Introductory Econometrics: A Modern Approach 6th Edition by Jeffrey M Wooldridge

Edition 6ISBN: 130527010XIntroductory Econometrics: A Modern Approach 6th Edition by Jeffrey M Wooldridge

Edition 6ISBN: 130527010Xi)Apply RESET from equation to the model estimated in Computer Exercise. Is there evidence of functional form misspecification in the equation?

(ii) Compute a heteroskedasticity-robust form of RESET. Does your conclusion from part (i) change?

y = ?0+ ?1x1+… + ?kxk+?1 2 + ?2

2 + ?2 3+error.

3+error.

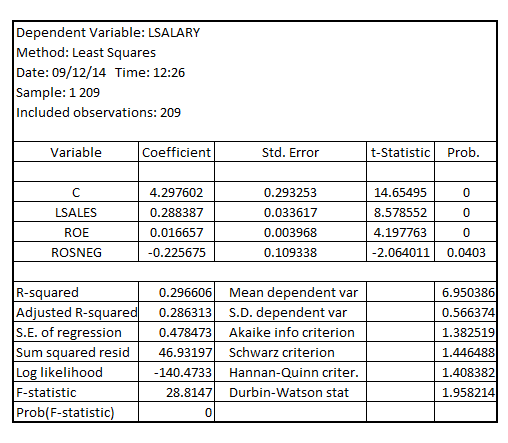

In Problem 4.2, we added the return on the firm’s stock, ros, to a model explaining CEO salary; ros turned out to be insignificant. Now, define a dummy variable, rosneg, which is equal to one if ros _ 0 and equal to zero if ros _ 0. Use CEOSAL1.RAW to estimate the model

Discuss the interpretation and statistical significance of 3.

3.

Step 1 of 4

(i)

The model estimated in Computer Exercise C5 in Chapter 7 is:

In order to apply usual OLS form RESET to test for the evidence of the functional form mis-specification in the equation, it is required to follow four steps:

1) Estimate the model and compute the estimated

2) Take the quadratic and cubic form of

3) Add  and

and as the explanatory variables in the model such that the model becomes:

as the explanatory variables in the model such that the model becomes:

4) Test for the joint significance of  and

and

Step1:

Estimating the model and computing the estimated

The estimate of  is obtained by fitting the equation:

is obtained by fitting the equation:

The  is represented by log (SALARY) _hat

is represented by log (SALARY) _hat

Step2:

In order to estimate the quadratic and cubic values for , obtain

, obtain  and

and by taking the square and cube of

by taking the square and cube of  respectively

respectively

They are represented as lsalary_hatsq and lsalary_hatcu respectively

Step3:

Estimate the model given by:

The result is:

Step 2 of 4

Step 3 of 4

Step 4 of 4

Why don’t you like this exercise?

Other