Introductory Econometrics: A Modern Approach 6th Edition by Jeffrey M Wooldridge

Edition 6ISBN: 130527010XIntroductory Econometrics: A Modern Approach 6th Edition by Jeffrey M Wooldridge

Edition 6ISBN: 130527010X Exercise 7

Use the data in HSEINV.RAW for this exercise.

(i) Test for a unit root in log(invpc), including a linear time trend and two lags of Alog(invpct). Use a 5% significance level.

(ii) Use the approach from part (i) to test for a unit root in log(price).

(iii) Given the outcomes in parts (i) and (ii), does it make sense to test for cointegration between log(invpc) and log(price)?

Step-by-step solution Verified

Verified

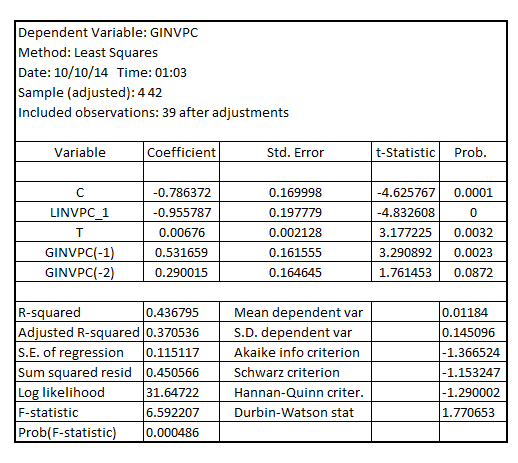

Step 1 of 3

(i)

Estimating the model that relates  to

to

The result is:

The t-statistic of the coefficient of  is -4.832608, less than the critical t-statistic of -3.41 at 5% level of significance when the time trend is present thereby; indicating that unit root in

is -4.832608, less than the critical t-statistic of -3.41 at 5% level of significance when the time trend is present thereby; indicating that unit root in is rejected at 5% level of significance

is rejected at 5% level of significance

Step 2 of 3

Step 3 of 3

Introductory Econometrics: A Modern Approach 6th Edition by Jeffrey M Wooldridge

Why don’t you like this exercise?

Other Minimum 8 character and maximum 255 character

Character 255