Introductory Econometrics: A Modern Approach 6th Edition by Jeffrey M Wooldridge

Edition 6ISBN: 130527010XIntroductory Econometrics: A Modern Approach 6th Edition by Jeffrey M Wooldridge

Edition 6ISBN: 130527010XUse the data in CONSUMP.RAW for this exercise.

(i) In Example, use the method from Section to test the single overidentify-ing restriction in estimating. What do you conclude?

(ii) Campbell and Mankiw (1990) use second lags of all variables as IVs because of potential data measurement problems and informational lags. Reestimate, using only gct-2, gyt-2, and r3t-2 as IVs. How do the estimates compare with those in?

(iii) Regress gyt on the IVs from part (ii) and test whether gyt is sufficiently correlated with them. Why is this important?

Step 1 of 4

(i)

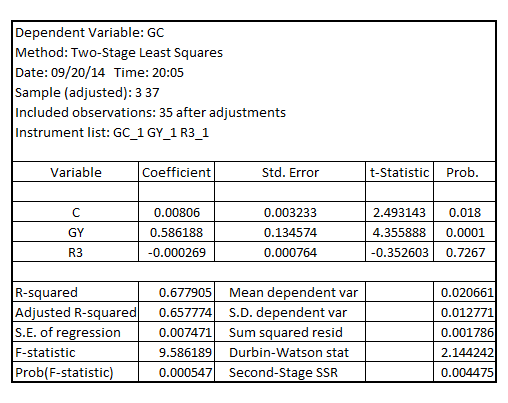

In order to test for over-identifying restrictions in the 2SLS estimation  such that

such that  are the set of instrument variables, follow the following steps:

are the set of instrument variables, follow the following steps:

1) Estimate the residuals from the 2SLS model  such that

such that  are the set of instrument variables

are the set of instrument variables

2) Regress the residuals from Step 1 on

3) Estimate  statistic and call it chi-squared statistic

statistic and call it chi-squared statistic

4) Estimate the (two-tailed) p-value of chi-squared statistic calculated in step 3 and compare it with critical p-value of 0.05 at 5% level of significance

Step1:

Estimate the residuals from the 2SLS model  such that

such that  are the set of instrument variables

are the set of instrument variables

The residuals is given by

Call  as

as

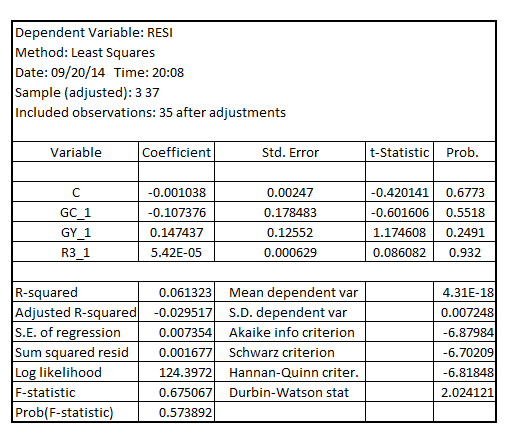

Step2:

Regress the residuals from Step 1 on

Step3:

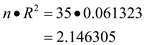

Hence,

The chi-squared value is 2.146305

Step4:

Since, there is one over-identifying restriction, so there is one degree of freedom

The p-value of chi-squared estimate at 2.146305 at one degree of freedom is 0.142914, which is greater than the critical p-value of 0.05 at 5% level of significance, indicating that the single over-identifying restriction has passed the IV test

Step 2 of 4

Step 3 of 4

Step 4 of 4

Why don’t you like this exercise?

Other