Deck 34: Management and Dissolution of a Corporation

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/28

Play

Full screen (f)

Deck 34: Management and Dissolution of a Corporation

1

Explain how a corporation can perform business transactions as an artificial being.

Corporation as Artificial Being:

Corporations are manifestations of law and created by individuals through law. Corporations are not real being, but artificial beings that are used by people in the course of business.

Individuals act as agents of the corporation and hold the trust of the corporation as with other individuals under law.

In short, corporations perform business transactions as artificial beings through individuals.

Corporations are manifestations of law and created by individuals through law. Corporations are not real being, but artificial beings that are used by people in the course of business.

Individuals act as agents of the corporation and hold the trust of the corporation as with other individuals under law.

In short, corporations perform business transactions as artificial beings through individuals.

2

Business Organization

East Park Limited Partnership signed a $9 million note. Before the note was due, Joseph Della Ratta, the general partner issued a "capital call" to try to squeeze out some of the limited partners. He informed them East Park could not pay the note, so they would have to pay their proportionate shares of the balance. He said he would try to refinance the note but did not. Some partners said they were withdrawing from East Park before the loan due date. Della Ratta responded that they would forfeit their interests in East Park if they did not pay and accelerated the capital call to a date prior to the limited partners' withdrawal date. The withdrawing partners sued. Must they pay the capital call or lose their interests in East Park? [ Della Ratta v. Larkin , 856 A.2d 643 (Md.)]

East Park Limited Partnership signed a $9 million note. Before the note was due, Joseph Della Ratta, the general partner issued a "capital call" to try to squeeze out some of the limited partners. He informed them East Park could not pay the note, so they would have to pay their proportionate shares of the balance. He said he would try to refinance the note but did not. Some partners said they were withdrawing from East Park before the loan due date. Della Ratta responded that they would forfeit their interests in East Park if they did not pay and accelerated the capital call to a date prior to the limited partners' withdrawal date. The withdrawing partners sued. Must they pay the capital call or lose their interests in East Park? [ Della Ratta v. Larkin , 856 A.2d 643 (Md.)]

Capital call:

It refers to the right of an investment firm to ask for payment of the money promised by the investors.

For example: when mutual fund companies receive an investment from a customer, they often invest borrowed money instead of the investor's money. When the fund acquires a certain extent of capital then the borrowed money is paid by issuing a capital call.

In this case, a note of $9 million is signed by EP Limited partnership. The general partner issued capital clause for squeezing some limited partners. But the withdrawing partners filled a case for this against EP Limited partnership.

In this case, the limited partners should try to retain their interests in the fund and they should try to pay the capital call.

This is due to the reason that company called for a capital call in order to flush out the limited partners. By acquiring the interests of the limited partners the company's interests will grow.

The limited partners can avoid this by paying off the capital call.

It refers to the right of an investment firm to ask for payment of the money promised by the investors.

For example: when mutual fund companies receive an investment from a customer, they often invest borrowed money instead of the investor's money. When the fund acquires a certain extent of capital then the borrowed money is paid by issuing a capital call.

In this case, a note of $9 million is signed by EP Limited partnership. The general partner issued capital clause for squeezing some limited partners. But the withdrawing partners filled a case for this against EP Limited partnership.

In this case, the limited partners should try to retain their interests in the fund and they should try to pay the capital call.

This is due to the reason that company called for a capital call in order to flush out the limited partners. By acquiring the interests of the limited partners the company's interests will grow.

The limited partners can avoid this by paying off the capital call.

3

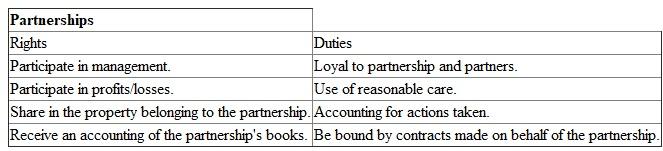

Manual Moses, a new lawyer, put an ad in a law journal requesting a mentorship opportunity with an experienced lawyer so he could get trial experience. Laurence Savedoff responded to the ad. Moses referred two cases to Savedoff's office, conducted some depositions in Savedoff's cases, and drafted some documents for Savedoff. Moses received some payments from Savedoff. Four years later, after the payments ceased, Moses sued Savedoff, alleging Savedoff had proposed they work as partners in a law practice and share equally in the profits from the cases they worked on together. Moses claimed they had an oral partnership agreement. Savedoff alleged that since there was no evidence they shared earnings equally, that Moses shared in law firm losses or expenses, or that Moses contributed capital, there was no evidence of a partnership. What should the court hold? [Moses v. Savedoff, 947 N.Y.S.2d 419 (N.Y. App. Div.)]

Rights and Duties in a Partnership:

The rights and duties of a partner in a partnership are shown in Table 1:

Table 1

Legal Reasoning:

Legal Reasoning:

In Moses v. Savedoff , 96 A.D.3d 466, 947 N.Y.S.2d 419, 2012 NY Sip Op 4400 (2012), the appellate court dismissed Moses' claim of oral partnership or any claim of partnership according to Moses' deposition.

Further, the court stated an absence of agreement to share profits and losses. The court noted that there were a couple of cases that Moses had a claim for fees, but nothing more.Therefore, the court should hold that NO PARTNERSHIP was formed between the parties.

The rights and duties of a partner in a partnership are shown in Table 1:

Table 1

Legal Reasoning: In Moses v. Savedoff , 96 A.D.3d 466, 947 N.Y.S.2d 419, 2012 NY Sip Op 4400 (2012), the appellate court dismissed Moses' claim of oral partnership or any claim of partnership according to Moses' deposition.

Further, the court stated an absence of agreement to share profits and losses. The court noted that there were a couple of cases that Moses had a claim for fees, but nothing more.Therefore, the court should hold that NO PARTNERSHIP was formed between the parties.

4

When TVG Network entered into a license agreement with Youbet.com, TVG received the right to purchase enough Youbet common stock to own 51 percent. Youbet was required "to use its best efforts" to allow TVG to designate directors to Youbet's board based on TVG's stock ownership. Youbet agreed not to "avoid or seek to avoid the observance or performance of any of the terms... hereunder... or take any act which is inconsistent with the rights granted to" TVG. Youbet hired a consulting firm to help develop a strategy regarding TVG's potential 51 percent ownership. In numerous meetings and documents, a strategy to discourage TVG from purchasing 51 percent by staggering the terms of the board and requiring a super majority of stockholders to change the bylaws was discussed. The Youbet board set an annual meeting to make these changes to the bylaws. It sent out proxy notices. These notices stated that the changes were to promote continuity and stability. They did not mention TVG or its potential 51 percent ownership. TVG sued, alleging that the proxy notices were misleading and that the board had breached its duty to disclose material information fully and fairly to the stockholders. Did TVG state a good case?

Unlock Deck

Unlock for access to all 28 flashcards in this deck.

Unlock Deck

k this deck

5

Vincent Meli was president of Flint Cold Storage (Flint) corporation, and his wife, Pauline, was secretary. Flint bought a life insurance policy on Vincent from Metropolitan Life Insurance Company (MetLife). Sometime later, Flint was dissolved. Twenty-five years after the dissolution, MetLife converted from a mutual insurance company owned by its policyholders, to a stock insurance company. As a result, MetLife had $188,000 payable to Flint, which it sent to the state unclaimed property office. Vincent died three years later. Pauline learned of the unclaimed $188,000 and tried to claim it in her capacity as an officer of a dissolved corporation. The state denied Pauline's claim, so she sued on behalf of Flint, alleging that although it had been dissolved 32 years previously, it had retained the right to sue. Did Flint have the right to sue for the funds?

Unlock Deck

Unlock for access to all 28 flashcards in this deck.

Unlock Deck

k this deck

6

May the management of a corporation legally solicit proxies for candidates selected by the board of directors? Explain.

Unlock Deck

Unlock for access to all 28 flashcards in this deck.

Unlock Deck

k this deck

7

How do directors directly control a corporation?

Unlock Deck

Unlock for access to all 28 flashcards in this deck.

Unlock Deck

k this deck

8

Business Organization

Morgan Joseph Holdings Inc. was organized to do investment banking and secured much of its initial funding from the sale of preferred shares of stock. The rights of the preferred stockholders were specified in Morgan Joseph Holding's certificate of incorporation. The certificate required Morgan Joseph to automatically redeem the Series A Preferred Stock if certain events, such as the merger of the company, occurred. The redemption value was to be $100 per share in such event. Moreover, the information material used to market the Series A Preferred Stock to investors supported the understanding that a redemption of Series A Preferred Stock would occur under certain circumstances. Almost ten years after its founding, Morgan Joseph Holdings merged with another investment bank. The newly created entity issued new Series A Preferred Stock and sought to exchange the new stock for Morgan Joseph' sold Series A Preferred Stock. The preferred stockholders sued, claiming that the automatic redemption provision in the certificate of incorporation should be considered when appraising the value of their old Series A Preferred Stock. Should the court consider the language of the certificate of incorporation when appraising the value of the Series A Preferred Stock? [ Shiftan v. Morgan Joseph Holding Inc. , 57 A.3d 928 (Del. Ch.)]

Morgan Joseph Holdings Inc. was organized to do investment banking and secured much of its initial funding from the sale of preferred shares of stock. The rights of the preferred stockholders were specified in Morgan Joseph Holding's certificate of incorporation. The certificate required Morgan Joseph to automatically redeem the Series A Preferred Stock if certain events, such as the merger of the company, occurred. The redemption value was to be $100 per share in such event. Moreover, the information material used to market the Series A Preferred Stock to investors supported the understanding that a redemption of Series A Preferred Stock would occur under certain circumstances. Almost ten years after its founding, Morgan Joseph Holdings merged with another investment bank. The newly created entity issued new Series A Preferred Stock and sought to exchange the new stock for Morgan Joseph' sold Series A Preferred Stock. The preferred stockholders sued, claiming that the automatic redemption provision in the certificate of incorporation should be considered when appraising the value of their old Series A Preferred Stock. Should the court consider the language of the certificate of incorporation when appraising the value of the Series A Preferred Stock? [ Shiftan v. Morgan Joseph Holding Inc. , 57 A.3d 928 (Del. Ch.)]

Unlock Deck

Unlock for access to all 28 flashcards in this deck.

Unlock Deck

k this deck

9

Archon Corp. issued preferred stock called Exchangeable Preferred Stock (EPS). The certificate stated EPS would have a liquidation preference of $2.14 per share plus accrued and unpaid dividends. The dividends were to be paid twice yearly and be cumulative at the initial rate of 8 percent of $2.14 plus accrued but unpaid dividends. For the first three years Archon could pay dividends in EPS shares instead of cash. Beginning in the fifth year, the dividend rate was to increase to 11 percent and additionally increase.5 percent each six months to a maximum of 16 percent. For the first three years, dividend payments were in EPS shares. After that, the dividends accrued and were not paid in cash. The EPS shares were redeemable by Archon at any time, and thirteen years after issuing them, Archon notified the holders that it would redeem them for $5.241 per share, saying that included all accrued dividends. That number reflected the correct percentage dividend, but only on $2.14, not on the unpaid dividends. A group of holders of EPS shares sued Archon, saying that because the shares were cumulative, and the dividend accrued on unpaid dividends, the percentage each dividend payment period should be multiplied by $2.14 PLUS the accrued, unpaid dividends. Figuring that way, total accrued and unpaid dividends were $6.55 per share, so they alleged that the redemption price should be $2.14 plus $6.55 or $8.69 per share. Should dividends be figured on only $2.14 for each payment period, or should they be figured on $2.14 plus accrued, unpaid dividends? [D.E. Shaw Laminar Portfolios, LLC v. Archon Corp., 755 F.Supp.2d 1122 (D. Nev.)]

Unlock Deck

Unlock for access to all 28 flashcards in this deck.

Unlock Deck

k this deck

10

How does the Sarbanes-Oxley Act expand the liability of corporate officers?

Unlock Deck

Unlock for access to all 28 flashcards in this deck.

Unlock Deck

k this deck

11

Hilb, Rogal Hamilton Company of Atlanta (HRH) bought Hugh Holley's independent insurance brokerage and made him a vice president of HRH. Holley earned a salary and bonuses for selling professional liability insurance to clients needing specialized policies. He resigned from HRH and began working for a competing brokerage the next business day. Without HRH's knowledge, two months before he resigned from HRH, Holley had gotten approval from an existing client to appoint him as the client's contact at the competing brokerage. He had established an e-mail account and telephone number at the competitor and had printed conference invitations listing him as an employee of the competitor. He provided price benchmarking information to the competitor, offered to share techniques to reduce premiums for clients, and offered information to the competitor about a potential broker acquisition prospect. HRH sued Holley for breach of fiduciary duty. Had he breached his fiduciary duty?

Unlock Deck

Unlock for access to all 28 flashcards in this deck.

Unlock Deck

k this deck

12

The owner of Central Plains, Joe Skeith, suggested to David Tate of C.J. Tate Sons that Tate work with Central Plains on a job and they would share the profits. They both supplied equipment at the site: Tate provided the bonding, hired the workers, and did all the payroll paperwork; Skeith supervised on the job, set the working hours, and arranged for housing and transportation. Both obtained workers' compensation insurance. Tate hired Dennis Hickson, who usually worked for Central. One day after being paid, Hickson and his coworker roommate, L, went to dinner and then a club. L got aggressive toward other patrons, so Skeith asked Hickson and another to take L to his motel room. When Hickson later returned, L and a woman were in the room. L and the woman left. Hickson went to sleep but let L in when he returned. The next thing Hickson remembered was waking to find L attacking him. Hickson was stabbed. Hickson filed a workers' compensation claim against Central, and Central moved to add Tate, alleging Tate was Hickson's employer. Tate alleged Hickson was an employee of a joint venture of Central and Tate. Who was Hickson's employer? [Central Plains Const. v. Hickson, 959 P.2d 998 (Okla. Ct. App.)]

Unlock Deck

Unlock for access to all 28 flashcards in this deck.

Unlock Deck

k this deck

13

What is normally a quorum, and how is it determined?

Unlock Deck

Unlock for access to all 28 flashcards in this deck.

Unlock Deck

k this deck

14

Under what circumstances may a director be held liable for an act when there is no evidence of bad faith or negligence?

Unlock Deck

Unlock for access to all 28 flashcards in this deck.

Unlock Deck

k this deck

15

The Central Laborers Pension Fund (CLPF) sued News Corporation (News) to compel it to produce books and records related to its acquisition of Shine Group Ltd. (Shine). CLPF wanted to investigate potential breaches of fiduciary duty in connection with that transaction. CLPF's demand for inspection did not include evidence of its ownership of News's stock. Should CLPF's demand for inspection be granted? [Central Laborers Pension Fund v. News Corp., 45 A.3d 139 (Del.)]

Unlock Deck

Unlock for access to all 28 flashcards in this deck.

Unlock Deck

k this deck

16

The board of directors of Dime Bancorp Inc., solicited proxies in favor of five sitting directors prior to the annual meeting. North Fork Bancorporation Inc., a shareholder, solicited proxies against them. Both sets of proxy cards contained a general authorization of the holder to vote all the shares held and then allowed stockholders to vote "for" the election of the five candidates or vote to "withhold authority" for the election of them. The votes were 23,800,000 in favor and 55,200,000 withheld. The bylaws required the affirmative vote of a majority of the voting power present at the meeting. Dime claimed that the proxies marked "withhold authority" did not give voting power at all so they did not count as "voting power present." By this reasoning, the five had been elected, basically unanimously. North Fork claimed that the shareholders who marked "withhold authority" gave instructions to the proxy holders to take action, so these proxies should be counted as "voting power present." Should the proxies be counted as "voting power present?" [North Fork Bancorp. Inc. v. Toal, 825 A.2d 860 (Del. Ch.)]

Unlock Deck

Unlock for access to all 28 flashcards in this deck.

Unlock Deck

k this deck

17

Paul Nielsen was the founder and sole shareholder of Clever Innovations Inc. His wife, Gwen, was elected vice president and treasurer. The couple operated the business from their home, with Gwen handling the financial affairs. Sometime later, the Nielsens issued 100 shares of stock to Christopher Dooley, thereby giving him ownership of 50 percent of the company. Dooley was not formally elected as an officer or director but participated in the ongoing business operations of the company. After Paul Nielsen's death, Gwen became the administrator of her husband's estate, which included his stock in Clever Innovations. Relations between Gwen and Dooley quickly soured. The two reached a temporary arrangement whereby Dooley would run the business and inform Gwen of financial considerations. In the meantime, the two agreed to work toward a sale of the estate's half interest in the corporation to Dooley. However, a short time later, Dooley opened up a new bank account for the corporation and funded it with $280,000 from existing customers. Dooley redirected mail to be sent to his home and ignored Gwen's communications related to the sale of the estate's stock in the company. Gwen sued on behalf of the estate, alleging that Dooley's actions were oppressive to the other shareholder. Gwen sought dissolution of the corporation and a mandatory buy-out of the estate's shares for a fair market price. Should the court order dissolution?

Unlock Deck

Unlock for access to all 28 flashcards in this deck.

Unlock Deck

k this deck

18

How does a corporation complete its dissolution?

Unlock Deck

Unlock for access to all 28 flashcards in this deck.

Unlock Deck

k this deck

19

In what way do stockholders' meetings act as a check on the board of directors?

Unlock Deck

Unlock for access to all 28 flashcards in this deck.

Unlock Deck

k this deck

20

Business Organization

Gary Beach and Paul Touradji formed a limited partnership called Playa Oil and Gas, LP for the purpose of exploring oil and gas prospects. Touradji's company, DeepRock Venture Partners, LP held an 80 percent ownership interest in the partnership and contributed the start-up capital. Beach controlled the remaining 20 percent through two different entities, and contributed his rights to titles and interests in certain gas and oil leases and exploration opportunities to the partnership. After an unsuccessful drilling attempt, each partner began to feel the other was missing good business opportunities and withholding information. As their business relationship fell apart, Beach proposed making a distribution to all partners, which DeepRock opposed. Despite this, Beach took approximately half of Playa Oil and Gas's cash on hand and distributed it to the partners. The distribution made it difficult for Playa Oil and Gas to meet its financial obligations and effectively made the company insolvent. DeepRock sued Beach on behalf of Playa Oil and Gas, alleging among other things, that Beach breached his fiduciary duty to the partnership. Did Beach act in the best interest of the partnership by making the distribution? [ Beach Capital Partnership, LP v. DeepRock Venture Partners, LP , 442 S.W.3d 609 (Tex. App.)]

Gary Beach and Paul Touradji formed a limited partnership called Playa Oil and Gas, LP for the purpose of exploring oil and gas prospects. Touradji's company, DeepRock Venture Partners, LP held an 80 percent ownership interest in the partnership and contributed the start-up capital. Beach controlled the remaining 20 percent through two different entities, and contributed his rights to titles and interests in certain gas and oil leases and exploration opportunities to the partnership. After an unsuccessful drilling attempt, each partner began to feel the other was missing good business opportunities and withholding information. As their business relationship fell apart, Beach proposed making a distribution to all partners, which DeepRock opposed. Despite this, Beach took approximately half of Playa Oil and Gas's cash on hand and distributed it to the partners. The distribution made it difficult for Playa Oil and Gas to meet its financial obligations and effectively made the company insolvent. DeepRock sued Beach on behalf of Playa Oil and Gas, alleging among other things, that Beach breached his fiduciary duty to the partnership. Did Beach act in the best interest of the partnership by making the distribution? [ Beach Capital Partnership, LP v. DeepRock Venture Partners, LP , 442 S.W.3d 609 (Tex. App.)]

Unlock Deck

Unlock for access to all 28 flashcards in this deck.

Unlock Deck

k this deck

21

Brothers Don and Harley Shoemaker signed a written partnership agreement for D H Real Estate, in which each had a 50 percent interest. The agreement provided that in the event of the withdrawal of a partner, the remaining partner(s) would have the right to continue the business of the partnership. Twelve years later, Harley sent Don a letter saying he was withdrawing from the partnership in 90 days. The parties could not agree on a valuation of Harley's partnership interest, and eventually Harley sued. Did Harley's withdrawal dissolve the partnership? [Shoemaker v. Shoemaker, 745 N.W.2d 299 (Neb.)]

Unlock Deck

Unlock for access to all 28 flashcards in this deck.

Unlock Deck

k this deck

22

After Lanier Carson retired from Kelley Manufacturing Company (KMC), James Martin became CEO and a member of the board. Timothy Maxwell became president, and he and Martin became the trustees of KMC's Employees Stock Ownership Plan (ESOP). The ESOP owned all the stock of KMC. Statements of account issued to employees who were ESOP participants reflected that the accounts were measured in "shares" vested in each participant. ESOP participants were referred to as shareholders. Martin and Maxwell got in a dispute with Carson. A few months later, Maxwell and Martin were fired by KMC, based on Carson's vote of 135 employees' proxies and powers of attorney. Also, both were removed as trustees of the ESOP, and Carson was voted the sole trustee of the ESOP and chairman of the board of KMC. Martin and Maxwell still had interests in the ESOP, with Martin's ESOP account being the largest single owner of an interest in KMC. When KMC did not allow them to inspect the proxies/powers of attorney and the list of shareholders at the time they were fired, they sued. Should they be allowed to inspect those corporate records?

Unlock Deck

Unlock for access to all 28 flashcards in this deck.

Unlock Deck

k this deck

23

What is a stockholder's most important right, and why is it the most important right?

Unlock Deck

Unlock for access to all 28 flashcards in this deck.

Unlock Deck

k this deck

24

East Park Limited Partnership signed a $9 million note. Before the note was due, Joseph Della Ratta, the general partner issued a "capital call" to try to squeeze out some of the limited partners. He informed them that East Park could not pay the note, so they would have to pay their proportionate shares of the balance. He said he would try to refinance the note but did not. Some partners said they were withdrawing from East Park before the loan due date. Della Ratta responded that they would forfeit their interests in East Park if they did not pay and accelerated the capital call to a date prior to the limited partners' withdrawal date. The withdrawing partners sued. Must they pay the capital call or lose their interests in East Park? [Della Ratta v. Larkin, 856 A.2d 643 (Md.)]

Unlock Deck

Unlock for access to all 28 flashcards in this deck.

Unlock Deck

k this deck

25

At a meeting of the Big Woods Springs Improvement Association Inc. (BWSIA), the president of the board of directors was handed a letter from Big Woods Land Development Inc. (BWLD). The letter stated BWLD had sold 288 lots to "new buyers," who allegedly took possession two days previously. The list of these buyers showed that 174 lots, only 20 of which were platted, were purportedly sold to Michael Nelson. The letter alleged that each "new buyer" had paid 1/12 of the annual BWSIA dues of $180. Hall was given a check for $4,320 ($15 x 288) and asked that all new members be allowed to vote. The letter was the only evidence that the "new members" had purchased lots. Following a motion for adjournment, second, and vote, the meeting was adjourned. After the existing members left, Nelson conducted a meeting of the "new members" at which he was elected president and a board member. BWSIA sued Nelson asking the court to prevent him from holding himself out as a director or officer and from exercising control of BWSIA assets. The BWSIA bylaws stated that a member must first pay the full annual assessment fee in order to vote. They also required a person to submit an application for membership in the association to the board of directors before obtaining ownership of any lot. Should the "new members" have been allowed to vote at the meeting?

Unlock Deck

Unlock for access to all 28 flashcards in this deck.

Unlock Deck

k this deck

26

Cooperative Bank was a commercial bank with deposits insured by the Federal Deposit Insurance Corporation (FDIC). The bank was routinely examined by the FDIC and independent auditors to ensure good underwriting and credit practices. The FDIC gave a "satisfactory" rating for the directors' management of the bank and the quality of assets held by the bank. An independent audit found that Cooperative Bank's loans were "well documented with credit memoranda that adequately articulated the credit decision process." After a period of economic turmoil, many of the loans approved by the bank were not repaid by borrowers. Cooperative Bank was declared insolvent and the FDIC was named as the bank's receiver. The FDIC sued the former directors of Cooperative Bank, alleging that the directors breached their fiduciary duty to shareholders by approving 86 loans that turned out to be bad credit decisions. Was the FDIC correct?

Unlock Deck

Unlock for access to all 28 flashcards in this deck.

Unlock Deck

k this deck

27

Suppose that an employee of a business finds some papers in a newspaper left on the subway. Miraculously, the papers are a report written by an employee of a competitor with some really helpful ideas for a report the employee has been asked to write. Would it be ethical for the employee to "borrow" the ideas in the found report and use them? Would it make any difference if the person who had written the report had intended to discard it?

Unlock Deck

Unlock for access to all 28 flashcards in this deck.

Unlock Deck

k this deck

28

Explain how a voting trust works.

Unlock Deck

Unlock for access to all 28 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 28 flashcards in this deck.