Deck 11: Flexible Budgets and Overhead Analysis

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

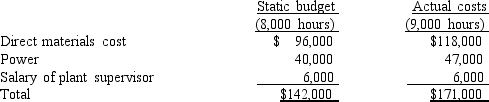

Refer to Figure 11-2. Comparing the static budget to the actual costs, we can conclude that

A) the manager spent more than should have been spent.

B) immediate action is needed to reduce costs.

C) the plant manager was clearly not efficient.

D) the plant manager should be dismissed.

E) None of these.

Question

Question

Question

Question

Question

Question

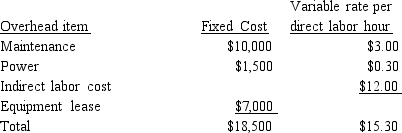

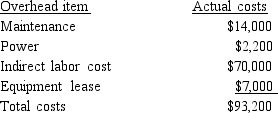

Montgomery normally produces 15,000 units (each unit requires 0.30 direct labor hours); however this year 19,000 units were produced with the following actual costs:

Montgomery normally produces 15,000 units (each unit requires 0.30 direct labor hours); however this year 19,000 units were produced with the following actual costs:

Refer to Figure 11-3. Calculate the after-the-fact budget for the actual level of activity.

A) $91,600

B) $115,000

C) $118,600

D) $77,400

E) None of these.

Question

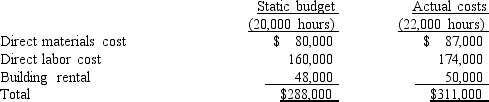

Refer to Figure 11-1. What is the flexible budget variance for the first quarter?

A) $1,000 U

B) $23,000 U

C) $23,000 F

D) $1,000 F

E) None of these.

Question

Question

Refer to Figure 11-2. What is the flexible budget for July?

A) $142,000

B) $159,000

C) $171,000

D) $165,000

E) None of these.

Question

Refer to Figure 11-1. Comparing the static budget to the actual outcomes, we can say the following:

A) the manager had more direct labor hours.

B) the variances are all unfavorable.

C) the comparison is not useful for assessing managerial efficiency.

D) a flexible budget should be used for assessing efficiency.

E) All of these.

Question

Question

Montgomery normally produces 15,000 units (each unit requires 0.30 direct labor hours); however this year 19,000 units were produced with the following actual costs:Refer to Figure 11-3. Prepare an overhead budget for the expected activity level of 10,000 units. The total budgeted overhead is

A) $139,400.

B) $64,400.

C) $124,000.

D) $12,400.

E) None of these.

Question

Question

Question

Refer to Figure 11-2. What is the flexible budget variance for July?

A) $12,000 U

B) $12,000 F

C) $29,000 U

D) $29,000 F

E) None of these.

Question

Refer to Figure 11-1. What is the flexible budget amount for the first quarter?

A) $288,000

B) $311,000

C) $312,000

D) $261,000

E) Cannot be determined.

Question

Question

Montgomery normally produces 15,000 units (each unit requires 0.30 direct labor hours); however this year 19,000 units were produced with the following actual costs:Refer to Figure 11-3. Calculate the variance for maintenance using an after-the-fact flexible budget.

A) $13,000 U

B) $13,100 F

C) $11,000 U

D) $1,000 F

E) None of these.

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/172

Play

Full screen (f)

Deck 11: Flexible Budgets and Overhead Analysis

1

Activity-based budgeting builds a budget for each activity based on the resources needed to provide the required activity output levels.

True

2

An activity-based budgetary approach can be used to emphasize cost reduction and process management.

True

3

Before-the-fact flexible budgets give expected outcomes for a range of activity levels.

True

4

Static budgets are the best benchmarks for preparing a performance report.

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

5

The fixed overhead spending variance is affected primarily by changes in production levels.

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

6

Responsibility for variable overhead spending and efficiency variances is generally assigned to production departments.

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

7

Activity-based budgeting focuses on estimating the costs of activities rather than the costs of departments and plants.

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

8

A static budget is a budget for a particular level of activity.

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

9

Although general responsibility for the volume variance is usually assigned to the purchasing department, responsibility on occasion may be assigned to the production department.

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

10

Activity flexible budgeting is the prediction of what activity costs will be as related output changes.

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

11

The volume variance is often interpreted as a measure of capacity utilization.

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

12

Activity-based budgeting supports continuous improvement and process management.

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

13

The variable overhead spending variance is conceptually identical to the price variances of materials and labor.

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

14

A static budget compares actual cost with budgeted costs.

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

15

The variable overhead variance is affected by input price changes only.

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

16

When overhead is applied on the basis of direct labor hours, the variable overhead efficiency variance always has the same sign as the labor efficiency variance.

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

17

Practical capacity is always used to calculate fixed overhead rates

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

18

An after-the-fact flexible budget allows managers to generate financial results from a number of potential scenarios.

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

19

Price changes of variable overhead items are easily controlled by production supervisors.

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

20

Fixed overhead costs are resources acquired as used and needed.

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

21

For a static activity budget in a company already using an ABC or ABM system, the activities within the organization must be identified.

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

22

Match the following terms with the items below:

a.(Actual hours Standard hours)SVOR

b.Prediction of what activity costs will be as activity output changes

c.A measure of capacity utilization

d.Actual variable overhead (SVOR Actual hours)

e.Difference between the actual amount and the flexible budget amount

f.A budget that specifies costs for a range of activity

g.A budget for a particular level of activity

h.Estimating activity output and then assessing the cost of resources to produce this output

i.A report that compares actual with planned costs

j.Difference between actual and budgeted fixed overhead

A _____________________ compares actual costs with budgeted costs.

a.(Actual hours Standard hours)SVOR

b.Prediction of what activity costs will be as activity output changes

c.A measure of capacity utilization

d.Actual variable overhead (SVOR Actual hours)

e.Difference between the actual amount and the flexible budget amount

f.A budget that specifies costs for a range of activity

g.A budget for a particular level of activity

h.Estimating activity output and then assessing the cost of resources to produce this output

i.A report that compares actual with planned costs

j.Difference between actual and budgeted fixed overhead

A _____________________ compares actual costs with budgeted costs.

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

23

Match the following terms with the items below:

-Performance report

A)(Actual hours - Standard hours)SVOR

B)Prediction of what activity costs will be as activity output changes

C)A measure of capacity utilization

D)Actual variable overhead - (SVOR * Actual hours)

E)Difference between the actual amount and the flexible budget amount

F)A budget that specifies costs for a range of activity

G)A budget for a particular level of activity

H)Estimating activity output and then assessing the cost of resources to produce this output

I)A report that compares actual with planned costs

J)Difference between actual and budgeted fixed overhead

-Performance report

A)(Actual hours - Standard hours)SVOR

B)Prediction of what activity costs will be as activity output changes

C)A measure of capacity utilization

D)Actual variable overhead - (SVOR * Actual hours)

E)Difference between the actual amount and the flexible budget amount

F)A budget that specifies costs for a range of activity

G)A budget for a particular level of activity

H)Estimating activity output and then assessing the cost of resources to produce this output

I)A report that compares actual with planned costs

J)Difference between actual and budgeted fixed overhead

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

24

Match the following terms with the items below:

-Fixed overhead volume variance

A)(Actual hours - Standard hours)SVOR

B)Prediction of what activity costs will be as activity output changes

C)A measure of capacity utilization

D)Actual variable overhead - (SVOR * Actual hours)

E)Difference between the actual amount and the flexible budget amount

F)A budget that specifies costs for a range of activity

G)A budget for a particular level of activity

H)Estimating activity output and then assessing the cost of resources to produce this output

I)A report that compares actual with planned costs

J)Difference between actual and budgeted fixed overhead

-Fixed overhead volume variance

A)(Actual hours - Standard hours)SVOR

B)Prediction of what activity costs will be as activity output changes

C)A measure of capacity utilization

D)Actual variable overhead - (SVOR * Actual hours)

E)Difference between the actual amount and the flexible budget amount

F)A budget that specifies costs for a range of activity

G)A budget for a particular level of activity

H)Estimating activity output and then assessing the cost of resources to produce this output

I)A report that compares actual with planned costs

J)Difference between actual and budgeted fixed overhead

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

25

Match the following terms with the items below:

-Static budget

A)(Actual hours - Standard hours)SVOR

B)Prediction of what activity costs will be as activity output changes

C)A measure of capacity utilization

D)Actual variable overhead - (SVOR * Actual hours)

E)Difference between the actual amount and the flexible budget amount

F)A budget that specifies costs for a range of activity

G)A budget for a particular level of activity

H)Estimating activity output and then assessing the cost of resources to produce this output

I)A report that compares actual with planned costs

J)Difference between actual and budgeted fixed overhead

-Static budget

A)(Actual hours - Standard hours)SVOR

B)Prediction of what activity costs will be as activity output changes

C)A measure of capacity utilization

D)Actual variable overhead - (SVOR * Actual hours)

E)Difference between the actual amount and the flexible budget amount

F)A budget that specifies costs for a range of activity

G)A budget for a particular level of activity

H)Estimating activity output and then assessing the cost of resources to produce this output

I)A report that compares actual with planned costs

J)Difference between actual and budgeted fixed overhead

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

26

A _______________ is a budget created in advance that is based on a particular level of activity.

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

27

Match the following terms with the items below:

-Flexible budget

A)(Actual hours - Standard hours)SVOR

B)Prediction of what activity costs will be as activity output changes

C)A measure of capacity utilization

D)Actual variable overhead -(SVOR * Actual hours)

E)Difference between the actual amount and the flexible budget amount

F)A budget that specifies costs for a range of activity

G)A budget for a particular level of activity

H)Estimating activity output and then assessing the cost of resources to produce this output

I)A report that compares actual with planned costs

J)Difference between actual and budgeted fixed overhead

-Flexible budget

A)(Actual hours - Standard hours)SVOR

B)Prediction of what activity costs will be as activity output changes

C)A measure of capacity utilization

D)Actual variable overhead -(SVOR * Actual hours)

E)Difference between the actual amount and the flexible budget amount

F)A budget that specifies costs for a range of activity

G)A budget for a particular level of activity

H)Estimating activity output and then assessing the cost of resources to produce this output

I)A report that compares actual with planned costs

J)Difference between actual and budgeted fixed overhead

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

28

An activity-based budgeting system may help support continuous improvement and process management.

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

29

Because activities are what consume resources, activity-based budgeting may prove to be a much more powerful planning and control tool than the traditional approach.

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

30

In an activity framework, controlling costs is equivalent to managing activities.

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

31

Activity-based budgeting classifies costs as variable or fixed with respect to the activity output measure.

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

32

Match the following terms with the items below:

-Fixed overhead spending variance

A)(Actual hours - Standard hours)SVOR

B)Prediction of what activity costs will be as activity output changes

C)A measure of capacity utilization

D)Actual variable overhead - (SVOR *Actual hours)

E)Difference between the actual amount and the flexible budget amount

F)A budget that specifies costs for a range of activity

G)A budget for a particular level of activity

H)Estimating activity output and then assessing the cost of resources to produce this output

I)A report that compares actual with planned costs

J)Difference between actual and budgeted fixed overhead

-Fixed overhead spending variance

A)(Actual hours - Standard hours)SVOR

B)Prediction of what activity costs will be as activity output changes

C)A measure of capacity utilization

D)Actual variable overhead - (SVOR *Actual hours)

E)Difference between the actual amount and the flexible budget amount

F)A budget that specifies costs for a range of activity

G)A budget for a particular level of activity

H)Estimating activity output and then assessing the cost of resources to produce this output

I)A report that compares actual with planned costs

J)Difference between actual and budgeted fixed overhead

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

33

Activity flexible budgeting is the prediction of what activity costs will be as production output changes.

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

34

The first step of building an activity-based budget is to identify the activities within an organization.

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

35

Match the following terms with the items below:

-Variable overhead efficiency variance

A)(Actual hours - Standard hours)SVOR

B)Prediction of what activity costs will be as activity output changes

C)A measure of capacity utilization

D)Actual variable overhead - (SVOR * Actual hours)

E)Difference between the actual amount and the flexible budget amount

F)A budget that specifies costs for a range of activity

G)A budget for a particular level of activity

H)Estimating activity output and then assessing the cost of resources to produce this output

I)A report that compares actual with planned costs

J)Difference between actual and budgeted fixed overhead

-Variable overhead efficiency variance

A)(Actual hours - Standard hours)SVOR

B)Prediction of what activity costs will be as activity output changes

C)A measure of capacity utilization

D)Actual variable overhead - (SVOR * Actual hours)

E)Difference between the actual amount and the flexible budget amount

F)A budget that specifies costs for a range of activity

G)A budget for a particular level of activity

H)Estimating activity output and then assessing the cost of resources to produce this output

I)A report that compares actual with planned costs

J)Difference between actual and budgeted fixed overhead

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

36

Match the following terms with the items below:

-Activity-based budgeting

A)(Actual hours - Standard hours)SVOR

B)Prediction of what activity costs will be as activity output changes

C)A measure of capacity utilization

D)Actual variable overhead - (SVOR * Actual hours)

E)Difference between the actual amount and the flexible budget amount

F)A budget that specifies costs for a range of activity

G)A budget for a particular level of activity

H)Estimating activity output and then assessing the cost of resources to produce this output

I)A report that compares actual with planned costs

J)Difference between actual and budgeted fixed overhead

-Activity-based budgeting

A)(Actual hours - Standard hours)SVOR

B)Prediction of what activity costs will be as activity output changes

C)A measure of capacity utilization

D)Actual variable overhead - (SVOR * Actual hours)

E)Difference between the actual amount and the flexible budget amount

F)A budget that specifies costs for a range of activity

G)A budget for a particular level of activity

H)Estimating activity output and then assessing the cost of resources to produce this output

I)A report that compares actual with planned costs

J)Difference between actual and budgeted fixed overhead

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

37

An activity-based budgetary approach can be used to emphasize cost increases through the reduction of wasteful activities and improving the efficiency of necessary activities.

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

38

Match the following terms with the items below:

-Variable overhead spending variance

A)(Actual hours - Standard hours)SVOR

B)Prediction of what activity costs will be as activity output changes

C)A measure of capacity utilization

D)Actual variable overhead - (SVOR * Actual hours)

E)Difference between the actual amount and the flexible budget amount

F)A budget that specifies costs for a range of activity

G)A budget for a particular level of activity

H)Estimating activity output and then assessing the cost of resources to produce this output

I)A report that compares actual with planned costs

J)Difference between actual and budgeted fixed overhead

-Variable overhead spending variance

A)(Actual hours - Standard hours)SVOR

B)Prediction of what activity costs will be as activity output changes

C)A measure of capacity utilization

D)Actual variable overhead - (SVOR * Actual hours)

E)Difference between the actual amount and the flexible budget amount

F)A budget that specifies costs for a range of activity

G)A budget for a particular level of activity

H)Estimating activity output and then assessing the cost of resources to produce this output

I)A report that compares actual with planned costs

J)Difference between actual and budgeted fixed overhead

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

39

Match the following terms with the items below:

-Activity flexible budget

A)(Actual hours - Standard hours)SVOR

B)Prediction of what activity costs will be as activity output changes

C)A measure of capacity utilization

D)Actual variable overhead -(SVOR * Actual hours)

E)Difference between the actual amount and the flexible budget amount

F)A budget that specifies costs for a range of activity

G)A budget for a particular level of activity

H)Estimating activity output and then assessing the cost of resources to produce this output

I)A report that compares actual with planned costs

J)Difference between actual and budgeted fixed overhead

-Activity flexible budget

A)(Actual hours - Standard hours)SVOR

B)Prediction of what activity costs will be as activity output changes

C)A measure of capacity utilization

D)Actual variable overhead -(SVOR * Actual hours)

E)Difference between the actual amount and the flexible budget amount

F)A budget that specifies costs for a range of activity

G)A budget for a particular level of activity

H)Estimating activity output and then assessing the cost of resources to produce this output

I)A report that compares actual with planned costs

J)Difference between actual and budgeted fixed overhead

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

40

Match the following terms with the items below:

-Flexible budget variance

A)(Actual hours - Standard hours)SVOR

B)Prediction of what activity costs will be as activity output changes

C)A measure of capacity utilization

D)Actual variable overhead - (SVOR * Actual hours)

E)Difference between the actual amount and the flexible budget amount

F)A budget that specifies costs for a range of activity

G)A budget for a particular level of activity

H)Estimating activity output and then assessing the cost of resources to produce this output

I)A report that compares actual with planned costs

J)Difference between actual and budgeted fixed overhead

-Flexible budget variance

A)(Actual hours - Standard hours)SVOR

B)Prediction of what activity costs will be as activity output changes

C)A measure of capacity utilization

D)Actual variable overhead - (SVOR * Actual hours)

E)Difference between the actual amount and the flexible budget amount

F)A budget that specifies costs for a range of activity

G)A budget for a particular level of activity

H)Estimating activity output and then assessing the cost of resources to produce this output

I)A report that compares actual with planned costs

J)Difference between actual and budgeted fixed overhead

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

41

The ________________________ measures the change in the actual variable overhead cost that occurs because of efficient (or inefficient) use of direct labor

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

42

The variable overhead efficiency variance is directly related to the __________________ or usage variance.

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

43

Budgeted costs change because total variable costs go up as output increases, therefore flexible budgets are sometimes referred to as _______________.

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

44

Activity-based budgeting begins with the _____________ and _______________ budgets.

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

45

A difference between the actual amount and the flexible budget amount is known as the ____________________.

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

46

The _________________________ focuses on the estimation of the costs of activities rather than the costs of departments and plants.

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

47

_______________________ is the difference between the actual variable overhead and applied variable overhead.

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

48

A _________________ enables a firm to compute expected costs for a range of activity levels.

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

49

The ______________________ is the difference between the actual fixed overhead and the budgeted fixed overhead.

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

50

The _____________________ measures the aggregate effect of differences between the actual variable overhead rate and the standard variable overhead rate.

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

51

______________________ is a prerequisite for assigning responsibility.

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

52

The ________________ budget is based on the actual level of activity.

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

53

A static budget is

A) considered a good choice for benchmarks in preparing a performance report.

B) computes expected costs for a range of activity levels.

C) compares actual costs with budgeted costs.

D) prepared for a particular level of activity.

E) None of these are correct.

A) considered a good choice for benchmarks in preparing a performance report.

B) computes expected costs for a range of activity levels.

C) compares actual costs with budgeted costs.

D) prepared for a particular level of activity.

E) None of these are correct.

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

54

The ____________________ budget gives expected outcomes for a range of activity levels.

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

55

Which budget should be used to determine managerial effectiveness?

A) before-the-fact flexible budget

B) after-the-fact flexible budget

C) static budget

D) financial budget

E) cash budget

A) before-the-fact flexible budget

B) after-the-fact flexible budget

C) static budget

D) financial budget

E) cash budget

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

56

_______________________ is the prediction of what activity costs will be as related output changes.

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

57

The ____________________ is the difference between budgeted fixed overhead and applied fixed overhead.

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

58

Often, the flexible budget formulas are based on ________________ instead of units.

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

59

The _____________________ is the difference between actual fixed overhead and applied fixed overhead.

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

60

_________________ are capacity costs acquired in advance of usage.

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

61

Refer to Figure 11-2. Comparing the static budget to the actual costs, we can conclude that

A) the manager spent more than should have been spent.

B) immediate action is needed to reduce costs.

C) the plant manager was clearly not efficient.

D) the plant manager should be dismissed.

E) None of these.

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

62

Which budget is used to assess managerial efficiency?

A) sales budget

B) production budget

C) static budget

D) flexible budget

E) cash budget

A) sales budget

B) production budget

C) static budget

D) flexible budget

E) cash budget

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

63

To create a meaningful performance report,

A) actual costs are compared with the expected costs found in the static budget.

B) actual costs are calculated as a percentage of sales.

C) actual costs are compared with the prior year's actual costs.

D) expected costs of the static budget are compared with the expected costs of the flexible budget.

E) actual costs are compared with the expected costs at the same level of activity.

A) actual costs are compared with the expected costs found in the static budget.

B) actual costs are calculated as a percentage of sales.

C) actual costs are compared with the prior year's actual costs.

D) expected costs of the static budget are compared with the expected costs of the flexible budget.

E) actual costs are compared with the expected costs at the same level of activity.

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

64

The variable overhead spending variance measures the aggregate effect of differences between the

A) the total variable overhead and the applied variable overhead.

B) the total variable overhead and total budgeted overhead costs.

C) the total variable overhead and the budgeted overhead for the expected activity.

D) the actual variable overhead rate and the standard variable overhead rate.

E) None of these.

A) the total variable overhead and the applied variable overhead.

B) the total variable overhead and total budgeted overhead costs.

C) the total variable overhead and the budgeted overhead for the expected activity.

D) the actual variable overhead rate and the standard variable overhead rate.

E) None of these.

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

65

A budget that allows the determination of expected costs for various levels of activity is a(n)

A) operational budget.

B) sales budget.

C) production budget.

D) financial budget.

E) flexible budget.

A) operational budget.

B) sales budget.

C) production budget.

D) financial budget.

E) flexible budget.

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

66

An after-the-fact flexible budget

A) is a budget for the actual level of activity.

B) is used for performance reports.

C) calculates what costs should have been for the actual level of activity.

D) is used to compare expected costs with actual costs.

E) All of these.

A) is a budget for the actual level of activity.

B) is used for performance reports.

C) calculates what costs should have been for the actual level of activity.

D) is used to compare expected costs with actual costs.

E) All of these.

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

67

Montgomery normally produces 15,000 units (each unit requires 0.30 direct labor hours); however this year 19,000 units were produced with the following actual costs:Refer to Figure 11-3. Calculate the after-the-fact budget for the actual level of activity.

A) $91,600

B) $115,000

C) $118,600

D) $77,400

E) None of these.

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

68

Refer to Figure 11-1. What is the flexible budget variance for the first quarter?

A) $1,000 U

B) $23,000 U

C) $23,000 F

D) $1,000 F

E) None of these.

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

69

A budget prepared for a particular level of activity is a(n)

A) operational budget.

B) ABB budget.

C) static budget.

D) flexible budget.

E) variable budget.

A) operational budget.

B) ABB budget.

C) static budget.

D) flexible budget.

E) variable budget.

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

70

Refer to Figure 11-2. What is the flexible budget for July?

A) $142,000

B) $159,000

C) $171,000

D) $165,000

E) None of these.

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

71

Refer to Figure 11-1. Comparing the static budget to the actual outcomes, we can say the following:

A) the manager had more direct labor hours.

B) the variances are all unfavorable.

C) the comparison is not useful for assessing managerial efficiency.

D) a flexible budget should be used for assessing efficiency.

E) All of these.

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

72

A performance report

A) always uses static budgets.

B) compares actual costs with budgeted costs.

C) uses a static or a flexible budget.

D) both compares actual costs with budgeted costs and always uses static budget.

E) both always uses static budgets and usually uses flexible budgets.

A) always uses static budgets.

B) compares actual costs with budgeted costs.

C) uses a static or a flexible budget.

D) both compares actual costs with budgeted costs and always uses static budget.

E) both always uses static budgets and usually uses flexible budgets.

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

73

Montgomery normally produces 15,000 units (each unit requires 0.30 direct labor hours); however this year 19,000 units were produced with the following actual costs:Refer to Figure 11-3. Prepare an overhead budget for the expected activity level of 10,000 units. The total budgeted overhead is

A) $139,400.

B) $64,400.

C) $124,000.

D) $12,400.

E) None of these.

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

74

A static budget is best used to

A) measure whether or not a manager accomplishes his or her goals.

B) compare expected costs at the actual level of activity with the actual costs.

C) assess how well costs were controlled during the year.

D) determine managerial efficiency.

E) None of these.

A) measure whether or not a manager accomplishes his or her goals.

B) compare expected costs at the actual level of activity with the actual costs.

C) assess how well costs were controlled during the year.

D) determine managerial efficiency.

E) None of these.

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

75

Flexible budgets are powerful control tools because

A) they allow managers to deal with uncertainty.

B) they allow the calculation of what cost should be for the actual level of activity.

C) they allow the preparation of meaningful performance reports.

D) they help measure managerial efficiency.

E) All of these.

A) they allow managers to deal with uncertainty.

B) they allow the calculation of what cost should be for the actual level of activity.

C) they allow the preparation of meaningful performance reports.

D) they help measure managerial efficiency.

E) All of these.

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

76

Refer to Figure 11-2. What is the flexible budget variance for July?

A) $12,000 U

B) $12,000 F

C) $29,000 U

D) $29,000 F

E) None of these.

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

77

Refer to Figure 11-1. What is the flexible budget amount for the first quarter?

A) $288,000

B) $311,000

C) $312,000

D) $261,000

E) Cannot be determined.

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

78

A before-the-fact flexible budget

A) calculates expected costs for various levels of activity.

B) allows managers to deal with uncertainty.

C) can be used to generate results for a number of plausible scenarios.

D) is a useful planning tool.

E) All of these.

A) calculates expected costs for various levels of activity.

B) allows managers to deal with uncertainty.

C) can be used to generate results for a number of plausible scenarios.

D) is a useful planning tool.

E) All of these.

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

79

Montgomery normally produces 15,000 units (each unit requires 0.30 direct labor hours); however this year 19,000 units were produced with the following actual costs:Refer to Figure 11-3. Calculate the variance for maintenance using an after-the-fact flexible budget.

A) $13,000 U

B) $13,100 F

C) $11,000 U

D) $1,000 F

E) None of these.

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

80

Assume that the expectations on the static budget were met. We can conclude that

A) the static budget was ill conceived.

B) the effectiveness of the manager is not in question.

C) the manager is very efficient.

D) there is no need for a flexible budget.

E) None of these.

A) the static budget was ill conceived.

B) the effectiveness of the manager is not in question.

C) the manager is very efficient.

D) there is no need for a flexible budget.

E) None of these.

Unlock Deck

Unlock for access to all 172 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 172 flashcards in this deck.