Introductory Econometrics: A Modern Approach 6th Edition by Jeffrey M Wooldridge

Edition 6ISBN: 130527010XIntroductory Econometrics: A Modern Approach 6th Edition by Jeffrey M Wooldridge

Edition 6ISBN: 130527010X Exercise 13

(i) For Example 12.4, using the data in BARIUM.RAW, obtain the iterative Cochrane-Orcutt estimates.

(ii) Are the Prais-Winsten and Cochrane-Orcutt estimates similar? Did you expect them to be?

Step-by-step solution Verified

Verified

Step 1 of 3

(i)

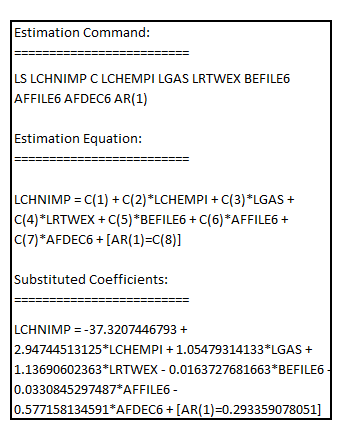

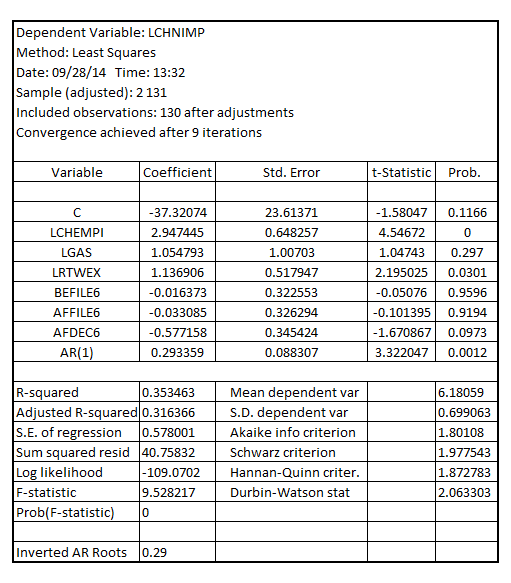

In order to obtain the iterative Cochrane-Orcutt estimates, estimate the regression using Cochrane-Orcutt method

The command to run Cochrane-Orcutt iterative procedures in Eviews is:

The result is:

It shall be noted that the coefficient of AR (1) is 0.293359

It is also the estimated

The iterative Cochrane-Orcutt estimates are the estimates of the coefficients of the different explanatory variables in the model

Step 2 of 3

Step 3 of 3

Introductory Econometrics: A Modern Approach 6th Edition by Jeffrey M Wooldridge

Why don’t you like this exercise?

Other Minimum 8 character and maximum 255 character

Character 255