Personal Finance 1st Edition by Jack R. Kapoor

Edition 1ISBN: 1308231393Personal Finance 1st Edition by Jack R. Kapoor

Edition 1ISBN: 1308231393Adjusting the Budget

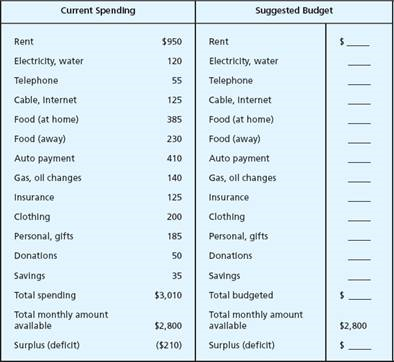

In a recent month, the Constantine family had a budget deficit, which is something they want to avoid so they do not have future financial difficulties. Jason and Karen Constantine, and their children (ages 10 and 12), plan to discuss the situation after dinner this evening.

While at work, Jason was talking with his friend Ken Lopez. Ken had been a regular saver since he was very young, starting with a small savings account. Those funds were then invested in various stocks and mutual funds. While in college, Ken was able to pay for his education while continuing to save between $50 and $100 a month. He closely monitored his spending. Ken realized that the few dollars here and there for snacks and other minor purchases quickly add up.

Today, Ken works as a customer service manager for the online division of a retailing company. He lives with his wife and their two young children. The family’s spending plan allows for all their needs and also includes regularly saving and investing for the children’s education and for retirement.

Jason asked Ken, “How come you never seem to have financial stress in your household?”

Ken replied, “Do you know where your money is going each month?”

“Not really,” was Jason’s response.

“You’d be surprised by how much is spent on little things you might do without,” Ken responded.

“I guess so. I just don’t want to have to go around with a notebook writing down every amount I spend,” Jason said in a troubled voice.

“Well, you have to take some action if you want your financial situation to change,” Ken countered.

That evening, the Constantine family met to discuss their budget situation:

What amounts would you suggest for the various categories for the family budget?

Step 1 of 3

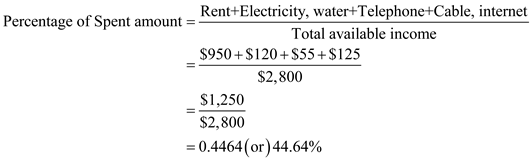

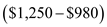

For a family of four with two children below the age of 18 years, Housing expenses should not be more than 35% of the total available income.

Calculate the percentage of amount spent:

Thus, percentage of spent amount is 44.64%. This is greater than the stated percentage. As per stated percentage (35%), the family should spend the amount of $980 on the highest side of the range. Hence, the difference amount is $270 .

.

Therefore, the family should look to slash these expenses by $270 to reach the optimal stage. This would also turn the deficit into surplus of $60 .

.

Step 2 of 3

Step 3 of 3

Why don’t you like this exercise?

Other