Deck 8: Relative, Asset-Oriented, and Real Option

Full screen (f)

Question

Question

Question

Question

Question

Question

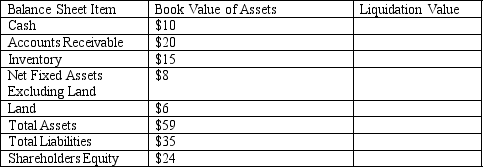

Titanic Corporation has reached agreement with its creditors to liquidate voluntarily its assets and to use the proceeds to pay off as much of its liabilities as possible. The firm anticipates that it will be able to sell off its assets in an orderly fashion, realizing as much as 70% of the book value of its receivables, 40% of its inventory, and 25% of its net fixed assets (excluding land). However, the firm believes that the land on which it is located can be sold for 120% of book value. The firm has legal and professional expenses associated with the liquidation process of $2,900,000. The firm has only common stock outstanding. Estimate the amount of cash that would remain for the firm's common shareholders once all assets have been liquidated.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/109

Play

Full screen (f)

Deck 8: Relative, Asset-Oriented, and Real Option

1

LAFCO Industries believes that its two primary product lines, automotive and commercial aircraft valves, are rapidly becoming

obsolete. Its free cash flow is rapidly diminishing as it loses market share to new firms entering its industry. LAFCO has $200

million in debt outstanding. Senior management expects the automotive and commercial aircraft valve product lines to

generate $25 million and $15 million, respectively, in earnings before interest, taxes, depreciation, and amortization next year. Senior management also believes that they will not be able to upgrade these product lines due to declining cash flow and excessive current leverage. A competitor to its automotive valve business last year sold for 10 times EBITDA. Moreover, a company that is similar to its commercial aircraft valve product line sold last month for 12 times EBITDA. Estimate LAFCO's breakup value before taxes.

obsolete. Its free cash flow is rapidly diminishing as it loses market share to new firms entering its industry. LAFCO has $200

million in debt outstanding. Senior management expects the automotive and commercial aircraft valve product lines to

generate $25 million and $15 million, respectively, in earnings before interest, taxes, depreciation, and amortization next year. Senior management also believes that they will not be able to upgrade these product lines due to declining cash flow and excessive current leverage. A competitor to its automotive valve business last year sold for 10 times EBITDA. Moreover, a company that is similar to its commercial aircraft valve product line sold last month for 12 times EBITDA. Estimate LAFCO's breakup value before taxes.

$230 million

PV (automotive valves) = 25 x 10 = 250

PV (aircraft valves) = 15 x 12 = 180

Less outstanding debt = 200

Break-up value = 230

PV (automotive valves) = 25 x 10 = 250

PV (aircraft valves) = 15 x 12 = 180

Less outstanding debt = 200

Break-up value = 230

2

Acquirer Company's management believes that there is a 60 percent chance that Target Company's free cash flow to the firm will grow at 20 percent per year during the next five years from this year's level of $5 million. Sustainable growth beyond the fifth year is estimated at 4 percent per year. However, they also believe that there is a 40 percent chance that cash flow will grow at half that annual rate during the next five years and then at a 4 percent rate thereafter. The discount rate is estimated to be 15 percent during the high growth period and 12 percent during the sustainable growth period for each scenario. What is the expected value of Target Company?

$94.93 million

PV20 = 5(1.20) + 5(1.2)2 + 5(1.2)3 + 5(1.2)4 + 5(1.2)5 + 5(1.2)5(1.04)/(.12-.04)

(1.15) (1.15)2 (1.15)3 (1.15)4 (1.15)5 (1.15)5

= 5.22 + 5.44 + 5.68 + 5.93 + 6.19 + 80.41 = 108.87

PV10 = 5(1.10) + 5(1.1)2 + 5(1.1)3 + 5 (1.1)4 + 5(1.1)5 + 5(1.1)5(1.04)/(.12-.04)

(1.15) (1.15)2 (1.15)3 (1.15)4 (1.15)5 (1.15)5

= 4.78 + 4.57 + 4.38 + 4.19 + 4.01 + 52.1 = 74.03

EV = .6 x 108.87 + .4 x 74.03 = 94.93

Solutions to End of Chapter

PV20 = 5(1.20) + 5(1.2)2 + 5(1.2)3 + 5(1.2)4 + 5(1.2)5 + 5(1.2)5(1.04)/(.12-.04)

(1.15) (1.15)2 (1.15)3 (1.15)4 (1.15)5 (1.15)5

= 5.22 + 5.44 + 5.68 + 5.93 + 6.19 + 80.41 = 108.87

PV10 = 5(1.10) + 5(1.1)2 + 5(1.1)3 + 5 (1.1)4 + 5(1.1)5 + 5(1.1)5(1.04)/(.12-.04)

(1.15) (1.15)2 (1.15)3 (1.15)4 (1.15)5 (1.15)5

= 4.78 + 4.57 + 4.38 + 4.19 + 4.01 + 52.1 = 74.03

EV = .6 x 108.87 + .4 x 74.03 = 94.93

Solutions to End of Chapter

3

An investor group has the opportunity to purchase a firm whose primary asset is ownership of the exclusive rights to develop a parcel of undeveloped land sometime during the next 5 years. Without considering the value of the option to develop the property, the investor group believes the net present value of the firm is $(10) million. However, to convert the property to commercial use (i.e., exercise the option), the investors will have to invest $60 million immediately in infrastructure improvements. The primary uncertainty associated with the property is how rapidly the surrounding area will grow. Based on their experience with similar properties, the investors estimated that the variance of the projected cash flows is 5% of the NPV, which is $55 million, of developing the property. Assume the risk-free rate of return is 4 percent. What is the value of the call option the investor group would obtain by buying the firm? Is it sufficient to justify the acquisition of the firm?

The value of the option is $13.47 million. The investor group should buy the firm since the value of the option more than offsets the $(10) million NPV of the firm if the call option were not exercised.

Value of the underlying asset (Expected value of the property) (S) = $55 million

Exercise price (Upfront investment to commercialize the property) (E) = $60 million:

Variance in underlying asset's value (Measure of cash flow risk) ( 2): .05

Time to expiration (t): 5

Risk free interest rate (R): 4

Where C = Theoretical call option value = SN(d1) - Ee-RtN(d2) = $55 x N(.6844) - $60 x 2.7183.04x5x N(.4920) =

$37.64 - $24.17 = $13.47 million.

d1 = ln(S/E) + [R + (1/2) 2} t = ln($55/$60) + [.04 + (1/2).05]5 = -.0870 + .3250

t .05 5 ..2236 x 2.2361

= .2380 = .4760

.50

d2 = d1 - t = .4760 - .5 = -.0240

S = Stock price or underlying asset price

E = Exercise price

R = Risk free interest rate corresponding to the life of the option

2 = Variance of the stock's or underlying asset's returns

t = Time to expiration of the option

N(d1) and N(d2) = Cumulative normal probability values of d1 and d2

e = 2.7183

Value of the underlying asset (Expected value of the property) (S) = $55 million

Exercise price (Upfront investment to commercialize the property) (E) = $60 million:

Variance in underlying asset's value (Measure of cash flow risk) ( 2): .05

Time to expiration (t): 5

Risk free interest rate (R): 4

Where C = Theoretical call option value = SN(d1) - Ee-RtN(d2) = $55 x N(.6844) - $60 x 2.7183.04x5x N(.4920) =

$37.64 - $24.17 = $13.47 million.

d1 = ln(S/E) + [R + (1/2) 2} t = ln($55/$60) + [.04 + (1/2).05]5 = -.0870 + .3250

t .05 5 ..2236 x 2.2361

= .2380 = .4760

.50

d2 = d1 - t = .4760 - .5 = -.0240

S = Stock price or underlying asset price

E = Exercise price

R = Risk free interest rate corresponding to the life of the option

2 = Variance of the stock's or underlying asset's returns

t = Time to expiration of the option

N(d1) and N(d2) = Cumulative normal probability values of d1 and d2

e = 2.7183

4

Under what circumstances might it be more appropriate to use relative valuation methods rather than the DCF approach? Be specific.

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

5

Does the application of the comparable companies' valuation method require the addition of an acquisition premium? Why? / Why not?

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

6

Titanic Corporation has reached agreement with its creditors to liquidate voluntarily its assets and to use the proceeds to pay off as much of its liabilities as possible. The firm anticipates that it will be able to sell off its assets in an orderly fashion, realizing as much as 70% of the book value of its receivables, 40% of its inventory, and 25% of its net fixed assets (excluding land). However, the firm believes that the land on which it is located can be sold for 120% of book value. The firm has legal and professional expenses associated with the liquidation process of $2,900,000. The firm has only common stock outstanding. Estimate the amount of cash that would remain for the firm's common shareholders once all assets have been liquidated.

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

7

Siebel Incorporated, a non-publicly traded company, has 2009 after-tax earnings of $20 million, which are expected to grow at 5

percent annually into the foreseeable future. The firm is debt-free, capital spending equals the firm's rate of depreciation; and the annual change in working capital is expected to be minimal. The firm's beta is estimated to be 2.0, the 10-year Treasury bond is 5 percent, and the historical risk premium of stocks over the risk-free rate is 5.5 percent. Publicly-traded Rand Technology, a direct competitor of Siebel's, was sold recently at a purchase price of 11 times its 2009 after-tax earnings, which included a 20 percent premium over its current market price. Aware of the premium paid for the purchase of Rand, Siebel's equity owners would like to determine what it might be worth if they were to attempt to sell the firm in the near future. They chose to value the firm using the discounted cash flow and comparable recent transactions methods. They believe that either method provides an equally valid. Estimate of the firm's value.

a What is the value of Siebel using the DCF method?

b What is the value using the comparable recent transactions method?

c What would be the value of the firm if we combine the results of both methods?

percent annually into the foreseeable future. The firm is debt-free, capital spending equals the firm's rate of depreciation; and the annual change in working capital is expected to be minimal. The firm's beta is estimated to be 2.0, the 10-year Treasury bond is 5 percent, and the historical risk premium of stocks over the risk-free rate is 5.5 percent. Publicly-traded Rand Technology, a direct competitor of Siebel's, was sold recently at a purchase price of 11 times its 2009 after-tax earnings, which included a 20 percent premium over its current market price. Aware of the premium paid for the purchase of Rand, Siebel's equity owners would like to determine what it might be worth if they were to attempt to sell the firm in the near future. They chose to value the firm using the discounted cash flow and comparable recent transactions methods. They believe that either method provides an equally valid. Estimate of the firm's value.

a What is the value of Siebel using the DCF method?

b What is the value using the comparable recent transactions method?

c What would be the value of the firm if we combine the results of both methods?

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

8

What are the key assumptions implicit in the comparable companies' valuation method? The recent transactions method? Be specific.

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

9

What are real options and how are they applied in valuing acquisitions?

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

10

How is the liquidation value of the firm calculated? Why is the assumption of orderly liquidation important?

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

11

BigCo's Chief Financial Officer is trying to determine a fair value for PrivCo, a non-publicly traded firm that BigCo's is

considering acquiring. Several of PrivCo's competitors, Ion International, and Zenon are publicly traded. Ion and Zenon have

price-to-earnings ratios of 20 and 15, respectively. Moreover, Ion and Zenon's shares are trading at a multiple of earnings

before interest, taxes, depreciation, and amortization (EBITDA) of 10 and 8, respectively. BigCo estimates that next year

PrivCo will achieve net income and EBITDA of $4 million and $8 million, respectively. To gain a controlling interest in the

firm, BigCo expects to have to pay at least a 30% premium to the firm's market value. What should BigCo expect to pay for

PrivCo?

a. Based on price-to-earnings ratios?

b. Based on EBITDA?

considering acquiring. Several of PrivCo's competitors, Ion International, and Zenon are publicly traded. Ion and Zenon have

price-to-earnings ratios of 20 and 15, respectively. Moreover, Ion and Zenon's shares are trading at a multiple of earnings

before interest, taxes, depreciation, and amortization (EBITDA) of 10 and 8, respectively. BigCo estimates that next year

PrivCo will achieve net income and EBITDA of $4 million and $8 million, respectively. To gain a controlling interest in the

firm, BigCo expects to have to pay at least a 30% premium to the firm's market value. What should BigCo expect to pay for

PrivCo?

a. Based on price-to-earnings ratios?

b. Based on EBITDA?

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

12

Best's Foods is seeking to acquire the Heinz Baking Company, whose shareholders equity and goodwill are $41 million and $7 million, respectively. A comparable bakery was recently acquired for $400 million, 30 percent more than its tangible book value (TBV). What was the tangible book value of the recently acquired bakery? How much should Best's Foods expect to have to pay for the Heinz Baking Company? Show your work.

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

13

Conventional DCF analysis does not incorporate the effects of real options into the valuation of an asset. How might an analyst

incorporate the potential impact of real options into conventional DCF valuation methods?

incorporate the potential impact of real options into conventional DCF valuation methods?

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

14

Which is generally considered more accurate: the comparable companies' or recent comparable transactions method? Explain your answer.

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

15

examples of pre- and post-closing real options.

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

16

PEG ratios allow for the adjustment of relative valuation methods for the expected growth of the firm. How might this be helpful in selecting potential acquisition targets? Be specific?

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

17

Acquirer Incorporated's management believes that the most reliable way to value a potential target firm is by averaging multiple valuation methods, since all methods have their shortcomings. Consequently, Acquirer's Chief Financial Officer estimates that the value of Target Inc. could range, before an acquisition premium is added, from a high of $650 million using discounted cash flow analysis to a low of $500 million using the comparable companies' relative valuation method. A valuation based on a recent comparable transaction is $672 million. The CFO anticipates that Target Inc.'s management and shareholders would be willing to sell for a 20 percent acquisition premium, based on the premium paid for the recent comparable transaction. The CEO asks the CFO to provide a single estimate of the value of Target Inc. based on the three estimates. In calculating a weighted average of the three estimates, she gives a value of .5 to the recent transactions method, 3 to the DCF estimate, and .2 to the comparable companies' estimate. What it weighted average estimate she gives to the CEO? Show your work.

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

18

Explain the primary differences between the income (discounted cash flow), relative (market-based), and asset-oriented valuation methods?

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

19

Photon Inc. is considering acquiring one of its competitors. Photon's management wants to buy a firm it believes is most undervalued. The firm's three major competitors, AJAX, BABO, and COMET, have current market values of $375 million, $310 million, and $265 million, respectively. AJAX's FCFE is expected to grow at 10 percent annually, while BABO's and COMET's FCFE are projected to grow by 12 and 14 percent per year, respectively. AJAX, BABO, and COMET's current year FCFE are $24, $22, and $17 million, respectively. The industry average price-to-FCFE ratio and growth rate are 10 and 8%, respectively. Estimate the market value of each of the three potential acquisition targets based on the information provided? Which firm is the most undervalued? Which firm is most overvalued?

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

20

Delhi Automotive Inc. is the leading supplier of specialty fasteners for passenger cars in the U.S. market, with an estimated 25

percent share of this $5 billion market. Delhi's rapid growth in recent years has been fueled by high levels of reinvestment in the firm. While this has resulted in the firm having "state of the art" plants, it has also resulted in the firm showing limited profitability and positive cash flow. Delhi is privately owned and has announced that it is going to undertake an initial public offering in the near future. Investors know that economies of scale are important in this high fixed cost industry and understand that market share is an important determinant of future profitability. Thornton Auto Inc., a publicly traded firm and the leader in this market, has an estimated market share of 38 percent and an $800 million market value. How should investors value the Delhi IPO? Show your work.

percent share of this $5 billion market. Delhi's rapid growth in recent years has been fueled by high levels of reinvestment in the firm. While this has resulted in the firm having "state of the art" plants, it has also resulted in the firm showing limited profitability and positive cash flow. Delhi is privately owned and has announced that it is going to undertake an initial public offering in the near future. Investors know that economies of scale are important in this high fixed cost industry and understand that market share is an important determinant of future profitability. Thornton Auto Inc., a publicly traded firm and the leader in this market, has an estimated market share of 38 percent and an $800 million market value. How should investors value the Delhi IPO? Show your work.

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

21

the market leader in an industry has a $300 million market value and a 30% market share, the market is valuing each percentage point of market share at $10 million. If a target company in the same industry has a 20% market share, the market value of the target company is $200 million.

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

22

The capitalization rate is equivalent to the discount rate when the firm's revenues are not expected to grow.

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

23

Market-based valuation measures are meaningful only for firms with a stable earnings, cash flow, or sales history.

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

24

comparable recent transactions method is usually considered less reliable than the comparable companies' valuation method.

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

25

Price-to-earnings ratios of comparable companies provide an excellent means of valuing the target firm at any point in the business cycle.

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

26

Book values are maligned as measures of value, because they represent historical rather than current market values.

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

27

Valuations of target firms based on the comparable companies and recent transactions methods must be adjusted to reflect control premiums.

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

28

replacement cost approach to valuation of a target firm ignores value created by operating the assets in combination as a going concern.

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

29

Based on the information given in the case, how would you estimate the value of Twitter at the time of the IPO based on a simple average of comparable firm enterprise to EBITDA multiples based on projected 2014 EBITDA?

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

30

Tangible book value is the value of shareholders' equity less net fixed assets.

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

31

Break-up value assumes that individual businesses can be sold quickly without any material loss of value.

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

32

The principal limitation to the comparable companies' valuation approach is the difficulty in finding companies that are truly comparable to the target firm.

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

33

Scenario analysis involves valuing businesses based on different sets assumptions about the future. What are the advantages and disadvantages of applying this methodology in determining an appropriate purchase price using relative valuation methods to estimate firm value?

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

34

Liquidation value provides an estimate of the minimum value of the target firm.

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

35

Asset oriented approaches to valuation involve the use of tangible book value, liquidation value, discounted cash flows, and break-up values.

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

36

valuation estimates in the preceding two questions are substantially different. What are the key assumptions underlying each valuation method? Be specific. How can an analyst combine the two valuation estimates assuming she believes that the enterprise to EBITDA ratio is twice as reliable as the valuation based on a revenue multiple?

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

37

Liquidation value is the projected sale value of a firm's assets.

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

38

comparable companies' valuation method uses the discounted value of a firm's free cash flow.

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

39

the tangible book value of a firm significantly exceeds its market value for an extended period of time, it can become an attractive takeover target.

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

40

Based on the information given in the case, how would you estimate the value of Twitter at the time of the IPO based on a simple average of comparable firm revenue multiples based on projected 2014 revenue?

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

41

Like the recent transactions method, comparable company valuation estimates do not require the addition of a purchase price premium.

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

42

The weighted average valuation approach involves the use of a number of different valuation methods, weighted by the relative importance the appraiser attributes to each method.

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

43

The use of market-based valuation methods usually reflect actual demand and supply considerations at a moment in time.

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

44

The enterprise value to EBITDA method is useful because more firms are likely to have negative earnings than negative EBITDA.

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

45

The analyst should be careful not to mechanically add an acquisition premium to the target firm's estimated value based on the comparable companies' method if there is evidence that the market values of these "comparable firms" already reflect the effects of acquisition activity elsewhere in the industry.

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

46

The comparable companies' method and recent transactions methods of valuation are conceptually similar.

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

47

Disadvantages of the comparable industry method of valuation include the presumption that industry multiples are actually comparable and that analysts' earnings projections are unbiased.

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

48

The comparable companies' method is widely used in so-called "fairness opinion" letters.

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

49

Analysts have increasingly used the relationship between enterprise value to earnings before interest and taxes, depreciation, and amortization to value firms.

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

50

The enterprise value to EBITDA multiple relates the total book value of the firm from the perspective of the liability side of the balance sheet (i.e., long-term debt plus preferred and common equity), excluding cash, to EBITDA.

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

51

The enterprise to EBITDA method of valuation can be compared more readily among firms exhibiting different levels of leverage than for other measures of earnings, since the numerator represents the total value of the firm and the denominator measures earnings before interest.

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

52

In constructing the enterprise value, the market value of the firm's common equity value is added to the market value of the firm's long-term debt and the market value of preferred stock.

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

53

Relative valuation methods are often described as market-based, as they reflect the amounts investors are willing to pay for each dollar of earnings, cash flow, sales, or book value at a moment in time.

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

54

Studies show that rival firms' share prices will rise in response to the announced acquisition of a competitor, regardless of whether the proposed acquisition is ultimately successful or unsuccessful.

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

55

The so-called PEG ratio is calculated by dividing the firm's price-to-earning ratio by the expected growth rate in the firm's share price.

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

56

The comparable companies' transactions valuation method is generally considered the most accurate of all the valuation methods.

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

57

If the P/E ratio for the comparable firm is equal to 10 and the after-tax earnings of the target firm are $2 million, the market value of the target firm would be $5 million.

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

58

Market-based valuation methods are less prone to manipulation than discounted cash flow methods because they require a more detailed statement of assumptions.

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

59

The value of the comparable companies' method may vary widely depending upon when it is calculated in the business cycle.

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

60

A higher P/E ratio for a firm may be justified if its earnings are expected to grow significantly faster than firm's future earnings.

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

61

It is critical for the analyst to remember that high growth rates by themselves are likely to increase multiples such as a firm's price to earnings ratio even without any improvement in financial returns.

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

62

The number of billing errors as a percent of total invoices is a specific example of a macro value driver.

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

63

Conceptually, firms with P/E ratios less than their projected growth rates may be considered undervalued; while those with P/E ratios greater than their projected growth rates may be viewed as overvalued.

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

64

Macro value drivers are those factors which directly influence specific activities within the firm.

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

65

Investors may be willing to pay considerably more for a stock whose PEG ratio is greater than one if they believe the increase in earnings will result in future financial returns that significantly exceed the firm's cost of equity.

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

66

In the absence of earnings, other factors that drive the creation of value for a firm may be used for valuation purposes.

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

67

Empirical evidence suggests that forecasts of earnings and other value indicators are better predictors of firm value than value indicators based on historical data.

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

68

The PEG ratio can be helpful in evaluating the potential market values of a number of different firms in the same industry in selecting which may be the most attractive acquisition target.

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

69

An option is the exclusive right, but not the obligation, to buy, sell, or use property for a specific period of time in exchange for a predetermined amount of money.

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

70

Tangible book value is widely used for valuing financial services companies, where tangible book value is primarily cash or liquid assets.

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

71

Liquidation or breakup value is the projected price of the firm's assets sold separately in liquidating or breaking up the firm.

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

72

Micro value drivers are those factors affecting specific functions within the firm.

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

73

The major advantage of the value driver approach to valuation is the implied assumption that a single value driver or factor is representative of the total value of the business.

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

74

Since real options provide flexibility that can greatly change the value of a project, it should be considered in capital budgeting methodology.

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

75

Valuing the assets separately in terms of what it would cost to replace them may seriously overstate the firm's true going concern value.

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

76

In determining the liquidation value of inventories, it is not necessary to look at their composition.

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

77

Real options include the right to buy land, commercial property, and equipment. Such assets can be valued as call options if its current value exceeds the difference between the asset's current value and some predetermined level.

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

78

When estimating liquidation value, analysts often make a simplifying assumption that the assets can be sold in an orderly fashion, which is defined as a reasonable amount of time to solicit bids from qualified buyers.

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

79

Real options, also called strategic management options, refer to management's ability to adopt and later revise corporate investment decisions.

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

80

The replacement cost approach to valuation estimates what it would cost to replace the target firm's assets at current market prices using professional appraisers less the present value of the firm's liabilities.

Unlock Deck

Unlock for access to all 109 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 109 flashcards in this deck.