Deck 4: Activity Based Costing and Analysis

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

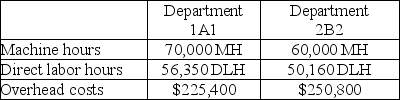

A company produces surgical equipment that goes through threes processes, 1A1, 2B2, and 3C3, before they are complete. Expected costs and activities for the three departments are shown below. All departments have departmental overhead rates based on direct labor hours. Therefore, the overhead rate for each department is $5 per direct labor hour.

Question

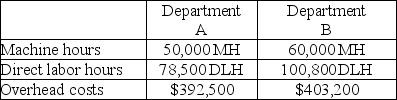

A company produces paint that goes through two operations, operation A and operation B, before it is complete. Expected costs and activities for the two departments are shown below. Given this information, the departmental overhead rate for Department B based on machine hours is $4 per machine hour.

Question

Turtle Company produces t-shirts that go through two operations, cutting and sewing, before they are complete. Expected costs and activities for the two departments are shown below. Given this information, the departmental overhead rate for the cutting department based on direct labor hours is $2.69 per direct labor hour (rounded to two decimals).

Question

Question

Question

Question

Question

A company produces garden benches that go through two operations, operation 1A1 and operation 2B2, before they are complete. Expected costs and activities for the two departments are shown below. Both departments have departmental overhead rates based on machine hours. Therefore, the overhead rates for department 1A1 and department 2B2 are the same.

Question

Question

A company produces heating elements that go through two operations, casting and assembling, before they are complete. Expected costs and activities for the two departments are shown below. Given this information, the departmental overhead rate for the assembling department based on direct labor hours is $5 per direct labor hour.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/220

Play

Full screen (f)

Deck 4: Activity Based Costing and Analysis

1

Products are the first stage cost objects when using a departmental overhead rate method.

False

2

Product costs consist of direct labor, direct materials, and overhead (indirect) costs.

True

3

Over recent decades, overhead costs have steadily decreased while direct labor costs have increased as a percentage of total manufacturing costs.

False

4

The cost to heat a manufacturing facility can be directly linked to the number of units produced.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

5

Activities are the cost objects of the second stage of ABC.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

6

Allocating overhead involves the following four steps: 1) Assign overhead costs to departmental cost pools. 2) Select an allocation base for each department. 3) Compute overhead allocation rates for each department and 4) Use departmental overhead rates to assign overhead costs to products.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

7

The plantwide overhead rate is total plantwide allocation base divided by total budgeted plantwide overhead cost.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

8

Data concerning volume-related measures are readily available in most manufacturing settings.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

9

The premise of ABC is that it takes activities to make products and provide services and these activities drive costs.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

10

Over recent decades, overhead costs have steadily increased while direct labor costs have decreased as a percentage of total manufacturing costs.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

11

Distorted product cost information can result in poor decisions.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

12

The departmental overhead rate method allows each department to have its own overhead rate and its own allocation base.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

13

Overhead costs are not directly related to production and cannot be traced to units of product like direct materials and direct labor can.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

14

Examples of volume-related measures include direct labor hours and machine hours.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

15

The departmental overhead rate method uses the same overhead rate for each production department.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

16

Departments are the cost objects when the plantwide overhead rate method is used.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

17

The departmental overhead rate method uses a different overhead rate for each production department.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

18

The plantwide overhead rate is determined using volume-related measures.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

19

The unit of product is the cost object when the plantwide overhead rate method is used.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

20

By definition, costs classified as overhead are consumed in basically the same manner regardless of the process involved.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

21

ABC is significantly less costly to implement and maintain than more traditional overhead costing systems.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

22

ABC allocates overhead costs to products based on input measures rather than output measures.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

23

A cost pool is a collection of costs that are related to the same or similar activity.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

24

Activity-based costing first assigns costs to products and then uses these product costs to assign costs to manufacturing activities.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

25

A single cost pool is used when allocating overhead using the activity-based costing method.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

26

Overhead costs are often affected by many issues and are frequently too complex to be explained by any one factor.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

27

Multiple cost pools are used when allocating overhead using the plantwide overhead rate method.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

28

The use of a plantwide overhead rate is not acceptable for external reporting under GAAP.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

29

Compared to the departmental overhead rate method, the plantwide overhead rate method usually results in more accurate overhead allocations.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

30

Compared to the plantwide overhead rate method, the departmental overhead rate method usually results in more accurate overhead allocations.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

31

Some companies allocate their overhead cost using a plantwide overhead rate largely because of its simplicity.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

32

Because departmental overhead costs are allocated based on measures closely related to production volume, they accurately assign overhead, such as utility costs.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

33

ABC can be used to assign costs to any cost object that is of management interest.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

34

Management's pricing and cost decisions for a product are influenced by that product's cost assignments.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

35

The usefulness of overhead allocations based on a plantwide overhead rate depends on two crucial assumptions: (1) the overhead cost is correlated with the allocation base; and (2) all products use overhead cost in dissimilar proportions.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

36

Allocated overhead costs vary depending upon the allocation methods used.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

37

The usefulness of overhead allocations based on a plantwide overhead rate depends on two crucial assumptions: (1) the overhead cost is correlated with the allocation base; and (2) all products use overhead cost in similar proportions.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

38

Activities are the cost objects of the first stage of ABC.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

39

When products differ in batch size and complexity, they usually consume different amounts of overhead resources.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

40

A major disadvantage of using a plantwide overhead rate is the extreme difficulty in gathering the needed information.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

41

Malone's plantwide overhead rate will be $20.99 per direct labor hour next year.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

42

If the direct labor time estimates are met, Malone will allocate $12.59 of overhead cost to each unit of Little X.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

43

ABC is more costly to implement and maintain than more traditional overhead costing systems.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

44

The more activities tracked by activity-based costing, the more accurately overhead costs are assigned.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

45

A company estimates that costs for the next year will be $500,000 for indirect labor, $50,000 for factory utilities, and $1,000,000 for the CEO's salary. The company uses machine hours as its overhead allocation base. If 25,000 machine hours are planned for this next year, then a product requiring 10 machine hours will be assigned $220 in overhead.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

46

A company produces surgical equipment that goes through threes processes, 1A1, 2B2, and 3C3, before they are complete. Expected costs and activities for the three departments are shown below. All departments have departmental overhead rates based on direct labor hours. Therefore, the overhead rate for each department is $5 per direct labor hour.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

47

A company produces paint that goes through two operations, operation A and operation B, before it is complete. Expected costs and activities for the two departments are shown below. Given this information, the departmental overhead rate for Department B based on machine hours is $4 per machine hour.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

48

Turtle Company produces t-shirts that go through two operations, cutting and sewing, before they are complete. Expected costs and activities for the two departments are shown below. Given this information, the departmental overhead rate for the cutting department based on direct labor hours is $2.69 per direct labor hour (rounded to two decimals).

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

49

In activity-based costing, an activity can involve several related tasks.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

50

Kinetic Company estimates that overhead costs for the next year will be $1,600,000 for indirect labor and $400,000 for factory utilities. The company uses direct labor hours as its overhead allocation base. If 50,000 direct labor hours are planned for this next year, then the plantwide overhead rate is $.025 per direct labor hour.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

51

Malone has 33,000 total estimated direct labor hours for next year.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

52

When using the plantwide overhead rate method, total budgeted overhead costs are combined into one overhead cost pool.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

53

A company produces garden benches that go through two operations, operation 1A1 and operation 2B2, before they are complete. Expected costs and activities for the two departments are shown below. Both departments have departmental overhead rates based on machine hours. Therefore, the overhead rates for department 1A1 and department 2B2 are the same.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

54

Kinetic Company estimates that overhead costs for the next year will be $1,600,000 for indirect labor and $400,000 for factory utilities. The company uses direct labor hours as its overhead allocation base, and plans to use 50,000 direct labor hours for this next year. If a product uses 5 direct labor hours, then it will be assigned $200 in overhead costs.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

55

A company produces heating elements that go through two operations, casting and assembling, before they are complete. Expected costs and activities for the two departments are shown below. Given this information, the departmental overhead rate for the assembling department based on direct labor hours is $5 per direct labor hour.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

56

The first step in using the departmental overhead rate method requires that overhead be traced to each of the company's departments.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

57

A company estimates that costs for the next year will be $500,000 for indirect labor, $50,000 for factory utilities, and $1,000,000 for the CEO's salary. The company uses machine hours as its overhead allocation base. If 25,000 machine hours are planned for this next year, then the plantwide overhead rate is $22 per machine hour.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

58

A company estimates total overhead costs for the next year to be $1,200,000 and wishes to use direct labor hours as its overhead allocation base. This company makes two products: (1) Fancy X, which requires three direct labor hours per unit, and (2) Plain X, which requires one direct labor hour per unit. If the company plans to make 10,000 units of Fancy X and 10,000 units of Plain X, then each unit produced will be allocated the same amount of overhead.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

59

Activity-based costing involves four steps: (1) identify activities and the costs they cause, (2) group similar activities into cost pools, (3) determine an activity rate for each activity cost pool, and (4) allocate overhead costs to products using those activity rates.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

60

The departmental overhead rate method traces costs to each department and then determines an allocation base for each department.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

61

Batch-level costs vary with the number of units produced.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

62

Which types of overhead allocation methods result in the use of more than one overhead rate during the same time period?

A) Plantwide overhead rate method and departmental overhead rate method.

B) Cost pool overhead rate method and plantwide overhead rate method.

C) Departmental overhead rate method and activity-based costing.

D) Activity-based costing and plantwide overhead rate method.

E) Departmental overhead rate method and cost pool overhead rate method.

A) Plantwide overhead rate method and departmental overhead rate method.

B) Cost pool overhead rate method and plantwide overhead rate method.

C) Departmental overhead rate method and activity-based costing.

D) Activity-based costing and plantwide overhead rate method.

E) Departmental overhead rate method and cost pool overhead rate method.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

63

Activity-based costing often shifts overhead costs from large volume, standardized products to low-volume, specialty products that consume disproportionate resources.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

64

Unit-level costs vary with the number of units produced.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

65

Plantwide overhead rates typically do a better job of matching each department's overhead costs to the products using the department's resources than do departmental overhead rates.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

66

Activities causing overhead cost in an organization are typically separated into four levels: (1) direct activities, (2) indirect activities, (3) batch level activities, and (4) facility level activities.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

67

Overhead costs:

A) Are directly related to production.

B) Can be traced to units of product in the same way that direct materials can.

C) Cannot be traced to units of product in the same way that direct labor can.

D) Are period costs.

E) Include only fixed costs.

A) Are directly related to production.

B) Can be traced to units of product in the same way that direct materials can.

C) Cannot be traced to units of product in the same way that direct labor can.

D) Are period costs.

E) Include only fixed costs.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

68

The cost object of the plantwide overhead rate method is:

A) The unit of product.

B) The production departments of the company.

C) The production activities of the company.

D) Manufacturing cost pools.

E) The time period.

A) The unit of product.

B) The production departments of the company.

C) The production activities of the company.

D) Manufacturing cost pools.

E) The time period.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

69

A quality-inspection cost is an example of unit-level costs.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

70

Activity-based costing eliminates the need for overhead allocation rates.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

71

Product-level costs do not vary with the number of units or batches produced.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

72

Which of the following would not be considered a product cost?

A) Direct labor costs.

B) Factory supervisor's salary.

C) Factory line worker's salary.

D) Cost accountant's salary.

E) Manufacturing overhead costs.

A) Direct labor costs.

B) Factory supervisor's salary.

C) Factory line worker's salary.

D) Cost accountant's salary.

E) Manufacturing overhead costs.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

73

Two big benefits of ABC costing are a) more accurate product cost information and b) more detailed information on costs and the drivers of those costs.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

74

Machine setup costs are an example of a batch level activity.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

75

Facility-level costs are not traceable to individual product lines, batches or units.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

76

Batch-level costs do not vary with the number of units produced.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

77

A method of assigning overhead costs to a product using a single overhead rate is:

A) Plantwide overhead rate method.

B) Cost pool overhead rate method.

C) Departmental overhead rate method.

D) Activity-based costing.

E) Overhead cost allocation method.

A) Plantwide overhead rate method.

B) Cost pool overhead rate method.

C) Departmental overhead rate method.

D) Activity-based costing.

E) Overhead cost allocation method.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

78

Facility-level costs vary with the number of units or batches produced.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

79

Product design costs are an example of a unit level activity.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

80

The final step of activity-based costing assigns overhead costs to pools rather than to products.

Unlock Deck

Unlock for access to all 220 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 220 flashcards in this deck.