Introductory Econometrics: A Modern Approach 6th Edition by Jeffrey M Wooldridge

Edition 6ISBN: 130527010XIntroductory Econometrics: A Modern Approach 6th Edition by Jeffrey M Wooldridge

Edition 6ISBN: 130527010XUse the data in BARIUM.RAW for this exercise.

(i) Add a linear time trend to equation (10.22). Are any variables, other than the trend, statistically significant?

(ii) In the equation estimated in part (i), test for joint significance of all variables except the time trend. What do you conclude?

(iii) Add monthly dummy variables to this equation and test for seasonality. Does including the monthly dummies change any other estimates or their standard errors in important ways?

Step 1 of 4

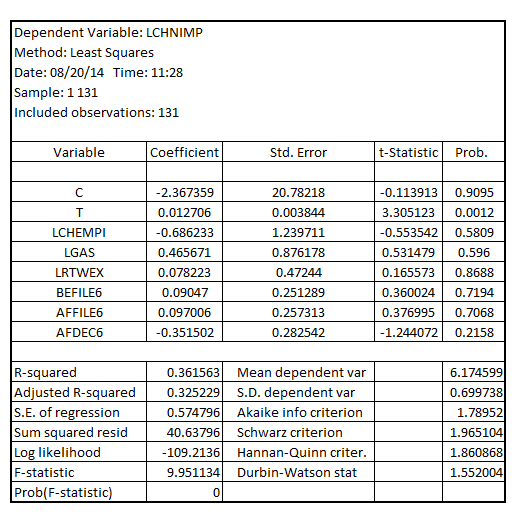

(i)

The regression model after adding a linear time trend is given by:

On executing this regression model, the result is:

It shall be noted that only the linear time trend variable  is statistically significant as the p-value corresponding to it is 0.0012 which is less than the critical p-value of 0.05 at 5% level of significance.

is statistically significant as the p-value corresponding to it is 0.0012 which is less than the critical p-value of 0.05 at 5% level of significance.

Step 2 of 4

Step 3 of 4

Step 4 of 4

Why don’t you like this exercise?

Other