Deck 17: Accounting for State and Local Governments, Part II

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

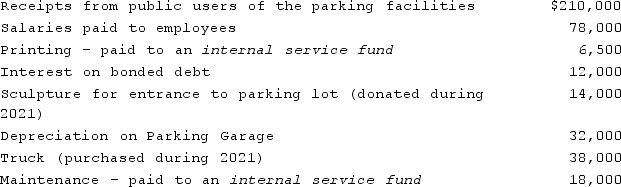

The parking garage and parking lots owned by the City of Barnard reported the following balances for 2021:  Required:Prepare the appropriate financial statement for the fund that was used to account for parking operations.

Required:Prepare the appropriate financial statement for the fund that was used to account for parking operations.

Required:Prepare the appropriate financial statement for the fund that was used to account for parking operations. Question

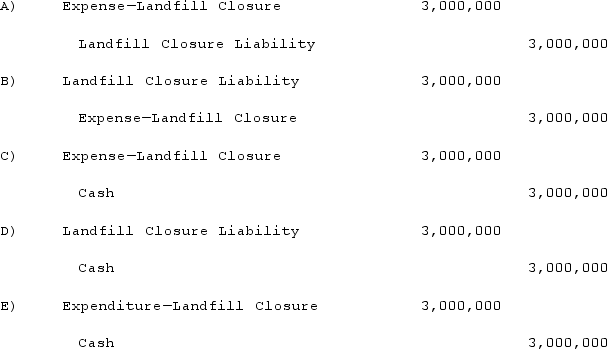

The Town of Harvest opened a solid waste landfill in 1998 that is filled to capacity in the current year. The city initially anticipated closure costs of $3 million. These costs were not expected to be incurred until the landfill was closed. What is the final journal entry to record these costs assuming the estimated $3 million closure costs were properly recorded and the landfill is accounted for in an enterprise fund?

A) Option A.

B) Option B.

C) Option C.

D) Option D.

E) Option E.

A) Option A.

B) Option B.

C) Option C.

D) Option D.

E) Option E.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

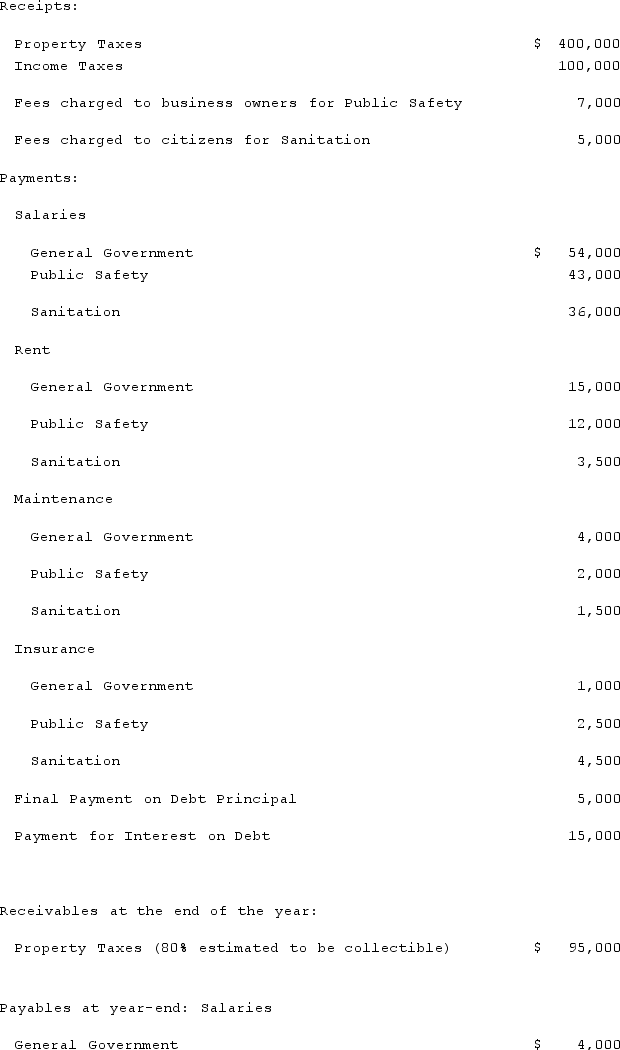

The Town of Portsmouth has at the beginning of the year a $213,000 Net Position balance, and a $52,000 Fund Balance.The following information relates to the activities within the Town of Portsmouth for the year of 2021.  Prepare a Statement of Revenues, Expenditures and Other Changes in Fund Balances for the year ended December 31, 2021.

Prepare a Statement of Revenues, Expenditures and Other Changes in Fund Balances for the year ended December 31, 2021.

Prepare a Statement of Revenues, Expenditures and Other Changes in Fund Balances for the year ended December 31, 2021. Question

Question

Question

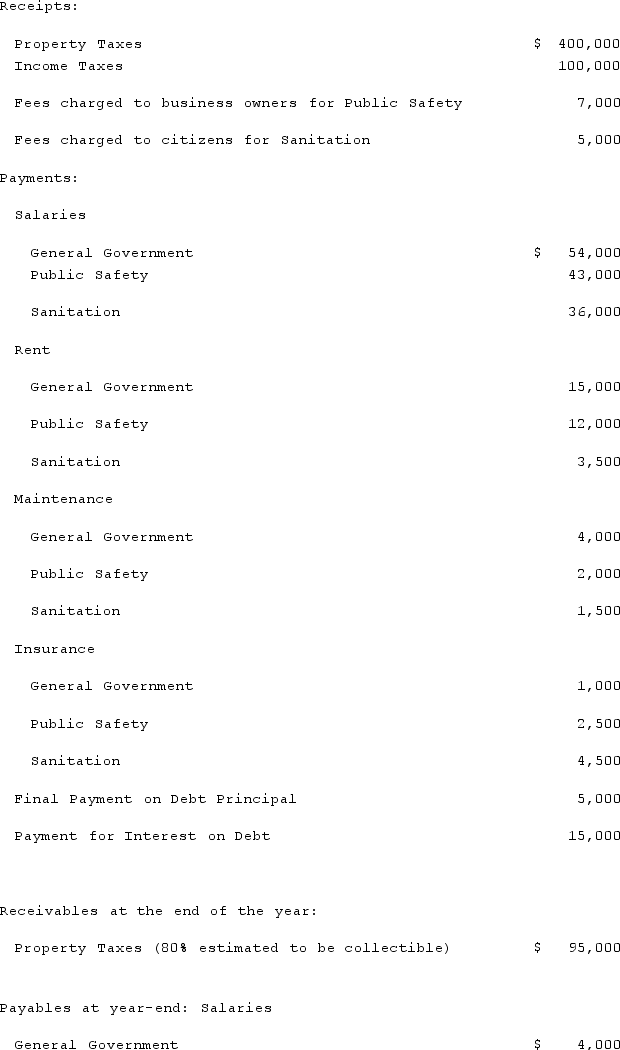

The Town of Portsmouth has at the beginning of the year a $213,000 Net Position balance, and a $52,000 Fund Balance.The following information relates to the activities within the Town of Portsmouth for the year of 2021.  Prepare a Statement of Net Position at December 31, 2021.

Prepare a Statement of Net Position at December 31, 2021.

Prepare a Statement of Net Position at December 31, 2021. Question

Match between columns

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/50

Play

Full screen (f)

Deck 17: Accounting for State and Local Governments, Part II

1

Which of the following is a financial statement of a proprietary fund?

A) Balance sheet.

B) Statement of Operations.

C) Statement of Changes in Cash Flows.

D) Statement of Net Position.

E) Statement of Revenues, Expenditures, and Changes in Fund Balance.

A) Balance sheet.

B) Statement of Operations.

C) Statement of Changes in Cash Flows.

D) Statement of Net Position.

E) Statement of Revenues, Expenditures, and Changes in Fund Balance.

D

2

All of the following about tax abatement agreements must be disclosed by state and local governments except:

A) The purpose of the tax abatement program.

B) The type of tax being abated.

C) Identify the companies receiving the abatements.

D) Dollar amount of taxes abated.

E) Commitments made by the government or other party.

A) The purpose of the tax abatement program.

B) The type of tax being abated.

C) Identify the companies receiving the abatements.

D) Dollar amount of taxes abated.

E) Commitments made by the government or other party.

C

3

Which statement is false regarding the Balance Sheet for Governmental Fund Financial Statements?

A) The Balance Sheet for Governmental Fund Financial Statements measures only current financial resources of the governmental entity.

B) The Balance Sheet for Governmental Fund Financial Statements uses the modified accrual method for timing purposes.

C) Capital Assets are not reported on the Balance Sheet for Governmental Fund Financial Statements.

D) The Balance Sheet for Governmental Fund Financial Statements measures only long-term financial resources of the governmental entity.

E) Long-term debts are not reported on the Balance Sheet for Governmental Fund Financial Statements.

A) The Balance Sheet for Governmental Fund Financial Statements measures only current financial resources of the governmental entity.

B) The Balance Sheet for Governmental Fund Financial Statements uses the modified accrual method for timing purposes.

C) Capital Assets are not reported on the Balance Sheet for Governmental Fund Financial Statements.

D) The Balance Sheet for Governmental Fund Financial Statements measures only long-term financial resources of the governmental entity.

E) Long-term debts are not reported on the Balance Sheet for Governmental Fund Financial Statements.

D

4

What are the three broad sections of a state or local government's CAFR?

A) Introductory, financial, and statistical.

B) Financial statements, notes to the financial statements, and component units.

C) Introductory, statistical, and component units.

D) Component units, financial, and statistical.

E) Financial statements, notes to the financial statements, and statistical.

A) Introductory, financial, and statistical.

B) Financial statements, notes to the financial statements, and component units.

C) Introductory, statistical, and component units.

D) Component units, financial, and statistical.

E) Financial statements, notes to the financial statements, and statistical.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

5

The modified approach to accounting for infrastructure assets may be utilized by a state or local government if:The government accumulates information about all infrastructure assets within either a network or subsystem of a network.The government capitalizes infrastructure assets.The government expenses costs of maintaining the infrastructure assets.The government chooses to depreciate its infrastructure assets.

A) i and ii.

B) i, ii, and iv.

C) ii and iii.

D) i, ii, and iii.

E) i, ii, iii, and iv.

A) i and ii.

B) i, ii, and iv.

C) ii and iii.

D) i, ii, and iii.

E) i, ii, iii, and iv.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

6

Which item is not included on the government-wide Statement of Activities?

A) Revenues.

B) Expenses.

C) Assets.

D) Operating grants.

E) Capital contributions.

A) Revenues.

B) Expenses.

C) Assets.

D) Operating grants.

E) Capital contributions.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

7

Which one of the following is a criterion for identifying a primary government?

A) it has an appointed board of directors.

B) it is fiscally dependent.

C) it is a local government.

D) it has a separately elected governing board.

E) it must prepare financial statements.

A) it has an appointed board of directors.

B) it is fiscally dependent.

C) it is a local government.

D) it has a separately elected governing board.

E) it must prepare financial statements.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

8

Jones College, a public institution of higher education, must prepare financial statements

A) As if the college was an enterprise fund.

B) Following the same rules as state and local governments.

C) According to GAAP.

D) As if the college was a fiduciary fund.

E) In the same manner as private colleges and universities.

A) As if the college was an enterprise fund.

B) Following the same rules as state and local governments.

C) According to GAAP.

D) As if the college was a fiduciary fund.

E) In the same manner as private colleges and universities.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

9

Which statement is false regarding the government-wide Statement of Net Position?

A) Noncurrent liabilities are presented separately from current liabilities.

B) Assets are reported excluding capital assets.

C) Capital assets are reported net of depreciation.

D) Investments are reported at fair value rather than historical cost.

E) Discretely presented component units are grouped and shown on the right of the total.

A) Noncurrent liabilities are presented separately from current liabilities.

B) Assets are reported excluding capital assets.

C) Capital assets are reported net of depreciation.

D) Investments are reported at fair value rather than historical cost.

E) Discretely presented component units are grouped and shown on the right of the total.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

10

For the purpose of government-wide financial statements, the cost of cleaning up a government-owned landfill and closing the landfill

A) Is not recognized until the costs are actually incurred.

B) Is accrued and amortized over the expected useful life of the landfill.

C) Is accrued on a pro-rated basis each period based on how full the landfill is.

D) Is accrued in full at the time the costs become estimable.

E) Is treated as an encumbrance at the time it become estimable, and then as an expenditure when it is actually paid.

A) Is not recognized until the costs are actually incurred.

B) Is accrued and amortized over the expected useful life of the landfill.

C) Is accrued on a pro-rated basis each period based on how full the landfill is.

D) Is accrued in full at the time the costs become estimable.

E) Is treated as an encumbrance at the time it become estimable, and then as an expenditure when it is actually paid.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

11

Which criteria must be met to be considered a special purpose government?(1.) Have a separately elected governing body.(2.) Be legally independent.(3.) Be fiscally independent.

A) 1 only.

B) 1 and 2.

C) 2 and 3.

D) 1 and 3.

E) 1, 2, and 3.

A) 1 only.

B) 1 and 2.

C) 2 and 3.

D) 1 and 3.

E) 1, 2, and 3.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

12

A local government's basic financial statements would include a statement of cash flows for all

A) proprietary fund types.

B) governmental fund types.

C) fund types.

D) fiduciary fund types.

E) A statement of cash flows is not required for any fund types.

A) proprietary fund types.

B) governmental fund types.

C) fund types.

D) fiduciary fund types.

E) A statement of cash flows is not required for any fund types.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

13

A method of accounting for infrastructure assets that allows the expensing of all maintenance costs each year instead of computing depreciation is called:

A) Government-wide depreciation.

B) Proprietary depreciation.

C) GASB depreciation.

D) Modified approach.

E) Alternative depreciation.

A) Government-wide depreciation.

B) Proprietary depreciation.

C) GASB depreciation.

D) Modified approach.

E) Alternative depreciation.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

14

Madison Township has received a donation of a rare painting worth $1,400,000. For Madison's government-wide financial statements, three criteria must be met before Madison can opt not to recognize the painting as an asset. Which of the following is not one of the three criteria?(1.) The painting is held for public exhibition, education, or research in furtherance of public service, rather than financial gain.(2.) The painting is scheduled to be sold immediately at auction.(3.) The painting is protected, kept unencumbered, cared for, and preserved.

A) Item 1 is not one of the three criteria.

B) Item 2 is not one of the three criteria.

C) Item 3 is not one of the three criteria.

D) All three items are required criteria.

E) None of the three items are required criteria.

A) Item 1 is not one of the three criteria.

B) Item 2 is not one of the three criteria.

C) Item 3 is not one of the three criteria.

D) All three items are required criteria.

E) None of the three items are required criteria.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

15

Which of the following is not a step in reporting a pension liability?

A) The pension benefit payments that will ultimately be required are estimated by an actuary.

B) The portion of those payments that are attributable to past periods of employee service is calculated.

C) The present value of amounts attributable to past periods of employee service is determined in order to arrive at the government's obligation at the present time.

D) Excess liability balance is shown in the government-wide financial statements as a net pension asset.

E) Excess liability balance is shown in the government-wide financial statements as a net pension liability.

A) The pension benefit payments that will ultimately be required are estimated by an actuary.

B) The portion of those payments that are attributable to past periods of employee service is calculated.

C) The present value of amounts attributable to past periods of employee service is determined in order to arrive at the government's obligation at the present time.

D) Excess liability balance is shown in the government-wide financial statements as a net pension asset.

E) Excess liability balance is shown in the government-wide financial statements as a net pension liability.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

16

All of the following are true about the modified approach to infrastructure depreciation except:

A) If specific guidelines are met, a government can choose to expense all maintenance costs each year in lieu of recording depreciation.

B) The modified approach specifically excludes infrastructure assets within a network or subsystem of a network.

C) If specific guidelines are met, additions and improvements must be capitalized.

D) For eligible assets, the government must establish a minimum acceptable condition level.

E) The government must have an asset management system in place to monitor the eligible assets.

A) If specific guidelines are met, a government can choose to expense all maintenance costs each year in lieu of recording depreciation.

B) The modified approach specifically excludes infrastructure assets within a network or subsystem of a network.

C) If specific guidelines are met, additions and improvements must be capitalized.

D) For eligible assets, the government must establish a minimum acceptable condition level.

E) The government must have an asset management system in place to monitor the eligible assets.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

17

According to the GASB (Governmental Accounting Standards Board), which one of the following is not a criterion for determining whether a government is legally separate?

A) The government can determine its own budget.

B) The government can issue bonded debt.

C) The government has corporate powers including the right to sue and be sued.

D) The government has the power to levy taxes.

E) The government can issue preferred stock.

A) The government can determine its own budget.

B) The government can issue bonded debt.

C) The government has corporate powers including the right to sue and be sued.

D) The government has the power to levy taxes.

E) The government can issue preferred stock.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

18

Which of the following is a section of the financial section of the comprehensive annual financial report (CAFR) of a state or local government?(1) Management's discussion and analysis (MD&A).(2) Required supplementary information (other than MD&A).(3) Basic financial statements and notes to financial statements.

A) 1 and 2.

B) 2 and 3.

C) 1 and 3.

D) 3 only.

E) 1, 2, and 3.

A) 1 and 2.

B) 2 and 3.

C) 1 and 3.

D) 3 only.

E) 1, 2, and 3.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

19

Which of the following is true regarding Management's Discussion and Analysis (MD&A)?

A) MD&A should provide an objective analysis of the financial activities based on currently known facts, decisions, or conditions.

B) MD&A should disclose total assets and liabilities for all substantial component units.

C) Management should provide a cash flow projection for at least three consecutive fiscal years in MD&A.

D) MD&A is optional for city governments.

E) MD&A is the final element of the introductory section of the comprehensive annual financial report (CAFR).

A) MD&A should provide an objective analysis of the financial activities based on currently known facts, decisions, or conditions.

B) MD&A should disclose total assets and liabilities for all substantial component units.

C) Management should provide a cash flow projection for at least three consecutive fiscal years in MD&A.

D) MD&A is optional for city governments.

E) MD&A is the final element of the introductory section of the comprehensive annual financial report (CAFR).

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

20

Which of the following statements regarding Management's Discussion and Analysis is true?

A) MD&A is required only for Proprietary Fund Financial Statements.

B) MD&A is reported in the statistical section of the annual report.

C) MD&A is required for comprehensive annual financial reports.

D) MD&A for state and local government financial statements must include an analysis of potential, untapped revenue sources.

E) MD&A is an optional inclusion for state and local government financial statements.

A) MD&A is required only for Proprietary Fund Financial Statements.

B) MD&A is reported in the statistical section of the annual report.

C) MD&A is required for comprehensive annual financial reports.

D) MD&A for state and local government financial statements must include an analysis of potential, untapped revenue sources.

E) MD&A is an optional inclusion for state and local government financial statements.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

21

Over the years, four alternatives have been suggested for constructing the financial statements for public colleges and universities. These alternatives include all of the following except:

A) Adopt FASB's requirements so that all colleges and universities (public and private) prepare comparable financial statements.

B) Apply a more traditional model focusing on fund financial statements and the wide variety of funds that such schools often have to maintain.

C) Create an entirely new set of financial statements designed specifically to meet the unique needs of public colleges and universities.

D) Adopt the requirements issued by the Private Company Council (PCC) of the FASB.

E) Adopt the same reporting model for public schools that has been created for state and local governments.

A) Adopt FASB's requirements so that all colleges and universities (public and private) prepare comparable financial statements.

B) Apply a more traditional model focusing on fund financial statements and the wide variety of funds that such schools often have to maintain.

C) Create an entirely new set of financial statements designed specifically to meet the unique needs of public colleges and universities.

D) Adopt the requirements issued by the Private Company Council (PCC) of the FASB.

E) Adopt the same reporting model for public schools that has been created for state and local governments.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

22

What is meant by the term legally independent?

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

23

Which information must be disclosed regarding tax abatement agreements?i) The purpose of the tax abatement program.ii) The dollar amount of abatement and the names of recipients.iii) The type of tax being abated.

A) i and iii.

B) i only.

C) ii only.

D) iii only.

E) i, ii, and iii.

A) i and iii.

B) i only.

C) ii only.

D) iii only.

E) i, ii, and iii.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

24

The City of Wade has a fiscal year ending June 30. Examine the following transactions for Wade:(A.) On 6/5/21, Wade opens a new landfill. The engineers estimate that at the end of 12 years the landfill will be full. Estimated costs to close the landfill are currently $4,800,000.(B.) On 6/18/21, Wade receives a donation of a vintage railroad steam engine. The engine will be put on display at the local town park. A fee will be charged to actually climb up into the engine. The engine has been valued at $650,000.(C.) On 6/30/21, Wade estimates that the landfill is 2% filled.Determine and prepare the journal entries for the City of Wade for each lettered item for the purposes of preparing the government-wide financial statements.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

25

Which statement is false regarding the Statement of Revenues, Expenditures, and Other Changes in Fund Balance when it is included with government-wide financial statements?

A) The Statement of Revenues, Expenditures, and Other Changes in Fund Balance uses the modified accrual method of accounting.

B) The Statement of Revenues, Expenditures, and Changes in Fund Balance presents revenues as either program revenues or general revenues.

C) A presentation reconciles the change in governmental fund balance to the change in net position for governmental activities.

D) Other financing sources are presented on the Statement of Revenues, Expenditures, and Other Changes in Fund Balance.

E) All non-major funds are combined and reported together.

A) The Statement of Revenues, Expenditures, and Other Changes in Fund Balance uses the modified accrual method of accounting.

B) The Statement of Revenues, Expenditures, and Changes in Fund Balance presents revenues as either program revenues or general revenues.

C) A presentation reconciles the change in governmental fund balance to the change in net position for governmental activities.

D) Other financing sources are presented on the Statement of Revenues, Expenditures, and Other Changes in Fund Balance.

E) All non-major funds are combined and reported together.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

26

What is meant by the term fiscally independent?

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

27

What are the three broad sections of a state or local government's CAFR?

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

28

A city operates a swimming pool as a proprietary fund because there is a $2 admission fee. In fund financial statements, where is this revenue reported?

A) Statement of Net Position.

B) Statement of Revenue, Expenditures, and Other Changes in Fund Balance.

C) Statement of Revenue, Expenses, and Other Changes in Fund Balance.

D) Statement of Net Revenue and Expenses.

E) Statement of Revenue, Expenses, and Other Changes in Net Position.

A) Statement of Net Position.

B) Statement of Revenue, Expenditures, and Other Changes in Fund Balance.

C) Statement of Revenue, Expenses, and Other Changes in Fund Balance.

D) Statement of Net Revenue and Expenses.

E) Statement of Revenue, Expenses, and Other Changes in Net Position.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

29

The City of Wade has a fiscal year ending June 30. Examine the following transactions for Wade:(A.) On 6/5/21, Wade opens a new landfill. The engineers estimate that at the end of 12 years the landfill will be full. Estimated costs to close the landfill are currently $4,800,000.(B.) On 6/18/21, Wade receives a donation of a vintage railroad steam engine. The engine will be put on display at the local town park. A fee will be charged to actually climb up into the engine. The engine has been valued at $650,000.(C.) On 6/30/21, Wade estimates that the landfill is 2% filled.Determine and prepare the general fund journal entries for the City of Wade for each lettered item for the purposes of preparing the fund financial statements.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

30

A city starts a solid waste landfill during 2020. When the landfill was opened the city estimated that it would fill to capacity within 6 years and that the cost to cover the facility would be $1.8 million which will not be paid until the facility is closed. At the end of 2020, the facility was 15% full, and at the end of 2021 the facility was 35% full.On government-wide financial statements, which of the following are the appropriate amounts to present in the financial statements for 2021?

A) Both expense and liability will be zero.

B) Expense will be $270,000 and liability will be $540,000.

C) Expense will be $540,000 and liability will be $540,000.

D) Expense will be $630,000 and liability will be $540,000.

E) Expense will be $360,000 and liability will be $630,000.

A) Both expense and liability will be zero.

B) Expense will be $270,000 and liability will be $540,000.

C) Expense will be $540,000 and liability will be $540,000.

D) Expense will be $630,000 and liability will be $540,000.

E) Expense will be $360,000 and liability will be $630,000.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

31

What are the four steps established by GASB Statement No. 68, Accounting for Financial Reporting for Pensions, in the reporting of a government's liability?

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

32

Which of the following is false regarding defined benefit pension plans provided to employees by a state or local government?

A) Defined benefit pension plans are fully funded by the employees of a state or local government.

B) Pension requirements create a huge financial obligation for many governments across the United States.

C) Many state and local governments establish pension trust funds to accumulate and invest monetary resources and to pay out pension benefits.

D) Pension trusts are classified as fiduciary funds.

E) Pension trusts are not included in reporting government-wide financial statements.

ESSAY. Write your answer in the space provided or on a separate sheet of paper.

31) What three criteria must be met to identify a governmental unit as a primary government?

A) Defined benefit pension plans are fully funded by the employees of a state or local government.

B) Pension requirements create a huge financial obligation for many governments across the United States.

C) Many state and local governments establish pension trust funds to accumulate and invest monetary resources and to pay out pension benefits.

D) Pension trusts are classified as fiduciary funds.

E) Pension trusts are not included in reporting government-wide financial statements.

ESSAY. Write your answer in the space provided or on a separate sheet of paper.

31) What three criteria must be met to identify a governmental unit as a primary government?

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

33

A city starts a solid waste landfill during 2020. When the landfill was opened the city estimated that it would fill to capacity within 6 years and that the cost to cover the facility would be $1.8 million which will not be paid until the facility is closed. At the end of 2020, the facility was 15% full, and at the end of 2021 the facility was 35% full.If the landfill is judged to be a governmental fund, what liability is reported on the fund financial statements at the end of 2021?

A) $0.

B) $270,000.

C) $360,000.

D) $540,000.

E) $630,000.

A) $0.

B) $270,000.

C) $360,000.

D) $540,000.

E) $630,000.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

34

How is the Statement of Cash Flows for Proprietary Funds similar and dissimilar to a Statement of Cash Flows for a for-profit business?

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

35

The parking garage and parking lots owned by the City of Barnard reported the following balances for 2021: Required:Prepare the appropriate financial statement for the fund that was used to account for parking operations.

Required:Prepare the appropriate financial statement for the fund that was used to account for parking operations. Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

36

The Town of Harvest opened a solid waste landfill in 1998 that is filled to capacity in the current year. The city initially anticipated closure costs of $3 million. These costs were not expected to be incurred until the landfill was closed. What is the final journal entry to record these costs assuming the estimated $3 million closure costs were properly recorded and the landfill is accounted for in an enterprise fund?

A) Option A.

B) Option B.

C) Option C.

D) Option D.

E) Option E.

A) Option A.

B) Option B.

C) Option C.

D) Option D.

E) Option E.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

37

Under GASB Statement No. 87, Leases, which of the following is false?

A) Unless the maximum life of a lease is one year or less, all leases are the equivalent of financing leases.

B) A lessee is required to recognize a lease liability and an intangible right-to-use lease asset.

C) The lessor records both a receivable and a deferred lease revenue at present value.

D) The lessor is provided with separate categories for all lease contracts.

E) The lessor reclassifies the deferred lease revenue as lease revenue over time and in a systematic and rational manner.

A) Unless the maximum life of a lease is one year or less, all leases are the equivalent of financing leases.

B) A lessee is required to recognize a lease liability and an intangible right-to-use lease asset.

C) The lessor records both a receivable and a deferred lease revenue at present value.

D) The lessor is provided with separate categories for all lease contracts.

E) The lessor reclassifies the deferred lease revenue as lease revenue over time and in a systematic and rational manner.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

38

What information is required in the introductory section of a state or local government's CAFR?

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

39

What three criteria must be met before a governmental unit can elect to not capitalize and therefore not report a work of art or historical treasure as an asset?

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

40

What information is required in the financial section of a state or local government's CAFR?

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

41

On December 31, 2020, the City of Oliver leases a large piece of construction equipment with a 25-year life for five years to use during a construction project. After the contract ends, the city must return the equipment to the lessor but has not guaranteed any residual value. The lease requires five annual payments of $40,000 per year beginning immediately. Oliver uses its own incremental borrowing rate of 10 percent per year because it does not know the implicit interest rate the lessor is charging. The present value of a $40,000 annuity due for five years at an annual interest rate of 10 percent is $166,795 (rounded).Prepare the journal entry/entries required for government-wide financial statements for this lease contract for 2020 and 2021.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

42

The City of Athens operates a motor pool serving all city-owned vehicles. The motor pool bought a new garage by paying $34,000 in cash and signing a note with the local bank for $320,000. Subsequently, the motor pool performed work for the police department at a cost of $19,000, which had not yet been collected. Depreciation on the garage amounted to $24,000. The first $14,000 payment made on the note included $5,200 in interest.Required:Prepare the journal entries for these transactions that are necessary to prepare government-wide financial statements.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

43

The City of Ibiza maintains a collection of paintings of a former citizen in its City Hall building. During the year, one painting was purchased by the city for $3,000 at an auction using appropriated funds in the General Fund. Also during the year, a donation of a painting valued at $3,600 was made to the city.Prepare the journal entry/entries for the two transactions for the purposes of preparing the government-wide financial statements.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

44

The Town of Sitka opened a solid waste landfill in 2020 that was at 25% capacity on December 31, 2020 and at 60% capacity on December 31, 2021. The city initially anticipated closure costs of $2.8 million but in 2021 revised the estimate of the closure costs to be $3.2 million. None of these costs will be incurred until the landfill is scheduled to be closed.Prepare the journal entry that should be recorded on December 31, 2021 for government-wide financial statements.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

45

The City of Ibiza maintains a collection of paintings of a former citizen in its City Hall building. During the year, one painting was purchased by the city for $3,000 at an auction using appropriated funds in the General Fund. Also during the year, a donation of a painting valued at $3,600 was made to the city.Prepare the journal entry/entries for the two transactions for the purposes of preparing the governmental fund financial statements.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

46

The Town of Portsmouth has at the beginning of the year a $213,000 Net Position balance, and a $52,000 Fund Balance.The following information relates to the activities within the Town of Portsmouth for the year of 2021. Prepare a Statement of Revenues, Expenditures and Other Changes in Fund Balances for the year ended December 31, 2021.

Prepare a Statement of Revenues, Expenditures and Other Changes in Fund Balances for the year ended December 31, 2021. Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

47

The Town of Sitka opened a solid waste landfill in 2020 that was at 25% capacity on December 31, 2020 and at 60% capacity on December 31, 2021. The city initially anticipated closure costs of $2.8 million but in 2021 revised the estimate of the closure costs to be $3.2 million. None of these costs will be incurred until the landfill is scheduled to be closed.Assuming the landfill is recorded within the General Fund, how would the landfill information be represented in the governmental fund financial statements at December 31, 2021?

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

48

On December 31, 2020, the City of Oliver leases a large piece of construction equipment with a 25-year life for five years to use during a construction project. After the contract ends, the city must return the equipment to the lessor but has not guaranteed any residual value. The lease requires five annual payments of $40,000 per year beginning immediately. Oliver uses its own incremental borrowing rate of 10 percent per year because it does not know the implicit interest rate the lessor is charging. The present value of a $40,000 annuity due for five years at an annual interest rate of 10 percent is $166,795 (rounded).Prepare the journal entry/entries required for fund financial statements for this lease contract for 2020 and 2021.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

49

The Town of Portsmouth has at the beginning of the year a $213,000 Net Position balance, and a $52,000 Fund Balance.The following information relates to the activities within the Town of Portsmouth for the year of 2021. Prepare a Statement of Net Position at December 31, 2021.

Prepare a Statement of Net Position at December 31, 2021. Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

51

Match between columns

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 50 flashcards in this deck.