Deck 12: Interim Reporting and Disclosures About Segments of an Enterprise

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Abitz Corporation has the following pretax operating income in its first three quarters of 20X5. The effective tax rate for each quarter is provided. Determine the third quarter income tax or benefit.

A) $3,750

B) $15,000

C) $15,750

D) $20,000

A) $3,750

B) $15,000

C) $15,750

D) $20,000

Question

Question

Question

Question

Scott Inc. expects to have financial income of $375,000 for 20X1 and estimates annual tax credits of $22,500. Included in Scott's income is interest income on municipal securities totaling $45,000 and meals and entertainment expenses of $62,500 of which 50% are not deductible under current tax code. Assume that the graduated tax rate schedule is as follows:

Required:

Required:

Determine the tax expense for the first quarter, assuming that taxable income is $85,000.

Required:Determine the tax expense for the first quarter, assuming that taxable income is $85,000.

Question

Question

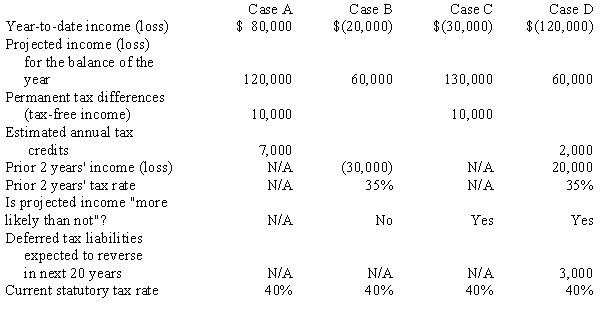

For each of the following independent cases, determine the estimated effective tax rate to be used for the current quarter's interim statements.

Question

Question

Millstone Company's first-quarter 20X3, pretax income is $25,000. The company anticipates an annual tax credit of $5,500. Millstone is projecting income for the remaining three quarters of $95,000. For the second quarter of 20X4, Millstone reports $55,000 of pretax income with a projected pre-tax income for the remainder of the year of $65,000. Millstone does not have any permanent differences between taxable income and financial income.

In the second quarter, Millstone decided to change their depreciation method used for financial reporting purposes. The change in depreciation methods has the following effect on the calculation and projection of income for Millstone:

The effect of the change on prior years is a decrease to retained earnings of $30,000.

The effect of the change on prior years is a decrease to retained earnings of $30,000.

The current tax schedule is:

Required:

Required:

Calculate the first and second quarter interim tax expenses on continuing income.

In the second quarter, Millstone decided to change their depreciation method used for financial reporting purposes. The change in depreciation methods has the following effect on the calculation and projection of income for Millstone:

The effect of the change on prior years is a decrease to retained earnings of $30,000.The current tax schedule is:

Required:Calculate the first and second quarter interim tax expenses on continuing income.

Question

Question

Question

Question

Question

Cracker Corporation's first-quarter 20X4, pretax income is $55,000. The company anticipates an annual tax credit of $15,500. Cracker is projecting income for the remaining three quarters of $135,000. For the second quarter of 20X4, Cracker reports $85,000 of pretax income with a projected pre-tax income for the remainder of the year of $165,000. Cracker does not have any permanent differences between taxable income and financial income.

In the second quarter, Cracker suffers an uninsured loss of one of its warehouses. The loss is determined to be unusual in nature and infrequent in occurrence. The amount of the loss is determined to be $140,000.

The current tax schedule is:

Required:

Required:

Calculate the first and second quarter interim tax expenses on continuing income and on the non-ordinary item.

In the second quarter, Cracker suffers an uninsured loss of one of its warehouses. The loss is determined to be unusual in nature and infrequent in occurrence. The amount of the loss is determined to be $140,000.

The current tax schedule is:

Required:Calculate the first and second quarter interim tax expenses on continuing income and on the non-ordinary item.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Lancaster Inc. expects to have taxable income of $275,000 for 20X1 and a tax credit of $12,250. Assume that the graduated tax rate schedule is as follows:

Required:

Required:

Determine the tax expense for the first quarter, assuming that taxable income is $65,000.

Required:Determine the tax expense for the first quarter, assuming that taxable income is $65,000.

Question

Question

Question

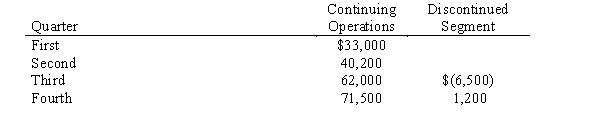

East Company, a highly diversified corporation, reports the results of operations quarterly. At the beginning of the third quarter, management decided to discontinue its recreational division. At this time, a formal plan was authorized, calling for disposal by year end. Results for the current year, excluding taxes, are as follows:

The following additional information was provided:

The following additional information was provided:

a.

The first two quarters include results of operations of the discontinued segment. The segment reported first and second quarter pretax losses of $8,000 and $12,000, respectively.

b.

The estimated annual income tax rate in the first and second quarters was 35%. Because of the decision to discontinue, the revised annual effective tax rate was determined to be 40%.

Required:

For each quarter, present the results of operations and the related tax expense or tax benefit. Where applicable, include the original and restated amounts in the presentation.

The following additional information was provided: a.

The first two quarters include results of operations of the discontinued segment. The segment reported first and second quarter pretax losses of $8,000 and $12,000, respectively.

b.

The estimated annual income tax rate in the first and second quarters was 35%. Because of the decision to discontinue, the revised annual effective tax rate was determined to be 40%.

Required:

For each quarter, present the results of operations and the related tax expense or tax benefit. Where applicable, include the original and restated amounts in the presentation.

Question

Question

Consider the following:

Case A

Income (loss) for quarters 1 through 4 is ($50,000), $30,000, $40,000, and $40,000, respectively. Future projected income for the year is uncertain at the end of quarters 1 and 2. Annual income at the end of quarter 3 is estimated to be $20,000. No carryback benefit exists, and any future annual benefit is uncertain.

Case B

Assume the same facts as in Case A. However, at the end of quarters 1 through 3, annual income is estimated to be $40,000.

Case C

Quarterly income (loss) levels were $15,000, ($35,000), ($75,000), and $25,000. A yearly operating loss of $70,000 was anticipated throughout the year. Prior years' income of $28,000 is available for carryback. The same tax rates were relevant to the carryback period

Required:

For cases A through C, complete the schedule that follows: Assume that the statutory tax rate is 15% on the first $50,000 of income, 25% on the next $25,000, and 30% on income in excess of $75,000.

Case A

Income (loss) for quarters 1 through 4 is ($50,000), $30,000, $40,000, and $40,000, respectively. Future projected income for the year is uncertain at the end of quarters 1 and 2. Annual income at the end of quarter 3 is estimated to be $20,000. No carryback benefit exists, and any future annual benefit is uncertain.

Case B

Assume the same facts as in Case A. However, at the end of quarters 1 through 3, annual income is estimated to be $40,000.

Case C

Quarterly income (loss) levels were $15,000, ($35,000), ($75,000), and $25,000. A yearly operating loss of $70,000 was anticipated throughout the year. Prior years' income of $28,000 is available for carryback. The same tax rates were relevant to the carryback period

Required:

For cases A through C, complete the schedule that follows: Assume that the statutory tax rate is 15% on the first $50,000 of income, 25% on the next $25,000, and 30% on income in excess of $75,000.

Question

Question

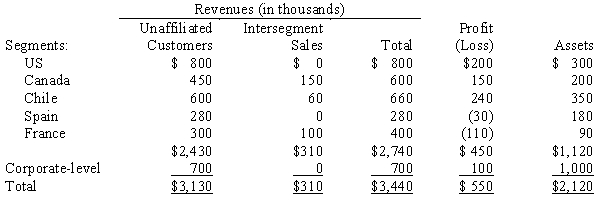

Santas Corporation is a diversified firm with operations in the United States, Canada, Chile, Spain, and France, each of which qualifies as a geographic segment. Data with respect to those segments follows:

Required:

Required:

Determine which of the Santas segments would be reportable segments, and explain why.

Required:Determine which of the Santas segments would be reportable segments, and explain why.

Question

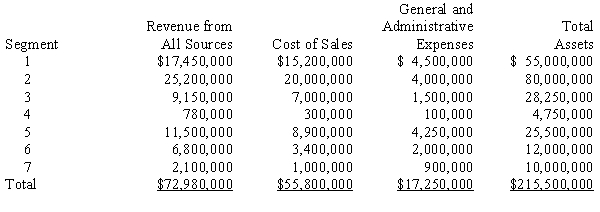

Information about the seven segments of the Kenny Corporation is presented below. Determine which of the segments are reportable and why.

Question

Question

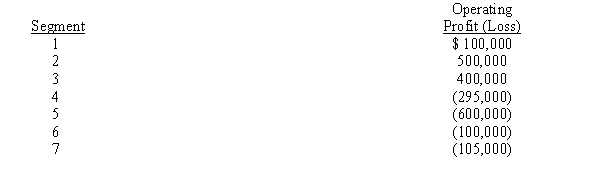

Adam Enterprise includes seven industry segments. Operating profits (losses) relating to those segments are:

Required:

Required:

Based only on the above operating profit(loss) information, which of Adam's segments would be reported separately?

Required:Based only on the above operating profit(loss) information, which of Adam's segments would be reported separately?

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/50

Play

Full screen (f)

Deck 12: Interim Reporting and Disclosures About Segments of an Enterprise

1

Which of the following statements about interim reporting is false?

A) If a company reports year-to-date financial information for the current year, it also must report the last twelve month-to-date information.

B) Under some circumstances, a company can restate the financial information of an earlier current-year quarter.

C) Tax benefits arising from earlier interim periods in the current year can be carried forward to the current interim period to offset tax expense.

D) The total of all nonordinary losses in the current quarter multiplied by the effective tax rate equals the amount of tax expense to be allocated among those losses.

A) If a company reports year-to-date financial information for the current year, it also must report the last twelve month-to-date information.

B) Under some circumstances, a company can restate the financial information of an earlier current-year quarter.

C) Tax benefits arising from earlier interim periods in the current year can be carried forward to the current interim period to offset tax expense.

D) The total of all nonordinary losses in the current quarter multiplied by the effective tax rate equals the amount of tax expense to be allocated among those losses.

A

2

For interim reporting, which of the following statements is true?

A) Under a standard cost system, unplanned or unanticipated variances should be recognized in the quarter in which they occur.

B) Under the LIFO method, recognition of layer liquidations, thought to be temporary, are postponed by using replacement cost in the calculation of interim cost of goods sold.

C) Under the lower of cost or market determination of ending inventory, a gain may not be recognized in an interim period.

D) All of these statements are true.

A) Under a standard cost system, unplanned or unanticipated variances should be recognized in the quarter in which they occur.

B) Under the LIFO method, recognition of layer liquidations, thought to be temporary, are postponed by using replacement cost in the calculation of interim cost of goods sold.

C) Under the lower of cost or market determination of ending inventory, a gain may not be recognized in an interim period.

D) All of these statements are true.

B

3

In order to generate interim financial reports that contain a reasonable portion of annual expenses, which of the following statements is true?

A) an allocation of a portion of an annual bonus would be made as an interim adjustment

B) any adjustments for inventory shrinkage would be deferred to year end

C) the allowance for uncollectible accounts receivable will be revised at year end

D) None of the above are true

A) an allocation of a portion of an annual bonus would be made as an interim adjustment

B) any adjustments for inventory shrinkage would be deferred to year end

C) the allowance for uncollectible accounts receivable will be revised at year end

D) None of the above are true

A

4

When a company makes a second quarter decision to discontinue a segment, the first quarter tax expense:

A) Results are not restated.

B) is split between the tax expense calculated on restated quarter one income from continuing operations and the discontinued segment by subtracting the tax expenses calculated on the restated first quarter income from the original tax expense calculated for the first quarter, before the decision was made.

C) is used to determine the incremental tax effect.

D) is used to calculate the effective tax rate for the discontinued segment.

A) Results are not restated.

B) is split between the tax expense calculated on restated quarter one income from continuing operations and the discontinued segment by subtracting the tax expenses calculated on the restated first quarter income from the original tax expense calculated for the first quarter, before the decision was made.

C) is used to determine the incremental tax effect.

D) is used to calculate the effective tax rate for the discontinued segment.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

5

Nonordinary items resulting in income or loss

A) include unusual but not infrequent gains.

B) are treated the same as ordinary items when calculating the effective tax rate.

C) are always treated as a total group when calculating the effective rate for the quarter.

D) are always excluded from interim reporting.

A) include unusual but not infrequent gains.

B) are treated the same as ordinary items when calculating the effective tax rate.

C) are always treated as a total group when calculating the effective rate for the quarter.

D) are always excluded from interim reporting.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

6

Abel Corporation sold equipment in the first quarter of 20X5 at a $150,000 loss. How much of the loss should appear in the 20X5 second- and third-quarter income?

A) $37,500 and $37,500

B) $50,000 and $50,000

C) $0 and $0

D) $100,000 and $0

A) $37,500 and $37,500

B) $50,000 and $50,000

C) $0 and $0

D) $100,000 and $0

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

7

Which of the following statements is NOT true concerning the determination of the effective tax rate to be used for interim reporting?

A) Tax rate changes should not be accounted for retroactively.

B) The effective tax rate for the entire year should be estimated.

C) The effective tax rate should reflect anticipated tax credits.

D) The estimated tax rate should reflect extraordinary items.

A) Tax rate changes should not be accounted for retroactively.

B) The effective tax rate for the entire year should be estimated.

C) The effective tax rate should reflect anticipated tax credits.

D) The estimated tax rate should reflect extraordinary items.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

8

During the first quarter, a company's application of lower of cost or market methods indicated a $150,000 loss from a temporary market decline, which is expected to be restored in the fiscal year. During the second quarter, the market reversed the decline. Which of the following situations indicates a proper treatment of these facts?

A) A $37,500 loss recognized in the first quarter and no recovery recognized in the second quarter.

B) A $150,000 loss recognized in the first quarter and a $90,000 recovery in the second quarter.

C) A $150,000 loss recognized in the first quarter and a $50,000 recovery in the second quarter.

D) No loss recognized in the first quarter and no recovery recognized in the second quarter.

A) A $37,500 loss recognized in the first quarter and no recovery recognized in the second quarter.

B) A $150,000 loss recognized in the first quarter and a $90,000 recovery in the second quarter.

C) A $150,000 loss recognized in the first quarter and a $50,000 recovery in the second quarter.

D) No loss recognized in the first quarter and no recovery recognized in the second quarter.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

9

Which of the following is NOT considered when determining whether an operating segment qualifies as a reportable segment?

A) revenue of the segment

B) the assets of the segment

C) the number of foreign offices

D) the absolute amount of its profit or loss

A) revenue of the segment

B) the assets of the segment

C) the number of foreign offices

D) the absolute amount of its profit or loss

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

10

The acquisition of a paper mill by a large publishing company is an example of

A) horizontal integration.

B) vertical integration.

C) diversification.

D) consolidation.

A) horizontal integration.

B) vertical integration.

C) diversification.

D) consolidation.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

11

Which of the following best describes the treatment given a change in accounting principles made during the second quarter?

A) The cumulative effect should be recognized in the quarter in which the decision to change is made.

B) Regardless of the quarter of change, the recognition is deferred until year end.

C) All prior interim periods are retrospectively restated.

D) Interim periods prior to the period of change are not restated.

A) The cumulative effect should be recognized in the quarter in which the decision to change is made.

B) Regardless of the quarter of change, the recognition is deferred until year end.

C) All prior interim periods are retrospectively restated.

D) Interim periods prior to the period of change are not restated.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

12

The primary emphasis of interim reporting is on:

A) interim cash flow

B) the interim statement of financial position

C) interim retained earnings

D) interim income data

A) interim cash flow

B) the interim statement of financial position

C) interim retained earnings

D) interim income data

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

13

Which of the following best describes how the tax benefit resulting from the extraordinary loss in an interim period is recognized?

A) The tax benefit is recognized in the period in which it occurs using the estimated effective rate.

B) The tax benefit is recognized in the period in which it occurs using the average tax rate for all income.

C) The tax benefit is allocated over the current and remaining periods using the estimated effective rate.

D) The tax benefit is recognized only if, more likely than not, the loss may be offset against income.

A) The tax benefit is recognized in the period in which it occurs using the estimated effective rate.

B) The tax benefit is recognized in the period in which it occurs using the average tax rate for all income.

C) The tax benefit is allocated over the current and remaining periods using the estimated effective rate.

D) The tax benefit is recognized only if, more likely than not, the loss may be offset against income.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

14

Which of the following is not a limitation on the number of reportable segments?

A) Consistency, i.e., the number of reportable segments this period, must be the same as last period.

B) Usually the number of segments should not exceed 10.

C) At least 75% of the combined revenue of sales to unaffiliated firms should be traceable to reportable segments.

D) None of the above is a limitation.

A) Consistency, i.e., the number of reportable segments this period, must be the same as last period.

B) Usually the number of segments should not exceed 10.

C) At least 75% of the combined revenue of sales to unaffiliated firms should be traceable to reportable segments.

D) None of the above is a limitation.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

15

The incremental income tax effect utilized to determine the tax effect of an extraordinary item is calculated by:

A) applying the estimated effective tax rate against the amount of the extraordinary item

B) the difference between the gross tax calculated on continuing operations and the gross tax on income from all sources, before tax credits are applied.

C) the difference between the estimated net tax calculated on the projected annual income from continuing operations and the estimated net tax calculated on projected annual income, including the non-ordinary items, after tax credits have been considered

D) none of the above.

A) applying the estimated effective tax rate against the amount of the extraordinary item

B) the difference between the gross tax calculated on continuing operations and the gross tax on income from all sources, before tax credits are applied.

C) the difference between the estimated net tax calculated on the projected annual income from continuing operations and the estimated net tax calculated on projected annual income, including the non-ordinary items, after tax credits have been considered

D) none of the above.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

16

Which of the following items should be disclosed with interim data?

A) basic and diluted earnings per share

B) contingent items

C) changes in accounting estimates

D) all of the above

A) basic and diluted earnings per share

B) contingent items

C) changes in accounting estimates

D) all of the above

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

17

If a company is utilizing LIFO inventory costing, what might be the effect on the calculation of Cost of Goods sold in an interim financial statement?

A) cost of goods sold is calculated on a historical cost basis only

B) the interim cost of goods sold includes the replacement cost of temporarily liquidated inventory

C) cost of goods sold is not adjusted for any changes due to liquidation of LIFO inventory

D) any of the effects of liquidation are deferred until year end

A) cost of goods sold is calculated on a historical cost basis only

B) the interim cost of goods sold includes the replacement cost of temporarily liquidated inventory

C) cost of goods sold is not adjusted for any changes due to liquidation of LIFO inventory

D) any of the effects of liquidation are deferred until year end

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

18

Abitz Corporation has the following pretax operating income in its first three quarters of 20X5. The effective tax rate for each quarter is provided. Determine the third quarter income tax or benefit.

A) $3,750

B) $15,000

C) $15,750

D) $20,000

A) $3,750

B) $15,000

C) $15,750

D) $20,000

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

19

In determining if two operating segments may be combined into one, which of the following factors should be considered?

A) similarities regarding profit margins

B) whether the nature of the products and services is similar

C) whether there is a similar amount of intracompany sales

D) whether there is a similar number of employees

A) similarities regarding profit margins

B) whether the nature of the products and services is similar

C) whether there is a similar amount of intracompany sales

D) whether there is a similar number of employees

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

20

Which of the following best describes the proper accounting for interim financial reports?

A) The interim period is viewed as an integral part of the annual accounting period.

B) The interim period is viewed as a distinct, independent accounting period.

C) Interim net income should be determined by using the same principles as those for the annual accounting period.

D) Net income should be computed on the cash basis except for sales, cost of goods sold, and depreciation.

A) The interim period is viewed as an integral part of the annual accounting period.

B) The interim period is viewed as a distinct, independent accounting period.

C) Interim net income should be determined by using the same principles as those for the annual accounting period.

D) Net income should be computed on the cash basis except for sales, cost of goods sold, and depreciation.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

21

Futura Corporation reported pretax net income of $30,000 in the first quarter of 20X1. The company anticipated pretax net income of $90,000 for the year. During the second quarter, after issuing the first-quarter interim statement, Futura decided to discontinue its electronics division and adopted a formal plan for its disposal.

During the first quarter, the biotech division reported a pretax loss of $70,000 and estimated a $270,000 operating loss for the year. During the second quarter, the division experienced an operating loss of $35,000 prior to the measurement date and $8,000 in the remainder of that quarter. The anticipated loss on the disposal of that division's assets was $40,000.

Futura had a flat 25% tax rate for 20X1. The firm is expecting a $5,000 tax credit attributed to operations outside of the electronic division. Second-quarter pretax income for the nonelectronics operations was $40,000. As of the end of the second quarter, annual pretax income of $225,000 was anticipated for continuing operations.

Required:

In good form, prepare a schedule showing the income (loss) and tax expense (benefit) determination for the first quarter, the restated first quarter, and the second quarter.

During the first quarter, the biotech division reported a pretax loss of $70,000 and estimated a $270,000 operating loss for the year. During the second quarter, the division experienced an operating loss of $35,000 prior to the measurement date and $8,000 in the remainder of that quarter. The anticipated loss on the disposal of that division's assets was $40,000.

Futura had a flat 25% tax rate for 20X1. The firm is expecting a $5,000 tax credit attributed to operations outside of the electronic division. Second-quarter pretax income for the nonelectronics operations was $40,000. As of the end of the second quarter, annual pretax income of $225,000 was anticipated for continuing operations.

Required:

In good form, prepare a schedule showing the income (loss) and tax expense (benefit) determination for the first quarter, the restated first quarter, and the second quarter.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

22

Scott Inc. expects to have financial income of $375,000 for 20X1 and estimates annual tax credits of $22,500. Included in Scott's income is interest income on municipal securities totaling $45,000 and meals and entertainment expenses of $62,500 of which 50% are not deductible under current tax code. Assume that the graduated tax rate schedule is as follows:

Required:

Determine the tax expense for the first quarter, assuming that taxable income is $85,000.

Required:Determine the tax expense for the first quarter, assuming that taxable income is $85,000.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

23

Which of the following statements about required disclosures in segmental reporting is not true?

A) No more than ten segments may be reported.

B) The name of each major customer does not have to be disclosed.

C) Even if there is only one reportable segment, the company must report revenues from external customers for each product or service or each group of related products or services.

D) Segmental information must be included in interim reporting.

A) No more than ten segments may be reported.

B) The name of each major customer does not have to be disclosed.

C) Even if there is only one reportable segment, the company must report revenues from external customers for each product or service or each group of related products or services.

D) Segmental information must be included in interim reporting.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

24

For each of the following independent cases, determine the estimated effective tax rate to be used for the current quarter's interim statements.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

25

Corriveau Industries decided to switch from an accelerated depreciation method to a straight-line method in the second quarter of 20X1. This is classified as a cumulative effect of a change in accounting principle. The first-quarter, pretax income reported was $30,000, and projected pretax income for 20X1 was $90,000. If Corriveau had used straight-line depreciation for the quarter, pretax income would have been $35,000 and projected pretax income for 20X1 would have been $110,000. The cumulative effect on prior years from the change is a $50,000 increase in retained earnings. The second-quarter income using straight-line depreciation is $20,000, and the expected annual earnings continue to be $110,000. Assume that Corriveau is subject to a flat 25% statutory tax rate for 20X1. Corriveau is expecting $5,000 of tax-free income during the third and fourth quarters of 20X1.

Required:

For all categories of income, calculate the interim tax expense for the first quarter, first quarter restated, and second quarter.

Required:

For all categories of income, calculate the interim tax expense for the first quarter, first quarter restated, and second quarter.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

26

Millstone Company's first-quarter 20X3, pretax income is $25,000. The company anticipates an annual tax credit of $5,500. Millstone is projecting income for the remaining three quarters of $95,000. For the second quarter of 20X4, Millstone reports $55,000 of pretax income with a projected pre-tax income for the remainder of the year of $65,000. Millstone does not have any permanent differences between taxable income and financial income.

In the second quarter, Millstone decided to change their depreciation method used for financial reporting purposes. The change in depreciation methods has the following effect on the calculation and projection of income for Millstone:

The effect of the change on prior years is a decrease to retained earnings of $30,000.

The current tax schedule is:

Required:

Calculate the first and second quarter interim tax expenses on continuing income.

In the second quarter, Millstone decided to change their depreciation method used for financial reporting purposes. The change in depreciation methods has the following effect on the calculation and projection of income for Millstone:

The effect of the change on prior years is a decrease to retained earnings of $30,000.The current tax schedule is:

Required:Calculate the first and second quarter interim tax expenses on continuing income.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

27

With regard to major customers, which of the following items is not true?

A) If it qualifies, the federal government is considered a single major customer.

B) The total amount of the sales to each major customer must be disclosed.

C) The names of the major customers must be disclosed.

D) The identity of the segments making the sales must be disclosed.

A) If it qualifies, the federal government is considered a single major customer.

B) The total amount of the sales to each major customer must be disclosed.

C) The names of the major customers must be disclosed.

D) The identity of the segments making the sales must be disclosed.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

28

A corporation made up of an automobile manufacturer, a plastics maker, a spark plug manufacturer, a steel mill, and a battery maker is an example of a

A) horizontally-integrated company.

B) vertically-integrated company.

C) diversified company.

D) conglomerate.

A) horizontally-integrated company.

B) vertically-integrated company.

C) diversified company.

D) conglomerate.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

29

The management approach to segmental reporting

A) focuses on how management organizes information for internal decision making.

B) requires that the company's chief executive officer decide what segments will be reported.

C) separates the costs of management from the costs of operations to determine segment profit or loss.

D) is required only in the United States.

A) focuses on how management organizes information for internal decision making.

B) requires that the company's chief executive officer decide what segments will be reported.

C) separates the costs of management from the costs of operations to determine segment profit or loss.

D) is required only in the United States.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

30

It is possible for segments to qualify as reportable, but not represent a material portion of the enterprise. What test is applied to ensure the segments reported represent a significant portion of enterprise activity?

A) Combined external segment revenues for reportable segments exceed 75% of internal and external segment revenues.

B) Total internal and external segment revenue exceeds 75% of total consolidated revenue.

C) Total external segment revenue of the reportable segments exceeds 75% of consolidated revenue.

D) Total segment assets of the reportable segments exceeds 75% of total consolidated assets.

A) Combined external segment revenues for reportable segments exceed 75% of internal and external segment revenues.

B) Total internal and external segment revenue exceeds 75% of total consolidated revenue.

C) Total external segment revenue of the reportable segments exceeds 75% of consolidated revenue.

D) Total segment assets of the reportable segments exceeds 75% of total consolidated assets.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

31

Cracker Corporation's first-quarter 20X4, pretax income is $55,000. The company anticipates an annual tax credit of $15,500. Cracker is projecting income for the remaining three quarters of $135,000. For the second quarter of 20X4, Cracker reports $85,000 of pretax income with a projected pre-tax income for the remainder of the year of $165,000. Cracker does not have any permanent differences between taxable income and financial income.

In the second quarter, Cracker suffers an uninsured loss of one of its warehouses. The loss is determined to be unusual in nature and infrequent in occurrence. The amount of the loss is determined to be $140,000.

The current tax schedule is:

Required:

Calculate the first and second quarter interim tax expenses on continuing income and on the non-ordinary item.

In the second quarter, Cracker suffers an uninsured loss of one of its warehouses. The loss is determined to be unusual in nature and infrequent in occurrence. The amount of the loss is determined to be $140,000.

The current tax schedule is:

Required:Calculate the first and second quarter interim tax expenses on continuing income and on the non-ordinary item.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

32

Good Time, Inc. is a worldwide manufacturer of toys and games. In accordance with generally accepted accounting principles, quarterly statements are prepared. At the end of the first quarter of 20X2, the following data have been collected from the financial records:

a.

Sales were $14,680,000.

b.

Expenses related directly to the sales were $10,600,000, of which $9,500,000 related to the cost of goods sold.

c.

Good Time, Inc. employs the LIFO method for inventory valuation and has liquidated a portion of its beginning inventory. The liquidation was in the amount of $600,000, which is included in the cost of goods sold of $9,500,000, and the cost to replace this inventory will be $1,400,000.

d.

Other transactions during the first quarter were as follows:

(1)

Research and development costs were incurred in the amount of $4,000,000 and are expected to benefit equally the next 3 years.

(2)

Advertising costs were $75,000, of which one-third related to the first-quarter sales.

(3)

There was a gain on the early extinguishment of debt in the amount of $1,115,000.

Assume that Good Time, Inc. had 500,000 shares of common stock outstanding throughout the first quarter.

Required:

In good form, present the quarterly income statement of Good Time, Inc. (assume an effective income tax rate of 40%).

a.

Sales were $14,680,000.

b.

Expenses related directly to the sales were $10,600,000, of which $9,500,000 related to the cost of goods sold.

c.

Good Time, Inc. employs the LIFO method for inventory valuation and has liquidated a portion of its beginning inventory. The liquidation was in the amount of $600,000, which is included in the cost of goods sold of $9,500,000, and the cost to replace this inventory will be $1,400,000.

d.

Other transactions during the first quarter were as follows:

(1)

Research and development costs were incurred in the amount of $4,000,000 and are expected to benefit equally the next 3 years.

(2)

Advertising costs were $75,000, of which one-third related to the first-quarter sales.

(3)

There was a gain on the early extinguishment of debt in the amount of $1,115,000.

Assume that Good Time, Inc. had 500,000 shares of common stock outstanding throughout the first quarter.

Required:

In good form, present the quarterly income statement of Good Time, Inc. (assume an effective income tax rate of 40%).

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

33

The following events took place in Morgan Corporation's second quarter.

a.

An expired insurance policy was replaced by a $12,000, 12-month policy.

b.

Morgan sold marketable securities at a $10,000 gain.

c.

Research and development costs of $15,000, which were expected to benefit the company over the next 12 months, were incurred.

d.

On the first day of the quarter, Morgan signed a one-year, $100,000 bank note carrying an 8% interest rate.

e.

Used equipment with a book value of $36,000 was sold for $18,000.

Required:

Determine the effect of the above events on Morgan Corporation's second-quarter income.

a.

An expired insurance policy was replaced by a $12,000, 12-month policy.

b.

Morgan sold marketable securities at a $10,000 gain.

c.

Research and development costs of $15,000, which were expected to benefit the company over the next 12 months, were incurred.

d.

On the first day of the quarter, Morgan signed a one-year, $100,000 bank note carrying an 8% interest rate.

e.

Used equipment with a book value of $36,000 was sold for $18,000.

Required:

Determine the effect of the above events on Morgan Corporation's second-quarter income.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

34

Scenario 12-1

Ansfield, Inc. has several potentially reportable segments. The following financial information has been determined for the current fiscal year:

-Refer to Scenario 12-1. The minimum amount of revenues a segment must have to qualify as reportable is ____.

A) $700,000

B) $800,000

C) $820,000

D) The answer cannot be determined from the information given.

Ansfield, Inc. has several potentially reportable segments. The following financial information has been determined for the current fiscal year:

-Refer to Scenario 12-1. The minimum amount of revenues a segment must have to qualify as reportable is ____.

A) $700,000

B) $800,000

C) $820,000

D) The answer cannot be determined from the information given.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

35

Abbott Inc. began the year with 750 units of inventory valued at $20 each under LIFO. During the first quarter, 300 units were purchased at $25 each and another 250 units were purchased at $28 each. Assume that 200 units are on hand at the end of the first quarter and that the current replacement cost is $30 per unit.

Required:

If Abbott plans to have 500 units on hand at year end, determine the cost of goods sold for the first quarter.

Required:

If Abbott plans to have 500 units on hand at year end, determine the cost of goods sold for the first quarter.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

36

Scenario 12-1

Ansfield, Inc. has several potentially reportable segments. The following financial information has been determined for the current fiscal year:

-Refer to Scenario 12-1. The minimum amount of assets a segment must have to qualify as reportable is ____.

A) $4,500,000

B) $5,000,000

C) $37,500,000

D) The answer cannot be determined from the information given.

Ansfield, Inc. has several potentially reportable segments. The following financial information has been determined for the current fiscal year:

-Refer to Scenario 12-1. The minimum amount of assets a segment must have to qualify as reportable is ____.

A) $4,500,000

B) $5,000,000

C) $37,500,000

D) The answer cannot be determined from the information given.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

37

In determining whether a segment should be reported, a profit and loss test can be used. The test selects segments for reporting by:

A) only including profitable segments.

B) comparing the absolute value of a segment's profit or loss to 10% of all segments cumulative profit or cumulative loss, whichever is higher.

C) comparing the absolute value of a segment's profit or loss to 10% of all segments combined profits and losses.

D) comparing the profit or loss of a segment to 10% of all segment external revenue.

A) only including profitable segments.

B) comparing the absolute value of a segment's profit or loss to 10% of all segments cumulative profit or cumulative loss, whichever is higher.

C) comparing the absolute value of a segment's profit or loss to 10% of all segments combined profits and losses.

D) comparing the profit or loss of a segment to 10% of all segment external revenue.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

38

Scenario 12-1

Ansfield, Inc. has several potentially reportable segments. The following financial information has been determined for the current fiscal year:

-Refer to Scenario 12-1. For Ansfield, Inc. to report a significant portion of its financial information as segments, its segments, in total, must represent

A) $37,500,000 in assets.

B) $6,000,000 in revenues.

C) $1,125,000 in operating income before taxes.

D) The answer cannot be determined from the information given.

Ansfield, Inc. has several potentially reportable segments. The following financial information has been determined for the current fiscal year:

-Refer to Scenario 12-1. For Ansfield, Inc. to report a significant portion of its financial information as segments, its segments, in total, must represent

A) $37,500,000 in assets.

B) $6,000,000 in revenues.

C) $1,125,000 in operating income before taxes.

D) The answer cannot be determined from the information given.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

39

Scenario 12-1

Ansfield, Inc. has several potentially reportable segments. The following financial information has been determined for the current fiscal year:

-Refer to Scenario 12-1. The minimum amount of profit or loss a segment must have to qualify as reported is ____.

A) $100,000

B) $135,000

C) $150,000

D) The answer cannot be determined from the information given.

Ansfield, Inc. has several potentially reportable segments. The following financial information has been determined for the current fiscal year:

-Refer to Scenario 12-1. The minimum amount of profit or loss a segment must have to qualify as reported is ____.

A) $100,000

B) $135,000

C) $150,000

D) The answer cannot be determined from the information given.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

40

Lancaster Inc. expects to have taxable income of $275,000 for 20X1 and a tax credit of $12,250. Assume that the graduated tax rate schedule is as follows:

Required:

Determine the tax expense for the first quarter, assuming that taxable income is $65,000.

Required:Determine the tax expense for the first quarter, assuming that taxable income is $65,000.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

41

Allee Co. has pretax, ordinary income of $7,000 and $38,000 in the first and second quarters, respectively. The projected ordinary income for the third and fourth quarters is $60,000 and $30,000. Occurring in the second quarter is a pretax, nonordinary loss of $50,000 and pretax nonordinary income of $35,000. The statutory tax rate is 15% on the first $50,000, 22% on the next $50,000, and 28% on income over $100,000.

Required:

Determine the tax impact traceable to the nonordinary income and nonordinary loss.

Required:

Determine the tax impact traceable to the nonordinary income and nonordinary loss.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

42

For purposes of interim reporting, US-GAAP permits certain modifications to year-end inventory rules.

Required:

Comment on the acceptability of the following independent situations concerning inventory valuation for an interim period:

a.

Management believes that since its firm does not have a perpetual inventory system, it would be too costly to take a physical inventory. Consequently, management has suggested to the accounting department that they estimate ending inventory.

b.

Since the LIFO inventory base was liquidated in the first quarter, management has recommended that the accounting department switch to FIFO valuation of inventory.

c.

Since the first quarter is a slow period for a manufacturing firm, management has suggested that the unfavorable volume variances from the firm's standard cost system be deferred until year end.

Required:

Comment on the acceptability of the following independent situations concerning inventory valuation for an interim period:

a.

Management believes that since its firm does not have a perpetual inventory system, it would be too costly to take a physical inventory. Consequently, management has suggested to the accounting department that they estimate ending inventory.

b.

Since the LIFO inventory base was liquidated in the first quarter, management has recommended that the accounting department switch to FIFO valuation of inventory.

c.

Since the first quarter is a slow period for a manufacturing firm, management has suggested that the unfavorable volume variances from the firm's standard cost system be deferred until year end.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

43

East Company, a highly diversified corporation, reports the results of operations quarterly. At the beginning of the third quarter, management decided to discontinue its recreational division. At this time, a formal plan was authorized, calling for disposal by year end. Results for the current year, excluding taxes, are as follows:

The following additional information was provided:

a.

The first two quarters include results of operations of the discontinued segment. The segment reported first and second quarter pretax losses of $8,000 and $12,000, respectively.

b.

The estimated annual income tax rate in the first and second quarters was 35%. Because of the decision to discontinue, the revised annual effective tax rate was determined to be 40%.

Required:

For each quarter, present the results of operations and the related tax expense or tax benefit. Where applicable, include the original and restated amounts in the presentation.

The following additional information was provided: a.

The first two quarters include results of operations of the discontinued segment. The segment reported first and second quarter pretax losses of $8,000 and $12,000, respectively.

b.

The estimated annual income tax rate in the first and second quarters was 35%. Because of the decision to discontinue, the revised annual effective tax rate was determined to be 40%.

Required:

For each quarter, present the results of operations and the related tax expense or tax benefit. Where applicable, include the original and restated amounts in the presentation.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

44

The management of Trident, Inc. is trying to determine if three of the company's nonreportable segments should be combined into one single segment for reporting purposes. In what five ways must these segments be similar in order to be reported as one?

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

45

Consider the following:

Case A

Income (loss) for quarters 1 through 4 is ($50,000), $30,000, $40,000, and $40,000, respectively. Future projected income for the year is uncertain at the end of quarters 1 and 2. Annual income at the end of quarter 3 is estimated to be $20,000. No carryback benefit exists, and any future annual benefit is uncertain.

Case B

Assume the same facts as in Case A. However, at the end of quarters 1 through 3, annual income is estimated to be $40,000.

Case C

Quarterly income (loss) levels were $15,000, ($35,000), ($75,000), and $25,000. A yearly operating loss of $70,000 was anticipated throughout the year. Prior years' income of $28,000 is available for carryback. The same tax rates were relevant to the carryback period

Required:

For cases A through C, complete the schedule that follows: Assume that the statutory tax rate is 15% on the first $50,000 of income, 25% on the next $25,000, and 30% on income in excess of $75,000.

Case A

Income (loss) for quarters 1 through 4 is ($50,000), $30,000, $40,000, and $40,000, respectively. Future projected income for the year is uncertain at the end of quarters 1 and 2. Annual income at the end of quarter 3 is estimated to be $20,000. No carryback benefit exists, and any future annual benefit is uncertain.

Case B

Assume the same facts as in Case A. However, at the end of quarters 1 through 3, annual income is estimated to be $40,000.

Case C

Quarterly income (loss) levels were $15,000, ($35,000), ($75,000), and $25,000. A yearly operating loss of $70,000 was anticipated throughout the year. Prior years' income of $28,000 is available for carryback. The same tax rates were relevant to the carryback period

Required:

For cases A through C, complete the schedule that follows: Assume that the statutory tax rate is 15% on the first $50,000 of income, 25% on the next $25,000, and 30% on income in excess of $75,000.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

46

The following lists account titles found on the books of Icell Corporation:

a.

Research and Development

b.

Inventory

c.

Annual Bonuses

d.

Unfavorable Materials Usage Variance

Required:

Discuss how each of these items is accounted for in interim financial statements.

a.

Research and Development

b.

Inventory

c.

Annual Bonuses

d.

Unfavorable Materials Usage Variance

Required:

Discuss how each of these items is accounted for in interim financial statements.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

47

Santas Corporation is a diversified firm with operations in the United States, Canada, Chile, Spain, and France, each of which qualifies as a geographic segment. Data with respect to those segments follows:

Required:

Determine which of the Santas segments would be reportable segments, and explain why.

Required:Determine which of the Santas segments would be reportable segments, and explain why.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

48

Information about the seven segments of the Kenny Corporation is presented below. Determine which of the segments are reportable and why.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

49

Explain the difference in the independent and integral viewpoints of accounting for interim periods. Which method best describes the accepted accounting practice for interim financial reporting?

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

50

Adam Enterprise includes seven industry segments. Operating profits (losses) relating to those segments are:

Required:

Based only on the above operating profit(loss) information, which of Adam's segments would be reported separately?

Required:Based only on the above operating profit(loss) information, which of Adam's segments would be reported separately?

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 50 flashcards in this deck.