Introductory Econometrics: A Modern Approach 6th Edition by Jeffrey M Wooldridge

Edition 6ISBN: 130527010XIntroductory Econometrics: A Modern Approach 6th Edition by Jeffrey M Wooldridge

Edition 6ISBN: 130527010XUse the data in FERTIL2.RAW to answer this question.

(i) Estimate the model

and report the usual and heteroskedasticity-robust standard errors. Are the robust standard errors always bigger than the nonrobust ones?

(ii) Add the three religious dummy variables and test whether they are jointly significant. What are the p-values for the nonrobust and robust tests?

(iii) From the regresion in part (ii), obtain the fitted values  and the residuals,

and the residuals,  Regress

Regress  and test the joint significance of the two regressors. Conclude that heteroskedasticity is present in the equation for children.

and test the joint significance of the two regressors. Conclude that heteroskedasticity is present in the equation for children.

(iv) Would you say the heteroskedasticity you found in part (iii) is practically important?

Step 1 of 7

(i)

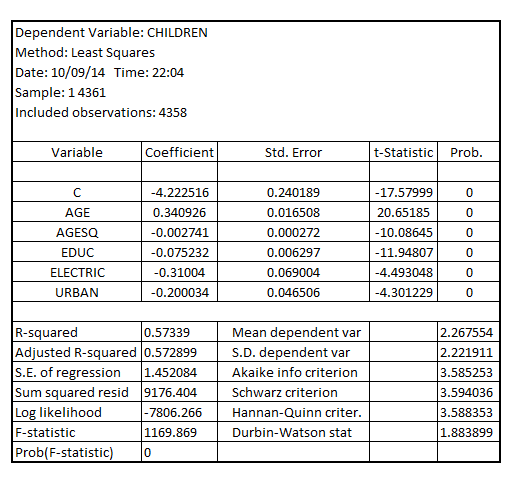

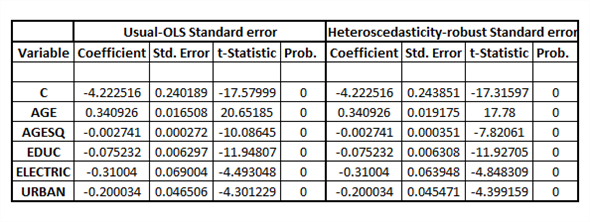

Estimating the model using the usual-OLS standard error, given by:

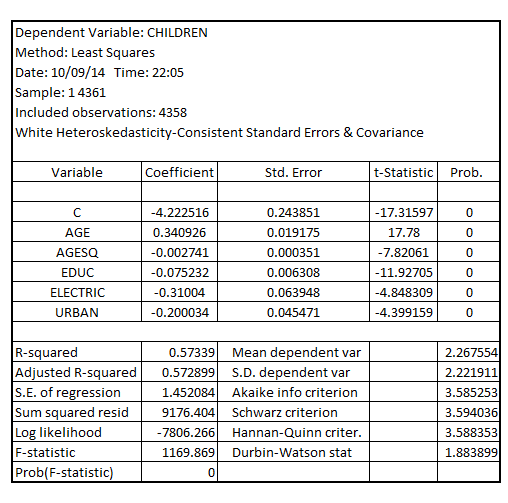

Estimating the model using the heteroscedasticity-robust standard error, given by:

On comparing the usual-OLS standard error with the heteroscedasticity-robust standard error, the result is:

It shall be noted that the heteroscedasticity-robust standard error are not always bigger than the non-robust (usual-OLS) standard error

For the explanatory variables  heteroscedasticity-robust standard error are slightly larger than the usual-OLS standard error, but for

heteroscedasticity-robust standard error are slightly larger than the usual-OLS standard error, but for , heteroscedasticity-robust standard error are smaller than the usual-OLS standard error

, heteroscedasticity-robust standard error are smaller than the usual-OLS standard error

Step 2 of 7

Step 3 of 7

Step 4 of 7

Step 5 of 7

Step 6 of 7

Step 7 of 7

Why don’t you like this exercise?

Other