Deck 6: Process Costing

Full screen (f)

Question

Question

Question

Question

Cost Information and FIFO

Gunnison Company had the following equivalent units schedule and cost information for its Sewing Department for the month of December:

Required:

1. Calculate the unit cost for December, using the FIFO method.

2. Calculate the cost of goods transferred out, calculate the cost of EWIP, and reconcile the costs assigned with the costs to account for.

3. What if you were asked for the unit cost from the month of November? Calculate November's unit cost and explain why this might be of interest to management.

Gunnison Company had the following equivalent units schedule and cost information for its Sewing Department for the month of December:

Required:

1. Calculate the unit cost for December, using the FIFO method.

2. Calculate the cost of goods transferred out, calculate the cost of EWIP, and reconcile the costs assigned with the costs to account for.

3. What if you were asked for the unit cost from the month of November? Calculate November's unit cost and explain why this might be of interest to management.

Question

FIFO Method, Valuation of Goods Transferred Out and Ending Work in Process

K-Briggs Company uses the FIFO method to account for the costs of production. For Crushing, the first processing department, the following equivalent units schedule has been prepared:

The cost per equivalent unit for the period was as follows:

The cost of beginning work in process was direct materials, $40,000; conversion costs, $30,000.

Required:

1. Determine the cost of ending work in process and the cost of goods transferred out.

2. Prepare a physical flow schedule.

K-Briggs Company uses the FIFO method to account for the costs of production. For Crushing, the first processing department, the following equivalent units schedule has been prepared:

The cost per equivalent unit for the period was as follows:

The cost of beginning work in process was direct materials, $40,000; conversion costs, $30,000.

Required:

1. Determine the cost of ending work in process and the cost of goods transferred out.

2. Prepare a physical flow schedule.

Question

Weighted Average Method, Single Department Analysis, Uniform Costs

Hatch Company produces a product that passes through three processes: Fabrication, Assembly, and Finishing. All manufacturing costs are added uniformly for all processes. The following information was obtained for the Fabrication Department for December:

a. Work in process, June 1, had 90,000 units (40 percent completed) and the following costs:

b. During the month of June, 180,000 units were completed and transferred to the Assembly Department, and the following costs were added to production:

c. On June 30, there were 45,000 partially completed units in process. These units were 80 percent complete.

Required:

Prepare a cost of production report for the Fabrication Department for June using the weighted average method of costing. The report should disclose the physical flow of units, equivalent units, and unit costs and should track the disposition of manufacturing costs.

Hatch Company produces a product that passes through three processes: Fabrication, Assembly, and Finishing. All manufacturing costs are added uniformly for all processes. The following information was obtained for the Fabrication Department for December:

a. Work in process, June 1, had 90,000 units (40 percent completed) and the following costs:

b. During the month of June, 180,000 units were completed and transferred to the Assembly Department, and the following costs were added to production:

c. On June 30, there were 45,000 partially completed units in process. These units were 80 percent complete.

Required:

Prepare a cost of production report for the Fabrication Department for June using the weighted average method of costing. The report should disclose the physical flow of units, equivalent units, and unit costs and should track the disposition of manufacturing costs.

Question

Question

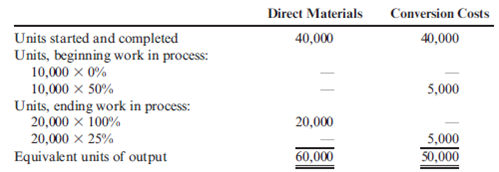

Equivalent Units: Weighted Average Method

The following data are for four independent process-costing departments. Inputs are added continuously.

Required:

Compute the equivalent units of production for each of the preceding departments using the weighted average method.

The following data are for four independent process-costing departments. Inputs are added continuously.

Required:

Compute the equivalent units of production for each of the preceding departments using the weighted average method.

Question

Question

Cost Flows

Lamont Company produced 80,000 machine parts for diesel engines. There were no beginning or ending work-in-process inventories in any department. Lamont incurred the following costs for May:

Required:

1. Calculate the costs transferred out of each department.

2. Prepare the journal entries corresponding to these transfers. Also, prepare the journal entry for Grinding that reflects the costs added to the transferred-in goods received from Molding.

3. What if the Grinding Department had an ending WIP of $12,000? Calculate the cost transferred out and provide the journal entry that would reflect this transfer. What is the effect on finished goods calculated in Requirement 1, assuming the other two departments have no ending WIP?

Lamont Company produced 80,000 machine parts for diesel engines. There were no beginning or ending work-in-process inventories in any department. Lamont incurred the following costs for May:

Required:

1. Calculate the costs transferred out of each department.

2. Prepare the journal entries corresponding to these transfers. Also, prepare the journal entry for Grinding that reflects the costs added to the transferred-in goods received from Molding.

3. What if the Grinding Department had an ending WIP of $12,000? Calculate the cost transferred out and provide the journal entry that would reflect this transfer. What is the effect on finished goods calculated in Requirement 1, assuming the other two departments have no ending WIP?

Question

Unit Information with BWIP, Weighted Average Method

Jackson Products produces a barbeque sauce using three departments: Cooking, Mixing, and Bottling. In the Cooking Department, all materials are added at the beginning of the process. Output is measured in ounces. The production data for July are as follows:

Required:

1. Prepare a physical flow schedule for July.

2. Prepare an equivalent units schedule for July using the weighted average method.

3. What if you were asked to calculate the FIFO units beginning with the weighted average equivalent units? Calculate the weighted average equivalent units by subtracting out the prior-period output found in BWIP.

Jackson Products produces a barbeque sauce using three departments: Cooking, Mixing, and Bottling. In the Cooking Department, all materials are added at the beginning of the process. Output is measured in ounces. The production data for July are as follows:

Required:

1. Prepare a physical flow schedule for July.

2. Prepare an equivalent units schedule for July using the weighted average method.

3. What if you were asked to calculate the FIFO units beginning with the weighted average equivalent units? Calculate the weighted average equivalent units by subtracting out the prior-period output found in BWIP.

Question

Question

Service Organization with Work-in-Process Inventories, Multiple Departments, FIFO Method, Unit Cost

Hepworth Credit Corporation is a wholly owned subsidiary of a large manufacturer of computers. Hepworth is in the business of financing computers, software, and other services that the parent corporation sells. Hepworth has two departments that are involved in financing services: the Credit Department and the Business Practices Department. The Credit Department receives requests for financing from field sales representatives, records customer information on a preprinted form, and then enters the information into the computer system to check the creditworthiness of the customer. (Other actions may be taken if the customer is not in the database.) Once creditworthiness information is known, a printout is produced with this information plus other customer-specific information. The completed form is transferred to the Business Practices Department.

The Business Practices Department modifies the standard loan covenant as needed (in response to customer request or customer risk profile). When this activity is completed, the loan is priced. This is done by keying information from the partially processed form into a personal computer spreadsheet program. The program provides a recommended interest rate for the loan. Finally, a form specifying the loan terms is attached to the transferred-in document. A copy of the loan-term form is sent to the sales representative and serves as the quote letter.

The following cost and service activity data for the Business Practices Department are provided for the month of May:

Required:

1. How would you define the output of the Business Practices Department?

2. Using the FIFO method, prepare the following for the Business Practices Department:

a. A physical flow schedule

b. An equivalent units schedule

Transferred-in applications

c. Calculation of unit costs

d. Cost of ending work in process and cost of units transferred out

e. A cost reconciliation

Hepworth Credit Corporation is a wholly owned subsidiary of a large manufacturer of computers. Hepworth is in the business of financing computers, software, and other services that the parent corporation sells. Hepworth has two departments that are involved in financing services: the Credit Department and the Business Practices Department. The Credit Department receives requests for financing from field sales representatives, records customer information on a preprinted form, and then enters the information into the computer system to check the creditworthiness of the customer. (Other actions may be taken if the customer is not in the database.) Once creditworthiness information is known, a printout is produced with this information plus other customer-specific information. The completed form is transferred to the Business Practices Department.

The Business Practices Department modifies the standard loan covenant as needed (in response to customer request or customer risk profile). When this activity is completed, the loan is priced. This is done by keying information from the partially processed form into a personal computer spreadsheet program. The program provides a recommended interest rate for the loan. Finally, a form specifying the loan terms is attached to the transferred-in document. A copy of the loan-term form is sent to the sales representative and serves as the quote letter.

The following cost and service activity data for the Business Practices Department are provided for the month of May:

Required:

1. How would you define the output of the Business Practices Department?

2. Using the FIFO method, prepare the following for the Business Practices Department:

a. A physical flow schedule

b. An equivalent units schedule

Transferred-in applications

c. Calculation of unit costs

d. Cost of ending work in process and cost of units transferred out

e. A cost reconciliation

Question

Question

Question

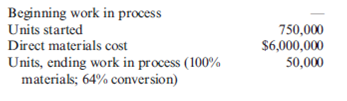

Weighted Average Method, Unit Cost, Valuation of Goods Transferred Out and Ending Work in Process

Holmes Products, Inc., produces plastic cases used for video cameras. The product passes through three departments. For April, the following equivalent units schedule was prepared for the first department:

Costs assigned to beginning work in process: direct materials, $90,000; conversion costs, $33,750. Manufacturing costs incurred during April: direct materials, $75,000; conversion costs, $220,000. Holmes uses the weighted average method.

Required:

1. Compute the unit cost for April.

2. Determine the cost of ending work in process and the cost of goods transferred out.

Holmes Products, Inc., produces plastic cases used for video cameras. The product passes through three departments. For April, the following equivalent units schedule was prepared for the first department:

Costs assigned to beginning work in process: direct materials, $90,000; conversion costs, $33,750. Manufacturing costs incurred during April: direct materials, $75,000; conversion costs, $220,000. Holmes uses the weighted average method.

Required:

1. Compute the unit cost for April.

2. Determine the cost of ending work in process and the cost of goods transferred out.

Question

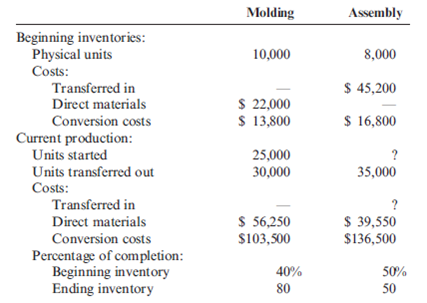

Weighted Average Method, Journal Entries

Muskoge Company uses a process-costing system. The company manufactures a product that is processed in two departments: Molding and Assembly. In the Molding Department, direct materials are added at the beginning of the process; in the Assembly Department, additional direct materials are added at the end of the process. In both departments, conversion costs are incurred uniformly throughout the process. As work is completed, it is transferred out. The following table summarizes the production activity and costs for February:

Required:

1. Using the weighted average method, prepare the following for the Molding Department:

a. A physical flow schedule

b. An equivalent units calculation

c. Calculation of unit costs. Round to four decimal places.

d. Cost of ending work in process and cost of goods transferred out

e. A cost reconciliation

2. Prepare journal entries that show the flow of manufacturing costs for the Molding Department. Materials are added at the beginning of the process.

3. Repeat Requirements 1 and 2 for the Assembly Department.

Muskoge Company uses a process-costing system. The company manufactures a product that is processed in two departments: Molding and Assembly. In the Molding Department, direct materials are added at the beginning of the process; in the Assembly Department, additional direct materials are added at the end of the process. In both departments, conversion costs are incurred uniformly throughout the process. As work is completed, it is transferred out. The following table summarizes the production activity and costs for February:

Required:

1. Using the weighted average method, prepare the following for the Molding Department:

a. A physical flow schedule

b. An equivalent units calculation

c. Calculation of unit costs. Round to four decimal places.

d. Cost of ending work in process and cost of goods transferred out

e. A cost reconciliation

2. Prepare journal entries that show the flow of manufacturing costs for the Molding Department. Materials are added at the beginning of the process.

3. Repeat Requirements 1 and 2 for the Assembly Department.

Question

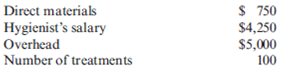

Unit Cost, No Work-in-Process Inventories

Lising Therapy has a physical therapist who performs electro-mechanical treatments for its patients. During April, Lising had the following cost and output information:

Required:

1. Calculate the cost per treatment for April.

2. Calculate the cost of services sold for April.

3. What if Lising found a way to reduce overhead costs by 20 percent? How would this affect the profit per treatment?

Lising Therapy has a physical therapist who performs electro-mechanical treatments for its patients. During April, Lising had the following cost and output information:

Required:

1. Calculate the cost per treatment for April.

2. Calculate the cost of services sold for April.

3. What if Lising found a way to reduce overhead costs by 20 percent? How would this affect the profit per treatment?

Question

Question

FIFO Method, Unit Cost, Valuation of Goods Transferred Out and Ending Work in Process

Dama Company produces women's blouses and uses the FIFO method to account for its manufacturing costs. The product Dama makes passes through two processes: Cutting and Sewing. During April, Dama's controller prepared the following equivalent units schedule for the Cutting Department:

Costs in beginning work in process were direct materials, $20,000; conversion costs, $80,000. Manufacturing costs incurred during April were direct materials, $240,000; conversion costs, $320,000.

Required:

1. Prepare a physical flow schedule for April.

2. Compute the cost per equivalent unit for April.

3. Determine the cost of ending work in process and the cost of goods transferred out.

4. Prepare the journal entry that transfers the costs from Cutting to Sewing.

Dama Company produces women's blouses and uses the FIFO method to account for its manufacturing costs. The product Dama makes passes through two processes: Cutting and Sewing. During April, Dama's controller prepared the following equivalent units schedule for the Cutting Department:

Costs in beginning work in process were direct materials, $20,000; conversion costs, $80,000. Manufacturing costs incurred during April were direct materials, $240,000; conversion costs, $320,000.

Required:

1. Prepare a physical flow schedule for April.

2. Compute the cost per equivalent unit for April.

3. Determine the cost of ending work in process and the cost of goods transferred out.

4. Prepare the journal entry that transfers the costs from Cutting to Sewing.

Question

Question

Question

Question

Weighted Average Method, Equivalent Units, Unit Cost, Multiple Departments

Fordman Company has a product that passes through two processes: Grinding and Polishing. During December, the Grinding Department transferred 20,000 units to the Polishing Department. The cost of the units transferred into the second department was $40,000. Direct materials are added uniformly in the second process. Units are measured the same way in both departments.

The second department (Polishing) had the following physical flow schedule for December:

Costs in beginning work in process for the Polishing Department were direct materials, $5,000; conversion costs, $6,000; and transferred in, $8,000. Costs added during the month: direct materials, $32,000; conversion costs, $50,000; and transferred in, $40,000.

Required:

1. Assuming the use of the weighted average method, prepare a schedule of equivalent units.

2. Compute the unit cost for the month.

Fordman Company has a product that passes through two processes: Grinding and Polishing. During December, the Grinding Department transferred 20,000 units to the Polishing Department. The cost of the units transferred into the second department was $40,000. Direct materials are added uniformly in the second process. Units are measured the same way in both departments.

The second department (Polishing) had the following physical flow schedule for December:

Costs in beginning work in process for the Polishing Department were direct materials, $5,000; conversion costs, $6,000; and transferred in, $8,000. Costs added during the month: direct materials, $32,000; conversion costs, $50,000; and transferred in, $40,000.

Required:

1. Assuming the use of the weighted average method, prepare a schedule of equivalent units.

2. Compute the unit cost for the month.

Question

Weighted Average Method, Two-Department Analysis, Change in Output Measure

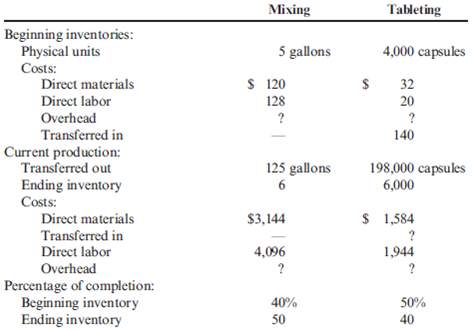

Healthway uses a process-costing system to compute the unit costs of the minerals that it produces. It has three departments: Mixing, Tableting, and Bottling. In Mixing, at the beginning of the process all materials are added and the ingredients for the minerals are measured, sifted, and blended together. The mix is transferred out in gallon containers. The Tableting Department takes the powdered mix and places it in capsules. One gallon of powdered mix converts to 1,600 capsules. After the capsules are filled and polished, they are transferred to Bottling where they are placed in bottles, which are then affixed with a safety seal and a lid and labeled. Each bottle receives 50 capsules.

During July, the following results are available for the first two departments (direct materials are added at the beginning in both departments):

Overhead in both departments is applied as a percentage of direct labor costs. In the Mixing Department, overhead is 200 percent of direct labor. In the Tableting Department, the overhead rate is 150 percent of direct labor.

Required:

1. Prepare a production report for the Mixing Department using the weighted average method. Follow the five steps outlined in the chapter. Round unit cost to three decimal places.

2. Prepare a production report for the Tableting Department. Materials are added at the beginning of the process. Follow the five steps outlined in the chapter. Round unit cost to four decimal places.

Healthway uses a process-costing system to compute the unit costs of the minerals that it produces. It has three departments: Mixing, Tableting, and Bottling. In Mixing, at the beginning of the process all materials are added and the ingredients for the minerals are measured, sifted, and blended together. The mix is transferred out in gallon containers. The Tableting Department takes the powdered mix and places it in capsules. One gallon of powdered mix converts to 1,600 capsules. After the capsules are filled and polished, they are transferred to Bottling where they are placed in bottles, which are then affixed with a safety seal and a lid and labeled. Each bottle receives 50 capsules.

During July, the following results are available for the first two departments (direct materials are added at the beginning in both departments):

Overhead in both departments is applied as a percentage of direct labor costs. In the Mixing Department, overhead is 200 percent of direct labor. In the Tableting Department, the overhead rate is 150 percent of direct labor.

Required:

1. Prepare a production report for the Mixing Department using the weighted average method. Follow the five steps outlined in the chapter. Round unit cost to three decimal places.

2. Prepare a production report for the Tableting Department. Materials are added at the beginning of the process. Follow the five steps outlined in the chapter. Round unit cost to four decimal places.

Question

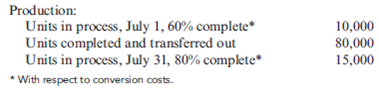

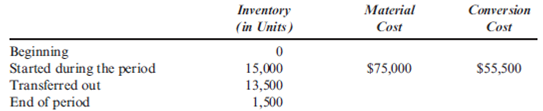

Physical Flow and Equivalent Units with EWIP

Fleming, Fleming, and Johnson, a local CPA firm, provided the following data for individual returns processed for March (output is measured in number of returns):

Required:

1. Prepare a physical flow schedule

2. Prepare an equivalent units schedule. Explain why output is measured in equivalent units.

3. What if EWIP is 80 percent complete? How would this change affect the physical flow schedule? The equivalent units schedule?

Fleming, Fleming, and Johnson, a local CPA firm, provided the following data for individual returns processed for March (output is measured in number of returns):

Required:

1. Prepare a physical flow schedule

2. Prepare an equivalent units schedule. Explain why output is measured in equivalent units.

3. What if EWIP is 80 percent complete? How would this change affect the physical flow schedule? The equivalent units schedule?

Question

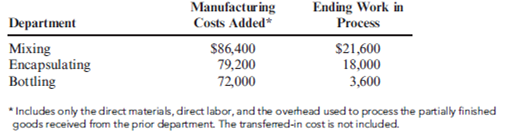

Journal Entries

Shorts Company has three process departments: Mixing, Encapsulating, and Bottling. At the beginning of the year, there were no work-in-process or finished goods inventories. The following data are available for the month of July:

Required:

1. Prepare journal entries that show the transfer of costs from one department to the next (including the entry to transfer the costs of the final department).

2. Prepare T-accounts for the entries made in Requirement 1. Use arrows to show the flow of costs.

Shorts Company has three process departments: Mixing, Encapsulating, and Bottling. At the beginning of the year, there were no work-in-process or finished goods inventories. The following data are available for the month of July:

Required:

1. Prepare journal entries that show the transfer of costs from one department to the next (including the entry to transfer the costs of the final department).

2. Prepare T-accounts for the entries made in Requirement 1. Use arrows to show the flow of costs.

Question

Question

Question

Question

Question

Question

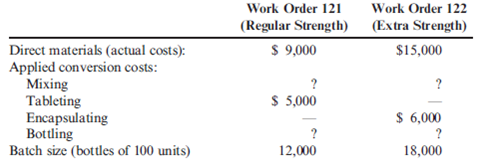

Operation Costing: Unit Costs and Journal Entries

Jacson Company produces two brands of a popular pain medication: regular strength and extra strength. Regular strength is produced in tablet form, and extra strength is produced in capsule form. All direct materials needed for each batch are requisitioned at the start. The work orders for two batches of the products are shown below, along with some associated cost information:

In the Mixing Department, conversion costs are applied on the basis of direct labor hours. Budgeted conversion costs for the department for the year were $60,000 for direct labor and $190,000 for overhead. Budgeted direct labor hours were 5,000. It takes one minute of labor time to mix the ingredients needed for a 100-unit bottle (for either product).

In the Bottling Department, conversion costs are applied on the basis of machine hours. Budgeted conversion costs for the department for the year were $400,000. Budgeted machine hours were 20,000. It takes one-half minute of machine time to fill a bottle of 100 units.

Required:

1. What are the conversion costs applied in the Mixing Department for each batch? The Bottling Department?

2. Calculate the cost per bottle for the regular and extra strength pain medications.

3. Prepare the journal entries that record the costs of the 12,000 regular strength batch as it moves through the various operations.

4. Suppose that the direct materials are requisitioned by each department as needed for a batch. For the 12,000 regular strength batch, direct materials are requisitioned for the Mixing and Bottling departments. Assume that the amount of cost is split evenly between the two departments. How will this change the journal entries made in Requirement 3?

Jacson Company produces two brands of a popular pain medication: regular strength and extra strength. Regular strength is produced in tablet form, and extra strength is produced in capsule form. All direct materials needed for each batch are requisitioned at the start. The work orders for two batches of the products are shown below, along with some associated cost information:

In the Mixing Department, conversion costs are applied on the basis of direct labor hours. Budgeted conversion costs for the department for the year were $60,000 for direct labor and $190,000 for overhead. Budgeted direct labor hours were 5,000. It takes one minute of labor time to mix the ingredients needed for a 100-unit bottle (for either product).

In the Bottling Department, conversion costs are applied on the basis of machine hours. Budgeted conversion costs for the department for the year were $400,000. Budgeted machine hours were 20,000. It takes one-half minute of machine time to fill a bottle of 100 units.

Required:

1. What are the conversion costs applied in the Mixing Department for each batch? The Bottling Department?

2. Calculate the cost per bottle for the regular and extra strength pain medications.

3. Prepare the journal entries that record the costs of the 12,000 regular strength batch as it moves through the various operations.

4. Suppose that the direct materials are requisitioned by each department as needed for a batch. For the 12,000 regular strength batch, direct materials are requisitioned for the Mixing and Bottling departments. Assume that the amount of cost is split evenly between the two departments. How will this change the journal entries made in Requirement 3?

Question

Cost Information

During October, McCourt Associates incurred total production costs of $60,000 for copyediting manuscripts and had the following equivalent units schedule:

Required:

1. Calculate the cost of copyediting one manuscript for October.

2. Assign costs to manuscripts completed and to EWIP and then do a cost reconciliation.

3. What if the costs assigned to units completed and EWIP total were calculated using a unit cost of $225? What is the discrepancy between the costs assigned and the costs to account for? What could have caused an incorrect unit cost?

During October, McCourt Associates incurred total production costs of $60,000 for copyediting manuscripts and had the following equivalent units schedule:

Required:

1. Calculate the cost of copyediting one manuscript for October.

2. Assign costs to manuscripts completed and to EWIP and then do a cost reconciliation.

3. What if the costs assigned to units completed and EWIP total were calculated using a unit cost of $225? What is the discrepancy between the costs assigned and the costs to account for? What could have caused an incorrect unit cost?

Question

Process Costing, Service Organization

A local barbershop cuts the hair of 1,200 customers per month. The clients are men, and the barbers offer no special styling. During the month of May, 1,200 customers were serviced. The cost of haircuts includes the following:

Required:

1. Explain why process costing is appropriate for this haircutting operation.

2. Calculate the cost per haircut.

3. Can you identify some possible direct materials used for this haircutting service? Is the usage of direct materials typical of services? If so, provide examples of services that use direct materials. Can you think of some services that would not use direct materials?

A local barbershop cuts the hair of 1,200 customers per month. The clients are men, and the barbers offer no special styling. During the month of May, 1,200 customers were serviced. The cost of haircuts includes the following:

Required:

1. Explain why process costing is appropriate for this haircutting operation.

2. Calculate the cost per haircut.

3. Can you identify some possible direct materials used for this haircutting service? Is the usage of direct materials typical of services? If so, provide examples of services that use direct materials. Can you think of some services that would not use direct materials?

Question

Question

Case on Process Costing, Operation Costing, Impact on Resource Allocation Decision

Golding Manufacturing, a division of Farnsworth Sporting, Inc., produces two different models of bows and eight models of knives. The bow-manufacturing process involves the production of two major subassemblies: the limbs and the handle. The limbs pass through four sequential processes before reaching final assembly: lay-up, molding, fabricating, and finishing. In the LayUp Department, limbs are created by laminating layers of wood. In Molding, the limbs are heat treated, under pressure, to form a strong resilient limb. In the Fabricating Department, any pro-truding glue or other processing residue is removed. Finally, in Finishing, the limbs are cleaned with acetone, dried, and sprayed with the final finishes.

The handles pass through two processes before reaching final assembly: pattern and finishing. In the Pattern Department, blocks of wood are fed into a machine that is set to shape the handles. Different patterns are possible, depending on the machine's setting. After coming out of the machine, the handles are cleaned and smoothed. They then pass to the Finishing Department where they are sprayed with the final finishes. In Final Assembly, the limbs and handles are assembled into different models using purchased parts such as pulley assemblies, weight adjustment bolts, side plates, and string.

Golding, since its inception, has been using process costing to assign product costs. A predetermined overhead rate is used based on direct labor dollars (80 percent of direct labor dollars). Recently, Golding has hired a new controller, Karen Jenkins. After reviewing the product costing procedures, Karen requested a meeting with the divisional manager, Aaron Suhr. The following is a transcript of their conversation:

KAREN : Aaron, I have some concerns about our cost accounting system. We make two different models of bows and are treating them as if they were the same product. Now I know that the only real difference between the models is the handle. The processing of the handles is the same, but the handles differ significantly in the amount and quality of wood used. Our current costing does not reflect this difference in direct material input.

AARON : Your predecessor is responsible. He believed that tracking the difference in direct material cost wasn't worth the effort. He simply didn't believe that it would make much difference in the unit cost of either model.

KAREN : Well, he may have been right, but I have my doubts. If there is a significant difference, it could affect our views of which model is more important to the company. The additional bookkeeping isn't very stringent. All we have to worry about is the Pattern Department. The other departments fit what I view as a process-costing pattern.

AARON: Why don't you look into it? If there is a significant difference, go ahead and adjust the costing system.

After the meeting, Karen decided to collect cost data on the two models: the Deluxe model and the Econo model. She decided to track the costs for one week. At the end of the week, she had collected the following data from the Pattern Department:

a. There were a total of 2,500 bows completed: 1,000 Deluxe models and 1,500 Econo models.

b. There was no beginning work in process; however, there were 300 units in ending work in process: 200 Deluxe and 100 Econo models. Both models were 80 percent complete with respect to conversion costs and 100 percent complete with respect to direct materials.

c. The Pattern Department experienced the following costs:

d. On an experimental basis, the requisition forms for direct materials were modified to identify the dollar value of the direct materials used by the Econo and Deluxe models:

Required:

1. Compute the unit cost for the handles produced by the Pattern Department, assuming that process costing is totally appropriate.

2. Compute the unit cost of each handle, using the separate cost information provided on materials.

3. Compare the unit costs computed in Requirements 1 and 2. Is Karen justified in her belief that a pure process-costing relationship is not appropriate? Describe the costing system that you would recommend.

4. In the past, the marketing manager has requested more money for advertising the Econo line. Aaron has repeatedly refused to grant any increase in this product's advertising budget because its per-unit profit (selling price less manufacturing cost) is so low. Given the results in Requirements 1 through 3, was Aaron justified in his position?

Golding Manufacturing, a division of Farnsworth Sporting, Inc., produces two different models of bows and eight models of knives. The bow-manufacturing process involves the production of two major subassemblies: the limbs and the handle. The limbs pass through four sequential processes before reaching final assembly: lay-up, molding, fabricating, and finishing. In the LayUp Department, limbs are created by laminating layers of wood. In Molding, the limbs are heat treated, under pressure, to form a strong resilient limb. In the Fabricating Department, any pro-truding glue or other processing residue is removed. Finally, in Finishing, the limbs are cleaned with acetone, dried, and sprayed with the final finishes.

The handles pass through two processes before reaching final assembly: pattern and finishing. In the Pattern Department, blocks of wood are fed into a machine that is set to shape the handles. Different patterns are possible, depending on the machine's setting. After coming out of the machine, the handles are cleaned and smoothed. They then pass to the Finishing Department where they are sprayed with the final finishes. In Final Assembly, the limbs and handles are assembled into different models using purchased parts such as pulley assemblies, weight adjustment bolts, side plates, and string.

Golding, since its inception, has been using process costing to assign product costs. A predetermined overhead rate is used based on direct labor dollars (80 percent of direct labor dollars). Recently, Golding has hired a new controller, Karen Jenkins. After reviewing the product costing procedures, Karen requested a meeting with the divisional manager, Aaron Suhr. The following is a transcript of their conversation:

KAREN : Aaron, I have some concerns about our cost accounting system. We make two different models of bows and are treating them as if they were the same product. Now I know that the only real difference between the models is the handle. The processing of the handles is the same, but the handles differ significantly in the amount and quality of wood used. Our current costing does not reflect this difference in direct material input.

AARON : Your predecessor is responsible. He believed that tracking the difference in direct material cost wasn't worth the effort. He simply didn't believe that it would make much difference in the unit cost of either model.

KAREN : Well, he may have been right, but I have my doubts. If there is a significant difference, it could affect our views of which model is more important to the company. The additional bookkeeping isn't very stringent. All we have to worry about is the Pattern Department. The other departments fit what I view as a process-costing pattern.

AARON: Why don't you look into it? If there is a significant difference, go ahead and adjust the costing system.

After the meeting, Karen decided to collect cost data on the two models: the Deluxe model and the Econo model. She decided to track the costs for one week. At the end of the week, she had collected the following data from the Pattern Department:

a. There were a total of 2,500 bows completed: 1,000 Deluxe models and 1,500 Econo models.

b. There was no beginning work in process; however, there were 300 units in ending work in process: 200 Deluxe and 100 Econo models. Both models were 80 percent complete with respect to conversion costs and 100 percent complete with respect to direct materials.

c. The Pattern Department experienced the following costs:

d. On an experimental basis, the requisition forms for direct materials were modified to identify the dollar value of the direct materials used by the Econo and Deluxe models:

Required:

1. Compute the unit cost for the handles produced by the Pattern Department, assuming that process costing is totally appropriate.

2. Compute the unit cost of each handle, using the separate cost information provided on materials.

3. Compare the unit costs computed in Requirements 1 and 2. Is Karen justified in her belief that a pure process-costing relationship is not appropriate? Describe the costing system that you would recommend.

4. In the past, the marketing manager has requested more money for advertising the Econo line. Aaron has repeatedly refused to grant any increase in this product's advertising budget because its per-unit profit (selling price less manufacturing cost) is so low. Given the results in Requirements 1 through 3, was Aaron justified in his position?

Question

Question

Question

Question

Appendix: Normal and Abnormal Spoilage

Larkin Company produces leather strips for western belts using three processes: cutting, design and coloring, and punching. The weighted average method is used for all three departments. The following information pertains to the Design and Coloring Department for the month of June:

a. There was no beginning work in process.

b. There were 400,000 units transferred in from the Cutting Department.

c. Ending work in process, June 30: 50,000 strips, 80 percent complete with respect to conversion costs.

d. Units completed and transferred out: 330,000 strips. The following costs were added during the month:

e. Direct materials are added at the beginning of the process.

f. Inspection takes place at the end of the process. All spoilage is considered normal.

Required:

1. Calculate equivalent units of production for transferred-in materials, direct materials added, and conversion costs.

2. Calculate unit costs for the three categories of Requirement 1.

3. What is the total cost of units transferred out? What is the cost of ending work-in-process inventory? How is the cost of spoilage treated?

4. Assume that all spoilage is considered abnormal. Now, how is spoilage treated? Give the journal entry to account for the cost of the spoiled units. Some companies view all spoilage as abnormal. Explain why.

5. Assume that 80 percent of the units spoiled are abnormal and 20 percent are normal spoilage. Show the spoilage treatment for this scenario.

Larkin Company produces leather strips for western belts using three processes: cutting, design and coloring, and punching. The weighted average method is used for all three departments. The following information pertains to the Design and Coloring Department for the month of June:

a. There was no beginning work in process.

b. There were 400,000 units transferred in from the Cutting Department.

c. Ending work in process, June 30: 50,000 strips, 80 percent complete with respect to conversion costs.

d. Units completed and transferred out: 330,000 strips. The following costs were added during the month:

e. Direct materials are added at the beginning of the process.

f. Inspection takes place at the end of the process. All spoilage is considered normal.

Required:

1. Calculate equivalent units of production for transferred-in materials, direct materials added, and conversion costs.

2. Calculate unit costs for the three categories of Requirement 1.

3. What is the total cost of units transferred out? What is the cost of ending work-in-process inventory? How is the cost of spoilage treated?

4. Assume that all spoilage is considered abnormal. Now, how is spoilage treated? Give the journal entry to account for the cost of the spoiled units. Some companies view all spoilage as abnormal. Explain why.

5. Assume that 80 percent of the units spoiled are abnormal and 20 percent are normal spoilage. Show the spoilage treatment for this scenario.

Question

Production Report

Tomar Company produces vitamin energy drinks. The Mixing Department, the first process department, mixes the ingredients required for the drinks. The following data are for April:

Direct materials are added throughout the process. Ending inventory is 60 percent complete with respect to direct labor and overhead.

Required:

1. Why would a manager want a production report?

2. Prepare a production report for the Mixing Department for April.

Tomar Company produces vitamin energy drinks. The Mixing Department, the first process department, mixes the ingredients required for the drinks. The following data are for April:

Direct materials are added throughout the process. Ending inventory is 60 percent complete with respect to direct labor and overhead.

Required:

1. Why would a manager want a production report?

2. Prepare a production report for the Mixing Department for April.

Question

JIT Manufacturing and Process Costing

Friedman Company uses JIT manufacturing. There are several manufacturing cells set up within one of its factories. One of the cells makes stands for flat-screen televisions. The cost of production for the month of April is given below.

During May, 30,000 stands were produced and sold.

Required:

1. Explain why process costing can be used for computing the cost of production for the stands.

2. Calculate the cost per unit for a stand.

3. Explain how activity-based costing can be used to determine the overhead assigned to the cell.

Friedman Company uses JIT manufacturing. There are several manufacturing cells set up within one of its factories. One of the cells makes stands for flat-screen televisions. The cost of production for the month of April is given below.

During May, 30,000 stands were produced and sold.

Required:

1. Explain why process costing can be used for computing the cost of production for the stands.

2. Calculate the cost per unit for a stand.

3. Explain how activity-based costing can be used to determine the overhead assigned to the cell.

Question

Question

Question

Question

Question

Question

Question

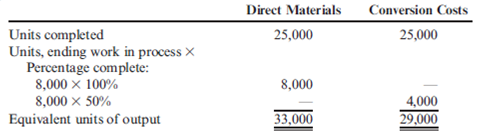

Nonuniform Inputs

Apeto Company produces premium chocolate candy bars. Conversion costs are added uniformly. For February, EWIP is 40 percent complete with respect to conversion costs. The following information is provided for February:

Required:

1. Calculate the equivalent units for each input category.

2. Calculate the unit cost for each category and in total.

3. What if a different type of materials is also added at the end of the process (a candy wrapper), costing $4,800? Calculate the new unit cost.

Apeto Company produces premium chocolate candy bars. Conversion costs are added uniformly. For February, EWIP is 40 percent complete with respect to conversion costs. The following information is provided for February:

Required:

1. Calculate the equivalent units for each input category.

2. Calculate the unit cost for each category and in total.

3. What if a different type of materials is also added at the end of the process (a candy wrapper), costing $4,800? Calculate the new unit cost.

Question

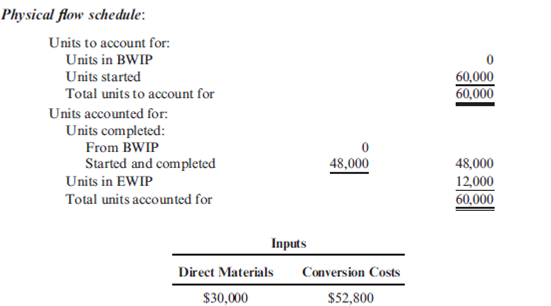

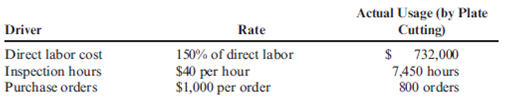

Physical Flow, Equivalent Units, Unit Costs, No Beginning WIP Inventory, Activity-Based Costing

Lacy, Inc., produces a subassembly used in the production of hydraulic cylinders. The subassemblies are produced in three departments: Plate Cutting, Rod Cutting, and Welding. Overhead is applied using the following drivers and activity rates:

Other data for the Plate Cutting Department are as follows:

Required:

1. Prepare a physical flow schedule.

2. Calculate equivalent units of production for:

a. Direct materials

b. Conversion costs

3. Calculate unit costs for:

a. Direct materials

b. Conversion costs

c. Total manufacturing

4. Provide the following information:

a. The total cost of units transferred out

b. The journal entry for transferring costs from Plate Cutting to Welding

c. The cost assigned to units in ending inventory

Lacy, Inc., produces a subassembly used in the production of hydraulic cylinders. The subassemblies are produced in three departments: Plate Cutting, Rod Cutting, and Welding. Overhead is applied using the following drivers and activity rates:

Other data for the Plate Cutting Department are as follows:

Required:

1. Prepare a physical flow schedule.

2. Calculate equivalent units of production for:

a. Direct materials

b. Conversion costs

3. Calculate unit costs for:

a. Direct materials

b. Conversion costs

c. Total manufacturing

4. Provide the following information:

a. The total cost of units transferred out

b. The journal entry for transferring costs from Plate Cutting to Welding

c. The cost assigned to units in ending inventory

Question

Question

Question

Question

(CPA 2011 Exam, adapted) A company uses process costing to assign product costs. Available inventory information for a period is as follows:

The ending inventory was 25% complete as to the conversion cost. 100% of direct material was added at the beginning of the process. What was the total cost transferred out?

A) $130,500

B) $126,973

C) $121,500

D) $117,450

The ending inventory was 25% complete as to the conversion cost. 100% of direct material was added at the beginning of the process. What was the total cost transferred out?

A) $130,500

B) $126,973

C) $121,500

D) $117,450

Question

Unit Information with BWIP, FIFO Method

Jackson Products produces a barbeque sauce using three departments: Cooking, Mixing, and Bottling. In the Cooking Department, all materials are added at the beginning of the process. Output is measured in ounces. The production data for July are as follows:

Required:

1. Prepare a physical flow schedule for July.

2. Prepare an equivalent units schedule for July using the FIFO method.

3. What if 60 percent of the materials were added at the beginning of the process and 40 percent were added at the end of the process (all ingredients used are treated as the same type or category of materials)? How many equivalent units of materials would there be?

Jackson Products produces a barbeque sauce using three departments: Cooking, Mixing, and Bottling. In the Cooking Department, all materials are added at the beginning of the process. Output is measured in ounces. The production data for July are as follows:

Required:

1. Prepare a physical flow schedule for July.

2. Prepare an equivalent units schedule for July using the FIFO method.

3. What if 60 percent of the materials were added at the beginning of the process and 40 percent were added at the end of the process (all ingredients used are treated as the same type or category of materials)? How many equivalent units of materials would there be?

Question

Production Report, No Beginning Inventory

Softkin Company manufactures sun protection lotion. The Mixing Department, the first process department, mixes the chemicals required for the repellant. The following data are for 2014:

Direct materials are added at the beginning of the process. Ending inventory is 95 percent complete with respect to direct labor and overhead.

Required:

Prepare a production report for the Mixing Department for 2014.

Softkin Company manufactures sun protection lotion. The Mixing Department, the first process department, mixes the chemicals required for the repellant. The following data are for 2014:

Direct materials are added at the beginning of the process. Ending inventory is 95 percent complete with respect to direct labor and overhead.

Required:

Prepare a production report for the Mixing Department for 2014.

Question

Weighted Average Method, Physical Flow, Equivalent Units, Unit Costs, Cost Assignment, ABC

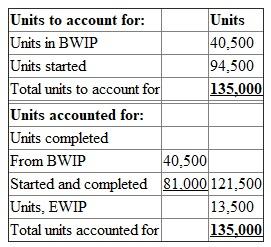

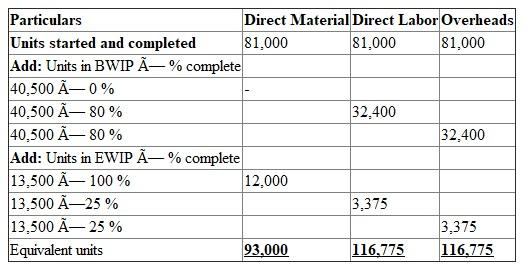

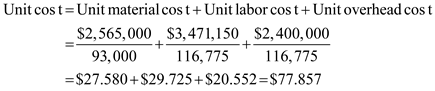

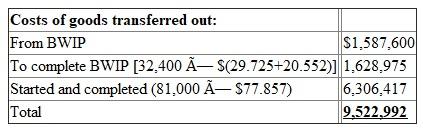

Swasey Fabrication, Inc., manufactures frames for bicycles. Each frame passes through three processes: Cutting, Welding, and Painting. In September, the Cutting Department of the Tulsa, Oklahoma, plant reported the following data:

a. In Cutting, all direct materials are added at the beginning of the process.

b. Beginning work in process consisted of 40,500 units, 20 percent complete with respect to direct labor and overhead. Costs in beginning inventory included direct materials, $1,215,000; direct labor, $222,600; and applied overhead, $150,000.

c. Costs added to production during the month were direct materials, $2,565,000; direct labor, $3,471,150. Overhead was assigned using the following information:

d. At the end of the month, 121,500 units were transferred out to Welding, leaving 13,500 units in ending work in process, or 25 percent complete.

Required:

1. Prepare a physical flow schedule.

2. Calculate equivalent units of production for direct materials and conversion costs.

3. Compute unit cost under weighted average.

4. Calculate the cost of goods transferred to Welding at the end of the month. Calculate the cost of ending inventory.

5. Prepare the journal entry that transfers the goods from Cutting to Welding.

Swasey Fabrication, Inc., manufactures frames for bicycles. Each frame passes through three processes: Cutting, Welding, and Painting. In September, the Cutting Department of the Tulsa, Oklahoma, plant reported the following data:

a. In Cutting, all direct materials are added at the beginning of the process.

b. Beginning work in process consisted of 40,500 units, 20 percent complete with respect to direct labor and overhead. Costs in beginning inventory included direct materials, $1,215,000; direct labor, $222,600; and applied overhead, $150,000.

c. Costs added to production during the month were direct materials, $2,565,000; direct labor, $3,471,150. Overhead was assigned using the following information:

d. At the end of the month, 121,500 units were transferred out to Welding, leaving 13,500 units in ending work in process, or 25 percent complete.

Required:

1. Prepare a physical flow schedule.

2. Calculate equivalent units of production for direct materials and conversion costs.

3. Compute unit cost under weighted average.

4. Calculate the cost of goods transferred to Welding at the end of the month. Calculate the cost of ending inventory.

5. Prepare the journal entry that transfers the goods from Cutting to Welding.

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/58

Play

Full screen (f)

Deck 6: Process Costing

1

Can process costing be used for a service organization? Explain. Describe how process costing can be used for JIT manufacturing firms.

not answer

2

Weighted Average Method, FIFO Method, Physical Flow, Equivalent Units

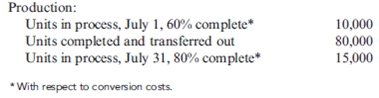

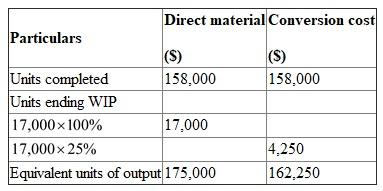

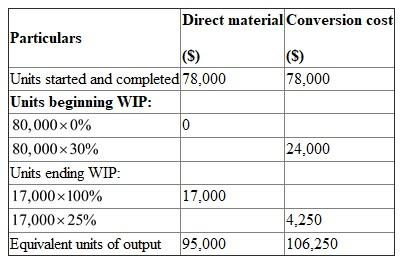

Heap Company manufactures a product that passes through two processes: Fabrication and Assembly.

The following information was obtained for the Fabrication Department for September:

a. All materials are added at the beginning of the process.

b. Beginning work in process had 80,000 units, 30 percent complete with respect to conversion costs.

c. Ending work in process had 17,000 units, 25 percent complete with respect to conversion costs.

d. Started in process, 95,000 units.

Required:

1. Prepare a physical flow schedule.

2. Compute equivalent units using the weighted average method.

3. Compute equivalent units using the FIFO method.

Heap Company manufactures a product that passes through two processes: Fabrication and Assembly.

The following information was obtained for the Fabrication Department for September:

a. All materials are added at the beginning of the process.

b. Beginning work in process had 80,000 units, 30 percent complete with respect to conversion costs.

c. Ending work in process had 17,000 units, 25 percent complete with respect to conversion costs.

d. Started in process, 95,000 units.

Required:

1. Prepare a physical flow schedule.

2. Compute equivalent units using the weighted average method.

3. Compute equivalent units using the FIFO method.

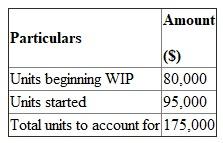

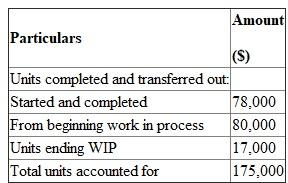

Heap Company manufactures product which passes through two processes. Based on the information available the following calculations are made.

1.Physical flow schedule:

Units to account for:-

Units accounted for

Units accounted for

2.Equivalent units using weighted average method:

2.Equivalent units using weighted average method:

3.Equivalent units using the FIFO method:

3.Equivalent units using the FIFO method:

1.Physical flow schedule:

Units to account for:-

Units accounted for 2.Equivalent units using weighted average method: 3.Equivalent units using the FIFO method: 3

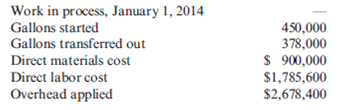

FIFO Method, Physical Flow, Equivalent Units, Unit Costs, Cost Assignment

Refer to the data in Problem 6.31. Assume that the FIFO method is used.

Required:

1. Prepare a physical flow schedule.

2. Calculate equivalent units of production for direct materials and conversion costs.

3. Compute unit cost. Round to three decimal places.

4. Calculate the cost of goods transferred to Painting at the end of the month. Calculate the cost of ending inventory.

Refer to the data in Problem 6.31. Assume that the FIFO method is used.

Required:

1. Prepare a physical flow schedule.

2. Calculate equivalent units of production for direct materials and conversion costs.

3. Compute unit cost. Round to three decimal places.

4. Calculate the cost of goods transferred to Painting at the end of the month. Calculate the cost of ending inventory.

Equivalent units:

Equivalent unit's also known as equivalent production. It is a measure for understanding percentage of completion from partially completed units. It is useful to know the equivalent number of whole units manufactured in a particular period for direct labour, direct materials, and overhead.

1.Prepare a Physical flow schedule:

2.Calculate Equivalent units:

2.Calculate Equivalent units:

3.Calculate Unit cost:

3.Calculate Unit cost:

4.Calculate cost of goods transferred:

4.Calculate cost of goods transferred:

Calculate cost of ending inventory:

Calculate cost of ending inventory:

Equivalent unit's also known as equivalent production. It is a measure for understanding percentage of completion from partially completed units. It is useful to know the equivalent number of whole units manufactured in a particular period for direct labour, direct materials, and overhead.

1.Prepare a Physical flow schedule:

2.Calculate Equivalent units: 3.Calculate Unit cost: 4.Calculate cost of goods transferred: Calculate cost of ending inventory: 4

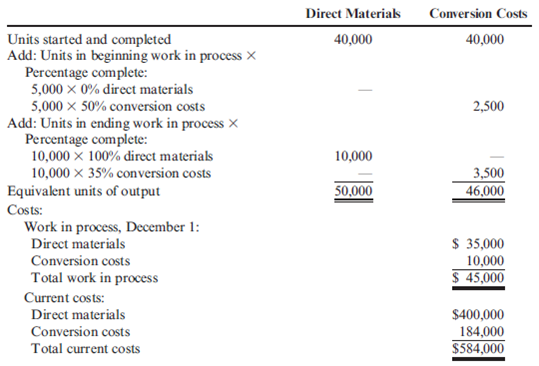

Cost Information and FIFO

Gunnison Company had the following equivalent units schedule and cost information for its Sewing Department for the month of December:

Required:

1. Calculate the unit cost for December, using the FIFO method.

2. Calculate the cost of goods transferred out, calculate the cost of EWIP, and reconcile the costs assigned with the costs to account for.

3. What if you were asked for the unit cost from the month of November? Calculate November's unit cost and explain why this might be of interest to management.

Gunnison Company had the following equivalent units schedule and cost information for its Sewing Department for the month of December:

Required:

1. Calculate the unit cost for December, using the FIFO method.

2. Calculate the cost of goods transferred out, calculate the cost of EWIP, and reconcile the costs assigned with the costs to account for.

3. What if you were asked for the unit cost from the month of November? Calculate November's unit cost and explain why this might be of interest to management.

Unlock Deck

Unlock for access to all 58 flashcards in this deck.

Unlock Deck

k this deck

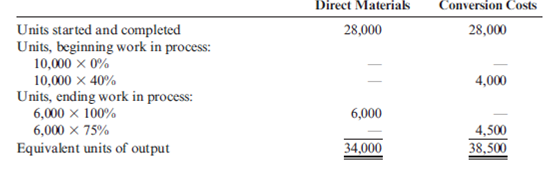

5

FIFO Method, Valuation of Goods Transferred Out and Ending Work in Process

K-Briggs Company uses the FIFO method to account for the costs of production. For Crushing, the first processing department, the following equivalent units schedule has been prepared:

The cost per equivalent unit for the period was as follows:

The cost of beginning work in process was direct materials, $40,000; conversion costs, $30,000.

Required:

1. Determine the cost of ending work in process and the cost of goods transferred out.

2. Prepare a physical flow schedule.

K-Briggs Company uses the FIFO method to account for the costs of production. For Crushing, the first processing department, the following equivalent units schedule has been prepared:

The cost per equivalent unit for the period was as follows:

The cost of beginning work in process was direct materials, $40,000; conversion costs, $30,000.

Required:

1. Determine the cost of ending work in process and the cost of goods transferred out.

2. Prepare a physical flow schedule.

Unlock Deck

Unlock for access to all 58 flashcards in this deck.

Unlock Deck

k this deck

6

Weighted Average Method, Single Department Analysis, Uniform Costs

Hatch Company produces a product that passes through three processes: Fabrication, Assembly, and Finishing. All manufacturing costs are added uniformly for all processes. The following information was obtained for the Fabrication Department for December:

a. Work in process, June 1, had 90,000 units (40 percent completed) and the following costs:

b. During the month of June, 180,000 units were completed and transferred to the Assembly Department, and the following costs were added to production:

c. On June 30, there were 45,000 partially completed units in process. These units were 80 percent complete.

Required:

Prepare a cost of production report for the Fabrication Department for June using the weighted average method of costing. The report should disclose the physical flow of units, equivalent units, and unit costs and should track the disposition of manufacturing costs.

Hatch Company produces a product that passes through three processes: Fabrication, Assembly, and Finishing. All manufacturing costs are added uniformly for all processes. The following information was obtained for the Fabrication Department for December:

a. Work in process, June 1, had 90,000 units (40 percent completed) and the following costs:

b. During the month of June, 180,000 units were completed and transferred to the Assembly Department, and the following costs were added to production:

c. On June 30, there were 45,000 partially completed units in process. These units were 80 percent complete.

Required:

Prepare a cost of production report for the Fabrication Department for June using the weighted average method of costing. The report should disclose the physical flow of units, equivalent units, and unit costs and should track the disposition of manufacturing costs.

Unlock Deck

Unlock for access to all 58 flashcards in this deck.

Unlock Deck

k this deck

7

What are equivalent units? Why are they needed in a process-costing system?

Unlock Deck

Unlock for access to all 58 flashcards in this deck.

Unlock Deck

k this deck

8

Equivalent Units: Weighted Average Method

The following data are for four independent process-costing departments. Inputs are added continuously.

Required:

Compute the equivalent units of production for each of the preceding departments using the weighted average method.

The following data are for four independent process-costing departments. Inputs are added continuously.

Required:

Compute the equivalent units of production for each of the preceding departments using the weighted average method.

Unlock Deck

Unlock for access to all 58 flashcards in this deck.

Unlock Deck

k this deck

9

FIFO Method, Single Department Analysis, One Cost Category

Refer to the data in Problem 6.33.

Required:

Prepare a cost of production report for the Fabrication Department for December using the FIFO method of costing.

Refer to the data in Problem 6.33.

Required:

Prepare a cost of production report for the Fabrication Department for December using the FIFO method of costing.

Unlock Deck

Unlock for access to all 58 flashcards in this deck.

Unlock Deck

k this deck

10

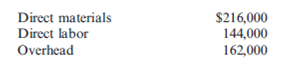

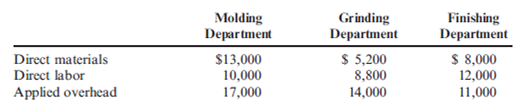

Cost Flows

Lamont Company produced 80,000 machine parts for diesel engines. There were no beginning or ending work-in-process inventories in any department. Lamont incurred the following costs for May:

Required:

1. Calculate the costs transferred out of each department.

2. Prepare the journal entries corresponding to these transfers. Also, prepare the journal entry for Grinding that reflects the costs added to the transferred-in goods received from Molding.

3. What if the Grinding Department had an ending WIP of $12,000? Calculate the cost transferred out and provide the journal entry that would reflect this transfer. What is the effect on finished goods calculated in Requirement 1, assuming the other two departments have no ending WIP?

Lamont Company produced 80,000 machine parts for diesel engines. There were no beginning or ending work-in-process inventories in any department. Lamont incurred the following costs for May:

Required:

1. Calculate the costs transferred out of each department.

2. Prepare the journal entries corresponding to these transfers. Also, prepare the journal entry for Grinding that reflects the costs added to the transferred-in goods received from Molding.

3. What if the Grinding Department had an ending WIP of $12,000? Calculate the cost transferred out and provide the journal entry that would reflect this transfer. What is the effect on finished goods calculated in Requirement 1, assuming the other two departments have no ending WIP?

Unlock Deck

Unlock for access to all 58 flashcards in this deck.

Unlock Deck

k this deck

11

Unit Information with BWIP, Weighted Average Method

Jackson Products produces a barbeque sauce using three departments: Cooking, Mixing, and Bottling. In the Cooking Department, all materials are added at the beginning of the process. Output is measured in ounces. The production data for July are as follows:

Required:

1. Prepare a physical flow schedule for July.

2. Prepare an equivalent units schedule for July using the weighted average method.

3. What if you were asked to calculate the FIFO units beginning with the weighted average equivalent units? Calculate the weighted average equivalent units by subtracting out the prior-period output found in BWIP.

Jackson Products produces a barbeque sauce using three departments: Cooking, Mixing, and Bottling. In the Cooking Department, all materials are added at the beginning of the process. Output is measured in ounces. The production data for July are as follows:

Required:

1. Prepare a physical flow schedule for July.

2. Prepare an equivalent units schedule for July using the weighted average method.

3. What if you were asked to calculate the FIFO units beginning with the weighted average equivalent units? Calculate the weighted average equivalent units by subtracting out the prior-period output found in BWIP.

Unlock Deck

Unlock for access to all 58 flashcards in this deck.

Unlock Deck

k this deck

12

Equivalent Units: FIFO Method

Using the data from Exercise 6.18, compute the equivalent units of production for each of the four departments using the FIFO method.

Using the data from Exercise 6.18, compute the equivalent units of production for each of the four departments using the FIFO method.

Unlock Deck

Unlock for access to all 58 flashcards in this deck.

Unlock Deck

k this deck

13

Service Organization with Work-in-Process Inventories, Multiple Departments, FIFO Method, Unit Cost

Hepworth Credit Corporation is a wholly owned subsidiary of a large manufacturer of computers. Hepworth is in the business of financing computers, software, and other services that the parent corporation sells. Hepworth has two departments that are involved in financing services: the Credit Department and the Business Practices Department. The Credit Department receives requests for financing from field sales representatives, records customer information on a preprinted form, and then enters the information into the computer system to check the creditworthiness of the customer. (Other actions may be taken if the customer is not in the database.) Once creditworthiness information is known, a printout is produced with this information plus other customer-specific information. The completed form is transferred to the Business Practices Department.

The Business Practices Department modifies the standard loan covenant as needed (in response to customer request or customer risk profile). When this activity is completed, the loan is priced. This is done by keying information from the partially processed form into a personal computer spreadsheet program. The program provides a recommended interest rate for the loan. Finally, a form specifying the loan terms is attached to the transferred-in document. A copy of the loan-term form is sent to the sales representative and serves as the quote letter.

The following cost and service activity data for the Business Practices Department are provided for the month of May:

Required:

1. How would you define the output of the Business Practices Department?

2. Using the FIFO method, prepare the following for the Business Practices Department:

a. A physical flow schedule

b. An equivalent units schedule

Transferred-in applications

c. Calculation of unit costs

d. Cost of ending work in process and cost of units transferred out

e. A cost reconciliation

Hepworth Credit Corporation is a wholly owned subsidiary of a large manufacturer of computers. Hepworth is in the business of financing computers, software, and other services that the parent corporation sells. Hepworth has two departments that are involved in financing services: the Credit Department and the Business Practices Department. The Credit Department receives requests for financing from field sales representatives, records customer information on a preprinted form, and then enters the information into the computer system to check the creditworthiness of the customer. (Other actions may be taken if the customer is not in the database.) Once creditworthiness information is known, a printout is produced with this information plus other customer-specific information. The completed form is transferred to the Business Practices Department.

The Business Practices Department modifies the standard loan covenant as needed (in response to customer request or customer risk profile). When this activity is completed, the loan is priced. This is done by keying information from the partially processed form into a personal computer spreadsheet program. The program provides a recommended interest rate for the loan. Finally, a form specifying the loan terms is attached to the transferred-in document. A copy of the loan-term form is sent to the sales representative and serves as the quote letter.

The following cost and service activity data for the Business Practices Department are provided for the month of May:

Required:

1. How would you define the output of the Business Practices Department?

2. Using the FIFO method, prepare the following for the Business Practices Department:

a. A physical flow schedule

b. An equivalent units schedule

Transferred-in applications

c. Calculation of unit costs

d. Cost of ending work in process and cost of units transferred out

e. A cost reconciliation

Unlock Deck

Unlock for access to all 58 flashcards in this deck.

Unlock Deck

k this deck

14

What is a process? Provide an example that illustrates the definition.

Unlock Deck

Unlock for access to all 58 flashcards in this deck.

Unlock Deck

k this deck

15

How is the equivalent unit calculation affected when direct materials are added at the beginning or end of the process rather than uniformly throughout the process?

Unlock Deck

Unlock for access to all 58 flashcards in this deck.

Unlock Deck

k this deck

16

Weighted Average Method, Unit Cost, Valuation of Goods Transferred Out and Ending Work in Process

Holmes Products, Inc., produces plastic cases used for video cameras. The product passes through three departments. For April, the following equivalent units schedule was prepared for the first department:

Costs assigned to beginning work in process: direct materials, $90,000; conversion costs, $33,750. Manufacturing costs incurred during April: direct materials, $75,000; conversion costs, $220,000. Holmes uses the weighted average method.

Required:

1. Compute the unit cost for April.

2. Determine the cost of ending work in process and the cost of goods transferred out.

Holmes Products, Inc., produces plastic cases used for video cameras. The product passes through three departments. For April, the following equivalent units schedule was prepared for the first department:

Costs assigned to beginning work in process: direct materials, $90,000; conversion costs, $33,750. Manufacturing costs incurred during April: direct materials, $75,000; conversion costs, $220,000. Holmes uses the weighted average method.

Required:

1. Compute the unit cost for April.

2. Determine the cost of ending work in process and the cost of goods transferred out.

Unlock Deck

Unlock for access to all 58 flashcards in this deck.

Unlock Deck

k this deck

17

Weighted Average Method, Journal Entries

Muskoge Company uses a process-costing system. The company manufactures a product that is processed in two departments: Molding and Assembly. In the Molding Department, direct materials are added at the beginning of the process; in the Assembly Department, additional direct materials are added at the end of the process. In both departments, conversion costs are incurred uniformly throughout the process. As work is completed, it is transferred out. The following table summarizes the production activity and costs for February:

Required:

1. Using the weighted average method, prepare the following for the Molding Department:

a. A physical flow schedule

b. An equivalent units calculation

c. Calculation of unit costs. Round to four decimal places.

d. Cost of ending work in process and cost of goods transferred out

e. A cost reconciliation

2. Prepare journal entries that show the flow of manufacturing costs for the Molding Department. Materials are added at the beginning of the process.

3. Repeat Requirements 1 and 2 for the Assembly Department.

Muskoge Company uses a process-costing system. The company manufactures a product that is processed in two departments: Molding and Assembly. In the Molding Department, direct materials are added at the beginning of the process; in the Assembly Department, additional direct materials are added at the end of the process. In both departments, conversion costs are incurred uniformly throughout the process. As work is completed, it is transferred out. The following table summarizes the production activity and costs for February:

Required:

1. Using the weighted average method, prepare the following for the Molding Department:

a. A physical flow schedule

b. An equivalent units calculation

c. Calculation of unit costs. Round to four decimal places.

d. Cost of ending work in process and cost of goods transferred out

e. A cost reconciliation

2. Prepare journal entries that show the flow of manufacturing costs for the Molding Department. Materials are added at the beginning of the process.

3. Repeat Requirements 1 and 2 for the Assembly Department.

Unlock Deck

Unlock for access to all 58 flashcards in this deck.

Unlock Deck

k this deck

18

Unit Cost, No Work-in-Process Inventories

Lising Therapy has a physical therapist who performs electro-mechanical treatments for its patients. During April, Lising had the following cost and output information:

Required:

1. Calculate the cost per treatment for April.

2. Calculate the cost of services sold for April.

3. What if Lising found a way to reduce overhead costs by 20 percent? How would this affect the profit per treatment?

Lising Therapy has a physical therapist who performs electro-mechanical treatments for its patients. During April, Lising had the following cost and output information:

Required:

1. Calculate the cost per treatment for April.

2. Calculate the cost of services sold for April.

3. What if Lising found a way to reduce overhead costs by 20 percent? How would this affect the profit per treatment?

Unlock Deck

Unlock for access to all 58 flashcards in this deck.

Unlock Deck

k this deck

19

Describe the five steps in accounting for the manufacturing activity of a processing department, and indicate how they interrelate.

Unlock Deck

Unlock for access to all 58 flashcards in this deck.

Unlock Deck

k this deck

20

FIFO Method, Unit Cost, Valuation of Goods Transferred Out and Ending Work in Process

Dama Company produces women's blouses and uses the FIFO method to account for its manufacturing costs. The product Dama makes passes through two processes: Cutting and Sewing. During April, Dama's controller prepared the following equivalent units schedule for the Cutting Department:

Costs in beginning work in process were direct materials, $20,000; conversion costs, $80,000. Manufacturing costs incurred during April were direct materials, $240,000; conversion costs, $320,000.

Required:

1. Prepare a physical flow schedule for April.

2. Compute the cost per equivalent unit for April.

3. Determine the cost of ending work in process and the cost of goods transferred out.

4. Prepare the journal entry that transfers the costs from Cutting to Sewing.

Dama Company produces women's blouses and uses the FIFO method to account for its manufacturing costs. The product Dama makes passes through two processes: Cutting and Sewing. During April, Dama's controller prepared the following equivalent units schedule for the Cutting Department:

Costs in beginning work in process were direct materials, $20,000; conversion costs, $80,000. Manufacturing costs incurred during April were direct materials, $240,000; conversion costs, $320,000.

Required:

1. Prepare a physical flow schedule for April.