Deck 7: Allocating Costs of Support Departments and Joint Products

Full screen (f)

Question

Question

Question

Question

Physical Units Method, Relative Sales Value Method

Farleigh Petroleum, Inc., is a small company that acquires high-grade crude oil from low-volume production wells owned by individuals and small partnerships. The crude oil is processed in a single refinery into Two Oil, Six Oil, and impure distillates. Farleigh Petroleum does not have the technology or capacity to process these products further and sells most of its output each month to major refineries. There were no beginning finished goods or work-in-process inventories on April 1. The production costs and output of Farleigh Petroleum for April are as follows:

Data on barrels produced and selling price:

Two Oil, 300,000 barrels produced; sales price, $45 per barrel

Six Oil, 170,000 barrels produced; sales price, $25 per barrel

Distillates, 80,000 barrels produced; sales price, $14 per barrel

Required:

1. Calculate the amount of joint production cost that Farleigh Petroleum would allocate to each of the three joint products by using the physical units method. (Carry out the ratio calculation to four decimal places. Round allocated costs to the nearest dollar.)

2. Calculate the amount of joint production cost that Farleigh Petroleum would allocate to each of the three joint products by using the relative sales value method. (Carry out the ratio calculation to four decimal places. Round allocated costs to the nearest dollar.)

Farleigh Petroleum, Inc., is a small company that acquires high-grade crude oil from low-volume production wells owned by individuals and small partnerships. The crude oil is processed in a single refinery into Two Oil, Six Oil, and impure distillates. Farleigh Petroleum does not have the technology or capacity to process these products further and sells most of its output each month to major refineries. There were no beginning finished goods or work-in-process inventories on April 1. The production costs and output of Farleigh Petroleum for April are as follows:

Data on barrels produced and selling price:

Two Oil, 300,000 barrels produced; sales price, $45 per barrel

Six Oil, 170,000 barrels produced; sales price, $25 per barrel

Distillates, 80,000 barrels produced; sales price, $14 per barrel

Required:

1. Calculate the amount of joint production cost that Farleigh Petroleum would allocate to each of the three joint products by using the physical units method. (Carry out the ratio calculation to four decimal places. Round allocated costs to the nearest dollar.)

2. Calculate the amount of joint production cost that Farleigh Petroleum would allocate to each of the three joint products by using the relative sales value method. (Carry out the ratio calculation to four decimal places. Round allocated costs to the nearest dollar.)

Question

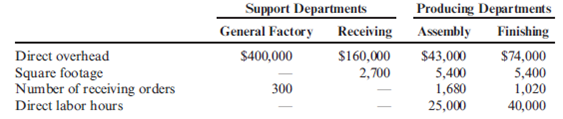

Direct Method of Support Department Cost Allocation

Valron Company has two support departments, Human Resources and General Factory, and two producing departments, Fabricating and Assembly.

The costs of the Human Resources Department are allocated on the basis of number of employees, and the costs of General Factory are allocated on the basis of square footage. Valron Company uses the direct method of support department cost allocation.

Required:

1. Calculate the allocation ratios for the four departments using the direct method.

2. Using the direct method, allocate the costs of the Human Resources and General Factory departments to the Fabricating and Assembly departments.

3. What if the General Factory Department had 40 employees? How would that affect the allocation of Human Resources Department costs to the Fabricating and Assembly departments?

Valron Company has two support departments, Human Resources and General Factory, and two producing departments, Fabricating and Assembly.

The costs of the Human Resources Department are allocated on the basis of number of employees, and the costs of General Factory are allocated on the basis of square footage. Valron Company uses the direct method of support department cost allocation.

Required:

1. Calculate the allocation ratios for the four departments using the direct method.

2. Using the direct method, allocate the costs of the Human Resources and General Factory departments to the Fabricating and Assembly departments.

3. What if the General Factory Department had 40 employees? How would that affect the allocation of Human Resources Department costs to the Fabricating and Assembly departments?

Question

Question

Reciprocal Method

Eilers Company has two producing departments and two support departments. The following budgeted data pertain to these four departments:

Required:

1. Allocate the overhead costs of the support departments to the producing departments using the reciprocal method. (Round allocation ratios to four significant digits. Round allocated costs to the nearest dollar.)

2. Using direct labor hours, compute departmental overhead rates. (Round to the nearest cent.)

Eilers Company has two producing departments and two support departments. The following budgeted data pertain to these four departments:

Required:

1. Allocate the overhead costs of the support departments to the producing departments using the reciprocal method. (Round allocation ratios to four significant digits. Round allocated costs to the nearest dollar.)

2. Using direct labor hours, compute departmental overhead rates. (Round to the nearest cent.)

Question

Fixed and Variable Cost Allocation

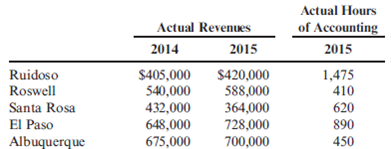

Welcome Inns is a chain of motels serving business travelers in New Mexico and southwest Texas. The chain has grown from one motel in 2011 to five motels. In 2015, the owner of the company decided to set up an internal Accounting Department to centralize control of financial information. (Previously, local CPAs handled each motel's bookkeeping and financial reporting.) The accounting office was opened in January 2015 by renting space adjacent to corporate headquarters in Ruidoso, New Mexico. All motels have been supplied with personal computers and internet access to transfer information to central accounting on a daily basis.

The Accounting Department has budgeted fixed costs of $135,000 per year. Variable costs are budgeted at $20 per hour. In 2015, actual cost for the Accounting Department was $223,000. Further information is as follows:

Required:

1. Suppose the total actual costs of the Accounting Department are allocated on the basis of 2015 sales revenue. How much will be allocated to each motel?

2. Suppose that Welcome Inns views 2014 sales figures as a proxy for budgeted capacity of the motels. Thus, fixed Accounting Department costs are allocated on the basis of 2014 sales, and variable costs are allocated according to 2015 usage multiplied by the variable rate. How much Accounting Department cost will be allocated to each motel?

3. Comment on the two allocation schemes. Which motels would prefer the method in Requirement 1? The method in Requirement 2? Explain.

Welcome Inns is a chain of motels serving business travelers in New Mexico and southwest Texas. The chain has grown from one motel in 2011 to five motels. In 2015, the owner of the company decided to set up an internal Accounting Department to centralize control of financial information. (Previously, local CPAs handled each motel's bookkeeping and financial reporting.) The accounting office was opened in January 2015 by renting space adjacent to corporate headquarters in Ruidoso, New Mexico. All motels have been supplied with personal computers and internet access to transfer information to central accounting on a daily basis.

The Accounting Department has budgeted fixed costs of $135,000 per year. Variable costs are budgeted at $20 per hour. In 2015, actual cost for the Accounting Department was $223,000. Further information is as follows:

Required:

1. Suppose the total actual costs of the Accounting Department are allocated on the basis of 2015 sales revenue. How much will be allocated to each motel?

2. Suppose that Welcome Inns views 2014 sales figures as a proxy for budgeted capacity of the motels. Thus, fixed Accounting Department costs are allocated on the basis of 2014 sales, and variable costs are allocated according to 2015 usage multiplied by the variable rate. How much Accounting Department cost will be allocated to each motel?

3. Comment on the two allocation schemes. Which motels would prefer the method in Requirement 1? The method in Requirement 2? Explain.

Question

Question

Question

Question

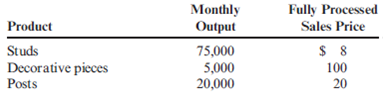

Physical Units Method, Relative Sales-Value-at-Split-off Method, Net Realizable Value Method, Decision Making

Sonimad Sawmill, Inc. (SSI), purchases logs from independent timber contractors and processes them into the following three types of lumber products:

1. Studs for residential construction (e.g., walls and ceilings)

2. Decorative pieces (e.g., fireplace mantels and beams for cathedral ceilings)

3. Posts used as support braces (e.g., mine support braces and braces for exterior fences around ranch properties)

These products are the result of a joint sawmill process that involves removing bark from the logs, cutting the logs into a workable size (ranging from 8 to 16 feet in length), and then cutting the individual products from the logs, depending upon the type of wood (pine, oak, walnut, or maple) and the size (diameter) of the log.

The joint process results in the following costs and output of products during a typical month:

Product yield and average sales value on a per-unit basis from the joint process are as follows:

The studs are sold as rough-cut lumber after emerging from the sawmill operation without further processing by SSI. Also, the posts require no further processing. The decorative pieces must be planed and further sized after emerging from the SSI sawmill. This additional processing costs SSI $100,000 per month and normally results in a loss of 10 percent of the units entering the process. Without this planing and sizing process, there is still an active intermediate market for the unfinished decorative pieces where the sales price averages $60 per unit.

Required:

1. Based on the information given for Sonimad Sawmill, Inc., allocate the joint processing costs of $1,000,000 to each of the three product lines using the:

a. Relative sales-value-at-split-off method

b. Physical units method at split-off

c. Estimated net realizable value method

2. Prepare an analysis for Sonimad Sawmill, Inc., to compare processing the decorative pieces further as it presently does, with selling the rough-cut product immediately at split-off. Be sure to provide all calculations.

3. Assume Sonimad Sawmill, Inc., announced that in six months it will sell the rough-cut product at split-off due to increasing competitive pressure. Identify at least three types of likely behavior that will be demonstrated by the skilled labor in the planing and sizing process as a result of this announcement. Explain how this behavior could be improved by management. (CMA adapted)

Sonimad Sawmill, Inc. (SSI), purchases logs from independent timber contractors and processes them into the following three types of lumber products:

1. Studs for residential construction (e.g., walls and ceilings)

2. Decorative pieces (e.g., fireplace mantels and beams for cathedral ceilings)

3. Posts used as support braces (e.g., mine support braces and braces for exterior fences around ranch properties)

These products are the result of a joint sawmill process that involves removing bark from the logs, cutting the logs into a workable size (ranging from 8 to 16 feet in length), and then cutting the individual products from the logs, depending upon the type of wood (pine, oak, walnut, or maple) and the size (diameter) of the log.

The joint process results in the following costs and output of products during a typical month:

Product yield and average sales value on a per-unit basis from the joint process are as follows:

The studs are sold as rough-cut lumber after emerging from the sawmill operation without further processing by SSI. Also, the posts require no further processing. The decorative pieces must be planed and further sized after emerging from the SSI sawmill. This additional processing costs SSI $100,000 per month and normally results in a loss of 10 percent of the units entering the process. Without this planing and sizing process, there is still an active intermediate market for the unfinished decorative pieces where the sales price averages $60 per unit.

Required:

1. Based on the information given for Sonimad Sawmill, Inc., allocate the joint processing costs of $1,000,000 to each of the three product lines using the:

a. Relative sales-value-at-split-off method

b. Physical units method at split-off

c. Estimated net realizable value method

2. Prepare an analysis for Sonimad Sawmill, Inc., to compare processing the decorative pieces further as it presently does, with selling the rough-cut product immediately at split-off. Be sure to provide all calculations.

3. Assume Sonimad Sawmill, Inc., announced that in six months it will sell the rough-cut product at split-off due to increasing competitive pressure. Identify at least three types of likely behavior that will be demonstrated by the skilled labor in the planing and sizing process as a result of this announcement. Explain how this behavior could be improved by management. (CMA adapted)

Question

Question

Question

Question

Question

Question

Question

Physical Units Method

Alomar Company manufactures four products from a joint production process: barlon, selene, plicene, and corsol. The joint costs for one batch are as follows:

At the split-off point, a batch yields 1,400 barlon, 2,600 selene, 2,500 plicene, and 3,500 corsol. All products are sold at the split-off point: barlon sells for $15 per unit, selene sells for $20 per unit, plicene sells for $26 per unit, and corsol sells for $35 per unit.

Carry out all percent calculations to four significant digits.

Required:

1. Allocate the joint costs using the physical units method.

2. Suppose that the products are weighted as shown on page 368.

Allocate the joint costs using the weighted average method.

Alomar Company manufactures four products from a joint production process: barlon, selene, plicene, and corsol. The joint costs for one batch are as follows:

At the split-off point, a batch yields 1,400 barlon, 2,600 selene, 2,500 plicene, and 3,500 corsol. All products are sold at the split-off point: barlon sells for $15 per unit, selene sells for $20 per unit, plicene sells for $26 per unit, and corsol sells for $35 per unit.

Carry out all percent calculations to four significant digits.

Required:

1. Allocate the joint costs using the physical units method.

2. Suppose that the products are weighted as shown on page 368.

Allocate the joint costs using the weighted average method.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

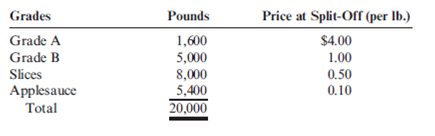

Allocating Joint Costs Using the Physical Units Method

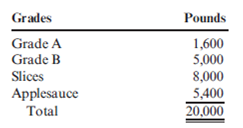

Orchard Fresh, Inc., purchases apples from local orchards and sorts them into four categories. Grade A are large blemish-free apples that can be sold to gourmet fruit sellers. Grade B apples are smaller and may be slightly out of proportion. These are packed in boxes and sold to grocery stores. Apples for slices are even smaller than Grade B apples and have blemishes. Apples for applesauce are of lower grade than apples for slices, yet still suitable for canning. Information on a recent purchase of 20,000 pounds of apples is as follows:

Total joint cost is $18,000.

Required:

1. Allocate the joint cost to the four grades of apples using the physical units method. (Carry out the percent calculations to four significant digits.)

2. Allocate the joint cost to the four grades of apples by finding the average joint cost per pound and multiplying it by the number of pounds in the grade. (Round all cost allocations to the nearest dollar.)

3. What if there were 2,000 pounds of Grade A apples and 4,600 pounds of Grade B? How would that affect the allocation of cost to these two grades? How would it affect the allocation of cost to the remaining common grades?

Orchard Fresh, Inc., purchases apples from local orchards and sorts them into four categories. Grade A are large blemish-free apples that can be sold to gourmet fruit sellers. Grade B apples are smaller and may be slightly out of proportion. These are packed in boxes and sold to grocery stores. Apples for slices are even smaller than Grade B apples and have blemishes. Apples for applesauce are of lower grade than apples for slices, yet still suitable for canning. Information on a recent purchase of 20,000 pounds of apples is as follows:

Total joint cost is $18,000.

Required:

1. Allocate the joint cost to the four grades of apples using the physical units method. (Carry out the percent calculations to four significant digits.)

2. Allocate the joint cost to the four grades of apples by finding the average joint cost per pound and multiplying it by the number of pounds in the grade. (Round all cost allocations to the nearest dollar.)

3. What if there were 2,000 pounds of Grade A apples and 4,600 pounds of Grade B? How would that affect the allocation of cost to these two grades? How would it affect the allocation of cost to the remaining common grades?

Question

Question

A company uses charging rates to allocate service department costs to the using departments. The accountant compiled the following information on one of the service departments:

If Department K plans to use 1,350 hours of the service department's service in the coming year, how much of the service department's cost is allocated to Department K?

A) $3,375

B) $27,300

C) $26,325

D) $23,950

If Department K plans to use 1,350 hours of the service department's service in the coming year, how much of the service department's cost is allocated to Department K?

A) $3,375

B) $27,300

C) $26,325

D) $23,950

Question

Question

Question

Chester Company provided information on overhead for its three producing departments as follows:

Overhead is applied on the basis of machine hours in Fabricating and direct labor hours in Assembly and in Finishing.

Job #13-198 had total prime cost of $6,700. The job took 40 machine hours in Fabricating, 100 direct labor hours in Assembly, and 20 direct labor hours in Finishing. What is the total cost of Job #13-198?

A) $6,700.00

B) $1,523.20

C) $8,223.20

D) $7,383.20

Overhead is applied on the basis of machine hours in Fabricating and direct labor hours in Assembly and in Finishing.

Job #13-198 had total prime cost of $6,700. The job took 40 machine hours in Fabricating, 100 direct labor hours in Assembly, and 20 direct labor hours in Finishing. What is the total cost of Job #13-198?

A) $6,700.00

B) $1,523.20

C) $8,223.20

D) $7,383.20

Question

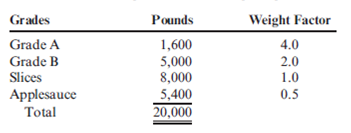

Allocating Joint Costs Using the Weighted Average Method

Refer to Cornerstone Exercise 7.7. Assume that Orchard Fresh, Inc., uses the weighted average method of joint cost allocation and has assigned the following weights to the four grades of apples:

Total joint cost is $18,000.

Required:

1. Allocate the joint cost to the four grades of apples using the weighted average method. (Carry out the percent calculations to four significant digits. Round all cost allocations to the nearest dollar.)

2. What if the factory found that Grade A apples were being valued less by customers and decided to decrease the weight factor for Grade A apples to 3.0? How would that affect the allocation of cost to Grade A apples? How would it affect the allocation of cost to the remaining grades?

Refer to Cornerstone Exercise 7.7. Assume that Orchard Fresh, Inc., uses the weighted average method of joint cost allocation and has assigned the following weights to the four grades of apples:

Total joint cost is $18,000.

Required:

1. Allocate the joint cost to the four grades of apples using the weighted average method. (Carry out the percent calculations to four significant digits. Round all cost allocations to the nearest dollar.)

2. What if the factory found that Grade A apples were being valued less by customers and decided to decrease the weight factor for Grade A apples to 3.0? How would that affect the allocation of cost to Grade A apples? How would it affect the allocation of cost to the remaining grades?

Question

Objectives of Allocation

Samantha and Rashida are planning a trip to Padre Island, Texas, during spring break. Members of the varsity volleyball team, they are looking forward to four days of beach volleyball and parasailing. They will drive Samantha's car and estimate that they will pay the following costs during the trip:

They have reservations at the SeaScape Motel, which charges $120 per night for a single, $145 per night for a double, and an additional $15 per night if a rollaway bed is added to a double room.

Samantha's little sister, Kallie, wants to go along. She isn't into sports but thinks that four days of partying and relaxing on the beach would be a great way to unwind from the rigors of school. She figures that she could ride with Samantha and Rashida and share their room.

Required:

1. Using incremental costs only, what would it cost Kallie to accompany Samantha and Rashida?

2. Using the benefits-received method, what would it cost Kallie to go on the trip?

Samantha and Rashida are planning a trip to Padre Island, Texas, during spring break. Members of the varsity volleyball team, they are looking forward to four days of beach volleyball and parasailing. They will drive Samantha's car and estimate that they will pay the following costs during the trip:

They have reservations at the SeaScape Motel, which charges $120 per night for a single, $145 per night for a double, and an additional $15 per night if a rollaway bed is added to a double room.

Samantha's little sister, Kallie, wants to go along. She isn't into sports but thinks that four days of partying and relaxing on the beach would be a great way to unwind from the rigors of school. She figures that she could ride with Samantha and Rashida and share their room.

Required:

1. Using incremental costs only, what would it cost Kallie to accompany Samantha and Rashida?

2. Using the benefits-received method, what would it cost Kallie to go on the trip?

Question

Question

Question

Single and Dual Charging Rates

Jeff McMillan owns a small neighborhood shopping mall. Of the 10 store spaces in the building, seven are rented by boutique owners and three are vacant. Jeff has decided that offering more services to stores in the mall would enable him to increase occupancy. He has decided to use one of the vacant spaces to provide, at cost, a gift-wrapping service to shops in the mall. The boutiques are enthusiastic about the new service. Most of them are staffed minimally, which means that every time they have to wrap a gift, phones go unanswered and other customers in line grow impatient. Jeff figured that the gift-wrapping service would incur the following costs: the store space would normally rent for $1,800 per month, part-time gift wrappers could be hired for $1,500 per month, and wrapping paper and ribbon would average $1.20 per gift. The boutique owners estimated the following number of gifts to be wrapped per month.

After the service had been in effect for six months, Jeff calculated the following actual average monthly number of gifts wrapped for each of the stores.

Required:

1. Calculate a single charging rate, on a per-gift basis, to be charged to the shops. Based on the shops' actual number of gifts wrapped, how much would be charged to each shop using the single charging rate?

2. Based on the shops' actual number of gifts wrapped, how much would be charged to each shop using the dual charging rate?

3. Which shops would prefer the single charging rate? Why? Which would prefer the dual charging rate, and why?

4. Several of the shop owners were angry about their bill for the gift-wrapping service. They pointed out that they were to be charged only for the cost of the service. How could you make a case for them?

Jeff McMillan owns a small neighborhood shopping mall. Of the 10 store spaces in the building, seven are rented by boutique owners and three are vacant. Jeff has decided that offering more services to stores in the mall would enable him to increase occupancy. He has decided to use one of the vacant spaces to provide, at cost, a gift-wrapping service to shops in the mall. The boutiques are enthusiastic about the new service. Most of them are staffed minimally, which means that every time they have to wrap a gift, phones go unanswered and other customers in line grow impatient. Jeff figured that the gift-wrapping service would incur the following costs: the store space would normally rent for $1,800 per month, part-time gift wrappers could be hired for $1,500 per month, and wrapping paper and ribbon would average $1.20 per gift. The boutique owners estimated the following number of gifts to be wrapped per month.

After the service had been in effect for six months, Jeff calculated the following actual average monthly number of gifts wrapped for each of the stores.

Required:

1. Calculate a single charging rate, on a per-gift basis, to be charged to the shops. Based on the shops' actual number of gifts wrapped, how much would be charged to each shop using the single charging rate?

2. Based on the shops' actual number of gifts wrapped, how much would be charged to each shop using the dual charging rate?

3. Which shops would prefer the single charging rate? Why? Which would prefer the dual charging rate, and why?

4. Several of the shop owners were angry about their bill for the gift-wrapping service. They pointed out that they were to be charged only for the cost of the service. How could you make a case for them?

Question

Question

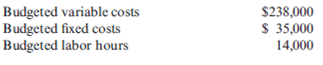

Calculating and Using a Single Charging Rate

The expected costs for the Maintenance Department of Stazler, Inc., for the coming year include:

Fixed costs (salaries, tools): $64,900 per year

Variable costs (supplies): $1.35 per maintenance hour

Estimated usage by:

Actual usage by:

Required:

1. Calculate a single charging rate for the Maintenance Department.

2. Use this rate to assign the costs of the Maintenance Department to the user departments based on actual usage. Calculate the total amount charged for maintenance for the year.

3. What if the Assembly Department used 4,000 maintenance hours in the year? How much would have been charged out to the three departments?

The expected costs for the Maintenance Department of Stazler, Inc., for the coming year include:

Fixed costs (salaries, tools): $64,900 per year

Variable costs (supplies): $1.35 per maintenance hour

Estimated usage by:

Actual usage by:

Required:

1. Calculate a single charging rate for the Maintenance Department.

2. Use this rate to assign the costs of the Maintenance Department to the user departments based on actual usage. Calculate the total amount charged for maintenance for the year.

3. What if the Assembly Department used 4,000 maintenance hours in the year? How much would have been charged out to the three departments?

Question

Allocating Joint Costs Using the Sales-Value-at-Split-Off Method

Refer to Cornerstone Exercise 7.7. Assume that Orchard Fresh, Inc., uses the sales-value-atsplit- off method of joint cost allocation and has provided the following information about the four grades of apples:

Total joint cost is $18,000.

Required:

1. Allocate the joint cost to the four grades of apples using the sales-value-at-split-off method. (Carry out the percent calculations to four significant digits. Round all cost allocations to the nearest dollar.)

2. What if the price at split-off of Grade B apples increased to $1.20 per pound? How would that affect the allocation of cost to Grade B apples? How would it affect the allocation of cost to the remaining grades?

Refer to Cornerstone Exercise 7.7. Assume that Orchard Fresh, Inc., uses the sales-value-atsplit- off method of joint cost allocation and has provided the following information about the four grades of apples:

Total joint cost is $18,000.

Required:

1. Allocate the joint cost to the four grades of apples using the sales-value-at-split-off method. (Carry out the percent calculations to four significant digits. Round all cost allocations to the nearest dollar.)

2. What if the price at split-off of Grade B apples increased to $1.20 per pound? How would that affect the allocation of cost to Grade B apples? How would it affect the allocation of cost to the remaining grades?

Question

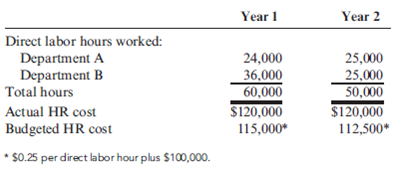

Actual versus Budgeted Costs

Kumar, Inc., evaluates managers of producing departments on their ability to control costs. In addition to the costs directly traceable to their departments, each production manager is held responsible for a share of the costs of a support center, the Human Resources (HR) Department. The total costs of HR are allocated on the basis of actual direct labor hours used. The total costs of HR and the actual direct labor hours worked by each producing department are as follows:

Required:

1. Allocate the HR costs to each producing department for Year 1 and Year 2 using the direct method with actual direct labor hours and actual HR costs.

2. Discuss the following statement: "The costs of human resource-related matters increased by 25 percent for Department A and decreased by over 16 percent for Department B. Thus, the manager of Department B must be controlling HR costs better than the manager of Department A."

3. Can you think of a way to allocate HR costs so that a more reasonable and fair assessment of cost control can be made? Explain.

Kumar, Inc., evaluates managers of producing departments on their ability to control costs. In addition to the costs directly traceable to their departments, each production manager is held responsible for a share of the costs of a support center, the Human Resources (HR) Department. The total costs of HR are allocated on the basis of actual direct labor hours used. The total costs of HR and the actual direct labor hours worked by each producing department are as follows:

Required:

1. Allocate the HR costs to each producing department for Year 1 and Year 2 using the direct method with actual direct labor hours and actual HR costs.

2. Discuss the following statement: "The costs of human resource-related matters increased by 25 percent for Department A and decreased by over 16 percent for Department B. Thus, the manager of Department B must be controlling HR costs better than the manager of Department A."

3. Can you think of a way to allocate HR costs so that a more reasonable and fair assessment of cost control can be made? Explain.

Question

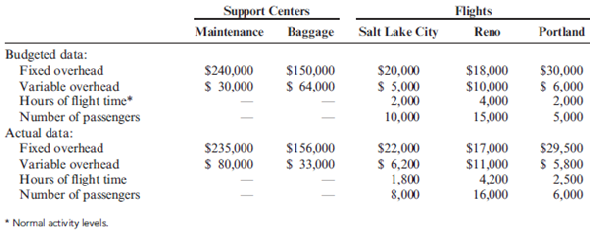

Direct Method, Variable versus Fixed Costing and Performance

AirBorne is a small airline operating out of Boise, Idaho. Its three flights travel to Salt Lake City, Reno, and Portland. The owner of the airline wants to assess the full cost of operating each flight. As part of this assessment, the costs of two support departments (maintenance and baggage) must be allocated to the three flights. The two support departments that support all three flights are located in Boise (any maintenance or baggage costs at the destination airports are directly traceable to the individual flights). Budgeted and actual data for the year are as follows for the support departments and the three flights:

Round all allocation ratios and variable rates to four significant digits. Round all allocated amounts to the nearest dollar.

Required:

1. Using the direct method, allocate the support service costs to each flight, assuming that the objective is to determine the cost of operating each flight.

2. Using the direct method, allocate the support service costs to each flight, assuming that the objective is to evaluate performance. Do any costs remain in the two support departments after the allocation? If so, how much? Explain.

AirBorne is a small airline operating out of Boise, Idaho. Its three flights travel to Salt Lake City, Reno, and Portland. The owner of the airline wants to assess the full cost of operating each flight. As part of this assessment, the costs of two support departments (maintenance and baggage) must be allocated to the three flights. The two support departments that support all three flights are located in Boise (any maintenance or baggage costs at the destination airports are directly traceable to the individual flights). Budgeted and actual data for the year are as follows for the support departments and the three flights:

Round all allocation ratios and variable rates to four significant digits. Round all allocated amounts to the nearest dollar.

Required:

1. Using the direct method, allocate the support service costs to each flight, assuming that the objective is to determine the cost of operating each flight.

2. Using the direct method, allocate the support service costs to each flight, assuming that the objective is to evaluate performance. Do any costs remain in the two support departments after the allocation? If so, how much? Explain.

Question

Question

Question

Question

Comparison of Methods of Allocation

Duweynie Pottery, Inc., is divided into two operating divisions: Pottery and Retail. The company allocates Power and General Factory department costs to each operating division. Power costs are allocated on the basis of the number of machine hours and general factory costs on the basis of square footage. No effort is made to separate fixed and variable costs; however, only budgeted costs are allocated. Allocations for the coming year are based on the following data:

Round all allocation ratios to four significant digits. Round all allocated amounts to the nearest dollar.

Required:

1. Allocate the support service costs using the direct method.

2. Allocate the support service costs using the sequential method. The support departments are ranked in order of highest cost to lowest cost.

3. Allocate the support service costs using the reciprocal method.

Duweynie Pottery, Inc., is divided into two operating divisions: Pottery and Retail. The company allocates Power and General Factory department costs to each operating division. Power costs are allocated on the basis of the number of machine hours and general factory costs on the basis of square footage. No effort is made to separate fixed and variable costs; however, only budgeted costs are allocated. Allocations for the coming year are based on the following data:

Round all allocation ratios to four significant digits. Round all allocated amounts to the nearest dollar.

Required:

1. Allocate the support service costs using the direct method.

2. Allocate the support service costs using the sequential method. The support departments are ranked in order of highest cost to lowest cost.

3. Allocate the support service costs using the reciprocal method.

Question

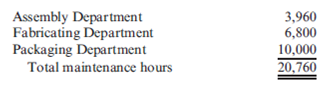

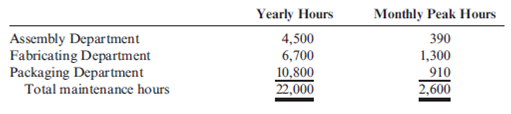

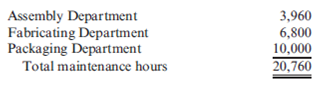

Calculating and Using Dual Charging Rates

The expected costs for the Maintenance Department of Stazler, Inc., for the coming year include:

Fixed costs (salaries, tools): $64,900 per year

Variable costs (supplies): $1.35 per maintenance hour

The Assembly and Packaging departments expect to use maintenance hours relatively evenly throughout the year. The Fabricating Department typically uses more maintenance hours in the month of November. Estimated usage in hours for the year and for the peak month is as follows:

Actual usage for the year by:

Required:

1. Calculate a variable rate for the Maintenance Department. Calculate the allocated fixed cost for each using department based on its budgeted peak month usage in maintenance hours.

2. Use the two rates to assign the costs of the Maintenance Department to the user departments based on actual usage. Calculate the total amount charged for maintenance for the year.

3. What if the Assembly Department used 4,000 maintenance hours in the year? How much would have been charged out to the three departments?

The expected costs for the Maintenance Department of Stazler, Inc., for the coming year include:

Fixed costs (salaries, tools): $64,900 per year

Variable costs (supplies): $1.35 per maintenance hour

The Assembly and Packaging departments expect to use maintenance hours relatively evenly throughout the year. The Fabricating Department typically uses more maintenance hours in the month of November. Estimated usage in hours for the year and for the peak month is as follows:

Actual usage for the year by:

Required:

1. Calculate a variable rate for the Maintenance Department. Calculate the allocated fixed cost for each using department based on its budgeted peak month usage in maintenance hours.

2. Use the two rates to assign the costs of the Maintenance Department to the user departments based on actual usage. Calculate the total amount charged for maintenance for the year.

3. What if the Assembly Department used 4,000 maintenance hours in the year? How much would have been charged out to the three departments?

Question

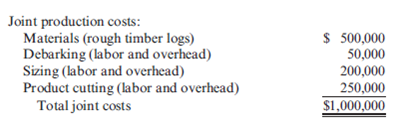

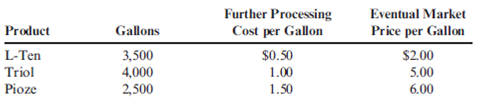

Allocating Joint Costs Using the Net Realizable Value Method

A company manufactures three products, L-Ten, Triol, and Pioze, from a joint process. Each production run costs $12,900. None of the products can be sold at split-off, but must be processed further. Information on one batch of the three products is as follows:

Required:

1. Allocate the joint cost to L-Ten, Triol, and Pioze using the net realizable value method. (Round the percentages to four significant digits. Round all cost allocations to the nearest dollar.)

2. What if it cost $2 to process each gallon of Triol beyond the split-off point? How would that affect the allocation of joint cost to the three products?

A company manufactures three products, L-Ten, Triol, and Pioze, from a joint process. Each production run costs $12,900. None of the products can be sold at split-off, but must be processed further. Information on one batch of the three products is as follows:

Required:

1. Allocate the joint cost to L-Ten, Triol, and Pioze using the net realizable value method. (Round the percentages to four significant digits. Round all cost allocations to the nearest dollar.)

2. What if it cost $2 to process each gallon of Triol beyond the split-off point? How would that affect the allocation of joint cost to the three products?

Question

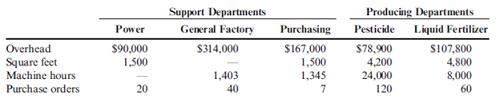

Direct Method and Overhead Rates

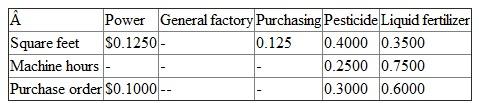

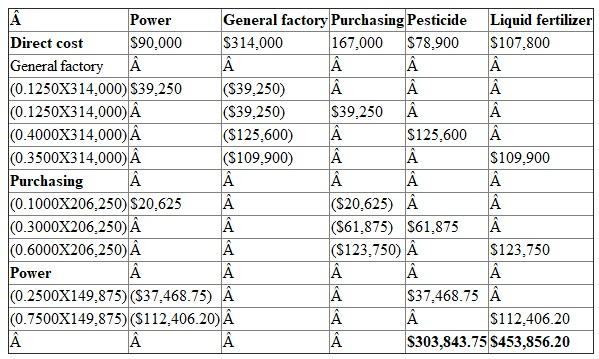

Jasmine Company manufactures both pesticide and liquid fertilizer, with each product manufactured in separate departments. Three support departments support the production departments: Power, General Factory, and Purchasing. Budgeted data on the five departments are as follows:

The company does not break overhead into fixed and variable components. The bases for allocation are power-machine hours; general factory-square feet; and purchasing-purchase orders.

Required:

1. Allocate the overhead costs to the producing departments using the direct method. (Take allocation ratios out to four significant digits.)

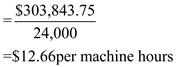

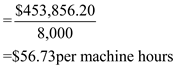

2. Using machine hours, compute departmental overhead rates. (Round the overhead rates to the nearest cent.)

Jasmine Company manufactures both pesticide and liquid fertilizer, with each product manufactured in separate departments. Three support departments support the production departments: Power, General Factory, and Purchasing. Budgeted data on the five departments are as follows:

The company does not break overhead into fixed and variable components. The bases for allocation are power-machine hours; general factory-square feet; and purchasing-purchase orders.

Required:

1. Allocate the overhead costs to the producing departments using the direct method. (Take allocation ratios out to four significant digits.)

2. Using machine hours, compute departmental overhead rates. (Round the overhead rates to the nearest cent.)

Question

Direct Method, Reciprocal Method, Overhead Rates

Macalister Corporation is developing departmental overhead rates based on direct labor hours for its two production departments-Molding and Assembly. The Molding Department employs 20 people, and the Assembly Department employs 80 people. Each person in these two departments works 2,000 hours per year. The production-related overhead costs for the Molding Department are budgeted at $190,000, and the Assembly Department costs are budgeted at $80,000. Two support departments-Engineering and General Factory-directly support the two production departments and have budgeted costs of $216,000 and $370,000, respectively. The production departments' overhead rates cannot be determined until the support departments' costs are properly allocated. The following schedule reflects the use of the Engineering Department's and General Factory Department's output by the various departments.

For all requirements, round allocation ratios to four significant digits and round allocated costs to the nearest dollar.

Required:

1. Calculate the overhead rates per direct labor hour for the Molding Department and the Assembly Department using the direct allocation method to charge the production departments for support department costs.

2. Calculate the overhead rates per direct labor hour for the Molding Department and the Assembly Department using the reciprocal method to charge support department costs to each other and to the production departments.

3. Explain the difference between the methods, and indicate the arguments generally presented to support the reciprocal method over the direct allocation method. (CMA adapted)

Macalister Corporation is developing departmental overhead rates based on direct labor hours for its two production departments-Molding and Assembly. The Molding Department employs 20 people, and the Assembly Department employs 80 people. Each person in these two departments works 2,000 hours per year. The production-related overhead costs for the Molding Department are budgeted at $190,000, and the Assembly Department costs are budgeted at $80,000. Two support departments-Engineering and General Factory-directly support the two production departments and have budgeted costs of $216,000 and $370,000, respectively. The production departments' overhead rates cannot be determined until the support departments' costs are properly allocated. The following schedule reflects the use of the Engineering Department's and General Factory Department's output by the various departments.

For all requirements, round allocation ratios to four significant digits and round allocated costs to the nearest dollar.

Required:

1. Calculate the overhead rates per direct labor hour for the Molding Department and the Assembly Department using the direct allocation method to charge the production departments for support department costs.

2. Calculate the overhead rates per direct labor hour for the Molding Department and the Assembly Department using the reciprocal method to charge support department costs to each other and to the production departments.

3. Explain the difference between the methods, and indicate the arguments generally presented to support the reciprocal method over the direct allocation method. (CMA adapted)

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/55

Play

Full screen (f)

Deck 7: Allocating Costs of Support Departments and Joint Products

1

Why must support service costs be assigned to products for purposes of inventory valuation?

Explanation:

The supporting departments are indirectly connected with the production departments as they give services to the production departments which help in smooth running of production and business like human resource department is very useful in factory which is used in production of items.

• And therefore the cost of the service departments are also to be allocated to the production departments to arrive at the actual product cost. The proper allocation of service cost is necessary to obtain the individual product cost.

• The valuation of goods is to be made in an appropriate manner so that it should reflect the correct information of cost of goods which also affects the profitability in the financial reports of the company.

• In GAAP the manufacturing unit's financial reports must show the actual picture of the company's affairs and therefore the cost of goods sold and the inventory has to be valued in a manner it will include the direct cost and the indirect cost incurred for the product.

• The indirect cost is the service cost which also has to be included in the cost of the individual product to arrive at the actual cost of the cost of inventory and cost of goods sold.

• As per Accounting standard 2, the cost of inventories should comprise of all cost of purchases, cost of conversion and all other costs which were incurred in bringing the inventories in present condition.

• Therefore, all the cost incurred in supporting department should also be added to the cost of production for valuation of inventory.

The supporting departments are indirectly connected with the production departments as they give services to the production departments which help in smooth running of production and business like human resource department is very useful in factory which is used in production of items.

• And therefore the cost of the service departments are also to be allocated to the production departments to arrive at the actual product cost. The proper allocation of service cost is necessary to obtain the individual product cost.

• The valuation of goods is to be made in an appropriate manner so that it should reflect the correct information of cost of goods which also affects the profitability in the financial reports of the company.

• In GAAP the manufacturing unit's financial reports must show the actual picture of the company's affairs and therefore the cost of goods sold and the inventory has to be valued in a manner it will include the direct cost and the indirect cost incurred for the product.

• The indirect cost is the service cost which also has to be included in the cost of the individual product to arrive at the actual cost of the cost of inventory and cost of goods sold.

• As per Accounting standard 2, the cost of inventories should comprise of all cost of purchases, cost of conversion and all other costs which were incurred in bringing the inventories in present condition.

• Therefore, all the cost incurred in supporting department should also be added to the cost of production for valuation of inventory.

2

Explain why variable bases should not be used to allocate fixed costs.

Explanation:

The fixed cost remains unchanged and it is known as capacity producing cost that is when the service department is established the size, scale of the department is usually determined keeping in mind the needs of the using department in the long run. Therefore for allocation of the fixed cost the estimate of long run usage of the each service department output by the each using departments is required.

• The fixed cost is allocated on the budgeted usage of the services by the production department because the fixed cost remains static and the use of variable basis will leads to variation in the allocation of cost by the change in the usage of service year by year which is not appropriate.

• The cost allocation will not be appropriate because fixed cost of the service department allocated to the production department does not changes year by year. Therefore, the fixed cost is allocated to the using department (Producing department) on the basis of the original needs of the support capacity that is the fixed cost is allocated on the basis of normal capacity usage of the using department which is estimated on the basis of long run usage of the services by the production departments.

• Therefore it will be appropriate if the fixed cost will be allocated on the basis of normal capacity of the producing departments.

The fixed cost remains unchanged and it is known as capacity producing cost that is when the service department is established the size, scale of the department is usually determined keeping in mind the needs of the using department in the long run. Therefore for allocation of the fixed cost the estimate of long run usage of the each service department output by the each using departments is required.

• The fixed cost is allocated on the budgeted usage of the services by the production department because the fixed cost remains static and the use of variable basis will leads to variation in the allocation of cost by the change in the usage of service year by year which is not appropriate.

• The cost allocation will not be appropriate because fixed cost of the service department allocated to the production department does not changes year by year. Therefore, the fixed cost is allocated to the using department (Producing department) on the basis of the original needs of the support capacity that is the fixed cost is allocated on the basis of normal capacity usage of the using department which is estimated on the basis of long run usage of the services by the production departments.

• Therefore it will be appropriate if the fixed cost will be allocated on the basis of normal capacity of the producing departments.

3

Sequential Method

Refer to the data in Exercise 7.20. The company has decided to use the sequential method of allocation instead of the direct method. The support departments are ranked in order of highest cost to lowest cost.

Required:

1. Allocate the overhead costs to the producing departments using the sequential method. (Take allocation ratios out to four significant digits.)

2. Using machine hours, compute departmental overhead rates. (Round the overhead rates to the nearest cent.)

Refer to the data in Exercise 7.20. The company has decided to use the sequential method of allocation instead of the direct method. The support departments are ranked in order of highest cost to lowest cost.

Required:

1. Allocate the overhead costs to the producing departments using the sequential method. (Take allocation ratios out to four significant digits.)

2. Using machine hours, compute departmental overhead rates. (Round the overhead rates to the nearest cent.)

Jasmine company manufactures both pesticide and liquid fertilizer. The detail information about the support department and producing department is given in the problem.

From the information the following calculations are made:

1.The allocation of the overhead costs to producing departments using the sequential method is as follows:

The allocation ratio is,

2.The department overhead rate is calculated as follows:

2.The department overhead rate is calculated as follows:

Pesticide:

Liquid fertilizer:

Liquid fertilizer:

From the information the following calculations are made:

1.The allocation of the overhead costs to producing departments using the sequential method is as follows:

The allocation ratio is,

2.The department overhead rate is calculated as follows:Pesticide:

Liquid fertilizer: 4

Physical Units Method, Relative Sales Value Method

Farleigh Petroleum, Inc., is a small company that acquires high-grade crude oil from low-volume production wells owned by individuals and small partnerships. The crude oil is processed in a single refinery into Two Oil, Six Oil, and impure distillates. Farleigh Petroleum does not have the technology or capacity to process these products further and sells most of its output each month to major refineries. There were no beginning finished goods or work-in-process inventories on April 1. The production costs and output of Farleigh Petroleum for April are as follows:

Data on barrels produced and selling price:

Two Oil, 300,000 barrels produced; sales price, $45 per barrel

Six Oil, 170,000 barrels produced; sales price, $25 per barrel

Distillates, 80,000 barrels produced; sales price, $14 per barrel

Required:

1. Calculate the amount of joint production cost that Farleigh Petroleum would allocate to each of the three joint products by using the physical units method. (Carry out the ratio calculation to four decimal places. Round allocated costs to the nearest dollar.)

2. Calculate the amount of joint production cost that Farleigh Petroleum would allocate to each of the three joint products by using the relative sales value method. (Carry out the ratio calculation to four decimal places. Round allocated costs to the nearest dollar.)

Farleigh Petroleum, Inc., is a small company that acquires high-grade crude oil from low-volume production wells owned by individuals and small partnerships. The crude oil is processed in a single refinery into Two Oil, Six Oil, and impure distillates. Farleigh Petroleum does not have the technology or capacity to process these products further and sells most of its output each month to major refineries. There were no beginning finished goods or work-in-process inventories on April 1. The production costs and output of Farleigh Petroleum for April are as follows:

Data on barrels produced and selling price:

Two Oil, 300,000 barrels produced; sales price, $45 per barrel

Six Oil, 170,000 barrels produced; sales price, $25 per barrel

Distillates, 80,000 barrels produced; sales price, $14 per barrel

Required:

1. Calculate the amount of joint production cost that Farleigh Petroleum would allocate to each of the three joint products by using the physical units method. (Carry out the ratio calculation to four decimal places. Round allocated costs to the nearest dollar.)

2. Calculate the amount of joint production cost that Farleigh Petroleum would allocate to each of the three joint products by using the relative sales value method. (Carry out the ratio calculation to four decimal places. Round allocated costs to the nearest dollar.)

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

5

Direct Method of Support Department Cost Allocation

Valron Company has two support departments, Human Resources and General Factory, and two producing departments, Fabricating and Assembly.

The costs of the Human Resources Department are allocated on the basis of number of employees, and the costs of General Factory are allocated on the basis of square footage. Valron Company uses the direct method of support department cost allocation.

Required:

1. Calculate the allocation ratios for the four departments using the direct method.

2. Using the direct method, allocate the costs of the Human Resources and General Factory departments to the Fabricating and Assembly departments.

3. What if the General Factory Department had 40 employees? How would that affect the allocation of Human Resources Department costs to the Fabricating and Assembly departments?

Valron Company has two support departments, Human Resources and General Factory, and two producing departments, Fabricating and Assembly.

The costs of the Human Resources Department are allocated on the basis of number of employees, and the costs of General Factory are allocated on the basis of square footage. Valron Company uses the direct method of support department cost allocation.

Required:

1. Calculate the allocation ratios for the four departments using the direct method.

2. Using the direct method, allocate the costs of the Human Resources and General Factory departments to the Fabricating and Assembly departments.

3. What if the General Factory Department had 40 employees? How would that affect the allocation of Human Resources Department costs to the Fabricating and Assembly departments?

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

6

Allocating Joint Costs Using the Constant Gross Margin Method

Refer to Cornerstone Exercise 7.10.

Required:

1. Calculate the total revenue, total costs, and total gross profit the company will earn on the sale of L-Ten, Triol, and Pioze.

2. Allocate the joint cost to L-Ten, Triol, and Pioze using the constant gross margin percentage method.

3. What if it cost $2 to process each gallon of Triol beyond the split-off point? How would that affect the allocation of joint cost to these three products?

Refer to Cornerstone Exercise 7.10.

Required:

1. Calculate the total revenue, total costs, and total gross profit the company will earn on the sale of L-Ten, Triol, and Pioze.

2. Allocate the joint cost to L-Ten, Triol, and Pioze using the constant gross margin percentage method.

3. What if it cost $2 to process each gallon of Triol beyond the split-off point? How would that affect the allocation of joint cost to these three products?

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

7

Reciprocal Method

Eilers Company has two producing departments and two support departments. The following budgeted data pertain to these four departments:

Required:

1. Allocate the overhead costs of the support departments to the producing departments using the reciprocal method. (Round allocation ratios to four significant digits. Round allocated costs to the nearest dollar.)

2. Using direct labor hours, compute departmental overhead rates. (Round to the nearest cent.)

Eilers Company has two producing departments and two support departments. The following budgeted data pertain to these four departments:

Required:

1. Allocate the overhead costs of the support departments to the producing departments using the reciprocal method. (Round allocation ratios to four significant digits. Round allocated costs to the nearest dollar.)

2. Using direct labor hours, compute departmental overhead rates. (Round to the nearest cent.)

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

8

Fixed and Variable Cost Allocation

Welcome Inns is a chain of motels serving business travelers in New Mexico and southwest Texas. The chain has grown from one motel in 2011 to five motels. In 2015, the owner of the company decided to set up an internal Accounting Department to centralize control of financial information. (Previously, local CPAs handled each motel's bookkeeping and financial reporting.) The accounting office was opened in January 2015 by renting space adjacent to corporate headquarters in Ruidoso, New Mexico. All motels have been supplied with personal computers and internet access to transfer information to central accounting on a daily basis.

The Accounting Department has budgeted fixed costs of $135,000 per year. Variable costs are budgeted at $20 per hour. In 2015, actual cost for the Accounting Department was $223,000. Further information is as follows:

Required:

1. Suppose the total actual costs of the Accounting Department are allocated on the basis of 2015 sales revenue. How much will be allocated to each motel?

2. Suppose that Welcome Inns views 2014 sales figures as a proxy for budgeted capacity of the motels. Thus, fixed Accounting Department costs are allocated on the basis of 2014 sales, and variable costs are allocated according to 2015 usage multiplied by the variable rate. How much Accounting Department cost will be allocated to each motel?

3. Comment on the two allocation schemes. Which motels would prefer the method in Requirement 1? The method in Requirement 2? Explain.

Welcome Inns is a chain of motels serving business travelers in New Mexico and southwest Texas. The chain has grown from one motel in 2011 to five motels. In 2015, the owner of the company decided to set up an internal Accounting Department to centralize control of financial information. (Previously, local CPAs handled each motel's bookkeeping and financial reporting.) The accounting office was opened in January 2015 by renting space adjacent to corporate headquarters in Ruidoso, New Mexico. All motels have been supplied with personal computers and internet access to transfer information to central accounting on a daily basis.

The Accounting Department has budgeted fixed costs of $135,000 per year. Variable costs are budgeted at $20 per hour. In 2015, actual cost for the Accounting Department was $223,000. Further information is as follows:

Required:

1. Suppose the total actual costs of the Accounting Department are allocated on the basis of 2015 sales revenue. How much will be allocated to each motel?

2. Suppose that Welcome Inns views 2014 sales figures as a proxy for budgeted capacity of the motels. Thus, fixed Accounting Department costs are allocated on the basis of 2014 sales, and variable costs are allocated according to 2015 usage multiplied by the variable rate. How much Accounting Department cost will be allocated to each motel?

3. Comment on the two allocation schemes. Which motels would prefer the method in Requirement 1? The method in Requirement 2? Explain.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

9

Explain how allocation of support service costs is useful for planning and control and in making pricing decisions.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

10

Why is the dual-rate charging method better than the single-rate method? In what circumstances would it not matter whether dual or single rates were used?

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

11

Direct Method

Refer to the data in Exercise 7.22. The company has decided to simplify its method of allocating support service costs by switching to the direct method.

Required:

1. Allocate the costs of the support departments to the producing departments using the direct method. (Round allocation ratios to four significant digits. Round allocated costs to the nearest dollar.)

2. Using direct labor hours, compute departmental overhead rates. (Round to the nearest cent.)

Refer to the data in Exercise 7.22. The company has decided to simplify its method of allocating support service costs by switching to the direct method.

Required:

1. Allocate the costs of the support departments to the producing departments using the direct method. (Round allocation ratios to four significant digits. Round allocated costs to the nearest dollar.)

2. Using direct labor hours, compute departmental overhead rates. (Round to the nearest cent.)

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

12

Physical Units Method, Relative Sales-Value-at-Split-off Method, Net Realizable Value Method, Decision Making

Sonimad Sawmill, Inc. (SSI), purchases logs from independent timber contractors and processes them into the following three types of lumber products:

1. Studs for residential construction (e.g., walls and ceilings)

2. Decorative pieces (e.g., fireplace mantels and beams for cathedral ceilings)

3. Posts used as support braces (e.g., mine support braces and braces for exterior fences around ranch properties)

These products are the result of a joint sawmill process that involves removing bark from the logs, cutting the logs into a workable size (ranging from 8 to 16 feet in length), and then cutting the individual products from the logs, depending upon the type of wood (pine, oak, walnut, or maple) and the size (diameter) of the log.

The joint process results in the following costs and output of products during a typical month:

Product yield and average sales value on a per-unit basis from the joint process are as follows:

The studs are sold as rough-cut lumber after emerging from the sawmill operation without further processing by SSI. Also, the posts require no further processing. The decorative pieces must be planed and further sized after emerging from the SSI sawmill. This additional processing costs SSI $100,000 per month and normally results in a loss of 10 percent of the units entering the process. Without this planing and sizing process, there is still an active intermediate market for the unfinished decorative pieces where the sales price averages $60 per unit.

Required:

1. Based on the information given for Sonimad Sawmill, Inc., allocate the joint processing costs of $1,000,000 to each of the three product lines using the:

a. Relative sales-value-at-split-off method

b. Physical units method at split-off

c. Estimated net realizable value method

2. Prepare an analysis for Sonimad Sawmill, Inc., to compare processing the decorative pieces further as it presently does, with selling the rough-cut product immediately at split-off. Be sure to provide all calculations.

3. Assume Sonimad Sawmill, Inc., announced that in six months it will sell the rough-cut product at split-off due to increasing competitive pressure. Identify at least three types of likely behavior that will be demonstrated by the skilled labor in the planing and sizing process as a result of this announcement. Explain how this behavior could be improved by management. (CMA adapted)

Sonimad Sawmill, Inc. (SSI), purchases logs from independent timber contractors and processes them into the following three types of lumber products:

1. Studs for residential construction (e.g., walls and ceilings)

2. Decorative pieces (e.g., fireplace mantels and beams for cathedral ceilings)

3. Posts used as support braces (e.g., mine support braces and braces for exterior fences around ranch properties)

These products are the result of a joint sawmill process that involves removing bark from the logs, cutting the logs into a workable size (ranging from 8 to 16 feet in length), and then cutting the individual products from the logs, depending upon the type of wood (pine, oak, walnut, or maple) and the size (diameter) of the log.

The joint process results in the following costs and output of products during a typical month:

Product yield and average sales value on a per-unit basis from the joint process are as follows:

The studs are sold as rough-cut lumber after emerging from the sawmill operation without further processing by SSI. Also, the posts require no further processing. The decorative pieces must be planed and further sized after emerging from the SSI sawmill. This additional processing costs SSI $100,000 per month and normally results in a loss of 10 percent of the units entering the process. Without this planing and sizing process, there is still an active intermediate market for the unfinished decorative pieces where the sales price averages $60 per unit.

Required:

1. Based on the information given for Sonimad Sawmill, Inc., allocate the joint processing costs of $1,000,000 to each of the three product lines using the:

a. Relative sales-value-at-split-off method

b. Physical units method at split-off

c. Estimated net realizable value method

2. Prepare an analysis for Sonimad Sawmill, Inc., to compare processing the decorative pieces further as it presently does, with selling the rough-cut product immediately at split-off. Be sure to provide all calculations.

3. Assume Sonimad Sawmill, Inc., announced that in six months it will sell the rough-cut product at split-off due to increasing competitive pressure. Identify at least three types of likely behavior that will be demonstrated by the skilled labor in the planing and sizing process as a result of this announcement. Explain how this behavior could be improved by management. (CMA adapted)

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

13

Sequential (Step) Method of Support Department Cost Allocation

Refer to Cornerstone Exercise 7.3. Now assume that Valron Company uses the sequential method to allocate support department costs. The support departments are ranked in order of highest cost to lowest cost.

Required:

1. Calculate the allocation ratios (rounded to four significant digits) for the four departments using the sequential method.

2. Using the sequential method, allocate the costs of the Human Resources and General Factory departments to the Fabricating and Assembly departments. (Round all allocated costs to the nearest dollar.)

3. What if the allocation ratios in Requirement 1 were rounded to six significant digits rather than four? How would that affect any rounding error in the allocation of costs?

Refer to Cornerstone Exercise 7.3. Now assume that Valron Company uses the sequential method to allocate support department costs. The support departments are ranked in order of highest cost to lowest cost.

Required:

1. Calculate the allocation ratios (rounded to four significant digits) for the four departments using the sequential method.

2. Using the sequential method, allocate the costs of the Human Resources and General Factory departments to the Fabricating and Assembly departments. (Round all allocated costs to the nearest dollar.)

3. What if the allocation ratios in Requirement 1 were rounded to six significant digits rather than four? How would that affect any rounding error in the allocation of costs?

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

14

Explain the difference between the direct method and the sequential method.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

15

Sequential Method

Refer to the data in Exercise 7.22. The support departments are ranked in order of highest cost to lowest cost.

Required:

1. Allocate the costs of the support departments using the sequential method. (Round allocation ratios to four significant digits. Round allocated costs to the nearest dollar.)

2. Using direct labor hours, compute departmental overhead rates. (Round to the nearest cent.)

Refer to the data in Exercise 7.22. The support departments are ranked in order of highest cost to lowest cost.

Required:

1. Allocate the costs of the support departments using the sequential method. (Round allocation ratios to four significant digits. Round allocated costs to the nearest dollar.)

2. Using direct labor hours, compute departmental overhead rates. (Round to the nearest cent.)

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

16

Single Charging Rates

House Corporation Board (HCB) of Tri-Gamma Sorority is responsible for the operation of a two-story sorority house on the State University campus. HCB has set a normal capacity of 60 women. At any given point in time, there are 100 members of the chapter: 60 living in the house and 40 living elsewhere (e.g., in the freshman dorms on campus). HCB needs to set rates for the use of the house for the coming year. The following costs are budgeted: $240,000 fixed and $34,800 variable. The fixed costs are fairly insensitive to the number of women living in the house. Food is budgeted at $40,000 and is included in the fixed costs; food does not seem to vary greatly given the stated capacity. The variable expenses consist of telephone bills and some of the utilities. HCB is not responsible for chapter dues, party fees, pledging and initiation fees, and other social expenditures. Women living in the house eat 20 meals per week there and live in a two-person room. (All in-house members' rooms, bathroom facilities, etc., are on the second floor.) All members eat Monday dinner at the house and have full use of house facilities (e.g., the two TV lounges, kitchens, access to milk and cereal at any time, study facilities, and so on).

HCB has traditionally set two rates: one for in-house members and one for out-of-house members. There are 32 weeks in a school year.

Required:

1. Discuss the factors that might go into determining the charging rate for the two types of sorority members.

2. Set charging rates for the in-house and out-of-house members.

House Corporation Board (HCB) of Tri-Gamma Sorority is responsible for the operation of a two-story sorority house on the State University campus. HCB has set a normal capacity of 60 women. At any given point in time, there are 100 members of the chapter: 60 living in the house and 40 living elsewhere (e.g., in the freshman dorms on campus). HCB needs to set rates for the use of the house for the coming year. The following costs are budgeted: $240,000 fixed and $34,800 variable. The fixed costs are fairly insensitive to the number of women living in the house. Food is budgeted at $40,000 and is included in the fixed costs; food does not seem to vary greatly given the stated capacity. The variable expenses consist of telephone bills and some of the utilities. HCB is not responsible for chapter dues, party fees, pledging and initiation fees, and other social expenditures. Women living in the house eat 20 meals per week there and live in a two-person room. (All in-house members' rooms, bathroom facilities, etc., are on the second floor.) All members eat Monday dinner at the house and have full use of house facilities (e.g., the two TV lounges, kitchens, access to milk and cereal at any time, study facilities, and so on).

HCB has traditionally set two rates: one for in-house members and one for out-of-house members. There are 32 weeks in a school year.

Required:

1. Discuss the factors that might go into determining the charging rate for the two types of sorority members.

2. Set charging rates for the in-house and out-of-house members.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

17

Assume that a company has decided not to allocate any support service costs to producing departments. Describe the likely behavior of the managers of the producing departments. Would this be good or bad? Explain why allocation would correct this type of behavior.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

18

Classifying Departments as Producing or Support-Manufacturing Firm

Classify each of the following departments in a factory that produces creme-filled snack cakes as a producing department or a support department.

a. Janitorial

b. Baking snack cakes)

c. Inspection

d. Mixing

e. Engineering

f. Grounds

g. Purchasing

h. Packaging

i. Icing (frosts top of snack cakes and adds decorative squiggle)

j. Filling (injects creme mixture into baked

k. Personnel

l. Cafeteria

m. General factory

n. Machine maintenance

o. Bookkeeping

Classify each of the following departments in a factory that produces creme-filled snack cakes as a producing department or a support department.

a. Janitorial

b. Baking snack cakes)

c. Inspection

d. Mixing

e. Engineering

f. Grounds

g. Purchasing

h. Packaging

i. Icing (frosts top of snack cakes and adds decorative squiggle)

j. Filling (injects creme mixture into baked

k. Personnel

l. Cafeteria

m. General factory

n. Machine maintenance

o. Bookkeeping

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

19

Physical Units Method

Alomar Company manufactures four products from a joint production process: barlon, selene, plicene, and corsol. The joint costs for one batch are as follows:

At the split-off point, a batch yields 1,400 barlon, 2,600 selene, 2,500 plicene, and 3,500 corsol. All products are sold at the split-off point: barlon sells for $15 per unit, selene sells for $20 per unit, plicene sells for $26 per unit, and corsol sells for $35 per unit.

Carry out all percent calculations to four significant digits.

Required:

1. Allocate the joint costs using the physical units method.

2. Suppose that the products are weighted as shown on page 368.

Allocate the joint costs using the weighted average method.

Alomar Company manufactures four products from a joint production process: barlon, selene, plicene, and corsol. The joint costs for one batch are as follows:

At the split-off point, a batch yields 1,400 barlon, 2,600 selene, 2,500 plicene, and 3,500 corsol. All products are sold at the split-off point: barlon sells for $15 per unit, selene sells for $20 per unit, plicene sells for $26 per unit, and corsol sells for $35 per unit.

Carry out all percent calculations to four significant digits.

Required:

1. Allocate the joint costs using the physical units method.

2. Suppose that the products are weighted as shown on page 368.

Allocate the joint costs using the weighted average method.

Unlock Deck