Introductory Econometrics: A Modern Approach 6th Edition by Jeffrey M Wooldridge

Edition 6ISBN: 130527010XIntroductory Econometrics: A Modern Approach 6th Edition by Jeffrey M Wooldridge

Edition 6ISBN: 130527010XUse the data in NYSE.RAW to answer these questions.

(i) Estimate the model in equation and obtain the squared OLS residuals. Find the average, minimum, and maximum values of û2t over the sample.

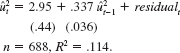

(ii) Use the squared OLS residuals to estimate the following model of heteroske-dasticity:

Report the estimated coefficients, the reported standard errors, the R-squared, and the adjusted R-squared.

(iii) Sketch the conditional variance as a function of the lagged return v For what value of return-1 is the variance the smallest, and what is the variance?

(iv) For predicting the dynamic variance, does the model in part (ii) produce any negative variance estimates?

(v) Does the model in part (ii) seem to fit better or worse than the ARCH(1) model in Example 12.9? Explain.

(vi) To the ARCH(1) regression in equation, add the second lag, û2t- 2. Does this lag seem important? Does the ARCH(2) model fit better than the model in part (ii)?

Why don’t you like this exercise?

Other