Fundamentals of Cost Accounting 3rd Edition by William N. Lanen, Shannon W. Anderson, Michael Maher

Edition 3ISBN: 0073527114Fundamentals of Cost Accounting 3rd Edition by William N. Lanen, Shannon W. Anderson, Michael Maher

Edition 3ISBN: 0073527114Cost Estimation, CVP Analysis, and Decision Making

Luke Corporation produces a variety of products, each within their own division. Last year, the managers at Luke developed and began marketing a new chewing gum, Bubbs, to sell in vending machines. The product, which sells for $5.25 per case, has not had the market success that managers expected and the company is considering dropping Bubbs.

The product-line income statement for the past twelve months follows:

Revenue |

| $14,682,150 |

Costs | ||

Manufacturing costs | $14,440,395 |

|

Allocated corporate costs (@5%) | 734,108 | 15,174,503 |

Product-line margin |

| $ (492,353) |

Allowance for tax (@20%) |

| 98,470 |

Product-line profit |

| $(393,883) |

All products at Luke receive an allocation of corporate overhead costs, which is computed as 5 percent of product revenue. The 5 percent rate is computed based on the most recent year’s corporate cost as a percentage of revenue. Data on corporate costs and revenues for the past two years follow:

| Corporate Revenue | Corporate Overhead Costs |

Most recent year | $106,750,000 | $5,337,500 |

Previous year | $ 76,200,000 | 4,221,000 |

Roy O. Andre, the product manager for Bubbs, is concerned about whether the product will be dropped by the company and has employed you as a financial consultant to help with some analysis. In addition to the information given above, Mr. Andre provides you with the following data on product costs for Bubbs:

Month | Cases | Production Costs |

1 | 207,000 | $1,139,828 |

2 | 217,200 | 1,161,328 |

3 | 214,800 | 1,169,981 |

4 | 228,000 | 1,185,523 |

5 | 224,400 | 1,187,827 |

6 | 237,000 | 1,208,673 |

7 | 220,200 | 1,183,699 |

8 | 247,200 | 1,226,774 |

9 | 238,800 | 1,225,226 |

10 | 252,600 | 1,237,325 |

11 | 250,200 | 1,241,760 |

12 | 259,200 | 1,272,451 |

Required

a. Bunk Stores has requested a quote for a special order of Bubbs. This order would not be subject to any corporate allocation (and would not affect corporate costs). What is the minimum price Mr. Andre can offer Bunk without reducing profit any further?

b. How many cases of Bubbs does Luke have to sell in order to break even on the product?

c. Suppose Luke has a requirement that all products have to earn 5 percent of sales (after tax and corporate allocations) or they will be dropped. How many cases of Bubbs does Mr. Andre need to sell to avoid seeing Bubbs dropped?

d. Assume all costs and prices will be the same in the next year. If Luke drops Bubbs, how much will Luke’s profits increase or decrease? Assume that fixed production costs can be avoided if Bubbs is dropped.

Step 1 of 4

?This problem is more subtle than it might appear, because the student must consider the effect on Luke Corporation and the Product Manager, Mr. Andre separately. In other words, it anticipates in a small way the issues in management control systems.

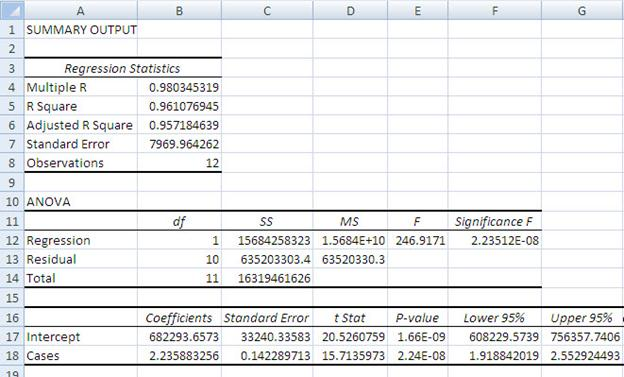

a.?$2.24 per case.

?This is a special order question similar to those discussed in Chapter 4. The relevant cost is the variable production cost. (The problem states that no corporate overhead will be allocated or affected by the order.) To determine the variable production cost, a regression analysis on the production data can be run. The results follow:

?

As shown, the estimated variable production cost is $2.24. This is the minumum that can be charged without reducing profit.

Step 2 of 4

Step 3 of 4

Step 4 of 4

Why don’t you like this exercise?

Other