are traced accurately to each type of purse? Explain.

McCourt Company produces two types of leather purses: standard and handcrafted. Both purses use equipment for cutting and stitching. The equipment also has the capability of creating standard designs. The standard purses use only these standard designs. They are all of the same size to accommodate the design features of the equipment. The handcrafted purses can be cut to any size because the designs are created manually. Many of the manually produced designs are in response to specific requests of retailers. The equipment must be specially configured to accommodate the production of a batch of purses that will receive a handcrafted design. McCourt Company assigns overhead using direct labor dollars. Muggs Clark, sales manager, is convinced that the purses are not being costed correctly.

To illustrate his point, he decided to focus on the expected annual setup and machine-related costs, which are as follows:

* Computed on a straight-line basis; book value at the beginning of the year was $250,000.

The machine has the capability of supplying 250,000 machine hours over its remaining life. Muggs also collected the expected annual prime costs for each purse, the machine hours, and the expected production (which is the normal output for the company).

Required:

1. Do you think that the direct labor costs and direct materials costs are accurately traced to each type of purse? Explain.

2. The controller has suggested that overhead costs be assigned to each product using a plantwide rate based on direct labor dollars. Machine costs and setup costs are overhead costs. Assume that these are the only overhead costs. For each type of purse, calculate the overhead per unit that would be assigned using a direct labor dollars overhead rate. Do you think that these costs are traced accurately to each purse? Explain.

3. Now calculate the overhead cost per unit per purse using two overhead rates: one for the setup activity and one for the machining activity. In choosing a driver to assign the setup costs, did you use number of setups or setup hours? Why? As part of your explanation, define transaction and duration drivers. Do you think machine costs are traced accurately to each type of purse? Explain.

Question

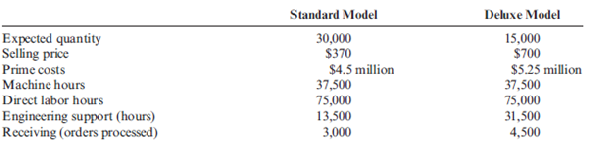

Unit-Based versus Activity-Based Costing

Fisico Company produces exercise bikes. One of its plants produces two versions: a standard model and a deluxe model. The deluxe model has a wider and sturdier base and a variety of electronic gadgets to help the exerciser monitor heartbeat, calories burned, distance traveled, etc. At the beginning of the year, the following data were prepared for this plant:

Additionally, the following overhead activity costs are reported:

Maintenance Engineering support Materials handling Setups Purchasing Receiving Paying suppliers

Required:

1. Calculate the cost per unit for each product using direct labor hours to assign all overhead costs.

2. Calculate activity rates and determine the overhead cost per unit. Compare these costs with those calculated using the unit-based method. Which cost is the most accurate? Explain.

Fisico Company produces exercise bikes. One of its plants produces two versions: a standard model and a deluxe model. The deluxe model has a wider and sturdier base and a variety of electronic gadgets to help the exerciser monitor heartbeat, calories burned, distance traveled, etc. At the beginning of the year, the following data were prepared for this plant:

Additionally, the following overhead activity costs are reported:

Maintenance Engineering support Materials handling Setups Purchasing Receiving Paying suppliers

Required:

1. Calculate the cost per unit for each product using direct labor hours to assign all overhead costs.

2. Calculate activity rates and determine the overhead cost per unit. Compare these costs with those calculated using the unit-based method. Which cost is the most accurate? Explain.

Question

Simplifying the ABC System: TDABC

Golding Bank provided the following data about its resources and activities for its checking account process:

Required:

1. Calculate the capacity cost rate for the checking account process.

2. Calculate the activity rates for the four activities. If the total number of statements issued was 20,000, calculate the cost of the issuing statements activity.

3. What if process improvements decreased the number of customer inquiries, leading to a 10 percent reduction in check processing hours and a $10,000 reduction in total resource costs? Update all the activity rates for these changes in operating conditions.

Golding Bank provided the following data about its resources and activities for its checking account process:

Required:

1. Calculate the capacity cost rate for the checking account process.

2. Calculate the activity rates for the four activities. If the total number of statements issued was 20,000, calculate the cost of the issuing statements activity.

3. What if process improvements decreased the number of customer inquiries, leading to a 10 percent reduction in check processing hours and a $10,000 reduction in total resource costs? Update all the activity rates for these changes in operating conditions.

Question

Question

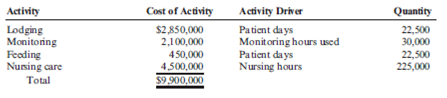

ABC, Resource Drivers, Service Industry

Glencoe Medical Clinic operates a cardiology care unit and a maternity care unit. Colby Hepworth, the clinic's administrator, is investigating the charges assigned to cardiology patients. Currently, all cardiology patients are charged the same rate per patient day for daily care services. Daily care services are broadly defined as occupancy, feeding, and nursing care. A recent study, however, revealed several interesting outcomes. First, the demands patients place on daily care services vary with the severity of the case being treated. Second, the occupancy activity is a combination of two activities: lodging and use of monitoring equipment. Since some patients require more monitoring than others, these activities should be separated. Third, the daily rate should reflect the difference in demands resulting from differences in patient type. Separating the occupancy activity into two separate activities also required the determination of the cost of each activity. Determining the costs of the monitoring activity was fairly easy because its costs were directly traceable. Lodging costs, however, are shared by two activities: lodging cardiology patients and lodging maternity care patients. The total lodging costs for the two activities were $5,700,000 per year and consisted of such items as building depreciation, building maintenance, and building utilities. The cardiology floor and the maternity floor each occupy 20,000 square feet. Hepworth determined that lodging costs would be assigned to each unit based on square feet.

To compute a daily rate that reflected the difference in demands, patients were placed in three categories according to illness severity, and the following annual data were collected:

The demands associated with patient severity are also provided:

Required:

1. Suppose that the costs of daily care are assigned using only patient days as the activity driver (which is also the measure of output). Compute the daily rate using this unit-based approach of cost assignment.

2. Compute activity rates using the given activity drivers (combine activities with the same driver).

3. Compute the charge per patient day for each patient type using the activity rates from Requirement 2 and the demands on each activity.

4. Suppose that the product is defined as "stay and treatment" where the treatment is bypass surgery. What additional information would you need to cost out this newly defined product?

5. Comment on the value of activity-based costing in service industries.

Glencoe Medical Clinic operates a cardiology care unit and a maternity care unit. Colby Hepworth, the clinic's administrator, is investigating the charges assigned to cardiology patients. Currently, all cardiology patients are charged the same rate per patient day for daily care services. Daily care services are broadly defined as occupancy, feeding, and nursing care. A recent study, however, revealed several interesting outcomes. First, the demands patients place on daily care services vary with the severity of the case being treated. Second, the occupancy activity is a combination of two activities: lodging and use of monitoring equipment. Since some patients require more monitoring than others, these activities should be separated. Third, the daily rate should reflect the difference in demands resulting from differences in patient type. Separating the occupancy activity into two separate activities also required the determination of the cost of each activity. Determining the costs of the monitoring activity was fairly easy because its costs were directly traceable. Lodging costs, however, are shared by two activities: lodging cardiology patients and lodging maternity care patients. The total lodging costs for the two activities were $5,700,000 per year and consisted of such items as building depreciation, building maintenance, and building utilities. The cardiology floor and the maternity floor each occupy 20,000 square feet. Hepworth determined that lodging costs would be assigned to each unit based on square feet.

To compute a daily rate that reflected the difference in demands, patients were placed in three categories according to illness severity, and the following annual data were collected:

The demands associated with patient severity are also provided:

Required:

1. Suppose that the costs of daily care are assigned using only patient days as the activity driver (which is also the measure of output). Compute the daily rate using this unit-based approach of cost assignment.

2. Compute activity rates using the given activity drivers (combine activities with the same driver).

3. Compute the charge per patient day for each patient type using the activity rates from Requirement 2 and the demands on each activity.

4. Suppose that the product is defined as "stay and treatment" where the treatment is bypass surgery. What additional information would you need to cost out this newly defined product?

5. Comment on the value of activity-based costing in service industries.

Question

Question

Multiple versus Single Overhead Rates, Activity Drivers

Deoro Company has identified the following overhead activities, costs, and activity drivers for the coming year:

Deoro produces two models of dishwashers with the following expected prime costs and activity demands:

The company's normal activity is 8,000 direct labor hours.

Required:

1. Determine the unit cost for each model using direct labor hours to apply overhead.

2. Determine the unit cost for each model using the four activity drivers.

3. Which method produces the more accurate cost assignment? Why?

Deoro Company has identified the following overhead activities, costs, and activity drivers for the coming year:

Deoro produces two models of dishwashers with the following expected prime costs and activity demands:

The company's normal activity is 8,000 direct labor hours.

Required:

1. Determine the unit cost for each model using direct labor hours to apply overhead.

2. Determine the unit cost for each model using the four activity drivers.

3. Which method produces the more accurate cost assignment? Why?

Question

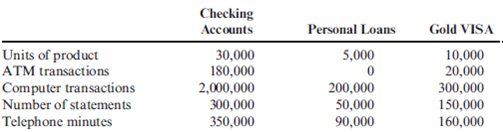

Activity-Based Costing: Service Firm

Glencoe First National Bank operated for years under the assumption that profitability can be increased by increasing dollar volumes. Historically, First National's efforts were directed toward increasing total dollars of sales and total dollars of account balances. In recent years, however, First National's profits have been eroding. Increased competition, particularly from savings and loan institutions, was the cause of the difficulties. As key managers discussed the bank's problems, it became apparent that they had no idea what their products were costing. Upon reflection, they realized that they had often made decisions to offer a new product which promised to increase dollar balances without any consideration of what it cost to provide the service.

After some discussion, the bank decided to hire a consultant to compute the costs of three products: checking accounts, personal loans, and the gold VISA. The consultant identified the following activities, costs, and activity drivers (annual data):

The following annual information on the three products was also made available:

In light of the new cost information, Larry Roberts, the bank president, wanted to know whether a decision made two years ago to modify the bank's checking account product was sound. At that time, the service charge was eliminated on accounts with an average annual balance greater than $1,000. Based on increases in the total dollars in checking, Larry was pleased with the new product. The checking account product is described as follows: (1) checking account balances greater than $500 earn interest of 2 percent per year, and (2) a service charge of $5 per month is charged for balances less than $1,000. The bank earns 4 percent on checking account deposits. Fifty percent of the accounts are less than $500 and have an average balance of $400 per account. Ten percent of the accounts are between $500 and $1,000 and average $750 per account. Twenty-five percent of the accounts are between $1,000 and $2,767; the average balance is $2,000. The remaining accounts carry a balance greater than $2,767. The average balance for these accounts is $5,000. Research indicates that the $2,000 category was by far the greatest contributor to the increase in dollar volume when the checking account product was modified two years ago.

Required:

1. Calculate rates for each activity.

2. Using the rates computed in Requirement 1, calculate the cost of each product.

3. Evaluate the checking account product. Are all accounts profitable? Compute the average annual profitability per account for the four categories of accounts described in the problem. What recommendations would you make to increase the profitability of the checking account product? (Break-even analysis for the unprofitable categories may be helpful.)

Glencoe First National Bank operated for years under the assumption that profitability can be increased by increasing dollar volumes. Historically, First National's efforts were directed toward increasing total dollars of sales and total dollars of account balances. In recent years, however, First National's profits have been eroding. Increased competition, particularly from savings and loan institutions, was the cause of the difficulties. As key managers discussed the bank's problems, it became apparent that they had no idea what their products were costing. Upon reflection, they realized that they had often made decisions to offer a new product which promised to increase dollar balances without any consideration of what it cost to provide the service.

After some discussion, the bank decided to hire a consultant to compute the costs of three products: checking accounts, personal loans, and the gold VISA. The consultant identified the following activities, costs, and activity drivers (annual data):

The following annual information on the three products was also made available:

In light of the new cost information, Larry Roberts, the bank president, wanted to know whether a decision made two years ago to modify the bank's checking account product was sound. At that time, the service charge was eliminated on accounts with an average annual balance greater than $1,000. Based on increases in the total dollars in checking, Larry was pleased with the new product. The checking account product is described as follows: (1) checking account balances greater than $500 earn interest of 2 percent per year, and (2) a service charge of $5 per month is charged for balances less than $1,000. The bank earns 4 percent on checking account deposits. Fifty percent of the accounts are less than $500 and have an average balance of $400 per account. Ten percent of the accounts are between $500 and $1,000 and average $750 per account. Twenty-five percent of the accounts are between $1,000 and $2,767; the average balance is $2,000. The remaining accounts carry a balance greater than $2,767. The average balance for these accounts is $5,000. Research indicates that the $2,000 category was by far the greatest contributor to the increase in dollar volume when the checking account product was modified two years ago.

Required:

1. Calculate rates for each activity.

2. Using the rates computed in Requirement 1, calculate the cost of each product.

3. Evaluate the checking account product. Are all accounts profitable? Compute the average annual profitability per account for the four categories of accounts described in the problem. What recommendations would you make to increase the profitability of the checking account product? (Break-even analysis for the unprofitable categories may be helpful.)

Question

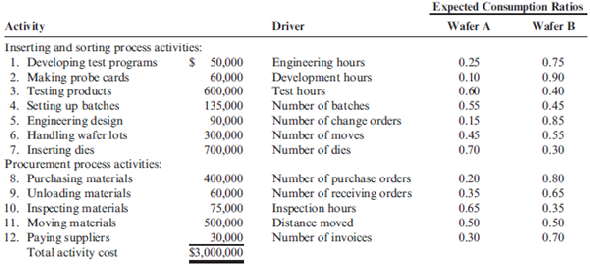

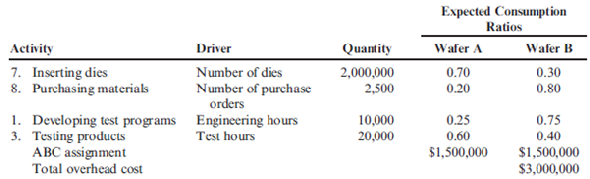

Simplifying the ABC System: Approximately Relevant ABC Systems

Patterson Company produces wafers for integrated circuits. Data for the most recent year are provided:

a Calculated using number of dies as the single unit-level driver.

a Calculated using number of dies as the single unit-level driver.

b Calculated by multiplying the consumption ratio of each product bythe cost of each activity.

Required:

1. Using the five most expensive activities, calculate the overhead cost assigned to each product. Assume that the costs of the other activities are assigned in proportion to the cost of the five activities.

2. Calculate the error relative to the fully specified ABC product cost and comment on the outcome.

3. What if activities 1, 2, 5, and 8 each had a cost of $650,000 and the remaining activities had a cost of $50,000? Calculate the cost assigned to Wafer A by a fully specified ABC system and then by an approximately relevant ABC approach. Comment on the implications for the approximately relevant approach.

Patterson Company produces wafers for integrated circuits. Data for the most recent year are provided:

a Calculated using number of dies as the single unit-level driver.b Calculated by multiplying the consumption ratio of each product bythe cost of each activity.

Required:

1. Using the five most expensive activities, calculate the overhead cost assigned to each product. Assume that the costs of the other activities are assigned in proportion to the cost of the five activities.

2. Calculate the error relative to the fully specified ABC product cost and comment on the outcome.

3. What if activities 1, 2, 5, and 8 each had a cost of $650,000 and the remaining activities had a cost of $50,000? Calculate the cost assigned to Wafer A by a fully specified ABC system and then by an approximately relevant ABC approach. Comment on the implications for the approximately relevant approach.

Question

Question

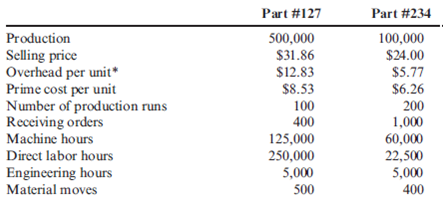

Product-Costing Accuracy, Corporate Strategy, ABC

Autotech Manufacturing is engaged in the production of replacement parts for automobiles. One plant specializes in the production of two parts: Part #127 and Part #2Part #127 produced the highest volume of activity, and for many years it was the only part produced by the plant. Five years ago, Part #234 was added. Part #234 was more difficult to manufacture and required special tooling and setups. Profits increased for the first three years after the addition of the new product. In the last two years, however, the plant faced intense competition, and its sales of Part #127 dropped. In fact, the plant showed a small loss in the most recent reporting period. Much of the competition was from foreign sources, and the plant manager was convinced that the foreign producers were guilty of selling the part below the cost of producing it. The following conversation between Patty Goodson, plant manager, and Joseph Fielding, divisional marketing manager, reflects the concerns of the division about the future of the plant and its products.

JOSEPH : You know, Patty, the divisional manager is real concerned about the plant's trend. He indicated that in this budgetary environment, we can't afford to carry plants that don't show a profit. We shut one down just last month because it couldn't handle the competition.

PATTY : Joe, you and I both know that Part #127 has a reputation for quality and value. It has been a mainstay for years. I don't understand what's happening.

JOSEPH : I just received a call from one of our major customers concerning Part #127. He said that a sales representative from another firm offered the part at $20 per unit-$11 less than what we charge. It's hard to compete with a price like that. Perhaps the plant is simply obsolete.

PATTY : No. I don't buy that. From my sources, I know we have good technology. We are efficient. And it's costing a little more than $21 to produce that part. I don't see how these companies can afford to sell it so cheaply. I'm not convinced that we should meet the price. Perhaps a better strategy is to emphasize producing and selling more of Part #234. Our margin is high on this product, and we have virtually no competition for it.

JOSEPH : You may be right. I think we can increase the price significantly and not lose business. I called a few customers to see how they would react to a 25 percent increase in price, and they all said that they would still purchase the same quantity as before.

PATTY : It sounds promising. However, before we make a major commitment to Part #234, I think we had better explore other possible explanations. I want to know how our production costs compare to those of our competitors. Perhaps we could be more efficient and find a way to earn our normal return on Part #127. The market is so much bigger for this part. I'm not sure we can survive with only Part #234. Besides, my production people hate that part. It's very difficult to produce.

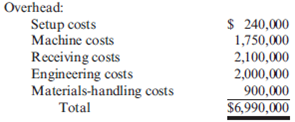

After her meeting with Joseph, Patty requested an investigation of the production costs and comparative efficiency. She received approval to hire a consulting group to make an independent investigation. After a three-month assessment, the consulting group provided the following information on the plant's production activities and costs associated with the two products:

* Calculated using a plantwide rate based on direct labor hours. This is the current way of assigning the plant's overhead to its products.

The consulting group recommended switching the overhead assignment to an activity-based approach. It maintained that activity-based cost assignment is more accurate and will provide better information for decision making. To facilitate this recommendation, it grouped the plant's activities into homogeneous sets with the following costs:

Required:

1. Verify the overhead cost per unit reported by the consulting group using direct labor hours to assign overhead. Compute the per-unit gross margin for each product.

2. After learning of activity-based costing, Patty asked the controller to compute the product cost using this approach. Recompute the unit cost of each product using activity-based costing. Compute the per-unit gross margin for each product.

3. Should the company switch its emphasis from the high-volume product to the low-volume product? Comment on the validity of the plant manager's concern that competitors are selling below the cost of making Part #127.

4. Explain the apparent lack of competition for Part #234. Comment also on the willingness of customers to accept a 25 percent increase in price for Part #234.

5. Assume that you are the manager of the plant. Describe what actions you would take based on the information provided by the activity-based unit costs.

Autotech Manufacturing is engaged in the production of replacement parts for automobiles. One plant specializes in the production of two parts: Part #127 and Part #2Part #127 produced the highest volume of activity, and for many years it was the only part produced by the plant. Five years ago, Part #234 was added. Part #234 was more difficult to manufacture and required special tooling and setups. Profits increased for the first three years after the addition of the new product. In the last two years, however, the plant faced intense competition, and its sales of Part #127 dropped. In fact, the plant showed a small loss in the most recent reporting period. Much of the competition was from foreign sources, and the plant manager was convinced that the foreign producers were guilty of selling the part below the cost of producing it. The following conversation between Patty Goodson, plant manager, and Joseph Fielding, divisional marketing manager, reflects the concerns of the division about the future of the plant and its products.

JOSEPH : You know, Patty, the divisional manager is real concerned about the plant's trend. He indicated that in this budgetary environment, we can't afford to carry plants that don't show a profit. We shut one down just last month because it couldn't handle the competition.

PATTY : Joe, you and I both know that Part #127 has a reputation for quality and value. It has been a mainstay for years. I don't understand what's happening.

JOSEPH : I just received a call from one of our major customers concerning Part #127. He said that a sales representative from another firm offered the part at $20 per unit-$11 less than what we charge. It's hard to compete with a price like that. Perhaps the plant is simply obsolete.

PATTY : No. I don't buy that. From my sources, I know we have good technology. We are efficient. And it's costing a little more than $21 to produce that part. I don't see how these companies can afford to sell it so cheaply. I'm not convinced that we should meet the price. Perhaps a better strategy is to emphasize producing and selling more of Part #234. Our margin is high on this product, and we have virtually no competition for it.

JOSEPH : You may be right. I think we can increase the price significantly and not lose business. I called a few customers to see how they would react to a 25 percent increase in price, and they all said that they would still purchase the same quantity as before.

PATTY : It sounds promising. However, before we make a major commitment to Part #234, I think we had better explore other possible explanations. I want to know how our production costs compare to those of our competitors. Perhaps we could be more efficient and find a way to earn our normal return on Part #127. The market is so much bigger for this part. I'm not sure we can survive with only Part #234. Besides, my production people hate that part. It's very difficult to produce.

After her meeting with Joseph, Patty requested an investigation of the production costs and comparative efficiency. She received approval to hire a consulting group to make an independent investigation. After a three-month assessment, the consulting group provided the following information on the plant's production activities and costs associated with the two products:

* Calculated using a plantwide rate based on direct labor hours. This is the current way of assigning the plant's overhead to its products.

The consulting group recommended switching the overhead assignment to an activity-based approach. It maintained that activity-based cost assignment is more accurate and will provide better information for decision making. To facilitate this recommendation, it grouped the plant's activities into homogeneous sets with the following costs:

Required:

1. Verify the overhead cost per unit reported by the consulting group using direct labor hours to assign overhead. Compute the per-unit gross margin for each product.

2. After learning of activity-based costing, Patty asked the controller to compute the product cost using this approach. Recompute the unit cost of each product using activity-based costing. Compute the per-unit gross margin for each product.

3. Should the company switch its emphasis from the high-volume product to the low-volume product? Comment on the validity of the plant manager's concern that competitors are selling below the cost of making Part #127.

4. Explain the apparent lack of competition for Part #234. Comment also on the willingness of customers to accept a 25 percent increase in price for Part #234.

5. Assume that you are the manager of the plant. Describe what actions you would take based on the information provided by the activity-based unit costs.

Question

Question

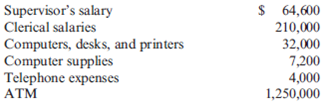

Assigning Resource Costs to Activities, Resource Drivers, Primary and Secondary Activities

Refer to the interview in Exercise 4.16 (especially to Questions 4 and 7). The general ledger reveals the following annual costs:

All nonlabor resources, other than the ATM, are spread evenly among the eight credit department employees (in terms of assignment and usage). Credit department employees have no contact with ATMs. Printers and desks are used in the same ratio as computers by the various activities.

Required:

1. Determine the cost of all primary and secondary activities.

2. Assign the cost of secondary activities to the primary activities.

Refer to the interview in Exercise 4.16 (especially to Questions 4 and 7). The general ledger reveals the following annual costs:

All nonlabor resources, other than the ATM, are spread evenly among the eight credit department employees (in terms of assignment and usage). Credit department employees have no contact with ATMs. Printers and desks are used in the same ratio as computers by the various activities.

Required:

1. Determine the cost of all primary and secondary activities.

2. Assign the cost of secondary activities to the primary activities.

Question

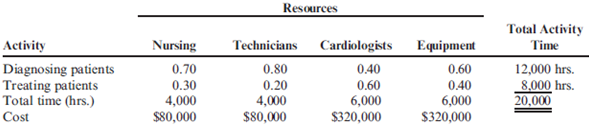

Time-Driven Activity-Based Costing Compared to ABC: Stage 1

The Bienestar Cardiology Clinic has two major activities: diagnostic and treatment. The two activities use four resources: nursing, medical technicians, cardiologists, and equipment. Detailed interviews have provided the work distribution matrix shown on page 196.

The total time estimated corresponds to practical capacity (interviewers adjusted the total time to about 80 percent of the available time). The equipment time is measured in machine hours. Thus, the total time (at practical capacity) in the system is 20,000 hours. In considering the implementation of a TDABC model, the following unit times and transaction information are also provided:

Required

1. Calculate the cost of each activity using the indicated values of the resource drivers.

2. Calculate the capacity cost rate for TDABC. Using the capacity cost rate, calculate the cost of each activity under TDABC. Compare these values with those obtained in Requirement 1 and discuss possible reasons for any differences.

3. Suppose that the actual activity driver quantities are 3,500 and 9,000. Calculate the cost of unused capacity.

4. Suppose that the clinic acquires new equipment that reduces the total time required for the two activities from 6,000 to 4,000 hours. The equipment cost remains the same. Explain how the ABC system would be updated and then describe how TDABC would provide updates.

5. Suppose that diagnosing patients without any cardiac disease takes two hours while diagnosing patients with mildly diseased hearts takes an additional 1.5 hours and those with more severe problems takes an additional two hours. Prepare a time equation and, using the capacity cost rate from Requirement 2, calculate the activity rate for each of the three types of patients.

The Bienestar Cardiology Clinic has two major activities: diagnostic and treatment. The two activities use four resources: nursing, medical technicians, cardiologists, and equipment. Detailed interviews have provided the work distribution matrix shown on page 196.

The total time estimated corresponds to practical capacity (interviewers adjusted the total time to about 80 percent of the available time). The equipment time is measured in machine hours. Thus, the total time (at practical capacity) in the system is 20,000 hours. In considering the implementation of a TDABC model, the following unit times and transaction information are also provided:

Required

1. Calculate the cost of each activity using the indicated values of the resource drivers.

2. Calculate the capacity cost rate for TDABC. Using the capacity cost rate, calculate the cost of each activity under TDABC. Compare these values with those obtained in Requirement 1 and discuss possible reasons for any differences.

3. Suppose that the actual activity driver quantities are 3,500 and 9,000. Calculate the cost of unused capacity.

4. Suppose that the clinic acquires new equipment that reduces the total time required for the two activities from 6,000 to 4,000 hours. The equipment cost remains the same. Explain how the ABC system would be updated and then describe how TDABC would provide updates.

5. Suppose that diagnosing patients without any cardiac disease takes two hours while diagnosing patients with mildly diseased hearts takes an additional 1.5 hours and those with more severe problems takes an additional two hours. Prepare a time equation and, using the capacity cost rate from Requirement 2, calculate the activity rate for each of the three types of patients.

Question

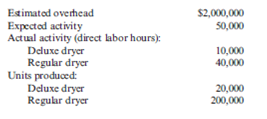

Applied Overhead and Unit Overhead Cost: Plantwide Rates

Seco, Inc., produces two types of clothes dryers: deluxe and regular. Seco uses a plantwide rate based on direct labor hours to assign its overhead costs. The company has the following estimated and actual data for the coming year:

Required:

1. Calculate the predetermined plantwide overhead rate and the applied overhead for each product, using direct labor hours.

2. Calculate the overhead cost per unit for each product.

3. What if the deluxe product used 20,000 hours (to produce 20,000 units) instead of 10,000 hours (total expected hours remain the same)? Calculate the effect on the profitability of this product line if all 20,000 units are sold, and then discuss the implications of this outcome.

Seco, Inc., produces two types of clothes dryers: deluxe and regular. Seco uses a plantwide rate based on direct labor hours to assign its overhead costs. The company has the following estimated and actual data for the coming year:

Required:

1. Calculate the predetermined plantwide overhead rate and the applied overhead for each product, using direct labor hours.

2. Calculate the overhead cost per unit for each product.

3. What if the deluxe product used 20,000 hours (to produce 20,000 units) instead of 10,000 hours (total expected hours remain the same)? Calculate the effect on the profitability of this product line if all 20,000 units are sold, and then discuss the implications of this outcome.

Question

Simplifying the ABC System: Equally Accurate Reduced ABC Systems

Selected activities and other information are provided for Patterson Company for its most recent year of operations.

Required:

1. Form reduced system cost pools for activities 7 and 8.

2. Assign the costs of the reduced system cost pools to Wafer A and Wafer B.

3. What if the two activities were 1 and 3? Repeat Requirements 1 and 2. What does this imply?

Selected activities and other information are provided for Patterson Company for its most recent year of operations.

Required:

1. Form reduced system cost pools for activities 7 and 8.

2. Assign the costs of the reduced system cost pools to Wafer A and Wafer B.

3. What if the two activities were 1 and 3? Repeat Requirements 1 and 2. What does this imply?

Question

Assigning Resource Costs to Activities, Resource Drivers, Primary and Secondary Activities

Bob Randall, cost accounting manager for Hemple Products, was asked to determine the costs of the activities performed within the company's Manufacturing Engineering Department. The department has the following activities: creating bills of materials (BOMs), studying manufacturing capabilities, improving manufacturing processes, training employees, and designing tools. The general ledger accounts reveal the following expenditures for Manufacturing Engineering:

The equipment is used for two activities: improving processes and designing tools. The equipment's time is divided by two activities: 40 percent for improving processes and 60 percent for designing tools. The salaries are for nine engineers, one who earns $100,000 and eight who earn $50,000 each. The $100,000 engineer spends 40 percent of her time training employees in new processes and 60 percent of her time on improving processes. One engineer spends 100 percent of her time on designing tools, and another engineer spends 100 percent of his time on improving processes. The remaining six engineers spend equal time on all activities. Supplies are consumed in the following proportions:

After determining the costs of the engineering activities, Bob was then asked to describe how these costs would be assigned to jobs produced within the factory. (The company manufactures machine parts on a job-order basis.) Bob responded by indicating that creating BOMs and designing tools were the only primary activities. The remaining were secondary activities. After some analysis, Bob concluded that studying manufacturing capabilities was an activity that enabled the other four activities to be realized. He also noted that all of the employees being trained are manufacturing workers-employees who work directly on the products. The major manufacturing activities are cutting, drilling, lathing, welding, and assembly. The costs of these activities are assigned to the various products using hours of usage (grinding hours, drilling hours, etc.). Furthermore, tools were designed to enable the production of specific jobs. Finally, the process improvement activity focused only on the five major manufacturing activities.

Required:

1. What is meant by unbundling general ledger costs? Why is it necessary?

2. What is the difference between a general ledger database system and an activity-based database system?

3. Using the resource drivers and direct tracing, calculate the costs of each manufacturing engineering activity. What are the resource drivers?

4. Describe in detail how the costs of the engineering activities would be assigned to jobs using activity-based costing. Include a description of the activity drivers that might be used. Where appropriate, identify both a possible transaction driver and a possible duration driver.

Bob Randall, cost accounting manager for Hemple Products, was asked to determine the costs of the activities performed within the company's Manufacturing Engineering Department. The department has the following activities: creating bills of materials (BOMs), studying manufacturing capabilities, improving manufacturing processes, training employees, and designing tools. The general ledger accounts reveal the following expenditures for Manufacturing Engineering:

The equipment is used for two activities: improving processes and designing tools. The equipment's time is divided by two activities: 40 percent for improving processes and 60 percent for designing tools. The salaries are for nine engineers, one who earns $100,000 and eight who earn $50,000 each. The $100,000 engineer spends 40 percent of her time training employees in new processes and 60 percent of her time on improving processes. One engineer spends 100 percent of her time on designing tools, and another engineer spends 100 percent of his time on improving processes. The remaining six engineers spend equal time on all activities. Supplies are consumed in the following proportions:

After determining the costs of the engineering activities, Bob was then asked to describe how these costs would be assigned to jobs produced within the factory. (The company manufactures machine parts on a job-order basis.) Bob responded by indicating that creating BOMs and designing tools were the only primary activities. The remaining were secondary activities. After some analysis, Bob concluded that studying manufacturing capabilities was an activity that enabled the other four activities to be realized. He also noted that all of the employees being trained are manufacturing workers-employees who work directly on the products. The major manufacturing activities are cutting, drilling, lathing, welding, and assembly. The costs of these activities are assigned to the various products using hours of usage (grinding hours, drilling hours, etc.). Furthermore, tools were designed to enable the production of specific jobs. Finally, the process improvement activity focused only on the five major manufacturing activities.

Required:

1. What is meant by unbundling general ledger costs? Why is it necessary?

2. What is the difference between a general ledger database system and an activity-based database system?

3. Using the resource drivers and direct tracing, calculate the costs of each manufacturing engineering activity. What are the resource drivers?

4. Describe in detail how the costs of the engineering activities would be assigned to jobs using activity-based costing. Include a description of the activity drivers that might be used. Where appropriate, identify both a possible transaction driver and a possible duration driver.

Question

Activity-Based Costing, Reducing the Number of Drivers and Equal Accuracy

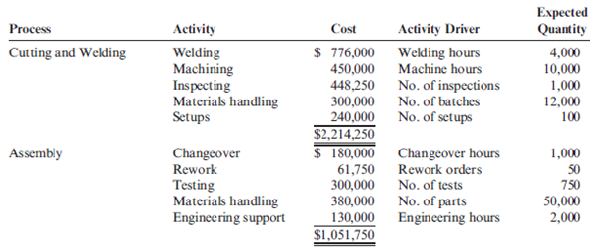

Reducir, Inc., produces two different types of hydraulic cylinders. Reducir produces a major subassembly for the cylinders in the Cutting and Welding Department. Other parts and the subassembly are then assembled in the Assembly Department. The activities, expected costs, and drivers associated with these two manufacturing processes are given below.

Note: In the assembly process, the materials-handling activity is a function of product characteristics rather than batch activity.

Other overhead activities, their costs, and drivers are listed below.

Other production information concerning the two hydraulic cylinders is also provided:

Required:

1. Using a plantwide rate based on machine hours, calculate the total overhead cost assigned to each product and the unit overhead cost.

2. Using activity rates, calculate the total overhead cost assigned to each product and the unit overhead cost. Comment on the accuracy of the plantwide rate.

3. Calculate the global consumption ratios.

4. Calculate the consumption ratios for welding and materials handling (Assembly) and show that two drivers, welding hours and number of parts, can be used to achieve the same ABC product costs calculated in Requirement 2. Explain the value of this simplification.

5. Calculate the consumption ratios for inspection and engineering, and show that the drivers for these two activities also duplicate the ABC product costs calculated in Requirement 2.

Reducir, Inc., produces two different types of hydraulic cylinders. Reducir produces a major subassembly for the cylinders in the Cutting and Welding Department. Other parts and the subassembly are then assembled in the Assembly Department. The activities, expected costs, and drivers associated with these two manufacturing processes are given below.

Note: In the assembly process, the materials-handling activity is a function of product characteristics rather than batch activity.

Other overhead activities, their costs, and drivers are listed below.

Other production information concerning the two hydraulic cylinders is also provided:

Required:

1. Using a plantwide rate based on machine hours, calculate the total overhead cost assigned to each product and the unit overhead cost.

2. Using activity rates, calculate the total overhead cost assigned to each product and the unit overhead cost. Comment on the accuracy of the plantwide rate.

3. Calculate the global consumption ratios.

4. Calculate the consumption ratios for welding and materials handling (Assembly) and show that two drivers, welding hours and number of parts, can be used to achieve the same ABC product costs calculated in Requirement 2. Explain the value of this simplification.

5. Calculate the consumption ratios for inspection and engineering, and show that the drivers for these two activities also duplicate the ABC product costs calculated in Requirement 2.

Question

Question

Question

Question

Approximately Relevant ABC

Refer to the data given in Problem 4.34 and suppose that the expected activity costs are reported as follows (all other data remain the same):

Other overhead activities:

The per unit overhead cost using the 14 activity-based drivers is $1,108 and $779 for Cylinder A and Cylinder B, respectively.

Required:

1. Determine the percentage of total costs represented by the three most expensive activities.

2. Allocate the costs of all other activities to the three activities identified in Requirement 1. Allocate the other activity costs to the three activities in proportion to their individual activity costs. Now assign these total costs to the products using the drivers of the three chosen activities.

3. Using the costs assigned in Requirement 2, calculate the percentage error using the ABC costs as a benchmark. Comment on the value and advantages of this ABC simplification.

Refer to the data given in Problem 4.34 and suppose that the expected activity costs are reported as follows (all other data remain the same):

Other overhead activities:

The per unit overhead cost using the 14 activity-based drivers is $1,108 and $779 for Cylinder A and Cylinder B, respectively.

Required:

1. Determine the percentage of total costs represented by the three most expensive activities.

2. Allocate the costs of all other activities to the three activities identified in Requirement 1. Allocate the other activity costs to the three activities in proportion to their individual activity costs. Now assign these total costs to the products using the drivers of the three chosen activities.

3. Using the costs assigned in Requirement 2, calculate the percentage error using the ABC costs as a benchmark. Comment on the value and advantages of this ABC simplification.

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/51

Play

Full screen (f)

Deck 4: Activity-Based Costing

1

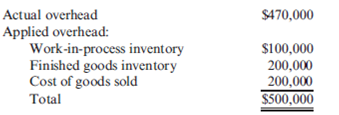

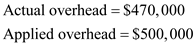

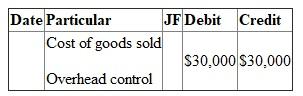

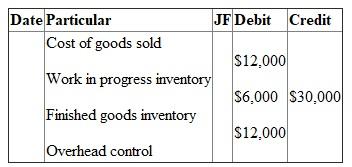

Overhead Variances and Their Disposal

Warner Company has the following data for the past year:

Warner uses the overhead control account to accumulate both actual and applied overhead.

Required:

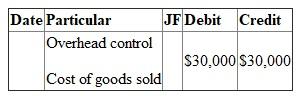

1. Calculate the overhead variance for the year and close it to cost of goods sold.

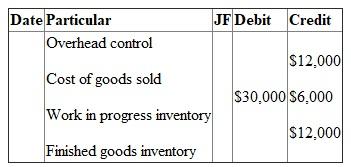

2. Assume the variance calculated is material. After prorating, close the variances to the appropriate accounts and provide the final ending balances of these accounts.

3. What if the variance is of the opposite sign calculated in Requirement 1? Provide the appropriate adjusting journal entries for Requirements 1 and 2.

Warner Company has the following data for the past year:

Warner uses the overhead control account to accumulate both actual and applied overhead.

Required:

1. Calculate the overhead variance for the year and close it to cost of goods sold.

2. Assume the variance calculated is material. After prorating, close the variances to the appropriate accounts and provide the final ending balances of these accounts.

3. What if the variance is of the opposite sign calculated in Requirement 1? Provide the appropriate adjusting journal entries for Requirements 1 and 2.

The past year's data of Warner Company is given:

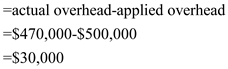

1.Given:

Over head variance is

Over head variance is

2.On proration as per the balances given:

2.On proration as per the balances given:

Unadjusted

Unadjusted

3.

3.

1.Given:

Over head variance is 2.On proration as per the balances given: Unadjusted 3. 2

What is a bill of activities?

A bill of activities specifies:

1. The product

2. Quantity expected of products

3. Activities

4. Consumption of activity by each product

1. The product

2. Quantity expected of products

3. Activities

4. Consumption of activity by each product

3

TDABC

Bob Randall, cost accounting manager for Hemple Products, was asked to determine the costs of the activities performed within the company's Manufacturing Engineering Department. The department has the following activities: creating bills of materials (BOMs), studying manufacturing capabilities, improving manufacturing processes, training employees, and designing tools. The resource costs (from the general ledger) and the times to perform one unit of each activity are provided below.

Total machine and labor hours (at practical capacity):