Deck 21: Cases

Full screen (f)

Question

Beauville Furniture Corporation produces sofas, recliners, and lounge chairs. Beauville is located in a medium-sized community in the southeastern part of the United States. It is a major employer in the community. In fact, the economic well-being of the community is tied very strongly to Beauville. Beauville operates a sawmill, a fabric plant, and a furniture plant in the same community.

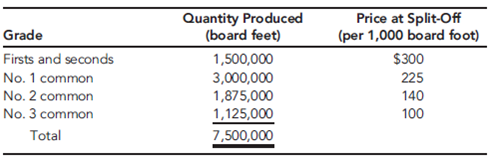

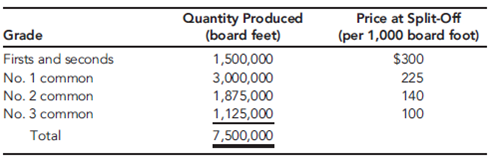

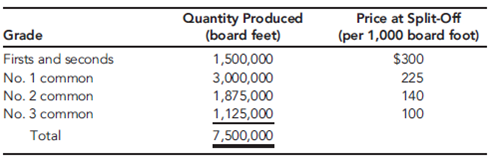

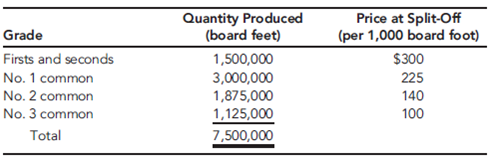

The sawmill buys logs from independent producers. The sawmill then processes the logs into four grades of lumber: firsts and seconds, No. 1 common, No. 2 common, and No. 3 common. All costs incurred in the mill are common to the four grades of lumber. All four grades of lumber are used by the furniture plant. The mill transfers everything it produces to the furniture plant, and the grades are transferred at cost. Trucks are used to move the lumber from the mill to the furniture plant. Although no outside sales exist, the mill could sell to external customers, and the selling prices of the four grades are known.

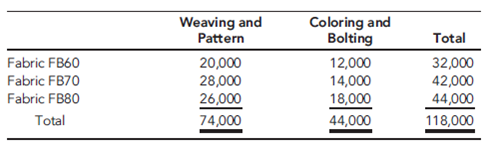

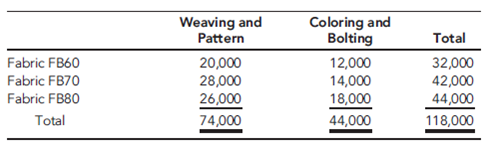

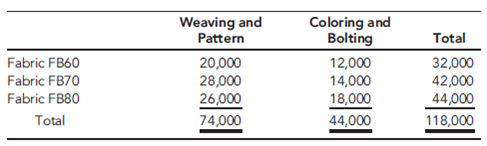

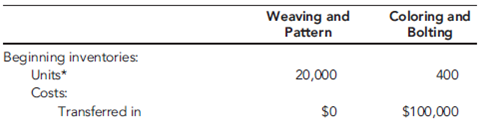

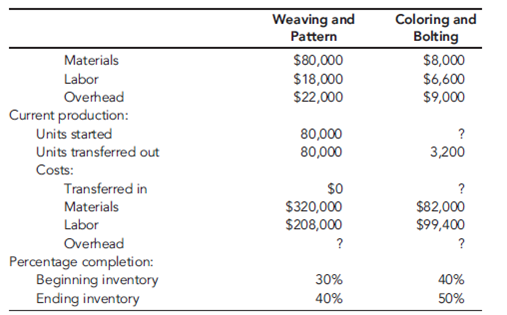

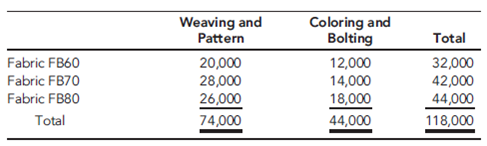

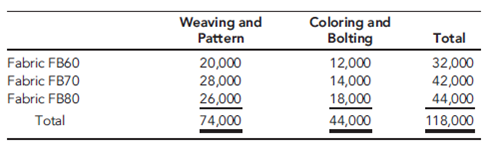

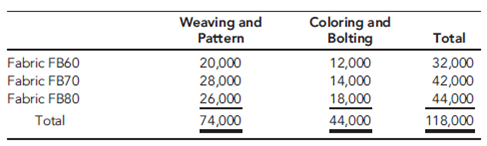

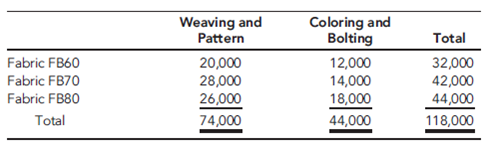

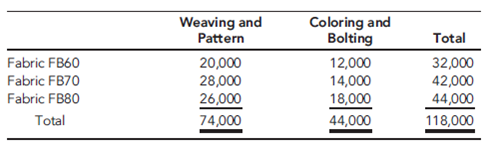

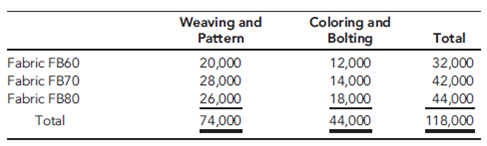

The fabric plant is responsible for producing the fabric that is used by the furniture plant. To produce three totally different fabrics (identified by fabric ID codes FB60, FB70, and FB80, respectively), the plant has three separate production operations-one for each fabric. Thus, production of all three fabrics occurs at the same time in different locations in the plant. Each fabric's production operation has two processes: the weaving and pattern process and the coloring and bolting process. In the weaving and pattern process, yarn is used to create yards of fabric with different designs. In the next process, the fabric is dyed, cut into 25-yard sections, and wrapped around cardboard rods to form 25-yard bolts. The bolts are transported by forklift to the furniture plant's Receiving Department. All of the output of the fabric plant is used by the furniture plant (to produce the sofas and chairs). For accounting purposes, the fabric is transferred at cost to the furniture plant.

The furniture plant produces orders for customers on a special-order basis. The customers specify the quantity, style, fabric, lumber grade, and pattern. Typically, jobs are large (involving at least 500 units). The plant has two production departments: Cutting and Assembly. In the Cutting Department, the fabric and wooden frame components are sized and cut. Other components are purchased from external suppliers and are removed from stores as needed for assembly. After the fabric and wooden components are finished for the entire job, they are moved to the Assembly Department. The Assembly Department takes the individual components and assembles the sofas (or chairs).

Beauville Furniture has been in business for over two decades and has a good reputation. However, during the past five years, Beauville experienced eroding profits and declining sales. Bids were increasingly lost (even aggressive bids) on the more popular models. Yet, the company was winning bids on some of the more-difficult-to-produce items. Lance Hays, the owner and manager, was frustrated. He simply couldn't understand how some of his competitors could sell for such low prices. On a common sofa job involving 500 units, Beauville's bids were running $25 per unit, or $12,500 per job more than the winning bids (on average). Yet, on the more difficult items, Beauville's bids were running about $60 per unit less than the next closest bid. Gisela Berling, vice president of finance, was assigned the task of preparing a cost analysis of the company's product lines. Lance wanted to know if the company's costs were excessive. Perhaps the company was being wasteful, and it was simply costing more to produce furniture than it was costing its competitors.

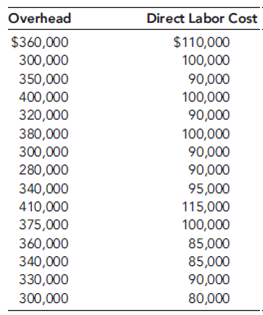

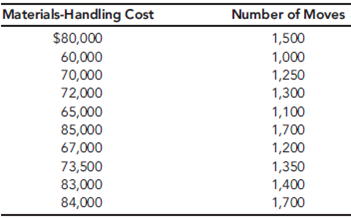

Gisela prepared herself by reading recent literature on cost management and product costing and attending several conferences that explored the same issues. She then reviewed the costing procedures of the company's mill and two plants and did a preliminary assessment of their soundness. The production costs of the mill were common to all lumber grades and were assigned using the physical units method. Since the output and production costs were fairly uniform throughout the year, the mill used an actual costing system. Although Gisela had no difficulty with actual costing, she decided to explore the effects of using the sales-value-at-split-off method. Thus, cost and production data for the mill were gathered so that an analysis could be conducted. The two plants used normal costing systems. The fabric plant used process costing, and the furniture plant used job-order costing. Both plants used plantwide overhead rates based on direct labor hours. Based on her initial reviews, she concluded that the costing procedures for the fabric plant were satisfactory. Essentially, there was no evidence of product diversity. A statistical analysis revealed that about 90 percent of the variability in the plant's overhead cost could be explained by direct labor hours. Thus, the use of a plantwide overhead rate based on direct labor hours seemed justified. What did concern her, though, was the material waste that she observed in the plant. Maybe a standard cost system would be useful for increasing the overall cost efficiency of the plant. Consequently, as part of her report to Lance, she decided to include a description of the fabric plant's costing procedures-at least for one of the fabric types. She also decided to develop a standard cost sheet for the chosen fabric. The furniture plant, however, was a more difficult matter. Product diversity was present and could be causing some distortions in product costs. Furthermore, statistical analysis revealed that only about 40 percent of the variability in overhead cost was explained by the direct labor hours. She decided that additional analysis was needed so that a sound product costing method could be recommended. One possibility would be to increase the number of overhead rates. Thus, she decided to include departmental data so that the effect of moving to departmental rates could be assessed. Finally, she also wanted to explore the possibility of converting the sawmill and fabric plant into profit centers and changing the existing transfer pricing policy.

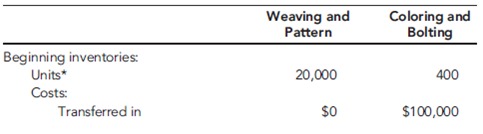

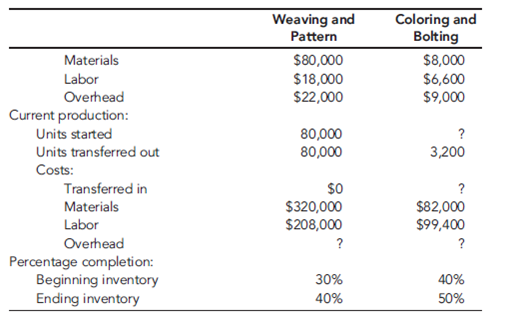

With the cooperation of the cost accounting manager for the mill and each plant's controller, she gathered the following data for last year:

Sawmill:

Joint manufacturing costs: $900,000

Fabric Plant:

Budgeted overhead: $1,200,000 (50% fixed)

Practical volume (direct labor hours): 120,000 hours

Actual overhead: $1,150,000 (50% fixed)

Actual hours worked:

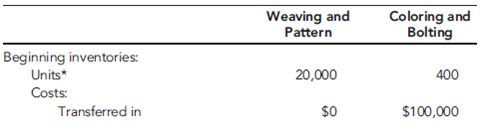

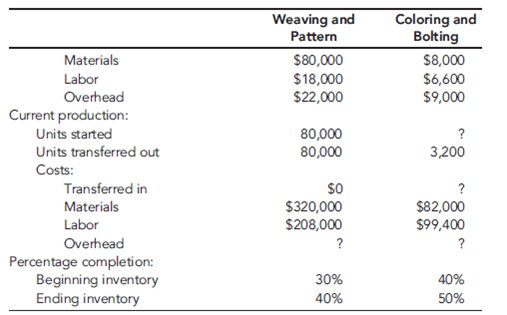

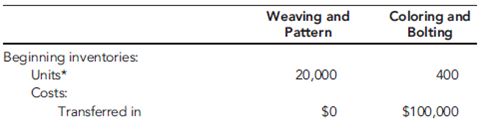

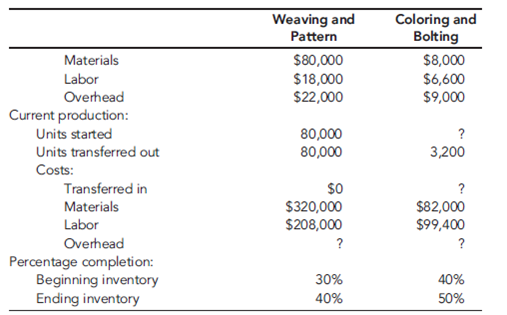

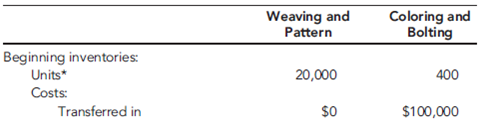

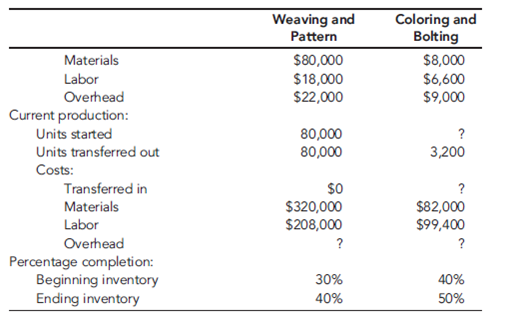

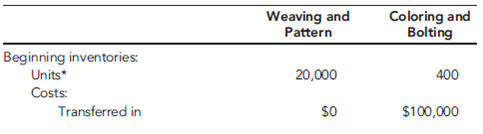

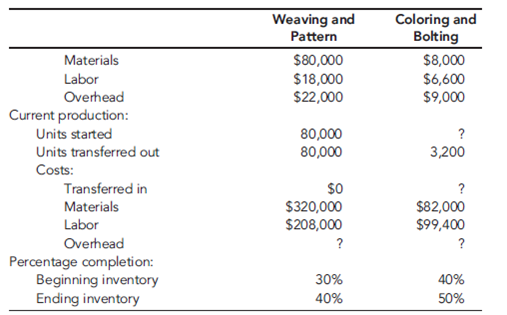

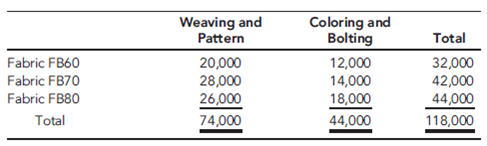

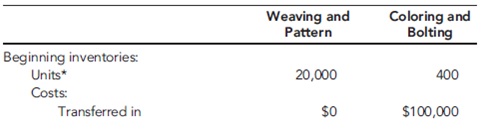

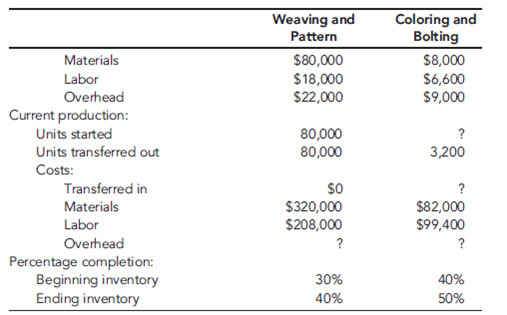

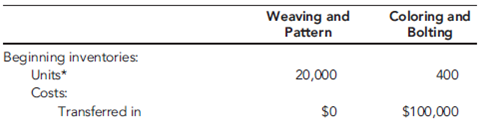

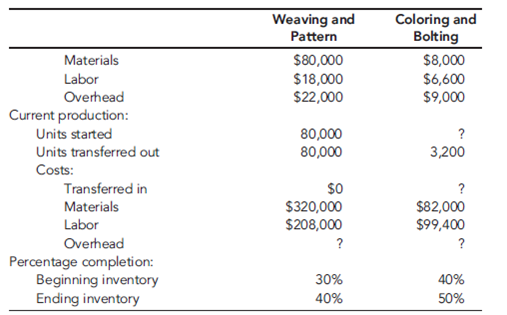

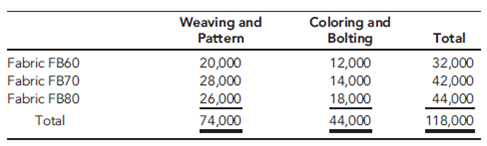

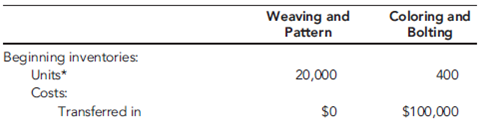

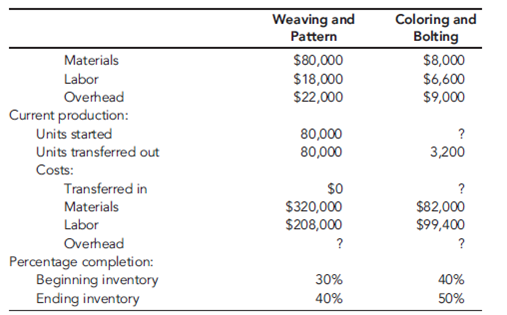

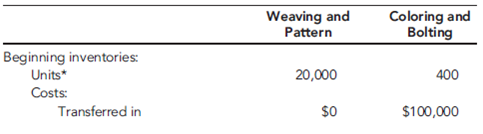

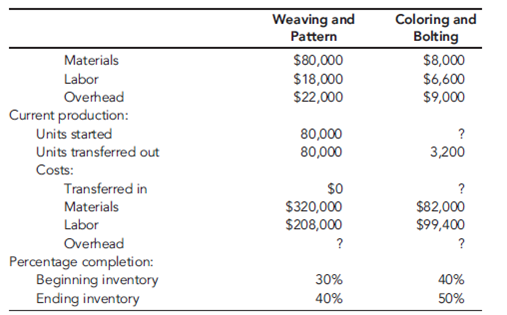

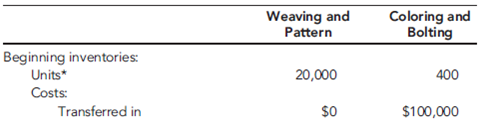

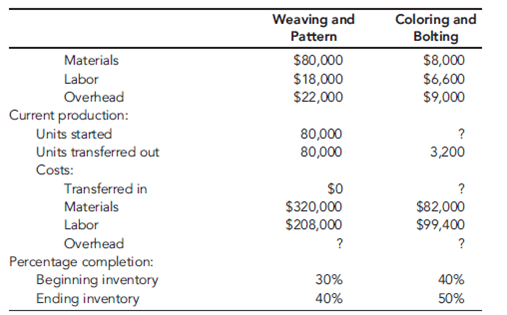

Departmental data on Fabric FB70 (actual costs and actual outcomes):

*Unitsare measured in yards for the Weaving and Pattern Department and in bolts forthe Coloring and Bolting Department. Note: With the exception of the cardboard bolt rods, materials are added at the beginning of each process. The cost of the rods is relatively insignificant and is included in overhead.

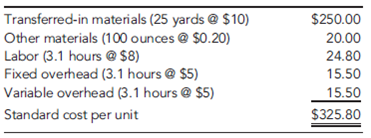

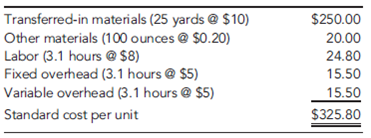

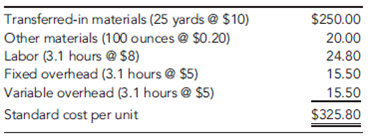

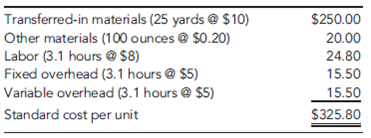

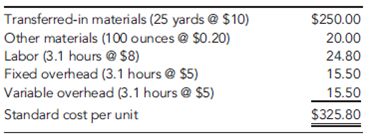

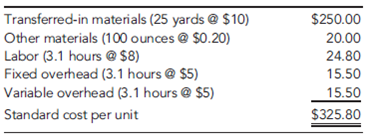

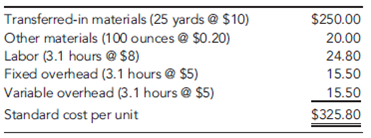

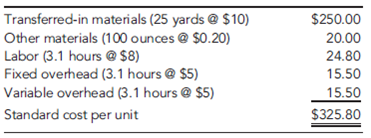

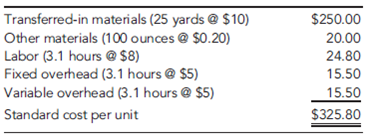

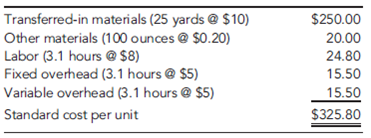

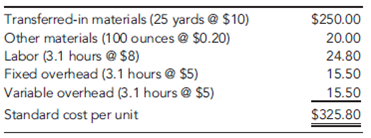

Proposed standard cost sheet for Fabric FB70 (for the Coloring and Bolting Department only):

Furniture Plant:

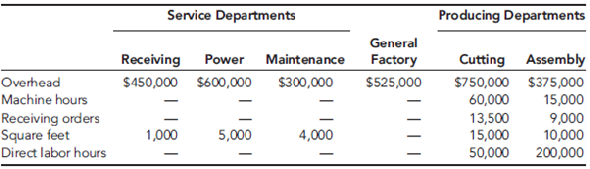

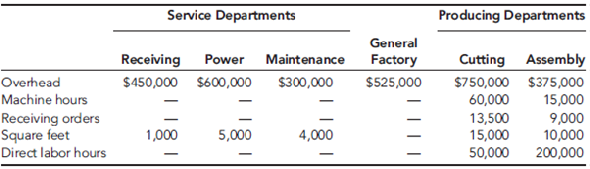

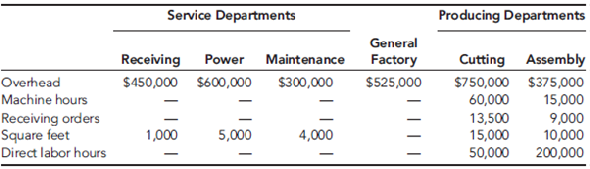

Departmental data (budgeted):

After some discussion with the furniture plant controller, Gisela decided to use machine hours to calculate the overhead rate for the Cutting Department and direct labor hours for the Assembly Department rate (the Cutting Department was more automated than the Assembly Department). As part of her report, she wanted to compare the effects of plantwide rates and departmental rates on the cost of jobs. She wanted to know if overhead costing could be the source of the pricing problems the company was experiencing.

To assess the effect of the different overhead assignment procedures, Gisela decided to examine two prospective jobs. One job, Job A500, could produce 500 sofas, using a frequently requested style and Fabric FB70. Bids on this type of job were being lost more frequently to competitors. The second job, Job B75, would produce 75 specially designed recliners. This job involved a new design and was more difficult for the workers to build. It involved some special cutting requirements and an unfamiliar assembly. Recently, the company seemed to be winning more bids on jobs of this type. To compute the costs of the two jobs, Gisela assembled the following information on the two jobs:

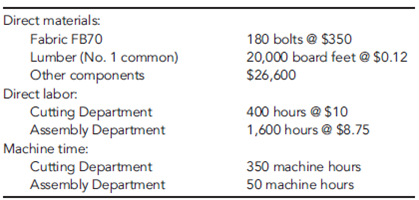

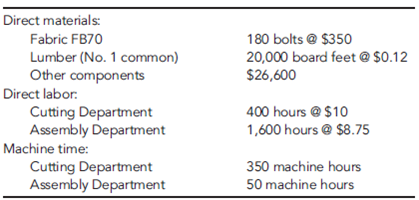

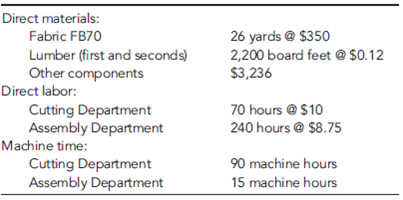

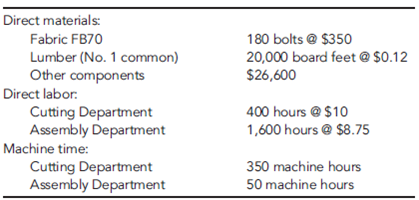

Job A500:

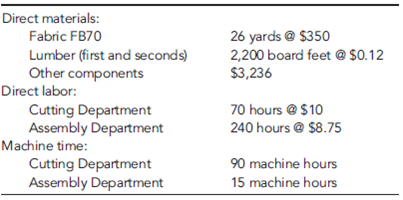

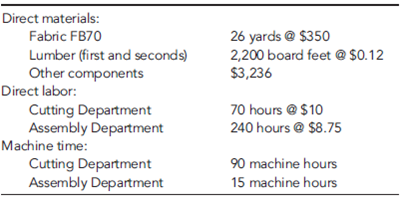

Job B75:

Required

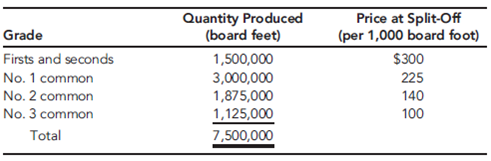

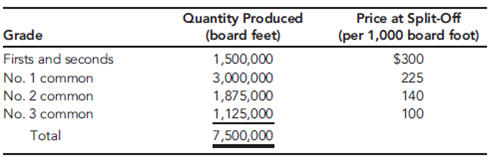

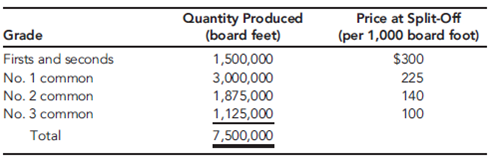

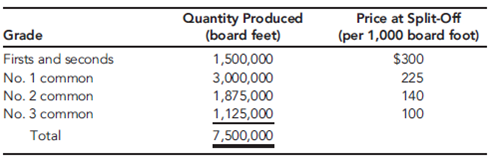

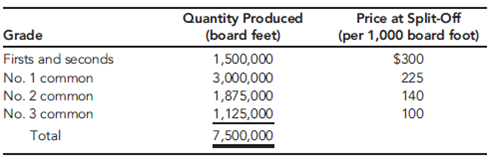

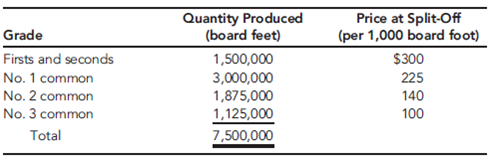

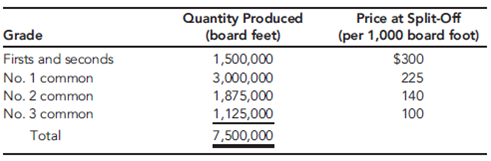

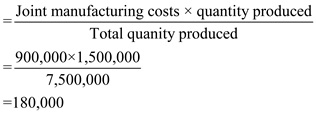

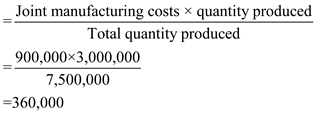

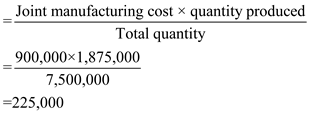

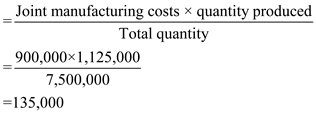

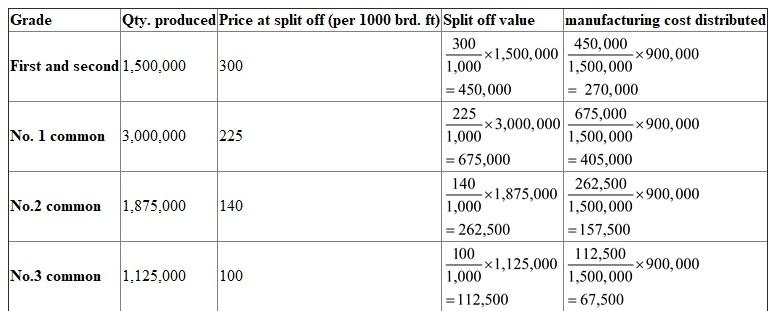

Allocate the joint manufacturing costs to each grade, and calculate the cost per board foot for each grade: (a) using the physical units method of allocation, and (b) using the sales-value-at- split-off method. Which method should the mill use? Explain. What is the effect on the cost of each proposed job if the mill switches to the sales-value-at-split-off method?

The sawmill buys logs from independent producers. The sawmill then processes the logs into four grades of lumber: firsts and seconds, No. 1 common, No. 2 common, and No. 3 common. All costs incurred in the mill are common to the four grades of lumber. All four grades of lumber are used by the furniture plant. The mill transfers everything it produces to the furniture plant, and the grades are transferred at cost. Trucks are used to move the lumber from the mill to the furniture plant. Although no outside sales exist, the mill could sell to external customers, and the selling prices of the four grades are known.

The fabric plant is responsible for producing the fabric that is used by the furniture plant. To produce three totally different fabrics (identified by fabric ID codes FB60, FB70, and FB80, respectively), the plant has three separate production operations-one for each fabric. Thus, production of all three fabrics occurs at the same time in different locations in the plant. Each fabric's production operation has two processes: the weaving and pattern process and the coloring and bolting process. In the weaving and pattern process, yarn is used to create yards of fabric with different designs. In the next process, the fabric is dyed, cut into 25-yard sections, and wrapped around cardboard rods to form 25-yard bolts. The bolts are transported by forklift to the furniture plant's Receiving Department. All of the output of the fabric plant is used by the furniture plant (to produce the sofas and chairs). For accounting purposes, the fabric is transferred at cost to the furniture plant.

The furniture plant produces orders for customers on a special-order basis. The customers specify the quantity, style, fabric, lumber grade, and pattern. Typically, jobs are large (involving at least 500 units). The plant has two production departments: Cutting and Assembly. In the Cutting Department, the fabric and wooden frame components are sized and cut. Other components are purchased from external suppliers and are removed from stores as needed for assembly. After the fabric and wooden components are finished for the entire job, they are moved to the Assembly Department. The Assembly Department takes the individual components and assembles the sofas (or chairs).

Beauville Furniture has been in business for over two decades and has a good reputation. However, during the past five years, Beauville experienced eroding profits and declining sales. Bids were increasingly lost (even aggressive bids) on the more popular models. Yet, the company was winning bids on some of the more-difficult-to-produce items. Lance Hays, the owner and manager, was frustrated. He simply couldn't understand how some of his competitors could sell for such low prices. On a common sofa job involving 500 units, Beauville's bids were running $25 per unit, or $12,500 per job more than the winning bids (on average). Yet, on the more difficult items, Beauville's bids were running about $60 per unit less than the next closest bid. Gisela Berling, vice president of finance, was assigned the task of preparing a cost analysis of the company's product lines. Lance wanted to know if the company's costs were excessive. Perhaps the company was being wasteful, and it was simply costing more to produce furniture than it was costing its competitors.

Gisela prepared herself by reading recent literature on cost management and product costing and attending several conferences that explored the same issues. She then reviewed the costing procedures of the company's mill and two plants and did a preliminary assessment of their soundness. The production costs of the mill were common to all lumber grades and were assigned using the physical units method. Since the output and production costs were fairly uniform throughout the year, the mill used an actual costing system. Although Gisela had no difficulty with actual costing, she decided to explore the effects of using the sales-value-at-split-off method. Thus, cost and production data for the mill were gathered so that an analysis could be conducted. The two plants used normal costing systems. The fabric plant used process costing, and the furniture plant used job-order costing. Both plants used plantwide overhead rates based on direct labor hours. Based on her initial reviews, she concluded that the costing procedures for the fabric plant were satisfactory. Essentially, there was no evidence of product diversity. A statistical analysis revealed that about 90 percent of the variability in the plant's overhead cost could be explained by direct labor hours. Thus, the use of a plantwide overhead rate based on direct labor hours seemed justified. What did concern her, though, was the material waste that she observed in the plant. Maybe a standard cost system would be useful for increasing the overall cost efficiency of the plant. Consequently, as part of her report to Lance, she decided to include a description of the fabric plant's costing procedures-at least for one of the fabric types. She also decided to develop a standard cost sheet for the chosen fabric. The furniture plant, however, was a more difficult matter. Product diversity was present and could be causing some distortions in product costs. Furthermore, statistical analysis revealed that only about 40 percent of the variability in overhead cost was explained by the direct labor hours. She decided that additional analysis was needed so that a sound product costing method could be recommended. One possibility would be to increase the number of overhead rates. Thus, she decided to include departmental data so that the effect of moving to departmental rates could be assessed. Finally, she also wanted to explore the possibility of converting the sawmill and fabric plant into profit centers and changing the existing transfer pricing policy.

With the cooperation of the cost accounting manager for the mill and each plant's controller, she gathered the following data for last year:

Sawmill:

Joint manufacturing costs: $900,000

Fabric Plant:

Budgeted overhead: $1,200,000 (50% fixed)

Practical volume (direct labor hours): 120,000 hours

Actual overhead: $1,150,000 (50% fixed)

Actual hours worked:

Departmental data on Fabric FB70 (actual costs and actual outcomes):

*Unitsare measured in yards for the Weaving and Pattern Department and in bolts forthe Coloring and Bolting Department. Note: With the exception of the cardboard bolt rods, materials are added at the beginning of each process. The cost of the rods is relatively insignificant and is included in overhead.

Proposed standard cost sheet for Fabric FB70 (for the Coloring and Bolting Department only):

Furniture Plant:

Departmental data (budgeted):

After some discussion with the furniture plant controller, Gisela decided to use machine hours to calculate the overhead rate for the Cutting Department and direct labor hours for the Assembly Department rate (the Cutting Department was more automated than the Assembly Department). As part of her report, she wanted to compare the effects of plantwide rates and departmental rates on the cost of jobs. She wanted to know if overhead costing could be the source of the pricing problems the company was experiencing.

To assess the effect of the different overhead assignment procedures, Gisela decided to examine two prospective jobs. One job, Job A500, could produce 500 sofas, using a frequently requested style and Fabric FB70. Bids on this type of job were being lost more frequently to competitors. The second job, Job B75, would produce 75 specially designed recliners. This job involved a new design and was more difficult for the workers to build. It involved some special cutting requirements and an unfamiliar assembly. Recently, the company seemed to be winning more bids on jobs of this type. To compute the costs of the two jobs, Gisela assembled the following information on the two jobs:

Job A500:

Job B75:

Required

Allocate the joint manufacturing costs to each grade, and calculate the cost per board foot for each grade: (a) using the physical units method of allocation, and (b) using the sales-value-at- split-off method. Which method should the mill use? Explain. What is the effect on the cost of each proposed job if the mill switches to the sales-value-at-split-off method?

Question

Zando Pharmaceuticals is an affiliate of the German-based Heisenberg Corporation, which employs 40,000 worldwide. Zando's St. Louis facility houses the U.S. corporate headquarters and Research and Development (R D). It produces 30 products, using 28 different batch processes. The facility has 2,000 employees on-site. In recent years, Zando's profitability has suffered, which can be attributed to increased competition, customer dissatisfaction, and regulatory pressures. Luis Alvarado, president of Zando, called a meeting to consider ways to improve profitability. He labeled the meeting a strategic planning session and invited the following officers: Kathy Shorts, environmental manager; Troy Lewis, head of R D; Johnny Mizukawa, vice president of production and quality; Larry Sower, vice president of finance; and Doreen Savara, marketing vice president.

Luis : "You all have received the quarterly financial reports for the last two years. The trends are negative. We are losing market share, profits are decreasing, and our costs seem to be increasing. We need to take actions to increase sales and reduce costs, and we need to do so as quickly as possible. Given our research strengths, it seems to me that our best bet is to grow revenues by introducing new products with proprietary rights. As far as costs are concerned, we need to improve our performance on that dimension as well. Lower per-unit costs for new and existing products are needed. Any suggestions?"

Troy : "For our products, our ability to control costs resides in development-my area-rather than manufacturing. We probably need to pay more attention to product and process design issues to ensure a reasonably level per-unit cost. Revenues are also affected in this stage. Once we patent a drug, the clock begins to tick, and we need to reduce time to market. Significantly, reducing time to market will allow us to generate revenues for a longer period of time than we are currently experiencing. It would also be helpful if we could reduce the cycle time for product development. Both actions would increase revenues. Finally, we can increase revenues by increasing the volume of new products."

Johnny : "There is a lot of merit to the observation that cost reduction opportunities reside mostly in product development. Once a drug is approved, its approval includes the manufacturing process. Any future changes in the manufacturing process require approval from the U.S. Food and Drug Administration. Because of this, we have been reluctant, historically, to engage in process improvement or reengineering. However, I wonder if we shouldn't reconsider this longstanding policy. Some of the quality problems we have could be corrected by changing some of our existing processes, and the costs saved may easily exceed any cost incurred from seeking FDA approval. I think our quality costs are at least 15 percent of sales. That's a lot of opportunity for improvement."

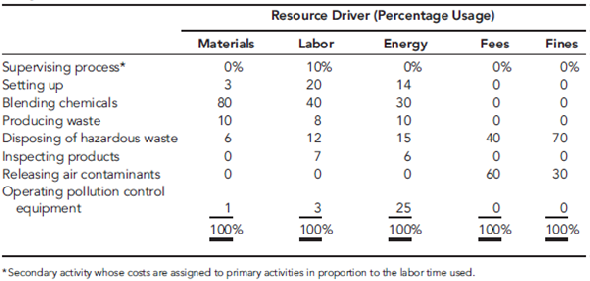

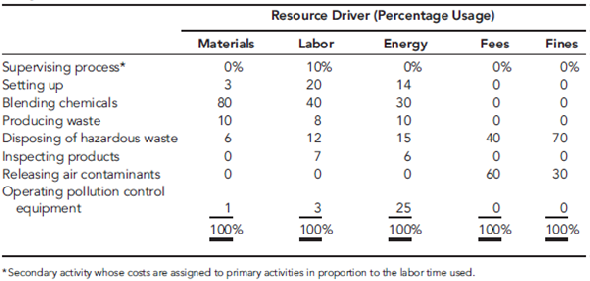

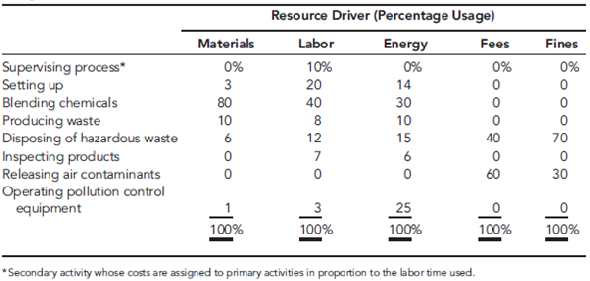

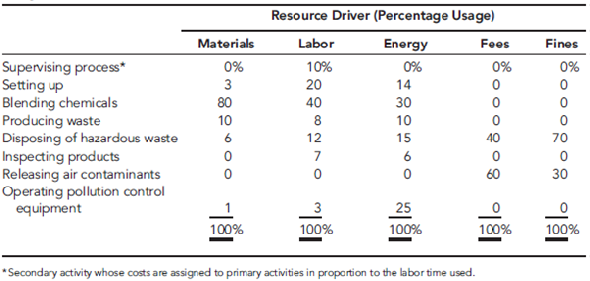

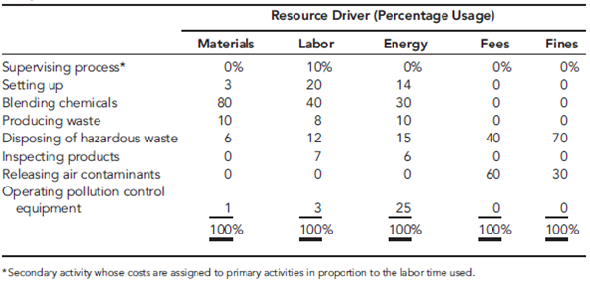

Kathy : "I agree that cost reduction-both in the product development stage and the manufacturing stage-should be a key strategic theme. The environmental area also offers some very good opportunities. A recent pollution prevention act passed by the legislature requires that we calculate the costs of generating hazardous substances for each process. This act was the incentive we needed to begin developing an environmental cost management system. The results so far indicate that environmental costs are much more than we realized. They are estimated to be in the range of 20 to 30 percent of total operating costs. Environmental costs can be reduced by such things as computerizing chemical inventory, eliminating the use of chlorinated solvents and other hazardous materials, reducing our use of virgin feedstocks, and redesigning processes and products so that we can reduce toxic residue release. We can really have a positive environmental impact while simultaneously reducing costs if more attention is paid to environmental issues during product development."

Doreen : "I like what I am hearing because I think that it also affects our ability to increase market share and revenues. For example, environmental impact is one of our major concerns. Some retail pharmacy chains pay particular attention to green products, and right now we are not competing well. Our environmental image is negative and needs to be improved. I am convinced that doing so will allow us to increase market share. Quality is another important matter. We have had to recall two batches of products during the past two years due to poor quality, and this has hurt our image more than the environmental issue. Improving the processes to avoid these kinds of problems will save us a lot of grief. Product image and reputation are essential to increasing customer satisfaction and market share."

Luis : "We started with the need to improve financial performance by increasing revenues and reducing costs. So far, we have some very good suggestions to help achieve these two objectives, but I have some concerns. First, do we have the talent and capabilities to improve quality and environmental performance? Troy, do your professionals really understand what they need to do to improve process and product designs so that we can see the desired quality and environmental improvements? Also, how can we reduce the cycle time for products and the time to market once patented?"

Troy : "Let me answer those questions in order. First, we probably are lacking the understanding on the design issues. We will need to do some training to help our research scientists and chemical engineers understand the consequences. We may need to hire a couple of professionals who have experience in dealing with these issues. Second, we may need to make cycle time and time to market significant performance measures and reward our people for actions that reduce those measures. Our employees need to align their interests with those of the company. If we can achieve this, we should see more revenue produced per employee."

Luis : "Good. Now, Johnny, tell us about production and quality. Do our manufacturing engineers and production workers need help with environmental and quality issues?"

Johnny : "Without question, training will be needed. Moreover, I really need to hire a couple of quality engineers."

Kathy : "I also think that we need an environmental engineer with experience in pharmaceutical manufacturing processes."

Luis : "Good. We certainly shouldn't ignore the necessary infrastructure to bring about the needed changes. Larry, you have been relatively quiet, what do you think about all this? Do you have any suggestions?"

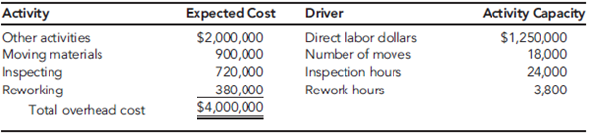

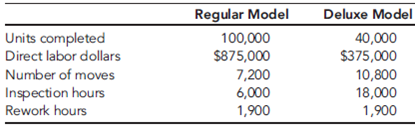

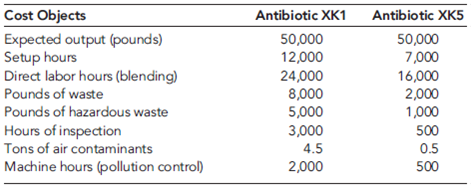

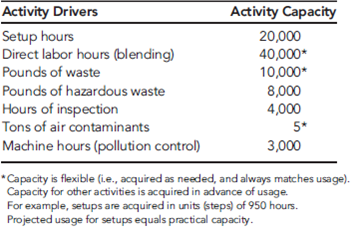

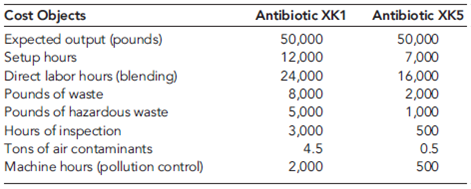

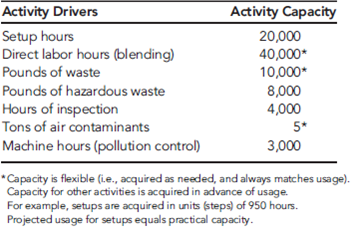

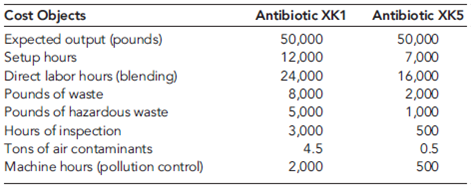

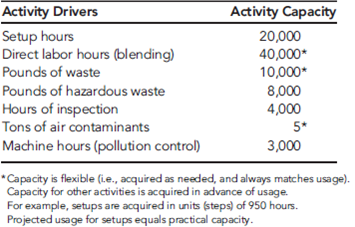

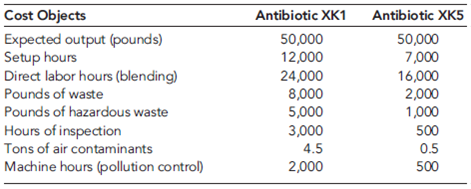

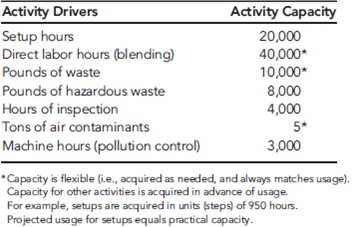

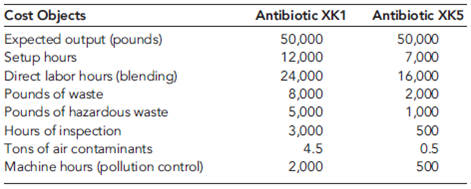

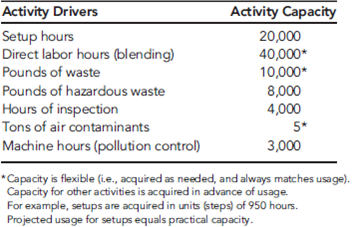

Larry : "Infrastructure is important. If this is all going to work, timely and accurate information will be needed. It is hard to design products and processes with cost being a significant issue without providing the right kind of cost information. We are in the process of revamping the cost management information system so that it is activity based and so that we can provide quality and environmental cost information. After listening to the comments made here, I might also suggest that we need a strategic measurement system that can be used to align the interests of our employees with our improvement strategy. People need to know what is important, that the important factors are being measured, and that they are going to be evaluated and rewarded based on these factors. Finally, I would encourage the use of target costing to help manage costs during product development. To help you all understand the importance of good information, I have assembled some activity data relating to two new products currently under development. These two products will use the same process, using different setups. The data are organized into resource, activity, and cost object modules with an accompanying list of activity drivers to facilitate the use of an ABC software package recently acquired by Zando."

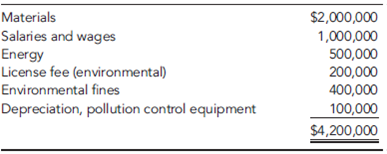

Resource Module (Projected General Ledger Costs of Manufacturing Process Associated with the Two Products)

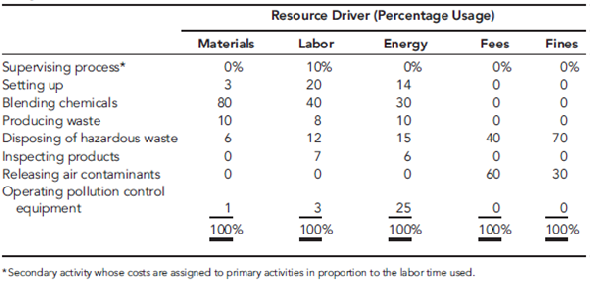

Activity Module

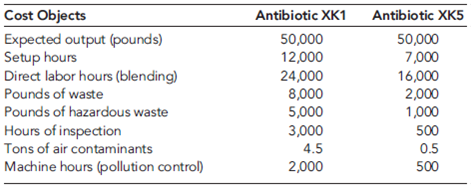

Cost Object Module (Products and Projected Activity Usage)

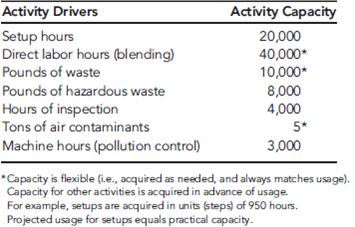

List of Activity Drivers

Required

Following Larry's suggestion, Luis decided to use target costing to help improve new product profitability. Based on analyses by Luis and Doreen, the target prices for XK1 and XK5 are $50 per pound and $35 per pound, respectively. Luis has indicated that any new product should earn a gross profit equal to 20 percent of sales. Based on this information, answer the following:

a. What is the target cost for each product? Given this information, what should be done?

b. Suppose Doreen indicates that sales for each product can be increased by 50 percent if the selling price is lowered by 10 percent. Assuming the same target profit (Luis wants the original target profit per pound maintained), calculate the new target costs. If all non-value-added costs were eliminated, could the target be met? (Calculate the unit cost at the 50,000-unit level.) Now, calculate the effect on total profits under a scenario where non-value-added costs are not eliminated versus a scenario where all non-value-added costs are eliminated. (Include in this analysis any possible increase in sales volume.)

Luis : "You all have received the quarterly financial reports for the last two years. The trends are negative. We are losing market share, profits are decreasing, and our costs seem to be increasing. We need to take actions to increase sales and reduce costs, and we need to do so as quickly as possible. Given our research strengths, it seems to me that our best bet is to grow revenues by introducing new products with proprietary rights. As far as costs are concerned, we need to improve our performance on that dimension as well. Lower per-unit costs for new and existing products are needed. Any suggestions?"

Troy : "For our products, our ability to control costs resides in development-my area-rather than manufacturing. We probably need to pay more attention to product and process design issues to ensure a reasonably level per-unit cost. Revenues are also affected in this stage. Once we patent a drug, the clock begins to tick, and we need to reduce time to market. Significantly, reducing time to market will allow us to generate revenues for a longer period of time than we are currently experiencing. It would also be helpful if we could reduce the cycle time for product development. Both actions would increase revenues. Finally, we can increase revenues by increasing the volume of new products."

Johnny : "There is a lot of merit to the observation that cost reduction opportunities reside mostly in product development. Once a drug is approved, its approval includes the manufacturing process. Any future changes in the manufacturing process require approval from the U.S. Food and Drug Administration. Because of this, we have been reluctant, historically, to engage in process improvement or reengineering. However, I wonder if we shouldn't reconsider this longstanding policy. Some of the quality problems we have could be corrected by changing some of our existing processes, and the costs saved may easily exceed any cost incurred from seeking FDA approval. I think our quality costs are at least 15 percent of sales. That's a lot of opportunity for improvement."

Kathy : "I agree that cost reduction-both in the product development stage and the manufacturing stage-should be a key strategic theme. The environmental area also offers some very good opportunities. A recent pollution prevention act passed by the legislature requires that we calculate the costs of generating hazardous substances for each process. This act was the incentive we needed to begin developing an environmental cost management system. The results so far indicate that environmental costs are much more than we realized. They are estimated to be in the range of 20 to 30 percent of total operating costs. Environmental costs can be reduced by such things as computerizing chemical inventory, eliminating the use of chlorinated solvents and other hazardous materials, reducing our use of virgin feedstocks, and redesigning processes and products so that we can reduce toxic residue release. We can really have a positive environmental impact while simultaneously reducing costs if more attention is paid to environmental issues during product development."

Doreen : "I like what I am hearing because I think that it also affects our ability to increase market share and revenues. For example, environmental impact is one of our major concerns. Some retail pharmacy chains pay particular attention to green products, and right now we are not competing well. Our environmental image is negative and needs to be improved. I am convinced that doing so will allow us to increase market share. Quality is another important matter. We have had to recall two batches of products during the past two years due to poor quality, and this has hurt our image more than the environmental issue. Improving the processes to avoid these kinds of problems will save us a lot of grief. Product image and reputation are essential to increasing customer satisfaction and market share."

Luis : "We started with the need to improve financial performance by increasing revenues and reducing costs. So far, we have some very good suggestions to help achieve these two objectives, but I have some concerns. First, do we have the talent and capabilities to improve quality and environmental performance? Troy, do your professionals really understand what they need to do to improve process and product designs so that we can see the desired quality and environmental improvements? Also, how can we reduce the cycle time for products and the time to market once patented?"

Troy : "Let me answer those questions in order. First, we probably are lacking the understanding on the design issues. We will need to do some training to help our research scientists and chemical engineers understand the consequences. We may need to hire a couple of professionals who have experience in dealing with these issues. Second, we may need to make cycle time and time to market significant performance measures and reward our people for actions that reduce those measures. Our employees need to align their interests with those of the company. If we can achieve this, we should see more revenue produced per employee."

Luis : "Good. Now, Johnny, tell us about production and quality. Do our manufacturing engineers and production workers need help with environmental and quality issues?"

Johnny : "Without question, training will be needed. Moreover, I really need to hire a couple of quality engineers."

Kathy : "I also think that we need an environmental engineer with experience in pharmaceutical manufacturing processes."

Luis : "Good. We certainly shouldn't ignore the necessary infrastructure to bring about the needed changes. Larry, you have been relatively quiet, what do you think about all this? Do you have any suggestions?"

Larry : "Infrastructure is important. If this is all going to work, timely and accurate information will be needed. It is hard to design products and processes with cost being a significant issue without providing the right kind of cost information. We are in the process of revamping the cost management information system so that it is activity based and so that we can provide quality and environmental cost information. After listening to the comments made here, I might also suggest that we need a strategic measurement system that can be used to align the interests of our employees with our improvement strategy. People need to know what is important, that the important factors are being measured, and that they are going to be evaluated and rewarded based on these factors. Finally, I would encourage the use of target costing to help manage costs during product development. To help you all understand the importance of good information, I have assembled some activity data relating to two new products currently under development. These two products will use the same process, using different setups. The data are organized into resource, activity, and cost object modules with an accompanying list of activity drivers to facilitate the use of an ABC software package recently acquired by Zando."

Resource Module (Projected General Ledger Costs of Manufacturing Process Associated with the Two Products)

Activity Module

Cost Object Module (Products and Projected Activity Usage)

List of Activity Drivers

Required

Following Larry's suggestion, Luis decided to use target costing to help improve new product profitability. Based on analyses by Luis and Doreen, the target prices for XK1 and XK5 are $50 per pound and $35 per pound, respectively. Luis has indicated that any new product should earn a gross profit equal to 20 percent of sales. Based on this information, answer the following:

a. What is the target cost for each product? Given this information, what should be done?

b. Suppose Doreen indicates that sales for each product can be increased by 50 percent if the selling price is lowered by 10 percent. Assuming the same target profit (Luis wants the original target profit per pound maintained), calculate the new target costs. If all non-value-added costs were eliminated, could the target be met? (Calculate the unit cost at the 50,000-unit level.) Now, calculate the effect on total profits under a scenario where non-value-added costs are not eliminated versus a scenario where all non-value-added costs are eliminated. (Include in this analysis any possible increase in sales volume.)

Question

Beauville Furniture Corporation produces sofas, recliners, and lounge chairs. Beauville is located in a medium-sized community in the southeastern part of the United States. It is a major employer in the community. In fact, the economic well-being of the community is tied very strongly to Beauville. Beauville operates a sawmill, a fabric plant, and a furniture plant in the same community.

The sawmill buys logs from independent producers. The sawmill then processes the logs into four grades of lumber: firsts and seconds, No. 1 common, No. 2 common, and No. 3 common. All costs incurred in the mill are common to the four grades of lumber. All four grades of lumber are used by the furniture plant. The mill transfers everything it produces to the furniture plant, and the grades are transferred at cost. Trucks are used to move the lumber from the mill to the furniture plant. Although no outside sales exist, the mill could sell to external customers, and the selling prices of the four grades are known.

The fabric plant is responsible for producing the fabric that is used by the furniture plant. To produce three totally different fabrics (identified by fabric ID codes FB60, FB70, and FB80, respectively), the plant has three separate production operations-one for each fabric. Thus, production of all three fabrics occurs at the same time in different locations in the plant. Each fabric's production operation has two processes: the weaving and pattern process and the coloring and bolting process. In the weaving and pattern process, yarn is used to create yards of fabric with different designs. In the next process, the fabric is dyed, cut into 25-yard sections, and wrapped around cardboard rods to form 25-yard bolts. The bolts are transported by forklift to the furniture plant's Receiving Department. All of the output of the fabric plant is used by the furniture plant (to produce the sofas and chairs). For accounting purposes, the fabric is transferred at cost to the furniture plant.

The furniture plant produces orders for customers on a special-order basis. The customers specify the quantity, style, fabric, lumber grade, and pattern. Typically, jobs are large (involving at least 500 units). The plant has two production departments: Cutting and Assembly. In the Cutting Department, the fabric and wooden frame components are sized and cut. Other components are purchased from external suppliers and are removed from stores as needed for assembly. After the fabric and wooden components are finished for the entire job, they are moved to the Assembly Department. The Assembly Department takes the individual components and assembles the sofas (or chairs).

Beauville Furniture has been in business for over two decades and has a good reputation. However, during the past five years, Beauville experienced eroding profits and declining sales. Bids were increasingly lost (even aggressive bids) on the more popular models. Yet, the company was winning bids on some of the more-difficult-to-produce items. Lance Hays, the owner and manager, was frustrated. He simply couldn't understand how some of his competitors could sell for such low prices. On a common sofa job involving 500 units, Beauville's bids were running $25 per unit, or $12,500 per job more than the winning bids (on average). Yet, on the more difficult items, Beauville's bids were running about $60 per unit less than the next closest bid. Gisela Berling, vice president of finance, was assigned the task of preparing a cost analysis of the company's product lines. Lance wanted to know if the company's costs were excessive. Perhaps the company was being wasteful, and it was simply costing more to produce furniture than it was costing its competitors.

Gisela prepared herself by reading recent literature on cost management and product costing and attending several conferences that explored the same issues. She then reviewed the costing procedures of the company's mill and two plants and did a preliminary assessment of their soundness. The production costs of the mill were common to all lumber grades and were assigned using the physical units method. Since the output and production costs were fairly uniform throughout the year, the mill used an actual costing system. Although Gisela had no difficulty with actual costing, she decided to explore the effects of using the sales-value-at-split-off method. Thus, cost and production data for the mill were gathered so that an analysis could be conducted. The two plants used normal costing systems. The fabric plant used process costing, and the furniture plant used job-order costing. Both plants used plantwide overhead rates based on direct labor hours. Based on her initial reviews, she concluded that the costing procedures for the fabric plant were satisfactory. Essentially, there was no evidence of product diversity. A statistical analysis revealed that about 90 percent of the variability in the plant's overhead cost could be explained by direct labor hours. Thus, the use of a plantwide overhead rate based on direct labor hours seemed justified. What did concern her, though, was the material waste that she observed in the plant. Maybe a standard cost system would be useful for increasing the overall cost efficiency of the plant. Consequently, as part of her report to Lance, she decided to include a description of the fabric plant's costing procedures-at least for one of the fabric types. She also decided to develop a standard cost sheet for the chosen fabric. The furniture plant, however, was a more difficult matter. Product diversity was present and could be causing some distortions in product costs. Furthermore, statistical analysis revealed that only about 40 percent of the variability in overhead cost was explained by the direct labor hours. She decided that additional analysis was needed so that a sound product costing method could be recommended. One possibility would be to increase the number of overhead rates. Thus, she decided to include departmental data so that the effect of moving to departmental rates could be assessed. Finally, she also wanted to explore the possibility of converting the sawmill and fabric plant into profit centers and changing the existing transfer pricing policy.

With the cooperation of the cost accounting manager for the mill and each plant's controller, she gathered the following data for last year:

Sawmill:

Joint manufacturing costs: $900,000

Fabric Plant:

Budgeted overhead: $1,200,000 (50% fixed)

Practical volume (direct labor hours): 120,000 hours

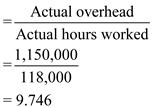

Actual overhead: $1,150,000 (50% fixed)

Actual hours worked:

Departmental data on Fabric FB70 (actual costs and actual outcomes):

*Unitsare measured in yards for the Weaving and Pattern Department and in bolts forthe Coloring and Bolting Department. Note: With the exception of the cardboard bolt rods, materials are added at the beginning of each process. The cost of the rods is relatively insignificant and is included in overhead.

Proposed standard cost sheet for Fabric FB70 (for the Coloring and Bolting Department only):

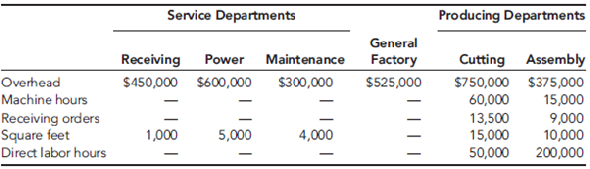

Furniture Plant:

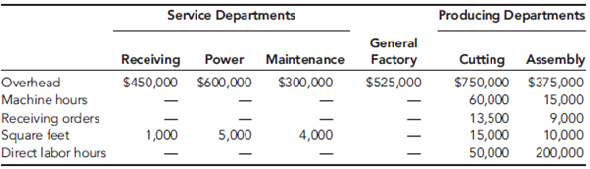

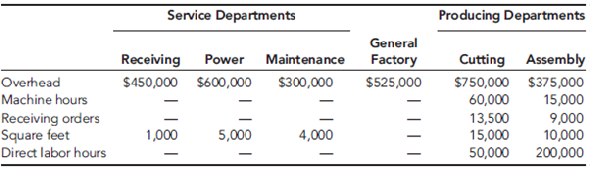

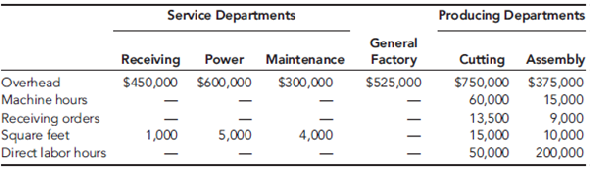

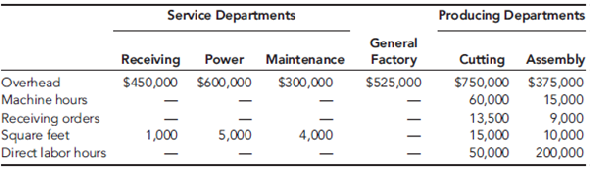

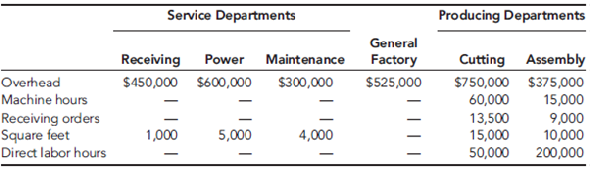

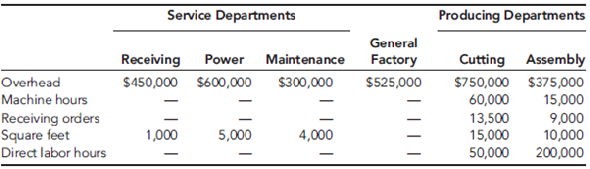

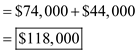

Departmental data (budgeted):

After some discussion with the furniture plant controller, Gisela decided to use machine hours to calculate the overhead rate for the Cutting Department and direct labor hours for the Assembly Department rate (the Cutting Department was more automated than the Assembly Department). As part of her report, she wanted to compare the effects of plantwide rates and departmental rates on the cost of jobs. She wanted to know if overhead costing could be the source of the pricing problems the company was experiencing.

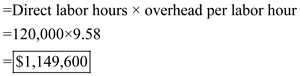

To assess the effect of the different overhead assignment procedures, Gisela decided to examine two prospective jobs. One job, Job A500, could produce 500 sofas, using a frequently requested style and Fabric FB70. Bids on this type of job were being lost more frequently to competitors. The second job, Job B75, would produce 75 specially designed recliners. This job involved a new design and was more difficult for the workers to build. It involved some special cutting requirements and an unfamiliar assembly. Recently, the company seemed to be winning more bids on jobs of this type. To compute the costs of the two jobs, Gisela assembled the following information on the two jobs:

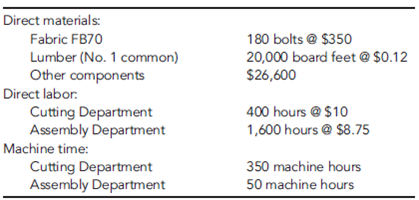

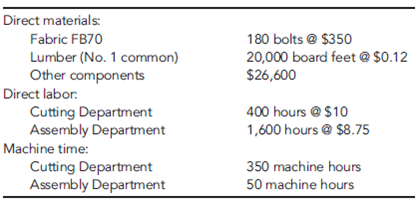

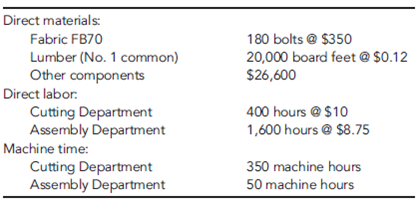

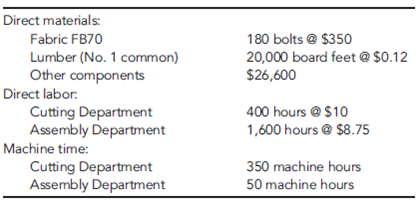

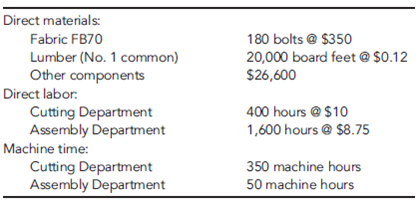

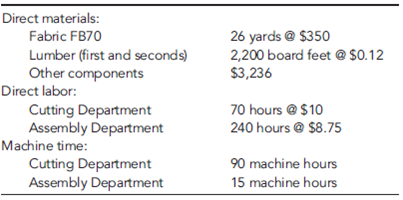

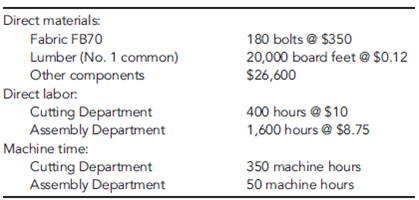

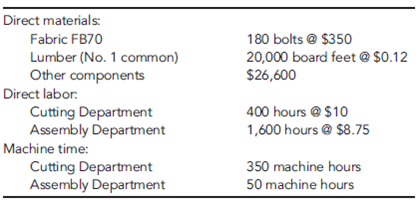

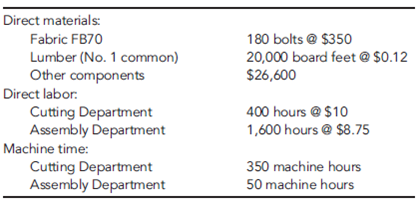

Job A500:

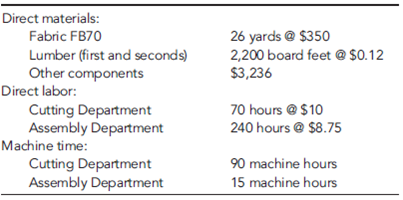

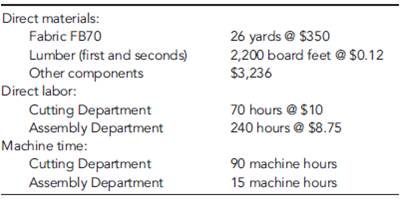

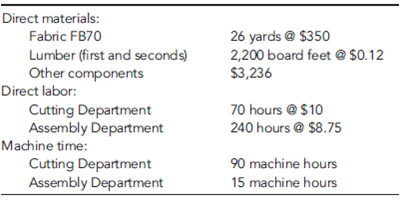

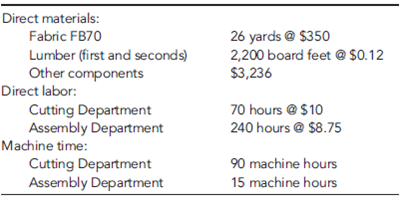

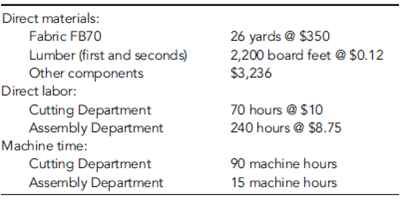

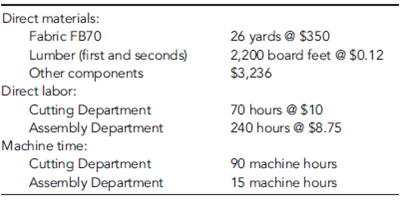

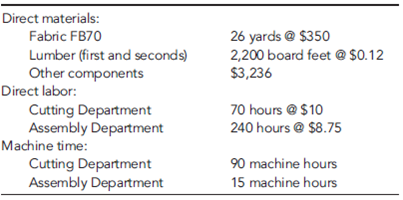

Job B75:

Required

Calculate the plantwide overhead rate for the fabric plant.

The sawmill buys logs from independent producers. The sawmill then processes the logs into four grades of lumber: firsts and seconds, No. 1 common, No. 2 common, and No. 3 common. All costs incurred in the mill are common to the four grades of lumber. All four grades of lumber are used by the furniture plant. The mill transfers everything it produces to the furniture plant, and the grades are transferred at cost. Trucks are used to move the lumber from the mill to the furniture plant. Although no outside sales exist, the mill could sell to external customers, and the selling prices of the four grades are known.

The fabric plant is responsible for producing the fabric that is used by the furniture plant. To produce three totally different fabrics (identified by fabric ID codes FB60, FB70, and FB80, respectively), the plant has three separate production operations-one for each fabric. Thus, production of all three fabrics occurs at the same time in different locations in the plant. Each fabric's production operation has two processes: the weaving and pattern process and the coloring and bolting process. In the weaving and pattern process, yarn is used to create yards of fabric with different designs. In the next process, the fabric is dyed, cut into 25-yard sections, and wrapped around cardboard rods to form 25-yard bolts. The bolts are transported by forklift to the furniture plant's Receiving Department. All of the output of the fabric plant is used by the furniture plant (to produce the sofas and chairs). For accounting purposes, the fabric is transferred at cost to the furniture plant.

The furniture plant produces orders for customers on a special-order basis. The customers specify the quantity, style, fabric, lumber grade, and pattern. Typically, jobs are large (involving at least 500 units). The plant has two production departments: Cutting and Assembly. In the Cutting Department, the fabric and wooden frame components are sized and cut. Other components are purchased from external suppliers and are removed from stores as needed for assembly. After the fabric and wooden components are finished for the entire job, they are moved to the Assembly Department. The Assembly Department takes the individual components and assembles the sofas (or chairs).

Beauville Furniture has been in business for over two decades and has a good reputation. However, during the past five years, Beauville experienced eroding profits and declining sales. Bids were increasingly lost (even aggressive bids) on the more popular models. Yet, the company was winning bids on some of the more-difficult-to-produce items. Lance Hays, the owner and manager, was frustrated. He simply couldn't understand how some of his competitors could sell for such low prices. On a common sofa job involving 500 units, Beauville's bids were running $25 per unit, or $12,500 per job more than the winning bids (on average). Yet, on the more difficult items, Beauville's bids were running about $60 per unit less than the next closest bid. Gisela Berling, vice president of finance, was assigned the task of preparing a cost analysis of the company's product lines. Lance wanted to know if the company's costs were excessive. Perhaps the company was being wasteful, and it was simply costing more to produce furniture than it was costing its competitors.

Gisela prepared herself by reading recent literature on cost management and product costing and attending several conferences that explored the same issues. She then reviewed the costing procedures of the company's mill and two plants and did a preliminary assessment of their soundness. The production costs of the mill were common to all lumber grades and were assigned using the physical units method. Since the output and production costs were fairly uniform throughout the year, the mill used an actual costing system. Although Gisela had no difficulty with actual costing, she decided to explore the effects of using the sales-value-at-split-off method. Thus, cost and production data for the mill were gathered so that an analysis could be conducted. The two plants used normal costing systems. The fabric plant used process costing, and the furniture plant used job-order costing. Both plants used plantwide overhead rates based on direct labor hours. Based on her initial reviews, she concluded that the costing procedures for the fabric plant were satisfactory. Essentially, there was no evidence of product diversity. A statistical analysis revealed that about 90 percent of the variability in the plant's overhead cost could be explained by direct labor hours. Thus, the use of a plantwide overhead rate based on direct labor hours seemed justified. What did concern her, though, was the material waste that she observed in the plant. Maybe a standard cost system would be useful for increasing the overall cost efficiency of the plant. Consequently, as part of her report to Lance, she decided to include a description of the fabric plant's costing procedures-at least for one of the fabric types. She also decided to develop a standard cost sheet for the chosen fabric. The furniture plant, however, was a more difficult matter. Product diversity was present and could be causing some distortions in product costs. Furthermore, statistical analysis revealed that only about 40 percent of the variability in overhead cost was explained by the direct labor hours. She decided that additional analysis was needed so that a sound product costing method could be recommended. One possibility would be to increase the number of overhead rates. Thus, she decided to include departmental data so that the effect of moving to departmental rates could be assessed. Finally, she also wanted to explore the possibility of converting the sawmill and fabric plant into profit centers and changing the existing transfer pricing policy.

With the cooperation of the cost accounting manager for the mill and each plant's controller, she gathered the following data for last year:

Sawmill:

Joint manufacturing costs: $900,000

Fabric Plant:

Budgeted overhead: $1,200,000 (50% fixed)

Practical volume (direct labor hours): 120,000 hours

Actual overhead: $1,150,000 (50% fixed)

Actual hours worked:

Departmental data on Fabric FB70 (actual costs and actual outcomes):

*Unitsare measured in yards for the Weaving and Pattern Department and in bolts forthe Coloring and Bolting Department. Note: With the exception of the cardboard bolt rods, materials are added at the beginning of each process. The cost of the rods is relatively insignificant and is included in overhead.

Proposed standard cost sheet for Fabric FB70 (for the Coloring and Bolting Department only):

Furniture Plant:

Departmental data (budgeted):

After some discussion with the furniture plant controller, Gisela decided to use machine hours to calculate the overhead rate for the Cutting Department and direct labor hours for the Assembly Department rate (the Cutting Department was more automated than the Assembly Department). As part of her report, she wanted to compare the effects of plantwide rates and departmental rates on the cost of jobs. She wanted to know if overhead costing could be the source of the pricing problems the company was experiencing.

To assess the effect of the different overhead assignment procedures, Gisela decided to examine two prospective jobs. One job, Job A500, could produce 500 sofas, using a frequently requested style and Fabric FB70. Bids on this type of job were being lost more frequently to competitors. The second job, Job B75, would produce 75 specially designed recliners. This job involved a new design and was more difficult for the workers to build. It involved some special cutting requirements and an unfamiliar assembly. Recently, the company seemed to be winning more bids on jobs of this type. To compute the costs of the two jobs, Gisela assembled the following information on the two jobs:

Job A500:

Job B75:

Required

Calculate the plantwide overhead rate for the fabric plant.

Question

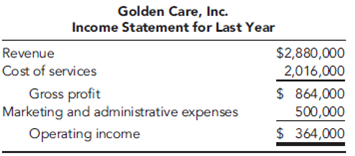

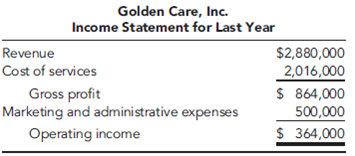

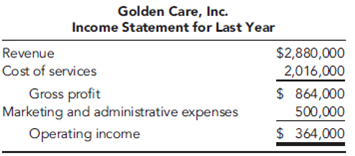

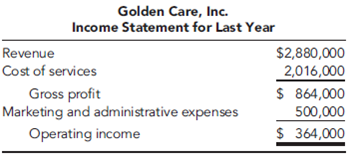

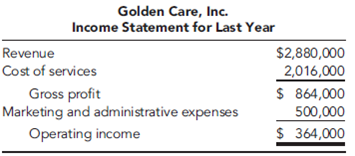

Sabrina Hoffman is founder and CEO of Golden Care, Inc., which owns and operates several assisted- living facilities. The facilities are apartment-style buildings with 25 to 30 one- or two-bedroom apartments. While each apartment has its own complete kitchen, in every building Golden Care offers communal dining options and an on-site nurse who is available 24 hours a day. Residents can choose monthly meal options that include one or two meals per day in the dining room. Residents who require nursing services (e.g., blood pressure monitoring and injections) can receive those services from the nurse. However, Golden Care facilities are not nursing homes, all residents are ambulatory, and custodial care is not an option. In the five years it has been in operation, the company has expanded from one facility to five, located in southwestern cities. The income statement for last year follows.

Sabrina originally got into the business because she had trouble finding adequate facilities for her mother. The concept worked well, and income over the past five years had grown nicely at 20 percent per year. However, Sabrina sensed clouds on the horizon. She knew that the population was aging and that her current clients would be moving to more traditional forms of nursing care. As a result, Sabrina wanted to consider adding one or more nursing homes to Golden Care. These nursing homes would be staffed around the clock with RNs and LPNs. The residents would likely have more severe medical problems and would be confined to beds or wheelchairs. Sabrina knew that quality care of this type was needed. So, she contacted Peter Verdon, her marketing manager, and Bernadette Masters, her accountant, for a brainstorming session.

Peter : "Sabrina, I really like the concept. As you know, several of our facilities have faced seeing their long-term residents move out to local nursing homes. Not only are these homes of lower quality than what we could provide, but losing a resident is heartrending for the staff, as well as for the remaining residents. I like the idea of providing a transition from less care to more."

Bernadette : "I agree with you, Peter. But let's not forget the differences between assisted-living and full-time, nursing-home-type care. Our expenses will really increase."

Sabrina : "That's why I wanted to talk with both of you. As you know, Golden Care's mission statement emphasizes the need to make a profit. We can't continue to serve our residents and provide high- quality care if we don't make enough money to pay our staff a living wage and earn enough of a profit to smooth over the rough patches and continue to improve our business. Could the two of you look into this idea, and get back to me in a week or so?"

Throughout the following week, the three communicated by e-mail. By the end of the week, a number of possibilities had surfaced, and these were summarized in a message from Bernadette to the others.

TO: [email protected], [email protected]

FROM: [email protected]

MESSAGE:

I've compiled the ideas from all of our e-mails into the following list. This may be a good starting point for our meeting tomorrow.

1. Buy an existing nursing home in one of Golden Care's current locations.

2. Buy an existing nursing home in another city.

3. Build a new nursing home facility in one of Golden Care's current locations.

4. Build a new nursing home facility in another city.

5. Build a wing on to an existing Golden Care facility. The Apache Junction facility has sufficient open land for an addition.

The next day, Sabrina, Peter, and Bernadette met again in Sabrina's office.

Sabrina : "I didn't realize there were so many possibilities. Are we going to have to work up numbers on each of them?"

Bernadette : "No, I think we can eliminate a few of them pretty quickly. For example, building a new facility would cost more than the other options, and it would involve the most risk."

Peter : "I agree, and I also think we might eliminate the purchase of an existing nursing home for the same reasons. Also, existing homes would not give us the option of building a facility that is state of the art and meets our needs, and it would lock us into a preexisting patient mix."

Sabrina : "I like that thinking. Let's restrict our attention to Option 5."

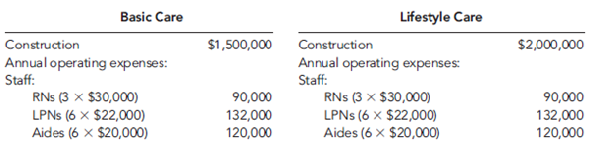

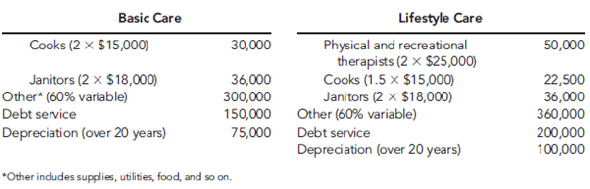

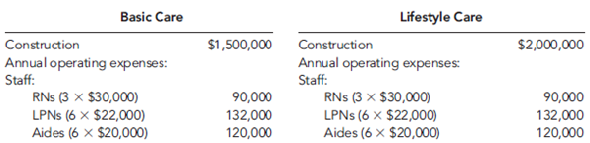

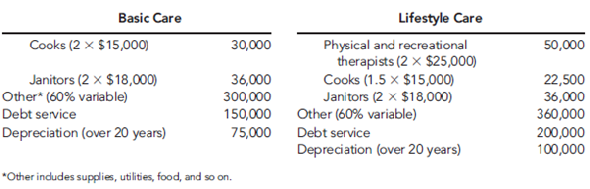

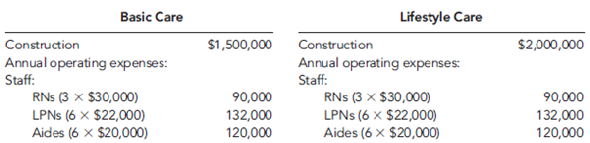

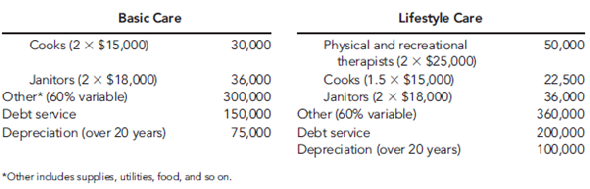

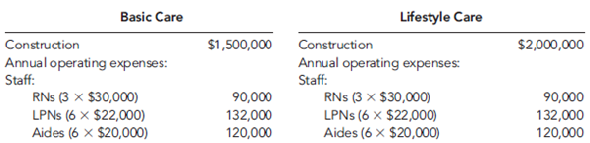

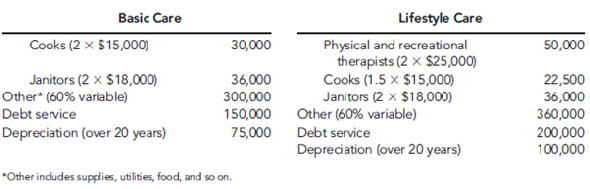

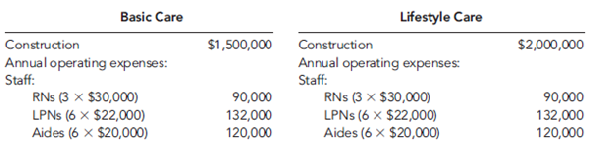

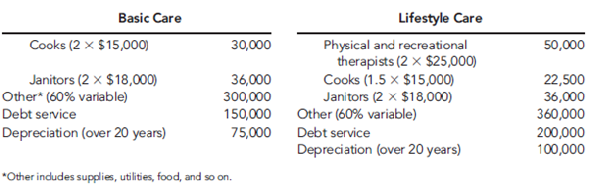

Bernadette : "I thought you might like that option, so Peter and I sketched out two alternatives for an extension of the Apache Junction building. We call the alternatives Basic Care and Lifestyle Care."

Peter : "There are different markets for each type of care. If we want to concentrate on Medicare and Medicaid patients, the reimbursement is lower, and we would want to offer the Basic Care option. Private insurance and private-pay patients could afford more services; if we are marketing to these patients, we could offer the Lifestyle Care option. Both alternatives provide high-quality nursing care. Basic Care concentrates on the quality nursing and maintenance activities. For example, the addition would have 25 double rooms, two nursing stations, two recreation rooms, a treatment room, and an office. The Lifestyle Care option adds physical and recreational therapy with a specially equipped gym and pool. That addition would have 30 single rooms, two nursing stations, a recreation room, a swimming pool, a hydrotherapy spa and gym, a treatment room, and an office. In each case, there would be cable TV and telephone hookups in each room and a buffer area between the nursing home and the apartments."

Sabrina : "Why the buffer area? Won't that add unnecessary cost?"

Peter : "It adds cost, but it will be well worth it. Sabrina, you must remember that the nursing home patients are different from the apartment residents. Some of the patients will have advanced dementia. We'll lose apartment residents in a hurry if they have to be reminded every day of what might be in store for them later on."

Sabrina : "I see your point. Bernadette, what will these two plans cost? I'll tell you right now that I like the Lifestyle Care option better. It fits with our history of doing whatever we can to make life better for our residents."

Bernadette : "I've checked into the costs of putting on a new wing and operating both alternatives. Here's a listing."

"In both cases, total administrative costs for Golden Care would increase by $30,000 per year. This seems high, but the increased legal and insurance requirements will add significantly more paperwork and accounting."

Sabrina : "All this sounds reasonable, but why is reimbursement such an important factor?"

Peter : "Well, if you admit Medicaid patients, the state will reimburse at most $30,000 per year. Private insurance policies will pay roughly $46,000 per year. We can charge up to about $65,000 for private patients, but this type of care is so expensive that many of these patients exhaust their funds and go on Medicaid. The nice aspect of Medicaid is that we can be virtually assured that we will operate at capacity."

Sabrina : "Can we cross that bridge when we come to it?"

Peter : " No, not really. Once the patient is a resident of our facility, it is hard to evict him or her. Also, while it is legal to force patients out before they go on Medicaid and to refuse to accept Medicaid patients, once we do accept Medicaid patients, we are prevented by law from evicting them-no matter how high our costs go."

Sabrina : "OK, it looks as if we have some hard work ahead of us to decide whether or not to get into this line of business."

Required

How did Sabrina, Bernadette, and Peter use the tactical decision-making model of Chapter 17?

Sabrina originally got into the business because she had trouble finding adequate facilities for her mother. The concept worked well, and income over the past five years had grown nicely at 20 percent per year. However, Sabrina sensed clouds on the horizon. She knew that the population was aging and that her current clients would be moving to more traditional forms of nursing care. As a result, Sabrina wanted to consider adding one or more nursing homes to Golden Care. These nursing homes would be staffed around the clock with RNs and LPNs. The residents would likely have more severe medical problems and would be confined to beds or wheelchairs. Sabrina knew that quality care of this type was needed. So, she contacted Peter Verdon, her marketing manager, and Bernadette Masters, her accountant, for a brainstorming session.

Peter : "Sabrina, I really like the concept. As you know, several of our facilities have faced seeing their long-term residents move out to local nursing homes. Not only are these homes of lower quality than what we could provide, but losing a resident is heartrending for the staff, as well as for the remaining residents. I like the idea of providing a transition from less care to more."

Bernadette : "I agree with you, Peter. But let's not forget the differences between assisted-living and full-time, nursing-home-type care. Our expenses will really increase."

Sabrina : "That's why I wanted to talk with both of you. As you know, Golden Care's mission statement emphasizes the need to make a profit. We can't continue to serve our residents and provide high- quality care if we don't make enough money to pay our staff a living wage and earn enough of a profit to smooth over the rough patches and continue to improve our business. Could the two of you look into this idea, and get back to me in a week or so?"

Throughout the following week, the three communicated by e-mail. By the end of the week, a number of possibilities had surfaced, and these were summarized in a message from Bernadette to the others.

TO: [email protected], [email protected]

FROM: [email protected]

MESSAGE:

I've compiled the ideas from all of our e-mails into the following list. This may be a good starting point for our meeting tomorrow.

1. Buy an existing nursing home in one of Golden Care's current locations.

2. Buy an existing nursing home in another city.

3. Build a new nursing home facility in one of Golden Care's current locations.

4. Build a new nursing home facility in another city.

5. Build a wing on to an existing Golden Care facility. The Apache Junction facility has sufficient open land for an addition.

The next day, Sabrina, Peter, and Bernadette met again in Sabrina's office.

Sabrina : "I didn't realize there were so many possibilities. Are we going to have to work up numbers on each of them?"

Bernadette : "No, I think we can eliminate a few of them pretty quickly. For example, building a new facility would cost more than the other options, and it would involve the most risk."

Peter : "I agree, and I also think we might eliminate the purchase of an existing nursing home for the same reasons. Also, existing homes would not give us the option of building a facility that is state of the art and meets our needs, and it would lock us into a preexisting patient mix."

Sabrina : "I like that thinking. Let's restrict our attention to Option 5."

Bernadette : "I thought you might like that option, so Peter and I sketched out two alternatives for an extension of the Apache Junction building. We call the alternatives Basic Care and Lifestyle Care."

Peter : "There are different markets for each type of care. If we want to concentrate on Medicare and Medicaid patients, the reimbursement is lower, and we would want to offer the Basic Care option. Private insurance and private-pay patients could afford more services; if we are marketing to these patients, we could offer the Lifestyle Care option. Both alternatives provide high-quality nursing care. Basic Care concentrates on the quality nursing and maintenance activities. For example, the addition would have 25 double rooms, two nursing stations, two recreation rooms, a treatment room, and an office. The Lifestyle Care option adds physical and recreational therapy with a specially equipped gym and pool. That addition would have 30 single rooms, two nursing stations, a recreation room, a swimming pool, a hydrotherapy spa and gym, a treatment room, and an office. In each case, there would be cable TV and telephone hookups in each room and a buffer area between the nursing home and the apartments."

Sabrina : "Why the buffer area? Won't that add unnecessary cost?"

Peter : "It adds cost, but it will be well worth it. Sabrina, you must remember that the nursing home patients are different from the apartment residents. Some of the patients will have advanced dementia. We'll lose apartment residents in a hurry if they have to be reminded every day of what might be in store for them later on."

Sabrina : "I see your point. Bernadette, what will these two plans cost? I'll tell you right now that I like the Lifestyle Care option better. It fits with our history of doing whatever we can to make life better for our residents."

Bernadette : "I've checked into the costs of putting on a new wing and operating both alternatives. Here's a listing."

"In both cases, total administrative costs for Golden Care would increase by $30,000 per year. This seems high, but the increased legal and insurance requirements will add significantly more paperwork and accounting."

Sabrina : "All this sounds reasonable, but why is reimbursement such an important factor?"

Peter : "Well, if you admit Medicaid patients, the state will reimburse at most $30,000 per year. Private insurance policies will pay roughly $46,000 per year. We can charge up to about $65,000 for private patients, but this type of care is so expensive that many of these patients exhaust their funds and go on Medicaid. The nice aspect of Medicaid is that we can be virtually assured that we will operate at capacity."

Sabrina : "Can we cross that bridge when we come to it?"

Peter : " No, not really. Once the patient is a resident of our facility, it is hard to evict him or her. Also, while it is legal to force patients out before they go on Medicaid and to refuse to accept Medicaid patients, once we do accept Medicaid patients, we are prevented by law from evicting them-no matter how high our costs go."

Sabrina : "OK, it looks as if we have some hard work ahead of us to decide whether or not to get into this line of business."

Required

How did Sabrina, Bernadette, and Peter use the tactical decision-making model of Chapter 17?

Question

Beauville Furniture Corporation produces sofas, recliners, and lounge chairs. Beauville is located in a medium-sized community in the southeastern part of the United States. It is a major employer in the community. In fact, the economic well-being of the community is tied very strongly to Beauville. Beauville operates a sawmill, a fabric plant, and a furniture plant in the same community.

The sawmill buys logs from independent producers. The sawmill then processes the logs into four grades of lumber: firsts and seconds, No. 1 common, No. 2 common, and No. 3 common. All costs incurred in the mill are common to the four grades of lumber. All four grades of lumber are used by the furniture plant. The mill transfers everything it produces to the furniture plant, and the grades are transferred at cost. Trucks are used to move the lumber from the mill to the furniture plant. Although no outside sales exist, the mill could sell to external customers, and the selling prices of the four grades are known.

The fabric plant is responsible for producing the fabric that is used by the furniture plant. To produce three totally different fabrics (identified by fabric ID codes FB60, FB70, and FB80, respectively), the plant has three separate production operations-one for each fabric. Thus, production of all three fabrics occurs at the same time in different locations in the plant. Each fabric's production operation has two processes: the weaving and pattern process and the coloring and bolting process. In the weaving and pattern process, yarn is used to create yards of fabric with different designs. In the next process, the fabric is dyed, cut into 25-yard sections, and wrapped around cardboard rods to form 25-yard bolts. The bolts are transported by forklift to the furniture plant's Receiving Department. All of the output of the fabric plant is used by the furniture plant (to produce the sofas and chairs). For accounting purposes, the fabric is transferred at cost to the furniture plant.

The furniture plant produces orders for customers on a special-order basis. The customers specify the quantity, style, fabric, lumber grade, and pattern. Typically, jobs are large (involving at least 500 units). The plant has two production departments: Cutting and Assembly. In the Cutting Department, the fabric and wooden frame components are sized and cut. Other components are purchased from external suppliers and are removed from stores as needed for assembly. After the fabric and wooden components are finished for the entire job, they are moved to the Assembly Department. The Assembly Department takes the individual components and assembles the sofas (or chairs).

Beauville Furniture has been in business for over two decades and has a good reputation. However, during the past five years, Beauville experienced eroding profits and declining sales. Bids were increasingly lost (even aggressive bids) on the more popular models. Yet, the company was winning bids on some of the more-difficult-to-produce items. Lance Hays, the owner and manager, was frustrated. He simply couldn't understand how some of his competitors could sell for such low prices. On a common sofa job involving 500 units, Beauville's bids were running $25 per unit, or $12,500 per job more than the winning bids (on average). Yet, on the more difficult items, Beauville's bids were running about $60 per unit less than the next closest bid. Gisela Berling, vice president of finance, was assigned the task of preparing a cost analysis of the company's product lines. Lance wanted to know if the company's costs were excessive. Perhaps the company was being wasteful, and it was simply costing more to produce furniture than it was costing its competitors.

Gisela prepared herself by reading recent literature on cost management and product costing and attending several conferences that explored the same issues. She then reviewed the costing procedures of the company's mill and two plants and did a preliminary assessment of their soundness. The production costs of the mill were common to all lumber grades and were assigned using the physical units method. Since the output and production costs were fairly uniform throughout the year, the mill used an actual costing system. Although Gisela had no difficulty with actual costing, she decided to explore the effects of using the sales-value-at-split-off method. Thus, cost and production data for the mill were gathered so that an analysis could be conducted. The two plants used normal costing systems. The fabric plant used process costing, and the furniture plant used job-order costing. Both plants used plantwide overhead rates based on direct labor hours. Based on her initial reviews, she concluded that the costing procedures for the fabric plant were satisfactory. Essentially, there was no evidence of product diversity. A statistical analysis revealed that about 90 percent of the variability in the plant's overhead cost could be explained by direct labor hours. Thus, the use of a plantwide overhead rate based on direct labor hours seemed justified. What did concern her, though, was the material waste that she observed in the plant. Maybe a standard cost system would be useful for increasing the overall cost efficiency of the plant. Consequently, as part of her report to Lance, she decided to include a description of the fabric plant's costing procedures-at least for one of the fabric types. She also decided to develop a standard cost sheet for the chosen fabric. The furniture plant, however, was a more difficult matter. Product diversity was present and could be causing some distortions in product costs. Furthermore, statistical analysis revealed that only about 40 percent of the variability in overhead cost was explained by the direct labor hours. She decided that additional analysis was needed so that a sound product costing method could be recommended. One possibility would be to increase the number of overhead rates. Thus, she decided to include departmental data so that the effect of moving to departmental rates could be assessed. Finally, she also wanted to explore the possibility of converting the sawmill and fabric plant into profit centers and changing the existing transfer pricing policy.

With the cooperation of the cost accounting manager for the mill and each plant's controller, she gathered the following data for last year:

Sawmill:

Joint manufacturing costs: $900,000

Fabric Plant:

Budgeted overhead: $1,200,000 (50% fixed)

Practical volume (direct labor hours): 120,000 hours

Actual overhead: $1,150,000 (50% fixed)

Actual hours worked:

Departmental data on Fabric FB70 (actual costs and actual outcomes):

*Unitsare measured in yards for the Weaving and Pattern Department and in bolts forthe Coloring and Bolting Department. Note: With the exception of the cardboard bolt rods, materials are added at the beginning of each process. The cost of the rods is relatively insignificant and is included in overhead.

Proposed standard cost sheet for Fabric FB70 (for the Coloring and Bolting Department only):

Furniture Plant:

Departmental data (budgeted):

After some discussion with the furniture plant controller, Gisela decided to use machine hours to calculate the overhead rate for the Cutting Department and direct labor hours for the Assembly Department rate (the Cutting Department was more automated than the Assembly Department). As part of her report, she wanted to compare the effects of plantwide rates and departmental rates on the cost of jobs. She wanted to know if overhead costing could be the source of the pricing problems the company was experiencing.

To assess the effect of the different overhead assignment procedures, Gisela decided to examine two prospective jobs. One job, Job A500, could produce 500 sofas, using a frequently requested style and Fabric FB70. Bids on this type of job were being lost more frequently to competitors. The second job, Job B75, would produce 75 specially designed recliners. This job involved a new design and was more difficult for the workers to build. It involved some special cutting requirements and an unfamiliar assembly. Recently, the company seemed to be winning more bids on jobs of this type. To compute the costs of the two jobs, Gisela assembled the following information on the two jobs:

Job A500:

Job B75:

Required

Calculate the amount of under- or overapplied overhead for the fabric plant.

The sawmill buys logs from independent producers. The sawmill then processes the logs into four grades of lumber: firsts and seconds, No. 1 common, No. 2 common, and No. 3 common. All costs incurred in the mill are common to the four grades of lumber. All four grades of lumber are used by the furniture plant. The mill transfers everything it produces to the furniture plant, and the grades are transferred at cost. Trucks are used to move the lumber from the mill to the furniture plant. Although no outside sales exist, the mill could sell to external customers, and the selling prices of the four grades are known.

The fabric plant is responsible for producing the fabric that is used by the furniture plant. To produce three totally different fabrics (identified by fabric ID codes FB60, FB70, and FB80, respectively), the plant has three separate production operations-one for each fabric. Thus, production of all three fabrics occurs at the same time in different locations in the plant. Each fabric's production operation has two processes: the weaving and pattern process and the coloring and bolting process. In the weaving and pattern process, yarn is used to create yards of fabric with different designs. In the next process, the fabric is dyed, cut into 25-yard sections, and wrapped around cardboard rods to form 25-yard bolts. The bolts are transported by forklift to the furniture plant's Receiving Department. All of the output of the fabric plant is used by the furniture plant (to produce the sofas and chairs). For accounting purposes, the fabric is transferred at cost to the furniture plant.

The furniture plant produces orders for customers on a special-order basis. The customers specify the quantity, style, fabric, lumber grade, and pattern. Typically, jobs are large (involving at least 500 units). The plant has two production departments: Cutting and Assembly. In the Cutting Department, the fabric and wooden frame components are sized and cut. Other components are purchased from external suppliers and are removed from stores as needed for assembly. After the fabric and wooden components are finished for the entire job, they are moved to the Assembly Department. The Assembly Department takes the individual components and assembles the sofas (or chairs).

Beauville Furniture has been in business for over two decades and has a good reputation. However, during the past five years, Beauville experienced eroding profits and declining sales. Bids were increasingly lost (even aggressive bids) on the more popular models. Yet, the company was winning bids on some of the more-difficult-to-produce items. Lance Hays, the owner and manager, was frustrated. He simply couldn't understand how some of his competitors could sell for such low prices. On a common sofa job involving 500 units, Beauville's bids were running $25 per unit, or $12,500 per job more than the winning bids (on average). Yet, on the more difficult items, Beauville's bids were running about $60 per unit less than the next closest bid. Gisela Berling, vice president of finance, was assigned the task of preparing a cost analysis of the company's product lines. Lance wanted to know if the company's costs were excessive. Perhaps the company was being wasteful, and it was simply costing more to produce furniture than it was costing its competitors.