Deck 1: Managerial Accounting and Cost Concepts

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

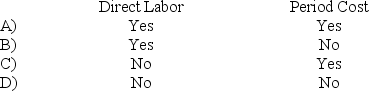

Wages paid to the supervisor of the warehouse where raw materials and parts are temporarily stored before being used in production is considered an example of:

A) Choice A

B) Choice B

C) Choice C

D) Choice D

A) Choice A

B) Choice B

C) Choice C

D) Choice D

Question

Question

Question

Question

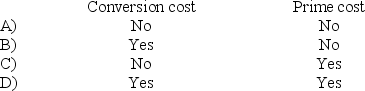

The costs of direct materials are classified as:

A) Choice A

B) Choice B

C) Choice C

D) Choice D

A) Choice A

B) Choice B

C) Choice C

D) Choice D

Question

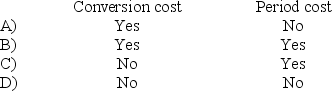

The cost of direct materials is classified as a:

A) Choice A

B) Choice B

C) Choice C

D) Choice D

A) Choice A

B) Choice B

C) Choice C

D) Choice D

Question

Question

Question

Question

Question

Question

Question

The cost of electricity for running production equipment is classified as:

A) Choice A

B) Choice B

C) Choice C

D) Choice D

A) Choice A

B) Choice B

C) Choice C

D) Choice D

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/299

Play

Full screen (f)

Deck 1: Managerial Accounting and Cost Concepts

1

Conversion cost equals product cost less direct materials cost.

True

2

Conversion cost is the sum of direct labor cost and manufacturing overhead cost.

True

3

Advertising is not considered a product cost even if it promotes a specific product.

True

4

Opportunity costs at a manufacturing company are not part of manufacturing overhead.

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

5

In a manufacturing company, all costs are period costs.

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

6

Administrative costs are indirect costs.

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

7

Depreciation is always considered a period cost for external financial reporting purposes in a manufacturing company.

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

8

A direct cost is a cost that can be easily traced to the particular cost object under consideration.

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

9

The sum of all manufacturing costs except for direct materials and direct labor is called manufacturing overhead.

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

10

A factory supervisor's salary would be classified as an indirect cost with respect to a unit of product.

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

11

Selling costs are indirect costs.

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

12

The cost of shipping parts from a supplier is considered a period cost.

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

13

The three cost elements ordinarily included in product costs are direct materials, direct labor, and manufacturing overhead.

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

14

Prime cost equals manufacturing overhead cost.

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

15

Selling and administrative expenses are period costs under generally accepted accounting principles.

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

16

A cost can be direct or indirect. The classification can change if the cost object changes.

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

17

Wages paid to production supervisors would be classified as manufacturing overhead.

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

18

Product costs are also known as inventoriable costs.

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

19

Prime cost is the sum of direct materials cost and direct labor cost.

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

20

Conversion cost is the same thing as manufacturing overhead.

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

21

Committed fixed costs remain largely unchanged in the short run.

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

22

Indirect costs, such as manufacturing overhead, are variable costs.

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

23

Depreciation on equipment a company uses in its selling and administrative activities would be classified as a period cost.

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

24

The cost of napkins put on each person's tray at a fast food restaurant is a variable cost with respect to how many persons are served.

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

25

As activity decreases within the relevant range, fixed costs remain constant on a per unit basis.

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

26

When operations are interrupted or cut back, committed fixed costs are cut in the short term because the costs of restoring them later are likely to be far less than the short-run savings that are realized

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

27

A fixed cost is constant if expressed on a per unit basis but the total dollar amount changes as the number of units increases or decreases.

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

28

Fixed costs expressed on a per unit basis do not change with changes in activity.

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

29

The concept of the relevant range does not apply to variable costs.

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

30

If the activity level increases, then one would expect the fixed cost per unit to increase as well.

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

31

In account analysis, an account is classified as either variable or fixed based on an analyst's prior knowledge of how the cost in the account behaves.

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

32

Within the relevant range, a change in activity results in a change in variable cost per unit and total fixed cost.

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

33

Cost behavior is considered curvilinear whenever a straight line is a reasonable approximation for the relation between cost and activity.

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

34

A fixed cost is a cost whose cost per unit varies as the activity level rises and falls.

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

35

A decrease in production will ordinarily result in a decrease in fixed production costs per unit.

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

36

A fixed cost fluctuates in total as activity changes but remains constant on a per unit basis over the relevant range.

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

37

The relevant range is the range of activity within which the assumption that cost behavior is strictly linear is reasonably valid.

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

38

If managers are reluctant to lay off direct labor employees when activity declines leads to a decrease in the ratio of variable to fixed costs.

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

39

The variable cost per unit depends on how many units are produced.

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

40

A step-variable cost is a cost that is obtained in large chunks and that increases or decreases only in response to fairly wide changes in activity.

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

41

The contribution format income statement is used as an internal planning and decision-making tool. Its emphasis on cost behavior aids cost-volume-profit analysis, management performance appraisals, and budgeting.

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

42

Although the traditional format income statement is useful for external reporting purposes, it has serious limitations when used for internal purposes because it does not distinguish between fixed and variable costs.

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

43

The following costs are all examples of committed fixed costs: depreciation on buildings, salaries of highly trained engineers, real estate taxes, and insurance expenses.

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

44

A contribution format income statement separates costs into fixed and variable categories, first deducting variable expenses from sales to obtain the contribution margin.

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

45

The potential benefit that is given up when one alternative is selected over another is called a sunk cost.

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

46

In a traditional format income statement, the gross margin is sales minus cost of goods sold.

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

47

Committed fixed costs represent organizational investments with a one-year planning horizon.

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

48

The relevant range concept is applicable to mixed costs.

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

49

The amount that a manufacturing company could earn by renting unused portions of its warehouse is an example of an opportunity cost.

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

50

A fixed cost is not constant per unit of product.

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

51

Variable costs per unit are not affected by changes in activity.

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

52

Contribution format income statements are prepared primarily for external reporting purposes

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

53

A variable cost remains constant if expressed on a unit basis.

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

54

Contribution margin and gross margin mean the same thing.

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

55

Most companies use the contribution approach in preparing financial statements for external reporting purposes.

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

56

Differential costs can only be variable.

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

57

In a traditional format income statement, the gross margin minus selling and administrative expenses equals net operating income.

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

58

In a contribution format income statement for a merchandising company, the cost of goods sold reports the product costs attached to the merchandise sold during the period.

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

59

In a traditional format income statement for a merchandising company, cost of goods sold is a variable cost that is included in the "Variable expenses" portion of the income statement.

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

60

A cost that differs from one month to another is known as a sunk cost.

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

61

Direct costs:

A) are incurred to benefit a particular accounting period.

B) are incurred due to a specific decision.

C) can be easily traced to a particular cost object.

D) are the variable costs of producing a product.

A) are incurred to benefit a particular accounting period.

B) are incurred due to a specific decision.

C) can be easily traced to a particular cost object.

D) are the variable costs of producing a product.

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

62

Which of the following statements about product costs is true?

A) Product costs are deducted from revenue when the production process is completed.

B) Product costs are deducted from revenue as expenditures are made.

C) Product costs associated with unsold finished goods and work in process appear on the balance sheet as assets.

D) Product costs appear on financial statements only when products are sold.

A) Product costs are deducted from revenue when the production process is completed.

B) Product costs are deducted from revenue as expenditures are made.

C) Product costs associated with unsold finished goods and work in process appear on the balance sheet as assets.

D) Product costs appear on financial statements only when products are sold.

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

63

Wages paid to the supervisor of the warehouse where raw materials and parts are temporarily stored before being used in production is considered an example of:

A) Choice A

B) Choice B

C) Choice C

D) Choice D

A) Choice A

B) Choice B

C) Choice C

D) Choice D

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

64

Which of the following is an example of a period cost in a company that makes clothing?

A) Fabric used to produce men's pants.

B) Advertising cost for a new line of clothing.

C) Factory supervisor's salary.

D) Monthly depreciation on production equipment.

A) Fabric used to produce men's pants.

B) Advertising cost for a new line of clothing.

C) Factory supervisor's salary.

D) Monthly depreciation on production equipment.

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

65

All of the following are examples of product costs except:

A) depreciation on the company's retail outlets.

B) salary of the plant manager.

C) insurance on the factory equipment.

D) rental costs of factory equipment.

A) depreciation on the company's retail outlets.

B) salary of the plant manager.

C) insurance on the factory equipment.

D) rental costs of factory equipment.

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

66

The salary paid to the president of a company would be classified on the income statement as a(n):

A) administrative expense.

B) direct labor cost.

C) manufacturing overhead cost.

D) selling expense.

A) administrative expense.

B) direct labor cost.

C) manufacturing overhead cost.

D) selling expense.

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

67

The costs of direct materials are classified as:

A) Choice A

B) Choice B

C) Choice C

D) Choice D

A) Choice A

B) Choice B

C) Choice C

D) Choice D

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

68

The cost of direct materials is classified as a:

A) Choice A

B) Choice B

C) Choice C

D) Choice D

A) Choice A

B) Choice B

C) Choice C

D) Choice D

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

69

Traditional format income statements are widely used for preparing external financial statements.

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

70

Rotonga Manufacturing Company leases a vehicle to deliver its finished products to customers. Which of the following terms correctly describes the monthly lease payments made on the delivery vehicle?

A) Direct Cost - Yes; Fixed Cost - Yes

B) Direct Cost - Yes; Fixed Cost - No

C) Direct Cost - No; Fixed Cost - Yes

D) Direct Cost - No; Fixed Cost - No

A) Direct Cost - Yes; Fixed Cost - Yes

B) Direct Cost - Yes; Fixed Cost - No

C) Direct Cost - No; Fixed Cost - Yes

D) Direct Cost - No; Fixed Cost - No

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

71

Materials used in a factory that are not an integral part of the final product, such as cleaning supplies, should be classified as:

A) direct materials.

B) a period cost.

C) administrative expense.

D) manufacturing overhead.

A) direct materials.

B) a period cost.

C) administrative expense.

D) manufacturing overhead.

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

72

Which of the following costs is classified as both a prime cost and a conversion cost?

A) Direct materials.

B) Direct labor.

C) Variable overhead.

D) Fixed overhead.

A) Direct materials.

B) Direct labor.

C) Variable overhead.

D) Fixed overhead.

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

73

Which of the following statements concerning direct and indirect costs is NOT true?

A) Whether a particular cost is classified as direct or indirect does not depend on the cost object.

B) A direct cost is one that can be easily traced to the particular cost object.

C) The factory manager's salary would be classified as an indirect cost of producing one unit of product.

D) A particular cost may be direct or indirect, depending on the cost object.

A) Whether a particular cost is classified as direct or indirect does not depend on the cost object.

B) A direct cost is one that can be easily traced to the particular cost object.

C) The factory manager's salary would be classified as an indirect cost of producing one unit of product.

D) A particular cost may be direct or indirect, depending on the cost object.

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

74

Which of the following is NOT a period cost?

A) Depreciation of factory maintenance equipment.

B) Salary of a clerk who handles customer billing.

C) Insurance on a company showroom where customers can view new products.

D) Cost of a seminar concerning tax law updates that was attended by the company's controller.

A) Depreciation of factory maintenance equipment.

B) Salary of a clerk who handles customer billing.

C) Insurance on a company showroom where customers can view new products.

D) Cost of a seminar concerning tax law updates that was attended by the company's controller.

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

75

The cost of electricity for running production equipment is classified as:

A) Choice A

B) Choice B

C) Choice C

D) Choice D

A) Choice A

B) Choice B

C) Choice C

D) Choice D

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

76

The cost of lubricants used to grease a production machine in a manufacturing company is an example of a(n):

A) period cost.

B) direct material cost.

C) indirect material cost.

D) opportunity cost.

A) period cost.

B) direct material cost.

C) indirect material cost.

D) opportunity cost.

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

77

A factory supervisor's wages are classified as:

A) Indirect labor - No; Fixed manufacturing overhead - No

B) Indirect labor - Yes; Fixed manufacturing overhead - Yes

C) Indirect labor - Yes; Fixed manufacturing overhead - No

D) Indirect labor - No; Fixed manufacturing overhead - Yes

A) Indirect labor - No; Fixed manufacturing overhead - No

B) Indirect labor - Yes; Fixed manufacturing overhead - Yes

C) Indirect labor - Yes; Fixed manufacturing overhead - No

D) Indirect labor - No; Fixed manufacturing overhead - Yes

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

78

Manufacturing overhead includes:

A) all direct material, direct labor and administrative costs.

B) all manufacturing costs except direct labor.

C) all manufacturing costs except direct labor and direct materials.

D) all selling and administrative costs.

A) all direct material, direct labor and administrative costs.

B) all manufacturing costs except direct labor.

C) all manufacturing costs except direct labor and direct materials.

D) all selling and administrative costs.

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

79

Which of the following would most likely NOT be included as manufacturing overhead in a furniture factory?

A) The cost of the glue in a chair.

B) The amount paid to the individual who stains a chair.

C) The workman's compensation insurance of the supervisor who oversees production.

D) The factory utilities of the department in which production takes place.

A) The cost of the glue in a chair.

B) The amount paid to the individual who stains a chair.

C) The workman's compensation insurance of the supervisor who oversees production.

D) The factory utilities of the department in which production takes place.

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

80

Product costs that have become expenses can be found in:

A) period costs.

B) selling expenses.

C) cost of goods sold.

D) administrative expenses.

A) period costs.

B) selling expenses.

C) cost of goods sold.

D) administrative expenses.

Unlock Deck

Unlock for access to all 299 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 299 flashcards in this deck.