Deck 12: Differential Analysis: The Key to Decision Making

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

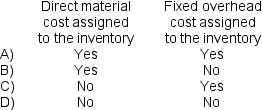

Which of the following would be relevant in the decision to sell or throw out obsolete inventory?

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Munafo Corporation is a specialty component manufacturer with idle capacity.Management would like to use its extra capacity to generate additional profits.A potential customer has offered to buy 6,500 units of component VGI.Each unit of VGI requires 1 unit of material I57 and 5 units of material M97.Data concerning these two materials follow:

Material I57 is in use in many of the company's products and is routinely replenished.Material M97 is no longer used by the company in any of its normal products and existing stocks would not be replenished once they are used up.

Material I57 is in use in many of the company's products and is routinely replenished.Material M97 is no longer used by the company in any of its normal products and existing stocks would not be replenished once they are used up.

What would be the relevant cost of the materials,in total,for purposes of determining a minimum acceptable price for the order for product VGI?

A) $174,850

B) $213,130

C) $213,850

D) $171,925

Material I57 is in use in many of the company's products and is routinely replenished.Material M97 is no longer used by the company in any of its normal products and existing stocks would not be replenished once they are used up.What would be the relevant cost of the materials,in total,for purposes of determining a minimum acceptable price for the order for product VGI?

A) $174,850

B) $213,130

C) $213,850

D) $171,925

Question

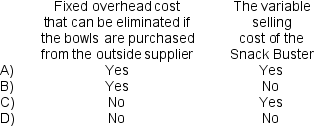

The Jabba Corporation manufactures the "Snack Buster" which consists of a wooden snack chip bowl with an attached porcelain dip bowl.Which of the following would be relevant in Jabba's decision to make the dip bowls or buy them from an outside supplier?

Question

Question

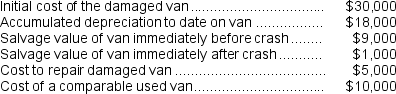

One of the employees of Davenport Corporation recently was involved in an accident with one of the corporation's delivery vans.The corporation is either going to repair the damaged van or sell it as is and buy a comparable used van.Information related to this decision is provided below:

Based on the information above,Davenport would be financially better off:

Based on the information above,Davenport would be financially better off:

A) $1,000 by buying the comparable van.

B) $2,000 by buying the comparable van.

C) $2,000 by repairing the damaged van.

D) $4,000 by repairing the damaged van.

Based on the information above,Davenport would be financially better off:A) $1,000 by buying the comparable van.

B) $2,000 by buying the comparable van.

C) $2,000 by repairing the damaged van.

D) $4,000 by repairing the damaged van.

Question

Question

Question

Question

Question

Question

Question

Question

Winder Corporation is a specialty component manufacturer with idle capacity.Management would like to use its extra capacity to generate additional profits.A potential customer has offered to buy 3,000 units of component QEA.Each unit of QEA requires 5 units of material F85 and 5 units of material E71.Data concerning these two materials follow:

Material F85 is in use in many of the company's products and is routinely replenished.Material E71 is no longer used by the company in any of its normal products and existing stocks would not be replenished once they are used up.

Material F85 is in use in many of the company's products and is routinely replenished.Material E71 is no longer used by the company in any of its normal products and existing stocks would not be replenished once they are used up.

What would be the relevant cost of the materials,in total,for purposes of determining a minimum acceptable price for the order for product QEA?

A) $126,702

B) $141,750

C) $126,295

D) $145,965

Material F85 is in use in many of the company's products and is routinely replenished.Material E71 is no longer used by the company in any of its normal products and existing stocks would not be replenished once they are used up.What would be the relevant cost of the materials,in total,for purposes of determining a minimum acceptable price for the order for product QEA?

A) $126,702

B) $141,750

C) $126,295

D) $145,965

Question

Question

Question

Question

Product U23N has been considered a drag on profits at Jinkerson Corporation for some time and management is considering discontinuing the product altogether.Data from the company's budget for the upcoming year appear below:

In the company's accounting system all fixed expenses of the company are fully allocated to products.Further investigation has revealed that $144,000 of the fixed manufacturing expenses and $93,000 of the fixed selling and administrative expenses are avoidable if product U23N is discontinued.The financial advantage (disadvantage)for the company of eliminating this product for the upcoming year would be:

In the company's accounting system all fixed expenses of the company are fully allocated to products.Further investigation has revealed that $144,000 of the fixed manufacturing expenses and $93,000 of the fixed selling and administrative expenses are avoidable if product U23N is discontinued.The financial advantage (disadvantage)for the company of eliminating this product for the upcoming year would be:

A) $15,000

B) $143,000

C) ($143,000)

D) ($15,000)

In the company's accounting system all fixed expenses of the company are fully allocated to products.Further investigation has revealed that $144,000 of the fixed manufacturing expenses and $93,000 of the fixed selling and administrative expenses are avoidable if product U23N is discontinued.The financial advantage (disadvantage)for the company of eliminating this product for the upcoming year would be:A) $15,000

B) $143,000

C) ($143,000)

D) ($15,000)

Question

Question

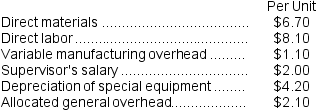

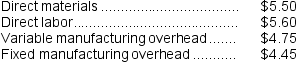

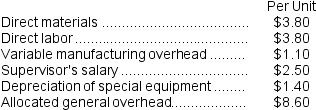

Part U16 is used by Mcvean Corporation to make one of its products.A total of 13,000 units of this part are produced and used every year.The company's Accounting Department reports the following costs of producing the part at this level of activity:

An outside supplier has offered to make the part and sell it to the company for $29.80 each.If this offer is accepted,the supervisor's salary and all of the variable costs,including the direct labor,can be avoided.The special equipment used to make the part was purchased many years ago and has no salvage value or other use.The allocated general overhead represents fixed costs of the entire company,none of which would be avoided if the part were purchased instead of produced internally.In addition,the space used to make part U16 could be used to make more of one of the company's other products,generating an additional segment margin of $25,000 per year for that product.The annual financial advantage (disadvantage)for the company as a result of buying part U16 from the outside supplier should be:

An outside supplier has offered to make the part and sell it to the company for $29.80 each.If this offer is accepted,the supervisor's salary and all of the variable costs,including the direct labor,can be avoided.The special equipment used to make the part was purchased many years ago and has no salvage value or other use.The allocated general overhead represents fixed costs of the entire company,none of which would be avoided if the part were purchased instead of produced internally.In addition,the space used to make part U16 could be used to make more of one of the company's other products,generating an additional segment margin of $25,000 per year for that product.The annual financial advantage (disadvantage)for the company as a result of buying part U16 from the outside supplier should be:

A) $25,000

B) ($79,000)

C) ($35,400)

D) $14,600

An outside supplier has offered to make the part and sell it to the company for $29.80 each.If this offer is accepted,the supervisor's salary and all of the variable costs,including the direct labor,can be avoided.The special equipment used to make the part was purchased many years ago and has no salvage value or other use.The allocated general overhead represents fixed costs of the entire company,none of which would be avoided if the part were purchased instead of produced internally.In addition,the space used to make part U16 could be used to make more of one of the company's other products,generating an additional segment margin of $25,000 per year for that product.The annual financial advantage (disadvantage)for the company as a result of buying part U16 from the outside supplier should be:A) $25,000

B) ($79,000)

C) ($35,400)

D) $14,600

Question

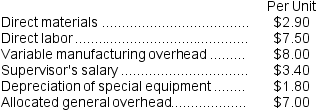

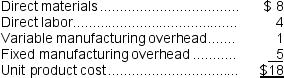

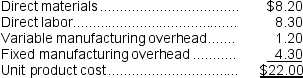

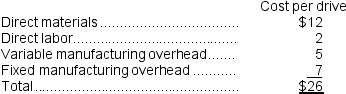

Supler Corporation produces a part used in the manufacture of one of its products.The unit product cost is $18,computed as follows:

An outside supplier has offered to provide the annual requirement of 4,000 of the parts for only $14 each.The company estimates that 60% of the fixed manufacturing overhead cost above could be eliminated if the parts are purchased from the outside supplier.Assume that direct labor is an avoidable cost in this decision.Based on these data,the financial advantage (disadvantage)of purchasing the parts from the outside supplier would be:

An outside supplier has offered to provide the annual requirement of 4,000 of the parts for only $14 each.The company estimates that 60% of the fixed manufacturing overhead cost above could be eliminated if the parts are purchased from the outside supplier.Assume that direct labor is an avoidable cost in this decision.Based on these data,the financial advantage (disadvantage)of purchasing the parts from the outside supplier would be:

A) ($1) per unit on average

B) $1 per unit on average

C) $2 per unit on average

D) ($4) per unit on average

An outside supplier has offered to provide the annual requirement of 4,000 of the parts for only $14 each.The company estimates that 60% of the fixed manufacturing overhead cost above could be eliminated if the parts are purchased from the outside supplier.Assume that direct labor is an avoidable cost in this decision.Based on these data,the financial advantage (disadvantage)of purchasing the parts from the outside supplier would be:A) ($1) per unit on average

B) $1 per unit on average

C) $2 per unit on average

D) ($4) per unit on average

Question

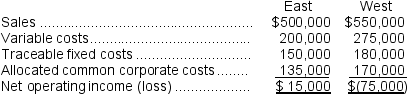

The Cook Corporation has two divisions--East and West.The divisions have the following revenues and expenses:

The management of Cook is considering the elimination of the West Division.If the West Division were eliminated,its traceable fixed costs could be avoided.Total common corporate costs would be unaffected by this decision.Given these data,the elimination of the West Division would result in an overall company net operating income (loss)of:

The management of Cook is considering the elimination of the West Division.If the West Division were eliminated,its traceable fixed costs could be avoided.Total common corporate costs would be unaffected by this decision.Given these data,the elimination of the West Division would result in an overall company net operating income (loss)of:

A) $15,000

B) $(155,000)

C) $(75,000)

D) $(60,000)

The management of Cook is considering the elimination of the West Division.If the West Division were eliminated,its traceable fixed costs could be avoided.Total common corporate costs would be unaffected by this decision.Given these data,the elimination of the West Division would result in an overall company net operating income (loss)of:A) $15,000

B) $(155,000)

C) $(75,000)

D) $(60,000)

Question

Norgaard Corporation makes 8,000 units of part G25 each year.This part is used in one of the company's products.The company's Accounting Department reports the following costs of producing the part at this level of activity:

An outside supplier has offered to make and sell the part to the company for $21.20 each.If this offer is accepted,the supervisor's salary and all of the variable costs,including direct labor,can be avoided.The special equipment used to make the part was purchased many years ago and has no salvage value or other use.The allocated general overhead represents fixed costs of the entire company.If the outside supplier's offer were accepted,only $2,000 of these allocated general overhead costs would be avoided.In addition,the space used to produce part G25 would be used to make more of one of the company's other products,generating an additional segment margin of $16,000 per year for that product.

An outside supplier has offered to make and sell the part to the company for $21.20 each.If this offer is accepted,the supervisor's salary and all of the variable costs,including direct labor,can be avoided.The special equipment used to make the part was purchased many years ago and has no salvage value or other use.The allocated general overhead represents fixed costs of the entire company.If the outside supplier's offer were accepted,only $2,000 of these allocated general overhead costs would be avoided.In addition,the space used to produce part G25 would be used to make more of one of the company's other products,generating an additional segment margin of $16,000 per year for that product.

The annual financial advantage (disadvantage)for the company as a result of buying part G25 from the outside supplier should be:

A) ($8,400)

B) $16,000

C) ($8,000)

D) ($40,000)

An outside supplier has offered to make and sell the part to the company for $21.20 each.If this offer is accepted,the supervisor's salary and all of the variable costs,including direct labor,can be avoided.The special equipment used to make the part was purchased many years ago and has no salvage value or other use.The allocated general overhead represents fixed costs of the entire company.If the outside supplier's offer were accepted,only $2,000 of these allocated general overhead costs would be avoided.In addition,the space used to produce part G25 would be used to make more of one of the company's other products,generating an additional segment margin of $16,000 per year for that product.The annual financial advantage (disadvantage)for the company as a result of buying part G25 from the outside supplier should be:

A) ($8,400)

B) $16,000

C) ($8,000)

D) ($40,000)

Question

Question

The management of Furrow Corporation is considering dropping product L07E.Data from the company's budget for the upcoming year appear below:

In the company's accounting system all fixed expenses of the company are fully allocated to products.Further investigation has revealed that $186,000 of the fixed manufacturing expenses and $106,000 of the fixed selling and administrative expenses are avoidable if product L07E is discontinued.The financial advantage (disadvantage)for the company of eliminating this product for the upcoming year would be:

In the company's accounting system all fixed expenses of the company are fully allocated to products.Further investigation has revealed that $186,000 of the fixed manufacturing expenses and $106,000 of the fixed selling and administrative expenses are avoidable if product L07E is discontinued.The financial advantage (disadvantage)for the company of eliminating this product for the upcoming year would be:

A) $8,000

B) ($173,000)

C) ($8,000)

D) $173,000

In the company's accounting system all fixed expenses of the company are fully allocated to products.Further investigation has revealed that $186,000 of the fixed manufacturing expenses and $106,000 of the fixed selling and administrative expenses are avoidable if product L07E is discontinued.The financial advantage (disadvantage)for the company of eliminating this product for the upcoming year would be:A) $8,000

B) ($173,000)

C) ($8,000)

D) $173,000

Question

The following information relates to next year's projected operating results of the Children's Division of Grunge Clothing Corporation:

If the Children's Division is eliminated,$170,000 of the above fixed expenses could be avoided.The annual financial advantage (disadvantage)for the company of eliminating this division should be:

If the Children's Division is eliminated,$170,000 of the above fixed expenses could be avoided.The annual financial advantage (disadvantage)for the company of eliminating this division should be:

A) ($300,000)

B) $30,000

C) ($30,000)

D) $300,000

If the Children's Division is eliminated,$170,000 of the above fixed expenses could be avoided.The annual financial advantage (disadvantage)for the company of eliminating this division should be:A) ($300,000)

B) $30,000

C) ($30,000)

D) $300,000

Question

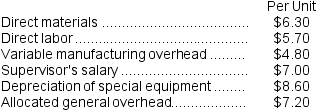

Part S51 is used in one of Haberkorn Corporation's products.The company makes 12,000 units of this part each year.The company's Accounting Department reports the following costs of producing the part at this level of activity:

An outside supplier has offered to produce this part and sell it to the company for $37.70 each.If this offer is accepted,the supervisor's salary and all of the variable costs,including direct labor,can be avoided.The special equipment used to make the part was purchased many years ago and has no salvage value or other use.The allocated general overhead represents fixed costs of the entire company.If the outside supplier's offer were accepted,only $17,000 of these allocated general overhead costs would be avoided.

An outside supplier has offered to produce this part and sell it to the company for $37.70 each.If this offer is accepted,the supervisor's salary and all of the variable costs,including direct labor,can be avoided.The special equipment used to make the part was purchased many years ago and has no salvage value or other use.The allocated general overhead represents fixed costs of the entire company.If the outside supplier's offer were accepted,only $17,000 of these allocated general overhead costs would be avoided.

The annual financial advantage (disadvantage)for the company as a result of buying the part from the outside supplier would be:

A) ($5,800)

B) ($22,800)

C) ($149,800)

D) ($39,800)

An outside supplier has offered to produce this part and sell it to the company for $37.70 each.If this offer is accepted,the supervisor's salary and all of the variable costs,including direct labor,can be avoided.The special equipment used to make the part was purchased many years ago and has no salvage value or other use.The allocated general overhead represents fixed costs of the entire company.If the outside supplier's offer were accepted,only $17,000 of these allocated general overhead costs would be avoided.The annual financial advantage (disadvantage)for the company as a result of buying the part from the outside supplier would be:

A) ($5,800)

B) ($22,800)

C) ($149,800)

D) ($39,800)

Question

The SP Corporation makes 40,000 motors to be used in the production of its sewing machines.The average cost per motor at this level of activity is:

An outside supplier recently began producing a comparable motor that could be used in the sewing machine.The price offered to SP Corporation for this motor is $18.If SP Corporation decides not to make the motors,there would be no other use for the production facilities and none of the fixed manufacturing overhead cost could be avoided.Direct labor is a variable cost in this company.The annual financial advantage (disadvantage)for the company as a result of making the motors rather than buying them from the outside supplier would be:

An outside supplier recently began producing a comparable motor that could be used in the sewing machine.The price offered to SP Corporation for this motor is $18.If SP Corporation decides not to make the motors,there would be no other use for the production facilities and none of the fixed manufacturing overhead cost could be avoided.Direct labor is a variable cost in this company.The annual financial advantage (disadvantage)for the company as a result of making the motors rather than buying them from the outside supplier would be:

A) $276,000

B) $86,000

C) ($92,000)

D) $178,000

An outside supplier recently began producing a comparable motor that could be used in the sewing machine.The price offered to SP Corporation for this motor is $18.If SP Corporation decides not to make the motors,there would be no other use for the production facilities and none of the fixed manufacturing overhead cost could be avoided.Direct labor is a variable cost in this company.The annual financial advantage (disadvantage)for the company as a result of making the motors rather than buying them from the outside supplier would be:A) $276,000

B) $86,000

C) ($92,000)

D) $178,000

Question

Sardi Inc.is considering whether to continue to make a component or to buy it from an outside supplier.The company uses 17,000 of the components each year.The unit product cost of the component according to the company's cost accounting system is given as follows:

Assume that direct labor is a variable cost.Of the fixed manufacturing overhead,70% is avoidable if the component were bought from the outside supplier.In addition,making the component uses 2 minutes on the machine that is the company's current constraint.If the component were bought,time would be freed up for use on another product that requires 4 minutes on this machine and that has a contribution margin of $7.00 per unit.

Assume that direct labor is a variable cost.Of the fixed manufacturing overhead,70% is avoidable if the component were bought from the outside supplier.In addition,making the component uses 2 minutes on the machine that is the company's current constraint.If the component were bought,time would be freed up for use on another product that requires 4 minutes on this machine and that has a contribution margin of $7.00 per unit.

When deciding whether to make or buy the component,what cost of making the component should be compared to the price of buying the component?

A) $24.21 per unit

B) $25.50 per unit

C) $20.71 per unit

D) $22.00 per unit

Assume that direct labor is a variable cost.Of the fixed manufacturing overhead,70% is avoidable if the component were bought from the outside supplier.In addition,making the component uses 2 minutes on the machine that is the company's current constraint.If the component were bought,time would be freed up for use on another product that requires 4 minutes on this machine and that has a contribution margin of $7.00 per unit.When deciding whether to make or buy the component,what cost of making the component should be compared to the price of buying the component?

A) $24.21 per unit

B) $25.50 per unit

C) $20.71 per unit

D) $22.00 per unit

Question

Question

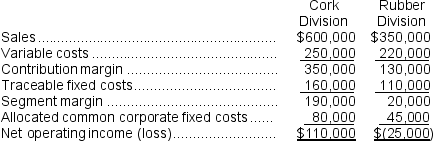

Vanik Corporation currently has two divisions which had the following operating results for last year:

Because the Rubber Division sustained a loss,the president of Vanik is considering the elimination of this division.All of the division's traceable fixed costs could be avoided if the division was dropped.None of the allocated common corporate fixed costs could be avoided.If the Rubber Division was dropped at the beginning of last year,the financial advantage (disadvantage)to the company for the year would have been:

Because the Rubber Division sustained a loss,the president of Vanik is considering the elimination of this division.All of the division's traceable fixed costs could be avoided if the division was dropped.None of the allocated common corporate fixed costs could be avoided.If the Rubber Division was dropped at the beginning of last year,the financial advantage (disadvantage)to the company for the year would have been:

A) ($20,000)

B) $20,000

C) $25,000

D) ($25,000)

Because the Rubber Division sustained a loss,the president of Vanik is considering the elimination of this division.All of the division's traceable fixed costs could be avoided if the division was dropped.None of the allocated common corporate fixed costs could be avoided.If the Rubber Division was dropped at the beginning of last year,the financial advantage (disadvantage)to the company for the year would have been:A) ($20,000)

B) $20,000

C) $25,000

D) ($25,000)

Question

Question

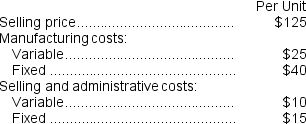

CoolAir Corporation manufactures portable window air conditioners.CoolAir has the capacity to manufacture and sell 80,000 air conditioners each year but is currently only manufacturing and selling 60,000.The following per unit numbers relate to annual operations at 60,000 units:

The City of Clearwater would like to purchase 3,000 air conditioners from CoolAir but only if they can get them for $75 each.Variable selling and administrative costs on this special order will drop down to $2 per unit.This special order will not affect the 60,000 regular sales and it will not affect the total fixed costs.The annual financial advantage (disadvantage)for the company as a result of accepting this special order from the City of Clearwater should be:

The City of Clearwater would like to purchase 3,000 air conditioners from CoolAir but only if they can get them for $75 each.Variable selling and administrative costs on this special order will drop down to $2 per unit.This special order will not affect the 60,000 regular sales and it will not affect the total fixed costs.The annual financial advantage (disadvantage)for the company as a result of accepting this special order from the City of Clearwater should be:

A) ($21,000)

B) $24,000

C) $144,000

D) ($129,000)

The City of Clearwater would like to purchase 3,000 air conditioners from CoolAir but only if they can get them for $75 each.Variable selling and administrative costs on this special order will drop down to $2 per unit.This special order will not affect the 60,000 regular sales and it will not affect the total fixed costs.The annual financial advantage (disadvantage)for the company as a result of accepting this special order from the City of Clearwater should be:A) ($21,000)

B) $24,000

C) $144,000

D) ($129,000)

Question

Question

Gordon Corporation produces 1,000 units of a part per year which are used in the assembly of one of its products.The unit cost of producing these parts is:

The part can be purchased from an outside supplier at $20 per unit.If the part is purchased from the outside supplier,two thirds of the total fixed costs incurred in producing the part can be avoided.The annual financial advantage (disadvantage)for the company as a result of buying the part from the outside supplier would be:

The part can be purchased from an outside supplier at $20 per unit.If the part is purchased from the outside supplier,two thirds of the total fixed costs incurred in producing the part can be avoided.The annual financial advantage (disadvantage)for the company as a result of buying the part from the outside supplier would be:

A) $3,000

B) ($1,000)

C) $7,000

D) ($5,000)

The part can be purchased from an outside supplier at $20 per unit.If the part is purchased from the outside supplier,two thirds of the total fixed costs incurred in producing the part can be avoided.The annual financial advantage (disadvantage)for the company as a result of buying the part from the outside supplier would be:A) $3,000

B) ($1,000)

C) $7,000

D) ($5,000)

Question

Rebelo Corporation is presently making part E07 that is used in one of its products.A total of 17,000 units of this part are produced and used every year.The company's Accounting Department reports the following costs of producing the part at this level of activity:

An outside supplier has offered to make and sell the part to the company for $20.80 each.If this offer is accepted,the supervisor's salary and all of the variable costs,including direct labor,can be avoided.The special equipment used to make the part was purchased many years ago and has no salvage value or other use.The allocated general overhead represents fixed costs of the entire company,none of which would be avoided if the part were purchased instead of produced internally.If management decides to buy part E07 from the outside supplier rather than to continue making the part,what would be the annual impact on the company's overall net operating income?

An outside supplier has offered to make and sell the part to the company for $20.80 each.If this offer is accepted,the supervisor's salary and all of the variable costs,including direct labor,can be avoided.The special equipment used to make the part was purchased many years ago and has no salvage value or other use.The allocated general overhead represents fixed costs of the entire company,none of which would be avoided if the part were purchased instead of produced internally.If management decides to buy part E07 from the outside supplier rather than to continue making the part,what would be the annual impact on the company's overall net operating income?

A) ($6,800)

B) ($163,200)

C) $163,200

D) $6,800

An outside supplier has offered to make and sell the part to the company for $20.80 each.If this offer is accepted,the supervisor's salary and all of the variable costs,including direct labor,can be avoided.The special equipment used to make the part was purchased many years ago and has no salvage value or other use.The allocated general overhead represents fixed costs of the entire company,none of which would be avoided if the part were purchased instead of produced internally.If management decides to buy part E07 from the outside supplier rather than to continue making the part,what would be the annual impact on the company's overall net operating income?A) ($6,800)

B) ($163,200)

C) $163,200

D) $6,800

Question

Zouar Computer Corporation currently manufactures the disk drives that it uses in its computers.The costs to produce 5,000 of these disk drives last year were as follows:

Kidal Electronics has offered to provide Zouar with all of its disk drive needs for $27 per drive.If Zouar accepts this offer,Zouar will be able to use the freed up space to generate an additional $40,000 of income each year to produce more of its computer keyboards.Only $3 per drive of the fixed manufacturing overhead cost above could be avoided.Direct labor is an avoidable cost in this decision.Based on this information,would Zouar be financially better off making the drives or buying the drives and by how much?

Kidal Electronics has offered to provide Zouar with all of its disk drive needs for $27 per drive.If Zouar accepts this offer,Zouar will be able to use the freed up space to generate an additional $40,000 of income each year to produce more of its computer keyboards.Only $3 per drive of the fixed manufacturing overhead cost above could be avoided.Direct labor is an avoidable cost in this decision.Based on this information,would Zouar be financially better off making the drives or buying the drives and by how much?

A) $15,000 better to buy

B) $20,000 better to buy

C) $35,000 better to buy

D) $60,000 better to make

Kidal Electronics has offered to provide Zouar with all of its disk drive needs for $27 per drive.If Zouar accepts this offer,Zouar will be able to use the freed up space to generate an additional $40,000 of income each year to produce more of its computer keyboards.Only $3 per drive of the fixed manufacturing overhead cost above could be avoided.Direct labor is an avoidable cost in this decision.Based on this information,would Zouar be financially better off making the drives or buying the drives and by how much?A) $15,000 better to buy

B) $20,000 better to buy

C) $35,000 better to buy

D) $60,000 better to make

Question

Sharp Corporation produces 8,000 parts each year,which are used in the production of one of its products.The unit product cost of a part is $36,computed as follows:

The parts can be purchased from an outside supplier for only $28 each.The space in which the parts are now produced would be idle and fixed production costs would be reduced by one-fourth.Based on these data,the financial advantage (disadvantage)of purchasing the parts from the outside supplier would be:

The parts can be purchased from an outside supplier for only $28 each.The space in which the parts are now produced would be idle and fixed production costs would be reduced by one-fourth.Based on these data,the financial advantage (disadvantage)of purchasing the parts from the outside supplier would be:

A) $24,000

B) ($24,000)

C) $56,000

D) ($56,000)

The parts can be purchased from an outside supplier for only $28 each.The space in which the parts are now produced would be idle and fixed production costs would be reduced by one-fourth.Based on these data,the financial advantage (disadvantage)of purchasing the parts from the outside supplier would be:A) $24,000

B) ($24,000)

C) $56,000

D) ($56,000)

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/203

Play

Full screen (f)

Deck 12: Differential Analysis: The Key to Decision Making

1

Future costs that do not differ between the alternatives in a decision are avoidable costs.

False

2

Sunk costs are never relevant in decision making.

True

3

Opportunity costs represent costs that can be reduced by effective management of operations.

False

4

Future costs that do differ among the alternatives are not relevant in a decision.

Unlock Deck

Unlock for access to all 203 flashcards in this deck.

Unlock Deck

k this deck

5

A cost that can be avoided by choosing one alternative over another is relevant for decision purposes.

Unlock Deck

Unlock for access to all 203 flashcards in this deck.

Unlock Deck

k this deck

6

Variable costs are always relevant costs in decisions.

Unlock Deck

Unlock for access to all 203 flashcards in this deck.

Unlock Deck

k this deck

7

A cost that is assigned to a product using activity-based costing may or may not be a relevant cost in a decision involving that product.

Unlock Deck

Unlock for access to all 203 flashcards in this deck.

Unlock Deck

k this deck

8

Fixed costs are sunk costs.

Unlock Deck

Unlock for access to all 203 flashcards in this deck.

Unlock Deck

k this deck

9

Sunk costs are costs that have proven to be unproductive.

Unlock Deck

Unlock for access to all 203 flashcards in this deck.

Unlock Deck

k this deck

10

Sunk costs and future costs that do not differ between the alternatives may or may not be relevant in a decision.

Unlock Deck

Unlock for access to all 203 flashcards in this deck.

Unlock Deck

k this deck

11

It may be a good decision to replace an asset before its original cost has been fully recovered through increased revenues or decreased costs.

Unlock Deck

Unlock for access to all 203 flashcards in this deck.

Unlock Deck

k this deck

12

The book value of an old machine is always considered an opportunity cost in a decision.

Unlock Deck

Unlock for access to all 203 flashcards in this deck.

Unlock Deck

k this deck

13

Fixed costs may be relevant in a decision.

Unlock Deck

Unlock for access to all 203 flashcards in this deck.

Unlock Deck

k this deck

14

Consistency demands that a cost that is relevant in one decision be regarded as relevant in other decisions as well.

Unlock Deck

Unlock for access to all 203 flashcards in this deck.

Unlock Deck

k this deck

15

An avoidable cost is a sunk cost that can be eliminated (in whole or in part)as a result of choosing one alternative over another.

Unlock Deck

Unlock for access to all 203 flashcards in this deck.

Unlock Deck

k this deck

16

A complete income statement need not be prepared as part of a differential cost analysis.

Unlock Deck

Unlock for access to all 203 flashcards in this deck.

Unlock Deck

k this deck

17

A cost that will be incurred regardless of which alternative is selected is not relevant when choosing between the alternatives.

Unlock Deck

Unlock for access to all 203 flashcards in this deck.

Unlock Deck

k this deck

18

Avoidable costs are irrelevant costs in decisions.

Unlock Deck

Unlock for access to all 203 flashcards in this deck.

Unlock Deck

k this deck

19

The variable costs of a product are relevant in a decision concerning whether to eliminate the product.

Unlock Deck

Unlock for access to all 203 flashcards in this deck.

Unlock Deck

k this deck

20

A cost that is traceable to a segment through activity-based costing is always an avoidable cost for decision making.

Unlock Deck

Unlock for access to all 203 flashcards in this deck.

Unlock Deck

k this deck

21

Two or more products that are produced from a common input are known as joint products.

Unlock Deck

Unlock for access to all 203 flashcards in this deck.

Unlock Deck

k this deck

22

The split-off point in a process that produces joint products is the point in the manufacturing process at which the joint products can be recognized as separate products.

Unlock Deck

Unlock for access to all 203 flashcards in this deck.

Unlock Deck

k this deck

23

Eliminating nonproductive processing time is particularly important in a bottleneck operation.

Unlock Deck

Unlock for access to all 203 flashcards in this deck.

Unlock Deck

k this deck

24

Which of the following would be relevant in the decision to sell or throw out obsolete inventory?

Unlock Deck

Unlock for access to all 203 flashcards in this deck.

Unlock Deck

k this deck

25

It is profitable to continue processing joint products after the split-off point if their total revenues exceed the joint costs.

Unlock Deck

Unlock for access to all 203 flashcards in this deck.

Unlock Deck

k this deck

26

In a decision to drop a product,the product should be charged for rent in proportion to the space it occupies even if the space has no alternative use and the rental payment is unavoidable.

Unlock Deck

Unlock for access to all 203 flashcards in this deck.

Unlock Deck

k this deck

27

A product whose revenues do not cover its variable costs and its traceable fixed costs should usually be dropped.

Unlock Deck

Unlock for access to all 203 flashcards in this deck.

Unlock Deck

k this deck

28

A vertically integrated company is less dependent on its suppliers than a company that is not vertically integrated.

Unlock Deck

Unlock for access to all 203 flashcards in this deck.

Unlock Deck

k this deck

29

Payment of overtime to a worker in order to relax a production constraint could increase the profits of a company.

Unlock Deck

Unlock for access to all 203 flashcards in this deck.

Unlock Deck

k this deck

30

A disadvantage of vertical integration is that by pooling demand for parts from a number of companies,a supplier may be able to enjoy economies of scale that result in higher quality and lower cost than if every company makes its own parts.

Unlock Deck

Unlock for access to all 203 flashcards in this deck.

Unlock Deck

k this deck

31

One way to increase the effective utilization of a bottleneck is to reduce the number of defective units.

Unlock Deck

Unlock for access to all 203 flashcards in this deck.

Unlock Deck

k this deck

32

When a company has a production constraint,total contribution margin will be maximized by emphasizing the products with the highest contribution margin per unit of the constrained resource.

Unlock Deck

Unlock for access to all 203 flashcards in this deck.

Unlock Deck

k this deck

33

Fixed costs are irrelevant in decisions about whether a product should be dropped.

Unlock Deck

Unlock for access to all 203 flashcards in this deck.

Unlock Deck

k this deck

34

When a company is involved in more than one activity in the entire value chain,it is vertically integrated.

Unlock Deck

Unlock for access to all 203 flashcards in this deck.

Unlock Deck

k this deck

35

An avoidable fixed production cost incurred before the split-off point in a joint process is relevant in a sell or process further decision.

Unlock Deck

Unlock for access to all 203 flashcards in this deck.

Unlock Deck

k this deck

36

In a factory operating at capacity,every machine and person should be working at the maximum possible rate.

Unlock Deck

Unlock for access to all 203 flashcards in this deck.

Unlock Deck

k this deck

37

In a special order situation,any fixed cost associated with the order would be irrelevant.

Unlock Deck

Unlock for access to all 203 flashcards in this deck.

Unlock Deck

k this deck

38

In a special order situation that involves using capacity that is not idle,opportunity costs are zero.

Unlock Deck

Unlock for access to all 203 flashcards in this deck.

Unlock Deck

k this deck

39

When a company has a production constraint,the product with the lowest contribution margin per unit of the constrained resource should usually be given highest priority.

Unlock Deck

Unlock for access to all 203 flashcards in this deck.

Unlock Deck

k this deck

40

The term joint cost is used to describe the costs incurred up to the split-off point in a process involving joint products.

Unlock Deck

Unlock for access to all 203 flashcards in this deck.

Unlock Deck

k this deck

41

Lusk Corporation produces and sells 10,000 units of Product X each month.The selling price of Product X is $40 per unit,and variable expenses are $32 per unit.A study has been made concerning whether Product X should be discontinued.The study shows that $70,000 of the $120,000 in monthly fixed expenses charged to Product X would not be avoidable even if the product was discontinued.If Product X is discontinued,the annual financial advantage (disadvantage)for the company of eliminating this product should be:

A) ($30,000)

B) $30,000

C) $40,000

D) ($40,000)

A) ($30,000)

B) $30,000

C) $40,000

D) ($40,000)

Unlock Deck

Unlock for access to all 203 flashcards in this deck.

Unlock Deck

k this deck

42

Milford Corporation has in stock 16,100 kilograms of material R that it bought five years ago for $5.75 per kilogram.This raw material was purchased to use in a product line that has been discontinued.Material R can be sold as is for scrap for $3.91 per kilogram.An alternative would be to use material R in one of the company's current products,S88Y,which currently requires 2 kilograms of a raw material that is available for $7.60 per kilogram.Material R can be modified at a cost of $0.77 per kilogram so that it can be used as a substitute for this material in the production of product S88Y.However,after modification,4 kilograms of material R is required for every unit of product S88Y that is produced.Milford Corporation has now received a request from a company that could use material R in its production process.Assuming that Milford Corporation could use all of its stock of material R to make product S88Y or the company could sell all of its stock of the material at the current scrap price of $3.91 per kilogram,what is the minimum acceptable selling price of material R to the company that could use material R in its own production process?

A) $0.88 per kg

B) $3.03 per kg

C) $4.57 per kg

D) $3.91 per kg

A) $0.88 per kg

B) $3.03 per kg

C) $4.57 per kg

D) $3.91 per kg

Unlock Deck

Unlock for access to all 203 flashcards in this deck.

Unlock Deck

k this deck

43

Kinsi Corporation manufactures five different products.All five of these products must pass through a stamping machine in its fabrication department.This machine is Kinsi's constrained resource.Kinsi would make the most profit if it produces the product that:

A) uses the least amount of stamping time.

B) generates the highest contribution margin per unit.

C) generates the highest contribution margin ratio.

D) generates the highest contribution margin per stamping machine hour.

A) uses the least amount of stamping time.

B) generates the highest contribution margin per unit.

C) generates the highest contribution margin ratio.

D) generates the highest contribution margin per stamping machine hour.

Unlock Deck

Unlock for access to all 203 flashcards in this deck.

Unlock Deck

k this deck

44

Munafo Corporation is a specialty component manufacturer with idle capacity.Management would like to use its extra capacity to generate additional profits.A potential customer has offered to buy 6,500 units of component VGI.Each unit of VGI requires 1 unit of material I57 and 5 units of material M97.Data concerning these two materials follow:

Material I57 is in use in many of the company's products and is routinely replenished.Material M97 is no longer used by the company in any of its normal products and existing stocks would not be replenished once they are used up.

What would be the relevant cost of the materials,in total,for purposes of determining a minimum acceptable price for the order for product VGI?

A) $174,850

B) $213,130

C) $213,850

D) $171,925

Material I57 is in use in many of the company's products and is routinely replenished.Material M97 is no longer used by the company in any of its normal products and existing stocks would not be replenished once they are used up.What would be the relevant cost of the materials,in total,for purposes of determining a minimum acceptable price for the order for product VGI?

A) $174,850

B) $213,130

C) $213,850

D) $171,925

Unlock Deck

Unlock for access to all 203 flashcards in this deck.

Unlock Deck

k this deck

45

The Jabba Corporation manufactures the "Snack Buster" which consists of a wooden snack chip bowl with an attached porcelain dip bowl.Which of the following would be relevant in Jabba's decision to make the dip bowls or buy them from an outside supplier?

Unlock Deck

Unlock for access to all 203 flashcards in this deck.

Unlock Deck

k this deck

46

In a sell or process further decision,consider the following costs:

I)A variable production cost incurred prior to split-off.

II)A variable production cost incurred after split-off.

III)An avoidable fixed production cost incurred after split-off.

Which of the above costs is (are)not relevant in a decision regarding whether the product should be processed further?

A) Only I

B) Only III

C) Only I and II

D) Only I and III

I)A variable production cost incurred prior to split-off.

II)A variable production cost incurred after split-off.

III)An avoidable fixed production cost incurred after split-off.

Which of the above costs is (are)not relevant in a decision regarding whether the product should be processed further?

A) Only I

B) Only III

C) Only I and II

D) Only I and III

Unlock Deck

Unlock for access to all 203 flashcards in this deck.

Unlock Deck

k this deck

47

One of the employees of Davenport Corporation recently was involved in an accident with one of the corporation's delivery vans.The corporation is either going to repair the damaged van or sell it as is and buy a comparable used van.Information related to this decision is provided below:

Based on the information above,Davenport would be financially better off:

A) $1,000 by buying the comparable van.

B) $2,000 by buying the comparable van.

C) $2,000 by repairing the damaged van.

D) $4,000 by repairing the damaged van.

Based on the information above,Davenport would be financially better off:A) $1,000 by buying the comparable van.

B) $2,000 by buying the comparable van.

C) $2,000 by repairing the damaged van.

D) $4,000 by repairing the damaged van.

Unlock Deck

Unlock for access to all 203 flashcards in this deck.

Unlock Deck

k this deck

48

Hodge Inc.has some material that originally cost $74,600.The material has a scrap value of $57,400 as is,but if reworked at a cost of $1,500,it could be sold for $54,400.What would be the financial advantage (disadvantage)of reworking and selling the material rather than selling it as is as scrap?

A) ($79,100)

B) ($21,700)

C) ($4,500)

D) $52,900

A) ($79,100)

B) ($21,700)

C) ($4,500)

D) $52,900

Unlock Deck

Unlock for access to all 203 flashcards in this deck.

Unlock Deck

k this deck

49

The opportunity cost of making a component part in a factory with excess capacity for which there is no alternative use is:

A) the variable manufacturing cost of the component.

B) the total manufacturing cost of the component.

C) the fixed manufacturing cost of the component.

D) zero.

A) the variable manufacturing cost of the component.

B) the total manufacturing cost of the component.

C) the fixed manufacturing cost of the component.

D) zero.

Unlock Deck

Unlock for access to all 203 flashcards in this deck.

Unlock Deck

k this deck

50

Product X-547 is one of the joint products in a joint manufacturing process.Management is considering whether to sell X-547 at the split-off point or to process X-547 further into Xylene.The following data have been gathered:

I)Selling price of X-547

II)Variable cost of processing X-547 into Xylene.

III)The avoidable fixed costs of processing X-547 into Xylene.

IV)The selling price of Xylene.

V)The joint cost of the process from which X-547 is produced.

Which of the above items are relevant in a decision of whether to sell the X-547 as is or process it further into Xylene?

A) I, II, and IV.

B) I, II, III, and IV.

C) II, III, and V.

D) I, II, III, and V.

I)Selling price of X-547

II)Variable cost of processing X-547 into Xylene.

III)The avoidable fixed costs of processing X-547 into Xylene.

IV)The selling price of Xylene.

V)The joint cost of the process from which X-547 is produced.

Which of the above items are relevant in a decision of whether to sell the X-547 as is or process it further into Xylene?

A) I, II, and IV.

B) I, II, III, and IV.

C) II, III, and V.

D) I, II, III, and V.

Unlock Deck

Unlock for access to all 203 flashcards in this deck.

Unlock Deck

k this deck

51

Otool Inc.is considering using stocks of an old raw material in a special project.The special project would require all 240 kilograms of the raw material that are in stock and that originally cost the company $2,112 in total.If the company were to buy new supplies of this raw material on the open market,it would cost $9.25 per kilogram.However,the company has no other use for this raw material and would sell it at the discounted price of $8.35 per kilogram if it were not used in the special project.The sale of the raw material would involve delivery to the purchaser at a total cost of $71 for all 240 kilograms.What is the relevant cost of the 240 kilograms of the raw material when deciding whether to proceed with the special project?

A) $1,933

B) $2,004

C) $2,220

D) $2,112

A) $1,933

B) $2,004

C) $2,220

D) $2,112

Unlock Deck

Unlock for access to all 203 flashcards in this deck.

Unlock Deck

k this deck

52

Which of the following costs are always irrelevant in decision making?

A) avoidable costs

B) sunk costs

C) opportunity costs

D) fixed costs

A) avoidable costs

B) sunk costs

C) opportunity costs

D) fixed costs

Unlock Deck

Unlock for access to all 203 flashcards in this deck.

Unlock Deck

k this deck

53

A joint product is:

A) any product which consists of several parts.

B) any product produced by a company with more than one product line.

C) any product involved in a make or buy decision.

D) one of several products produced from a common input.

A) any product which consists of several parts.

B) any product produced by a company with more than one product line.

C) any product involved in a make or buy decision.

D) one of several products produced from a common input.

Unlock Deck

Unlock for access to all 203 flashcards in this deck.

Unlock Deck

k this deck

54

Costs that can be eliminated in whole or in part if a particular business segment is discontinued are called:

A) sunk costs.

B) opportunity costs.

C) avoidable costs.

D) irrelevant costs.

A) sunk costs.

B) opportunity costs.

C) avoidable costs.

D) irrelevant costs.

Unlock Deck

Unlock for access to all 203 flashcards in this deck.

Unlock Deck

k this deck

55

Winder Corporation is a specialty component manufacturer with idle capacity.Management would like to use its extra capacity to generate additional profits.A potential customer has offered to buy 3,000 units of component QEA.Each unit of QEA requires 5 units of material F85 and 5 units of material E71.Data concerning these two materials follow:

Material F85 is in use in many of the company's products and is routinely replenished.Material E71 is no longer used by the company in any of its normal products and existing stocks would not be replenished once they are used up.

What would be the relevant cost of the materials,in total,for purposes of determining a minimum acceptable price for the order for product QEA?

A) $126,702

B) $141,750

C) $126,295

D) $145,965

Material F85 is in use in many of the company's products and is routinely replenished.Material E71 is no longer used by the company in any of its normal products and existing stocks would not be replenished once they are used up.What would be the relevant cost of the materials,in total,for purposes of determining a minimum acceptable price for the order for product QEA?

A) $126,702

B) $141,750

C) $126,295

D) $145,965

Unlock Deck

Unlock for access to all 203 flashcards in this deck.

Unlock Deck

k this deck

56

United Industries manufactures a number of products at its highly automated factory.The products are very popular,with demand far exceeding the factory's capacity.To maximize profit,management should rank products based on their:

A) gross margin

B) contribution margin

C) selling price

D) contribution margin per unit of the constrained resource

A) gross margin

B) contribution margin

C) selling price

D) contribution margin per unit of the constrained resource

Unlock Deck

Unlock for access to all 203 flashcards in this deck.

Unlock Deck

k this deck

57

Hamby Corporation is preparing a bid for a special order that would require 780 liters of material W34C.The company already has 640 liters of this raw material in stock that originally cost $8.30 per liter.Material W34C is used in the company's main product and is replenished on a periodic basis.The resale value of the existing stock of the material is $7.60 per liter.New stocks of the material can be readily purchased for $8.35 per liter.What is the relevant cost of the 780 liters of the raw material when deciding how much to bid on the special order?

A) $6,481

B) $6,376

C) $6,513

D) $5,928

A) $6,481

B) $6,376

C) $6,513

D) $5,928

Unlock Deck

Unlock for access to all 203 flashcards in this deck.

Unlock Deck

k this deck

58

Schickel Inc.regularly uses material B39U and currently has in stock 460 liters of the material for which it paid $3,128 several weeks ago.If this were to be sold as is on the open market as surplus material,it would fetch $5.95 per liter.New stocks of the material can be purchased on the open market for $6.45 per liter,but it must be purchased in lots of 1,000 liters.You have been asked to determine the relevant cost of 760 liters of the material to be used in a job for a customer.The relevant cost of the 760 liters of material B39U is:

A) $4,902

B) $4,672

C) $4,522

D) $6,450

A) $4,902

B) $4,672

C) $4,522

D) $6,450

Unlock Deck

Unlock for access to all 203 flashcards in this deck.

Unlock Deck

k this deck

59

Product U23N has been considered a drag on profits at Jinkerson Corporation for some time and management is considering discontinuing the product altogether.Data from the company's budget for the upcoming year appear below:

In the company's accounting system all fixed expenses of the company are fully allocated to products.Further investigation has revealed that $144,000 of the fixed manufacturing expenses and $93,000 of the fixed selling and administrative expenses are avoidable if product U23N is discontinued.The financial advantage (disadvantage)for the company of eliminating this product for the upcoming year would be:

A) $15,000

B) $143,000

C) ($143,000)

D) ($15,000)

In the company's accounting system all fixed expenses of the company are fully allocated to products.Further investigation has revealed that $144,000 of the fixed manufacturing expenses and $93,000 of the fixed selling and administrative expenses are avoidable if product U23N is discontinued.The financial advantage (disadvantage)for the company of eliminating this product for the upcoming year would be:A) $15,000

B) $143,000

C) ($143,000)

D) ($15,000)

Unlock Deck

Unlock for access to all 203 flashcards in this deck.

Unlock Deck

k this deck

60

Accepting a special order will improve overall net operating income if the revenue from the special order exceeds:

A) the contribution margin on the order.

B) the incremental costs associated with the order.

C) the variable costs associated with the order.

D) the sunk costs associated with the order.

A) the contribution margin on the order.

B) the incremental costs associated with the order.

C) the variable costs associated with the order.

D) the sunk costs associated with the order.

Unlock Deck

Unlock for access to all 203 flashcards in this deck.

Unlock Deck

k this deck

61

Part U16 is used by Mcvean Corporation to make one of its products.A total of 13,000 units of this part are produced and used every year.The company's Accounting Department reports the following costs of producing the part at this level of activity:

An outside supplier has offered to make the part and sell it to the company for $29.80 each.If this offer is accepted,the supervisor's salary and all of the variable costs,including the direct labor,can be avoided.The special equipment used to make the part was purchased many years ago and has no salvage value or other use.The allocated general overhead represents fixed costs of the entire company,none of which would be avoided if the part were purchased instead of produced internally.In addition,the space used to make part U16 could be used to make more of one of the company's other products,generating an additional segment margin of $25,000 per year for that product.The annual financial advantage (disadvantage)for the company as a result of buying part U16 from the outside supplier should be:

A) $25,000

B) ($79,000)

C) ($35,400)

D) $14,600

An outside supplier has offered to make the part and sell it to the company for $29.80 each.If this offer is accepted,the supervisor's salary and all of the variable costs,including the direct labor,can be avoided.The special equipment used to make the part was purchased many years ago and has no salvage value or other use.The allocated general overhead represents fixed costs of the entire company,none of which would be avoided if the part were purchased instead of produced internally.In addition,the space used to make part U16 could be used to make more of one of the company's other products,generating an additional segment margin of $25,000 per year for that product.The annual financial advantage (disadvantage)for the company as a result of buying part U16 from the outside supplier should be:A) $25,000

B) ($79,000)

C) ($35,400)

D) $14,600

Unlock Deck

Unlock for access to all 203 flashcards in this deck.

Unlock Deck

k this deck

62

Supler Corporation produces a part used in the manufacture of one of its products.The unit product cost is $18,computed as follows:

An outside supplier has offered to provide the annual requirement of 4,000 of the parts for only $14 each.The company estimates that 60% of the fixed manufacturing overhead cost above could be eliminated if the parts are purchased from the outside supplier.Assume that direct labor is an avoidable cost in this decision.Based on these data,the financial advantage (disadvantage)of purchasing the parts from the outside supplier would be:

A) ($1) per unit on average

B) $1 per unit on average

C) $2 per unit on average

D) ($4) per unit on average

An outside supplier has offered to provide the annual requirement of 4,000 of the parts for only $14 each.The company estimates that 60% of the fixed manufacturing overhead cost above could be eliminated if the parts are purchased from the outside supplier.Assume that direct labor is an avoidable cost in this decision.Based on these data,the financial advantage (disadvantage)of purchasing the parts from the outside supplier would be:A) ($1) per unit on average

B) $1 per unit on average

C) $2 per unit on average

D) ($4) per unit on average

Unlock Deck

Unlock for access to all 203 flashcards in this deck.

Unlock Deck

k this deck

63

The Cook Corporation has two divisions--East and West.The divisions have the following revenues and expenses:

The management of Cook is considering the elimination of the West Division.If the West Division were eliminated,its traceable fixed costs could be avoided.Total common corporate costs would be unaffected by this decision.Given these data,the elimination of the West Division would result in an overall company net operating income (loss)of:

A) $15,000

B) $(155,000)

C) $(75,000)

D) $(60,000)

The management of Cook is considering the elimination of the West Division.If the West Division were eliminated,its traceable fixed costs could be avoided.Total common corporate costs would be unaffected by this decision.Given these data,the elimination of the West Division would result in an overall company net operating income (loss)of:A) $15,000

B) $(155,000)

C) $(75,000)

D) $(60,000)

Unlock Deck

Unlock for access to all 203 flashcards in this deck.

Unlock Deck

k this deck

64

Norgaard Corporation makes 8,000 units of part G25 each year.This part is used in one of the company's products.The company's Accounting Department reports the following costs of producing the part at this level of activity:

An outside supplier has offered to make and sell the part to the company for $21.20 each.If this offer is accepted,the supervisor's salary and all of the variable costs,including direct labor,can be avoided.The special equipment used to make the part was purchased many years ago and has no salvage value or other use.The allocated general overhead represents fixed costs of the entire company.If the outside supplier's offer were accepted,only $2,000 of these allocated general overhead costs would be avoided.In addition,the space used to produce part G25 would be used to make more of one of the company's other products,generating an additional segment margin of $16,000 per year for that product.

The annual financial advantage (disadvantage)for the company as a result of buying part G25 from the outside supplier should be:

A) ($8,400)

B) $16,000

C) ($8,000)

D) ($40,000)

An outside supplier has offered to make and sell the part to the company for $21.20 each.If this offer is accepted,the supervisor's salary and all of the variable costs,including direct labor,can be avoided.The special equipment used to make the part was purchased many years ago and has no salvage value or other use.The allocated general overhead represents fixed costs of the entire company.If the outside supplier's offer were accepted,only $2,000 of these allocated general overhead costs would be avoided.In addition,the space used to produce part G25 would be used to make more of one of the company's other products,generating an additional segment margin of $16,000 per year for that product.The annual financial advantage (disadvantage)for the company as a result of buying part G25 from the outside supplier should be:

A) ($8,400)

B) $16,000

C) ($8,000)

D) ($40,000)

Unlock Deck

Unlock for access to all 203 flashcards in this deck.

Unlock Deck

k this deck

65

Fabri Corporation is considering eliminating a department that has an annual contribution margin of $35,000 and $70,000 in annual fixed costs.Of the fixed costs,$25,000 cannot be avoided.The annual financial advantage (disadvantage)for the company of eliminating this department would be:

A) $10,000

B) ($10,000)

C) $35,000

D) ($35,000)

A) $10,000

B) ($10,000)

C) $35,000

D) ($35,000)

Unlock Deck

Unlock for access to all 203 flashcards in this deck.

Unlock Deck

k this deck

66

The management of Furrow Corporation is considering dropping product L07E.Data from the company's budget for the upcoming year appear below:

In the company's accounting system all fixed expenses of the company are fully allocated to products.Further investigation has revealed that $186,000 of the fixed manufacturing expenses and $106,000 of the fixed selling and administrative expenses are avoidable if product L07E is discontinued.The financial advantage (disadvantage)for the company of eliminating this product for the upcoming year would be:

A) $8,000

B) ($173,000)

C) ($8,000)

D) $173,000

In the company's accounting system all fixed expenses of the company are fully allocated to products.Further investigation has revealed that $186,000 of the fixed manufacturing expenses and $106,000 of the fixed selling and administrative expenses are avoidable if product L07E is discontinued.The financial advantage (disadvantage)for the company of eliminating this product for the upcoming year would be:A) $8,000

B) ($173,000)

C) ($8,000)

D) $173,000

Unlock Deck

Unlock for access to all 203 flashcards in this deck.

Unlock Deck

k this deck

67

The following information relates to next year's projected operating results of the Children's Division of Grunge Clothing Corporation:

If the Children's Division is eliminated,$170,000 of the above fixed expenses could be avoided.The annual financial advantage (disadvantage)for the company of eliminating this division should be:

A) ($300,000)

B) $30,000

C) ($30,000)

D) $300,000

If the Children's Division is eliminated,$170,000 of the above fixed expenses could be avoided.The annual financial advantage (disadvantage)for the company of eliminating this division should be:A) ($300,000)

B) $30,000

C) ($30,000)

D) $300,000

Unlock Deck

Unlock for access to all 203 flashcards in this deck.

Unlock Deck

k this deck

68

Part S51 is used in one of Haberkorn Corporation's products.The company makes 12,000 units of this part each year.The company's Accounting Department reports the following costs of producing the part at this level of activity:

An outside supplier has offered to produce this part and sell it to the company for $37.70 each.If this offer is accepted,the supervisor's salary and all of the variable costs,including direct labor,can be avoided.The special equipment used to make the part was purchased many years ago and has no salvage value or other use.The allocated general overhead represents fixed costs of the entire company.If the outside supplier's offer were accepted,only $17,000 of these allocated general overhead costs would be avoided.

The annual financial advantage (disadvantage)for the company as a result of buying the part from the outside supplier would be:

A) ($5,800)

B) ($22,800)

C) ($149,800)

D) ($39,800)

An outside supplier has offered to produce this part and sell it to the company for $37.70 each.If this offer is accepted,the supervisor's salary and all of the variable costs,including direct labor,can be avoided.The special equipment used to make the part was purchased many years ago and has no salvage value or other use.The allocated general overhead represents fixed costs of the entire company.If the outside supplier's offer were accepted,only $17,000 of these allocated general overhead costs would be avoided.The annual financial advantage (disadvantage)for the company as a result of buying the part from the outside supplier would be:

A) ($5,800)

B) ($22,800)

C) ($149,800)

D) ($39,800)

Unlock Deck

Unlock for access to all 203 flashcards in this deck.

Unlock Deck

k this deck

69

The SP Corporation makes 40,000 motors to be used in the production of its sewing machines.The average cost per motor at this level of activity is:

An outside supplier recently began producing a comparable motor that could be used in the sewing machine.The price offered to SP Corporation for this motor is $18.If SP Corporation decides not to make the motors,there would be no other use for the production facilities and none of the fixed manufacturing overhead cost could be avoided.Direct labor is a variable cost in this company.The annual financial advantage (disadvantage)for the company as a result of making the motors rather than buying them from the outside supplier would be:

A) $276,000

B) $86,000

C) ($92,000)

D) $178,000

An outside supplier recently began producing a comparable motor that could be used in the sewing machine.The price offered to SP Corporation for this motor is $18.If SP Corporation decides not to make the motors,there would be no other use for the production facilities and none of the fixed manufacturing overhead cost could be avoided.Direct labor is a variable cost in this company.The annual financial advantage (disadvantage)for the company as a result of making the motors rather than buying them from the outside supplier would be:A) $276,000

B) $86,000

C) ($92,000)

D) $178,000

Unlock Deck

Unlock for access to all 203 flashcards in this deck.

Unlock Deck

k this deck

70

Sardi Inc.is considering whether to continue to make a component or to buy it from an outside supplier.The company uses 17,000 of the components each year.The unit product cost of the component according to the company's cost accounting system is given as follows:

Assume that direct labor is a variable cost.Of the fixed manufacturing overhead,70% is avoidable if the component were bought from the outside supplier.In addition,making the component uses 2 minutes on the machine that is the company's current constraint.If the component were bought,time would be freed up for use on another product that requires 4 minutes on this machine and that has a contribution margin of $7.00 per unit.

When deciding whether to make or buy the component,what cost of making the component should be compared to the price of buying the component?

A) $24.21 per unit

B) $25.50 per unit

C) $20.71 per unit

D) $22.00 per unit

Assume that direct labor is a variable cost.Of the fixed manufacturing overhead,70% is avoidable if the component were bought from the outside supplier.In addition,making the component uses 2 minutes on the machine that is the company's current constraint.If the component were bought,time would be freed up for use on another product that requires 4 minutes on this machine and that has a contribution margin of $7.00 per unit.When deciding whether to make or buy the component,what cost of making the component should be compared to the price of buying the component?

A) $24.21 per unit

B) $25.50 per unit

C) $20.71 per unit

D) $22.00 per unit

Unlock Deck

Unlock for access to all 203 flashcards in this deck.

Unlock Deck

k this deck

71

A study has been conducted to determine if Product A should be dropped.Sales of the product total $500,000; variable expenses total $340,000.Fixed expenses charged to the product total $210,000.The company estimates that $60,000 of these fixed expenses are not avoidable even if the product is dropped.If Product A is dropped,the annual financial advantage (disadvantage)for the company of eliminating this product should be:

A) ($10,000)

B) $10,000

C) ($50,000)

D) $50,000

A) ($10,000)

B) $10,000

C) ($50,000)

D) $50,000

Unlock Deck

Unlock for access to all 203 flashcards in this deck.

Unlock Deck

k this deck

72

Vanik Corporation currently has two divisions which had the following operating results for last year:

Because the Rubber Division sustained a loss,the president of Vanik is considering the elimination of this division.All of the division's traceable fixed costs could be avoided if the division was dropped.None of the allocated common corporate fixed costs could be avoided.If the Rubber Division was dropped at the beginning of last year,the financial advantage (disadvantage)to the company for the year would have been:

A) ($20,000)

B) $20,000

C) $25,000

D) ($25,000)

Because the Rubber Division sustained a loss,the president of Vanik is considering the elimination of this division.All of the division's traceable fixed costs could be avoided if the division was dropped.None of the allocated common corporate fixed costs could be avoided.If the Rubber Division was dropped at the beginning of last year,the financial advantage (disadvantage)to the company for the year would have been:A) ($20,000)

B) $20,000

C) $25,000

D) ($25,000)

Unlock Deck

Unlock for access to all 203 flashcards in this deck.

Unlock Deck

k this deck

73

A study has been conducted to determine if one of the departments in Carry Corporation should be discontinued.The contribution margin in the department is $80,000 per year.Fixed expenses charged to the department are $95,000 per year.It is estimated that $50,000 of these fixed expenses could be eliminated if the department is discontinued.These data indicate that if the department is discontinued,the yearly financial advantage (disadvantage)for the company would be:

A) ($15,000)

B) $15,000

C) ($30,000)

D) $30,000

A) ($15,000)

B) $15,000

C) ($30,000)

D) $30,000

Unlock Deck

Unlock for access to all 203 flashcards in this deck.

Unlock Deck

k this deck

74

CoolAir Corporation manufactures portable window air conditioners.CoolAir has the capacity to manufacture and sell 80,000 air conditioners each year but is currently only manufacturing and selling 60,000.The following per unit numbers relate to annual operations at 60,000 units:

The City of Clearwater would like to purchase 3,000 air conditioners from CoolAir but only if they can get them for $75 each.Variable selling and administrative costs on this special order will drop down to $2 per unit.This special order will not affect the 60,000 regular sales and it will not affect the total fixed costs.The annual financial advantage (disadvantage)for the company as a result of accepting this special order from the City of Clearwater should be:

A) ($21,000)

B) $24,000

C) $144,000

D) ($129,000)