Deck 11: Retirement Planning

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

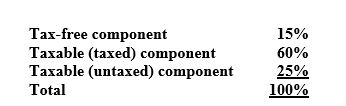

Ms Ayumi Sapporo recently retired from her position as head chef of the Red Blossom Japanese restaurant on 12 June 2014. She retired a few weeks before her 60th birthday (on the 30th June 2014) to give herself time to organise a large birthday party for which she is expecting guests to arrive from Japan to celebrate with her. Ayumi is wanting to use her retirement funds to provide money to pay for the party as well as to pay-out her home mortgage as well as a car loan and credit card debts that she struggled to meet whilst she was working. In total Ayumi is seeking to withdraw $450,000 on the 29th June 2014 as a lump sum from her accumulated retirement funds in order to provide for these financial commitments. Ayumi has been provided a statement from the ACME Superannuation Fund calculated to the 29th June 2014 showing an accumulated retirement funds balance of $850,000 allocated as follows:

Whilst catching a bus home from the market on the 27th June 2014 where she was starting to buy her supplies for her birthday party, Ayumi heard some people on the bus say that a financial adviser that they had recently had an appointment with had stated that where possible retirees should look to withdraw their retirement funds after they turn age 60 and not before.

Whilst catching a bus home from the market on the 27th June 2014 where she was starting to buy her supplies for her birthday party, Ayumi heard some people on the bus say that a financial adviser that they had recently had an appointment with had stated that where possible retirees should look to withdraw their retirement funds after they turn age 60 and not before.

Calculate the tax payable by Ayumi if she proceeds with the information given in the question and withdraws $450,000 on the 29th June 2014 from the ACME Superannuation Fund and the alternative advice she overheard on the bus that recommended leaving the withdrawal of the designated retirement funds until at least the 30th June 2014. Briefly comment on the calculated outcomes. Note: Assume that the total balance of Ayumi's retirement funds of $850,000 and the allocations previously provided do not change.

Whilst catching a bus home from the market on the 27th June 2014 where she was starting to buy her supplies for her birthday party, Ayumi heard some people on the bus say that a financial adviser that they had recently had an appointment with had stated that where possible retirees should look to withdraw their retirement funds after they turn age 60 and not before.Calculate the tax payable by Ayumi if she proceeds with the information given in the question and withdraws $450,000 on the 29th June 2014 from the ACME Superannuation Fund and the alternative advice she overheard on the bus that recommended leaving the withdrawal of the designated retirement funds until at least the 30th June 2014. Briefly comment on the calculated outcomes. Note: Assume that the total balance of Ayumi's retirement funds of $850,000 and the allocations previously provided do not change.

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/30

Play

Full screen (f)

Deck 11: Retirement Planning

1

In accordance with financial mathematics concepts, for a given nominal rate of return and present value, a larger number of periods all other things being equal will:

A) increase the payment for a superannuant in pension mode.

B) decrease the payment for a superannuant in pension mode.

C) leave the payment unchanged for a superannuant in pension mode.

D) either a or c

A) increase the payment for a superannuant in pension mode.

B) decrease the payment for a superannuant in pension mode.

C) leave the payment unchanged for a superannuant in pension mode.

D) either a or c

B

2

Age pension entitlements in Australia are subject to a(n):

A) assets test up to an age of 75.

B) income test up to an age of 80.

C) assets test and income test regardless of a person's age.

D) assets test up to an age of 80 and income test regardless of a person's age.

A) assets test up to an age of 75.

B) income test up to an age of 80.

C) assets test and income test regardless of a person's age.

D) assets test up to an age of 80 and income test regardless of a person's age.

C

3

The amount of tax payable on the release of superannuation moneys is a function of:

A) the 'type' of superannuation money held in the superannuant's account, the age of the individual and what the moneys will be spent on.

B) the 'type' of superannuation money held in the superannuant's account, the age of the individual and whether the money is withdrawn as a lump sum or income stream.

C) the 'type' of superannuation money held in the superannuant's account, the gender of the individual and whether the money is withdrawn as a lump sum or income stream.

D) none of the above are relevant.

A) the 'type' of superannuation money held in the superannuant's account, the age of the individual and what the moneys will be spent on.

B) the 'type' of superannuation money held in the superannuant's account, the age of the individual and whether the money is withdrawn as a lump sum or income stream.

C) the 'type' of superannuation money held in the superannuant's account, the gender of the individual and whether the money is withdrawn as a lump sum or income stream.

D) none of the above are relevant.

B

4

Reverse mortgages:

A) may be suitable for older people with a large amount of borrowings on their family home but with little disposable income.

B) may be suitable for older people with a large amount of equity in their family home but with little disposable income.

C) may be suitable for older people with a large amount of equity in their family home and surplus disposable income.

D) none of the above.

A) may be suitable for older people with a large amount of borrowings on their family home but with little disposable income.

B) may be suitable for older people with a large amount of equity in their family home but with little disposable income.

C) may be suitable for older people with a large amount of equity in their family home and surplus disposable income.

D) none of the above.

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

5

In general, for a lump sum withdrawal of untaxed superannuation money:

A) taxes will be greater than that for taxed superannuation money.

B) taxes will be lower than that for taxed superannuation money.

C) taxes will be the same as that for taxed superannuation money.

D) either b or c

A) taxes will be greater than that for taxed superannuation money.

B) taxes will be lower than that for taxed superannuation money.

C) taxes will be the same as that for taxed superannuation money.

D) either b or c

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

6

The deductible amount of a life expectancy income stream purchased for $1 million will:

A) increase with the greater relative age of the purchaser at commencement.

B) decrease with the greater relative age of the purchaser at commencement.

C) increase each year with the increasing age of the purchaser.

D) decrease each year with the increasing age of the purchaser.

A) increase with the greater relative age of the purchaser at commencement.

B) decrease with the greater relative age of the purchaser at commencement.

C) increase each year with the increasing age of the purchaser.

D) decrease each year with the increasing age of the purchaser.

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

7

The main difference between transition to retirement income streams (TTR) and account-based pensions relate to:

A) a lower maximum annual income drawdown for TTRs.

B) a lower minimum annual income drawdown for TTRs.

C) the capital balance of TTRs cannot be commuted until the superannuant reaches preservation age.

D) both a and c

A) a lower maximum annual income drawdown for TTRs.

B) a lower minimum annual income drawdown for TTRs.

C) the capital balance of TTRs cannot be commuted until the superannuant reaches preservation age.

D) both a and c

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

8

Conditions of release include where the individual has:

A) died.

B) reached the age of 65.

C) become temporarily incapacitated.

D) both a and b

A) died.

B) reached the age of 65.

C) become temporarily incapacitated.

D) both a and b

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

9

As a result of divorce or separation, splitting of superannuation money:

A) is relatively straightforward for accumulation style superannuation accounts and can happen immediately.

B) may result in a payment split for defined benefit style superannuation accounts where the funds remain in the defined benefit account until retirement.

C) both a and b

D) can only occur for accumulated superannuation balances exceeding $250,000.

A) is relatively straightforward for accumulation style superannuation accounts and can happen immediately.

B) may result in a payment split for defined benefit style superannuation accounts where the funds remain in the defined benefit account until retirement.

C) both a and b

D) can only occur for accumulated superannuation balances exceeding $250,000.

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

10

For non-account based lifetime income streams with no guarantee period:

A) commutations are generally not possible.

B) longevity risk is borne by the individual.

C) any capital amount is forfeited upon death.

D) both a and c

A) commutations are generally not possible.

B) longevity risk is borne by the individual.

C) any capital amount is forfeited upon death.

D) both a and c

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

11

A lower relative inflation rate for a given real rate results in:

A) a lower nominal rate of return.

B) a higher nominal rate of return.

C) no change in the nominal rate of return.

D) none of the above.

A) a lower nominal rate of return.

B) a higher nominal rate of return.

C) no change in the nominal rate of return.

D) none of the above.

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

12

Nadia Seffener, aged 57, immediately withdrew $250,000 from a taxed superannuation fund upon her retirement in May 2014. Nadia's accumulated superannuation balance on retirement has a tax-free component of 30%. Ignoring the Medicare levy, advise Nadia how much tax will be payable.

A) $37,500

B) $11,250

C) $26,250

D) Nil

A) $37,500

B) $11,250

C) $26,250

D) Nil

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

13

In Australia, life expectancy tables published in the last 100 years have shown a:

A) significant rise in average life expectancies.

B) significant fall in average life expectancies.

C) survivorship bias.

D) both a and c

A) significant rise in average life expectancies.

B) significant fall in average life expectancies.

C) survivorship bias.

D) both a and c

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

14

The tax consequences of leaving a superannuation lump sum death benefit to a beneficiary will be if the:

A) beneficiary is a dependant; any lump sum will be tax-free.

B) beneficiary is a non-dependant; any lump sum will be divided into a tax-free and a taxable component.

C) taxable component contains taxed superannuation money, this will be taxed at 30%.

D) both a and b

A) beneficiary is a dependant; any lump sum will be tax-free.

B) beneficiary is a non-dependant; any lump sum will be divided into a tax-free and a taxable component.

C) taxable component contains taxed superannuation money, this will be taxed at 30%.

D) both a and b

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

15

Sally Sheltern, 54 years of age, commenced receiving a reversionary lifetime pension following the recent sudden death of her partner, Harry, 59 years of age, in July 2014. The pension payments were allocated into the following components; tax-free allocation of 30%, taxable (taxed) allocation of 50% and taxable (untaxed) allocation of 20%. For the 2015 year Sally received a total of $95,000 in pension payments from the reversionary income stream. Sally has a marginal tax of 32.5%. Ignoring the Medicare levy, the net tax payable by Sally on the pension payments will be:

A) $0.

B) $30,875.

C) $24,605.

D) $17,480.

A) $0.

B) $30,875.

C) $24,605.

D) $17,480.

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

16

The more aggressive an investment strategy:

A) the higher the expected nominal rate of return.

B) the lower the expected nominal rate of return.

C) the higher the expected inflation rate.

D) none of the above.

A) the higher the expected nominal rate of return.

B) the lower the expected nominal rate of return.

C) the higher the expected inflation rate.

D) none of the above.

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

17

For death benefit termination payments (DBTP):

A) the tax payable depends on who is the recipient of the DBTP and tax will not be payable by the deceased's estate if distributed to a beneficiary.

B) tax will be payable by the deceased's estate regardless whether the DBTP is distributed to a beneficiary.

C) the payment may include both a tax-free and taxable component.

D) both a and c

A) the tax payable depends on who is the recipient of the DBTP and tax will not be payable by the deceased's estate if distributed to a beneficiary.

B) tax will be payable by the deceased's estate regardless whether the DBTP is distributed to a beneficiary.

C) the payment may include both a tax-free and taxable component.

D) both a and c

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

18

Retirement planning includes consideration of:

A) trade-offs between what is desirable and what is achievable.

B) lifestyle issues.

C) investment strategies.

D) all of the above.

A) trade-offs between what is desirable and what is achievable.

B) lifestyle issues.

C) investment strategies.

D) all of the above.

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

19

Max Colbey, 58 years of age, retired on 1 August 2014 with $500,000 accumulated in his superannuation account from which he will commence an account based income stream. The superannuation administrators have advised that his superannuation balance consists of a tax-free component of 36% with the remainder comprising a taxable (untaxed) component. In the 2015 year Max received a total of $70,000 in payments from the income stream. Max has a marginal tax of 37%. Ignoring the Medicare levy, the net tax payable by Max on the income stream will be:

A) $25,900.

B) $159,100.

C) $16,576.

D) $9,324.

A) $25,900.

B) $159,100.

C) $16,576.

D) $9,324.

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

20

In Australia the market for long-term annuities purchased from life insurance companies to fund the public's retirement needs:

A) is relatively small compared to other forms of annuities.

B) is currently serviced by a large number of life companies.

C) includes lifetime annuities.

D) both a and c

A) is relatively small compared to other forms of annuities.

B) is currently serviced by a large number of life companies.

C) includes lifetime annuities.

D) both a and c

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

21

The issue of longevity risk has been identified as an increasing problem in more recent times, particularly in a relatively low-inflationary environment. Comment on this statement.

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

22

Discuss how the factor of self-esteem can sometimes be a difficult issue for retirees to adequately deal with.

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

23

Mr Jobe Laney has recently invested part of his retirement funds, an amount of $65,000 into a term deposit with the Wakpac Credit Union at an interest rate of 6% with interest compounding annually and all funds returned at maturity. If inflation was forecast to be 3% in year 1 and 4% in year 2, using a method that calculates a real rate of return each year, calculate the real amount (in dollars) that Jobe would have on maturity and the overall real rate of return on the investment.

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

24

What is the relevance of a deductible amount to income stream payments in retirement?

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

25

Briefly discuss some of the principal decisions that a person needs to make in relation to the use of their accumulated retirement funds.

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

26

Briefly discuss why a superannuation fund member's benefit balance is subject to the preservation rules.

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

27

Why is it important when modelling retirement income streams to consider survivor bias?

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

28

Jacinta Bailey, 57 years of age, has $330,000 in superannuation money (tax-free amount of $148,500 with the remainder being a taxable [taxed] amount) that she has taken to an income-stream provider who has offered her a payment of $37,000 annually in arrears for the next 15 years with no residual value at this time. Given that Jacinta is on a 32.5% marginal tax rate, calculate how much tax Jacinta is likely to pay each year on the $37,000 annual income-stream until the time she turns 60 and the amount of tax payable thereafter?

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

29

David Sweet, 56 years of age, has recently visited your office for advice regarding undertaking a recontribution strategy with his accumulated superannuation retirement funds of $650,000 (allocated as 25% tax-free component and 75% taxable component). Given that he has satisfied a condition of release but is on the highest individual marginal tax rate, he is seeking your assistance for the 2014 financial year to maximise a lump-sum withdrawal from his accumulated retirement funds that will not be taxable and then recontributing this amount as a non-concessional superannuation contribution. Outline how assistance could be provided to David in order to meet his objective and state the percentages forming the tax-free and taxable components of his accumulated superannuation retirement funds of $650,000 after the process has been undertaken. Briefly comment on this outcome.

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

30

Ms Ayumi Sapporo recently retired from her position as head chef of the Red Blossom Japanese restaurant on 12 June 2014. She retired a few weeks before her 60th birthday (on the 30th June 2014) to give herself time to organise a large birthday party for which she is expecting guests to arrive from Japan to celebrate with her. Ayumi is wanting to use her retirement funds to provide money to pay for the party as well as to pay-out her home mortgage as well as a car loan and credit card debts that she struggled to meet whilst she was working. In total Ayumi is seeking to withdraw $450,000 on the 29th June 2014 as a lump sum from her accumulated retirement funds in order to provide for these financial commitments. Ayumi has been provided a statement from the ACME Superannuation Fund calculated to the 29th June 2014 showing an accumulated retirement funds balance of $850,000 allocated as follows:

Whilst catching a bus home from the market on the 27th June 2014 where she was starting to buy her supplies for her birthday party, Ayumi heard some people on the bus say that a financial adviser that they had recently had an appointment with had stated that where possible retirees should look to withdraw their retirement funds after they turn age 60 and not before.

Calculate the tax payable by Ayumi if she proceeds with the information given in the question and withdraws $450,000 on the 29th June 2014 from the ACME Superannuation Fund and the alternative advice she overheard on the bus that recommended leaving the withdrawal of the designated retirement funds until at least the 30th June 2014. Briefly comment on the calculated outcomes. Note: Assume that the total balance of Ayumi's retirement funds of $850,000 and the allocations previously provided do not change.

Whilst catching a bus home from the market on the 27th June 2014 where she was starting to buy her supplies for her birthday party, Ayumi heard some people on the bus say that a financial adviser that they had recently had an appointment with had stated that where possible retirees should look to withdraw their retirement funds after they turn age 60 and not before.Calculate the tax payable by Ayumi if she proceeds with the information given in the question and withdraws $450,000 on the 29th June 2014 from the ACME Superannuation Fund and the alternative advice she overheard on the bus that recommended leaving the withdrawal of the designated retirement funds until at least the 30th June 2014. Briefly comment on the calculated outcomes. Note: Assume that the total balance of Ayumi's retirement funds of $850,000 and the allocations previously provided do not change.

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 30 flashcards in this deck.