Advanced Accounting 11th Edition by Paul Fischer,William Tayler, Rita Cheng

Edition 11ISBN: 978-0538480284Advanced Accounting 11th Edition by Paul Fischer,William Tayler, Rita Cheng

Edition 11ISBN: 978-0538480284 Exercise 3

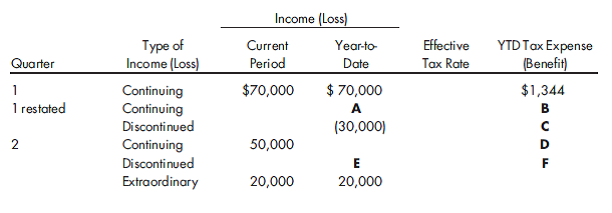

Effective tax rates and nonordinary items. The following schedule was developed forMonroe Corporation to support interim reporting for the year 2014.

The following additional 2014 information is available:

1. The statutory tax rate is as follows: 15% on the first $50,000 of taxable income 20% on the next $50,000 of taxable income 25% on the next $50,000 of taxable income 30% on all additional taxable income

2. At the end of 2013, the first year of operations, the company reported a net operating loss of $80,000 and a tax credit of $5,000. At that time, the company did not recognize any of the tax benefit associated with the operating loss or tax credit. However, the company was hopeful that these benefits could be recognized in the future due to the ability to carry forward both items against future taxable income and taxes.

3. Originally, at the end of the first quarter, the company estimated pretax income for the balance of the year of $60,000.

4. During the second quarter, the company decided to discontinue an operation. Originally, in quarter 1, the operation had reported losses of $30,000 and projected losses for the balance of 2014 in the amount of $40,000. During quarter 2, the discontinued operation reported operating losses of $60,000 and realized losses on the disposal of assets of $25,000. Although not yet realized, the operation anticipated that assets to be sold in the future would net $30,000 less than their book value (carrying value) as reported at the end of quarter 2, 2014.

5. During the second quarter, the company reported pretax income from continuing operations of $50,000 and projected pretax income from continuing operations of $60,000 for the balance of the year. During the second quarter, the company also experienced an extraordinary pretax gain of $20,000. Provide the value for the items A through F.

The following additional 2014 information is available:

1. The statutory tax rate is as follows: 15% on the first $50,000 of taxable income 20% on the next $50,000 of taxable income 25% on the next $50,000 of taxable income 30% on all additional taxable income

2. At the end of 2013, the first year of operations, the company reported a net operating loss of $80,000 and a tax credit of $5,000. At that time, the company did not recognize any of the tax benefit associated with the operating loss or tax credit. However, the company was hopeful that these benefits could be recognized in the future due to the ability to carry forward both items against future taxable income and taxes.

3. Originally, at the end of the first quarter, the company estimated pretax income for the balance of the year of $60,000.

4. During the second quarter, the company decided to discontinue an operation. Originally, in quarter 1, the operation had reported losses of $30,000 and projected losses for the balance of 2014 in the amount of $40,000. During quarter 2, the discontinued operation reported operating losses of $60,000 and realized losses on the disposal of assets of $25,000. Although not yet realized, the operation anticipated that assets to be sold in the future would net $30,000 less than their book value (carrying value) as reported at the end of quarter 2, 2014.

5. During the second quarter, the company reported pretax income from continuing operations of $50,000 and projected pretax income from continuing operations of $60,000 for the balance of the year. During the second quarter, the company also experienced an extraordinary pretax gain of $20,000. Provide the value for the items A through F.

Explanation Verified

Verified

Item B

Effective tax rate of quarter 1-...

Advanced Accounting 11th Edition by Paul Fischer,William Tayler, Rita Cheng

Why don’t you like this exercise?

Other Minimum 8 character and maximum 255 character

Character 255