Accounting: What the Numbers Mean 9th Edition by Wayne W McManus, Daniel F Viele, David H Marshall

Edition 9ISBN: 0073527068Accounting: What the Numbers Mean 9th Edition by Wayne W McManus, Daniel F Viele, David H Marshall

Edition 9ISBN: 0073527068Analytical case (part 2)—prepare owners’ equity amounts and disclosures for 2011 using transaction information (Note: You should review the solution to Case 8.29, provided by your instructor, before attempting to complete this case.) The transactions affecting the owners’ equity accounts of DeZurik Corp. for the year ended June 30, 2011, are summarized here:

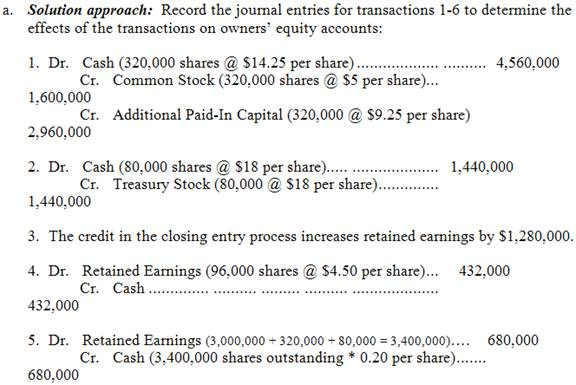

1. 320,000 shares of common stock were issued at $14.25 per share.

2. 80,000 shares of treasury (common) stock were sold for $18 per share.

3. Net income for the year was $1,280 (in thousands).

4. The fiscal 2011 preferred dividends were paid in full. Assume that all 96,000 shares were outstanding throughout the year ended June 30, 2011.

5. A cash dividend of $.20 per share was declared and paid to common stockholders. Assume that transactions (1) and (2) occurred before the dividend was declared.

6. The preferred stock was split 2 for 1 on June 30, 2011. (Note: This transaction had no effect on transaction 4.)

Required:

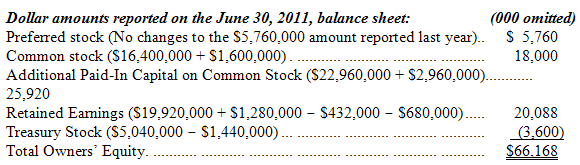

a. Calculate the dollar amounts that DeZurik Corp. would report for each owners’ equity caption on its June 30, 2011, balance sheet after recording the effects of transactions 1-6. Note that total owners’ equity at June 30, 2011, is provided as a check figure. (Hint: To determine the Retained Earnings balance, begin with the June 30, 2010, balance of $19,920 (in thousands) as determined in Case 8.29, and then make adjustments for the effects of transactions 3-5.)

b. Indicate how the owners’ equity caption details for DeZurik Corp. would change for the June 30, 2011, balance sheet, as compared to the disclosures shown in Case 8.29 for the 2010 balance sheet.

c. What was the average issue price of common stock shown on the June 30, 2011, balance sheet?

Step 1 of 3

6. No entry is required for a 2 for 1 stock split. The number of shares issued and outstanding are each doubled (i.e., multiplied by two); the par value per share and the annual dividend per share are each halved (i.e., divided by two). The market price per share is likely to settle at approximately half of its pre-split value.

Note that the number of shares authorized will normally be increased to accommodate a stock split, but this requires shareholder approval. In this case, the 200,000 shares authorized would be sufficient to accommodate the post-split number of shares issued of 96,000. However, there would not be much cushion for future share issuances. Thus, a stock split in these circumstances would not normally be affected until it is approved at the next annual shareholders’ meeting (along with the approval to increase the number of authorized shares, perhaps to 400,000).

Step 2 of 3

Step 3 of 3

Why don’t you like this exercise?

Other