Fundamentals of Cost Accounting 3rd Edition by William N. Lanen, Shannon W. Anderson, Michael Maher

Edition 3ISBN: 0073527114Fundamentals of Cost Accounting 3rd Edition by William N. Lanen, Shannon W. Anderson, Michael Maher

Edition 3ISBN: 0073527114Racketeer, Inc (Comprehensive Overview of Budgets and Variance)

“I just don’t understand these financial statements at all!” exclaimed Mr Elmo Knapp Mr Knapp explained that he had turned over management of Racketeer, Inc, a division of American Recreation Equipment, Inc, to his son, Otto, the previous month Racketeer, Inc, manufactures tennis rackets.

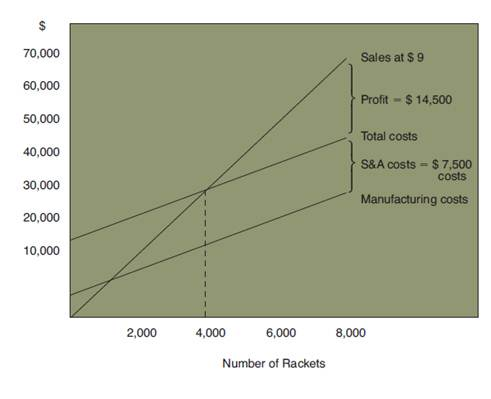

? “I was really proud of Otto,” he beamed “He was showing us all the tricks he learned in business school, and if I do say so myself, I think he was doing a rather good job for us For example, he put together this budget for Racketeer, which makes it very easy to see how much profit we’ll make at any sales volume (Exhibit 178) As best as I can figure it, in March we expected to have a volume of 8,000 units and a profit of $14,500 on our rackets But we did much better than that! We sold 10,000 rackets, so we should have made almost $21,000 on them.”

| Per Racket | |

Raw material |

| |

Frame (one frame per racket) | $315 | |

Stringing materials: 20 feet at 3¢ per foot | 060 | |

Direct labor |

| |

Skilled: 1/8 hour at $960 per hour | 120 | |

Unskilled: 1/8 hour at $560 per hour | 070 | |

Plant overhead |

| |

Indirect labor | 010 | |

Power | 003 | |

Supervision | 012b | |

Depreciation | 020b | |

Other | 015b | |

Total standard cost per frame | $625 | |

a Standard costs are calculated for an estimated production volume of 8,000 units each month.

b Fixed costs .

?“Another one of Otto’s innovations is this standard cost system,” said Mr Knapp proudly “He sat down with our production people and came up with a standard production cost per unit (see Exhibit 179) He tells me this will let us know how well our production people are performing Also, he claims it will cut down on our clerical work.”

?Mr. Knapp continued, “But one thing puzzles me My calculations show that we should have earned profit of nearly $21,000 in March However, our accountants came up with less than $19,000 in the monthly income statement (Exhibit 1710) This bothers me a great deal Now, I’m sure our accountants are doing their job properly But still, it appears to me that they’re about $2,200 short.

?“As you can probably guess,” Mr Knapp concluded, “we are one big happy family around here I just wish I knew what those accountants were up to coming in with a low net income like that.”

Required

Prepare a report for Mr Elmo Knapp and Mr Otto Knapp that reconciles the profit graph with the actual results for March (see Exhibit 1711) Show the source of each variance from the original plan (8,000 rackets) in as much detail as you can and evaluate Racketeer’s performance in March Recommend improvements in Racketeer’s profit planning and control methods.

RACKETEER, INC Income Statement, For the Month of March—Actual | |

Sales |

|

10,000 rackets at $9 | $90,000 |

Standard cost of goods sold |

|

10,000 rackets at $625 | 62,500 |

Gross profit after standard costs | $27,500 |

Variances |

|

Materials variance | (490) |

Labor variance | (392) |

Overhead variance | (660) |

Gross profit | $25,958 |

Selling and administrative expenses | 7,200 |

Operating profit | $18,758 |

Direct materials purchased and used Stringing materials |

|

|

| 175,000 | feet at 250 per foot |

Frames (some frames were ruined during production) | 7,100 | at $315 per frame |

Labor |

|

|

Skilled ($980 per hour) | 900 | hours |

Unskilled ($580 per hour) | 840 | hours |

Overhead |

|

|

Indirect labor | $ 800 |

|

Power | $ 250 |

|

Depreciation | $1,600 |

|

Supervision | $ 960 |

|

Other | $1,250 |

|

Production | 7,000 | rackets |

The following solution is based on a rep ...

Why don’t you like this exercise?

Other