Deck 15: Allocation of Support Activity Costs and Joint Costs

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

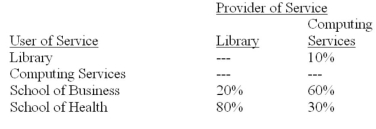

Lakehead College has two service departments, the Library and Computing Services, that assist the School of Business and the School of Health. Budgeted costs of the Library and Computing Services are $800,000 and $1,800,000, respectively. Usage of the service departments' output during the year is anticipated to be:  Required:

Required:

A. Use the direct method to allocate the costs of the Library and Computing Services to the School of Business and the School of Health.

B. Repeat requirement "A" using the step-down method. Lakehead allocates the cost of Computing Services first.

Required:A. Use the direct method to allocate the costs of the Library and Computing Services to the School of Business and the School of Health.

B. Repeat requirement "A" using the step-down method. Lakehead allocates the cost of Computing Services first.

Question

Question

Question

Question

Question

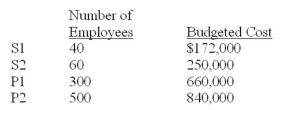

Snakesaw Inc. has two service departments (S1 and S2) and two production departments (P1 and P2). S1 and S2 both use the number of employees as an allocation base. The following data are available:  Required:

Required:

A. Assuming use of the direct method:

1. Over how many employees would S1's budgeted cost be allocated?

2. How much of S2's cost would be allocated to P1?

3. How much of P1's cost would be allocated to S1?

B. Assuming use of the step-down method:

1. How much of S1's cost would be allocated to S2? Navan allocates S1's costs prior to allocating those of S2.

2. How much of S2's total cost would be allocated to P2?

3. How much of S2's total cost would be allocated to S1?

Required:A. Assuming use of the direct method:

1. Over how many employees would S1's budgeted cost be allocated?

2. How much of S2's cost would be allocated to P1?

3. How much of P1's cost would be allocated to S1?

B. Assuming use of the step-down method:

1. How much of S1's cost would be allocated to S2? Navan allocates S1's costs prior to allocating those of S2.

2. How much of S2's total cost would be allocated to P2?

3. How much of S2's total cost would be allocated to S1?

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

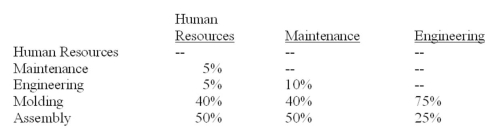

La Mer Company manufactures gauges for automobile dashboards. The company has two production departments, Molding and Assembly. There are three service departments: Human Resources, Maintenance, and Engineering. Usage of services by the various departments follows.  The budgeted costs in La Mer's service departments are: Human Resources, $180,000; Maintenance, $270,000; and Engineering, $200,000. The company rounds all calculations to the nearest dollar.

The budgeted costs in La Mer's service departments are: Human Resources, $180,000; Maintenance, $270,000; and Engineering, $200,000. The company rounds all calculations to the nearest dollar.

Required:

A. Use the direct method to allocate La Mer's service department costs to the production departments.

B. Determine the proper departmental sequence to use in allocating the company's service costs by the step-down method.

C. Ignoring your answer in part "B," assume that Human Resources costs are allocated first, Maintenance costs second, and Engineering costs third. Use the step-down method to allocate La Mer's service department costs.

The budgeted costs in La Mer's service departments are: Human Resources, $180,000; Maintenance, $270,000; and Engineering, $200,000. The company rounds all calculations to the nearest dollar.Required:

A. Use the direct method to allocate La Mer's service department costs to the production departments.

B. Determine the proper departmental sequence to use in allocating the company's service costs by the step-down method.

C. Ignoring your answer in part "B," assume that Human Resources costs are allocated first, Maintenance costs second, and Engineering costs third. Use the step-down method to allocate La Mer's service department costs.

Question

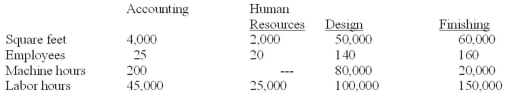

Yole Incorporated has two service departments (Accounting and Human Resources) and two production departments (Design and Finishing). The company uses the direct method of service-department cost allocation, allocating Accounting cost on the basis of square footage and Human Resources cost on the basis of number of employees. Budgeted allocation-base and operating data for the four departments are as follows.

Additional information:

Additional information:

Budgeted costs of Accounting and Human Resources respectively amount to $2,240,000 and $1,500,000.

The anticipated overhead costs incurred directly in the Design and Finishing Departments respectively total $3,840,000 and $3,340,000.

The manufacturing overhead application bases used by Yole's production departments are: Design, labour hours; Finishing, machine hours.

Yole's policy holds that a department's overhead application rate is based on a department's own overhead plus an allocated share of service-department cost.

Required:

A. Allocate the company's service-department costs to the producing departments.

B. Compute the overhead application rates for Design and Finishing.

Additional information:Budgeted costs of Accounting and Human Resources respectively amount to $2,240,000 and $1,500,000.

The anticipated overhead costs incurred directly in the Design and Finishing Departments respectively total $3,840,000 and $3,340,000.

The manufacturing overhead application bases used by Yole's production departments are: Design, labour hours; Finishing, machine hours.

Yole's policy holds that a department's overhead application rate is based on a department's own overhead plus an allocated share of service-department cost.

Required:

A. Allocate the company's service-department costs to the producing departments.

B. Compute the overhead application rates for Design and Finishing.

Question

Question

Ferndale Corp. is developing departmental overhead rates based on direct labour hours for its two production departments, Molding and Assembly. The Molding Department worked 20,000 hours during the period just ended, and the Assembly Department worked 40,000 hours. The overhead costs incurred by Molding and Assembly were $151,250 and $440,750, respectively.

Two service departments, Repair and Power, directly support the two production departments and have costs of $90,000 and $250,000, respectively. The following schedule reflects the use of Repair and Power's output by the various departments:

Required:

Required:

A. Allocate the company's service department costs to production departments by using the direct method.

B. Calculate the overhead application rates of the production departments. Hint: Consider both directly traceable and allocated overhead when deriving your answer.

C. Allocate the company's service department costs to production departments by using the step-down method. Begin with the Power Department, and round calculations to the nearest dollar.

Two service departments, Repair and Power, directly support the two production departments and have costs of $90,000 and $250,000, respectively. The following schedule reflects the use of Repair and Power's output by the various departments:

Required:A. Allocate the company's service department costs to production departments by using the direct method.

B. Calculate the overhead application rates of the production departments. Hint: Consider both directly traceable and allocated overhead when deriving your answer.

C. Allocate the company's service department costs to production departments by using the step-down method. Begin with the Power Department, and round calculations to the nearest dollar.

Question

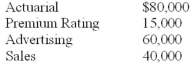

Home Life Insurance Company has two service departments (actuarial and premium rating) and two production departments (advertising and sales). The distribution of each service department's efforts (in percentages) to the other departments is as follows:

The direct operating costs of the departments are:

The direct operating costs of the departments are:  Required:

Required:

A. Use the reciprocal services method to formulate the equations to be used for allocating the total cost to advertising and sales and calculate the reciprocated cost of each service department.

B. Use the reciprocal cost method and calculate the total cost allocated to each operating department.

The direct operating costs of the departments are: Required:A. Use the reciprocal services method to formulate the equations to be used for allocating the total cost to advertising and sales and calculate the reciprocated cost of each service department.

B. Use the reciprocal cost method and calculate the total cost allocated to each operating department.

Question

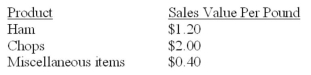

Suppose that one hog yields 200 pounds of ham, 75 pounds of chops, and 25 pounds of miscellaneous items. The sales value of each of the products is as follows:  The hog costs $550. Processing costs are $40.

The hog costs $550. Processing costs are $40.

Required:

A. Determine the proper allocation of joint costs to the three products by using the physical-units method.

B. Repeat part "B" by using the relative-sales-value method.

The hog costs $550. Processing costs are $40.Required:

A. Determine the proper allocation of joint costs to the three products by using the physical-units method.

B. Repeat part "B" by using the relative-sales-value method.

Question

Barry Company manufactures X-111, X-112, and X-113 from a joint process. The following information is available for the period just ended:

Required:

Required:

A. Does Barry allocate joint costs by using the physical-units method? Explain.

B. Assume that Barry does not use the physical-units method but instead allocates joint costs by using the relative-sales-value method. Find the four unknowns in the preceding table.

Required:A. Does Barry allocate joint costs by using the physical-units method? Explain.

B. Assume that Barry does not use the physical-units method but instead allocates joint costs by using the relative-sales-value method. Find the four unknowns in the preceding table.

Question

Question

Question

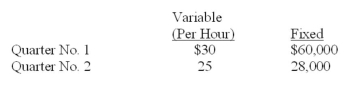

Digitech Corporation, has centralized much of its specialized data processing operation, with the Computer Department performing services for Departments A and B. Service hours consumed during Quarter No. 1 and Quarter No. 2 follow:

Computer Department operating costs were:

Computer Department operating costs were:  Company policy currently requires that total variable and fixed costs be combined and allocated as a lump-sum to users based on service hours.

Company policy currently requires that total variable and fixed costs be combined and allocated as a lump-sum to users based on service hours.

Digitech has been financially healthy for a number of years but began to experience problems toward the end of Quarter No. 1. In response to these problems, management issued a directive to closely monitor costs and computer usage, effective at the start of Quarter No. 2.

Required:

A. Compute Quarter No. 1's total computer cost and determine the allocation to Department A and Department B.

B. How much cost would be allocated to Departments A and B during Quarter No. 2, and how would the heads of these departments likely react to the allocations in light of management's directive?

C. Assume that at the beginning of Quarter No. 2, the company switched to dual-cost allocations, with variable costs allocated based on current usage and fixed costs allocated based on long-run average utilization. An analysis of projected usage found that work for Department A was expected to consume 55% of the Computer Department's time over the coming year. How much cost would be allocated to A and B in Quarter No. 2?

Computer Department operating costs were: Company policy currently requires that total variable and fixed costs be combined and allocated as a lump-sum to users based on service hours.Digitech has been financially healthy for a number of years but began to experience problems toward the end of Quarter No. 1. In response to these problems, management issued a directive to closely monitor costs and computer usage, effective at the start of Quarter No. 2.

Required:

A. Compute Quarter No. 1's total computer cost and determine the allocation to Department A and Department B.

B. How much cost would be allocated to Departments A and B during Quarter No. 2, and how would the heads of these departments likely react to the allocations in light of management's directive?

C. Assume that at the beginning of Quarter No. 2, the company switched to dual-cost allocations, with variable costs allocated based on current usage and fixed costs allocated based on long-run average utilization. An analysis of projected usage found that work for Department A was expected to consume 55% of the Computer Department's time over the coming year. How much cost would be allocated to A and B in Quarter No. 2?

Question

Question

Florek Inc. allocates joint costs by using the net-realizable-value method. In the company's Chicago plant, products 1 and 2 emerge from a joint process that costs $310,000. Product 2 is then processed at a cost of $320,000 into products 3 and 4. Data pertaining to 1, 3, and 4 follow.

Required:

Required:

A. Allocate the $320,000 processing cost between products 3 and 4. Round to the nearest whole dollar.

B. From a profitability perspective, should product 2 be processed into products 3 and 4? Show your calculations.

C. Assume that the net realizable value associated with 2 is zero. How would you allocate the joint cost of $25310,000?

Required:A. Allocate the $320,000 processing cost between products 3 and 4. Round to the nearest whole dollar.

B. From a profitability perspective, should product 2 be processed into products 3 and 4? Show your calculations.

C. Assume that the net realizable value associated with 2 is zero. How would you allocate the joint cost of $25310,000?

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/67

Play

Full screen (f)

Deck 15: Allocation of Support Activity Costs and Joint Costs

1

Morningside Company has two service departments (Maintenance and Human Resources) and three production departments (Machining, Assembly, and Finishing). The two service departments service the production departments as well as each other, and studies have shown that Maintenance provides the greatest amount of service. On the basis of this information, which of the following cost allocations would likely occur under the step-down method?

A)Machining cost would be allocated to Assembly.

B)Maintenance cost would be assigned to the Finishing Department only.

C)Maintenance cost would be assigned to the Human Resources Department only.

D)Human Resources cost would be allocated to Maintenance.

E)Maintenance cost would be allocated to both Finishing and Human Resources.

A)Machining cost would be allocated to Assembly.

B)Maintenance cost would be assigned to the Finishing Department only.

C)Maintenance cost would be assigned to the Human Resources Department only.

D)Human Resources cost would be allocated to Maintenance.

E)Maintenance cost would be allocated to both Finishing and Human Resources.

E

2

The Cassidy Clinic has two service departments (Human Resources and Information Resources) and two "production" departments (In-patient Treatment and Out-patient Treatment). The service departments service the "production" departments as well as each other, and studies have shown that Information Resources provides the greater amount of service. Which of the following allocations would occur if Cassidy uses the direct method of cost allocation?

A)Information Resources cost would be allocated to In-patient Treatment and Out-patient Treatment.

B)Information Resources cost would be allocated to Human Resources.

C)Human Resources cost would be allocated to Information Resources.

D)In-patient Treatment cost would be allocated to Out-patient Treatment.

E)Out-patient Treatment cost would be allocated to Information Resources.

A)Information Resources cost would be allocated to In-patient Treatment and Out-patient Treatment.

B)Information Resources cost would be allocated to Human Resources.

C)Human Resources cost would be allocated to Information Resources.

D)In-patient Treatment cost would be allocated to Out-patient Treatment.

E)Out-patient Treatment cost would be allocated to Information Resources.

A

3

Riverview Inc. has two service departments (Maintenance and Human Resources) and three production departments (Machining, Assembly, and Finishing). Maintenance is the largest service department and Assembly is the largest production department. The two service departments service each other as well as the three producing departments. On the basis of this information, which of the following cost allocations would not occur under the direct method?

A)Maintenance cost would be allocated to Assembly.

B)Maintenance cost would be allocated to Finishing.

C)Maintenance cost would be allocated to Machining.

D)Human Resources cost would be allocated to Finishing.

E)Maintenance cost would be allocated to Human Resources.

A)Maintenance cost would be allocated to Assembly.

B)Maintenance cost would be allocated to Finishing.

C)Maintenance cost would be allocated to Machining.

D)Human Resources cost would be allocated to Finishing.

E)Maintenance cost would be allocated to Human Resources.

E

4

Hunt Corporation has two service departments (S1 and S2) and two production departments (P1 and P2), and uses the step-down method of cost allocation. Management has determined that S1 provides more service to the firm than S2, and has decided that the number of employees is the best allocation base to use for S1. The following data are available: Which of the following statements is (are) true if S1 and S2 have respective operating costs of $280,000 and $350,000?

A)S2 should allocate a portion of its $350,000 cost to S1.

B)S1's cost should be allocated over 140 employees.

C)S1's cost should be allocated over 150 employees.

D)S2 should allocate a total of $390,000 to P1 and P2.

E)S1's cost should be allocated over 140 employees and S2 should allocate a total of $390,000 to P1 and P2.

A)S2 should allocate a portion of its $350,000 cost to S1.

B)S1's cost should be allocated over 140 employees.

C)S1's cost should be allocated over 150 employees.

D)S2 should allocate a total of $390,000 to P1 and P2.

E)S1's cost should be allocated over 140 employees and S2 should allocate a total of $390,000 to P1 and P2.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

5

The Maplewood Clinic has two service departments (Human Resources and Information Systems) and two "production" departments (In-patient Treatment and Out-patient Treatment). The service departments service the "production" departments as well as each other, and studies have shown that Information Systems provides the greatest amount of service. Which of the following allocations would not occur if Maplewood uses the step-down method of cost allocation?

A)Information Systems cost would be allocated to Human Resources.

B)Human Resources cost would be allocated to Out-patient Treatment.

C)Human Resources cost would be allocated to In-patient Treatment.

D)In-patient Treatment cost would be allocated to Out-patient Treatment.

E)Human Resources cost would be allocated to Information Systems.

A)Information Systems cost would be allocated to Human Resources.

B)Human Resources cost would be allocated to Out-patient Treatment.

C)Human Resources cost would be allocated to In-patient Treatment.

D)In-patient Treatment cost would be allocated to Out-patient Treatment.

E)Human Resources cost would be allocated to Information Systems.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

6

Hilton Hamlet Corp. has an Advertising Department and a Human Resources Department that provide service to three store locations. The Human Resources Department cost is allocated on the basis of employees, and the Advertising Department cost is allocated on the basis of space. The following information is available: Using the step-down method and assuming that Human Resources cost is allocated first, the amount of Human Resources cost allocated to Store # 3 is:

A)$0.

B)$8,750.

C)$9,545.

D)$10,000.

E)$14,458.

A)$0.

B)$8,750.

C)$9,545.

D)$10,000.

E)$14,458.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

7

Which of the following would not be considered a service department for an airline?

A)Maintenance.

B)Information Systems.

C)Purchasing.

D)Flight Catering.

E)Plant Maintenance.

A)Maintenance.

B)Information Systems.

C)Purchasing.

D)Flight Catering.

E)Plant Maintenance.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

8

Hilton Hamlet Corp. has an Advertising Department and a Human Resources Department that provide service to three store locations. The Human Resources Department cost is allocated on the basis of employees, and the Advertising Department cost is allocated on the basis of space. The following information is available: Using the direct method, the amount of Advertising Department cost allocated to Store #2 is:

A)$5,789.

B)$5,964.

C)$7,500.

D)$11,579.

E)$15,000.

A)$5,789.

B)$5,964.

C)$7,500.

D)$11,579.

E)$15,000.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

9

The Scarsdale Clinic has two service departments (S1 and S2) and two "production" departments (P1 and P2). The service departments service the "production" departments as well as each other, and studies have shown that S2 provides the greatest amount of service. Which of the following choices correctly denotes an allocation that would occur under the step-down method of cost allocation?

A)S1's cost would be allocated to P1.

B)P1's cost would be allocated to P2.

C)S2's cost would be allocated to S1.

D)P1's cost would be allocated to S1.

E)P2's cost would be allocated to P1.

A)S1's cost would be allocated to P1.

B)P1's cost would be allocated to P2.

C)S2's cost would be allocated to S1.

D)P1's cost would be allocated to S1.

E)P2's cost would be allocated to P1.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

10

When the step-down method is used, the service department whose costs are allocated first is often the department that:

A)obtains the highest yield.

B)has the lowest cost.

C)is the newest.

D)serves the greatest number of other service departments.

E)serves the fewest other service departments.

A)obtains the highest yield.

B)has the lowest cost.

C)is the newest.

D)serves the greatest number of other service departments.

E)serves the fewest other service departments.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

11

Western Incorporated has two service departments (Human Resources and Building Maintenance) and two production departments (Machining and Assembly). The company allocates Building Maintenance cost on the basis of square footage and believes that Building Maintenance provides more service than Human Resources. The square footage occupied by each department follows. Over how many square feet would the Building Maintenance cost be allocated (i.e., spread) with the direct method and the step-down method?

A)1

B)2

C)3

D)4

E)5

A)1

B)2

C)3

D)4

E)5

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

12

The Scarsdale Clinic has two service departments (S1 and S2) and two "production" departments (P1 and P2). The service departments service the "production" departments as well as each other, and studies have shown that S2 provides the greatest amount of service. Which one of the following choices correctly denotes an allocation that would occur under the direct method?

A)S1's cost would be allocated to P1 and P2.

B)P1's cost would be allocated to P2.

C)S2's cost would be allocated to S1.

D)P1's cost would be allocated to S1.

E)P1's cost would be allocated to S2.

A)S1's cost would be allocated to P1 and P2.

B)P1's cost would be allocated to P2.

C)S2's cost would be allocated to S1.

D)P1's cost would be allocated to S1.

E)P1's cost would be allocated to S2.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

13

Pattinson Limited has two service departments (Human Resources and Public Relations) and two production departments (Assembly and Finishing). The number of employees in each department follows. Pattinson uses the direct method of cost allocation and allocates cost on the basis of employees. If Public Relations cost amounts to $2,000,000, how much of the department's cost would be allocated to Assembly?

A)$750,000.

B)$1,081,081.

C)$1,200,000.

D)$1,250,000.

E)$2,000,000.

A)$750,000.

B)$1,081,081.

C)$1,200,000.

D)$1,250,000.

E)$2,000,000.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

14

Hillary Corporation has two service departments (Human Resources and Accounting & Finance) and two production departments (Machining and Assembly). The company allocates Human Resources cost on the basis of square footage and believes that Human Resources provides more service than Accounting & Finance. The square footage occupied by each department follows. Assuming use of the direct method, over how many square feet would the Accounting and Finance cost be allocated?

A)12,000.

B)27,000.

C)66,000.

D)81,000.

E)93,000.

A)12,000.

B)27,000.

C)66,000.

D)81,000.

E)93,000.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

15

Pitt Productions Company has two service departments (Accounting and Admin. and Public Relations) and two production departments (Set Assembly and Productions). The company allocates Public Relations cost on the basis of square footage and Accounting and Admin. cost on the basis of employees, and believes that Public Relations provides more service than Accounting and Admin. The square footage and employees in each department follows. Assuming use of the step-down method, which of the following choices correctly denotes the number of square feet and employees over which the Public Relations and Accounting and Admin. cost would be allocated respectively?

A)47,000, 260.

B)49,000, 260.

C)58,000, 115.

D)58,000, 260.

E)60,000, 115.

A)47,000, 260.

B)49,000, 260.

C)58,000, 115.

D)58,000, 260.

E)60,000, 115.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

16

Which of the following methods recognizes some (but not all) of the services that occur between service departments?

A)Direct method.

B)Step-down method.

C)Indirect method.

D)Reciprocal method.

E)Dual-cost allocation method.

A)Direct method.

B)Step-down method.

C)Indirect method.

D)Reciprocal method.

E)Dual-cost allocation method.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

17

Which of the following would not be considered a service department in a hospital?

A)Security.

B)Cardiac Care.

C)Patient Records.

D)Accounting.

E)Human Resources.

A)Security.

B)Cardiac Care.

C)Patient Records.

D)Accounting.

E)Human Resources.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

18

Treasures Corporation has two service departments (Human Resources and Marketing) and two production departments (Machining and Assembly). The company allocates Marketing cost on the basis of square footage and believes that Marketing provides more service than Human Resources. The square footage occupied by each department follows. Assuming use of the step-down method, over how many square feet would the Marketing cost be allocated?

A)22,000.

B)30,000.

C)52,000.

D)60,000.

E)82,000.

A)22,000.

B)30,000.

C)52,000.

D)60,000.

E)82,000.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

19

Quickdraw Corporation has two service departments (Accounting and Human Resources) and two production departments (Machining and Assembly). The number of employees in each department follows. Quickdraw uses the step-down method of cost allocation and allocates cost on the basis of employees. Human Resources and Accounting cost amounts to $2,400,000 and $1,300,000 respectively. Management believes that the Human Resources department provides more service to the firm than Accounting. How much Human Resources cost would be allocated to Machining?

A)$0.

B)$1,285,714.

C)$1,333,333.

D)$1,384,615.

E)$1,440,000.

A)$0.

B)$1,285,714.

C)$1,333,333.

D)$1,384,615.

E)$1,440,000.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

20

Which of the following methods ignores the fact that some service departments provide service to other service departments?

A)Direct method.

B)Indirect method.

C)Step-down method.

D)Reciprocal method.

E)Dual-cost allocation method.

A)Direct method.

B)Indirect method.

C)Step-down method.

D)Reciprocal method.

E)Dual-cost allocation method.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

21

Which of the following methods accounts for 100% of the services that occur between service departments?

A)Direct method.

B)Indirect method.

C)Reciprocal method.

D)Step-down method.

E)Dual-cost allocation method.

A)Direct method.

B)Indirect method.

C)Reciprocal method.

D)Step-down method.

E)Dual-cost allocation method.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

22

The Glowmeter Manufacturing Company has two production departments (Assembly and Finishing) and two service departments (Human Resources and Maintenance). The projected usage of the two service departments is as follows: The budgeted costs in the service departments are: Human Resources, $60,000 and Maintenance, $30,000. Using the direct method, the amount of Maintenance Department cost allocated to the Finishing Department is:

A)$0.

B)$3,000.

C)$18,000.

D)$20,000.

E)$40,000.

A)$0.

B)$3,000.

C)$18,000.

D)$20,000.

E)$40,000.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

23

Under dual-cost allocation, fixed costs are allocated on the basis of a user department's:

A)long-run usage of a service department's output.

B)short-run usage of a service department's output.

C)long-run usage and short-run usage of a service department's output.

D)neither long-run usage nor short-run usage of a service department's output.

E)either long-run usage or short-run usage of a service department's output.

A)long-run usage of a service department's output.

B)short-run usage of a service department's output.

C)long-run usage and short-run usage of a service department's output.

D)neither long-run usage nor short-run usage of a service department's output.

E)either long-run usage or short-run usage of a service department's output.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

24

The Glowmeter Manufacturing Company has two production departments (Assembly and Finishing) and two service departments (Human Resources and Maintenance). The projected usage of the two service departments is as follows: The budgeted costs in the service departments are: Human Resources, $60,000 and Maintenance, $30,000. Using the step-down method and assuming the Human Resources Department cost is allocated first, the total amount of service department cost allocated to the Finishing Department is:

A)$0.

B)$15,000.

C)$37,000.

D)$42,000.

E)$60,000.

A)$0.

B)$15,000.

C)$37,000.

D)$42,000.

E)$60,000.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

25

Nashville Corporation allocates administrative costs on the basis of staff hours. Short-run monthly usage and anticipated long-run monthly usage of staff hours for Operating Departments 1 and 2 follow. Variable and fixed administrative costs total $180,000 and $400,000, respectively. If Nashville uses dual-cost accounting procedures, the total amount of administrative cost to allocate to Department 2 would be:

A)$301,600.

B)$307,000.

C)$313,600.

D)$319,000.

E)$400,000.

A)$301,600.

B)$307,000.

C)$313,600.

D)$319,000.

E)$400,000.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

26

Which of the following methods would be of little use when allocating service department costs to production departments?

A)The direct method.

B)The reciprocal method.

C)The step-down method.

D)The net-realizable-value method.

E)The dual-cost allocation method.

A)The direct method.

B)The reciprocal method.

C)The step-down method.

D)The net-realizable-value method.

E)The dual-cost allocation method.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

27

When allocating service department costs, companies should use:

A)actual costs rather than budgeted costs, and separate rates for variable and fixed costs.

B)budgeted costs rather than actual costs, and separate rates for variable and fixed costs.

C)budgeted costs rather than actual costs, and a rate that combines variable and fixed costs.

D)actual costs rather than budgeted costs, and a rate that combines variable and fixed costs.

E)a rate that is based on matrix theory.

A)actual costs rather than budgeted costs, and separate rates for variable and fixed costs.

B)budgeted costs rather than actual costs, and separate rates for variable and fixed costs.

C)budgeted costs rather than actual costs, and a rate that combines variable and fixed costs.

D)actual costs rather than budgeted costs, and a rate that combines variable and fixed costs.

E)a rate that is based on matrix theory.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

28

Hilton Hamlet Corp. has an Advertising Department and a Human Resources Department that provide service to three store locations. The Human Resources Department cost is allocated on the basis of employees, and the Advertising Department cost is allocated on the basis of space. The following information is available: Using the step-down method and assuming Human Resources cost is allocated first, the amount of Advertising cost allocated to Store #2 is:

A)$5,789.

B)$5,964.

C)$6,506.

D)$7,500.

E)$11,579.

A)$5,789.

B)$5,964.

C)$6,506.

D)$7,500.

E)$11,579.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

29

Which of the following methods should be selected if a company terminates all processing at the split-off point and desires to use a cost-allocation approach that considers the "revenue-producing ability" of each product?

A)Gross margin at split-off method.

B)Reciprocal-accounting method.

C)Relative-sales-value method.

D)Physical-units method.

E)Net-realizable-value method.

A)Gross margin at split-off method.

B)Reciprocal-accounting method.

C)Relative-sales-value method.

D)Physical-units method.

E)Net-realizable-value method.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

30

The Glowmeter Manufacturing Company has two production departments (Assembly and Finishing) and two service departments (Human Resources and Maintenance). The projected usage of the two service departments is as follows: The budgeted costs in the service departments are: Human Resources, $60,000 and Maintenance, $30,000. Using the step-down method and assuming the Human Resources Department cost is allocated first, the amount of Human Resources cost allocated to the Assembly Department is:

A)$0.

B)$15,000.

C)$42,000.

D)$44,211.

E)$60,000.

A)$0.

B)$15,000.

C)$42,000.

D)$44,211.

E)$60,000.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

31

A company that uses activity-based costing would likely allocate costs from:

A)service departments to production departments.

B)service departments to products and services.

C)service departments to production departments and then to products and services.

D)activity cost pools to production departments.

E)activity cost pools to products or services.

A)service departments to production departments.

B)service departments to products and services.

C)service departments to production departments and then to products and services.

D)activity cost pools to production departments.

E)activity cost pools to products or services.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

32

The point in a joint production process where each individual product becomes separately identifiable is commonly called the:

A)decision point.

B)separation point.

C)individual product point.

D)split-off point.

E)joint product point.

A)decision point.

B)separation point.

C)individual product point.

D)split-off point.

E)joint product point.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

33

Bowmanville Manufacturing Company uses the step-down method for allocating its support department costs to operating departments. The overhead costs of support Department A are to be allocated first, followed by the costs of Department B, and then those of Department C. The distribution of services is as follows:

The percentage of Support Department B's costs allocated to Operating Department Y is:

A)15%.

B)20%.

C)25%.

D)40%.

E) 55%.

The percentage of Support Department B's costs allocated to Operating Department Y is:

A)15%.

B)20%.

C)25%.

D)40%.

E) 55%.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

34

Memorex Clinic has two service departments (Laboratory and Human Resources) and three production departments (In-patient Treatment, Neurology, and After-Care). The two service departments service each other, and studies have shown that Laboratory provides the greatest amount of service. Given the various cost allocation methods, which of the following choices correctly denotes whether Laboratory cost would be allocated to Human Resources?

A)Direct, Step-down, and Reciprocal.

B)Direct.

C)Direct, and Reciprocal.

D)Step-down.

E)Step-down and Reciprocal.

A)Direct, Step-down, and Reciprocal.

B)Direct.

C)Direct, and Reciprocal.

D)Step-down.

E)Step-down and Reciprocal.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

35

The joint-cost allocation method that recognizes the revenues at split-off but does not consider any further processing costs is the:

A)relative-sales-value method.

B)net-realizable-value method.

C)physical-units method.

D)reciprocal-services method.

E)gross margin at split-off method.

A)relative-sales-value method.

B)net-realizable-value method.

C)physical-units method.

D)reciprocal-services method.

E)gross margin at split-off method.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

36

Southside General Hospital has two service departments (Patient Records and Accounting) and two production departments (Internal Medicine and Surgery). Which of the following allocations would likely take place under the reciprocal-services method?

A)Allocation of Accounting cost to Patient Records.

B)Allocation of Patient Records cost to Internal Medicine.

C)Allocation of Surgery cost to Accounting.

D)Allocation of Internal Medicine cost to Surgery.

E)Allocation of Accounting cost to Patient Records and Allocation of Patient Records cost to Accounting.

A)Allocation of Accounting cost to Patient Records.

B)Allocation of Patient Records cost to Internal Medicine.

C)Allocation of Surgery cost to Accounting.

D)Allocation of Internal Medicine cost to Surgery.

E)Allocation of Accounting cost to Patient Records and Allocation of Patient Records cost to Accounting.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

37

The process of allocating fixed and variable costs separately is called:

A)the separate allocation procedure (SAP).

B)diverse allocation.

C)reciprocal cost allocation.

D)common cost allocation.

E)dual cost allocation.

A)the separate allocation procedure (SAP).

B)diverse allocation.

C)reciprocal cost allocation.

D)common cost allocation.

E)dual cost allocation.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

38

Trifecta Inc. allocates administrative costs on the basis of square footage. Short-run monthly usage and anticipated long-run monthly usage of square footage for Operating Departments 1 and 2 follow. If Trifecta uses dual-cost accounting procedures and variable administrative costs total $320,000, the amount of variable administrative cost to allocate to Department 1 would be:

A)$96,000.

B)$128,000.

C)$160,000.

D)$192,000.

E)$320,000.

A)$96,000.

B)$128,000.

C)$160,000.

D)$192,000.

E)$320,000.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

39

Coronation General Hospital has two service departments (Patient Records and Accounting) and two "production" departments (Internal Medicine and Surgery). Which of the following allocations would not take place under the reciprocal-services method of cost allocation?

A)Allocation of Accounting cost to Patient Records.

B)Allocation of Patient Records cost to Internal Medicine.

C)Allocation of Surgery cost to Accounting.

D)Allocation of Internal Medicine cost to Surgery.

E)Allocation of Surgery cost to Accounting and allocation of Internal Medicine cost to Surgery.

A)Allocation of Accounting cost to Patient Records.

B)Allocation of Patient Records cost to Internal Medicine.

C)Allocation of Surgery cost to Accounting.

D)Allocation of Internal Medicine cost to Surgery.

E)Allocation of Surgery cost to Accounting and allocation of Internal Medicine cost to Surgery.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

40

Ronan Corporation allocates administrative costs on the basis of staff hours. Short-run monthly usage and anticipated long-run monthly usage of staff hours for Operating Departments 1 and 2 follow. If Ronan uses dual-cost accounting procedures and fixed administrative costs total $1,000,000, the amount of fixed administrative cost to allocate to Department 1 would be:

A)$400,000.

B)$450,000.

C)$500,000.

D)$850,000.

E)$1,000,000.

A)$400,000.

B)$450,000.

C)$500,000.

D)$850,000.

E)$1,000,000.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

41

Lakehead College has two service departments, the Library and Computing Services, that assist the School of Business and the School of Health. Budgeted costs of the Library and Computing Services are $800,000 and $1,800,000, respectively. Usage of the service departments' output during the year is anticipated to be: Required:

A. Use the direct method to allocate the costs of the Library and Computing Services to the School of Business and the School of Health.

B. Repeat requirement "A" using the step-down method. Lakehead allocates the cost of Computing Services first.

Required:A. Use the direct method to allocate the costs of the Library and Computing Services to the School of Business and the School of Health.

B. Repeat requirement "A" using the step-down method. Lakehead allocates the cost of Computing Services first.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

42

Rocky Mountain Company produces two products (X and Y) from a joint process. Each product may be sold at the split-off point or processed further. Additional processing requires no special facilities, and production costs of further processing are entirely variable and traceable to the products involved. Joint manufacturing costs for the year were $60,000. Sales values and costs were as follows:

If the joint production costs are allocated based on the physical-units method, the amount of joint cost assigned to product X would be:

A)$20,000.

B)$24,000.

C)$30,000.

D)$36,000.

E)$40,000.

If the joint production costs are allocated based on the physical-units method, the amount of joint cost assigned to product X would be:

A)$20,000.

B)$24,000.

C)$30,000.

D)$36,000.

E)$40,000.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

43

Mission Mars Incorporated uses the physical-units method to allocate costs among its three joint products: X, Y, and Z. The following data are available for the period just ended: Joint processing cost: $800,000

Total production: 150,000 pounds

Share of joint cost allocated to X: $160,000

Share of joint cost allocated to Y: $400,000

Which of the following statements is true?

A)The Company would have relied on the sales value of each product when allocating joint costs to X, Y, and Z.

B)The Company produced 30,000 pounds of Z during the period.

C)The Company produced 45,000 pounds of Z during the period.

D)The Company produced 105,000 pounds of Z during the period.

E)The Company produced 150,000 pounds of Z during the period.

Total production: 150,000 pounds

Share of joint cost allocated to X: $160,000

Share of joint cost allocated to Y: $400,000

Which of the following statements is true?

A)The Company would have relied on the sales value of each product when allocating joint costs to X, Y, and Z.

B)The Company produced 30,000 pounds of Z during the period.

C)The Company produced 45,000 pounds of Z during the period.

D)The Company produced 105,000 pounds of Z during the period.

E)The Company produced 150,000 pounds of Z during the period.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

44

Rocky Mountain Company produces two products (X and Y) from a joint process. Each product may be sold at the split-off point or processed further. Additional processing requires no special facilities, and production costs of further processing are entirely variable and traceable to the products involved. Joint manufacturing costs for the year were $60,000. Sales values and costs were as follows:

If the joint production costs are allocated based on the relative-sales-value method, the amount of joint cost assigned to product X would be:

A)$18,000.

B)$27,000.

C)$33,000.

D)$40,000.

E)$20,000.

If the joint production costs are allocated based on the relative-sales-value method, the amount of joint cost assigned to product X would be:

A)$18,000.

B)$27,000.

C)$33,000.

D)$40,000.

E)$20,000.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

45

Which of the following choices correctly denotes the data needed to allocate joint costs under the relative-sales-value method?

A)1

B)2

C)3

D)4

E)5

A)1

B)2

C)3

D)4

E)5

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

46

Snakesaw Inc. has two service departments (S1 and S2) and two production departments (P1 and P2). S1 and S2 both use the number of employees as an allocation base. The following data are available: Required:

A. Assuming use of the direct method:

1. Over how many employees would S1's budgeted cost be allocated?

2. How much of S2's cost would be allocated to P1?

3. How much of P1's cost would be allocated to S1?

B. Assuming use of the step-down method:

1. How much of S1's cost would be allocated to S2? Navan allocates S1's costs prior to allocating those of S2.

2. How much of S2's total cost would be allocated to P2?

3. How much of S2's total cost would be allocated to S1?

Required:A. Assuming use of the direct method:

1. Over how many employees would S1's budgeted cost be allocated?

2. How much of S2's cost would be allocated to P1?

3. How much of P1's cost would be allocated to S1?

B. Assuming use of the step-down method:

1. How much of S1's cost would be allocated to S2? Navan allocates S1's costs prior to allocating those of S2.

2. How much of S2's total cost would be allocated to P2?

3. How much of S2's total cost would be allocated to S1?

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

47

Watrus Manufacturing Co. makes three products, 1, 2, and 3, all of which are joint products, and products 4, which is classified as a by-product. If joint manufacturing costs amount to $600,000 and the company is using a popular accounting method, the firm will:

A)allocate $600,000 among 1, 2, and 3.

B)allocate $600,000 among 1, 2, 3, and 4.

C)increase $600,000 by the net realizable value of 4 and then allocate the total among 1, 2, and 3.

D)decrease $600,000 by the net realizable value of 4 and then allocate the total among 1, 2, and 3.

E)decrease $600,000 by the net realizable value of 4 and then allocate the total among 1, 2, 3, and 4.

A)allocate $600,000 among 1, 2, and 3.

B)allocate $600,000 among 1, 2, 3, and 4.

C)increase $600,000 by the net realizable value of 4 and then allocate the total among 1, 2, and 3.

D)decrease $600,000 by the net realizable value of 4 and then allocate the total among 1, 2, and 3.

E)decrease $600,000 by the net realizable value of 4 and then allocate the total among 1, 2, 3, and 4.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

48

When allocating joint costs, Grimsby Company calculates the final sales value of the various products manufactured and subtracts appropriate separable costs. The company is using the:

A)gross margin at split-off method.

B)reciprocal-accounting method.

C)relative-sales-value method.

D)physical-units method.

E)net-realizable-value method.

A)gross margin at split-off method.

B)reciprocal-accounting method.

C)relative-sales-value method.

D)physical-units method.

E)net-realizable-value method.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

49

Garvin Corporation manufactures joint products P1 and P2. During a recent period, joint costs amounted to $30,000 in the production of 10,000 gallons of P1 and 20,000 gallons of P2. Garvin can sell P1 and P2 at split-off for $2.00 per gallon and $2.50 per gallon, respectively. Alternatively, both products can be processed beyond the split-off point, as follows: The joint cost allocated to P2 under the relative-sales-value method would be:

A)$8,571.43.

B)$13,333.33.

C)$16,666.67.

D)$21,428.57.

E)$30,000.00

A)$8,571.43.

B)$13,333.33.

C)$16,666.67.

D)$21,428.57.

E)$30,000.00

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

50

Rocky Mountain Company produces two products (X and Y) from a joint process. Each product may be sold at the split-off point or processed further. Additional processing requires no special facilities, and production costs of further processing are entirely variable and traceable to the products involved. Joint manufacturing costs for the year were $60,000. Sales values and costs were as follows:

If the joint production costs are allocated based on the net-realizable-value method, the amount of joint cost assigned to product Y would be:

A)$20,000.

B)$27,000.

C)$33,000.

D)$40,000.

E)$60,000.

If the joint production costs are allocated based on the net-realizable-value method, the amount of joint cost assigned to product Y would be:

A)$20,000.

B)$27,000.

C)$33,000.

D)$40,000.

E)$60,000.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

51

Victoria Manufacturing Co. manufactures two products (A and B) from a joint process that cost $200,000 for the year just ended. Each product may be sold at the split-off point or processed further. Additional processing requires no special facilities, and production costs of further processing are entirely variable and traceable to the products involved. Further information follows.

If the joint costs are allocated based on the physical-units method, the amount of joint cost assigned to product A would be:

A)$80,000.

B)$100,000.

C)$104,000.

D)$120,000.

E)$200,000.

If the joint costs are allocated based on the physical-units method, the amount of joint cost assigned to product A would be:

A)$80,000.

B)$100,000.

C)$104,000.

D)$120,000.

E)$200,000.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

52

Consider the following four independent cases that relate to service department cost allocations:

Case A: Strickland Company has two service departments [Human Resources (H/R) and Information Systems] and two production departments (Machining and Assembly). Human Resource cost is allocated by using the direct method based on the number of personnel in each department. For the period just ended, there were 189 employees in Machining, and Machining received $90,000 of H/R's overhead of $200,000. How many employees are in the Assembly Department?

Case B: Walter Burke, controller of Alexander Enterprises, wants service department managers to be aware that their use of other service departments costs the firm a substantial amount of money. Would Burke prefer the direct method or the step-down method of cost allocation? Why?

Case C: Lockwood Company has four service departments (S1, S2, S3, and S4) and two production departments (P1 and P2). The costs of S1 are allocated first, followed in order by the costs of S2, S3, and S4. Lockwood uses the step-down method, and the costs of S2 are allocated based on the number of computer hours used. Computer hours logged during the period were as follows: S1, 4,600; S2, 7,100; S3, 10,400; S4, 17,600; P1, 37,000; and P2, 48,600. Over how many hours would S2's cost be allocated?

Case D: A recently hired staff accountant noted that given the nature of the allocations, the total cost allocated to production departments is typically less under the step-down method than under the direct method. Do you agree with the accountant? Why?

Required:

Answer the questions that are raised in Cases A, B, C, and

Case A: Strickland Company has two service departments [Human Resources (H/R) and Information Systems] and two production departments (Machining and Assembly). Human Resource cost is allocated by using the direct method based on the number of personnel in each department. For the period just ended, there were 189 employees in Machining, and Machining received $90,000 of H/R's overhead of $200,000. How many employees are in the Assembly Department?

Case B: Walter Burke, controller of Alexander Enterprises, wants service department managers to be aware that their use of other service departments costs the firm a substantial amount of money. Would Burke prefer the direct method or the step-down method of cost allocation? Why?

Case C: Lockwood Company has four service departments (S1, S2, S3, and S4) and two production departments (P1 and P2). The costs of S1 are allocated first, followed in order by the costs of S2, S3, and S4. Lockwood uses the step-down method, and the costs of S2 are allocated based on the number of computer hours used. Computer hours logged during the period were as follows: S1, 4,600; S2, 7,100; S3, 10,400; S4, 17,600; P1, 37,000; and P2, 48,600. Over how many hours would S2's cost be allocated?

Case D: A recently hired staff accountant noted that given the nature of the allocations, the total cost allocated to production departments is typically less under the step-down method than under the direct method. Do you agree with the accountant? Why?

Required:

Answer the questions that are raised in Cases A, B, C, and

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

53

Which of the following statements about joint-cost allocation is false?

A)Joint cost allocation is useful in deciding whether to further process a product after split-off.

B)Joint cost allocation is useful in making a profit determination about individual joint products.

C)Joint cost allocation is helpful in inventory valuation.

D)Joint cost allocation can be based on the number of units produced.

E)Joint cost allocation can be accomplished by using several different methods that focus on sales value and product "worth."

A)Joint cost allocation is useful in deciding whether to further process a product after split-off.

B)Joint cost allocation is useful in making a profit determination about individual joint products.

C)Joint cost allocation is helpful in inventory valuation.

D)Joint cost allocation can be based on the number of units produced.

E)Joint cost allocation can be accomplished by using several different methods that focus on sales value and product "worth."

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

54

Burlington Corporation manufactures joint products W and X. During a recent period, joint costs amounted to $300,000 in the production of 20,000 gallons of W and 60,000 gallons of X. Both products will be processed beyond the split-off point, giving rise to the following data: The joint cost allocated to W under the net-realizable-value method would be:

A)$75,000.

B)$80,000.

C)$84,000.

D)$90,000.

E)$300,000.

A)$75,000.

B)$80,000.

C)$84,000.

D)$90,000.

E)$300,000.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

55

Companies are free to use the direct, step-down, and reciprocal allocation methods when dealing with service-department costs.

Required:

A. How does the direct method work? What is its chief limitation?

B. Is the step-down method an improvement over the direct method? Explain.

C. Which of the three methods is the most correct from a conceptual viewpoint? Why?

Required:

A. How does the direct method work? What is its chief limitation?

B. Is the step-down method an improvement over the direct method? Explain.

C. Which of the three methods is the most correct from a conceptual viewpoint? Why?

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

56

La Mer Company manufactures gauges for automobile dashboards. The company has two production departments, Molding and Assembly. There are three service departments: Human Resources, Maintenance, and Engineering. Usage of services by the various departments follows. The budgeted costs in La Mer's service departments are: Human Resources, $180,000; Maintenance, $270,000; and Engineering, $200,000. The company rounds all calculations to the nearest dollar.

Required:

A. Use the direct method to allocate La Mer's service department costs to the production departments.

B. Determine the proper departmental sequence to use in allocating the company's service costs by the step-down method.

C. Ignoring your answer in part "B," assume that Human Resources costs are allocated first, Maintenance costs second, and Engineering costs third. Use the step-down method to allocate La Mer's service department costs.

The budgeted costs in La Mer's service departments are: Human Resources, $180,000; Maintenance, $270,000; and Engineering, $200,000. The company rounds all calculations to the nearest dollar.Required:

A. Use the direct method to allocate La Mer's service department costs to the production departments.

B. Determine the proper departmental sequence to use in allocating the company's service costs by the step-down method.

C. Ignoring your answer in part "B," assume that Human Resources costs are allocated first, Maintenance costs second, and Engineering costs third. Use the step-down method to allocate La Mer's service department costs.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

57

Yole Incorporated has two service departments (Accounting and Human Resources) and two production departments (Design and Finishing). The company uses the direct method of service-department cost allocation, allocating Accounting cost on the basis of square footage and Human Resources cost on the basis of number of employees. Budgeted allocation-base and operating data for the four departments are as follows.

Additional information:

Budgeted costs of Accounting and Human Resources respectively amount to $2,240,000 and $1,500,000.

The anticipated overhead costs incurred directly in the Design and Finishing Departments respectively total $3,840,000 and $3,340,000.

The manufacturing overhead application bases used by Yole's production departments are: Design, labour hours; Finishing, machine hours.

Yole's policy holds that a department's overhead application rate is based on a department's own overhead plus an allocated share of service-department cost.

Required:

A. Allocate the company's service-department costs to the producing departments.

B. Compute the overhead application rates for Design and Finishing.

Additional information:Budgeted costs of Accounting and Human Resources respectively amount to $2,240,000 and $1,500,000.

The anticipated overhead costs incurred directly in the Design and Finishing Departments respectively total $3,840,000 and $3,340,000.

The manufacturing overhead application bases used by Yole's production departments are: Design, labour hours; Finishing, machine hours.

Yole's policy holds that a department's overhead application rate is based on a department's own overhead plus an allocated share of service-department cost.

Required:

A. Allocate the company's service-department costs to the producing departments.

B. Compute the overhead application rates for Design and Finishing.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

58

Many companies use the dual-cost method of cost allocation.

Required:

A. How does the dual-cost method work?

B. Is there any advantage of the dual-cost method over a method that uses a combined, lump-sum single rate? Briefly explain.

Required:

A. How does the dual-cost method work?

B. Is there any advantage of the dual-cost method over a method that uses a combined, lump-sum single rate? Briefly explain.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

59

Ferndale Corp. is developing departmental overhead rates based on direct labour hours for its two production departments, Molding and Assembly. The Molding Department worked 20,000 hours during the period just ended, and the Assembly Department worked 40,000 hours. The overhead costs incurred by Molding and Assembly were $151,250 and $440,750, respectively.

Two service departments, Repair and Power, directly support the two production departments and have costs of $90,000 and $250,000, respectively. The following schedule reflects the use of Repair and Power's output by the various departments:

Required:

A. Allocate the company's service department costs to production departments by using the direct method.

B. Calculate the overhead application rates of the production departments. Hint: Consider both directly traceable and allocated overhead when deriving your answer.

C. Allocate the company's service department costs to production departments by using the step-down method. Begin with the Power Department, and round calculations to the nearest dollar.

Two service departments, Repair and Power, directly support the two production departments and have costs of $90,000 and $250,000, respectively. The following schedule reflects the use of Repair and Power's output by the various departments:

Required:A. Allocate the company's service department costs to production departments by using the direct method.

B. Calculate the overhead application rates of the production departments. Hint: Consider both directly traceable and allocated overhead when deriving your answer.

C. Allocate the company's service department costs to production departments by using the step-down method. Begin with the Power Department, and round calculations to the nearest dollar.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

60

Home Life Insurance Company has two service departments (actuarial and premium rating) and two production departments (advertising and sales). The distribution of each service department's efforts (in percentages) to the other departments is as follows:

The direct operating costs of the departments are: Required:

A. Use the reciprocal services method to formulate the equations to be used for allocating the total cost to advertising and sales and calculate the reciprocated cost of each service department.

B. Use the reciprocal cost method and calculate the total cost allocated to each operating department.

The direct operating costs of the departments are: Required:A. Use the reciprocal services method to formulate the equations to be used for allocating the total cost to advertising and sales and calculate the reciprocated cost of each service department.

B. Use the reciprocal cost method and calculate the total cost allocated to each operating department.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

61

Suppose that one hog yields 200 pounds of ham, 75 pounds of chops, and 25 pounds of miscellaneous items. The sales value of each of the products is as follows: The hog costs $550. Processing costs are $40.

Required:

A. Determine the proper allocation of joint costs to the three products by using the physical-units method.

B. Repeat part "B" by using the relative-sales-value method.

The hog costs $550. Processing costs are $40.Required:

A. Determine the proper allocation of joint costs to the three products by using the physical-units method.

B. Repeat part "B" by using the relative-sales-value method.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

62

Barry Company manufactures X-111, X-112, and X-113 from a joint process. The following information is available for the period just ended:

Required:

A. Does Barry allocate joint costs by using the physical-units method? Explain.

B. Assume that Barry does not use the physical-units method but instead allocates joint costs by using the relative-sales-value method. Find the four unknowns in the preceding table.

Required:A. Does Barry allocate joint costs by using the physical-units method? Explain.

B. Assume that Barry does not use the physical-units method but instead allocates joint costs by using the relative-sales-value method. Find the four unknowns in the preceding table.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

63

Higgins Corporation manufactures two chemicals (Flextra and Hydro) in a joint process. Data from a recent month follow.

Direct materials used: $360,000

Direct labour: $150,000

Manufacturing overhead: $690,000

Manufacturing output:

Flextra: 40,000 gallons

Hydro: 120,000 gallons

Flextra sells for $15 per gallon and Hydro sells for $20 per gallon.

Required:

A. Compute the total joint costs to be allocated to Flextra and Hydro.

B. Compute the joint costs that would be allocated to Flextra by using the physical-units method.

C. Compute the joint costs that would be allocated to Hydro by using the relative-sales-value method.

D. Assume that Hydro can be converted into a more refined product, Hydro-R, in a totally separable process at an additional cost of $4 per gallon. If the refined product can be sold in the marketplace for $26 per gallon, compute the net realizable value of Hydro-R

Direct materials used: $360,000

Direct labour: $150,000

Manufacturing overhead: $690,000

Manufacturing output:

Flextra: 40,000 gallons

Hydro: 120,000 gallons

Flextra sells for $15 per gallon and Hydro sells for $20 per gallon.

Required:

A. Compute the total joint costs to be allocated to Flextra and Hydro.

B. Compute the joint costs that would be allocated to Flextra by using the physical-units method.

C. Compute the joint costs that would be allocated to Hydro by using the relative-sales-value method.

D. Assume that Hydro can be converted into a more refined product, Hydro-R, in a totally separable process at an additional cost of $4 per gallon. If the refined product can be sold in the marketplace for $26 per gallon, compute the net realizable value of Hydro-R

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

64

Newfoundland Chemical Company manufactures two industrial chemicals in a joint process. In October, $120,000 of direct materials were processed at a cost of $300,000, resulting in 16,000 pounds of Pentex and 4,000 pounds of Glaxco. Pentex sells for $35 per pound and Glaxco sells for $60 per pound. Management generally processes each of these chemicals further in separable processes to manufacture more refined products. Pentex is processed separately at a cost of $7.50 per pound, with the resulting product, Pentex-R, selling for $45 per pound. Glaxco is processed separately at a cost of $10 per pound, and the resulting product, Glaxco-R, sells for $100 per pound.

Required:

A. Compute the company's total joint production costs.

B. Assuming that total joint production costs amounted to $500,000, allocate these costs by using:

1. The physical-units method.2. The relative-sales-value method.3. The net-realizable-value method.

Required:

A. Compute the company's total joint production costs.

B. Assuming that total joint production costs amounted to $500,000, allocate these costs by using:

1. The physical-units method.2. The relative-sales-value method.3. The net-realizable-value method.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

65

Digitech Corporation, has centralized much of its specialized data processing operation, with the Computer Department performing services for Departments A and B. Service hours consumed during Quarter No. 1 and Quarter No. 2 follow:

Computer Department operating costs were: Company policy currently requires that total variable and fixed costs be combined and allocated as a lump-sum to users based on service hours.

Digitech has been financially healthy for a number of years but began to experience problems toward the end of Quarter No. 1. In response to these problems, management issued a directive to closely monitor costs and computer usage, effective at the start of Quarter No. 2.

Required:

A. Compute Quarter No. 1's total computer cost and determine the allocation to Department A and Department B.

B. How much cost would be allocated to Departments A and B during Quarter No. 2, and how would the heads of these departments likely react to the allocations in light of management's directive?

C. Assume that at the beginning of Quarter No. 2, the company switched to dual-cost allocations, with variable costs allocated based on current usage and fixed costs allocated based on long-run average utilization. An analysis of projected usage found that work for Department A was expected to consume 55% of the Computer Department's time over the coming year. How much cost would be allocated to A and B in Quarter No. 2?

Computer Department operating costs were: Company policy currently requires that total variable and fixed costs be combined and allocated as a lump-sum to users based on service hours.Digitech has been financially healthy for a number of years but began to experience problems toward the end of Quarter No. 1. In response to these problems, management issued a directive to closely monitor costs and computer usage, effective at the start of Quarter No. 2.

Required:

A. Compute Quarter No. 1's total computer cost and determine the allocation to Department A and Department B.

B. How much cost would be allocated to Departments A and B during Quarter No. 2, and how would the heads of these departments likely react to the allocations in light of management's directive?

C. Assume that at the beginning of Quarter No. 2, the company switched to dual-cost allocations, with variable costs allocated based on current usage and fixed costs allocated based on long-run average utilization. An analysis of projected usage found that work for Department A was expected to consume 55% of the Computer Department's time over the coming year. How much cost would be allocated to A and B in Quarter No. 2?

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

66