Introductory Econometrics: A Modern Approach 6th Edition by Jeffrey M Wooldridge

Edition 6ISBN: 130527010XIntroductory Econometrics: A Modern Approach 6th Edition by Jeffrey M Wooldridge

Edition 6ISBN: 130527010X Exercise 12

Step-by-step solution Verified

Verified

Step 1 of 7

(i)

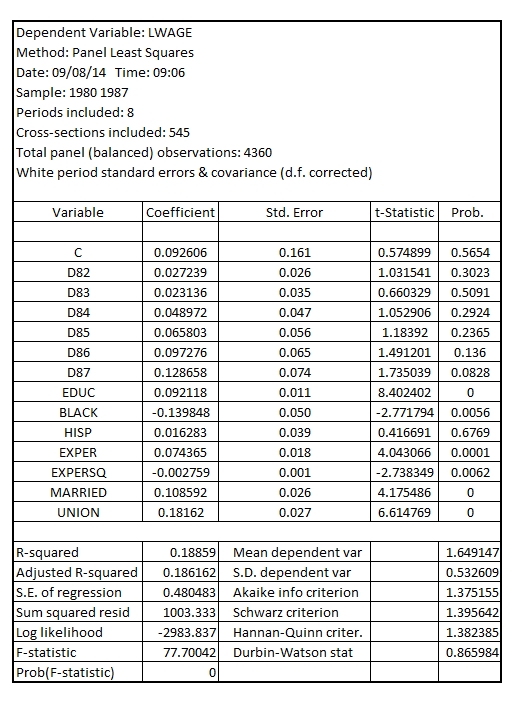

Estimating the model using pooled OLS and assuming standard error robust to serial correlation and heteroscedasticity, the result is:

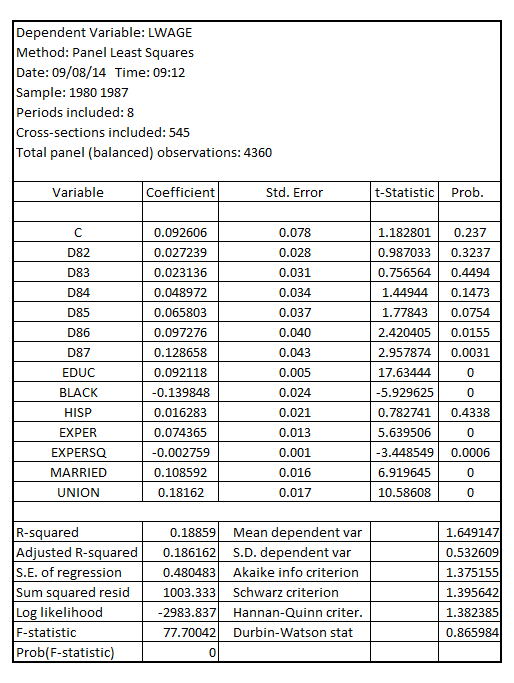

Estimating the model using pooled OLS and assuming standard error non-robust to serial correlation and heteroscedasticity, the result is:

On comparing the robust and non-robust standard error, the result is:

Step 2 of 7

Step 3 of 7

Step 4 of 7

Step 5 of 7

Step 6 of 7

Step 7 of 7

Introductory Econometrics: A Modern Approach 6th Edition by Jeffrey M Wooldridge

Why don’t you like this exercise?

Other Minimum 8 character and maximum 255 character

Character 255