Introductory Econometrics: A Modern Approach 6th Edition by Jeffrey M Wooldridge

Edition 6ISBN: 130527010XIntroductory Econometrics: A Modern Approach 6th Edition by Jeffrey M Wooldridge

Edition 6ISBN: 130527010XUse the data in HSEINV.RAW for this exercise.

(i) Find the first order autocorrelation in log(invpc). Now, find the autocorrelation after linearly detrending log(invpc). Do the same for log(price). Which of the two series may have a unit root?

(ii) Based on your findings in part (i), estimate the equation log(invpct) ?0 + ?1?log(pricet) ?2t + ut

and report the results in standard form. Interpret the coefficient

and determine whether it is statistically significant.

(iii) Linearly detrend log(invpct) and use the detrended version as the dependent variable in the regression from part (ii) (see Section 10.5). What happens to R2?

(iv) Now use ?log(invpct) as the dependent variable. How do your results change from part (ii)? Is the time trend still significant? Why or why not?

Step 1 of 9

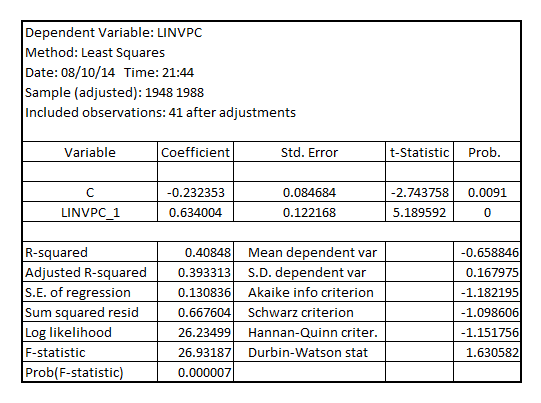

The first order autocorrelation in  is the coefficient of

is the coefficient of  in the AR(1) model as stated as:

in the AR(1) model as stated as:

Consider,  , then AR(1) model is:

, then AR(1) model is:

The result is as follows:

Hence, the first order autocorrelation in  is 0.634.

is 0.634.

Step 2 of 9

Step 3 of 9

Step 4 of 9

Step 5 of 9

Step 6 of 9

Step 7 of 9

Step 8 of 9

Step 9 of 9

Why don’t you like this exercise?

Other