Deck 5: IFRS for Small-And Medium-Sized Entities

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

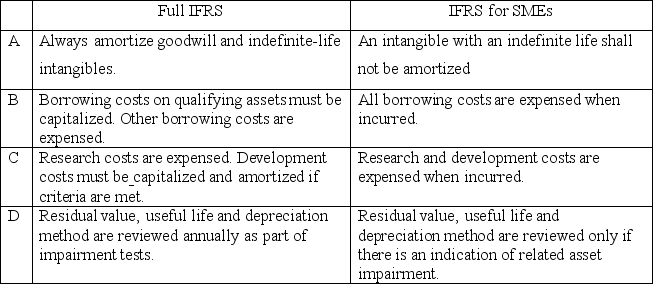

Which comparison between full IFRS and IFRS for SMEs is incorrect?

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/7

Play

Full screen (f)

Deck 5: IFRS for Small-And Medium-Sized Entities

1

Which following organizations)is are)the founders)of the "blue-ribbon" panel?

A)AICPA

B)FAF

C)FASB

D)NASBA

E)All of the above

A)AICPA

B)FAF

C)FASB

D)NASBA

E)All of the above

E

2

Which is one of the options from full IFRS eliminated for SMEs?

A)For inventory,measurement is driven by circumstances rather than allowing an accounting policy choice between the FIFO and Lower of Cost or Market models

B)Various options for non-profit organization grants eliminated in favor of a single simplified model.

C)Biological assets measured at fair value with changes taken to profit and loss only when fair value is readily determinable without undue cost or effort.Otherwise,use cost-depreciation-impairment model.

D)Share-based payments require use future value of the compensation option

A)For inventory,measurement is driven by circumstances rather than allowing an accounting policy choice between the FIFO and Lower of Cost or Market models

B)Various options for non-profit organization grants eliminated in favor of a single simplified model.

C)Biological assets measured at fair value with changes taken to profit and loss only when fair value is readily determinable without undue cost or effort.Otherwise,use cost-depreciation-impairment model.

D)Share-based payments require use future value of the compensation option

C

3

Which of the following entities may not gain distinct advantages from adopting IFRS for SMEs?

A)Entities owned by a foreign parent currently using IFRS

B)Entities that have cooperation with foreign companies using IFRS

C)Entities with foreign investors familiar with IFRS

D)Growing entities preparing to enter public markets where a full IFRS would otherwise be required

A)Entities owned by a foreign parent currently using IFRS

B)Entities that have cooperation with foreign companies using IFRS

C)Entities with foreign investors familiar with IFRS

D)Growing entities preparing to enter public markets where a full IFRS would otherwise be required

B

4

Which is one criterion of SMEs?

A)Have no publicly-traded assets or equity

B)Publish general-purpose financial statements

C)Not hold assets as fiduciary for a broad group of outsiders

D)Pass the certain size test created by the IASB to qualify

A)Have no publicly-traded assets or equity

B)Publish general-purpose financial statements

C)Not hold assets as fiduciary for a broad group of outsiders

D)Pass the certain size test created by the IASB to qualify

Unlock Deck

Unlock for access to all 7 flashcards in this deck.

Unlock Deck

k this deck

5

The Blue Ribbon Panel was in charge of recommending an approach to standard setting for private companies in the U.S.to the FAF,what did the Blue Ribbon Panel determine?

A)A separate standard setting board for private company financial reporting should be established under the FAF's oversight.

B)Initially the new Board should focus on making exceptions and modifications to U.S.GAAP for private companies rather than moving toward a separate,self-contained GAAP for private companies.

C)The new Board should also work to develop a framework for determining which standards should be exempted or modified for private companies.

D)All of the above

A)A separate standard setting board for private company financial reporting should be established under the FAF's oversight.

B)Initially the new Board should focus on making exceptions and modifications to U.S.GAAP for private companies rather than moving toward a separate,self-contained GAAP for private companies.

C)The new Board should also work to develop a framework for determining which standards should be exempted or modified for private companies.

D)All of the above

Unlock Deck

Unlock for access to all 7 flashcards in this deck.

Unlock Deck

k this deck

6

Which of the following is included in full IFRS but eliminated for SMEs' IFRS?

A)Pro forma financial reporting

B)Segment reporting

C)Special accounting for securities held for sale

D)Revaluation of intangibles

A)Pro forma financial reporting

B)Segment reporting

C)Special accounting for securities held for sale

D)Revaluation of intangibles

Unlock Deck

Unlock for access to all 7 flashcards in this deck.

Unlock Deck

k this deck

7

Which comparison between full IFRS and IFRS for SMEs is incorrect?

Unlock Deck

Unlock for access to all 7 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 7 flashcards in this deck.