Introductory Econometrics: A Modern Approach 6th Edition by Jeffrey M Wooldridge

Edition 6ISBN: 130527010XIntroductory Econometrics: A Modern Approach 6th Edition by Jeffrey M Wooldridge

Edition 6ISBN: 130527010XUse the data in PHILLIPS.RAW to answer these questions.

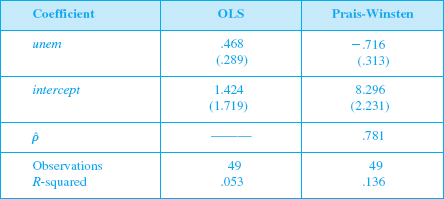

(i) Using the entire data set, estimate the static Phillips curve equation inf1 = ?0 + ?1 unemt + ut by OLS and report the results in the usual form.

(ii) Obtain the OLS residuals from part (i), ût, and obtain p from the regression ût on ût-1. (It is fine to include an intercept in this regression.) Is there strong evidence of serial correlation?

(iii) Now estimate the static Phillips curve model by iterative Prais-Winsten. Compare the estimate of ?1 with that obtained in Table 12.2. Is there much difference in the estimate when the later years are added?

(iv) Rather than using Prais-Winsten, use iterative Cochrane-Orcutt. How similar are the final estimates of p? How similar are the PW and CO estimates of ?1?

Dependent Variable: inf

Why don’t you like this exercise?

Other