Deck 5: Consolidated Financial Statementsintra-Entity Asset Transactions

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

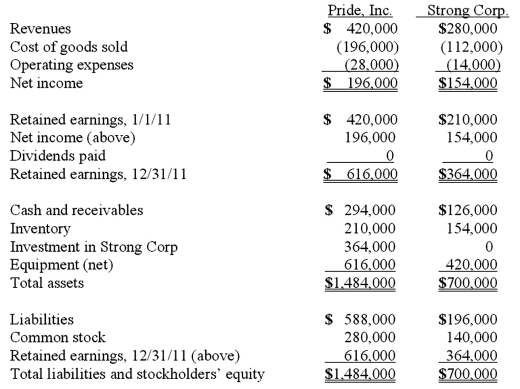

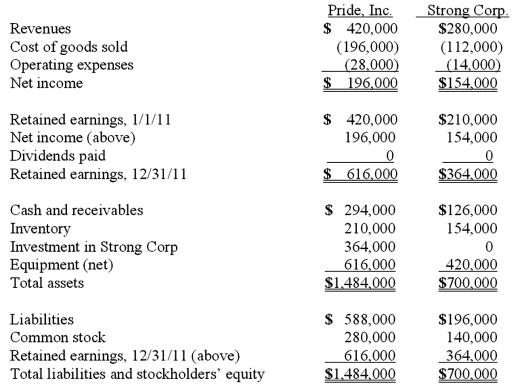

On January 1, 2011, Pride, Inc. acquired 80% of the outstanding voting common stock of Strong Corp. for $364,000. There is no active market for Strong's stock. Of this payment, $28,000 was allocated to equipment (with a five-year life) that had been undervalued on Strong's books by $35,000. Any remaining excess was attributable to goodwill which has not been impaired.

As of December 31, 2011, before preparing the consolidated worksheet, the financial statements appeared as follows:

During 2011, Pride bought inventory for $112,000 and sold it to Strong for $140,000. Only half of this purchase had been paid for by Strong by the end of the year. 60% of these goods were still in the company's possession on December 31.

What is the consolidated total for inventory at December 31, 2011?

A) $336,000.

B) $280,000.

C) $364,000.

D) $347,200.

E) $349,300.

As of December 31, 2011, before preparing the consolidated worksheet, the financial statements appeared as follows:

During 2011, Pride bought inventory for $112,000 and sold it to Strong for $140,000. Only half of this purchase had been paid for by Strong by the end of the year. 60% of these goods were still in the company's possession on December 31.

What is the consolidated total for inventory at December 31, 2011?

A) $336,000.

B) $280,000.

C) $364,000.

D) $347,200.

E) $349,300.

Question

Question

Question

Question

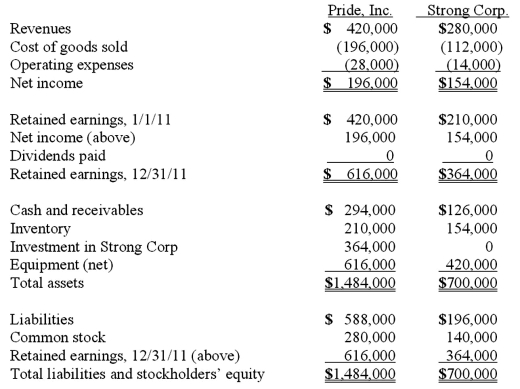

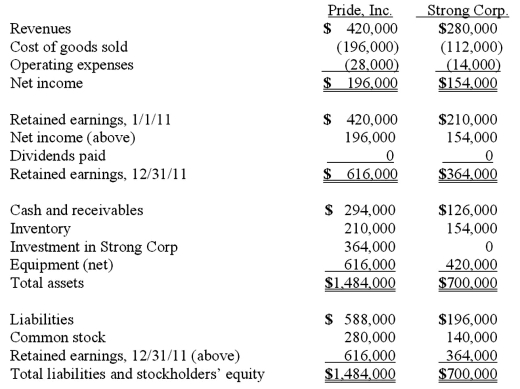

On January 1, 2011, Pride, Inc. acquired 80% of the outstanding voting common stock of Strong Corp. for $364,000. There is no active market for Strong's stock. Of this payment, $28,000 was allocated to equipment (with a five-year life) that had been undervalued on Strong's books by $35,000. Any remaining excess was attributable to goodwill which has not been impaired.

As of December 31, 2011, before preparing the consolidated worksheet, the financial statements appeared as follows:

During 2011, Pride bought inventory for $112,000 and sold it to Strong for $140,000. Only half of this purchase had been paid for by Strong by the end of the year. 60% of these goods were still in the company's possession on December 31.

What is the total of consolidated operating expenses?

A) $42,000.

B) $47,600.

C) $53,200.

D) $49,000.

E) $35,000.

As of December 31, 2011, before preparing the consolidated worksheet, the financial statements appeared as follows:

During 2011, Pride bought inventory for $112,000 and sold it to Strong for $140,000. Only half of this purchase had been paid for by Strong by the end of the year. 60% of these goods were still in the company's possession on December 31.

What is the total of consolidated operating expenses?

A) $42,000.

B) $47,600.

C) $53,200.

D) $49,000.

E) $35,000.

Question

Question

Question

Question

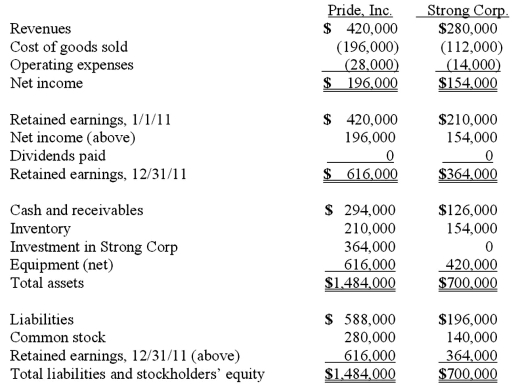

On January 1, 2011, Pride, Inc. acquired 80% of the outstanding voting common stock of Strong Corp. for $364,000. There is no active market for Strong's stock. Of this payment, $28,000 was allocated to equipment (with a five-year life) that had been undervalued on Strong's books by $35,000. Any remaining excess was attributable to goodwill which has not been impaired.

As of December 31, 2011, before preparing the consolidated worksheet, the financial statements appeared as follows:

During 2011, Pride bought inventory for $112,000 and sold it to Strong for $140,000. Only half of this purchase had been paid for by Strong by the end of the year. 60% of these goods were still in the company's possession on December 31.

What is the consolidated total for equipment (net) at December 31, 2011?

A) $952,000.

B) $1,058,400.

C) $1,069,600.

D) $1,064,000.

E) $1,066,800.

As of December 31, 2011, before preparing the consolidated worksheet, the financial statements appeared as follows:

During 2011, Pride bought inventory for $112,000 and sold it to Strong for $140,000. Only half of this purchase had been paid for by Strong by the end of the year. 60% of these goods were still in the company's possession on December 31.

What is the consolidated total for equipment (net) at December 31, 2011?

A) $952,000.

B) $1,058,400.

C) $1,069,600.

D) $1,064,000.

E) $1,066,800.

Question

Question

Question

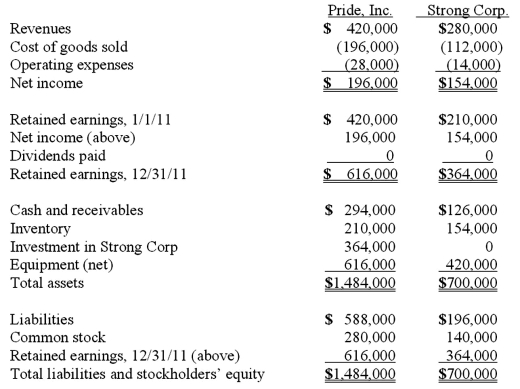

On January 1, 2011, Pride, Inc. acquired 80% of the outstanding voting common stock of Strong Corp. for $364,000. There is no active market for Strong's stock. Of this payment, $28,000 was allocated to equipment (with a five-year life) that had been undervalued on Strong's books by $35,000. Any remaining excess was attributable to goodwill which has not been impaired.

As of December 31, 2011, before preparing the consolidated worksheet, the financial statements appeared as follows:

During 2011, Pride bought inventory for $112,000 and sold it to Strong for $140,000. Only half of this purchase had been paid for by Strong by the end of the year. 60% of these goods were still in the company's possession on December 31.

What is the total of consolidated revenues?

A) $700,000.

B) $644,000.

C) $588,000.

D) $560,000.

E) $840,000.

As of December 31, 2011, before preparing the consolidated worksheet, the financial statements appeared as follows:

During 2011, Pride bought inventory for $112,000 and sold it to Strong for $140,000. Only half of this purchase had been paid for by Strong by the end of the year. 60% of these goods were still in the company's possession on December 31.

What is the total of consolidated revenues?

A) $700,000.

B) $644,000.

C) $588,000.

D) $560,000.

E) $840,000.

Question

On January 1, 2011, Pride, Inc. acquired 80% of the outstanding voting common stock of Strong Corp. for $364,000. There is no active market for Strong's stock. Of this payment, $28,000 was allocated to equipment (with a five-year life) that had been undervalued on Strong's books by $35,000. Any remaining excess was attributable to goodwill which has not been impaired.

As of December 31, 2011, before preparing the consolidated worksheet, the financial statements appeared as follows:

During 2011, Pride bought inventory for $112,000 and sold it to Strong for $140,000. Only half of this purchase had been paid for by Strong by the end of the year. 60% of these goods were still in the company's possession on December 31.

What is the total of consolidated cost of goods sold?

A) $196,000.

B) $212,800.

C) $184,800.

D) $203,000.

E) $168,000.

As of December 31, 2011, before preparing the consolidated worksheet, the financial statements appeared as follows:

During 2011, Pride bought inventory for $112,000 and sold it to Strong for $140,000. Only half of this purchase had been paid for by Strong by the end of the year. 60% of these goods were still in the company's possession on December 31.

What is the total of consolidated cost of goods sold?

A) $196,000.

B) $212,800.

C) $184,800.

D) $203,000.

E) $168,000.

Question

Question

Question

On January 1, 2011, Pride, Inc. acquired 80% of the outstanding voting common stock of Strong Corp. for $364,000. There is no active market for Strong's stock. Of this payment, $28,000 was allocated to equipment (with a five-year life) that had been undervalued on Strong's books by $35,000. Any remaining excess was attributable to goodwill which has not been impaired.

As of December 31, 2011, before preparing the consolidated worksheet, the financial statements appeared as follows:

During 2011, Pride bought inventory for $112,000 and sold it to Strong for $140,000. Only half of this purchase had been paid for by Strong by the end of the year. 60% of these goods were still in the company's possession on December 31.

What is the consolidated total of non-controlling interest appearing in the balance sheet?

A) $100,800.

B) $97,440.

C) $93,800.

D) $120,400.

E) $117,040.

As of December 31, 2011, before preparing the consolidated worksheet, the financial statements appeared as follows:

During 2011, Pride bought inventory for $112,000 and sold it to Strong for $140,000. Only half of this purchase had been paid for by Strong by the end of the year. 60% of these goods were still in the company's possession on December 31.

What is the consolidated total of non-controlling interest appearing in the balance sheet?

A) $100,800.

B) $97,440.

C) $93,800.

D) $120,400.

E) $117,040.

Question

Gargiulo Company, a 90% owned subsidiary of Posito Corporation, sells inventory to Posito at a 25% profit on selling price. The following data are available pertaining to intra-entity purchases. Gargiulo was acquired on January 1, 2010.

Assume the equity method is used. The following data are available pertaining to Gargiulo's income and dividends.

For consolidation purposes, what amount would be debited to cost of goods sold for the 2011 consolidation worksheet with regard to the unrealized gross profit of the 2011 intra-entity transfer of merchandise?

A) $1,000.

B) $800.

C) $3,000.

D) $2,400.

E) $900.

Assume the equity method is used. The following data are available pertaining to Gargiulo's income and dividends.

For consolidation purposes, what amount would be debited to cost of goods sold for the 2011 consolidation worksheet with regard to the unrealized gross profit of the 2011 intra-entity transfer of merchandise?

A) $1,000.

B) $800.

C) $3,000.

D) $2,400.

E) $900.

Question

Question

Gargiulo Company, a 90% owned subsidiary of Posito Corporation, sells inventory to Posito at a 25% profit on selling price. The following data are available pertaining to intra-entity purchases. Gargiulo was acquired on January 1, 2010.

Assume the equity method is used. The following data are available pertaining to Gargiulo's income and dividends.

Compute the equity in earnings of Gargiulo reported on Posito's books for 2012.

A) $84,600.

B) $84,375.

C) $83,925.

D) $84,825.

E) $84,850.

Assume the equity method is used. The following data are available pertaining to Gargiulo's income and dividends.

Compute the equity in earnings of Gargiulo reported on Posito's books for 2012.

A) $84,600.

B) $84,375.

C) $83,925.

D) $84,825.

E) $84,850.

Question

Question

Gargiulo Company, a 90% owned subsidiary of Posito Corporation, sells inventory to Posito at a 25% profit on selling price. The following data are available pertaining to intra-entity purchases. Gargiulo was acquired on January 1, 2010.

Assume the equity method is used. The following data are available pertaining to Gargiulo's income and dividends.

For consolidation purposes, what amount would be debited to January 1 retained earnings for the 2010 consolidation worksheet entry with regard to the unrealized gross profit of the 2010 intra-entity transfer of merchandise?

A) $0.

B) $1,600.

C) $300.

D) $240.

E) $270.

Assume the equity method is used. The following data are available pertaining to Gargiulo's income and dividends.

For consolidation purposes, what amount would be debited to January 1 retained earnings for the 2010 consolidation worksheet entry with regard to the unrealized gross profit of the 2010 intra-entity transfer of merchandise?

A) $0.

B) $1,600.

C) $300.

D) $240.

E) $270.

Question

Gargiulo Company, a 90% owned subsidiary of Posito Corporation, sells inventory to Posito at a 25% profit on selling price. The following data are available pertaining to intra-entity purchases. Gargiulo was acquired on January 1, 2010.

Assume the equity method is used. The following data are available pertaining to Gargiulo's income and dividends.

Compute the equity in earnings of Gargiulo reported on Posito's books for 2010.

A) $63,000.

B) $62,730.

C) $63,270.

D) $70,000.

E) $62,700.

Assume the equity method is used. The following data are available pertaining to Gargiulo's income and dividends.

Compute the equity in earnings of Gargiulo reported on Posito's books for 2010.

A) $63,000.

B) $62,730.

C) $63,270.

D) $70,000.

E) $62,700.

Question

Gargiulo Company, a 90% owned subsidiary of Posito Corporation, sells inventory to Posito at a 25% profit on selling price. The following data are available pertaining to intra-entity purchases. Gargiulo was acquired on January 1, 2010.

Assume the equity method is used. The following data are available pertaining to Gargiulo's income and dividends.

For consolidation purposes, what amount would be debited to January 1 retained earnings for the 2011 consolidation worksheet entry with regard to the unrealized gross profit of the 2010 intra-entity transfer of merchandise?

A) $240.

B) $300.

C) $2,000.

D) $1,600.

E) $270.

Assume the equity method is used. The following data are available pertaining to Gargiulo's income and dividends.

For consolidation purposes, what amount would be debited to January 1 retained earnings for the 2011 consolidation worksheet entry with regard to the unrealized gross profit of the 2010 intra-entity transfer of merchandise?

A) $240.

B) $300.

C) $2,000.

D) $1,600.

E) $270.

Question

Gargiulo Company, a 90% owned subsidiary of Posito Corporation, sells inventory to Posito at a 25% profit on selling price. The following data are available pertaining to intra-entity purchases. Gargiulo was acquired on January 1, 2010.

Assume the equity method is used. The following data are available pertaining to Gargiulo's income and dividends.

Compute the non-controlling interest in Gargiulo's net income for 2010.

A) $6,970.

B) $7,000.

C) $7,030.

D) $6,270.

E) $6,230.

Assume the equity method is used. The following data are available pertaining to Gargiulo's income and dividends.

Compute the non-controlling interest in Gargiulo's net income for 2010.

A) $6,970.

B) $7,000.

C) $7,030.

D) $6,270.

E) $6,230.

Question

Question

Question

Gargiulo Company, a 90% owned subsidiary of Posito Corporation, sells inventory to Posito at a 25% profit on selling price. The following data are available pertaining to intra-entity purchases. Gargiulo was acquired on January 1, 2010.

Assume the equity method is used. The following data are available pertaining to Gargiulo's income and dividends.

Compute the non-controlling interest in Gargiulo's net income for 2012.

A) $9,400.

B) $9,375.

C) $9,425.

D) $9,325.

E) $8,485.

Assume the equity method is used. The following data are available pertaining to Gargiulo's income and dividends.

Compute the non-controlling interest in Gargiulo's net income for 2012.

A) $9,400.

B) $9,375.

C) $9,425.

D) $9,325.

E) $8,485.

Question

Question

Gargiulo Company, a 90% owned subsidiary of Posito Corporation, sells inventory to Posito at a 25% profit on selling price. The following data are available pertaining to intra-entity purchases. Gargiulo was acquired on January 1, 2010.

Assume the equity method is used. The following data are available pertaining to Gargiulo's income and dividends.

For consolidation purposes, what amount would be debited to cost of goods sold for the 2012 consolidation worksheet with regard to the unrealized gross profit of the 2012 intra-entity transfer of merchandise?

A) $600.

B) $750.

C) $3,760.

D) $3,000.

E) $675.

Assume the equity method is used. The following data are available pertaining to Gargiulo's income and dividends.

For consolidation purposes, what amount would be debited to cost of goods sold for the 2012 consolidation worksheet with regard to the unrealized gross profit of the 2012 intra-entity transfer of merchandise?

A) $600.

B) $750.

C) $3,760.

D) $3,000.

E) $675.

Question

Question

Question

Gargiulo Company, a 90% owned subsidiary of Posito Corporation, sells inventory to Posito at a 25% profit on selling price. The following data are available pertaining to intra-entity purchases. Gargiulo was acquired on January 1, 2010.

Assume the equity method is used. The following data are available pertaining to Gargiulo's income and dividends.

Compute the non-controlling interest in Gargiulo's net income for 2011.

A) $8,500.

B) $8,570.

C) $8,430.

D) $8,400.

E) $7,580.

Assume the equity method is used. The following data are available pertaining to Gargiulo's income and dividends.

Compute the non-controlling interest in Gargiulo's net income for 2011.

A) $8,500.

B) $8,570.

C) $8,430.

D) $8,400.

E) $7,580.

Question

Question

Gargiulo Company, a 90% owned subsidiary of Posito Corporation, sells inventory to Posito at a 25% profit on selling price. The following data are available pertaining to intra-entity purchases. Gargiulo was acquired on January 1, 2010.

Assume the equity method is used. The following data are available pertaining to Gargiulo's income and dividends.

Compute the equity in earnings of Gargiulo reported on Posito's books for 2011.

A) $76,500.

B) $77,130.

C) $75,870.

D) $75,600.

E) $75,800.

Assume the equity method is used. The following data are available pertaining to Gargiulo's income and dividends.

Compute the equity in earnings of Gargiulo reported on Posito's books for 2011.

A) $76,500.

B) $77,130.

C) $75,870.

D) $75,600.

E) $75,800.

Question

Gargiulo Company, a 90% owned subsidiary of Posito Corporation, sells inventory to Posito at a 25% profit on selling price. The following data are available pertaining to intra-entity purchases. Gargiulo was acquired on January 1, 2010.

Assume the equity method is used. The following data are available pertaining to Gargiulo's income and dividends.

For consolidation purposes, what amount would be debited to cost of goods sold for the 2010 consolidation worksheet with regard to unrealized gross profit of the intra-entity transfer of merchandise?

A) $300.

B) $240.

C) $2,000.

D) $1,600.

E) $270.

Assume the equity method is used. The following data are available pertaining to Gargiulo's income and dividends.

For consolidation purposes, what amount would be debited to cost of goods sold for the 2010 consolidation worksheet with regard to unrealized gross profit of the intra-entity transfer of merchandise?

A) $300.

B) $240.

C) $2,000.

D) $1,600.

E) $270.

Question

Question

Gargiulo Company, a 90% owned subsidiary of Posito Corporation, sells inventory to Posito at a 25% profit on selling price. The following data are available pertaining to intra-entity purchases. Gargiulo was acquired on January 1, 2010.

Assume the equity method is used. The following data are available pertaining to Gargiulo's income and dividends.

For consolidation purposes, what amount would be debited to January 1 retained earnings for the 2012 consolidation worksheet entry with regard to the unrealized gross profit of the 2011 intra-entity transfer of merchandise?

A) $3,000.

B) $2,400.

C) $1,000.

D) $800.

E) $900.

Assume the equity method is used. The following data are available pertaining to Gargiulo's income and dividends.

For consolidation purposes, what amount would be debited to January 1 retained earnings for the 2012 consolidation worksheet entry with regard to the unrealized gross profit of the 2011 intra-entity transfer of merchandise?

A) $3,000.

B) $2,400.

C) $1,000.

D) $800.

E) $900.

Question

Question

Question

Wilson owned equipment with an estimated life of 10 years when it was acquired for an original cost of $80,000. The equipment had a book value of $50,000 at January 1, 2010. On January 1, 2010, Wilson realized that the useful life of the equipment was longer than originally anticipated, at ten remaining years.

On April 1, 2010 Simon Company, a 90% owned subsidiary of Wilson Company, bought the equipment from Wilson for $68,250 and for depreciation purposes used the estimated remaining life as of that date. The following data are available pertaining to Simon's income and dividends:

Compute the gain on transfer of equipment reported by Wilson for 2010.

A) $19,500.

B) $18,250.

C) $11,750.

D) $38,250.

E) $37,500.

On April 1, 2010 Simon Company, a 90% owned subsidiary of Wilson Company, bought the equipment from Wilson for $68,250 and for depreciation purposes used the estimated remaining life as of that date. The following data are available pertaining to Simon's income and dividends:

Compute the gain on transfer of equipment reported by Wilson for 2010.

A) $19,500.

B) $18,250.

C) $11,750.

D) $38,250.

E) $37,500.

Question

Question

Question

Wilson owned equipment with an estimated life of 10 years when it was acquired for an original cost of $80,000. The equipment had a book value of $50,000 at January 1, 2010. On January 1, 2010, Wilson realized that the useful life of the equipment was longer than originally anticipated, at ten remaining years.

On April 1, 2010 Simon Company, a 90% owned subsidiary of Wilson Company, bought the equipment from Wilson for $68,250 and for depreciation purposes used the estimated remaining life as of that date. The following data are available pertaining to Simon's income and dividends:

Compute Wilson's share of income from Simon for consolidation for 2010.

A) $72,000.

B) $90,000.

C) $73,575.

D) $73,800.

E) $72,500.

On April 1, 2010 Simon Company, a 90% owned subsidiary of Wilson Company, bought the equipment from Wilson for $68,250 and for depreciation purposes used the estimated remaining life as of that date. The following data are available pertaining to Simon's income and dividends:

Compute Wilson's share of income from Simon for consolidation for 2010.

A) $72,000.

B) $90,000.

C) $73,575.

D) $73,800.

E) $72,500.

Question

Question

Question

Wilson owned equipment with an estimated life of 10 years when it was acquired for an original cost of $80,000. The equipment had a book value of $50,000 at January 1, 2010. On January 1, 2010, Wilson realized that the useful life of the equipment was longer than originally anticipated, at ten remaining years.

On April 1, 2010 Simon Company, a 90% owned subsidiary of Wilson Company, bought the equipment from Wilson for $68,250 and for depreciation purposes used the estimated remaining life as of that date. The following data are available pertaining to Simon's income and dividends:

Compute the amortization of gain through a depreciation adjustment for 2011 for consolidation purposes.

A) $1,950.

B) $1,825.

C) $2,000.

D) $1,500.

E) $7,000.

On April 1, 2010 Simon Company, a 90% owned subsidiary of Wilson Company, bought the equipment from Wilson for $68,250 and for depreciation purposes used the estimated remaining life as of that date. The following data are available pertaining to Simon's income and dividends:

Compute the amortization of gain through a depreciation adjustment for 2011 for consolidation purposes.

A) $1,950.

B) $1,825.

C) $2,000.

D) $1,500.

E) $7,000.

Question

Question

Question

Wilson owned equipment with an estimated life of 10 years when it was acquired for an original cost of $80,000. The equipment had a book value of $50,000 at January 1, 2010. On January 1, 2010, Wilson realized that the useful life of the equipment was longer than originally anticipated, at ten remaining years.

On April 1, 2010 Simon Company, a 90% owned subsidiary of Wilson Company, bought the equipment from Wilson for $68,250 and for depreciation purposes used the estimated remaining life as of that date. The following data are available pertaining to Simon's income and dividends:

Compute Wilson's share of income from Simon for consolidation for 2011.

A) $108,000

B) $110,000.

C) $106,000.

D) $109,825.

E) $109,800.

On April 1, 2010 Simon Company, a 90% owned subsidiary of Wilson Company, bought the equipment from Wilson for $68,250 and for depreciation purposes used the estimated remaining life as of that date. The following data are available pertaining to Simon's income and dividends:

Compute Wilson's share of income from Simon for consolidation for 2011.

A) $108,000

B) $110,000.

C) $106,000.

D) $109,825.

E) $109,800.

Question

Question

Wilson owned equipment with an estimated life of 10 years when it was acquired for an original cost of $80,000. The equipment had a book value of $50,000 at January 1, 2010. On January 1, 2010, Wilson realized that the useful life of the equipment was longer than originally anticipated, at ten remaining years.

On April 1, 2010 Simon Company, a 90% owned subsidiary of Wilson Company, bought the equipment from Wilson for $68,250 and for depreciation purposes used the estimated remaining life as of that date. The following data are available pertaining to Simon's income and dividends:

Compute the amortization of gain through a depreciation adjustment for 2010 for consolidation purposes.

A) $1,950.

B) $1,825.

C) $1,500.

D) $2,000.

E) $5,250.

On April 1, 2010 Simon Company, a 90% owned subsidiary of Wilson Company, bought the equipment from Wilson for $68,250 and for depreciation purposes used the estimated remaining life as of that date. The following data are available pertaining to Simon's income and dividends:

Compute the amortization of gain through a depreciation adjustment for 2010 for consolidation purposes.

A) $1,950.

B) $1,825.

C) $1,500.

D) $2,000.

E) $5,250.

Question

Wilson owned equipment with an estimated life of 10 years when it was acquired for an original cost of $80,000. The equipment had a book value of $50,000 at January 1, 2010. On January 1, 2010, Wilson realized that the useful life of the equipment was longer than originally anticipated, at ten remaining years.

On April 1, 2010 Simon Company, a 90% owned subsidiary of Wilson Company, bought the equipment from Wilson for $68,250 and for depreciation purposes used the estimated remaining life as of that date. The following data are available pertaining to Simon's income and dividends:

Compute Wilson's share of income from Simon for consolidation for 2012.

A) $118,825.

B) $115,000.

C) $117,000.

D) $119,000.

E) $118,800.

On April 1, 2010 Simon Company, a 90% owned subsidiary of Wilson Company, bought the equipment from Wilson for $68,250 and for depreciation purposes used the estimated remaining life as of that date. The following data are available pertaining to Simon's income and dividends:

Compute Wilson's share of income from Simon for consolidation for 2012.

A) $118,825.

B) $115,000.

C) $117,000.

D) $119,000.

E) $118,800.

Question

Question

Wilson owned equipment with an estimated life of 10 years when it was acquired for an original cost of $80,000. The equipment had a book value of $50,000 at January 1, 2010. On January 1, 2010, Wilson realized that the useful life of the equipment was longer than originally anticipated, at ten remaining years.

On April 1, 2010 Simon Company, a 90% owned subsidiary of Wilson Company, bought the equipment from Wilson for $68,250 and for depreciation purposes used the estimated remaining life as of that date. The following data are available pertaining to Simon's income and dividends:

Compute the amortization of gain through a depreciation adjustment for 2012 for consolidation purposes.

A) $1,925.

B) $1,825.

C) $2,000.

D) $1,500.

E) $7,000.

On April 1, 2010 Simon Company, a 90% owned subsidiary of Wilson Company, bought the equipment from Wilson for $68,250 and for depreciation purposes used the estimated remaining life as of that date. The following data are available pertaining to Simon's income and dividends:

Compute the amortization of gain through a depreciation adjustment for 2012 for consolidation purposes.

A) $1,925.

B) $1,825.

C) $2,000.

D) $1,500.

E) $7,000.

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/127

Play

Full screen (f)

Deck 5: Consolidated Financial Statementsintra-Entity Asset Transactions

1

Yukon Co. acquired 75% percent of the voting common stock of Ontario Corp. on January 1, 2011. During the year, Yukon made sales of inventory to Ontario. The inventory cost Yukon $260,000 and was sold to Ontario for $390,000. Ontario still had $60,000 of the goods in its inventory at the end of the year. The amount of unrealized intra-entity profit that should be eliminated in the consolidation process at the end of 2011 is

A) $15,000.

B) $20,000.

C) $32,500.

D) $30,000.

E) $110,000.

A) $15,000.

B) $20,000.

C) $32,500.

D) $30,000.

E) $110,000.

B

2

Gentry Inc. acquired 100% of Gaspard Farms on January 5, 2010. During 2010, Gentry sold Gaspard Farms for $625,000 goods which had cost $425,000. Gaspard Farms still owned 12% of the goods at the end of the year. In 2011, Gentry sold goods with a cost of $800,000 to Gaspard Farms for $1,000,000, and Gaspard Farms still owned 10% of the goods at year-end. For 2011, cost of goods sold was $5,400,000 for Gentry and $1,200,000 for Gaspard Farms. What was consolidated cost of goods sold for 2011?

A) $6,600,000.

B) $6,604,000.

C) $5,620,000.

D) $5,596,000.

E) $5,625,000.

A) $6,600,000.

B) $6,604,000.

C) $5,620,000.

D) $5,596,000.

E) $5,625,000.

D

3

X-Beams Inc. owned 70% of the voting common stock of Kent Corp. During 2011, Kent made several sales of inventory to X-Beams. The total selling price was $180,000 and the cost was $100,000. At the end of the year, 20% of the goods were still in X-Beams' inventory. Kent's reported net income was $300,000. What was the non-controlling interest in Kent's net income?

A) $90,000.

B) $85,200.

C) $54,000.

D) $94,800.

E) $86,640.

A) $90,000.

B) $85,200.

C) $54,000.

D) $94,800.

E) $86,640.

B

4

Bauerly Co. owned 70% of the voting common stock of Devin Co. During 2010, Devin made frequent sales of inventory to Bauerly. There were unrealized gains of $40,000 in the beginning inventory and $25,000 of unrealized gains at the end of the year. Devin reported net income of $137,000 for 2010. Bauerly decided to use the equity method to account for the investment. What is the non-controlling interest's share of Devin's net income for 2010?

A) $41,100.

B) $33,600.

C) $21,600.

D) $45,600.

E) $36,600.

A) $41,100.

B) $33,600.

C) $21,600.

D) $45,600.

E) $36,600.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

5

Gibson Corp. owned a 90% interest in Sparis Co. Sparis frequently made sales of inventory to Gibson. The sales, which include a markup over cost of 25%, were $420,000 in 2010 and $500,000 in 2011. At the end of each year, Gibson still owned 30% of the goods. Net income for Sparis was $912,000 during 2011. What was the non-controlling interest's share of Sparis' net income for 2011?

A) $85,680.

B) $90,600.

C) $90,720.

D) $91,680.

E) $91,800.

A) $85,680.

B) $90,600.

C) $90,720.

D) $91,680.

E) $91,800.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

6

Justings Co. owned 80% of Evana Corp. During 2011, Justings sold to Evana land with a book value of $48,000. The selling price was $70,000. In its accounting records, Justings should

A) not recognize a gain on the sale of the land since it was made to a related party.

B) recognize a gain of $17,600.

C) defer recognition of the gain until Evana sells the land to a third party.

D) recognize a gain of $8,000.

E) recognize a gain of $22,000.

A) not recognize a gain on the sale of the land since it was made to a related party.

B) recognize a gain of $17,600.

C) defer recognition of the gain until Evana sells the land to a third party.

D) recognize a gain of $8,000.

E) recognize a gain of $22,000.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

7

On November 8, 2011, Power Corp. sold land to Wood Co., its wholly owned subsidiary. The land cost $61,500 and was sold to Wood for $89,000. From the perspective of the combination, when is the gain on the sale of the land realized?

A) Proportionately over a designated period of years.

B) When Wood Co. sells the land to a third party.

C) No gain can be recognized.

D) As Wood uses the land.

E) When Wood Co. begins using the land productively.

A) Proportionately over a designated period of years.

B) When Wood Co. sells the land to a third party.

C) No gain can be recognized.

D) As Wood uses the land.

E) When Wood Co. begins using the land productively.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

8

Clemente Co. owned all of the voting common stock of Snider Co. On January 2, 2010, Clemente sold equipment to Snider for $125,000. The equipment had cost Clemente $140,000. At the time of the sale, the balance in accumulated depreciation was $40,000. The equipment had a remaining useful life of five years and a $0 salvage value. Straight-line depreciation is used by both Clemente and Snider.

At what amount should the equipment (net of depreciation) be included in the consolidated balance sheet dated December 31, 2011?

A) $110,000.

B) $105,000.

C) $100,000.

D) $90,000.

E) $60,000.

At what amount should the equipment (net of depreciation) be included in the consolidated balance sheet dated December 31, 2011?

A) $110,000.

B) $105,000.

C) $100,000.

D) $90,000.

E) $60,000.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

9

Edgar Co. acquired 60% of Stendall Co. on January 1, 2011. During 2011, Edgar made several sales of inventory to Stendall. The cost and selling price of the goods were $140,000 and $200,000, respectively. Stendall still owned one-fourth of the goods at the end of 2011. Consolidated cost of goods sold for 2011 was $2,140,000 because of a consolidating adjustment for intra-entity sales less the entire profit remaining in Stendall's ending inventory.

How would non-controlling interest in net income have differed if the transfers had been for the same amount and cost, but from Stendall to Edgar?

A) Non-controlling interest in net income would have decreased by $6,000.

B) Non-controlling interest in net income would have increased by $24,000.

C) Non-controlling interest in net income would have increased by $20,000.

D) Non-controlling interest in net income would have decreased by $18,000.

E) Non-controlling interest in net income would have decreased by $56,000.

How would non-controlling interest in net income have differed if the transfers had been for the same amount and cost, but from Stendall to Edgar?

A) Non-controlling interest in net income would have decreased by $6,000.

B) Non-controlling interest in net income would have increased by $24,000.

C) Non-controlling interest in net income would have increased by $20,000.

D) Non-controlling interest in net income would have decreased by $18,000.

E) Non-controlling interest in net income would have decreased by $56,000.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

10

On January 1, 2011, Race Corp. acquired 80% of the voting common stock of Gallow Inc. During the year, Race sold to Gallow for $450,000 goods which cost $330,000. Gallow still owned 15% of the goods at year-end. Gallow's reported net income was $204,000, and Race's net income was $806,000. Race decided to use the equity method to account for this investment. What was the non-controlling interest's share of consolidated net income?

A) $3,600.

B) $22,800.

C) $30,900.

D) $32,900.

E) $40,800.

A) $3,600.

B) $22,800.

C) $30,900.

D) $32,900.

E) $40,800.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

11

On January 1, 2011, Payton Co. sold equipment to its subsidiary, Starker Corp., for $115,000. The equipment had cost $125,000, and the balance in accumulated depreciation was $45,000. The equipment had an estimated remaining useful life of eight years and $0 salvage value. Both companies use straight-line depreciation. On their separate 2011 income statements, Payton and Starker reported depreciation expense of $84,000 and $60,000, respectively. The amount of depreciation expense on the consolidated income statement for 2011 would have been

A) $144,000.

B) $148,375.

C) $109,000.

D) $134,000.

E) $139,625.

A) $144,000.

B) $148,375.

C) $109,000.

D) $134,000.

E) $139,625.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

12

Prince Corp. owned 80% of Kile Corp.'s common stock. During October 2011, Kile sold merchandise to Prince for $140,000. At December 31, 2011, 50% of this merchandise remained in Prince's inventory. For 2011, gross profit percentages were 30% of sales for Prince and 40% of sales for Kile. The amount of unrealized intra-entity profit in ending inventory at December 31, 2011 that should be eliminated in the consolidation process is

A) $28,000.

B) $56,000.

C) $22,400.

D) $21,000.

E) $42,000.

A) $28,000.

B) $56,000.

C) $22,400.

D) $21,000.

E) $42,000.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

13

Pot Co. holds 90% of the common stock of Skillet Co. During 2011, Pot reported sales of $1,120,000 and cost of goods sold of $840,000. For this same period, Skillet had sales of $420,000 and cost of goods sold of $252,000.

Included in the amounts for Pot's sales were Pot's sales of merchandise to Skillet for $140,000. There were no sales from Skillet to Pot. Intra-entity sales had the same markup as sales to outsiders. Skillet still had 40% of the intra-entity sales as inventory at the end of 2011. What are consolidated sales and cost of goods sold for 2011?

A) $1,400,000 and $952,000.

B) $1,400,000 and $966,000.

C) $1,540,000 and $1,078,000.

D) $1,400,000 and $1,022,000.

E) $1,540,000 and $1,092,000.

Included in the amounts for Pot's sales were Pot's sales of merchandise to Skillet for $140,000. There were no sales from Skillet to Pot. Intra-entity sales had the same markup as sales to outsiders. Skillet still had 40% of the intra-entity sales as inventory at the end of 2011. What are consolidated sales and cost of goods sold for 2011?

A) $1,400,000 and $952,000.

B) $1,400,000 and $966,000.

C) $1,540,000 and $1,078,000.

D) $1,400,000 and $1,022,000.

E) $1,540,000 and $1,092,000.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

14

During 2010, Von Co. sold inventory to its wholly-owned subsidiary, Lord Co. The inventory cost $30,000 and was sold to Lord for $44,000. From the perspective of the combination, when is the $14,000 gain realized?

A) When the goods are sold to a third party by Lord.

B) When Lord pays Von for the goods.

C) When Von sold the goods to Lord.

D) When the goods are used by Lord.

E) No gain can be recognized since the transaction was between related parties.

A) When the goods are sold to a third party by Lord.

B) When Lord pays Von for the goods.

C) When Von sold the goods to Lord.

D) When the goods are used by Lord.

E) No gain can be recognized since the transaction was between related parties.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

15

Norek Corp. owned 70% of the voting common stock of Thelma Co. On January 2, 2010, Thelma sold a parcel of land to Norek. The land had a book value of $32,000 and was sold to Norek for $45,000. Thelma's reported net income for 2010 was $119,000. What is the non-controlling interest's share of Thelma's net income?

A) $35,700.

B) $31,800.

C) $39,600.

D) $22,200.

E) $26,100.

A) $35,700.

B) $31,800.

C) $39,600.

D) $22,200.

E) $26,100.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

16

Edgar Co. acquired 60% of Stendall Co. on January 1, 2011. During 2011, Edgar made several sales of inventory to Stendall. The cost and selling price of the goods were $140,000 and $200,000, respectively. Stendall still owned one-fourth of the goods at the end of 2011. Consolidated cost of goods sold for 2011 was $2,140,000 because of a consolidating adjustment for intra-entity sales less the entire profit remaining in Stendall's ending inventory.

How would consolidated cost of goods sold have differed if the inventory transfers had been for the same amount and cost, but from Stendall to Edgar?

A) Consolidated cost of goods sold would have remained $2,140,000.

B) Consolidated cost of goods sold would have been more than $2,140,000 because of the controlling interest in the subsidiary.

C) Consolidated cost of goods sold would have been less than $2,140,000 because of the non-controlling interest in the subsidiary.

D) Consolidated cost of goods sold would have been more than $2,140,000 because of the non-controlling interest in the subsidiary.

E) The effect on consolidated cost of goods sold cannot be predicted from the information provided.

How would consolidated cost of goods sold have differed if the inventory transfers had been for the same amount and cost, but from Stendall to Edgar?

A) Consolidated cost of goods sold would have remained $2,140,000.

B) Consolidated cost of goods sold would have been more than $2,140,000 because of the controlling interest in the subsidiary.

C) Consolidated cost of goods sold would have been less than $2,140,000 because of the non-controlling interest in the subsidiary.

D) Consolidated cost of goods sold would have been more than $2,140,000 because of the non-controlling interest in the subsidiary.

E) The effect on consolidated cost of goods sold cannot be predicted from the information provided.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

17

Chain Co. owned all of the voting common stock of Shannon Corp. The corporations' balance sheets dated December 31, 2010, include the following balances for land: for Chain--$416,000, and for Shannon--$256,000. On the original date of acquisition, the book value of Shannon's land was equal to its fair value. On April 4, 2011, Chain sold to Shannon a parcel of land with a book value of $65,000. The selling price was $83,000. There were no other transactions which affected the companies' land accounts during 2010. What is the consolidated balance for land on the 2011 balance sheet?

A) $672,000.

B) $690,000.

C) $755,000.

D) $737,000.

E) $654,000.

A) $672,000.

B) $690,000.

C) $755,000.

D) $737,000.

E) $654,000.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

18

Pot Co. holds 90% of the common stock of Skillet Co. During 2011, Pot reported sales of $1,120,000 and cost of goods sold of $840,000. For this same period, Skillet had sales of $420,000 and cost of goods sold of $252,000.

Included in the amounts for Skillet's sales were Skillet's sales of merchandise to Pot for $140,000. There were no sales from Pot to Skillet. Intra-entity sales had the same markup as sales to outsiders. Pot still had 40% of the intra-entity sales as inventory at the end of 2011. What are consolidated sales and cost of goods sold for 2011?

A) $1,400,000 and $952,000.

B) $1,400,000 and $966,000.

C) $1,540,000 and $1,078,000.

D) $1,400,000 and $974,400.

E) $1,540,000 and $1,092,000.

Included in the amounts for Skillet's sales were Skillet's sales of merchandise to Pot for $140,000. There were no sales from Pot to Skillet. Intra-entity sales had the same markup as sales to outsiders. Pot still had 40% of the intra-entity sales as inventory at the end of 2011. What are consolidated sales and cost of goods sold for 2011?

A) $1,400,000 and $952,000.

B) $1,400,000 and $966,000.

C) $1,540,000 and $1,078,000.

D) $1,400,000 and $974,400.

E) $1,540,000 and $1,092,000.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

19

Clemente Co. owned all of the voting common stock of Snider Co. On January 2, 2010, Clemente sold equipment to Snider for $125,000. The equipment had cost Clemente $140,000. At the time of the sale, the balance in accumulated depreciation was $40,000. The equipment had a remaining useful life of five years and a $0 salvage value. Straight-line depreciation is used by both Clemente and Snider.

At what amount should the equipment (net of depreciation) be included in the consolidated balance sheet dated December 31, 2010?

A) $105,000.

B) $100,000.

C) $95,000.

D) $80,000.

E) $85,000.

At what amount should the equipment (net of depreciation) be included in the consolidated balance sheet dated December 31, 2010?

A) $105,000.

B) $100,000.

C) $95,000.

D) $80,000.

E) $85,000.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

20

Webb Co. acquired 100% of Rand Inc. on January 5, 2011. During 2011, Webb sold goods to Rand for $2,400,000 that cost Webb $1,800,000. Rand still owned 40% of the goods at the end of the year. Cost of goods sold was $10,800,000 for Webb and $6,400,000 for Rand. What was consolidated cost of goods sold?

A) $17,200,000.

B) $15,040,000.

C) $14,800,000.

D) $16,960,000.

E) $14,560,000.

A) $17,200,000.

B) $15,040,000.

C) $14,800,000.

D) $16,960,000.

E) $14,560,000.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

21

Strickland Company sells inventory to its parent, Carter Company, at a profit during 2010. One-third of the inventory is sold by Carter in 2010.

In the consolidation worksheet for 2011, assuming Carter uses the initial value method of accounting for its investment in Strickland, which of the following choices would be a credit entry to eliminate unrealized intra-entity gross profit with regard to the 2010 intra-entity sales?

A) Retained earnings.

B) Cost of goods sold.

C) Inventory.

D) Investment in Strickland Company.

E) Sales.

In the consolidation worksheet for 2011, assuming Carter uses the initial value method of accounting for its investment in Strickland, which of the following choices would be a credit entry to eliminate unrealized intra-entity gross profit with regard to the 2010 intra-entity sales?

A) Retained earnings.

B) Cost of goods sold.

C) Inventory.

D) Investment in Strickland Company.

E) Sales.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

22

Walsh Company sells inventory to its subsidiary, Fisher Company, at a profit during 2010. One-third of the inventory is sold by Walsh uses the equity method to account for its investment in Fisher.

In the consolidation worksheet for 2010, which of the following choices would be a debit entry to eliminate unrealized intra-entity gross profit with regard to the 2010 intra-entity sales?

A) Retained earnings.

B) Cost of goods sold.

C) Inventory.

D) Investment in Fisher Company.

E) Sales.

In the consolidation worksheet for 2010, which of the following choices would be a debit entry to eliminate unrealized intra-entity gross profit with regard to the 2010 intra-entity sales?

A) Retained earnings.

B) Cost of goods sold.

C) Inventory.

D) Investment in Fisher Company.

E) Sales.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

23

Pot Co. holds 90% of the common stock of Skillet Co. During 2011, Pot reported sales of $1,120,000 and cost of goods sold of $840,000. For this same period, Skillet had sales of $420,000 and cost of goods sold of $252,000.

Include in the amounts for Pot's sales were Pot's sales of merchandise to Skillet for $140,000. There were no sales from Skillet to Pot. Intra-entity sales had the same markup as sales to outsiders. Skillet had resold all of the intra-entity purchase from Pot to outside parties during 2011. What are consolidated sales and cost of goods sold for 2011?

A) $1,400,000 and $952,000.

B) $1,400,000 and $1,092,000.

C) $1,540,000 and $952,000.

D) $1,400,000 and $1,232,000.

E) $1,540,000 and $1,092,000.

Include in the amounts for Pot's sales were Pot's sales of merchandise to Skillet for $140,000. There were no sales from Skillet to Pot. Intra-entity sales had the same markup as sales to outsiders. Skillet had resold all of the intra-entity purchase from Pot to outside parties during 2011. What are consolidated sales and cost of goods sold for 2011?

A) $1,400,000 and $952,000.

B) $1,400,000 and $1,092,000.

C) $1,540,000 and $952,000.

D) $1,400,000 and $1,232,000.

E) $1,540,000 and $1,092,000.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

24

Walsh Company sells inventory to its subsidiary, Fisher Company, at a profit during 2010. One-third of the inventory is sold by Walsh uses the equity method to account for its investment in Fisher.

In the consolidation worksheet for 2010, which of the following choices would be a credit entry to eliminate unrealized intra-entity gross profit with regard to the 2010 intra-entity sales?

A) Retained earnings.

B) Cost of goods sold.

C) Inventory.

D) Investment in Fisher Company.

E) Sales.

In the consolidation worksheet for 2010, which of the following choices would be a credit entry to eliminate unrealized intra-entity gross profit with regard to the 2010 intra-entity sales?

A) Retained earnings.

B) Cost of goods sold.

C) Inventory.

D) Investment in Fisher Company.

E) Sales.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

25

On January 1, 2011, Pride, Inc. acquired 80% of the outstanding voting common stock of Strong Corp. for $364,000. There is no active market for Strong's stock. Of this payment, $28,000 was allocated to equipment (with a five-year life) that had been undervalued on Strong's books by $35,000. Any remaining excess was attributable to goodwill which has not been impaired.

As of December 31, 2011, before preparing the consolidated worksheet, the financial statements appeared as follows:

During 2011, Pride bought inventory for $112,000 and sold it to Strong for $140,000. Only half of this purchase had been paid for by Strong by the end of the year. 60% of these goods were still in the company's possession on December 31.

What is the consolidated total for inventory at December 31, 2011?

A) $336,000.

B) $280,000.

C) $364,000.

D) $347,200.

E) $349,300.

As of December 31, 2011, before preparing the consolidated worksheet, the financial statements appeared as follows:

During 2011, Pride bought inventory for $112,000 and sold it to Strong for $140,000. Only half of this purchase had been paid for by Strong by the end of the year. 60% of these goods were still in the company's possession on December 31.

What is the consolidated total for inventory at December 31, 2011?

A) $336,000.

B) $280,000.

C) $364,000.

D) $347,200.

E) $349,300.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

26

Dalton Corp. owned 70% of the outstanding common stock of Shrugs Inc. On January 1, 2009, Dalton acquired a building with a ten-year life for $420,000. No salvage value was anticipated and the building was to be depreciated on the straight-line basis. On January 1, 2011, Dalton sold this building to Shrugs for $392,000. At that time, the building had a remaining life of eight years but still no expected salvage value. In preparing financial statements for 2011, how does this transfer affect the calculation of Dalton's share of consolidated net income?

A) Consolidated net income must be reduced by $44,800.

B) Consolidated net income must be reduced by $50,400.

C) Consolidated net income must be reduced by $49,000.

D) Consolidated net income must be reduced by $56,000.

E) Consolidated net income must be reduced by $34,300.

A) Consolidated net income must be reduced by $44,800.

B) Consolidated net income must be reduced by $50,400.

C) Consolidated net income must be reduced by $49,000.

D) Consolidated net income must be reduced by $56,000.

E) Consolidated net income must be reduced by $34,300.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

27

Walsh Company sells inventory to its subsidiary, Fisher Company, at a profit during 2010. One-third of the inventory is sold by Walsh uses the equity method to account for its investment in Fisher.

In the consolidation worksheet for 2010, which of the following choices would be a debit entry to eliminate the intra-entity transfer of inventory?

A) Retained earnings.

B) Cost of goods sold.

C) Inventory.

D) Investment in Fisher Company.

E) Sales.

In the consolidation worksheet for 2010, which of the following choices would be a debit entry to eliminate the intra-entity transfer of inventory?

A) Retained earnings.

B) Cost of goods sold.

C) Inventory.

D) Investment in Fisher Company.

E) Sales.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

28

Strickland Company sells inventory to its parent, Carter Company, at a profit during 2010. One-third of the inventory is sold by Carter in 2010.

In the consolidation worksheet for 2010, which of the following choices would be a credit entry to eliminate the intra-entity transfer of inventory?

A) Retained earnings.

B) Cost of goods sold.

C) Inventory.

D) Investment in Strickland Company.

E) Sales.

In the consolidation worksheet for 2010, which of the following choices would be a credit entry to eliminate the intra-entity transfer of inventory?

A) Retained earnings.

B) Cost of goods sold.

C) Inventory.

D) Investment in Strickland Company.

E) Sales.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

29

On January 1, 2011, Pride, Inc. acquired 80% of the outstanding voting common stock of Strong Corp. for $364,000. There is no active market for Strong's stock. Of this payment, $28,000 was allocated to equipment (with a five-year life) that had been undervalued on Strong's books by $35,000. Any remaining excess was attributable to goodwill which has not been impaired.

As of December 31, 2011, before preparing the consolidated worksheet, the financial statements appeared as follows:

During 2011, Pride bought inventory for $112,000 and sold it to Strong for $140,000. Only half of this purchase had been paid for by Strong by the end of the year. 60% of these goods were still in the company's possession on December 31.

What is the total of consolidated operating expenses?

A) $42,000.

B) $47,600.

C) $53,200.

D) $49,000.

E) $35,000.

As of December 31, 2011, before preparing the consolidated worksheet, the financial statements appeared as follows:

During 2011, Pride bought inventory for $112,000 and sold it to Strong for $140,000. Only half of this purchase had been paid for by Strong by the end of the year. 60% of these goods were still in the company's possession on December 31.

What is the total of consolidated operating expenses?

A) $42,000.

B) $47,600.

C) $53,200.

D) $49,000.

E) $35,000.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

30

Walsh Company sells inventory to its subsidiary, Fisher Company, at a profit during 2010. One-third of the inventory is sold by Walsh uses the equity method to account for its investment in Fisher.

In the consolidation worksheet for 2011, which of the following choices would be a credit entry to eliminate unrealized intra-entity gross profit with regard to the 2010 intra-entity sales?

A) Retained earnings.

B) Cost of goods sold.

C) Inventory.

D) Investment in Fisher Company.

E) Sales.

In the consolidation worksheet for 2011, which of the following choices would be a credit entry to eliminate unrealized intra-entity gross profit with regard to the 2010 intra-entity sales?

A) Retained earnings.

B) Cost of goods sold.

C) Inventory.

D) Investment in Fisher Company.

E) Sales.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

31

Strickland Company sells inventory to its parent, Carter Company, at a profit during 2010. One-third of the inventory is sold by Carter in 2010.

In the consolidation worksheet for 2010, which of the following choices would be a debit entry to eliminate unrealized intra-entity gross profit with regard to the 2010 intra-entity sales?

A) Retained earnings.

B) Cost of goods sold.

C) Inventory.

D) Investment in Strickland Company.

E) Sales.

In the consolidation worksheet for 2010, which of the following choices would be a debit entry to eliminate unrealized intra-entity gross profit with regard to the 2010 intra-entity sales?

A) Retained earnings.

B) Cost of goods sold.

C) Inventory.

D) Investment in Strickland Company.

E) Sales.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

32

Strickland Company sells inventory to its parent, Carter Company, at a profit during 2010. One-third of the inventory is sold by Carter in 2010.

In the consolidation worksheet for 2011, assuming Carter uses the initial value method of accounting for its investment in Strickland, which of the following choices would be a debit entry to eliminate unrealized intra-entity gross profit with regard to the 2010 intra-entity sales?

A) Retained earnings.

B) Cost of goods sold.

C) Inventory.

D) Investment in Strickland Company.

E) Sales.

In the consolidation worksheet for 2011, assuming Carter uses the initial value method of accounting for its investment in Strickland, which of the following choices would be a debit entry to eliminate unrealized intra-entity gross profit with regard to the 2010 intra-entity sales?

A) Retained earnings.

B) Cost of goods sold.

C) Inventory.

D) Investment in Strickland Company.

E) Sales.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

33

On January 1, 2011, Pride, Inc. acquired 80% of the outstanding voting common stock of Strong Corp. for $364,000. There is no active market for Strong's stock. Of this payment, $28,000 was allocated to equipment (with a five-year life) that had been undervalued on Strong's books by $35,000. Any remaining excess was attributable to goodwill which has not been impaired.

As of December 31, 2011, before preparing the consolidated worksheet, the financial statements appeared as follows:

During 2011, Pride bought inventory for $112,000 and sold it to Strong for $140,000. Only half of this purchase had been paid for by Strong by the end of the year. 60% of these goods were still in the company's possession on December 31.

What is the consolidated total for equipment (net) at December 31, 2011?

A) $952,000.

B) $1,058,400.

C) $1,069,600.

D) $1,064,000.

E) $1,066,800.

As of December 31, 2011, before preparing the consolidated worksheet, the financial statements appeared as follows:

During 2011, Pride bought inventory for $112,000 and sold it to Strong for $140,000. Only half of this purchase had been paid for by Strong by the end of the year. 60% of these goods were still in the company's possession on December 31.

What is the consolidated total for equipment (net) at December 31, 2011?

A) $952,000.

B) $1,058,400.

C) $1,069,600.

D) $1,064,000.

E) $1,066,800.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

34

Strickland Company sells inventory to its parent, Carter Company, at a profit during 2010. One-third of the inventory is sold by Carter in 2010.

In the consolidation worksheet for 2010, which of the following choices would be a credit entry to eliminate unrealized intra-entity gross profit with regard to the 2010 intra-entity sales?

A) Retained earnings.

B) Cost of goods sold.

C) Inventory.

D) Investment in Strickland Company.

E) Sales.

In the consolidation worksheet for 2010, which of the following choices would be a credit entry to eliminate unrealized intra-entity gross profit with regard to the 2010 intra-entity sales?

A) Retained earnings.

B) Cost of goods sold.

C) Inventory.

D) Investment in Strickland Company.

E) Sales.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

35

Walsh Company sells inventory to its subsidiary, Fisher Company, at a profit during 2010. One-third of the inventory is sold by Walsh uses the equity method to account for its investment in Fisher.

In the consolidation worksheet for 2010, which of the following choices would be a credit entry to eliminate the intra-entity transfer of inventory?

A) Retained earnings.

B) Cost of goods sold.

C) Inventory.

D) Investment in Fisher Company.

E) Sales.

In the consolidation worksheet for 2010, which of the following choices would be a credit entry to eliminate the intra-entity transfer of inventory?

A) Retained earnings.

B) Cost of goods sold.

C) Inventory.

D) Investment in Fisher Company.

E) Sales.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

36

On January 1, 2011, Pride, Inc. acquired 80% of the outstanding voting common stock of Strong Corp. for $364,000. There is no active market for Strong's stock. Of this payment, $28,000 was allocated to equipment (with a five-year life) that had been undervalued on Strong's books by $35,000. Any remaining excess was attributable to goodwill which has not been impaired.

As of December 31, 2011, before preparing the consolidated worksheet, the financial statements appeared as follows:

During 2011, Pride bought inventory for $112,000 and sold it to Strong for $140,000. Only half of this purchase had been paid for by Strong by the end of the year. 60% of these goods were still in the company's possession on December 31.

What is the total of consolidated revenues?

A) $700,000.

B) $644,000.

C) $588,000.

D) $560,000.

E) $840,000.

As of December 31, 2011, before preparing the consolidated worksheet, the financial statements appeared as follows:

During 2011, Pride bought inventory for $112,000 and sold it to Strong for $140,000. Only half of this purchase had been paid for by Strong by the end of the year. 60% of these goods were still in the company's possession on December 31.

What is the total of consolidated revenues?

A) $700,000.

B) $644,000.

C) $588,000.

D) $560,000.

E) $840,000.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

37

On January 1, 2011, Pride, Inc. acquired 80% of the outstanding voting common stock of Strong Corp. for $364,000. There is no active market for Strong's stock. Of this payment, $28,000 was allocated to equipment (with a five-year life) that had been undervalued on Strong's books by $35,000. Any remaining excess was attributable to goodwill which has not been impaired.

As of December 31, 2011, before preparing the consolidated worksheet, the financial statements appeared as follows:

During 2011, Pride bought inventory for $112,000 and sold it to Strong for $140,000. Only half of this purchase had been paid for by Strong by the end of the year. 60% of these goods were still in the company's possession on December 31.

What is the total of consolidated cost of goods sold?

A) $196,000.

B) $212,800.

C) $184,800.

D) $203,000.

E) $168,000.

As of December 31, 2011, before preparing the consolidated worksheet, the financial statements appeared as follows:

During 2011, Pride bought inventory for $112,000 and sold it to Strong for $140,000. Only half of this purchase had been paid for by Strong by the end of the year. 60% of these goods were still in the company's possession on December 31.

What is the total of consolidated cost of goods sold?

A) $196,000.

B) $212,800.

C) $184,800.

D) $203,000.

E) $168,000.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

38

Walsh Company sells inventory to its subsidiary, Fisher Company, at a profit during 2010. One-third of the inventory is sold by Walsh uses the equity method to account for its investment in Fisher.

In the consolidation worksheet for 2011, which of the following choices would be a debit entry to eliminate unrealized intra-entity gross profit with regard to the 2010 intra-entity sales?

A) Retained earnings.

B) Cost of goods sold.

C) Inventory.

D) Investment in Fisher Company.

E) Sales.

In the consolidation worksheet for 2011, which of the following choices would be a debit entry to eliminate unrealized intra-entity gross profit with regard to the 2010 intra-entity sales?

A) Retained earnings.

B) Cost of goods sold.

C) Inventory.

D) Investment in Fisher Company.

E) Sales.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

39

Strickland Company sells inventory to its parent, Carter Company, at a profit during 2010. One-third of the inventory is sold by Carter in 2010.

In the consolidation worksheet for 2010, which of the following choices would be a debit entry to eliminate the intra-entity transfer of inventory?

A) Retained earnings.

B) Cost of goods sold.

C) Inventory.

D) Investment in Strickland Company.

E) Sales.

In the consolidation worksheet for 2010, which of the following choices would be a debit entry to eliminate the intra-entity transfer of inventory?

A) Retained earnings.

B) Cost of goods sold.

C) Inventory.

D) Investment in Strickland Company.

E) Sales.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

40

On January 1, 2011, Pride, Inc. acquired 80% of the outstanding voting common stock of Strong Corp. for $364,000. There is no active market for Strong's stock. Of this payment, $28,000 was allocated to equipment (with a five-year life) that had been undervalued on Strong's books by $35,000. Any remaining excess was attributable to goodwill which has not been impaired.

As of December 31, 2011, before preparing the consolidated worksheet, the financial statements appeared as follows:

During 2011, Pride bought inventory for $112,000 and sold it to Strong for $140,000. Only half of this purchase had been paid for by Strong by the end of the year. 60% of these goods were still in the company's possession on December 31.

What is the consolidated total of non-controlling interest appearing in the balance sheet?

A) $100,800.

B) $97,440.

C) $93,800.

D) $120,400.

E) $117,040.

As of December 31, 2011, before preparing the consolidated worksheet, the financial statements appeared as follows:

During 2011, Pride bought inventory for $112,000 and sold it to Strong for $140,000. Only half of this purchase had been paid for by Strong by the end of the year. 60% of these goods were still in the company's possession on December 31.

What is the consolidated total of non-controlling interest appearing in the balance sheet?

A) $100,800.

B) $97,440.

C) $93,800.

D) $120,400.

E) $117,040.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

41

Gargiulo Company, a 90% owned subsidiary of Posito Corporation, sells inventory to Posito at a 25% profit on selling price. The following data are available pertaining to intra-entity purchases. Gargiulo was acquired on January 1, 2010.

Assume the equity method is used. The following data are available pertaining to Gargiulo's income and dividends.

For consolidation purposes, what amount would be debited to cost of goods sold for the 2011 consolidation worksheet with regard to the unrealized gross profit of the 2011 intra-entity transfer of merchandise?

A) $1,000.

B) $800.

C) $3,000.

D) $2,400.

E) $900.

Assume the equity method is used. The following data are available pertaining to Gargiulo's income and dividends.

For consolidation purposes, what amount would be debited to cost of goods sold for the 2011 consolidation worksheet with regard to the unrealized gross profit of the 2011 intra-entity transfer of merchandise?

A) $1,000.

B) $800.

C) $3,000.

D) $2,400.

E) $900.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

42

An intra-entity sale took place whereby the transfer price was less than the book value of a depreciable asset. Which statement is true for the year following the sale?

A) A worksheet entry is made with a debit to investment in subsidiary for an upstream transfer.

B) A worksheet entry is made with a debit to investment in subsidiary for a downstream transfer.

C) A worksheet entry is made with a credit to investment in subsidiary for a downstream transfer when the parent uses the equity method.

D) A worksheet entry is made with a debit to retained earnings for an upstream transfer, regardless of the method used to account for the investment.

E) No worksheet entry is necessary.

A) A worksheet entry is made with a debit to investment in subsidiary for an upstream transfer.

B) A worksheet entry is made with a debit to investment in subsidiary for a downstream transfer.

C) A worksheet entry is made with a credit to investment in subsidiary for a downstream transfer when the parent uses the equity method.

D) A worksheet entry is made with a debit to retained earnings for an upstream transfer, regardless of the method used to account for the investment.

E) No worksheet entry is necessary.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

43

Gargiulo Company, a 90% owned subsidiary of Posito Corporation, sells inventory to Posito at a 25% profit on selling price. The following data are available pertaining to intra-entity purchases. Gargiulo was acquired on January 1, 2010.

Assume the equity method is used. The following data are available pertaining to Gargiulo's income and dividends.

Compute the equity in earnings of Gargiulo reported on Posito's books for 2012.

A) $84,600.

B) $84,375.

C) $83,925.

D) $84,825.

E) $84,850.

Assume the equity method is used. The following data are available pertaining to Gargiulo's income and dividends.

Compute the equity in earnings of Gargiulo reported on Posito's books for 2012.

A) $84,600.

B) $84,375.

C) $83,925.

D) $84,825.

E) $84,850.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

44

When comparing the difference between an upstream and downstream transfer of inventory, and using the initial value method, which of the following statements is true when there is a non-controlling interest?

A) Income from subsidiary will be lower by the amount of the ending inventory profit multiplied by the non-controlling interest percentage for downstream transfers.

B) Income from subsidiary will be higher by the amount of the ending inventory profit multiplied by the non-controlling interest percentage for downstream transfers.

C) Income from subsidiary will be reduced for downstream ending inventory profit but not for upstream profit, before the effect of the non-controlling interest.

D) Income from subsidiary will be reduced for upstream ending inventory profit but not for downstream profit, before the effect of the non-controlling interest.

E) Income from subsidiary will be the same for upstream and downstream profit.

A) Income from subsidiary will be lower by the amount of the ending inventory profit multiplied by the non-controlling interest percentage for downstream transfers.

B) Income from subsidiary will be higher by the amount of the ending inventory profit multiplied by the non-controlling interest percentage for downstream transfers.

C) Income from subsidiary will be reduced for downstream ending inventory profit but not for upstream profit, before the effect of the non-controlling interest.

D) Income from subsidiary will be reduced for upstream ending inventory profit but not for downstream profit, before the effect of the non-controlling interest.

E) Income from subsidiary will be the same for upstream and downstream profit.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

45

Gargiulo Company, a 90% owned subsidiary of Posito Corporation, sells inventory to Posito at a 25% profit on selling price. The following data are available pertaining to intra-entity purchases. Gargiulo was acquired on January 1, 2010.

Assume the equity method is used. The following data are available pertaining to Gargiulo's income and dividends.

For consolidation purposes, what amount would be debited to January 1 retained earnings for the 2010 consolidation worksheet entry with regard to the unrealized gross profit of the 2010 intra-entity transfer of merchandise?

A) $0.

B) $1,600.

C) $300.

D) $240.

E) $270.

Assume the equity method is used. The following data are available pertaining to Gargiulo's income and dividends.

For consolidation purposes, what amount would be debited to January 1 retained earnings for the 2010 consolidation worksheet entry with regard to the unrealized gross profit of the 2010 intra-entity transfer of merchandise?

A) $0.

B) $1,600.

C) $300.

D) $240.

E) $270.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

46