Introductory Econometrics: A Modern Approach 6th Edition by Jeffrey M Wooldridge

Edition 6ISBN: 130527010XIntroductory Econometrics: A Modern Approach 6th Edition by Jeffrey M Wooldridge

Edition 6ISBN: 130527010XUse the data in PHILLIPS.RAW for this exercise.

(i) Estimate an AR(1) model for the unemployment rate. Use this equation to predict the unemployment rate for 2004. Compare this with the actual unemployment rate for 2004. (You can find this information in a recent Economic Report of the President.)

(ii) Add a lag of inflation to the AR(1) model from part (i). Is inft-1 statistically significant?

(iii) Use the equation from part (ii) to predict the unemployment rate for 2004. Is the result better or worse than in the model from part (i)?

(iv) Use the method from Section 6.4 to construct a 95% prediction interval for the 2004 unemployment rate. Is the 2004 unemployment rate in the interval?

Step 1 of 7

(i)

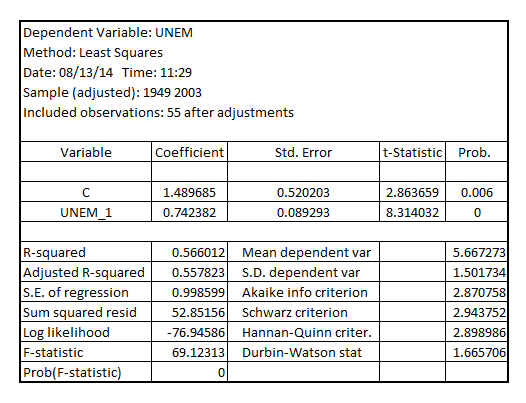

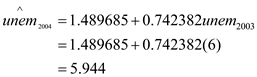

Estimating AR (1) model for the unemployment rate, the model is as follows:

The result is as follows:

The standard form of AR (1) model is,

In 2003, the unemployment rate is 6%. With the given AR (1) model, the predicted unemployment rate in 2004 is

The predicted unemployment rate in 2004 is 5.944%. The actual unemployment rate in 2004 is 5.5%

Step 2 of 7

Step 3 of 7

Step 4 of 7

Step 5 of 7

Step 6 of 7

Step 7 of 7

Why don’t you like this exercise?

Other