Introductory Econometrics: A Modern Approach 6th Edition by Jeffrey M Wooldridge

Edition 6ISBN: 130527010XIntroductory Econometrics: A Modern Approach 6th Edition by Jeffrey M Wooldridge

Edition 6ISBN: 130527010XUse the data in LOANAPP.RAW for this exercise.

(i) Estimate the equation in part (iii) of Computer Exercise, computing the heteroskedasticity-robust standard errors. Compare the 95% confidence interval on ?white with the nonrobust confidence interval.

(ii) Obtain the fitted values from the regression in part (i). Are any of them less than zero? Are any of them greater than one? What does this mean about applying weighted least squares?

Use the data in LOANAPP.RAW for this exercise. The binary variable to be explained is approve, which is equal to one if a mortgage loan to an individual was approved. The key explanatory variable is white, a dummy variable equal to one if the applicant was white. The other applicants in the data set are black and Hispanic.

To test for discrimination in the mortgage loan market, a linear probability model can be used:

(i) If there is discrimination against minorities, and the appropriate factors have been controlled for, what is the sign of ?1?

(ii) Regress approve on white and report the results in the usual form. Interpret the coefficient on white. Is it statistically significant? Is it practically large?

(iii) As controls, add the variables hrat, obrat, loanprc, unem, male, married, dep, sch, cosign, chist, pubrec, mortlat1, mortlat2, and vr. What happens to the coefficient on white? Is there still evidence of discrimination against nonwhites?

(iv) Now, allow the effect of race to interact with the variable measuring other obligations as a percentage of income (obrat). Is the interaction term significant?

(v) Using the model from part (iv), what is the effect of being white on the probability of approval when obrat = 32, which is roughly the mean value in the sample? Obtain a 95% confidence interval for this effect.

Step 1 of 2

(i)

Estimate the model where  is regressed on:

is regressed on:

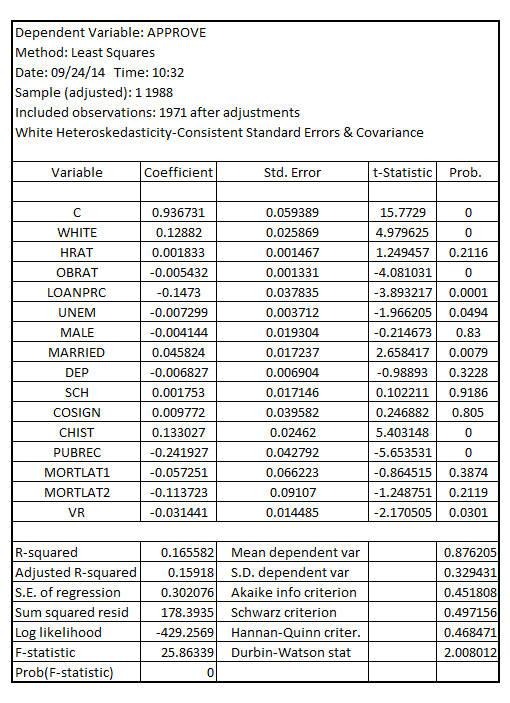

Assuming the heteroskedasticity-robust standard error, the result is as follows:

The confidence interval of the coefficient of  is given by:

is given by:

Lower limit:

Upper limit:

Estimate the model where  is regressed on:

is regressed on:

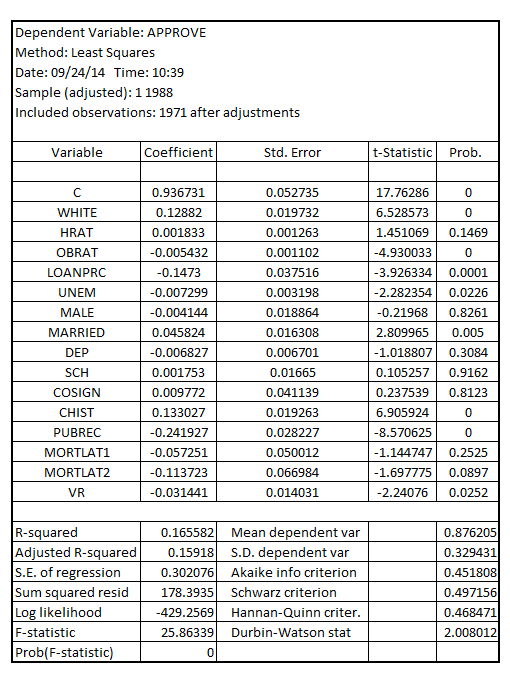

Assuming the usual OLS standard error, the result is as follows:

The confidence interval of the coefficient of  is given by:

is given by:

Lower limit:

Upper limit:

Thus, the confidence limit of  when assuming heteroskedasticity-robust standard error is 0.07811 to 0.1795 whereas, when assuming the usual OLS standard error, the confidence limit is 0.09014 to 0.16749.

when assuming heteroskedasticity-robust standard error is 0.07811 to 0.1795 whereas, when assuming the usual OLS standard error, the confidence limit is 0.09014 to 0.16749.

Step 2 of 2

Why don’t you like this exercise?

Other